1

CLOVER INDUSTRIES LIMITED

Merrill Lynch conference

Sun City – 15 March 2013

2

AGENDA

• Introduction & background

• Business drivers

• Challenges

• Potential

• What keeps us awake

3

INTRODUCTION

AND BACKGROUND

4

CLOVER IS…

• A JSE listed Branded Consumer Goods (BCG) Company with a

114 year heritage

• One of the largest distribution companies in SA

• The largest chilled distributor in South Africa

• Substantial critical mass due to its milk delivery frequency

• Strong Beverages brand portfolio

5

The of Italy

The of New Zealand

The of France

The of Spain

The of Argentina

CLOVER IS…

6

Vision

To be a leading branded foods and beverages group in South Africa and

selected African countries, providing accessible nutrition to all consumers

Mission

Clover's mission is to reach the Group’s widely dispersed customers on a daily

basis, and to provide trusting consumers with quality products through its

extensive network underpinned by its leading dairy business. Care is taken to

develop or acquire brands which have the potential to occupy the number one or

two positions in their chosen segments. It focusses on way better operations

across the supply chain including services to the trade, and on delivering

sustainable shareholder value by being a responsible corporate citizen and

preferred employer

7

OUR BRANDS

8

KEY RECENT EVENTS

Change in mind-set

at Clover

Evolution of the

business platform

from a co-operative

dynamic to a

corporate dynamic

Achieved with the

full support of milk

producers

Clover positioned to raise capital

to implement growth and efficient plans

2003

2006

2007

2010

2011

• National Co-operative Dairies Limited converted to Clover Industries Limited

• Fundamental shift from a “supply driven” company to a “demand driven” company

• Clover SA acquires Danone’s 39.5% shareholding in Clover Beverages

• Sale of UltraMel custard brand to Danone

• Sale of 45% shareholding in Danone Clover for R1.08bn to Danone

• Dual share structure abolished

• Delinking of ordinary shares from milk delivery agreements together with the

amendment to the rights attached to the preference shares

• Buy-back of Hosken Consolidated Investments ordinary shares

• Listing on the JSE

• Buy out of minority shareholders in Clover Beverages Limited

• Transfer of the Clover Beverages business into Clover SA

9

THE SOUTHERN AFRICAN DAIRY MARKET

• South African national dairy production is ±2,7bn litres

• The market is predominantly a liquid (drinking) milk market

• Fresh milk constitutes the majority of the liquid milk market

• The annual market is approximately R36bn for dairy based products

• Clover buys approximately 24% of national milk production

(including milk for Danone)

• Import potential limited to cheese, butter, powders and long life milk

• Unlike Europe and the USA liquid milk is still very much a branded domain

with DOB market shares in the top end (Spar, Shoprite, Pick n Pay) being:

› Fresh milk 31%

› UHT 45%

› Butter 28%

› Cheese 12%

10

THE SOUTHERN AFRICAN

NON-ALCOHOLIC BEVERAGE MARKET

• South African national market for non-alcoholic beverages is ±R56bn

• Markets not currently serviced and investigated by Clover are:

› Carbonated beverages

› Long life fruit drinks

11

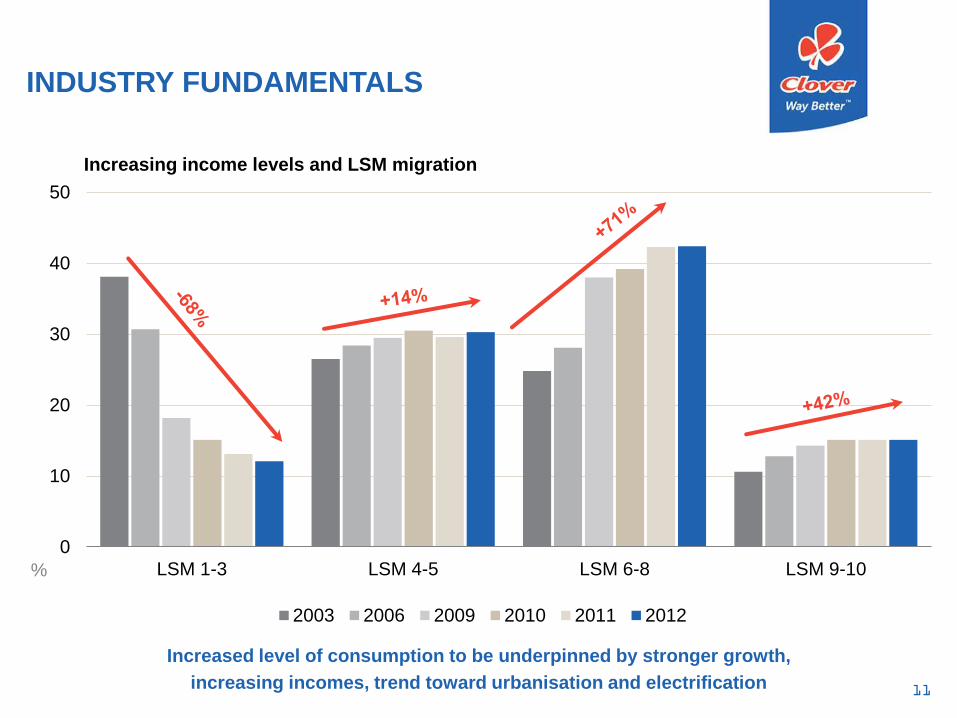

0

10

20

30

40

50

LSM 1-3 LSM 4-5 LSM 6-8 LSM 9-10%

Increasing income levels and LSM migration

2003 2006 2009 2010 2011 2012

INDUSTRY FUNDAMENTALS

Increased level of consumption to be underpinned by stronger growth,

increasing incomes, trend toward urbanisation and electrification

12

MILK CONSUMPTION PER CAPITA

13

100% JUICE AND NECTAR

ANNUAL CONSUMPTION PER CAPITA

33.331.3

27.826.6

22.8

8.7 8.0

2.41.1

0

5

10

15

20

25

30

35

Germany Finland USA France UK SouthAfrica

Mexico Brazil NigeriaLitresper capita

Developed market median of 28 litres per capita

14

KEY BUSINESS DRIVERS

15

KEY BUSINESS DRIVERS

• Strong brands with leading market position

• Extensive distribution platform

• Increasing efficiencies and capacity (Project Cielo Blu)

16

STRONG BRANDS WITH LEADING MARKET POSITION

17

STRONG BRANDS

123

123

123

123

124

126

126

127

132

134

Cadbury

Handy Andy

Nokia

Standard…

Woolworths

KFC

Shoprite

Clover

Coca-Cola

Pick 'n Pay

SA top 10 most engaging brands

1.92

1.95

2.03

2.08

2.43

2.44

3.00

3.00

4.00

16.00

BMW

Levi

Nokia

SAB

KFC

Clover

Nike

KOO

Vodacom

Coca-Cola

SA’s most favourite brand

This is a totally spontaneous mention question –

people can vote for any brand they love

18

34

34

35

35

36

37

37

37

39

40

41

43

45

46

46

47

47

47

47

48

50

50

50

55

57

57

60

65

0 10 20 30 40 50 60 70

Aromat

Simba

All Gold

Eskort

Koo fruit

Pick n Pay

Jik

Black & Crosswell

Ackermans

Vodacom

KFC

Clover

Nokia

Sunlight

MTN

Dulux

Jet

Black Cat

JC Le Roux

Albany

Coca-Cola

Robertsons

Sunlight

Koo

Mr Price

Huletts

All Gold

Edgars

Average

STRONG BRANDS

15 236 interviews over 10 months across 8 000 brands in 450 product categories

19

Clover awards: F2012/13

Awards Brand Comments

Apex Awards Tropika Bronze Sustainable brand in marketing and business

Arrow Awards

Tropika

Clover Krush

Clover Milk

Clover Cheese

Diamond

Diamond

1st (Gold)

1st (Gold)

Best marketing campaign

Most successful product launch

Sunday Times

Top Brands

Tropika

Krush

Top 3

Winner

Sunday Times

Youth SurveyTropika Top 10

6th

4th

Cold drinks

Dairy drinks category

Products

of the Year

Danao

Clover UHT Prisma

Clover 800g Cheese

Winner

Innovation

Icon Brands

2012

Clover Fresh Milk

Clover Cheese

Icon status

3rd Dairy category

STRONG BRANDS

20

TANGIBLE BRAND PREMIUMS

10%13%

23%

-7%

23%

29%

3%

32%

8%

-12%-10%

20%

13%11%

40%

Clover 2ltFresh

Clover 1LUHT milk

Fresh Milk1L

CloverFeta

cheese400gr

CloverPre-packNaturalCheese240gr

Elite Pre-pack

NaturalCheese300gr

CloverPre-packNaturalCheese450gr

Tropikadairy fruit

mix 2lt

Krush purefresh juice

1.5lt

Manhattanice tea500ml

Aquartz500ml Still

water

Super Mflavoured

milk 300ml

FreshCream250ml

Butter -Mooi River

500gr

Danao 1Ldairy fruit

mix

21

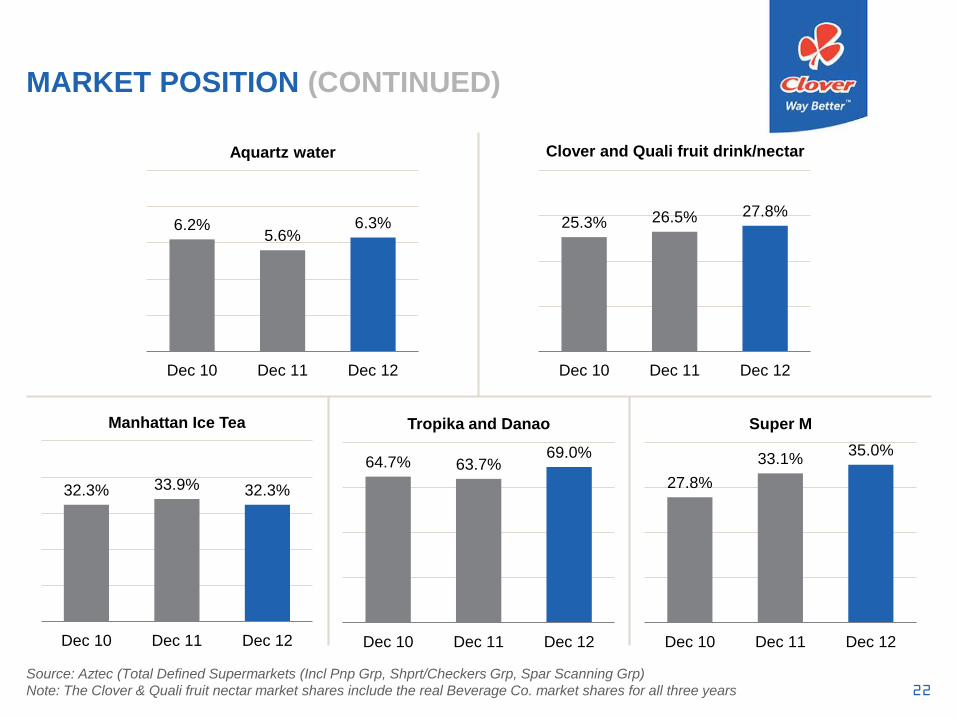

MARKET POSITION

Source: Aztec (Total Defined Supermarkets (Incl Pnp Grp, Shprt/Checkers Grp, Spar Scanning Grp)

Note: The Krush & Quali fresh juices market shares include the real Beverage Co. market shares for all three years

28.4% 29.0%31.0%

Dec 10 Dec 11 Dec 12

Fresh and UP milk

24.7% 25.6%

19.6%

Dec 10 Dec 11 Dec 12

UHT milk

40.0% 38.8%41.7%

Dec 10 Dec 11 Dec 12

Cream

47.0% 46.6% 46.6%

Dec 10 Dec 11 Dec 12

Krush and Quali fresh juices

38.5%

30.2%

36.9%

Dec 10 Dec 11 Dec 12

Feta cheese

47.2% 45.4%40.2%

Dec 10 Dec 11 Dec 12

Pre-packed cheese

22

6.2%5.6%

6.3%

Dec 10 Dec 11 Dec 12

Aquartz water

25.3% 26.5% 27.8%

Dec 10 Dec 11 Dec 12

32.3% 33.9% 32.3%

Dec 10 Dec 11 Dec 12

Manhattan Ice Tea

64.7% 63.7%69.0%

Dec 10 Dec 11 Dec 12

Tropika and Danao

27.8%

33.1%35.0%

Dec 10 Dec 11 Dec 12

Super M

MARKET POSITION (CONTINUED)

Source: Aztec (Total Defined Supermarkets (Incl Pnp Grp, Shprt/Checkers Grp, Spar Scanning Grp)

Note: The Clover & Quali fruit nectar market shares include the real Beverage Co. market shares for all three years

Clover and Quali fruit drink/nectar

23

EXTENSIVE DISTRIBUTION PLATFORM

24

EXTENSIVE DISTRIBUTION NETWORK

Distribution network

is a key enabling

platform, is a

sustainable

competitive

advantage and is

central to the growth

prospects of Clover

Deep penetration

with c. 14,000

delivery points with

high frequency of

delivery due to milk

25

INCREASING EFFICIENCIES AND CAPACITY

(PROJECT CIELO BLU)

26

INCREASING EFFICIENCIES:

PROJECT CIELO BLU

Project Cielo Blu creates

efficiencies in production and

capacities in the distribution

network to support current and

future growth

Project Cielo Blu seeks to:

• Address historical

inefficiencies in the supply

chain

• Create capacity to sustain

growth of the business

• Improve profitability

Mayfair beverages production

moved to Clayville facility

JohannesburgPretoria

Port ElizabethCape Town

Durban

Clayville UHT facilities

moved to Pinetown

and Port Elizabeth

Clayville, Queensburgh and

PE distribution capacity

extensions

27

73 48 34 019 71 58 10

73

120

154 154

19

90

148157

0

50

100

150

200

0

20

40

60

80

2010/11 2011/12 2012/13 2013/14

Cum

ula

tive c

apex s

pend (

Rm

)

Annual ca

pe

xsp

en

d (

Rm

)

Capex expenditure: planned August 2010 Capex expenditure: updated January 2013

Original cumulative estimate Updated cumulative estimate

PROJECT CIELO BLU

PRODUCTION: CAPITAL EXPENDITURE

28

4

12

36

63

5

13

27

60

0

10

20

30

40

50

60

70

2010/11 2011/12 2012/13 2013/14Rm

Original projected annual savings Updated projected annual savings

PROJECT CIELO BLU

PRODUCTION: SAVINGS (EBITDA)

29

147 16 2069 12 82 21

147

163

184 184

6981

163

184

0

50

100

150

200

0

40

80

120

160

2010/11 2011/12 2012/13 2013/14

Cum

ula

tive c

apex s

pend (

Rm

)

An

nu

al ca

pe

x s

pe

nd

(R

m)

Capex expenditure: planned August 2010 Capex expenditure: planned December 2012

Original cumulative estimate Updated cumulative estimate

PROJECT CIELO BLU

DISTRIBUTION: CAPITAL EXPENDITURE

30

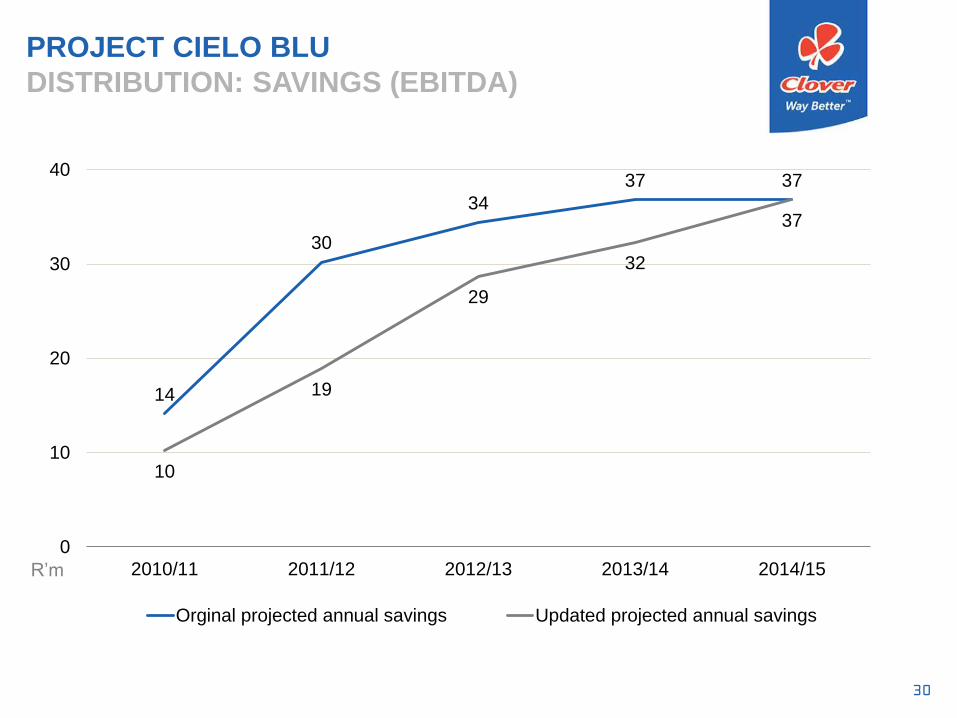

PROJECT CIELO BLU

DISTRIBUTION: SAVINGS (EBITDA)

14

30

34

37 37

10

19

29

32

37

0

10

20

30

40

2010/11 2011/12 2012/13 2013/14 2014/15R’m

Orginal projected annual savings Updated projected annual savings

31

CHALLENGES

FACING THE BUSINESS

32

CHALLENGES FACING THE BUSINESS

Africa expansion

• Pilot project in Nigeria with Tropika dairy fruit mix

• Contract manufacturing by Nigerian company

• Sales and distribution partner

• Aim of pilot is to understand route to market

• Production facilities are key to sustainable model and search is on

• Eventual aim to expand product basket

• Existing presence in Southern African countries with view to expand

influence

33

CHALLENGES FACING THE BUSINESS

Balancing local milk production with local demand

• Milk producers require growth in excess of local market growth

• Traditionally not sufficient raw milk balancing capacity in SA

• Much more long life capacity created in last 18 months

• Locally produced product not always internationally competitive:

› Foreign farmer subsidies

› Economies of scale

• Strong growth in SA exports

34

POTENTIAL

35

ATTRACTIVE GROWTH PROSPECTS

clover

Leveraging

the sales and

distribution

network

Leveraging

the brand

– immense

potential

Product

innovation

Product

extension

Supply chain

cost

efficiencies

Route

to market

FMCG

industry

consolidation

Africa

36

WHAT KEEPS US AWAKE

37

WHAT KEEPS US AWAKE

• Project Cielo Blu implementation:

› Within budget

› Achieving projected benefits

› On time

• Prioritisation of capital for productivity and expansion projects

• Balancing short term shareholder expectations with long term

strategic direction

38

DISCLAIMER

This report contains certain forward-looking statements. Forward-looking statements include, but are not limited to, those with

respect to capital expenditures, cost savings associated with capital projects, timing of capital projects, currency fluctuations,

national milk production, farm gate inflation and expected selling price movements. In certain cases, forward-looking statements

can be identified by the use of words such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled",

"estimates", "forecasts", "intends", "anticipates", or "does not anticipate", or "believes" or variations of such words and phrases,

or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-

looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results,

performance or achievements of the Company to be materially different from any future results, performance or achievement

expressed or implied by the forward-looking statements. Although the Company has attempted to identify important factors that

could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may

be other factors that cause actions, events or results not to be as anticipated, estimated or intended.

It is important to note, that:

• unless otherwise indicated, forward-looking statements indicate the Group’s expectations as at 26 March 2012;

• actual results may differ materially from the Group’s expectations if known and unknown risks or uncertainties affect its

business, or if estimates or assumptions prove inaccurate;

• the Group cannot guarantee that any forward-looking statement will materialise and, accordingly, readers are cautioned not

to place undue reliance on these forward-looking statements; and

• the Group disclaims any intention and assumes no obligation to update or revise any forward-looking statement even if

new information becomes available, as a result of future events, or for any other reason.

39

THANK YOU

Questions and Answers