J o u r n a l o f E c o n o m i c C o o p e r a t i o n

& Development

J o u r n a l o f E c o n o m i c C o o p e r a t i o n

& Development

Stat i s t ica l Economic and Socia l Research

and Training Centre for Islamic Countries

(SESRIC)

Journ

al of Econ

omic C

ooperation

and

Develop

men

t

Se

pte

mb

er 2016

VO

LU

ME

37, N

o.3

ISSN 1308 - 7800 Volume 37, No. 3 September 2016ISSN 1308 - 7800 Volume 37, No. 3 September 2016

Oil Price Effects on Exchange Rate, Output and Consumer Price: A Case Study of Small Open Economy of Oman

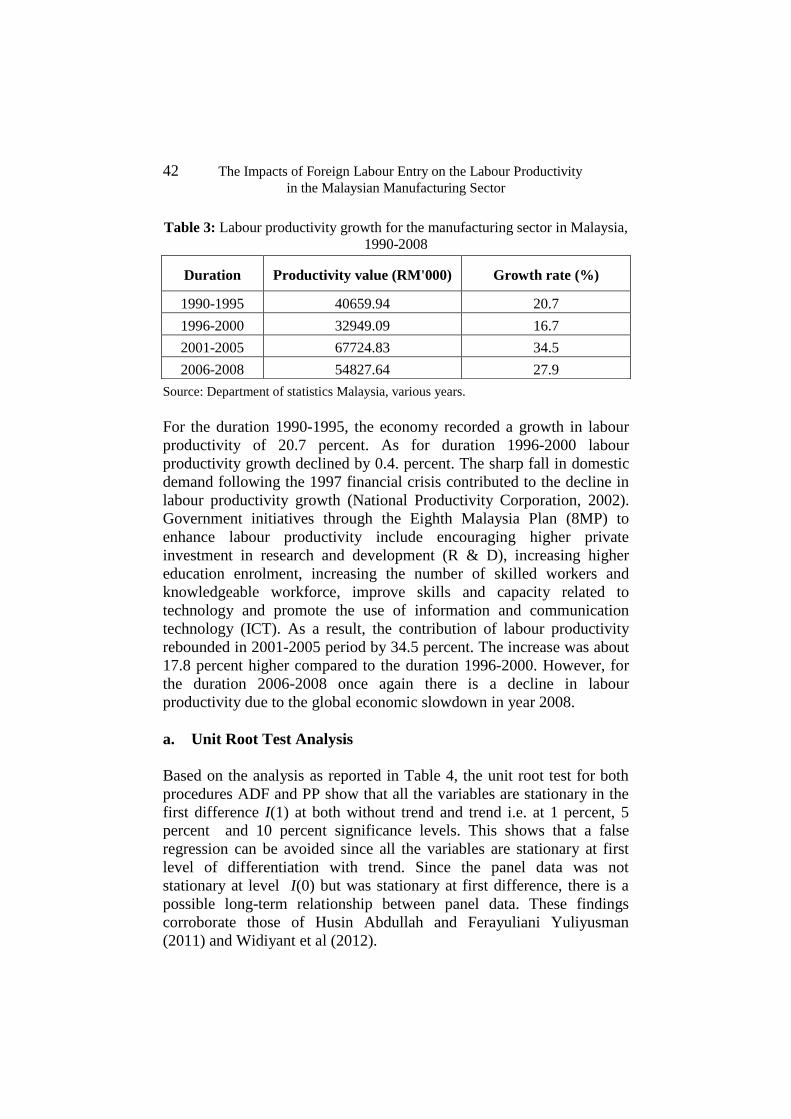

The Impacts of Foreign Labour Entry on the Labour Productivity in the Malaysian Manufacturing Sector

The Real Effect of Government Debt: Evidence from the Malaysian Economy

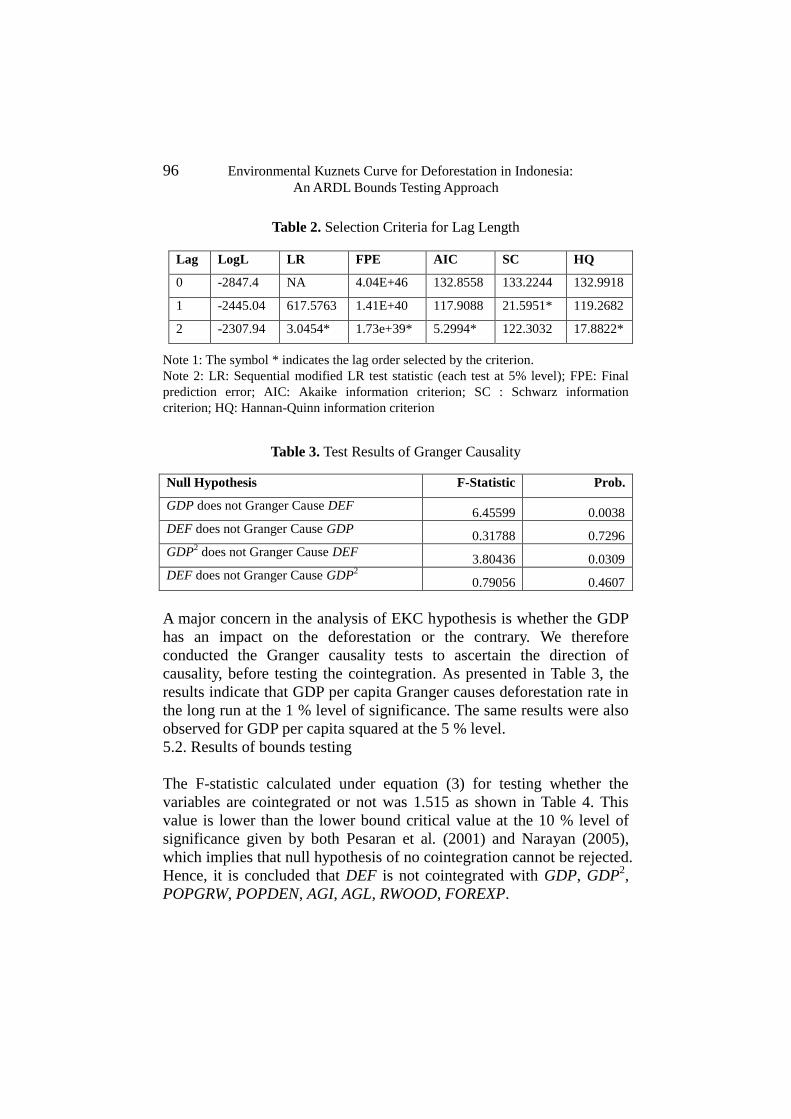

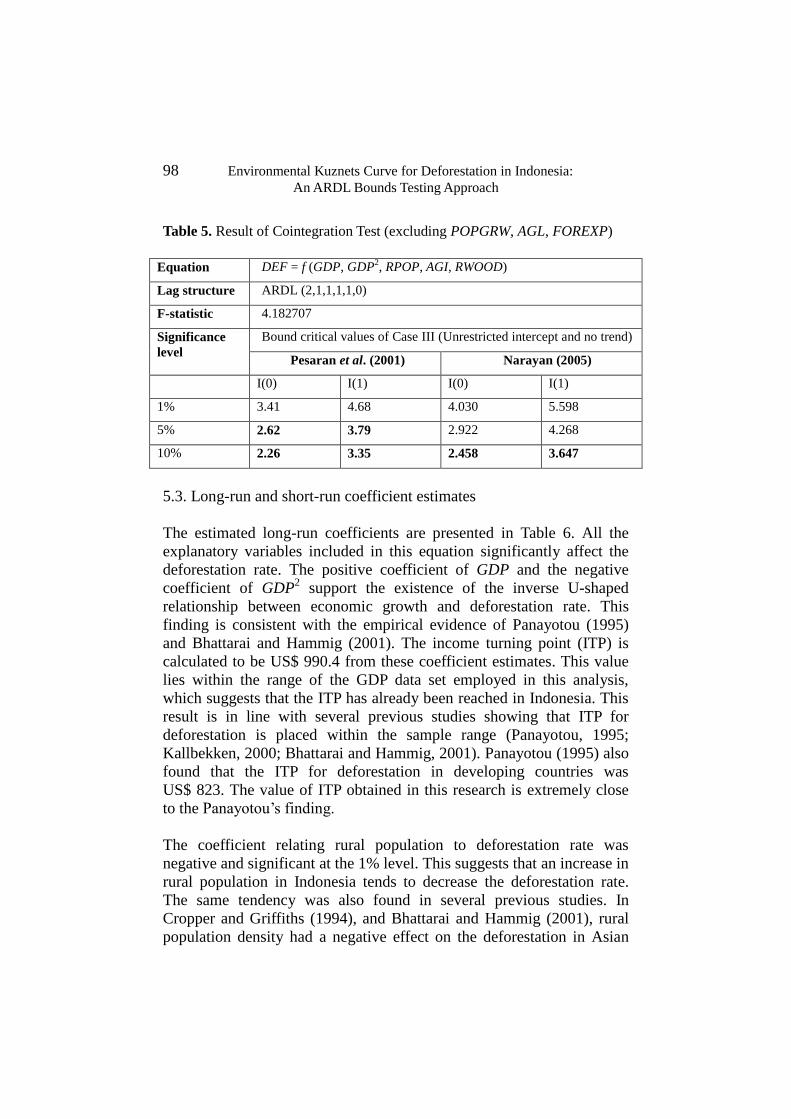

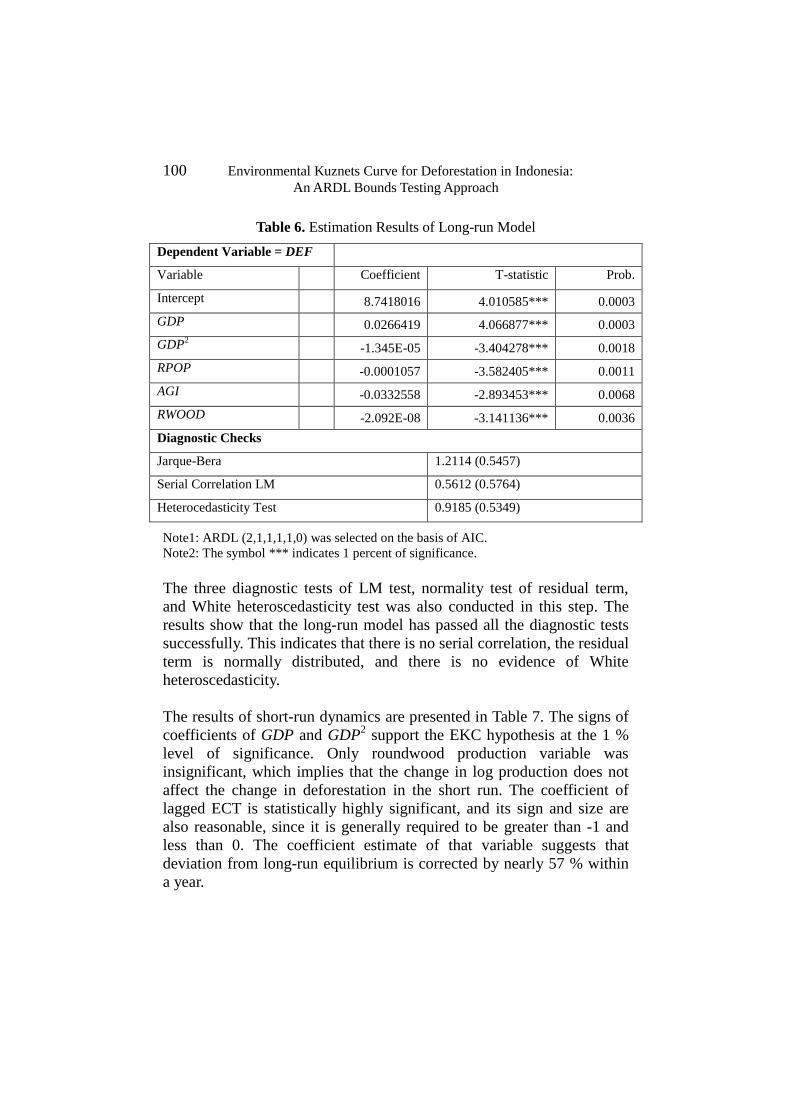

Environmental Kuznets Curve for Deforestation in Indonesia: An ARDL Bounds Testing Approach

Determination of the Degree of Development and the Impact of the Information Environment on the Formation of A System of Social Control in Procurement Under the Russian Contract System (Method of Content Analysis of Information Resources on the Internet)

Bilateral Trade through Official Channel between India and Bangladesh: An Analysis with the Use of Time Series Forecasting Models

Ahmed Nawaz Hakro and Abdallah Mohammed Omezzine

Nur Sabrina Mohd Palel, Rahmah Ismail and Abdul Hair Awang

Siti Nurazira Mohd Daud

Efendi Agus Waluyo and Taku Terawaki

N.A. Mamedova and A.N. Baykova

Muhammad Mahboob Ali and Anita Medhekar

CMYK

CMYK

STATISTICAL, ECONOMIC AND SOCIAL RESEARCHAND TRAINING CENTRE FOR ISLAMIC COUNTRIES

Kudüs Cad. No:9 Diplomatik Site 06450 ORAN-Ankara, TurkeyTel: (90-312) 468 61 72-76 Fax: (90-312) 468 57 26

Email: [email protected] Web: www.sesric.org

STATISTICAL, ECONOMIC AND SOCIAL RESEARCHAND TRAINING CENTRE FOR ISLAMIC COUNTRIES

Kudüs Cad. No:9 Diplomatik Site 06450 ORAN-Ankara, TurkeyTel: (90-312) 468 61 72-76 Fax: (90-312) 468 57 26

Email: [email protected] Web: www.sesric.org

ISSN 1308 – 7800 Volume 37, No.3, September 2016

J o u r n a l o f

E c o n o m i c C o o p e r a t i o n

& D e v e l o p m e n t

Statistical Economic and Social Research

and Training Centre for Islamic Countries

(SESRIC)

Contents

Ahmed Nawaz Hakro and Abdallah Mohammed Omezzine

Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman .................................... 1

Nur Sabrina Mohd Palel, Rahmah Ismail and Abdul Hair Awang

The Impacts of Foreign Labour Entry on the Labour Productivity in the

Malaysian Manufacturing Sector ........................................................... 29

Siti Nurazira Mohd Daud

The Real Effect of Government Debt: Evidence from the Malaysian

Economy ................................................................................................. 57

Efendi Agus Waluyo and Taku Terawaki

Environmental Kuznets Curve for Deforestation in Indonesia:

An ARDL Bounds Testing Approach .................................................... 87

N.A. Mamedova and A.N. Baykova

Determination of the Degree of Development and the Impact of the

Information Environment on the Formation of A System of Social

Control in Procurement Under the Russian Contract System (Method of

Content Analysis of Information Resources on the Internet)............... 109

Muhammad Mahboob Ali and Anita Medhekar

Bilateral Trade through Official Channel between India and Bangladesh:

An Analysis with the Use of Time Series Forecasting Models ........... 135

EDITORIAL NOTE

While many developed and developing countries are still suffering the

negative impact of the global economic and financial crisis in terms of

continuous slowdown of economic growth and high unemployment rates,

the development of various sectors at international, regional and national

levels seems to be still struggling.

In this current issue of the Journal of Economic Cooperation and

Development – September 2016, six valuable articles have been selected

that analyse global oil prices, the importance of labour productivity in the

manufacturing sector, the relationship between government debt and

economic growth, deforestation rates, social control in procurement, and

bilateral trade and focus on trends in some Asian countries such as

Bangladesh, India, Indonesia, Malaysia, Oman and Russia.

The first article examines and explores the sharp fluctuations in global oil

prices and their associated impact on global economic imbalances which

have contributed to the renewed debate among the policy makers regarding

the nature and extent of these fluctuations. It also investigates the impact of

oil prices on the small open economy of Oman.

The second article emphasizes that the improvement and strengthening of

labour productivity has become an important approach to accelerate the

growth of the manufacturing sector in Malaysia. It also attempts to analyse

the impacts of the entry of foreign workers on the labour productivity of the

manufacturing sector in Malaysia stressing the fact that the contribution of

foreign labour on labour productivity is smaller compared to the local

labour.

The third article investigates the real effect of government debt on

Malaysia’s economy stating the fact that there is a long-run relationship

between federal government debt and economic growth in Malaysia and

that there is also an evidence of a non-linear relationship between the

federal government debt and economic growth, which suggests the optimal

level of debt that the government should hold.

The fourth article is meant to empirically demonstrate the inverse U-shaped

relationship, which is generally called the environmental Kuznets curve

(EKC), between economic development and deforestation rate in Indonesia.

Results support the long-run inverted-U relationship, which implies that,

while the deforestation rate increases at the initial stage of economic

growth, it declines after a threshold point.

The fifth article is a result of research on the effect of environment on the

development of information system of social control in procurement.

Informatization process of social relations largely determines how certain

trends of social activity will be popular and durable. To determine the

degree of maturity of information content on the theme of social control in

procurement in Russia, the study also used the method of content analysis

of information resources.

The sixth and last article sheds light on bilateral trade between India and

Bangladesh which will be mutually beneficial to both countries and

improve welfare as per trade theory. It also tries to forecast impact of trade

between two countries considering the time period 1991-2014. By engaging

in bilateral trade with India, Bangladeshi producers and suppliers ought to

be concerned about attaining long term sustainability in their business, by

improving quality of the products so that export can be raised in a

competitive manner. This will help to promote and nurture bilateral trade

relations, ensure sustainability of business and mutually benefit both the

countries through free trade agreement.

Amb. Musa KULAKLIKAYA

Editor-in-chief

Journal of Economic Cooperation and Development, 37, 3 (2016), 1-28

Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Ahmed Nawaz Hakro1 and Abdallah Mohammed Omezzine

2

Sharp fluctuations in global oil prices and their associated impact on global

economic imbalances have contributed to the renewed debate among the policy

makers regarding the nature and the extent of these fluctuations. This study is

designed to investigate the impact of oil prices on the small open economy of

Oman. Structural Vector Auto Regressive (SVAR) model has been adopted to

trace the dynamic inter-relationships among the key macroeconomic variables.

Evidence suggests that changes in crude oil prices significantly affect output,

external balances and the monetary and fiscal variables. The external shocks

induced by positive changes in global oil prices likely affect the demand

management policies in the short and long-run. In the long-run, changes in oil

prices determine the output and subsequent fiscal and monetary policy

changes, while in the short-run, fluctuations are contained well through

demand management policies. Continuation of expansionary fiscal and

monetary policies may likely contain the effects of imported inflation.

However, in the long run, over reliance on expansionary policies may less

likely to be a feasible option.

1. Introduction

Oil price shocks have significantly shifted the wealth of nations; induce

huge windfalls and external imbalances for both oil importing and

exporting countries (see, for example, Coudert et. al., 2008). The impact

of shocks and their associated effects on output, consumer prices and on

external balances have been recognized by a number of scholars

(Schneider, 2004; Setser, 2007; Roubini and Setser, 2004; Allsopp,

2006, among others).

1 Associate Professor, University of Nizwa, P.O Box 33, Post Code, 616, Nizwa, Sultanate of

Oman. E-Mail: [email protected] 2 Professor, University of Nizwa, Sultanate of Oman

2 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Theoretically, in fixed exchange rate economies, oil price shocks are

transmitted to exchange rates through terms of trade channel. A typical

positive oil price shock induces the consumer prices of imported and

non-traded goods in domestic economy and appreciates the real

exchange rates. Governments in these situations usually anticipate wage-

price spiral cycles. The inflationary expectations are being countered by

resorting towards expansionary fiscal policy measures, such as, price

subsidies and wage adjustments. Increasing inflationary pressure and

appreciation in real exchange rate are usually the compelling conditions

for turning the real interest rates into negative zone. This complicates

the conduct of fiscal and monetary policies. The use of expansionary

fiscal or monetary policies in these situations turns to be a riskier option

(expansionary fiscal policy at the times when it requires containing the

inflationary expectations, expansionary monetary policy may aggravate

the prices). A fall in oil prices may have a reverse effect such as loss in

government revenues, lower government spending or a situation of

disinflation and a rise in real interest rates. A restrictive monetary policy

could put the growth objective in danger.

The small oil-based open economy of Oman is an interesting case study

in this context. Oman is known as one of the impressive success stories

in the Gulf and in the Arab world, despite possessing relatively smaller

resources as compared to its neighbours. With a consistent high growth,

lower level of inflation and stable external account surpluses, Oman has

achieved a significant progress on the economic front. The economic

growth primarily is driven by its hydrocarbon sector. Nominal GDP is

roughly 80.5 billion of US dollars in 2014. The current account balance

(percentage of GDP) is 10.6 percent with a global rank of 15. Table 1

refers to the average trends in the major macroeconomic variables from

2011-2014. Most economic indicators show impressive trends in last

few years. Real GDP growth is 4.4 percent on average for last four

years. Consumer price index is around 2.25 percent on average. Fiscal

balance is 6.2 percent of GDP and current account balance is around

12.7 percent of GDP on average.

Journal of Economic Cooperation and Development 3

Table 1: Oman’s Economic Performance since 2011-2014

Variable Average

2011-14 2011 2012 2013 2014

Real GDP (annual change, percent)

4.4 4.0 5.7 4.8 3.4

Nominal GDP (billions of US dollars)

57.1 67.7 75.4 77.1 80.5

CPI (year average; percent) 4.0 3.2 2.8 0.3 2.7 Broad Money Growth (annual change; percent)

39.3 36.6 37.2 39.7 43.8

Fiscal Balance (percent of GDP)

6.2 9.4 4.6 8.1 3.0

Government Debt (percent of GDP)

6.8 5.6 6.2 7.3 8.1

Current Account Balance (percent of GDP)

12.7 15.8 13.3 11.9 9.9

Nominal effective exchange rate index (end of the period average)*

101.3 96.5 99.5 103.9 105.3

Sources: International Financial Statistics (IFS), World Development Indicators (WDI)

and Ministry of National Economy (MONE) Sultanate of Oman. Central Bank of

Oman (CBO) Sultanate of Oman

*https://www.quandl.com/#/data/WORLDBANK/OMN_NEER-Oman-Nominal-

Effecive-Exchange-Rate http://mecometer.com/whats/oman/gdp-per-capita-ppp/

Figure 1 indicates that trend in real GDP growth is steep during the last

three decades. The GDP per capita (PPP) of Oman is US$29,800 with a

global rank of 43.

Figure 1: Real Gross Domestic Product of Oman (1980-2010

4 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Figure 2 indicates the growth in GDP per capita since 1980. The trend

shows that GDP per capita is increasing on average at around 9-10

percent. Oman’s exchange rate is pegged with the US dollar and has

long been maintained at 0.35 Omani riyal to 1 US $ from 1975 till 1985

and thereafter, at 0.38 riyals to 1 US $ from 1986, and it remains stable

since long. The officially declared purpose of the peg is to maintain the

price stability in the country, apparently fixed exchange rate regime

which is linked to US interest rates3.

Figure 2: Growth Trend of GDP per Capita since 1980

Year (1980-2010- 31 observations)

However, the global economic trends are changing. In particular, the

changes are frequently occurring in the real value of US dollar and real

oil prices, which have continuously been affecting the business cycles of

both the oil exporting and importing countries as well. In these

circumstances, continuation of fixed or pegged exchange rate policy or

dollar pegging of Omani riyal has widely been questioned. The

continuation of pegging of Omani riyal with dollar may be a suitable

policy option to anchor the exchange rate fluctuations in short run, but at

least it may be a less feasible option in long run. Since the commodity

prices are traded in dollar, it is often noticed when real oil price rises the

real value of dollar declines. The oil exporting economies and their

dollar pegged currencies are usually appreciated in these situations.

3 Central Bank of Oman (CBO) has indicated that there are no plans to drop the peg to

the US dollar; fiscal policy will remain the main tool to curb inflation (Times of Oman,

16 March 2008).

Journal of Economic Cooperation and Development 5

The divergence and deviations in oil and dollar prices are likely to be

persistent in global economic trends in the medium and long run.

Therefore, countries with pegged exchange rates, may likely observe

fluctuations in their currencies in real terms.

It is, therefore, perceived that short run changes in global real oil prices

are likely affecting the domestic economy. These changes have usually

been perceived through terms of trade channel. Changes in tradable

prices are apparently channelled through real exchange rate

appreciation or depreciation, which in turn, affects the real interest rates,

government consumption expenditures and the domestic non-tradable

consumer prices. It indirectly affects the aggregate demand. If the price

shocks remain persistent, Oman economy may likely experience

positive terms of trade with exchange rate appreciation. Generally, the

oil price shock is assumed to pass-through the channels of real exchange

rate, terms trade, commodity prices to fiscal and monetary variables in

second round effects.

Consequently, it is very important to investigate the continuation of

existing policy options and to understand the impact of oil price shocks

on the real exchange rate, output and prices of small open economy of

Oman. This investigation aims to examine the relationship of changes in

oil prices with domestic economic dynamics of Oman. The study is an

attempt to establish the extent of inter-linkages of external and domestic

structural variants and their inter relationships in dynamic model.

Rest of the study is organized as follows, section two reviews the

relevant literature, section three discusses the methodology, while

section four focuses on the model estimation and presentation of results

and section five consists of conclusion and policy recommendations.

2. Literature Review

Coudert, Couharde and Mignon (2008) by compiling recent evidences

on the link between real effective exchange rate (REER) and commodity

terms of trade, establish the long run elasticity between the two, which is

6 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

around 0.5 on average4. Korhonen and Jurikkala (2007) reveal that the

price of oil has a significant and positive effect on real exchange rates

for OPEC and three oil producing commonwealth of independent states.

Habib and Kalamova (2007) in a study on Russia, Norway, and Saudi

Arabia indicate a long run relationship between real oil price and real

exchange rate but only for Russia.

Besides the oil price shocks, foreign output shocks also play an

important role in business cycle fluctuations in most developing

counties. In this context (Mendoza, 1995; Kose, 2002; and Kim et. al.,

2005) conclude that most of the business cycle fluctuations in aggregate

output are largely explained by external shocks. Hoffmaister and Roldos

(1997) and Ahmed and Loungani (1999) conclude that external output

and oil price shocks play an important role in business cyclical

fluctuations in developing countries. Hahn (2003) results suggest that

the size and the speed of the pass through in Euro zone area appear to be

robust over the time under different identification schemes. Similar

work of McCarthy (2000) indicates that exchange rates have modest

effects on domestic price inflation while import prices have stronger

effects. Pass-through is larger and has a prominent role in the inflation

process in countries with a larger import share and more persistent

exchange rates. Bems and Filho (2009) discover strong links between

real exchange rates and the terms of trade but with limited explanatory

power, while current account variable fits in the data well for oil

exporting countries. Authors use the price related methodologies

suggested by (Bayoumi, Tamim et. al., 1994; Williamson, 1994; Isard

and Faruqee, 1998; Abiad et. al., 2009). Bahamani-Oskooee and Kutan

(2008) examine the impact of exchange rate devaluation and

depreciation on output in context of nine emerging economies of the

Eastern Europe. They explain that economies which are relatively small

and heavily open depend on export revenues to promote their economic

growth, exchange rate devaluations affect their economic growth

negatively. Ito and Sato (2006), on East Asian countries after financial

crises, suggest that exchange rate depreciation results in higher rates of

inflation, especially in Indonesia. These studies establish the channels

4The evidences are based on the studies (Amano and Van Norden, 1995; Chen and

Rogoff, 2003; MacDonald and Ricci, 2001; Cashin et. al., 2004; Ricci et. al., 2008) .

Journal of Economic Cooperation and Development 7

and pass through links between the global oil price and external shocks

with the domestic macroeconomic dynamics of stated economies.

A number of other studies which determine the global oil price shocks

related to Middle East and North African (MENA) region countries are

also conducted. Hirata, Kim and Kose (2004) recognize a substantial

fraction of cyclical fluctuations for MENA region countries. They find

that 60 per cent of variation in aggregate output, domestic productivity

shocks explain close to 40 per cent of business cycle variation in

aggregate output for the region. Spending shocks and world interest rate

shocks are important in accounting for the volatility of business cycles

in certain macroeconomic variables. Makdisi, Fattah and Limon (2006)

suggest that MENA economies are quite vulnerable to exogenous shocks

associated with the terms of trade fluctuations, as these economes are

heavily dependent on export revenues of their primary products. Shahin

and El-Achkar (2010) study the impact of exchange rate policies on

price stability in eighteen MENA region countries from 1975-2005.

They find exchange rates along with monetary variables such as money

growth and lag inflation are the contributing variables to lower

inflation5. Bhattacharya (2003) study concludes that a lack of evidence

to account for the impact of exchange rates on real wage and relative

price flexibility and the difficulty in finding the substitute for exchange

rates as a nominal anchor. Jbili and Kramarenko (2003) in their analysis

clarify those different results that suggest the choice of exchange rates

for Lebanon and Jordan. Ghosh, Gulde, Ostry and Wolf (1997) state the

relationship between the nature of exchange rate regime inflation and

economic growth. The results indicate that inflation is lower and stable

under pegged exchange rate arrangements than in floating regimes.

Money and output growth are highly significant, whereas the interest

rate term is very insignificant. Clarida, Richard, Gali, Jordi, Gertler and

Mark (1999) investigate the terms of trade impact on exchange rate for

commodity and oil exporters’ case and reveal that real exchange rates

co-move with commodity prices in the long run and the response to oil

5 The authors find no significant link between exchange rate regime and inflation of

any peg periods for industrialized countries.

8 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

prices is somewhat lower than the commodity prices6. Coudert,

Couharde and Mignon (2008) estimate a long term relationship between

real effective exchange rate and economic fundamentals. Their results

demonstrate that real exchange rates co-move with commodity prices in

the long run and respond to oil prices somewhat less than the

commodity prices. Hakro and Omezzine (2010) also measure the global

food and oil price shocks and consequent macroeconomic implications

for Oman economy. They discover that external oil and food price

shocks significantly affect real exchange rate, consumer price index and

other macroeconomic variables of Oman economy.

Edward (1989) widely quoted study raises the crucial question about the

nature of link between the fluctuation in the exchange rate with the

output in short run or long run. By using 12 developing countries data,

the study regresses the real GDP on nominal and real exchange rate

along with other macroeconomic variables. He finds mixed evidence

which indicates that initial contractionary effects could be reversed after

some time. Agenor (1991) in a similar study on 24 developing countries

reveals surprisingly that real exchange rate depreciation actually boosts

output growth while depreciation of real exchange rate has, in fact, a

very constructive effect. Morley (1995) on 28 developing countries

notes that depreciations in the real exchange rate value at level reduce

output over a period of two years. Gala and Lucinda (2006) argue that

the productivity differential may have an important role on the impact of

real exchange levels on per capita real income growth rates. These

results show that 10 percent real exchange rate devaluation given

everything else being constant average growth rates could be higher by

0.122 per cent. Rodrik (2008) suggests that undervaluation (a high real

exchange rate) estimates result in economic growth. This may be the

case particularly in developing countries where tradable goods suffer

disproportionately from the distortions that keep poor countries from

converging. However, Kamin and Klau (1998) estimate the impact of

devaluation on 27 countries and find no evidence of contractionary

impact in the long run, contradicting the conventional view that

devaluations are expansionary.

6 Aizenman and Chrichton (2006) evaluate the impact of international reserves, terms

of trade shocks and the capital flows on the real exchange rate (REER). The major

effect is on the Asian and oil exporting countries.

Journal of Economic Cooperation and Development 9

Apart from the above studies, a large number of other set of studies

conducted, support the proposition that exchange rate shocks lead to

negative effect on output, Particularly for Latin American countries (for

example; Rogers and Wang, 1995; Santaella and Vela, 1996; Copelman

and Warner, 1995; and Kamin and Rogers, 2000; Rodriquez and Diaz,

1995). similar results are found for Peru, and in Hoffmaist and Vesh

(1996) for Uruguay. There is hardly any study which suggests high

depreciation combined with high level of output and high appreciation

of exchange rate with high level of depressed output (Kamin and

Rogers, 2000).

Most of the studies have used the Vector Auto Regression (VAR)

mechanism to find the inter-relationship between exchange rates with

output and prices in different countries contexts. Case studies such as

Ndung’u (1993, 1997), by estimating a six variable VAR on the data set

of Kenya, discover the link between the rate of inflation and exchange

rate explaining each other. Montiel (1989) by using VAR model for

Argentina, Brazil and Israel observes that exchange rate movements

explain inflation. Dornbush et. al. (1990) find that real exchange rate is

an important source of inflation in Argentina, Brazil, Peru, and Mexico

but not in Bolivia. Inflation seems to be inertial with regard to exchange

rate and is being determined through demand shocks. Exchange rate and

inflation are also studied in several other countries context (see e.g.,

Kamin, 1996; Odedokum, 1997; London, 1989; Cannetti and Greene,

1991; Calvo et. al., 1995; Elbadawi, 1990).

The available evidence is quite rich in its content and methodological

rigorousness. It addresses and formulates the impact and channels

through which the oil price induces the changes in domestic dynamics.

To the best of authors’ knowledge, hardly any significant attempt has

ever been made towards the understanding of these channels in the

context of small open economy of Oman. This study fills the gap.

3. Methodology

Structural Vector Auto Regression (SVAR) model is considered a very

useful approach to find the link between the oil price shocks and the

domestic economy. The SVAR has a number of advantages. It identifies

the structural shocks through innovations with identifiable restrictions

10 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

and thereafter, generalizes the impact through impulse response

functions and variance decompositions, capable to trace out individual

shocks and variances on each variable. The study considers the SVAR

model initially with 6-7 variables based on theoretical relationship

among the set of variables in a VAR system. The choices of variables

are based on the procedure adopted to incorporate the vector of

endogenous variables used by (McCarthy, 2000; and Hahn, 2003).

Supply shocks are identified and derived from changes in global oil

prices and through changes in external balances. The demand side

effects traced in changes in real output growth, changes in government

consumption expenditures. Interest rate, international prices, real

effective exchange rate, money supply and interest rate variables are

used to allow the effects of monetary policy and fiscal policy responses

on inflation and output. Real effective exchange rate is used primarily to

avoid bilateral exchange rate vis-à-vis the US dollar. This will give us a

leverage to measure the extent to which the country’s trade dependence

with other countries. The use of this variable shall provide the real

currency appreciation or depreciation or a gain or loss in the price

competitiveness. It also provides the extent to which the country is

facing the inflationary pressure through imports. CPI is used for

domestic inflation.

The structural model is identified by imposing zero restrictions on the

number of endogenous variables based on the theoretical relationship of

the endogenous variables. The changes in oil prices are ordered first

because the oil price variable is likely to affect all the other variables in

the system. Real output gap is placed second and the interest rate and

money supply (M2) is ordered fourth. The use of money supply in place

of interest rate turns out to be a better choice. It is more reasonable to

measure monetary policy shocks to contemporaneous effects after

exchange rate variants or pass through on monetary variables reflected

after changes in oil and output variables. The policy reaction function is

assumed to flow from the changes in oil prices to GDP gap,

subsequently affects the monetary and fiscal variables. Real effective

exchange rate variable is placed ahead of government consumption

expenditures and domestic prices. This implies that the real effective

exchange rate responds contemporaneously to supply and demand

management policies of the government towards containing the effects

of the shocks.

Journal of Economic Cooperation and Development 11

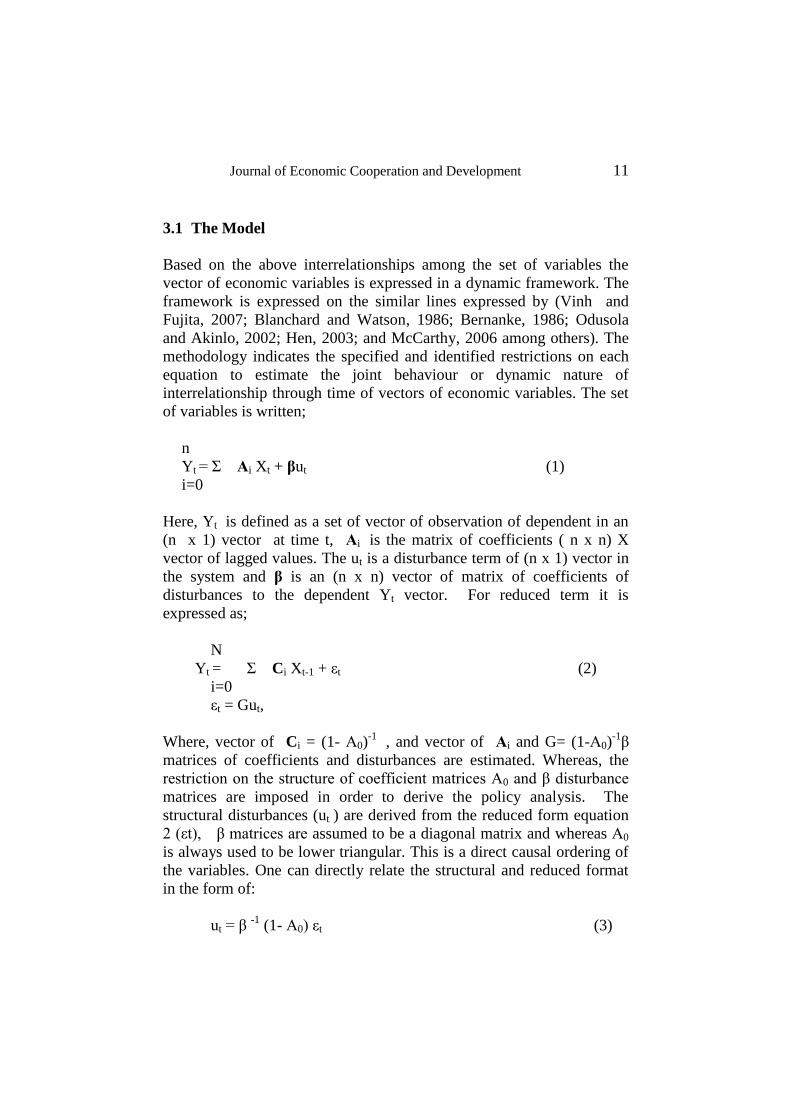

3.1 The Model

Based on the above interrelationships among the set of variables the

vector of economic variables is expressed in a dynamic framework. The

framework is expressed on the similar lines expressed by (Vinh and

Fujita, 2007; Blanchard and Watson, 1986; Bernanke, 1986; Odusola

and Akinlo, 2002; Hen, 2003; and McCarthy, 2006 among others). The

methodology indicates the specified and identified restrictions on each

equation to estimate the joint behaviour or dynamic nature of

interrelationship through time of vectors of economic variables. The set

of variables is written;

n

Yt = Σ Аi Xt + βut (1)

i=0

Here, Yt is defined as a set of vector of observation of dependent in an

(n x 1) vector at time t, Аi is the matrix of coefficients ( n x n) X

vector of lagged values. The ut is a disturbance term of (n x 1) vector in

the system and β is an (n x n) vector of matrix of coefficients of

disturbances to the dependent Yt vector. For reduced term it is

expressed as;

N

Yt = Σ Ci Xt-1 + εt (2)

i=0

εt = Gut,

Where, vector of Ci = (1- А0)-1

, and vector of Аi and G= (1-А0)-1

β

matrices of coefficients and disturbances are estimated. Whereas, the

restriction on the structure of coefficient matrices А0 and β disturbance

matrices are imposed in order to derive the policy analysis. The

structural disturbances (ut ) are derived from the reduced form equation

2 (εt), β matrices are assumed to be a diagonal matrix and whereas А0

is always used to be lower triangular. This is a direct causal ordering of

the variables. One can directly relate the structural and reduced format

in the form of:

ut = β -1

(1- А0) εt (3)

12 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

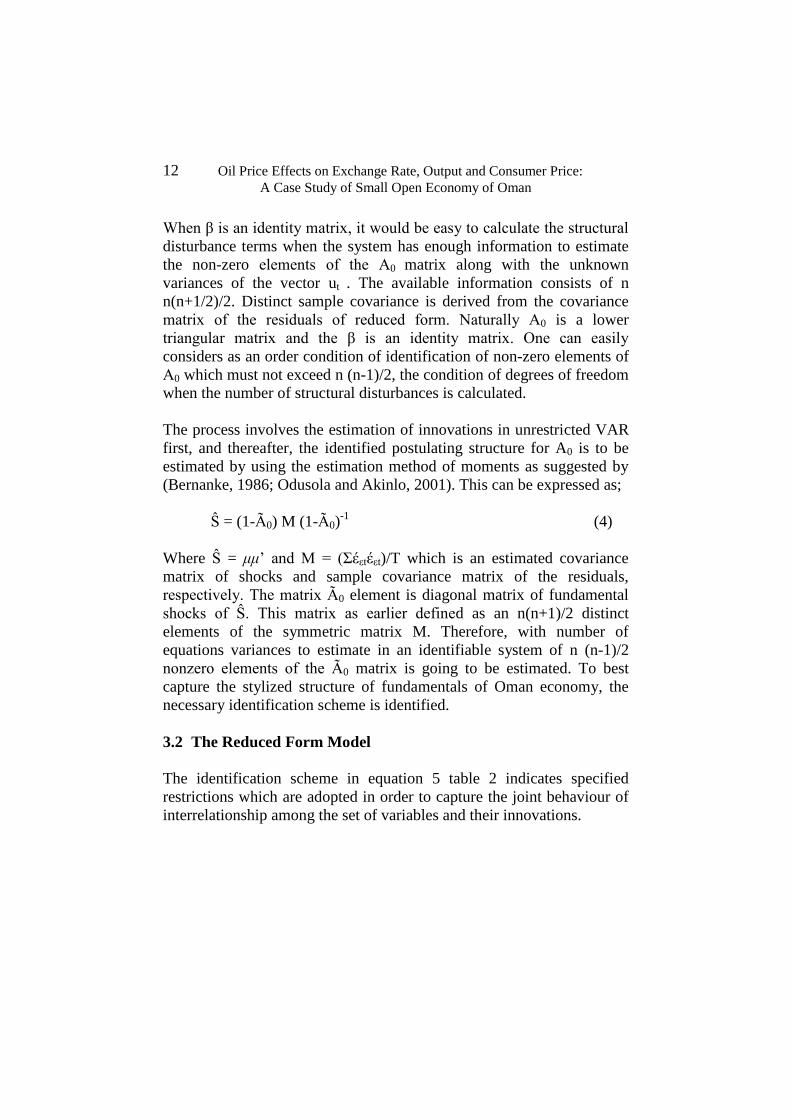

When β is an identity matrix, it would be easy to calculate the structural

disturbance terms when the system has enough information to estimate

the non-zero elements of the А0 matrix along with the unknown

variances of the vector ut . The available information consists of n

n(n+1/2)/2. Distinct sample covariance is derived from the covariance

matrix of the residuals of reduced form. Naturally А0 is a lower

triangular matrix and the β is an identity matrix. One can easily

considers as an order condition of identification of non-zero elements of

А0 which must not exceed n (n-1)/2, the condition of degrees of freedom

when the number of structural disturbances is calculated.

The process involves the estimation of innovations in unrestricted VAR

first, and thereafter, the identified postulating structure for A0 is to be

estimated by using the estimation method of moments as suggested by

(Bernanke, 1986; Odusola and Akinlo, 2001). This can be expressed as;

Ŝ = (1-Ã0) M (1-Ã0)-1

(4)

Where Ŝ = μμ’ and M = (Σέεtέεt)/T which is an estimated covariance

matrix of shocks and sample covariance matrix of the residuals,

respectively. The matrix Ã0 element is diagonal matrix of fundamental

shocks of Ŝ. This matrix as earlier defined as an n(n+1)/2 distinct

elements of the symmetric matrix M. Therefore, with number of

equations variances to estimate in an identifiable system of n (n-1)/2

nonzero elements of the Ã0 matrix is going to be estimated. To best

capture the stylized structure of fundamentals of Oman economy, the

necessary identification scheme is identified.

3.2 The Reduced Form Model

The identification scheme in equation 5 table 2 indicates specified

restrictions which are adopted in order to capture the joint behaviour of

interrelationship among the set of variables and their innovations.

Journal of Economic Cooperation and Development 13

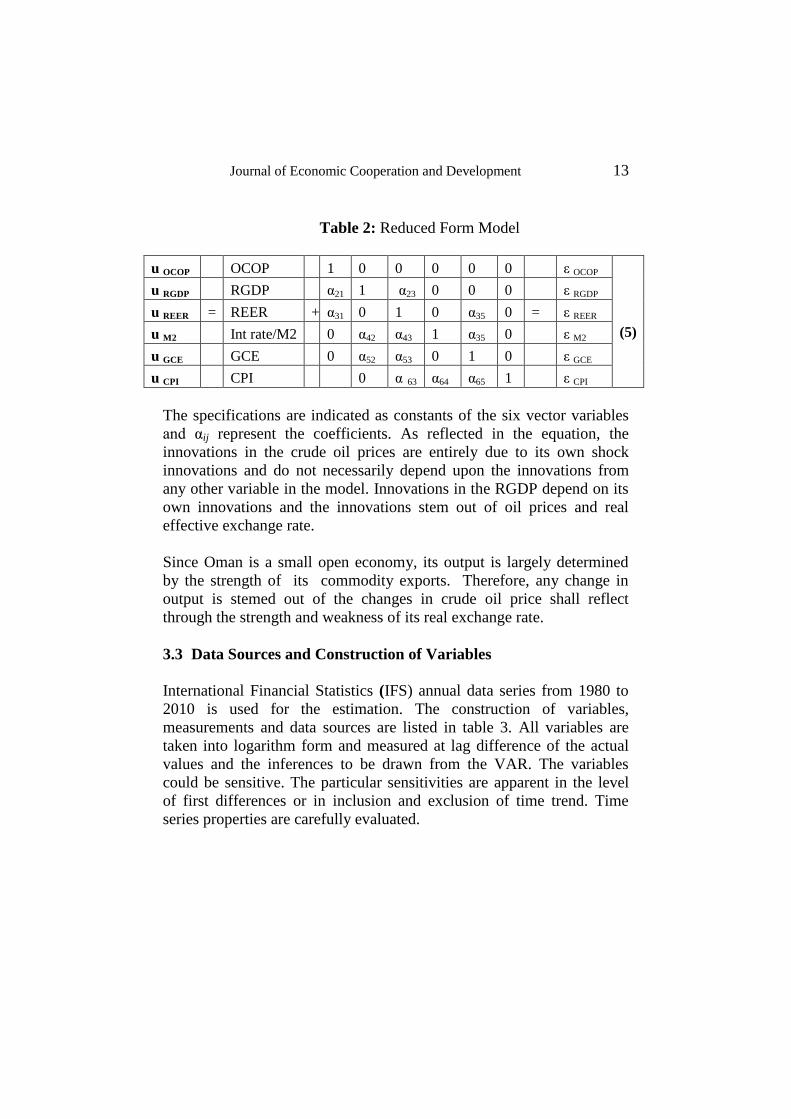

Table 2: Reduced Form Model

u OCOP OCOP 1 0 0 0 0 0 ε OCOP

(5)

u RGDP RGDP α21 1 α23 0 0 0 ε RGDP

u REER = REER + α31 0 1 0 α35 0 = ε REER

u M2 Int rate/M2 0 α42 α43 1 α35 0 ε M2

u GCE GCE 0 α52 α53 0 1 0 ε GCE

u CPI CPI 0 α 63 α64 α65 1 ε CPI

The specifications are indicated as constants of the six vector variables

and αij represent the coefficients. As reflected in the equation, the

innovations in the crude oil prices are entirely due to its own shock

innovations and do not necessarily depend upon the innovations from

any other variable in the model. Innovations in the RGDP depend on its

own innovations and the innovations stem out of oil prices and real

effective exchange rate.

Since Oman is a small open economy, its output is largely determined

by the strength of its commodity exports. Therefore, any change in

output is stemed out of the changes in crude oil price shall reflect

through the strength and weakness of its real exchange rate.

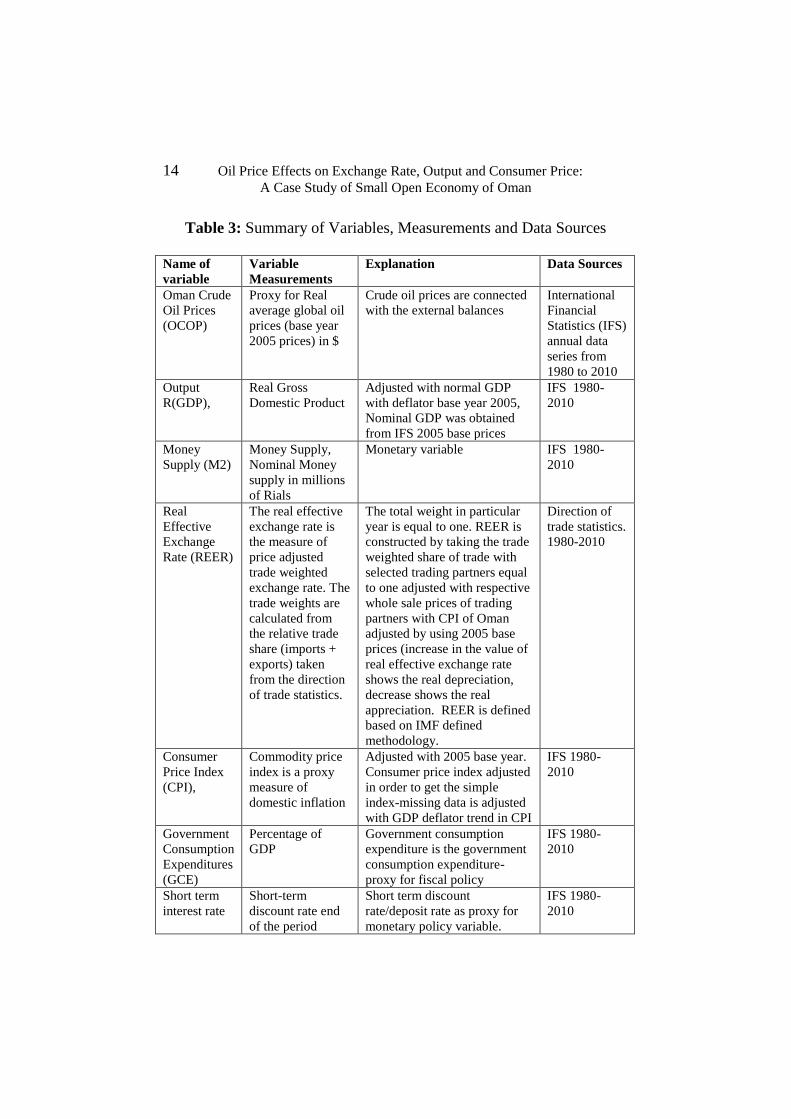

3.3 Data Sources and Construction of Variables

International Financial Statistics (IFS) annual data series from 1980 to

2010 is used for the estimation. The construction of variables,

measurements and data sources are listed in table 3. All variables are

taken into logarithm form and measured at lag difference of the actual

values and the inferences to be drawn from the VAR. The variables

could be sensitive. The particular sensitivities are apparent in the level

of first differences or in inclusion and exclusion of time trend. Time

series properties are carefully evaluated.

14 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Table 3: Summary of Variables, Measurements and Data Sources

Name of

variable

Variable

Measurements

Explanation Data Sources

Oman Crude

Oil Prices

(OCOP)

Proxy for Real

average global oil

prices (base year

2005 prices) in $

Crude oil prices are connected

with the external balances

International

Financial

Statistics (IFS)

annual data

series from

1980 to 2010

Output

R(GDP),

Real Gross

Domestic Product

Adjusted with normal GDP

with deflator base year 2005,

Nominal GDP was obtained

from IFS 2005 base prices

IFS 1980-

2010

Money

Supply (M2)

Money Supply,

Nominal Money

supply in millions

of Rials

Monetary variable IFS 1980-

2010

Real

Effective

Exchange

Rate (REER)

The real effective

exchange rate is

the measure of

price adjusted

trade weighted

exchange rate. The

trade weights are

calculated from

the relative trade

share (imports +

exports) taken

from the direction

of trade statistics.

The total weight in particular

year is equal to one. REER is

constructed by taking the trade

weighted share of trade with

selected trading partners equal

to one adjusted with respective

whole sale prices of trading

partners with CPI of Oman

adjusted by using 2005 base

prices (increase in the value of

real effective exchange rate

shows the real depreciation,

decrease shows the real

appreciation. REER is defined

based on IMF defined

methodology.

Direction of

trade statistics.

1980-2010

Consumer

Price Index

(CPI),

Commodity price

index is a proxy

measure of

domestic inflation

Adjusted with 2005 base year.

Consumer price index adjusted

in order to get the simple

index-missing data is adjusted

with GDP deflator trend in CPI

IFS 1980-

2010

Government

Consumption

Expenditures

(GCE)

Percentage of

GDP

Government consumption

expenditure is the government

consumption expenditure-

proxy for fiscal policy

IFS 1980-

2010

Short term

interest rate

Short-term

discount rate end

of the period

Short term discount

rate/deposit rate as proxy for

monetary policy variable.

IFS 1980-

2010

Journal of Economic Cooperation and Development 15

4. Estimation and Result Discussion

Augmented Dickey Fuller (ADF) and Philips- Perron (PP) tests at level

and first difference are conducted. The first differencing variables are

integrated at different orders. Variables such as Real Gross Domestic

Product (RGDP), Government Consumption Expenditures (GCE) and

Consumer Price Index (CPI) variables are adjusted as rates of change

rather levels. Other variables such as Average Oman Crude Oil Price

(OCOP), Money Supply (M2) and Real Effective Exchange Rate

(REER) are used as level. Since the data series are in annual form, no

seasonal trend is observed and this has been verified and checked. Serial

correlation test is performed by using Lagrange Multiplier (LM)

statistics to check the robustness of ADF tests. Lag lengths are

determined by using Akaike Information Criterion (AIC).

The VAR model is estimated with log differences of six variables by

using yearly data with two lags in each equation. The two year lag

period is estimated over the period 1980-20107. Most of the variables

are found to be cointegarated. Therefore, the Vector Error Correction

model is used. The model allows the long term behaviour of the set of

endogenous variables to converge and cointegrating the long term

equilibrium relationship along with their short term dynamics. The

cointegration relationship is tested by using Johansen Cointegration Test

(1995). Four co-integrating vectors linking each other are found.

Cointegrating vectors are tested based on the trace and max-eigen

statistics. The cointegration relationship among the variables is

presented in the panel of table 4.

7 Charemza and Deadman (1992) suggest use of cointegrating vector for REER

variable, when it is used in long series, in short series, the variable may turns out to be

inconsistent in theoretical terms.

16 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Table 4: Summary of the Reduced Form Estimation

The coefficient signs indicate the adjustments to the long run deviations.

Unlike the oil prices, the domestic prices are adjusted from a long run

path in a relatively longer time period than the adjustment in

goveronment expenditure which is relatively quick to adjust from its

deviations. The adjustment coefficient corresponds -0.04 per cent for

exchange rate, while for government consumption expenditure

coefficient is -0.288 and for real output, it is -0.171. Coefficients

suggest that government expenditure is relatively quick to adjust to the

equilibrium path, as compared to real output and real oil prices.

However, the real output responds to the external shocks relatively

slower than the response to government consumption expenditure. The

adjustment process indicates that output is positively responding to the

external shocks. Relatively slow adjustment in real oil prices and

domestic prices to equilibrium path indicate the long run relationship

among the two variables. Oman economy is a small economy, its

exportable share of commodities volume is very small compared to the

world demand. It seems less likely that oil prices of Oman crude affects

the global oil prices.

4.1 The Structural Model and Impulse Response Functions

The SVAR model suggested with structural restrictions in equation 5

and table 2 is estimated by using the VEC model. The results are

presented in the table 5. Structural response function of SVAR in a form

of coefficients in table 5 and Figure 3 indicates the generalized impulse

response functions.

Test statistics Average

Crude

Price of

Oil

RGDP Money

Supply

M2

REER Govt.

Cons Exp.

CPI

Co integration

equation

-0.04

(-0.34)

-0.171

(-2.45)

0.613

(2.66)

5.796

(3.30)

-0.288

(-2.34)

-0.005

(-0.06)

Goodness of fit statistics

Adjusted R2 0.46 0.21 0.52 0.51 0.64 0.18

SEE 0.02 0.00 0.08 4.77 0.02 0.01

Journal of Economic Cooperation and Development 17

Table 5: Structural VAR Regression Impulse Response Function of

SVAR ε OCOP = 0.05μ COP

(7.4)***

6.1

ε RGDP = 0.38 OCOP

(4.14)***

6.2

ε REER = 0.09 OCOP

(0.02)

4.50GCE 6.3

(0.47)

ε M2 = -2.67RGDP

(7.88)***

-0.02REER

(2.09)**

-0.25GCE 6.4

(2.1)**

ε GCE = +1.89RGDP

(3.85)***

-0.04REER

(1.51)

6.5

ε CPI = -1.34RGDP

(-3.13)***

-0.002REER

(0.88)

-0.32M2 6.6

(-2.4)***

The coefficients in table 5 are structural impulse response functions of

SVAR. These coefficients are driven from the vector error correction

and cointegrated series with structural restrictions. These coefficients

may not appear to be very precise. This may be possible because of the

estimation techniques and the nature of standard errors as cautioned by

(Bernanke, 1986; Calomiris and Hubbard, 1989, Turner, 199; Kiguel,

Lizondo and O’Connell, 1997).

4.2 Discussion

The results suggest that innovations in crude oil prices positively affect

the real output innovations (refer equation 6.1 in table 5). One

percentage point variation in real crude oil prices significantly impact

the real output by 0.38 per cent in the same direction. This means every

10 per cent increase in oil prices positively influence the real output by

3.8 per cent in long run. The innovations in real output also significantly

impact the changes in the money supply. However, these changes are

inconsistent with changes in real output growth. In the long run, shocks

in both real output and money supply become smooth. Changes in

output are primarily driven by changes in oil prices, whereas the

changes in output induce increase in money supply.

18 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Figure 3: Response to Generalized One S.D Innovations to 2S.E

Journal of Economic Cooperation and Development 19

One percentage point increase in real Oman crude oil prices affects the

real exchange rate by 0.09 per cent, but this effect is statistically very

insignificant. This suggests that changes in global oil prices, in fact, do

affect the real exchange rate, but that effect is a very minor. Innovations

in real effective exchange rate affect the government consumption

expenditures positively but insignificantly. This result is consistent with

the trends in government consumption expenditures which are usually

increasing at the time of positive external balances. Innovations in real

exchange rates are having a negative and negligible impact on money

supply expansion. Changes in real output negatively affect the money

supply and it is quite clear that real output growth induces by the

external trade revenues but the output is not influenced by the changes

in domestic money supply. Innovations in real output infuence the

government consumption expenditures significantly and positively. One

percentage point increase in real output increases the government

consumption expenditure by 1.89 per cent. Innovations in output growth

affect the fiscal side of government consumption expenditure positively

and significantly. Real appreciation in exchange rate has a negligible

effect on prices. It means that real appreciation of exchange rate effect

on domestic prices is nominal. Because the domestic prices are not

much affected by appreciation or depreciation in real exchange rate. In

figure 3 response to generalized one standard deviation innovations to

two standard errors suggest consistency with the structural coefficients

in table 5. The results suggest negative response of external balances to

a real effective exchange rate. While real effective exchange rate has a

positive effect on real interest rate.

Pegged exchange rate policy seems to be performing well in anchoring

the inflationary expectation in Oman.. However, the changes in real

output significantly affect the prices negatively. Monetary expansion has

a negative effect on domestic prices. This also suggests that

expansionary monetary policy traces the pace of output and balances the

inflationary expectations. Oman has relatively stable prices in last few

decades. Every one per cent increases in money supply adjust the pace

of inflationary expectations by 0.32 per cent. Increase in output is

accompanied by decline in prices. This suggests that stabilization

policies works well with a mixture of expansion in output growth

coupled with monetary expansion accommodating the price changes.

20 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

The results are in line with the established theoretical propositions and

the evidence discussed earlier. The innovations in real effective

exchange rate not necessarily affect the consumer prices. However,

innovations to real output affect prices negatively. The relationship of

output innovations with government consumption expenditure positively

affect output which leads to an expansionary fiscal policy.

5. Conclusion

The study has examined the relationship of real oil prices shocks and its

channels to domestic macroeconomic dynamics of small open economy

of Oman. It has established the extent of interlinks of external and

domestic structural variants and their inter relationships. The dynamic

structural vector autoregressive econometric model along with stylized

structural variants of Oman economy has shed lights on the

interrelationship of macro variables and trace out their dynamic

moments. The results are consistent with the theory and provide the

important insights into the policy directions.

The results imply that crude oil price emerges to be a very significant

variable inducing output extends the monetary and government

consumption expenditures. In other words, changes in oil prices induce

output and consequent response to fiscal and monetary policy responses.

Monetary and fiscal policies anchor the global price shock and the long

run inflationary pressures. Monetary variables such as money supply

responses to changes in output and affects prices. The changes in

exchange rate are presumably positive shock to terms of trade or

external favourable effect. Results from impulse response functions

imply that innovation in output is influenced by oil prices. Exchange

rate, in fact, do appreciates due to increase in oil prices; the response to

fiscal expansion is derived out of changes in oil prices which is

straightforward theoretical result. Structural impulse response

coefficients indicate consistency with the earlier results.

Output and demand management policies in Oman economy are largely

dependent on the external factors, particularly oil prices. The shocks to

oil prices may likely affect the demand management policies. It seems in

the long run changes in oil prices determine the output and subsequent

fiscal and monetary policies which serve well to contain the inflationary

Journal of Economic Cooperation and Development 21

expectations and maintain positive external balances. In short run

fluctuations in oil prices or global imbalances though are contained well

in mixture of stabilization policies, continuation of a mixture of fiscal

and monetary stabilization policies may serve well the purpose of the

domestic dynamics of Oman economy. However, in the long run, over

reliance on stabilization policies in days of global imbalances may

provide fewer options to contain the external shocks. Therefore, the

exchange rate policy of pegging with dollar may be questionable in the

longer term.

22 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

References:

Abiad, A. G., Balakrishnan, R., Koeva Brooks, P., Leigh, D., & Tytell, I.

(2009), "What’s the damage? Medium-term output dynamics after

banking crises". IMF working papers, 1-37.

Agénor, P. R. (1991), "Output, devaluation and the real exchange rate in

developing countries". Weltwirtschaftliches Archiv, 127(1), 18-41.

Ahmed, S., & Loungani, P. (1999), Business cycles in emerging market

economies. Manuscript, IMF and Board of Governors of the Fed.

Aizenman, J., & Riera-Crichton, D. (2008), "Real exchange rate and

international reserves in an era of growing financial and trade

integration," The Review of Economics and Statistics, 90(4), 812-815.

Allsopp, C. (2006), "Why is the Macroeconomic Impact of Oil Prices

Different this Time?," In Oxford Energy Forum (Vol. 66, p. 20). The

Oxford Institute for Energy Studies.

Amano, R. A., & Van Norden, S. (1995), "Terms of trade and real

exchange rates: the Canadian evidence" Journal of International Money

and Finance, 14(1), 83-104.

Bayoumi, T., & Symansky, S (1994), The Robustness of Equilibrium

Exchange Rate Calculations to Alternative Assumptions and

Methodologies, (eds) John Williamson, equilibrium exchange rates.

Peterson Institute, 1994,pp. 19–59.

Bahmani-Oskooee, M., & Kutan, A. M. (2008), "Are devaluations

contractionary in emerging economies of Eastern Europe?". Economic

Change and Restructuring, 41(1), 61-74.

Carvalho Filho, I. E., & Bems, R. (2009), "Exchange rate assessments:

methodologies for oil exporting countries", IMF Working Papers, 1-35.

Bhattacharya, R. (2003), "Sources of variation in regional economies,"

The Annals of Regional science, 37(2), 291-302.

Journal of Economic Cooperation and Development 23

Blanchard, O. J., & Watson, M. W. (1986), "Are business cycles all

alike?," In The American business cycle: Continuity and change (pp.

123-180). University of Chicago Press.

Bernanke, B. S. (1986), "Alternative explanations of the money-income

correlation" In Carnegie-Rochester conference series on public policy

(Vol. 25, pp. 49-99). North-Holland.

Calvo, G. A., Reinhart, C. M., & Vegh, C. A. (1995), "Targeting the real

exchange rate: theory and evidence," Journal of Development

Economics, 47(1), 97-133.

Canetti, E. (1991), Monetary growth and exchange rate depreciation as

causes of inflation in African countries: An empirical analysis. (eds)

Centre for Economic Research on Africa Research Monograph Series,

School of Business-Montclair State University, New Jersey.

Cashin, P., Céspedes, L. F., & Sahay, R. (2004), "Commodity currencies

and the real exchange rate," Journal of Development Economics, 75(1),

239-268.

Clarida, Richard., Gali, Jordi., Gertler, Mark (1999), "The Science of

Monetary Policy: A New Keynesian Perspective," Journal of Economic

Literature, 37/ 2 : 1661-1707.

Calomiris, C. W., & Hubbard, R. G. (1989), "Price flexibility, credit

availability, and economic fluctuations: evidence from the United States,

1894-1909," The Quarterly Journal of Economics, 429-452.

Central Bank of Oman (2014), Annual Report 2014, Sultanate of Oman

Charemza, W.W. and Deadman, D.F. (1992), New Directions in

Econometric Practice, Edward Elgar: Aldershot

Chen, Yu-chin. Kenneth, Rogoff. (2003), “Commodity currencies,”

Journal of International Economics, 60/1: 133-160.

24 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Copelman, M., & Werner, A. M. (1995), "The monetary transmission

mechanism in Mexico" (No. 521). Board of Governors of the Federal

Reserve System.

Coudert, V., Couharde, C., & Mignon, V. (2008), "Do terms of trade

drive real exchange rates? Comparing oil and commodity currencies,"

Centre d'Etudes Prospectives et d'Informations Internationales (CEPII),

Paris, 32.

Dornbusch, R., Sturzenegger, F., Wolf, H., Fischer, S., & Barro, R. J.

(1990), "Extreme inflation: dynamics and stabilization," Brookings

Papers on Economic Activity, 1990(2), 1-84.

Edwards, S. (1989), Real Exchange Rates, Devaluation, and

Adjustment: Exchange Rate Policy in Developing Countries,

Cambridge, Mass.: MIT Press

Elbadawi, I. A. (1990), "Inflationary process, stabilization and the role

of public expenditure in Uganda," Washington, DC: World Bank.

Gala, P., & Lucinda, C. R. (2006), "Exchange rate misalignment and

growth: old and new econometric evidence," Revista Economia, 7(4),

165-187.

Ghosh, A. R., Gulde, A. M., Ostry, J. D., & Wolf, H. C. (1997), "Does

the nominal exchange rate regime matter?" (No. w5874). National

Bureau of Economic Research.

Habib, M. M., & Kalamova, M. M. (2007), "Are there oil currencies?

The real exchange rate of oil exporting countries," Working Paper, No.

839, European Central Bank.

Hakro, A. N., & Omezzine, A. M. (2010), "Macroeconomic effects of

oil and food price shocks to the oman economy," Middle Eastern

Finance and Economics, 6(2010), 72-89.

Hirata, H., Kim, S. H., & Kose, M. A. (2004), "Integration and

fluctuations: the case of MENA," Emerging Markets Finance and

Trade, 40(6), 48-67.

Journal of Economic Cooperation and Development 25

Hoffmaister, A. W., & Roldós, J. E. (1997), "Are business cycles

different in Asia and Latin America?"Working Paper No. 97/9,

International Monetary Fund.

Hoffmaister, A. W., & Végh, C. A. (1996), "Disinflation and the

recession-now-versus-recession-later hypothesis: evidence from

Uruguay," Staff Papers-International Monetary Fund, 355-394.

Hahn, E. (2003), "Pass-through of external shocks to euro area

inflation," Working paper, 243, European Central Bank.

Isard, P., & Faruqee, H. (1998), "Exchange rate assessment: extension of

the macroeconomic balance approach" (Vol. 167). International

monetary fund.

Ito, T., & Sato, K. (2006), "Exchange rate changes and inflation in post-

crisis Asian economies: VAR analysis of the exchange rate pass-

through" (No. w12395). National Bureau of Economic Research.

Jbili, A., & Kramarenko, V. (2003), "Choosing exchange regimes in the

Middle East and North Africa," International Monetary Fund

Kamin, S. B., & Klau, M. (1998), "Some multi-country evidence on the

effects of real exchange rates on output," FRB International Finance

Discussion Paper, (611).

Kamin, S. B. (1996), "Real Exchange rates and Inflation in exchange-

Rate based Stabilizations: an empirical examination," International

Finance Discussion Papers, (554).

Kamin, S. B., & Rogers, J. H. (2000), "Output and the real exchange

rate in developing countries: an application to Mexico," Journal of

development economics, 61(1), 85-109.

Kiguel, M. A., Lizondo, J. S., & O'Connell, S. A. (Eds.). (1997),

Parallel Exchange Rates in Developing Countries. St. Martin's Press.

26 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Kim, S. H., & Ahn, H. D. (2005), "Dynamics of open economy business

cycle models: the case of Korea," Korea Development Review, 1(1),

157-84.

Korhonen, I. and T. Juurikkala (2007), "Equilibrium exchange rates in

oil-dependent countries," BOFIT Discussion Papers No. 8.

Kose, M. A. (2002), "Explaining business cycles in small open

economies:‘How much do world prices matter?," Journal of

International Economics, 56(2), 299-327.

London, A. (1989), "Money, inflation and adjustment policy in Africa:

some further evidence," African Development Review, 1(1), 87-111.

MacDonald, R., & Ricci, L. A. (2001). "PPP and the Balassa Samuelson

effect: The role of the distribution sector," (Vol. 442). International

Monetary Fund.

Makdisi, S., Fattah, Z., & Limam, I. (2006), "Determinants of Growth in

the MENA Countries," Contributions to economic analysis, 278, 31-60.

McCarthy, J. (2000), "Pass-through of exchange rates and import prices

to domestic inflation in some industrialized economies," FRB of New

York Staff Report, (111).

Mendoza, E. G. (1995), "The terms of trade, the real exchange rate, and

economic fluctuations," International Economic Review, 101-137.

Montiel, P. J. (1989), "Empirical analysis of high-inflation episodes in

Argentina, Brazil, and Israel," Staff Papers-International Monetary

Fund, 527-549.

Morley, S. A. (1995),. "Structural adjustment and the determinants of

poverty in Latin America," Coping with austerity: Poverty and

inequality in Latin America, 42.

Ndung’u, Njuguna. (1993), Dynamics of the Inflationary Process in

Kenya, Göteborg: University of Göteborg.

Journal of Economic Cooperation and Development 27

Ndung'u, N. S. (1997), "Price and Exchange Rate Dynamics in Kenya:

An Empirical Investigation," (No. 58).African Economic Resarch

Consortium (AERC)African Economic Research Consortium, AERC

Research Paper /58.

Odusola, A. F., & Akinlo, A. E. (2001),"Output, inflation, and exchange

rate in developing countries: An application to Nigeria," The Developing

Economies, 39(2), 199-222.

Odedokun, M. O. (1997)," Dynamics of inflation in Sub-Saharan Africa:

the role of foreign inflation, official and parallel market exchange rates,

and monetary growth," Applied Financial Economics, 7(4), 395-402.

Ricci, M. L. A., Lee, M. J., & Milesi-Ferretti, M. G. M. (2008), "Real

exchange rates and fundamentals: A cross-country perspective," (No. 8-

13). International Monetary Fund.

Rodriguez, G. H., & Gazani, G. D. (1995), "Fluctuaciones

macroeconómicas en la economía peruana" Banco Central de la

República Dominicana.

Rodrik, D. (2008), "Normalizing industrial policy," International Bank

for Reconstruction and Development/The World Bank.

Rogers, J. H., & Wang, P. (1995), "Output, inflation, and stabilization in

a small open economy: evidence from Mexico," journal of Development

Economics, 46(2), 271-293.

Roubini, Nouriel, and Brad Setser. (2004), "The US as a net debtor: The

sustainabil- ity of the U.S. external imbalances," New York University.

Mimeograph.

Santaella, J. A., & Vela, A. (1996),"The 1987 Mexican disinflation

program: an exchange rate-based stabilization?" International Monetary

Fund.

28 Oil Price Effects on Exchange Rate, Output and Consumer Price:

A Case Study of Small Open Economy of Oman

Schneider, M., & Tornell, A. (2004), "Balance sheet effects, bailout

guarantees and financial crises," The Review of Economic Studies, 71(3),

883-913.

Setser, B. (2007), "The case for exchange rate flexibility in oil-exporting

economies," (No. PB07-8). Peterson Institute for International

Economics.

Shahin, Wassim and Elias El-Achkar,( 2010), "Regional Monetary

Coordination between GCC Monetary Union and Other MENA

Countries," paper presented at the workshop, "The Evolving

International Role of the GCC," Economies at the Mediterranean

Research Meeting of the European University Institute.

Times of Oman, (2008), Daily Times of Oman, Muscat, 16 March,

Muscat, Sultanate of Oman.

Turner, P. M. (1993),. "A structural vector autoregression model of the

UK business cycle," Scottish Journal of Political Economy, 40(2), 143-

164.

Vinh, Nguyen Thi Thuy, and Seiichi Fujita (2001), "The impact of real

exchange rate on output and inflation in Vietnam: A VAR approach,"

Pesaran, M., Y.Shin and R. Smith (2001). "Bounds testing approaches to

the analysis of level relationships", Journal of Applied Econometrics 16

(2007): 289-326.

Williamson, J. (1994), Estimating equilibrium exchange rates. Peterson

Institute.

Journal of Economic Cooperation and Development, 37, 3 (2016), 29-56

The Impacts of Foreign Labour Entry on the Labour Productivity

in the Malaysian Manufacturing Sector

Nur Sabrina Mohd Palel

1, Rahmah Ismail

2 and Abdul Hair Awang

3

Improvement and strengthening of labour productivity is an important

approach to accelerate the growth of the manufacturing sector in Malaysia.

This study attempts to analyses the impacts of the entry of foreign workers on

the labour productivity of the manufacturing sector in Malaysia. The analysis

of this study employs the dynamic panel data method which combines time

series and cross-section data. The data used was from the year 1990 to 2008,

covering 15 selected sub-sectors in the Malaysia manufacturing sector. Core to

the analysis in the study is the Pooled Mean Group (PMG) estimation model.

The study found that foreign labour, local labour, capital intensity and foreign

direct investment (FDI) have positive and significant effects on the labour

productivity growth. The study differentiates between local and foreign labour

into categories of skilled and unskilled labour. The findings indicated that

unskilled foreign and local labour are negatively and significantly affect the

growth of labour productivity in the long run. Inversely, skilled local and

foreign labour had a significant and positive impact on the labour productivity

growth. However, the contribution of foreign labour on labour productivity is

smaller compared to the local labour.

1. Introduction

Labour productivity is an important, frequently emphasised element in

any sector as part of an effort to keep a sector competitive in the global

market. The growth of the industrial sector has been successful in

increasing export and this effectively led to the innovation of new

1 MEc Student, Faculty of Economics and Management, Universiti Kebangsaan

Malaysia Email:nur02862yahoo.com 2 Senior Lecturer, Faculty of Economics and Management, Universiti Kebangsaan

Malaysia Email:[email protected] 3 Senior Lecturer, Faculty of Social Sciences and Humanities,Universiti Kebangsaan

Malaysia Email: [email protected]

30 The Impacts of Foreign Labour Entry on the Labour Productivity

in the Malaysian Manufacturing Sector

technologies and improvements in the internal management of firms.

Since independence, Malaysia has experienced encouraging phases of

economic development through various economic development policies

and strategies. In fact, before the Asian financial crisis in the year 1997,

the country is known as one of the rapidly growing economies on par

with the developed economies in East Asia such as Japan, South Korea,

Taiwan and Hong Kong (Ishak Yussof & Nor Aini, 2009). A rapidly

growing manufacturing sector can speed up the growth of an economy

due to its share in the Gross Domestic Product (GDP), job creation and

foreign exchange. One of the most effective ways to further improve this

sector is by improving labour productivity. The logic is simple; a higher

productivity means that the same number of inputs can produce higher

quantities of output. Sahar (2002) explains that a high labour

productivity in the manufacturing sector can help create sustainable

growth and development of a country.

Economic growth is an important determinant of national development

and these are two interrelated concepts. A country can grow without

developing, but to develop, a country needs to grow. Economic growth

requires a combination of a number of factors, including labour, land,

capital and technology being employed efficiently without waste.

Labour - local and foreign - is an important part of this equation. In

general, the rationale behind employing foreign labour is to fill the gap

create by the shortage of labour supply in the local labour market

especially in sectors like farming, construction, service, industrial and

manufacturing. This is a short term solution according to Preibisch

(2007). Nevertheless, the output generated through the foreign labour

contributes positively to the country's export.

It must be noted that foreign labour has contributed to Malaysia's

economic growth, especially with regard to the GDP and aggregate

expenditure. The government has effectively prevented excessive

increases in wages and inflation. The wages paid to the foreign workers

are considerably lower than the what the locals receive. Despite the

relatively lower wages, the foreign labour positively contribute to

increase in demand (Borjas, 2006). However, being a short-term

solution, the economy cannot continuously depend on the contributions

of foreign workers. With the country looking to become a high earning

economy by 2020, a switch of strategy is important and thus, rather than

Journal of Economic Cooperation and Development 31

relying on the number of inputs, more emphasis should be given to

increasing productivity of input.

An influx of foreign workers can affect an economy both positively and

negatively. Its influence on the labour market depends on its role,

whether as a substitute or a complement to the local workers. Borjas

(1993) found a negative impact of foreign workers. However, he

stressed that such negative influence is only valid for unskilled foreign

labour. The direction of the effects of foreign worker entry on a market

depends on their productivity. Highly productive, skilled foreign worker

can immensely contribute to an (Hercowitz et al. 1999). On the other

hand, unskilled foreign workers may have problems adapting and may

end up needing more help than contributing. It is worth noting that

several studies have been conducted on this topic but the results have

been inconsistent. As such, the issue is very much inconclusive. It is

therefore imperative for researchers to keep on studying the subject and

more importantly on the factors that make the results so inconsistent.

Compared to more developed economies like China, Singapore and

South Korea, our labour productivity is still relatively modest (Malaysia

Productivity Corporation, 2013). A shortage of labour during the period

of the 7th Malaysia Plan (7MP) has tightened the labour market and

pushed wages up. As part of the effort to reduce the shortage, a

programme was initiated to allow for foreign workers entry. It was,

however, at that time, unclear how the influx of skilled and unskilled

foreign workers can generate growth of the manufacturing sector in the

longer term.

Overall, the study aims to contribute to the literature on this topic

through its measurement method which was used to estimate the impact

of foreign workers entry on labour productivity. The method is known

as Autoregressive Distributed Lag (ARDL) dynamic panel test method

using Pooled Mean Group (PMG) estimation model. This method

allows the researcher to observe the relationship between the

independent and dependent variables in the short and long terms.

Furthermore, this study provides a more detailed insight by dividing the

foreign labour into skilled and unskilled categories.

The objective of this study is to analyse the short and long term effects

of foreign worker entry in general on the productivity of labour. The

32 The Impacts of Foreign Labour Entry on the Labour Productivity

in the Malaysian Manufacturing Sector

study also sought to examine the influences of the use of foreign and

local, skilled and unskilled labour on the productivity of labour. This

paper is organised into five sections, namely introduction, literature

review, methodologies, research findings and the last part from this

study is conclusions and suggestions.

1.1 Trend of Foreign Labour in Malaysia

Rapid economic development has led to rapid changes in the labour

market. With demand for labour increasing more than the supply, there

was a need to address this shortage by allowing entry of foreign workers

into the domestic market. As a result, there has been a steady influx of

foreign workers from various countries such as Indonesia, India, Nepal,

Bangladesh and Filipina. Table 1 summarises the development of the

entry of foreign workers into Malaysia from the year 2007 to 2011. It is

clear, however, that while entry is still occurring, the numbers were

declining steadily. Manufacturing sector recorded the highest inflow of

foreign workers from year 2007 to year 2011 compared to other sectors.

Local Electrical and Electronics (E &E) industry was the main sector

contributing 55.9 percent of the country's exports and employs 28.8

percent of the national labour force (Prime Minister's Department,

2012). This industry has also successfully developed the ability and

skills for the manufacturing sector, consumer electronics, and electronic

and electrical components. Productivity generated by foreign labour has

helped increase total exports and consequently contribute to the surplus

in the balance of payments. Strong export revenue growth is directly

driven by high export value. Therefore, the enhancement and

strengthening of productivity is one approach that can be taken to

accelerate the growth of the manufacturing sector in Malaysia.

Journal of Economic Cooperation and Development 33

Table 1:Number of foreign labour in Malaysia by sector , 2007-2011 (’000).

Sector 2007 2008 2009 2010 2011

Total 2,044,805 2,062,596 1,918,146 1,817,871 1,5730,61

Agriculture 165,698

(8.1)

186,967

(9)

181,660

(9.4)

231,515

(12.7)

152,325

(9.6)

Farming 337,503

(16.5)

333,900

(16.1)

318,250

(16.5)

266,196

(14.6)

299,217

(19)

Manufacturing 733,372

(35.8)

728,867

(35.3)

663,667

(34.5)

672,823

(37)

580,820

(36.9)

Construction 293,509

(14.3)

306,873

(14.8)

299,575

(15.6)

235,010

(12.9)

223,688

(14.2)

Service 200,428

(9.8)

212,630

(10.3)

203,639

(10.6)

165,258

(9)

132,919

(8.4)

House maid 314,295

(15.3)

293,359

(14.2)

251 355

(13.1)

247,069

(13.5)

184,092

(11.7)

Source: Ministry of Home Affairs, various years.

Note: Values in bracket are percentage.

In the duration of the 9MP, the government was committed to reform the

labour market, with particular emphasis on the increased mobility of

labour and increasing the skills of the workforce. Labour market reforms

were essential to provide a platform for the country to continue to grow

towards becoming a high income economy.

Table 2: Number of foreign labour by skill (’000) for the year 1990-2008

Source: Department of Statistics Malaysia, various years.

Table 2 reports that the number of unskilled foreign workers has more

than doubled in the 2000s compared to the 1990s (from 86,847 in 1990

to 198,876 in 2000). This influx of unskilled foreign workers can be

attributed to the unwillingness of the locals to be involved in

occupations which has the features of 3D (Dirty, Dangerous, Difficult).

Year Skilled Unskilled

1990 9,154 86,847

1995 7,016 104,665

2000 6,986 198,876

2005 9,022 336,055

2008 11,245 421,985

34 The Impacts of Foreign Labour Entry on the Labour Productivity

in the Malaysian Manufacturing Sector

Meanwhile, the number of skilled foreign labour has shown a steady

decrease from the year 1990 until 2000 but steadily increased again until

2008. The skilled foreign workers are complements to the local skilled

workers and a combination of both is needed to facilitate the growth of

the economy towards becoming more competitive.

2. Literature Review

Productivity refers to the comparison between the output and the input

used to produce it. The inputs for a business are resources within an

organisation which include human capital, finances, etc. while output is

the product produced using the available input (Braid 1983; Prokopenko

1987). Most of the definitions of productivity are related to the

measurement of efficiency of input in the production of output and the

measurement of effectiveness by observing the ratio between the actual

output and the projected output (Pritchard, 1995).

Peri (2012) used the Cobb Douglas function to examine the long-term

effects of the entry of foreign workers on the American labour market

for the year 1960, 2000 and 2006. The findings indicate that foreign

workers have a positive effect on the specialisation of local workers.

Moreover, no evidence that foreign labour crowded-out employment,

rather it encourages efficient specialisation and encourages better use of

technology among the less skilled workers.

Huber et al. (2010), on the contrary, explains the entry of foreign

workers in a more negative light. They explained that locals normally

view foreigners as a threat to their employability. With increasing

population and labour supply, such view is natural. They also studied on