Download - Lecture 3-Job Order Costing

Accy211: Management Accounting IIAutumn Session 2013

Week 3 1

Job Order CostingLearning Objectives

2

1. Distinguish between job costing and process costing

2. Job costing overview3. Compute predetermined overhead rate (POHR)4. Compute job cost5. Track the flow of costs in a job-costing system6. Record transactions in the general and subsidiary

ledgers7. Account for end-of-period underallocated or

overallocated indirect costs using alternative methods

Learning Objective 1

Distinguish between process costing and job-order costing and identify companies that

would use each costing method.

3

Job-Costing: system accounting for distinct cost objects called Jobs. Each job may be different from the next, and consumes different resources

Wedding announcementsAircraftadvertising

Process-Costing: system accounting for mass production of identical or similar products

Oil refining, orange juice

Types of Product-Costing Systems

4

Used for production of small, identical, low cost items.Mass produced in automated continuous production process.Costs cannot be directly traced to each unit of product.Typical process cost applications:

Petrochemical refineryPaint manufacturerPaper mill

Process Costing

5

Used for production of large, unique, high-cost items. Built to order rather than mass produced.Many costs can be directly traced to each job.Job-shop operations--Products manufactured in very low volumes or one at a time.Batch-production operations Multiple products in batches of relatively small quantity. Typical job-order cost applications: Special-order printing, Building construction, Also used in service industry—Hospitals, Law firm.

Job Order Costing

6

Page 1 of 12

A company that manufactures dentures for use by local dentists would use

A) process costing.B) personal costing.C) operations costing.D) job costing.

Quick Check

7

Which of the following companies would be likely to use job-order costing rather than process costing?a. Scott Paper Company for Kleenex.b. Architects.c. Heinz for ketchup.d. Caterer for a wedding reception.e. Builder of commercial fishing vessels.

Quick Check

8

Costing Systems Illustrated

9

Learning Objective 2

Job Order Costing Overview

10

Traced directlyto each job

Traced directly

to each job

TheJob

Direct labor

Directmaterials

Manufacturing overhead (OH) Applied to each job

using a predetermined rate

1

24

3

Applie

d us

ing

a

pred

eter

min

ed ra

te

Step 1: Identify the chosen cost object.Step 2: Identify the direct costs of the job. Step 3: Compute the indirect costs of the Job.Step 4: Compute the total cost of the job.

11

Manufacturing Overhead

Trace direct

material and direct labor costs to each job as work is

performed.

Direct Materials

Direct Labor

Direct Manufacturing Costs

Job No. 2DM xxDL xxMOH xx

xx

Job No. 3DM xxDL xxMOH xx

xx

Job No. 1DM xxDL xxMOH xx

xx

12

Page 2 of 12

Manufacturing Overhead, including indirect

materials and indirect labor, are allocated

to all jobs rather than

directly traced to each job.

Indirect Manufacturing Costs

Direct Materials

Direct Labor

Manufacturing Overhead

Job No. 2DM xxDL xxMOH xx

xx

Job No. 3DM xxDL xxMOH xx

xx

Job No. 1DM xxDL xxMOH xx

xx

13

Job Costing

Actual Costing

Normal Costing

14

Job DM xxDL xxMOH xx

xx

Actual cost (AR x AQ)

Job DM xxDL xxMOH xx

xx

Actual cost (AR x AQ)

Actual cost (AR x AQ)

Actual cost (AR x AQ)

Actual cost (AR x AQ)

Budgeted cost (BR xAQ)

Learning Objective 3

Compute predetermined overhead rate

(POHR)

15

Direct Materials

Direct Labor

Manufacturing Overhead

Job No. 2DM xxDL xxMOH xx

xx

Job No. 3DM xxDL xxMOH xx

xx

Job No. 1DM xxDL xxMOH xx

xx

Manufacturing overhead is applied to jobs that are in

process.

An allocation base, such as direct labor hours, direct labor dollars, or machine

hours, is used to assign manufacturing

overhead to individual jobs.

16

Why Use an Allocation Base?We use an allocation base because:1. It is impossible or difficult to trace overhead costs

to particular jobs.2. Manufacturing overhead consists of many

different items ranging from the grease used in machines to production manager’s salary.

3. Many types of manufacturing overhead costs are fixed even though output fluctuates during the period.

17

The predetermined overhead rate (POHR) used to apply overhead to jobs is determined before

the period begins.

Manufacturing Overhead Application

18

Page 3 of 12

Using a predetermined rate makes itpossible to estimate total job costs sooner.

Actual overhead for the period is notknown until the end of the period.

The Need for a POHR

19

Determining Predetermined Overhead Rates

Predetermined overhead rates are calculated using a three-step process.

Estimate the level of production for the

period.

Estimate total amount of the allocation base

for the period.

Estimate total manufacturing

overhead costs.

POHR = ÷ 20

Actual amount of allocation is based upon the actual level of

activity (normal costing system).

Based on estimates, and determined before the

period begins.

Application of Manufacturing Overhead

Overhead applied = POHR × Actual activity

21

Learning Objective 4

Compute Job Order Cost

22

Actual Costing- Example

23

Freeman company is planning to sell a batch of 25 special machines (Job 650) to a retailer for $114,800. Direct costs are: Direct materials $50,000; Direct manufacturing labor $19,000. The cost allocation base is machine-hours and Job 650 used 500 machine-hours of the 2,480 machine-hours used by all jobs. Actual manufacturing overhead costs were $65,100.

What is the gross margin of the Job650?

24

Step 1: Identify the chosen cost object. ……….Step 2: Identify the direct costs of the job.

Step 3: Identify the indirect costs of the job.

Step 4: Compute the total cost of the job.

RevenuesCost of goods soldGross margin

Gross Margin

Page 4 of 12

Job Costing

Actual Costing

Actual direct material and direct labor

combined with actual overhead.

Normal Costing

Actual direct material and direct labour

combined with predetermined

overhead. 25

The total cost of the job No 650Direct materials $50,000Direct labor 19,000Factory overhead 12,500Total $81,500

The total cost of the job No 650Direct materials $50,000Direct labor 19,000Factory overhead 13,125Total $82,125 Job WR53 at NW Fab, Inc. required $200 of direct

materials and 10 direct labor hours at $15 per hour. Estimated total overhead for the year was $760,000 and estimated direct labor hours were 20,000. What would be recorded as the cost of job WR53?

a. $200.b. $350.c. $380.d. $730.

Quick Check

26

Job-Order Costing Source Documents

27

Job Cost RecordRoseCo Job-Cost Record

Job Number A - 143 Date Initiated 3-4-X6Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labor Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate Amount

Cost Summary Units ShippedAmount Date Number Balance

Direct MaterialsDirect LaborManufacturing OverheadTotal CostUnit Cost

Product Costs

28

Materials Requisition FormRoseCo Materials Requisition Form

Requisition No. X7 - 6890 Date 3-4-X6Job No. A - 143Department B3

Description Quantity Unit Cost Total Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

Authorized Signature Will E. Delite

29

Employee Time TicketRoseCo Employee Time Ticket

Time Ticket No. 36 Date 3-5-X6Employee I. M. Skilled Station 42

Starting Ending Hours HourlyTime Time Completed Rate Amount Job No.0800 1600 8.00 11.00$ 88.00$ A-143

Totals 8.00 11.00$ 88.00$ A-143

Supervisor C. M. Workman

30

Page 5 of 12

Rose Co applies overhead based on direct- labor hours. Total estimated overhead for the year is $640,000. Total estimated labor cost is $1,400,000 and total estimated labor hours are 160,000.

Overhead Application Example

$640,000160,000 direct-labor hours (DLH)

MOHR =

MOHR = $4.00 per DLH

For each direct labor hour worked on a job, $4.00 of factory overhead will be applied to

the job.

MOHR = Budgeted manufacturing overhead costBudgeted amount of cost driver (or activity base)

31

RoseCo Job-Cost Record

Job Number A - 143 Date Initiated 3-4-X6Date Completed 3-5-X6

Department B3 Units Completed 2Item Wooden cargo crate

Direct Materials Direct Labor Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$ 36 8 88$ 8 4$ 32$

Cost Summary Units ShippedAmount Date Number Balance

Direct Materials 116$ Direct Labor 88$ Manufacturing Overhead 32$ Total Cost 236$ Unit Cost 118$

Product Costs

Completed Job Cost Record

32

Learning Objective 5

Understand the flow of costs in a job-order costing system and prepare appropriate accounting

entries to record costs.

33

Job-Order Costing Document Flow Summary

A sales order is the basis of issuing a production order.

A production order initiates work on a job.

34

Job Cost Sheets

MaterialsRequisition

Manufacturing Overhead Account

Direct materials

Indirect materials

Materialsused may be

either direct orindirect.

35

Job Cost Sheets

Employee Time Ticket

Manufacturing Overhead Account

Anemployee’s

time may be eitherdirect orindirect.

Direct Labor

Indirect Labor

36

Page 6 of 12

Manufacturing Overhead Account

OtherActual OHCharges

Job Cost Sheets

POHR rate used to apply

overhead

MaterialsRequisition

EmployeeTime Ticket

IndirectLabor

IndirectMaterial

37

Using normal costing rather than actual costing requires that the allocating of indirect manufacturing costs to work in process be

A) done on a more timely basis, such as every two weeks rather than every month.

B) journalized only at year end when adjusting entries are normally made.

C) calculated by using the budgeted rate times actual quantity of allocation base.

D) calculated by using the budgeted rate times the budgeted quantity of allocation base.

Quick Check

38

Job-Order Costing –Typical Accounting

Entries

39

Material Purchases

Raw material purchases are recorded in material control account.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Raw Materials XXXXX Accounts Payable XXXXX

40

Direct materials issued to a job increase Work in Process and decrease Raw Materials. Indirect materials used on a job are charged to Manufacturing Overhead and also

decrease Raw Materials.

Material Use

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work-in-Process XXXXXManufacturing Overhead XXXXX Raw Materials XXXXX

41

Labor

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work-in-Process XXXXXManufacturing Overhead XXXXX Salaries and Wages Payable XXXXX

The cost of direct labor incurred on a job increases Work in Process and the cost of indirect labor on a

job increases Manufacturing Overhead.

42

Page 7 of 12

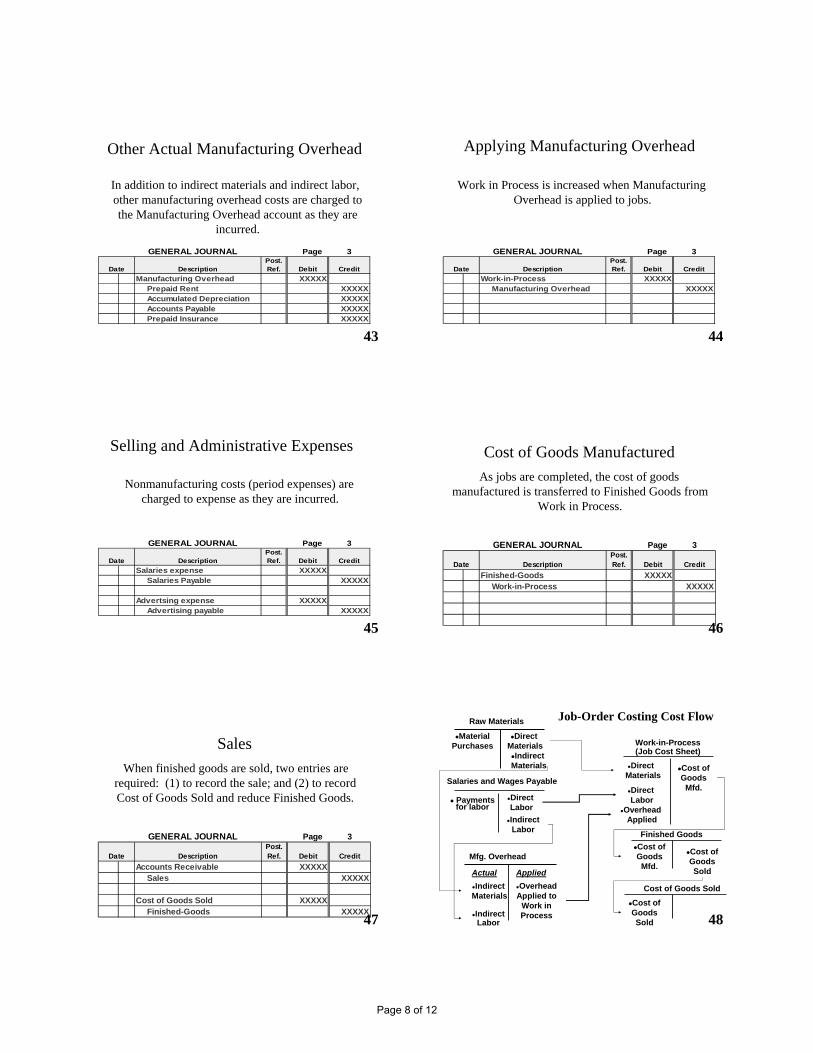

Other Actual Manufacturing Overhead

In addition to indirect materials and indirect labor, other manufacturing overhead costs are charged to the Manufacturing Overhead account as they are

incurred.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Manufacturing Overhead XXXXX Prepaid Rent XXXXX Accumulated Depreciation XXXXX Accounts Payable XXXXX Prepaid Insurance XXXXX

43

Applying Manufacturing Overhead

Work in Process is increased when Manufacturing Overhead is applied to jobs.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work-in-Process XXXXX Manufacturing Overhead XXXXX

44

Selling and Administrative Expenses

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Salaries expense XXXXX Salaries Payable XXXXX

Advertsing expense XXXXX Advertising payable XXXXX

Nonmanufacturing costs (period expenses) are charged to expense as they are incurred.

45

Cost of Goods ManufacturedAs jobs are completed, the cost of goods

manufactured is transferred to Finished Goods from Work in Process.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Finished-Goods XXXXX Work-in-Process XXXXX

46

SalesWhen finished goods are sold, two entries are

required: (1) to record the sale; and (2) to record Cost of Goods Sold and reduce Finished Goods.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Accounts Receivable XXXXX Sales XXXXX

Cost of Goods Sold XXXXX Finished-Goods XXXXX

47

Raw Materials

MaterialPurchases

DirectMaterials

IndirectMaterials

DirectLabor

Mfg. Overhead

Salaries and Wages Payable

Work-in-Process(Job Cost Sheet)

DirectMaterials

OverheadApplied to

Work inProcessIndirect

Labor

DirectLabor

OverheadAppliedIndirect

Labor

IndirectMaterials

Actual Applied

Payments for labor

Job-Order Costing Cost Flow

Cost ofGoodsMfd.

Finished Goods

Cost ofGoodsSold

Cost of Goods Sold

Cost ofGoodsSold

Cost ofGoods

Mfd.

48

Page 8 of 12

(1)(2)

−

−

−(3)

−

−

−

−(4)(5)

(6)

− Job No 650—500 hours

− Job No 651—1,000 hours

− Job No 652—980 hours(7)

(8)(9)Required:(a)(b)(C)

(I)

(II)

Manufacturing Overheads allocated

Ending Balances

Work in process $24,500 $64,500Finished Goods $25,000 $38,000Cost of goods sold $12,500 $81,500

$62,000 $184,000

Record the above transactions in the ledger

Wages payable were paid

Job No. 651 incurred direct labour costs of $3,000, Job No. 652 incurred direct labour costs of $10,000. $5,000 of indirect labour was also incurred.

Assume that depreciation for the period is $26,000. Other manufacturing overhead incurred amounted to $19,100.

Overhead allocated to the jobs using machine hours. The actual machine hours used by each job is as follows:

Job No. 650 incurred direct labour costs of $19,000

Jobs costing $119,500 (Job No 650 and 651) were completed and transferred to finished goods.Job 650 was sold for $114,800. Marketing and administrative salaries were $9,000 and $10,000.

$50,000 were issued to Job No. 650 and $10,000 were issued to Job No. 651 $30,000 were issued to job No. 652 $15,000 of indirect materials were also issued

Total manufacturing payroll for the period was $37,000.

write off to cost of goods soldManufacturing overhead data and ending balances of inventories at the year end are as follows:

Job Order Costing Example

Compute the under or over allocated manufacturing overheadDispose under or over allocated overheads using

Proration based on ending balances in work in process, finished goods and cost of goods sold.

Freeman company in Wollongong uses a normal costing system and allocates manufacturing overhead costs to jobs using machine hours. The company budgets $60,000 for total manufacturing overhead costs and 2,400 machine hours. The following data pertain to th

$110,000 worth of materials (direct and indirect) were purchased on credit. Materials costing $105,000 were sent to the manufacturing plant floor.

Page 9 of 12

Manufacturing Overhead Allocation RateP

POHR=

Manufacturing Overheads AllocatedJob 650Job 651Job 652

Job 651

Job 652

SUBSIDIARY LEDGERMarketing and Administrative Salaries

Marketing and Administrative Salaries Payable

Job 650

Accumulated Depreciations

Miscellaneous Accounts

Accounts Receivable Control

Sales

Manufacturing Overhead Control

Cash Control

Finished Goods Control

Cost of Goods Control

Direct Materials Control Accounts Payable Control

Wages Payable Control Work in Process Control

Page 10 of 12

Learning Objective 8

Approaches to disposing underallocated

or overallocated overhead

49

Problems of Overhead ApplicationThe difference between the overhead cost applied to Work in Process and the actual overhead costs of a period is referred to as either underapplied or overapplied overhead.

Underapplied overheadexists when the amount of overhead applied to jobs

during the period using the predetermined overhead rate is less than the total

amount of overhead actually incurred during the period.

Overapplied overheadexists when the amount of overhead applied to jobs

during the period using the predetermined overhead

rate is greater than the total amount of overhead actually incurred during the period.

50

Underallocated indirect costs

Note: credit balance shows an over allocated manufacturing overhead costs

Manufacturing Overhead Control(2) 15,000(3) 5,000(5) 45,100Bal. 3,100

(6) 62,000 2,480 mh× $25 MOA rate

= $62,000

65,100

51

Actual manufacturing overhead costs of $65,100 are more than the budgeted amount of $60,000.Actual machine-hours of 2,480 are more than the budgeted amount of 2,400 hours.As a result, 2,480x 25 =$62,000 allocated to jobs when actual MOH costs was $65100, resulting $3,100 under allocated overhead cost.

What caused the under/over allocated manufacturing overheads?

Budget ActualCost $60,000 $65,100Machine hours 2400 h 2480hRate 25.00 26.25

52

Tiger, Inc. had actual manufacturing overhead costs of $1,210,000 and a predetermined overhead rate of $4.00 per machine hour. Tiger, Inc. worked 290,000 machine hours during the period. Tiger’s manufacturing overhead is

a. $50,000 overapplied.b. $50,000 underapplied.c. $60,000 overapplied.d. $60,000 underapplied.

Quick Check

53

Disposition of Under- or OverappliedOverhead

$3,100 may beclosed directly to

cost of goods sold.

Cost of Goods Sold

Work inProcess

FinishedGoods

Cost of Goods Sold

$3,100may be allocatedto these accounts.

OR

54

Page 11 of 12

(1) Immediate Write-off to Cost ofGoods Sold Approach

Manufacturing Overhead 65,100 62,000

3,100 0

Cost of Goods Sold 81,500 3,100

84,600

55

(2) Allocating Under- or OverappliedOverhead Between Accounts

Ending balances of Work in Process,Finished Goods, and Cost of Goods Sold

Work in Process $ 64,500 35%Finished Goods 38,000 21%Cost of Goods Sold 81,500 44%Total $184,000 100%

Allocation of $3,100

1,085651

1,3643,100

56

Manufacturing Overhead Finished Goods65,100 62,000 62,500

3,100 651 0 63,151

Cost of Goods Sold Work in Process81,500 40,000 1,364 1,085

83,236 41,085

57

Which of the following accounts is not classified as an asset?

A)Manufacturing overhead control B) Materials controlC) Work-in-process controlD)Finished goods control

Quick Check

58

The Precision Widget Company had the following balances in their accounts at the end of the accounting period:

Work in Process $ 15,000Finished Goods 35,000Cost of Goods Sold 200,000

If their manufacturing overhead was overallocated by $8,000 and Precision Widget adjusts their accounts using a proration based on total ending balances, the revised ending balance for Cost ofGoods Sold would be

A)$193,600B) $200,000C)$207,120.D)$208,000.

Quick Check

59

END

60

Page 12 of 12