Navigating the emerging markets Malaysia Obstacles to success, offset, international relationships, procurement strategies, and defence industrial intelligence Guy Anderson Chief analyst, Jane’s Defence Industry 19 May 2011

Malaysia – Market summary Higher defence spending and greater procurement clarity can be expected, but significant challenges remain

Higher spending ahead: Malaysia is forecast*1 to commit US$28 billion to defence funding between 2010 and 2015 – core spending will rise 48% over the five years

Spending Clarity: Publication of the 10th Malaysia Plan expected this year – commitment to dedicate 10% of government revenues to defence and security spending.

Economic growth: Greater spending to be underpinned by relatively high economic growth of 5.8% pa (average 2010 to 2015)*2

*1 Jane’s Defence Budgets – Jdb.janes.com *2 IHS Global Insight

Challenges…

Delayed procurement: A series of major programmes (from self-propelled howitzers to multi-purpose support ships) were delayed during the 9th plan. Commitment to focus capital expenditure on delayed programmes during the first two years of the 10th plan – but will this leave adequate funds for latter years of the 10th plan? Offset – greater demands: Malaysia’s offset regime to be overhauled during 2011 – more arduous demands can be expected

Limited local capabilities: Meeting technology transfer and local participation demands will be challenging given limited capabilities of local industries

Politicised procurement and corruption: Major programme decisions often circumvent usual procurement routes. Allegations of improper conduct are not unknown

Malaysia – In figures

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

2.20%

3

3.5

4

4.5

5

5.5

FY08 FY09 FY10 FY11f FY12f FY13f FY14f FY15f

Defence spending (USD bn) Defence spending as % GDP

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

100

150

200

250

300

350

400

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Nominal GDP (USD bn) Real GDP (% change)

Defence spending (US$ bn v expenditure as % GDP)

Nominal GDP (US$ bn) v real gdp (% change year on year)

IHS Global Insight Jane’s Defence Budgets – jdb.janes.com

Malaysia – Defence spending (trends)

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

2.20%

3

3.5

4

4.5

5

5.5

FY08 FY09 FY10 FY11f FY12f FY13f FY14f FY15f

Defence spending (USD bn)

Defence spending as % GDP

Defence spending (US$ bn v expenditure as % GDP)

Jane’s Defence Budgets – jdb.janes.com

Declared and actual spending: Actual defence spending has historically outstripped disclosed defence spending – the difference is falling, however (from 25% in 2005 to 5.7% in 2008)*1.

2010: 2010 expenditure is likely to have been below the year’s allocation as a result of programme delays / retrenchment resulting from economic challenges

Spending as % of GDP: Defence spending as a percentage of GDP is low by global standards (1.57% in 2010 and forecast to average 1.6% 2011 to 2015*2 – consistent with regional peers, however)

Spending plans: 9th Malaysia Plan (2006 – 2010) dedicated MYR15.3 billion to defence development although MYR18.5 billion was actually allocated.

Post 2011 - 10th Malaysia Plan (2011 – 2016) to include defence / security development allocation of MYR23 billion – indications that defence spending will be between MYR15-18 billion with remaining funds allocated to security domains *1 Malay Ministry of Finance Economic Reports

*2 Jane’s Defence Budgets

Malaysia – In figures (materiel suppliers - nations)

*Based on SIPRI Trade Equivalent Units Source SIPRI

Suppliers of defence materiel (2000 to 2008 - by percentage total value of military imports* )

Australia 0.03%

Brazil 1.49%

Canada 0.32%

France 8.79%

Germany 18.82%

Indonesia 0.47%

Italy 6.18%

Pakistan 0.50%

Poland 5.13%

Russia 40.27%

South Africa 0.62%

Spain 7.00%

Sweden 0.35%

Switzerland 0.56%

Turkey 2.34%

UK 4.43%

US 2.70%

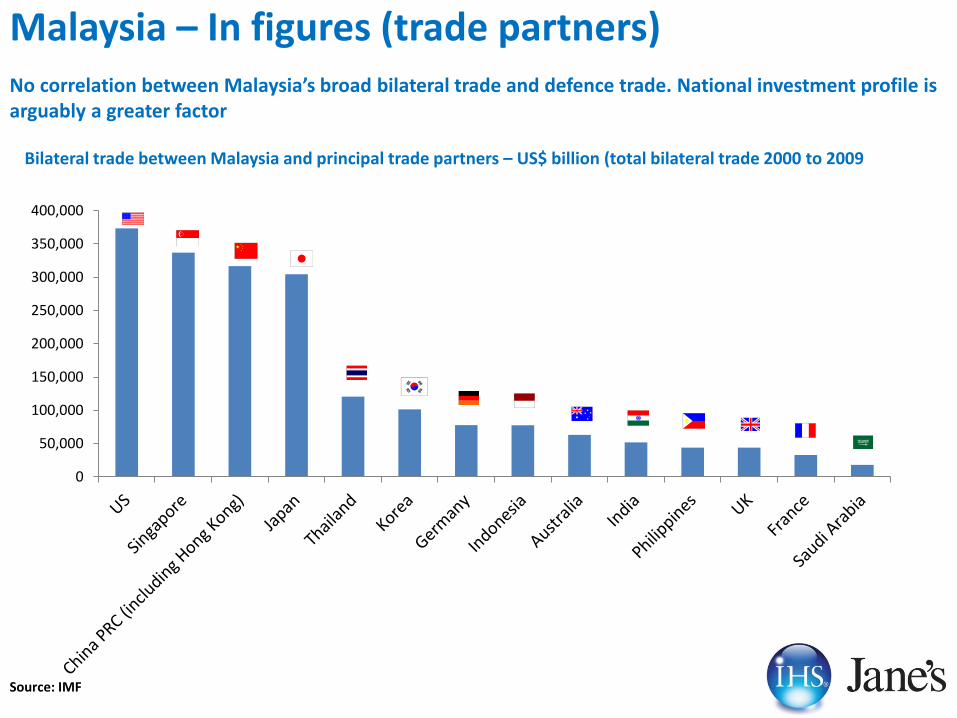

Malaysia – In figures (trade partners) No correlation between Malaysia’s broad bilateral trade and defence trade. National investment profile is arguably a greater factor

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Bilateral trade between Malaysia and principal trade partners – US$ billion (total bilateral trade 2000 to 2009

Source: IMF

Malaysia – In figures (procurement spending)

Procurement spending by service (US$ m) FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Army 173 136 129 129 145 152 174 182 Navy 534 436 413 412 462 486 594 624 Air 617 501 492 491 569 598 706 741 Other / joint 33 32 38 38 39 41 48 51 TOTAL 1,357 1,105 1,072 1,070 1,215 1,277 1,522 1,598

0

0.5

1

1.5

2

Army Navy Air Other / joint

Procurement spending by services (US$ bn - actual and forecast)

Source Jane's Defence Budgets

Army 12%

Navy 39%

Air 46%

Joint / other

3%

Procurement spending by services (% of forecast total – 2010 to 2015)

Malaysia – Market opportunities by sector – 2011 to 2016

C3, 1.88

Ground Vehicles,

2.24

Aircraft, 5.70

Ships, 1.84

Unmanned Systems,

0.04

EOIR, 0.34

Radar, 0.57

Sonar, 0.06 Precision Weapons,

0.39

Forecast spending by platform / system type - US$ bn *

• Assessment / forecasts based on known programmes and identified opportunities (eg, stated realisable procurement aims during coming spending period) Source: Jane’s DS Forecast

Market Sector % total allocated funds - 2011 to 2016*

C3 14.40%

Ground Vehicles 17.15%

Aircraft 43.64%

Ships 14.09%

Space Systems 0.02%

Unmanned Systems 0.31%

EOIR 2.60%

Radar 4.36%

Sonar 0.46%

Precision Weapons 2.99%

Malaysia – Procurement procedures

1. MINDEF Procurement Division draws up programme specification with technical advice from STRIDE and legal support of Attorney General

2. Anticipated size of procurement determines level of oversight – sub US$2.2 million awards handled within MINDEF / US$2.2 million + awards require MoF approval

3. Tender route chosen:

A) Open tenders to pre-qualified candidates B) Open tenders to Bumiputra-status companies C) Limited tenders (for small scale procurement – sub US$1.6m) D) Direct tenders (v small scale procurement – sub US$14k)

4. Tender documents published at www.eperolehan.com.my and through local / international media (eg, Jane’s Defence Weekly)

5. Tender Opening Committee (without sight of bidders’ details) tasked with opening and recording tenders

6. Decision taken by MINDEF (or MINDEF and MoF). Larger procurements require approval of Malaysian cabinet. Cabinet intervenes in cases of disagreement between MINDEF and MoF

7. Letter of Intent (LoI) presented to chosen bidder. Letter of Acceptance subject to further negotiations

8. Offset agreements (for procurements of US$13 million +) must be agreed / signed before procurement contract conclusion

9. Contract award

Broad military procurement process of Malaysia

External oversight: Malaysian Parliament / Federal Auditor / Independent Commission on Anti Corruption

Malaysia – Procurement practices

Politicised major procurement: Major programme procurement decision appear to circumvent MINDEF entirely – raises questions of drivers behind decisions / transparency issues.

Inadequate over-sight: Parliament has the right of oversight, but has not proved an effective watchdog given dearth of information available to representatives.

Favouring of Bumiputra-status companies: Right to issue tenders directly to ethnic Malay owned companies – typically applies to low-tech / low-value requirements given limited indigenous capabilities

Balancing international procurement: Malaysia’s procurement relationships have been extremely broad – whether this points to appropriate (albeit short-sighted) acquisition, or efforts to balance relations is open to question.

Graft: Allegations of improper practices are not unknown, but corruption is largely limited to low level contact and smaller contracts (where oversight is minimal)

Role of “middle-men”: Emphasis on maximising involvement through offset and awarding contracts directly to domestic organisations in partnership with foreign contractors made emergence of middle-men and “local facilitators” inevitable.

Defence acquisitions are subject to fair and open procurement with extensive checks and balances; independent oversight and parliamentary scrutiny…. in theory

Malaysia – Procurement - novel mechanisms?

Malaysia considered alternative procurement models in the wake of the 2007 global financial crisis

Private finance initiatives: Malaysia has previously used PFI to underpin procurement (eg, the 2008 Air Combat Manoeuvring Instrumentation Systems accord). Signs as of 2010 / 2011 that the PFI model is gaining favour once again – PFI funding vehicles to be used to support development of Malaysia Defence & Security Technology Park

Islamic Finance: Use of “Sukuk” *Islamic law-compliant bonds] has been raised by the Malaysian Defence minister. He suggested in 2009 that the Navy should use Islamic finance to fund upgrade programmes. There is a risk that funding mechanisms not compatible / set up in compliance with Islamic law may prove problematic

Joint Procurement – Southeast Asia: Malaysia was a driving force (2009 and 2010 ) behind calls for the Association of Southeast Asian Nations (ASEAN) to pursue greater common procurement and defence industrial collaboration. The body was to be loosely based on the European Defence Agency. Progress has been sluggish to date.

Malaysia – Defence industrial development Timeline

1970s: Defence industrialisation follows independence (1957) with some results by 1970s. Ambitions modest: emphasis on MRO and munitions. Eg, Airod (est 1976) and SME.

1980s: Clear that defence industrial competencies lagging Singapore / South Korea. Sluggish development during the decade

1990s: More rapid progress and privatisation efforts (eg, Boustead Naval Shipyard (1995)and Malaysia Marine and Heavy Engineering (1991). Main defence companies of today established in 1990s.Post-1997 crisis hits development

2000s: Efforts to reinvigorate industry. Defence Industrial Blueprint ( first of its kind) published 2005.

2010s: New Economic Model launched in 2009.. Defence industrial strategy aligned with wider goals . Aim to create “higher-value” economic output

Malaysia – Defence industrial development Social and economic drivers

NEM – to 2020: Defence industrial reform yoked to New Economic Model (itself a development of the national Vision 2020 strategy)

Offset and NEM: Offset reforms – ranging from transfer of technology to export facilitation – consistent with NEM. Offset policy delayed in 2010 to ensure compliance with NEM

Export – balance of trade: Malaysia keen to use defence development to improve trade balance; hence pending emphasis on materiel counter-trade and export facilitation (eg, Colt M4 license production includes regional marketing rights). Outlook for success is limited

Employment

Quality before quantity: Defence industrialisation of previous decades sought to ease poverty / unemployment among ethnic Malays – current emphasis will be on quality of jobs given low unemployment (3% 2010 and falling*1) but low average incomes ($3k pa) *2.

Brain-drain reversal: 305,000 people left the country between March 2008 and August 2009 and 1 million Malaysians currently live/work abroad. *3 Malaysia keen to stem this flow through the creation of meaningful opportunities *1 / 2* IHS Global Insight

*3 Malaysian Parliamentary Report – reported by Asian Sentinel (Malaysia’s Brain Drain – 18 February 2011)

2.50%

2.70%

2.90%

3.10%

3.30%

3.50%

3.70%

3.90%

Malaysia: Unemployment rate (%)

IHS Global Insight

Colt M4 carbine. Source Colt

Malaysia’s reliance on imported materiel is high - risk of strategic weak spot is clear:

Indigenous contributions to procurement programmes stood at 25% in 2009 *1

90% of the inventory of the Malaysian Armed Forces is based on offshore designs (2008) *2

External threats – regional challenges driving procurement:

Malaysia – Defence industrial development Strategic drivers

*1 Jane’s Defence Industry News, “Malaysia seeks tech transfer and joint ventures”, 10 July 2009 *2 “Defence industrialisation in Malaysia: Development challenges and the revolution in military affairs”, Kogila Balakrishnan, Summer 2008

Spratly archipelago: Disputed by Malaysia, Vietnam, China (PRC and Taiwan), Brunei, Philippines)

Disputed maritime demarcation zone around Sabah: Disputed by Indonesia, Malaysia, Philippines

People’s Republic of China: Regional power projection by Beijing helping to drive Malaysian defence spending

Malacca Strait: Need to ensure safe passage driving maritime / surveillance procurement and development efforts

Imag

e so

urc

e: G

oo

gle

Singapore: Desire to maintain parity with increasingly capable armed forces

Piracy / wider Immigration concerns

Malaysia – Defence industrial capabilities

Indigenous defence industrial capabilities are limited and focused on low-technology domains – national ambitions to date have been modest, but a change in direction is underway

Small-scale industrial base - Defence industrial base extends to around 50 organisations and an estimated 20,000 employees

Development has lagged regional peers (eg, Singapore, South Korea and even Indonesia)

Indigenous capabilities reflected modest early ambitions to maintain local inventories Therefore abilities concentrated in aerospace maintenance, repair and overhaul; the manufacture of small arms and munitions; ship repair and fabrication; metal working; and basic land systems – reflects earlier ambitions to merely maintain local inventories

Significant capability gaps exist (notably in C4ISR domains, plus more general research, design and development capabilities)

Offset dependence is notable – few indigenous capabilities are self-sustaining

Offset opportunities wasted during 1990s – low value-added counter-trade accords provided economic “quick fix” following Asian Financial Crisis

Efforts to reinvigorate domestic industries began in 2000s – first ever defence industrial strategy (Defence Industrial Blue-Print) not published until 2005. Efforts currently underway to coral defence industrial development into wider economic development plans

RDT&E expenditure as percentage of total defence spending – Malaysia ver. regional peers / emerging producers

Malaysia – Limited R&D investment / skills

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

FY08 FY09 FY10

*1 2008. Malaysian govt figs *2 UNESCO 2009

Negligible R&DTE investment has hampered development of national capabilities – reflects emphasis on foreign procurement / local involvement rather than focus on indigenous solutions

Malaysia’s defence industrial workforce is relatively low-skilled – just seven research scientists for every 10,000 sector employees*1

Relatively skills of population a barrier to development – almost 10% are illiterate while almost two thirds do not complete education beyond secondary level*2

Jane’s Defence Budgets – jdb.janes.com

Malaysia – Offset and counter-trade

Malaysia has imposed offset obligations for two decades, but has operated a formal policy for just six years. Results so far have been lacklustre

Strong indications of offset reliance – indigenous firms almost always act in a junior role under foreign contractors

Exports: No record of an indigenously produced Malaysian system having achieved an international sale. Offset has failed to facilitate global market involvement.

Job creation has been woeful: just 100 new jobs linked to offset between 2000 and 2004*

Offset has failed – on the whole - to create self-sustaining capabilities: As of 2010…

38% of offset recipients continue to rely on foreign technology, components and process machine (beyond obligation period)

50% continue to rely on consultancy services of foreign partners*

* “Evaluating the role of offsets in creating a sustainable defence industrial base: the case of Malaysia”, Kogila Balakrishnan, midas.mod.gov.my

Malaysia – Offset and counter-trade Numerous opportunities to benefit from offset obligations have been wasted – largely as a result of a failure to take a coherent, long-term view of industrial participation. For example…

FNSS

Programme: ACV-300 (2002)

Details: 136 ACVs purchased from Turkey’s FNSS, of which 65 were built by DefTech in Malaysia in CKD form

Result: Plant / transferred equipment being abandoned at end of offset period. Dearth of subsequent opportunities blamed

Programme: Short Integrated Ramp Motorised Pontoon Bridge (2002)

Details: Acquired from France’s CNIM. Malaysia’s CTRM provided carbon composite launch rails.

Result: Offset package valued at US$3 million (including US$1.5 million training). CTRM abandoned composite rail manufacture after just three years.

Jane’s

Malaysia – Offset and counter-trade (reform)

Raised offset thresholds: From EUR10 million to EUR20 million – an apparently counter-intuitive strategy which reflected a focus on meaningful returns from larger programmes

Export facilitation: Malaysian military exports have been negligible (US$300m - 2009). Counter-purchases of Malaysian produced materiel will be encouraged. Aim will be to reduce use of lower-value-added counter-purchases of commodities

Technology transfer / joint ventures: Greater emphasis on JVs and ToT, with government looking at means of encouraging both (existing policy permits but does not obligate ToT / JVs). Buy-back clauses to allow offset joint ventures to return to sole-Malaysian ownership under consideration

Malaysia Defence & Security Technology Park: Effort to create defence industry, science and technology hub in Sungkai (defence minister’s constituency). At design phase as of 2011. Offset will be used to fund and populate the park (eg, attraction of anchor tenants). Malaysia expects to benefit from offset obligations of third countries (where there is potential to export back to Malaysia)

Offset policy is under review. Updated guidance is expected to be published late 2011 / early 2012. Publication was delayed by 12 months from Q1 2010

Pending reforms:

Malaysia – Final thoughts…. Market Success?

Defence trade with Malaysia can be eased by willingness / ability to ….. Establish a footprint on the ground Enter partnerships with local entities

Acquiesce to technology transfer programmes (within capabilities of venture partners)

Provide training to underpin procurement – both industrial staff and military personnel

Enter into majority Malaysian-owned joint ventures - and ultimately exit to permit local sole ownership

Facilitate major counter-trade arrangements – both in defence domains and beyond

Be flexible – Malaysian offset demands have at times verged on the surreal (including the launch of a Malaysian cosmonaut attached to Sukhoi procurement)

Success - the French example: France accounted for 8.9% of Malaysia’s military imports between 2000 and 2008. It is forecast by Jane’s to account for 6.9% from 2011 to 2016.

The US$1 billion Scorpene procurement (2002) can be viewed as a model example: The Offset package included: Majority-local owned JV (60 per cent in favour of Boustead Heavy Industries) Transfer of technology to facilitate maintenance work Potential for learned capabilities to be exported elsewhere in the region – maintenance, repair, logistics Potential for great maintenance and upgrade gains given life of the programmes

Paris agreed to: The counter purchase of palm oil valued at EUR230 million Unusual offset demands including the increased frequency of Malaysian Airline System flights to Paris

Malaysia – Final thoughts…. Market Success?

Malaysia – Final thoughts….

Defence expenditure outlook is positive, but headwinds remain (eg, efforts to cut overall deficit may affect discretionary spending while military budgets are pegged to overall government income)

Malaysia is unlikely to increase self-sufficiency / export profile to significant degree in near term – limited indigenous capabilities and dearth of RDT&E expenditure mean international reliance will continue

Opportunities to use offset to develop indigenous capabilities have been largely wasted for twenty years – remains to be seen whether coherent view anticipated in 2011 reforms translates into longer term success

Increased technology transfer and military materiel export facilitation demands through offset will place a greater burden on foreign contractors – absorption of technologies / training at a local level will remain challenging

Efforts to increase military technologies co-operation and common procurement through the ASEAN cluster are unlikely to yield results – disparities between spending and industrial capabilities of regional actors remain too great

Navigating the Emerging Markets Malaysia

Thank you for your attention

Questions?

Guy Anderson

Chief analyst, Jane’s Defence Industry - London

0044 (0) 208 7003843

With thanks to:

Jonathan Grevatt

Jane’s Asia Pacific Industrial Analyst - Bangkok

Jane’s DS Forecast / Jane’s Defence Budgets

(London and Washington DC)