MacquarieResearchEquities

The economic outlook and trendsfor the Australian

mobile telecommunications industry

Tim SmartMacquarie Research Equities

Phone: (612) 8232 [email protected]

www.macquarie.com.au/research

In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. Please see disclaimer.

MacquarieResearchEquities

Page 2 of 17

Presentation outline

Overview of recent developments

Assessing the current market in Australia

Snapshot – key industry metrics

Subscriber growth – racing towards the end of the track

Retention costs – handset subsidies fuelling subs growth and shorter handset refresh cycle

ARPU

Voice revenues under threat

Data revenues – where is the vision?

Economic outlook – is consolidation needed?

MacquarieResearchEquities

Page 3 of 17

Attempt to reduce/eliminate handset subsidies in 2002

Telstra introduces “more4you”

Vodafone introduces “no plans” and reduces contract subsidies

Optus wins market share, improves margins

Handset subsidies reintroduced aggressively

Fuels market growth (sub adds for 6 months to June 03, 7.5% greater than in corresponding 6 months in 02)

Penetration now up to 71.8%

Recent developments and trends - local

MacquarieResearchEquities

Page 4 of 17

Hutchison 3G launches in April in Sydney and Melbourne and in July launched in remaining capital cities

Telstra, Optus, Vodafone marketing 2.5G services

Vodafone announces it will supply 3G services by 1H05, preference to share, rather than build infrastructure

Telstra,Optus remain non-committal on 3G timing – not in FY04

ACCC investigates mobile termination rates

Recent developments and trends - local

MacquarieResearchEquities

Page 5 of 17

European regulators aggressively reduce mobile termination rates

Hutchison launches 3G services in UK, Italy and Sweden

Wi-fi growth accelerates – carriers looking to integrate with mobile data offering

Performance and take up of new data services (2.5G, MMS, 3G) mixed

The outlook for mobile carriers continues to be difficult globally

Recent developments and trends - global

MacquarieResearchEquities

Page 6 of 17

Global wireless indices

Notes: Asian index excludes JapanAll indices are in US$

Source: Bloomberg

MacquarieResearchEquities

Page 7 of 17

Australian mobile market snapshot –key metrics

Penetration at 71.8% at June 2003

Telstra and Optus remain dominant

ARPU falling as prepaid increases and voice yields fall

Australian Mobile Subscribers

-

1,000

2,000

3,000

4,000

5,000

6,000

2002 2003 2004 2005

Su

bs

('00

0s)

Postpaid

Prepaid

3G

2003 2004f 2005fSubscribers Penetration 71.8% 79.5% 82.5% Number of subscribers ('000s) 14,349 16,047 16,820 Subscriber growth (YoY) 16% 12% 5% Percentage postpaid 61.0% 55.1% 52.1% Percentage prepaid 38.9% 42.9% 44.0% Percentage 3G 0.1% 2.1% 3.9%

Market Shares Telstra 46.3% 45.8% 44.7% Optus 34.2% 34.1% 34.1% Vodafone 17.5% 18.1% 17.5% 3 (Hutchison) 1.9% 2.1% 3.8%

Revenues Industry revenues (A$ '000s) 9,019.5 9,738.8 10,322.7 Revenue growth 7.2% 8.0% 6.0%

ARPU ARPU - blended 50.87 48.09 46.98 Growth -9.1% -5.5% -2.3% ARPU - postpaid 66.89 65.70 65.05 ARPU - prepaid 23.62 23.30 23.07 ARPU - 3G 55.02 95.62 95.18 Voice rev/min 100.24 103.75 107.90 Data ARPU 4.99 7.07 10.52Source: MRE

Source: MRE

MacquarieResearchEquities

Page 8 of 17

Mobile profitability – a three part equation

SUBSCRIBERS: mobile penetration x market share

TIMES

ARPU: outgoing voice revenues + incoming termination revenues

+ data revenues

MINUS

COSTS: cost of retention / acquisition (incl. handset subsidies) +

other operating costs

= MOBILE PROFITABILITY

MacquarieResearchEquities

Page 9 of 17

Subscriber growth – has been the dominant component of the mobile profit equation…

…BUT growth is finite

Reintroduction handset subsidies and H3G entry has accelerated growth again

Australia now at 71.8% penetration

Penetration forecast to reach 80% by FY05

Having been the dominant component in industry profitability equation, it will soon become least important part of equation

Singapore market growth has slowed dramatically since penetration neared 80%

Subscribers – racing towards the end of the track

MacquarieResearchEquities

Page 10 of 17

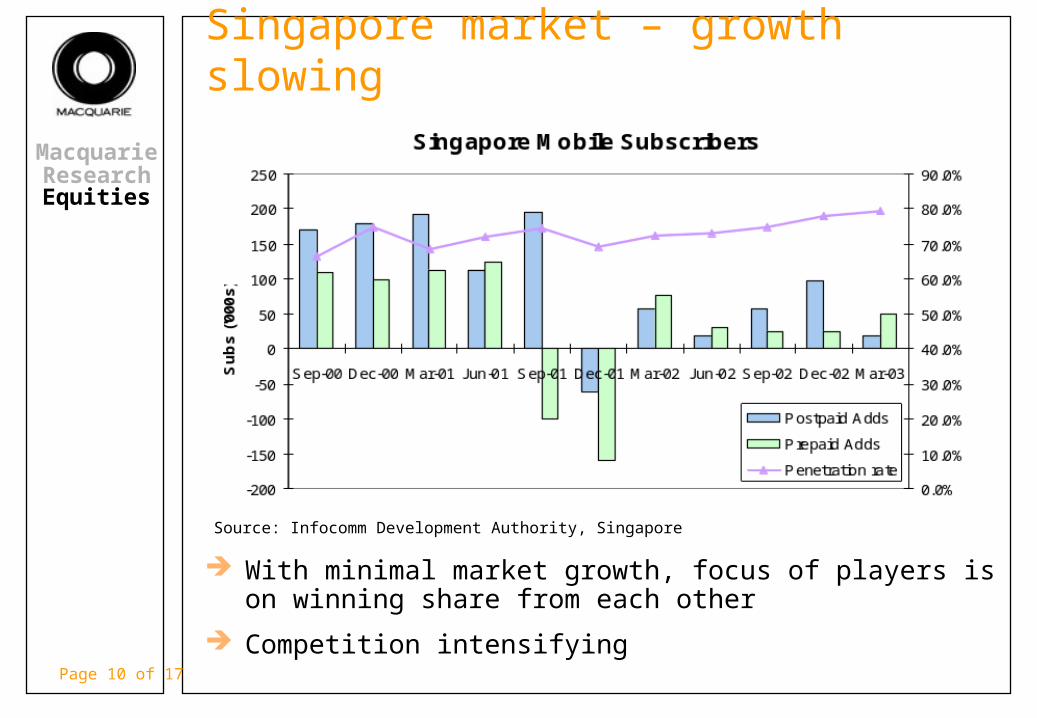

Singapore market – growth slowing

Source: Infocomm Development Authority, Singapore

With minimal market growth, focus of players is on winning share from each other

Competition intensifying

MacquarieResearchEquities

Page 11 of 17

So, where is Australia?

Source: MRE

Subscriber growth is likely to slow dramatically after 2004, with penetration growing slightly above 80% level

MacquarieResearchEquities

Page 12 of 17

ARPU – voice under pressure Voice yields falling at double digit rates and likely to continue. Why?

Lack of industry subs growth will intensify competition for existing subscribers. Reducing voice one way to win market share.

3G introduces massive new capacity. Little incremental cost so voice will be priced down to increase network utilisation.

Incoming voice revenues subject to regulatory threat (ACCC review)

Source: MRE Source: MRE

MacquarieResearchEquities

Page 13 of 17

Source: MRE

Steady data growth driven by SMS

Little take-up of new data services

Data ARPU – key to the industry’s future

MacquarieResearchEquities

Page 14 of 17

If voice yields fall at double digit rates (10%) as we expect and incoming termination rates decline at 5% pa (or worse), then data ARPUs would need to grow at a compound rate of 20% pa just to maintain overall ARPU in 5 years time.

MMS, 2.5G, 1x and 3G networks all in place…BUT service delivery is poor and take up minimal

SMS remains main component of data revenues

Issue: Can telcos deliver content and services that customers actually want?

Evidence in Australia to date is not positive

Some offshore carriers appear to doing a better job

Sprint PCS Vision saw a 62% subscriber growth from 1.3m in 1Q03 to 2.1m in 2Q03. Data ARPU per subscriber also grew during the same period by 29%.

Data ARPU – key to the industry’s future

MacquarieResearchEquities

Page 15 of 17

Handset refresh cycle is shortening

Estimate 5.2m handset sales in 2003, an increase of 25% on 2002. Subscriber growth in 2003 is 16%.

Colour screen phones, cameras and polyphonic ringtones encouraging refresh cycle BUT accompanied by increasing subsidies.

Potentially dangerous combination – handset life cycle down, handset subsidies up…

…good for handset vendors (and dealers) but not good for carriers.

Costs – retention / acquisition costs increasing

MacquarieResearchEquities

Page 16 of 17

Good news: Average annual revenues growth forecast to be 6.3% pa for the next 5 years – above GDP level

Bad news: Good revenue growth does not mean attractive returns eg. aviation industry

Key issue: How much capital is invested in the industry

Consolidation – is it needed?

…not at the service layer – sufficient industry size, diversity and niches to justify many service providers

…issue is at the infrastructure level

Number of 3G networks will be the dominant factor in determining returns for the industry over the next 5-10 years.

Economic outlook

MacquarieResearchEquities

Page 17 of 17

Disclaimer: Macquarie Equities (Australia) Ltd; Macquarie Equities (UK) Ltd; Macquarie Securities (USA) Inc; Macquarie Equities (Asia) Ltd; Macquarie Securities (Asia) Pte Ltd; and Macquarie Equities New Zealand Ltd are not authorised deposit-taking institutions for the purposes of the Banking Act (Commonwealth of Australia) 1959, and their obligations do not represent deposits or other liabilities of Macquarie Bank Ltd ABN 46 008 583 542. Macquarie Bank Ltd does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. © Macquarie Group. This research has been prepared for the use of the wholesale clients of Macquarie Bank Ltd and its wholly-owned subsidiaries (the “Macquarie Group”) and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the information in this research in any way. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice and accurately reflect the analyst(s)' personal views at the time of writing. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. This research has been issued and distributed in Australia, by Macquarie Equities (Australia) Ltd (ABN 58 002 832 126), a licensed securities dealer and a participating organisation of the Australian Stock Exchange Ltd; in the UK and Germany, by Macquarie Equities (UK) Ltd, which is authorised and regulated by the Financial Services Authority (No. 3704031). Its related body corporate, Macquarie Bank Ltd, is a member of the London Stock Exchange and is authorised and regulated by the Financial Services Authority (the investments and investment services the subject of this research are not available to private customers in the UK); in the US, by Macquarie Securities (USA) Inc. Any transactions by US persons in any security discussed in this research must be carried out through Macquarie Securities (USA) Inc; in Hong Kong, by Macquarie Equities (Asia) Ltd, a registered dealer under the Securities and Futures Ordinance; approved for distribution in Singapore by Macquarie Securities (Asia) Pte Ltd, a licensed dealer and investment adviser in Singapore. All enquiries from Singapore residents in relation to securities referred to in this research should be directed to Macquarie Securities (Asia) Pte Ltd; in New Zealand, by Macquarie Equities New Zealand Ltd, a licensed sharebroker and member of the New Zealand Stock Exchange. The Macquarie Group of companies and their officers and employees may have interests in securities referred to in this research, including being directors of, or providing investment banking services to, their issuer. Further, they may act as market maker or buy or sell those securities as principal or agent, and as such may effect transactions which are not consistent with the recommendations (if any) in this research. The analyst(s) principally responsible for the preparation of this research receives compensation based on the Firm's overall revenues, including investment banking revenues. The reader should assume that the Macquarie Group receives or has received compensation in connection with these relationships. Disclosures applicable to research with respect to issuers, if any, mentioned herein, are available at www.macquarie.com.au/research/disclosures, through Macquarie Research Equities at [email protected] or your Macquarie representative.