Download - Marketing On The Go

Interactive Marketing Virtual Conference and Trade Show

Marketing On The Go

Hot Button Panel 1

Harnessing The Latest Tech

Advancements To Reach Mobile Users

Interactive Marketing Virtual Conference and Trade Show

Featured Speakers

Hot Button Panel 1

Brian MorrisseyDigital Editor

Adweek

Nicholas CoveyMarketing Analytics &

Development Manager

Nielsen Wireless & Nielsen

Games

Kevin PerkinsCEO

Greenlight Wireless

Brian MorrisseyDigital Editor

Adweek

The Next Frontier

• 2.6 billion mobile phone

subscribers worldwide; 4 billion

by 2010 (iSuppli)

• 89% of major brands plan to

market on mobile phones next

year (Airwide Solutions, 2/06)

• 52% see mobile occupying 5-25%

of their marketing budget by 2011

(Airwide Solutions, 2/06)

• Market forecast to hit $14 billion

in 2011. (eMarketer)

Current Landscape

• Market: $1.5 billion spent worldwide on mobile ad programs in 2006 (eMarketer)

• Formats: Most programs are texting, banner ads

• Consumer adoption: Phones still used mostly for calling 9 percent use phones for e-mail,15 percent use search (Harris Interactive, 6/07)

• Consumer wariness: 19 percent trust mobile advertising, lowest of all media formats (Nielsen survey, 4/08); majority found all forms of mobile advertising “not acceptable at all” (Harris Interactive, 06/07)

Developments

Internet giants make their moves

• Yahoo: started mobile ad network

in March

• AOL: purchased mobile ad

network Third Screen Media in

May

• Microsoft: bought ScreenTonic in

May

• Google: Here comes the

GPhone?

Carriers vs Internet giants

• Carriers control access to their

networks

• Invested billions in setting up

networks; now see advertising

as key to their future.

• Handset makers like Nokia

want to add services; paid $8

billion for NavTeq

Formats-Search

• Carriers

• Search Engines

• Geo-targeting:Nokia

and Navteq

Formats-Display/Video

• Networks: AdMob,

Third Screen, Yahoo

• Video ads: MobiTV

Formats-Applications

• Special K diet tips

• Nokia city maps in

London

ConfidentialConfidentialConfidential

Advertising and the Mobile Consumer –Research from Nielsen Mobile

Adweek Technology Virtual Tradeshow

October 16, 2007

ConfidentialConfidentialConfidential

Nielsen’s Strategic Acquisition of Telephia

• Telephia has been the leading provider of consumer research to the mobile industry since 1998.

• Serving over 100 telecom and media clients

• Broad portfolio of technology based measurement tools

• Nielsen acquired Telephia in August. We are rapidly integrating.

• Integrate existing data and build new products together

• Provide integrated client service and analytics

• Together, Nielsen and Telephia will allow the mobile media business to develop faster – provide the essential measurement infrastructure

• Market research - provide the consumer data that media companies and operators need to

make programming, pricing, and promotion decisions

• Audience measurement - support a scalable mobile advertising marketplace by providing data

required for targeted advertising

• We will coordinate mobile media measurement with other Nielsen products – holistic, consistent view of media consumption

ConfidentialConfidentialConfidential

Nielsen mobile advertising research addresses each mobile media vehicle available to advertisers

Product Methodology Key Metrics Competitive Advantage Delivery

Mobile Internet

& IM Report

Telephia survey of

~4,000 active mobile

internet users

Top websites, reach, unique

audience, demographic profiling

and segmentation

Largest sample of internet/IM

users per month

Monthly online

(Mobile Internet &

IM)

Mobile Video

Report

Survey of 1,000+

active mobile video

users per quarter

Top channels and programs,

availability, reach,

demographics, daypart, session

length, consumer preferences,

satisfaction

Only source for such a detailed

report due to unparalleled sample

sizes

Quarterly PPT

Mobile Audio,

Applications,

Game, Premium

SMS Reports

Direct measurement

from bills of ~40,000

wireless lines per

month

Top titles (games, ringtones, full-

track music, client apps, short

codes), downloads, purchases,

revenue share, price paid, new

vs. repeat subscriptions,

demographics

Only source for bill-based data

that delivers accurate title-level

detail and revenue performance

Monthly Online

(Games, Audio)

Quarterly XL (Apps,

PSMS)

Mobile

Advertising

Report

Survey of ~20,000

mobile content users

per quarter

Mobile advertising recall,

responses, attitudes and

preferences

Largest sample of mobile content

usersQuarterly PPT

ConfidentialConfidentialConfidential

Source: Telephia bill panel and

survey analysis. Extrapolation

from CTIA and Telephia mobile

universe estimates.

Note: Includes prepaid, postpaid,

and all carriers. Does not include

off-bill.

Text messaging continues to be most popular service; mobile internet is up to 77 million subs

* Trend Break. Classification

Updated

216221

227232

237

124 128

144 148

63 6373 74 77

30

54 54

42

5 6 7 8

166

59

45

97

77

55

68

12

0

50

100

150

200

250

Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007

T o tal US Subs

T ext M essaging

Internet

D o wnlo ad

M ult imedia M essaging

Video

34%

140%

97%

22%

131%

10%

Mobile Content Subscribers (millions)Q2 2006 – Q2 2007, National

YOY growth

ConfidentialConfidentialConfidential

Audience size of audio and games downloaders are reaching critical mass

30

45

54 54

59

25 26 27 27

1416 17

1921

4

9 8

32

13

9

1718

0

10

20

30

40

50

60

70

Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007

T o tal D o wnlo aders

A udio

Games

A pps

P remium SM S

Mobile Downloaders (in millions)Q106-Q107, US

Note: Includes prepaid, postpaid,

and all carriers. Does not include

off-bill.

Source: Telephia bill panel and

survey analysis. Extrapolation

from CTIA and Telephia mobile

universe estimates

* Trend Break. Classification

Updated

*

*

28%

225%

N/A

50%

97%

YOY growth

*

*

ConfidentialConfidentialConfidential

67% 68% 64% 64% 54% 59% 60% 62%

Agree

Disagree

I believe that advertising on my mobile device is

unacceptable

26% 26% 27% 32%45%

34% 31% 35%

Agree

Disagree

I would be willing to have advertising on my mobile

device in exchange for something

15% 14% 15% 23%36%

19% 15%27%

Agree

Disagree

I expect to see more advertising on my mobile phone

12% 12% 14% 17%32%

19% 17% 24%Agree

Disagree

I don’t mind advertising on my mobile phone so long

as it is relevant to my interests

All Data

UsersSMS MMS WAP Video Game Audio App

All Data

UsersSMS MMS WAP Video Game Audio App

All Data

UsersSMS MMS WAP Video Game Audio App

All Data

UsersSMS MMS WAP Video Game Audio App

Source: Q1 07 TAM Survey T1980: How strongly do you agree

or disagree with the following

statements?

How do consumer attitudes towards mobile advertising differ by media vehicle?

ConfidentialConfidentialConfidential 18

70%

61%58%

54%

45%

58%53% 54%

14%

16%18%

20%

27%

18%21% 19%

9%

13% 15%16% 16%

15% 15%15%

3%4% 4% 5% 7% 4% 4% 6%

4% 5% 5% 6% 5% 5% 6% 6%

All Mobile Subs Text

Messenging/SMS

Picture

Messaging/MMS

Mobile Internet Video/Mobile TV Ringtone

dow nloads

Game dow nloads Application

dow nloads

Other/Decline

Asian/Pac

B lack/A f Am

Hispanic

White

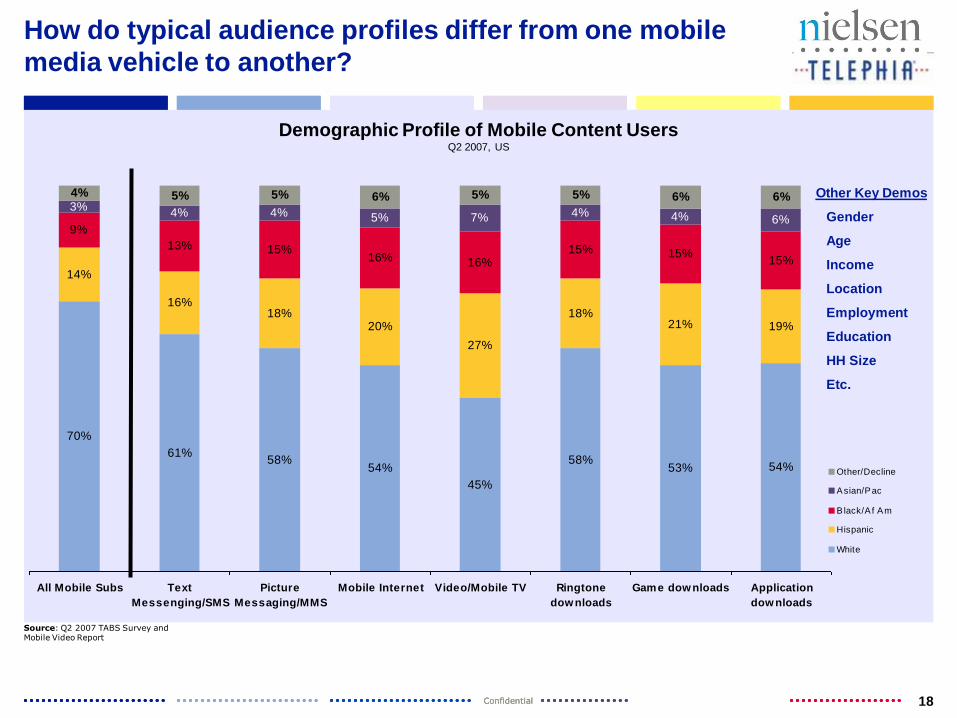

Demographic Profile of Mobile Content UsersQ2 2007, US

How do typical audience profiles differ from one mobile

media vehicle to another?

Source: Q2 2007 TABS Survey and Mobile Video Report

Other Key Demos

Gender

Age

Income

Location

Employment

Education

HH Size

Etc.

ConfidentialConfidentialConfidential

Mobile Internet

ConfidentialConfidentialConfidential

Who has the highest overall reach and frequency on the mobile web?

Top Mobile Internet Websites by Active ReachJuly 2007

34.3%

20.4% 19.9% 19.4%

15.1%

13.0%11.8% 11.5% 11.2%

9.8%

Yahoo!

The W

eath

er

Channel

Searc

h

MS

N H

otm

ail

Gm

ail

AO

L M

ail

ES

PN

CN

N

Maps

MapQ

uest

216.9

110.8

76.8 74.0

51.7 49.8

30.6 30.321.6 21.6

Yahoo!

MS

N H

otm

ail

AO

L M

ail

Gm

ail

The W

eath

er

Channel

Searc

h

ES

PN

CN

N

Maps

Com

cast

Top Mobile Internet Websites by Sessions (M)July 2007

ConfidentialConfidentialConfidential

Mobile Video

ConfidentialConfidentialConfidential

38%

34%

33%

32%

31%

30%

30%

29%

29%

29%

28%

28%

27%

25%

24%

24%

23%

23%

23%

23%

FOX News

Weather Channel

Comedy Central

NBC Mobile

ESPN

FOX Sports

Discovery

MSNBC

CNN to Go

ABC News Now

MTV

ESPN3GTV

Fuse

You tube

HBO Mobile

NFL Network

PrimeTime TV

CNBC

FOX Mobile

Music Choice

Access Reach* – Video ChannelsCurrent Mobile Video Users who Identified their Mobile Video Service (N=1,006)

*Notes – Access indicates the percent of Current Mobile Video users with access to a particular brand or channel. Access Reach indicates that among those with access to a brand or channel, the percent who have watched said channel in the last 30 days.

In addition, only channels and brands with an Access base of 30 or greater were considered for ranking.

M860 Series: Which of the following channels or branded content have you watched on your mobile phone in the past 30 days?

96%

96%

86%

81%

78%

76%

72%

72%

59%

57%

57%

53%

53%

53%

53%

53%

53%

53%

53%

53%

FOX Sports

Weather Channel

ABC News Now

NBC Mobile

Comedy Time

ESPN3GTV

Fashion TV

Mic Hip Hop

iFilm

MAXX SPORTS

Toon World TV

Shift Alternative

Chaos Extreme

TLC

V40

Oxygen Network

IGN Mobile

Animal Planet

CNET

CSPAN

Access – Most Available Video ChannelsCurrent Mobile Video Users who Identified their Mobile Video Service (N=1,006)

Which mobile TV programs have the highest reach

potential?

Mobile Video Channel Subscribers= Among Cingular Video, MobiTV, SprintTV, VCAST and Alltel TV Subscribers

Source: Q1 2007 Mobile Video Survey

Detailed

Demographics by

Video Content

Available

ConfidentialConfidentialConfidential

Mobile Text Campaigns

ConfidentialConfidentialConfidential

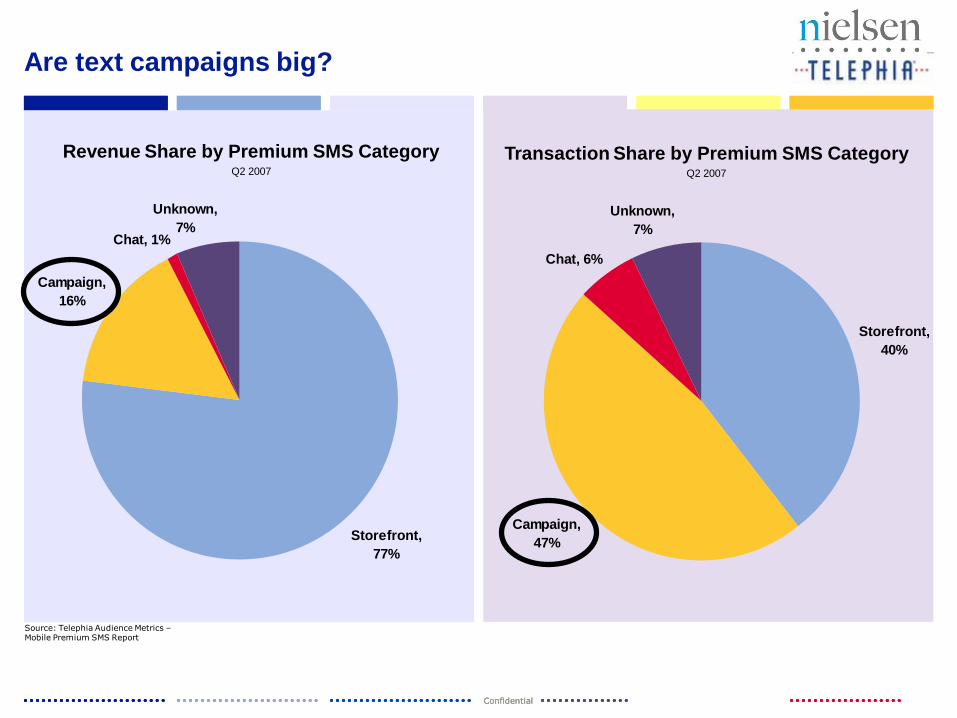

Source: Telephia Audience Metrics –Mobile Premium SMS Report

Revenue Share by Premium SMS CategoryQ2 2007

Are text campaigns big?

Campaign,

16%

Chat, 1%

Unknown,

7%

Storefront,

77%

Campaign,

47%

Chat, 6%

Unknown,

7%

Storefront,

40%

Transaction Share by Premium SMS CategoryQ2 2007

ConfidentialConfidentialConfidential

How have different campaigns reached different audiences?

72, 35%169, 44%136, 34%113, 26%

378,

21%

821,

38%

132, 65%

211, 56%269,

66%

315,

74%

1,435,

79%

1,317,

62%

NBC - Deal Or No Deal Fox - American Idol

Challenge

Fox - My Games Fever CBS New Motion -

bid4prizes

NBC - 1 vs. 100

Female

M ale

2,138

1,813

428 406 380

204

Top PSMS Campaigns by Participants (000)Q2 2007

ConfidentialConfidentialConfidential

Additional Mobile Advertising Metrics

ConfidentialConfidentialConfidential

79%

21%

Viewed Ad

Did Not View Ad

Ad Recall Among Data UsersQ1 2007

Top Ads Recalled Among Ad ViewersQ1 2007

18%

17%

14%

11%

7%

7%

21%

19%

30%

24%

E-mail Sent to

Phone

WAP Banner Ad

Sponsored

Wallpaper

Ringtone Ad

Sponsored

App/Game

Ad While Playing

Game

Ad w/ Phone

Functions

Sponsored

Faceplate

Mobile TV Ad

Music/Streaming

Radio Ad

Source: Q1 07 TAM Survey

Ad Effectiveness: Know which types of ads have the highest recall

ConfidentialConfidentialConfidential

79%

10%

11%

Viewed Ad, Did Not Respond

Viewed Ad, Responded

Did Not View Ad

Ad Recall and Response Among Data UsersQ1 2007

Top Responses Among Ad ViewersQ1 2007

Source: Q1 07 TAM Survey

Ad Effectiveness: Understand how subscribers are interacting with advertisers

18%

18%

15%

13%

12%

11%

21%

20%

29%

22%

Sent SMS

Sent Email

Sent MMS

Visited WAP Site

Click to Call

Entered

Sweepstakes

Made a Purchase

Via Phone

Made a Purchase

Via Store

Used Mobile

Coupon

Requested Mobile

Coupon

ConfidentialConfidentialConfidential

79%

10%

11%

Viewed Ad, Did Not Respond

Viewed Ad, Responded

Did Not View Ad

Ad Recall and Response Among Data UsersQ1 2007

Top Reasons for No ResponseQ1 2007

8%

7%

7%

35%

53%

17%

24%

I wasnt interested in the product

advertised

I never respond to any advertising

I was too busy at the time

I am concerned about privacy or

security

I didnt understand how to respond

My phone data connection is too

slow

Other

Ad Effectiveness: Optimize ad strategies by knowing why subscribers don’t respond to ads

Source: Q1 07 TAM Survey

ConfidentialConfidentialConfidential

Thank You

To learn more about the integrated Nielsen Mobile, contact

Nicholas CoveyNielsen Mobile(312) [email protected]

© Greenlight Wireless 2007 • Slide #31

Understanding Mobile Advertising

Presented By Kevin PerkinsCEO Greenlight Wireless for Nielsen

Where’s Mobile Advertising?

• With over 2 billion phone users worldwide, the

Mobile Search and Advertising industry is

poised to reach $11 billion by year 2011*

© Greenlight Wireless 2007 • Slide #32

2007 2011

$600MM

$11B

?

Bigger??

Smaller?

Farther out?

Sources: Informa Telecoms & Media, Datacomm Research, Piper Jaffray

Greenlight Wireless

Publishers Face Challenges With

Mobile Web

• Publishers need to create efficient mobile content dynamically

• Users want quick, transactional access to relevant content

• Devices are extremely diverse and not standardized

• Content is consumed on a much smaller display

© Greenlight Wireless • All Rights Reserved • Slide #33

Greenlight Wireless

Facts About Mobile Advertising

• Many new “made-for-mobile” ad companies have emerged, yet their ad supply is scarce and untargeted (run-of-site)

• Made-for-mobile ads average about $0.02 - $0.04 cost-per-click (CPC), before revenue sharing

• Made-for-mobile banner adsmonetize even worse: publishers average $1 - $3 CPM (cost per thousand impressions)

© Greenlight Wireless • All Rights Reserved • Slide #34

Examples of

“made-for-mobile”

ads

Greenlight Wireless

Mobile Advertising Specifications

Courtesy: Mobile Marketing Association

What To Watch Out For

• Costly, over-reaching campaigns

– What are you really getting?

– Where there’s mystery, there’s margin!

• Metrics hype

– “We served _______ ads this month.”

• Low revenue-per-impression/click

– Distribution is key

– Rev share needs to be factored in

© Greenlight Wireless 2007 • Slide #36

What Are Keys To Adoption?

• User Experience

– Must Be Easy: to

use, access, and

react

• Push vs. Pull

– Users need to initiate

• Relevant*

– If your offer is relevant

to a user, then the

stigma of “advertising”

is not a factor

© Greenlight Wireless 2007 • Slide #37

Why won’t you do what I want?!!

Greenlight Wireless

Campaign Fits and Starts

• Branding Example– Carl’s Jr.’s “Hot Buns” ringtone

• Leveraged existing creatives

• No carrier involvement; straight-to-end-user via website

• Viral, Free

• SMS Voting In Media– American Idol

– Privacy concerns

• M-Commerce– Emergence of mobile coupon

companies

– Not a technical issue; it’s the supply chain

Courtesy: Cellfire.com

Courtesy: ATT.com

Courtesy: CarlsJr.com

What Kind Of Mobile Advertising

Shows The Most Promise?

• Local Search = “I need to find now.”

• Click-to-Call = “I need to act now.”

• Social Networks = “I need you now.”

© Greenlight Wireless 2007 • Slide #39

Mobile users want

transactional information

that puts them at the

epicenter of their actions

Courtesy: Pepperdine.edu

Getting Started

Find a good cost-per-click provider that has transparency to where your ads are distributed

Look for a technology or platform that can leverage your existing marketing efforts

Don’t waste money on channels that don’t convert

Get metrics

Ask around, do some homework; don’t be afraid to run many trials until your result is accomplished

© Greenlight Wireless 2007 • Slide #40

Greenlight Wireless

Greenlight Wireless

Kevin Perkins, CEO

22651 Lambert Street, Suite 106

Lake Forest, CA 92630

O: +1-949-421-1551

www.greenlightwireless.net

© Greenlight Wireless 2007 • Slide #41

Interactive Marketing Virtual Conference and Trade Show

Q & A Panel

Hot Button Panel 1

Brian MorrisseyDigital Editor

Adweek

Nicholas CoveyMarketing Analytics &

Development Manager

Nielsen Wireless & Nielsen

Games

Kevin PerkinsCEO

Greenlight Wireless

Interactive Marketing Virtual Conference and Trade Show Hot Button Panel 1

Upcoming Presentations

3:00 pm Eastern

Hot Button Panel #2:

Reach Out And Touch Somebody:

Embrace Social Networking And Extend Brand Awareness

5:00 pm Eastern

Hot Button Panel #3:

Everything You Need To Know About Search Engine

Marketing