Japan’s Insurance Market 2015

To Our Clients

Tomoatsu Noguchi

President and Chief Executive, The Toa Reinsurance Company, Limited 1

1. The Earthquake Insurance System and Japan Earthquake Reinsurance Co., Ltd.

Masamichi Irie

President

Japan Earthquake Reinsurance Co., Ltd. 2

2. General Concepts Applied to a Proprietary View of Risk

Oriol Gaspa Rebull

Catastrophe Management, Aon Benfield

John Moore

Head of International Analytics, Aon Benfield 10

3. Preparing for a Japan Typhoon Megadisaster

Milan Simic, Ph.D., SVP

Managing Director of International Operations, AIR Worldwide

Ruilong Li, Ph.D.

Senior Engineer, AIR Worldwide 19

4. Recent Developments in Enterprise Risk Management among Japanese Insurance Companies

Nobuyoshi Yamori

Professor, Research Institute for Economics and Business Administration

Kobe University 25

5. Trends in Japan’s Non-Life Insurance Industry

Underwriting & Planning Department

The Toa Reinsurance Company, Limited 29

6. Trends in Japan’s Life Insurance Industry

Life Underwriting & Planning Department

The Toa Reinsurance Company, Limited 34

Supplemental Data: Results of Japanese Major Non-Life Insurance Groups (Company)

for Fiscal 2014, Ended March 31, 2015 (Non-Consolidated Basis) 40

Japan’s Insurance Market 2015

Contents Page

©2015 The Toa Reinsurance Company, Limited. All rights reserved. The contents may be reproduced only with the written permission of

The Toa Reinsurance Company, Limited.

It gives me great pleasure to have the opportunity to welcome you to our brochure, Japan’s

Insurance Market 2015. It is encouraging to know that over the years our brochures have been well

received even beyond our own industry’s boundaries as a source of useful, up-to-date information about

Japan’s insurance market, as well as contributing to a wider interest in and understanding of our

domestic market.

During fiscal 2014, the year ended March 31, 2015, the Japanese economy remained on a

moderate recovery track. Although the consumption tax increase weakened personal consumption

somewhat, capital investment trended upward, reflecting an improvement in corporate earnings.

In the non-life insurance industry in Japan, net premium income and profit trended upward

mainly owing to strong sales of fire insurance policies and new types of insurance policies, while

also benefiting from the revision of insurance premium rates and insurance products for

automotive insurance.

In the life insurance industry in Japan, net premium income trended upward supported by

buoyant sales of savings-type insurance products and medical insurance policies.

In the reinsurance market, owing to the large amount of capital flowing from financial markets

into the reinsurance market and the brisk performance of reinsurance companies, reinsurance premium

rates further softened and competition for contracts intensified among reinsurers.

In these circumstances, in accordance with the Forward 2014 medium-term management plan

launched in 2012, the Toa Re Group implemented initiatives to realize the corporate vision articulated

in the plan. Utilizing sophisticated expertise and intelligence, we provide peace of mind with high-

quality solutions and services with the goal of being a growing, profitable global reinsurance group

trusted by all stakeholders.

By endeavoring to act as an exemplary reinsurance company, we are resolved to fulfill our mission:

“Providing Peace of Mind.”

In conclusion, I hope that our brochure will provide a greater insight into the Japanese insurance

market and I would like to express my gratitude to all who kindly contributed so much time and effort

towards its making.

Tomoatsu NoguchiPresident and Chief Executive

The Toa Reinsurance Company, Limited

To Our Clients

1

The Earthquake Insurance System and Japan Earthquake Reinsurance Co., Ltd.

Masamichi IriePresidentJapan Earthquake Reinsurance Co., Ltd.1. Japan’s land area is only 0.25% of Earth’s total land area, but 20.8% of

earthquakes of magnitude 6.0 or greater worldwide have occurred in Japan, and

27,271 earthquakes have occurred in Japan over the 10 years since 2005. Japan is

located on the boundary between an oceanic plate and a continental plate. The

oceanic plate moves beneath the continental plate at a rate of several centimeters per

year, which causes large subduction earthquakes and inland earthquakes due to plate

movement. Moreover, Japan is located in the Ring of Fire and has about 7% of the

world’s active volcanoes. Japan is therefore prone to earthquakes.

Japan Earthquake Reinsurance Co., Ltd. (JER) is the only reinsurance company

in Japan that exclusively handles earthquake insurance, and will celebrate its 50th

anniversary next year. I would therefore like to provide an overview of our position in

Japan’s earthquake insurance system and discuss JER’s preparation for major

earthquakes.

(1) Specifics and Features of Earthquake InsuranceInsured risk:

Loss or damage due to fire, destruction, burial or flooding caused directly or indirectly

by any earthquake or volcanic eruption, or resulting tsunami (earthquake, etc.)

Insured interests:

Buildings for residential use and/or personal property. Commercial and industrial

risks (extended coverage for earthquake) are not insured.

Underwriting method:

Rider attached to a fire insurance policy. Currently, an earthquake insurance rider is

attached to just under 60% of fire insurance policies.

Sum insured:

30% to 50% of the sum insured by the main policy (fire insurance). However, the

sum insured is limited to a maximum of 50 million yen for a building and 10

million yen for personal property.

Payable degrees of loss:

Total loss, half loss, partial loss

Payable benefits:

• Total loss – total sum insured

• Half loss – 50% of sum insured

• Partial loss – 5% of sum insured

Limit of total amount of insurance claims to be paid:

Total amount of insurance claims to be paid is limited to 7,000 billion yen per

earthquake, etc. for all of the non-life insurance market.

Foreword

1. Earthquake Insurance System in Japan

2

(2) Reinsurance Mechanism1 Reinsurance Flow

JER concludes a reinsurance treaty (Treaty A) on earthquake risk with each direct

insurance company that sells earthquake insurance. As Figure 1 shows, in accordance

with the Act on Earthquake Insurance, direct insurance companies cede to JER 100%

of the sum insured they accept, and JER is obliged to take up the full liability for this

earthquake insurance without question. JER also concludes an earthquake retrocession

treaty (Treaty B) with each direct insurance company, and with Toa Re, to retrocede a

certain part of the liabilities accepted under Treaty A in accordance with the

predetermined share for each company. In addition, JER enters into an excess of loss

retrocession treaty (Treaty C) with the government and retrocedes to the government

part of the insurance liability taken up under Treaty A. JER retains the liabilities that

remain after retrocession through Treaty B and Treaty C of insurance liabilities

underwritten under Treaty A.

Figure 1: Reinsurance Flow

2 Reinsurance Scheme

As shown in Figure 2, the current reinsurance scheme consists of three layers. In the

first layer, JER as a private insurance company pays reinsurance claims up to 100 billion

yen per earthquake, etc. In the second layer, the government and non-life insurance

companies equally share reinsurance claims for the layer covering 262 billion yen in

excess of 100 billion yen. In the third layer, the government pays a majority of

reinsurance claims (approximately 99.5%) for the portion exceeding 362 billion yen up

to 7,000 billion yen. In portions of insurance claims to be paid by the private sector, JER

pays 100% of reinsurance claims in the first layer. In the second and third layers, non-

life insurance companies pay the lower portion and JER bears the upper portion.

Reinsurance (Collection and equalization of

risks at JER)

Direct insurance

Retrocession (Distribution of risks)

Treaty

A

Treaty

CTreaty

BRetention

Application for earthquake insurance policy

(Payment of premiums)

100% reinsurance(Payment of reinsurance

premiums)

Retrocession(Payment of retrocession premiums)

Retrocession(Payment of retrocession premiums)

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

Policyholders

Non-Life insurance companies

JER

Government (Earthquake Reinsurance Special Account)

Non-Life insurance companies

JER

3

3 Accumulation of Reserves

The probability of earthquake loss is extremely low compared with other insured

incidents, but the damage from earthquakes can be massive. Japan’s earthquake

insurance system is therefore predicated on an equilibrium between premiums and

payouts over an extremely long period. The reinsurance premiums that the government

receives from JER are accumulated in a reserve in a separate account, the “Earthquake

Reinsurance Special Account.” The government would first reverse this reserve to pay

out reinsurance claims in the event of a major earthquake, and would then pay from a

fund, which would be transferred from the general account or debt, to cover a temporary

shortfall should the reserve be insufficient. This fund would be repaid with future

reinsurance premium income, which serves as a mechanism to maintain the equilibrium

between premiums and payouts. At the same time, private insurance companies reserve

net premium income after deducting relevant operating expenses from premium income

in the reserve at the end of each fiscal year. In addition, insurance companies are

obligated to accumulate investment income from these reserves, which is a mechanism

that keeps insurance companies from profiting from this system.

100

billion yen

131.0 billion yen

31.8

billion yen99.2 billion yen

4.9 billion yen

25.5 billion yen

6,607.6 billion yen

Up to

362.0 billion yen

Approx.

1,451.9 billion yen7,000

billion yen

Reinsurance claims

Up to 100 billion yen

Up to

163.6 billion yen

Direct insurance companies 36.7 billion yen

JER 224.7 billion yen

Private sector total 261.4 billion yen

Government 6,738.6 billion yen

Total 7,000.0 billion yen

Liability limits

Approx.

99.5%

50%100%

50%

Approx.

0.5%

1. The Earthquake Insurance System and Japan Earthquake Reinsurance Co., Ltd.

Figure 2: Reinsurance Scheme (As of April 1, 2015)

1st layer 2nd layer 3rd layer

4

4 Liability Limit and Reserves

Private non-life insurance companies are supposed to bear as much of the liability

from earthquake insurance as they are able. However, excessive liability would impact

their ability to underwrite other types of insurance. Another problem is that a massive

earthquake could saddle insurance companies with liabilities that threaten their ability

to remain in business. A liability limit has therefore been set based on the reserves of

insurance companies. However, the decrease in reserves among private insurance

companies as a result of the Great East Japan Earthquake provided the impetus for a

fiscal 2013 change of the liability limit of the private sector to address two consecutive

major earthquakes. This added reliability to insurance benefit payouts and enhanced

trust in the earthquake insurance system.

Table 1: Liability Limit and Reserves (Billions of yen)

Fiscal yearPrivate sector Government

Liability limit Reserves Liability limit Reserves

2010 1,198.75 913.5 4,301.25 1,342.7

2011 724.45 394.2 4,775.55 886.8

2012 488.00 421.5 5,712.00 962.3

2013 240.50 450.6 5,959.50 1,072.7

2014 261.40 491.7 6,738.60 1,193.4

5 Penetration Ratio and Ratio of Fire Insurance Policies with an Earthquake Rider

Attached

Every area of Japan is exposed to earthquake risk. Japan therefore created an

earthquake insurance system with the goal of providing stability in the lives of people

who are affected by major earthquakes. This resulted in a need to increase the number

of policyholders by popularizing earthquake insurance. The General Insurance

Association of Japan (GIAJ) and non-life insurance companies therefore engage in a

diverse range of activities to promote understanding of earthquake insurance and

increase the penetration ratio.

Figure 3 shows that the penetration ratio is below 30% even though major

earthquakes in the past have resulted in steady increases in the penetration ratio.

Recent data show that the ratio of fire insurance policies with an earthquake rider

attached is just under 60%. The industry must maintain ongoing initiatives to increase

these ratios.

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

5

Figure 3: Household Earthquake Insurance Coverage Ratio and Ratio of Fire

Insurance Policies with an Earthquake Rider Attached

Note: The household coverage ratio for fiscal 2014 is a provisional figure calculated using the

number of households for fiscal 2013. The earthquake rider ratio had not been publicly

announced when this article was being written.

(1) History of JER The frequency and magnitude of earthquakes are difficult to determine

statistically. The irregular timing of earthquakes and risk that they can be massive

creates various issues for risk coverage by the conventional insurance system. However,

the massive damage caused by the Niigata Earthquake of 1964 added momentum to

the movement to create an earthquake insurance system, which was established in

June 1966 along with JER.

Japan’s earthquake insurance system was created with the assumption that it

would be supported by the government and would be managed according to the

relevant laws. These laws are the basis for JER’s role as a company that reinsures the

liabilities assumed by insurance companies. JER is a completely private company

funded by Japan’s non-life insurance companies to serve as the government’s

counterparty in reinsurance contracts for earthquake risk, and is therefore a central

component of a reinsurance system designed to strengthen the core of the earthquake

insurance system provided by a public-private partnership.

(2) JER’s Operations JER’s management philosophy is to be a company that society broadly trusts by

contributing to the continuity and development of a well-funded and reliable social

system through the sound management of a system for providing earthquake insurance.

Our mission is to financially support the swift payout of insurance benefits by

direct non-life insurance companies by paying out reinsurance claims in order to

immediately stabilize policyholders’ lives in the event of a massive earthquake.

2. JER’s History and Current Status

1. The Earthquake Insurance System and Japan Earthquake Reinsurance Co., Ltd.

20142010200520001995

Household coverage ratio (right scale)Policies (left scale) Earthquake rider ratio (right scale)

(Thousands) (%)

(Fiscal years)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0

10

20

30

40

50

60

70

2013

6

JER administers and manages the reserves of direct insurance companies

collectively with its own reserves to ensure the rapid availability of capital if massive

earthquake damage occurs. Our approach to asset management focuses first and

foremost on soundness and liquidity because we may have to dispose of all assets to

handle massive reinsurance claims payouts. The profitability of asset management is

important for us, but as an additional consideration to soundness and liquidity. We

primarily invest in highly liquid, highly rated financial instruments including

government bonds, and do not invest in riskier assets such as equities.

JER is a small company with about 30 employees, but is concentrating intensely

on strengthening and raising the sophistication of its business continuity management

(BCM) in the event of a massive earthquake. Our compact organization requires all

employees to enhance their performance, and we emphasize employee development as

a key management priority.

(3) Key Performance Indicators Our key performance indicators for the past five years follow below. Net premium

income has increased by 50% over the past five years. On the other hand, net claims

paid after recovery of reinsurance claims increased to nearly 200 billion yen in fiscal

2011, but has been trending downward in tandem with payout of insurance benefits

by direct insurance companies resulting from the Great East Japan Earthquake.

Total assets decreased by more than half to the 500 billion yen range as a result of

payment for the Great East Japan Earthquake, but currently have recovered to the 600

billion yen range. Return on investment was nearly one-third the level five years ago

because interest rates have remained low amid persistent deflationary conditions and

have been further impacted by the ultra-low interest rates that have become the norm

worldwide.

Table 2: Key Performance Indicators of JER (Millions of yen)

Fiscal year 2010 2011 2012 2013 2014

Net premium income 71,532 83,671 92,996 92,248 108,994

Net claims paid 1,033 196,625 31,607 15,010 9,563

Total assets 1,154,108 509,498 536,808 577,305 640,137

Return on investment 1.20% 1.18% 0.89% 0.70% 0.42%

Number of employees 25 26 27 26 29

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

7

On March 11, 2011, the non-life insurance industry established the Earthquake

Insurance Central Command at GIAJ after the Great East Japan Earthquake occurred.

Rapid payment of a large number of claims to policyholders ensued, with the industry

paying out more than 1,200 billion yen for 780 thousand claims within about three

months.

The payout of estimated reinsurance claims was an initiative that was the first of

its kind since Japan’s earthquake insurance system was established. In a typical

reinsurance transaction, the direct insurance company first pays claims to

policyholders and then submits a statement of account for a reinsurance claim to the

reinsurer. However, the advance payments to policyholders by direct insurance

companies could run into trillions of yen if a massive earthquake occurs. The

earthquake insurance system therefore created a procedure for paying estimated

reinsurance claims. As a result of this procedure, JER had provided a total of nearly 1

trillion yen in four payments to direct insurance companies by May 25, 2011, or 75

days after the earthquake occurred on March 11, 2011.

The experience of the Great East Japan Earthquake reaffirmed the importance of

business continuation at JER because we are infrastructure that secures the cash flow

of non-life direct insurance companies. JER functioned effectively after the

earthquake, but Tokyo did not suffer significant damage and our normal business

activities resumed soon after the earthquake occurred. We have been upgrading

various aspects of our operations environment including IT system infrastructure to

maintain highly precise operations even in the high-pressure situation of an inland

earthquake in the Tokyo metropolitan area.

Specifically, in fiscal 2012 we renovated internal IT system infrastructure and

established a virtual IT platform at data centers in Tokyo. At the same time, we

established a backup data center in Okinawa because it does not rely on the Tokyo

electric power grid, which experienced electricity shortages as a result of problems at

nuclear power plants after the Great East Japan Earthquake, and the probability that it

will experience a disaster at the same time as Tokyo is low. We also constructed a

framework for synchronizing data in Tokyo and Okinawa using telecommunication

lines. In addition, we installed thin client terminals and consolidated data in the

virtual platform to introduce a remote access framework that allows employees to

directly access data center systems via the Internet from their homes or other offsite

locations. Moreover, in fiscal 2014 we established a provisional office in Saitama

Prefecture to secure space we can use if a disaster renders the head office unusable. We

completed the installation of terminals and other equipment needed to conduct

operations, thus constructing a system that enables operations to continue within the

same IT system infrastructure as the head office through the use of remote access.

We have conducted repeated training and drills from employee homes and the

provisional office using the environment we have prepared so that we can conduct

various crucial operations such as the payout of estimated reinsurance claims if an

emergency occurs. These initiatives do not have an endpoint because they are an

important ongoing effort to improve our capabilities.

4. Preparing for Future Earthquakes: Specific Initiatives in Anticipation of an Inland Earthquake in the Tokyo Metropolitan Area

3. JER’s Role after the Great East Japan Earthquake

1. The Earthquake Insurance System and Japan Earthquake Reinsurance Co., Ltd.

8

In 2013, the government’s Central Disaster Management Council estimated the

probability of a magnitude 7 class inland earthquake in metropolitan Tokyo within the

next 30 years at approximately 70%, and predicted the probability of a magnitude 8

to 9 class Nankai Trough earthquake at 70% as well.

The government’s Disaster Management Basic Plan advocates that the earthquake

insurance system should be strengthened as a means for citizens to enhance their own

efforts to prepare for an earthquake. Rapid, reliable insurance benefit payouts from the

earthquake insurance system when an emergency occurs will become even more

important.

Given these circumstances, JER’s role and mission are to function reliably in the

event of a massive earthquake and to contribute to the earthquake insurance system’s

evolution and development as a company that specializes in earthquake reinsurance.

JER initiated a three-year medium-term management plan in fiscal 2015 as a step

toward its next 50 years. The subtitle of the plan is “Strengthening Our Ability to Pay

Earthquake Reinsurance Claims,” and implementing these initiatives is a top priority.

Japan’s earthquake insurance system is an excellent public-private partnership

within an outstanding framework, and the system functioned effectively after the

Great East Japan Earthquake. JER has an important role as the only company in Japan

that exclusively handles earthquake reinsurance. We have reaffirmed the importance of

our responsibility to society and will fulfill our role and mission.

Conclusion

Surveillance

Virtual Platform(An environment in

anticipation of disasters)

Temporary Office(Saitama City)

Remote Access(Home)

Remote Access(Out of the office)

Head Office(Tokyo)

Okinawa Data Center

Surveillance

Virtual Platform(Main)

Tokyo Data Center

Surv

Internet (KDDI)

Internet (USEN)

Firewall Active/Standby L3 Switch

[Redundancy]

Data Synchronization

Active

Active

Standby

Standby

L3 Switch[Redundancy]

ActiveStandby

WAN

Thin Client

Figure 4: IT System Infrastructure in Anticipation of an Inland Earthquake in the Tokyo Metropolitan Area

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

9

General Concepts Applied to a Proprietary View of Risk

Oriol Gaspa RebullCatastrophe Management, Aon Benfield

John MooreHead of International Analytics, Aon Benfield2. In recent years, owning a view of risk has become a crucial part of a good

Enterprise Risk Management (ERM), but having a proprietary view of risk can be

subject to strong requirements, such as those set by Solvency II and the Own Risk

and Solvency Assessment (ORSA) in Europe.

Throughout this article we will try to provide some guidance on general concepts

involved in a “proprietary” view of risk, together with examples of tools and processes

used to accurately assess and manage risk, with a view to shedding light on how to

face and respond to present and future regulatory requests.

At the heart of the prudential Solvency II directive, the ORSA is defined as a set

of processes constituting a tool for decision-making and strategic analysis. It aims to

assess, in a continuous and prospective way, the overall solvency needs related to the

specific risk profile of the insurance company.

The second pillar of Solvency II plans to complement the quantitative capital

requirements with qualitative ones and a global and appropriate risk management

system. The reform provides measures on governance, internal control and internal

audit in order to ensure sound and prudent management practices from insurers.

Impacts in terms of risk and solvency should feed into upstream strategic decisions.

The internal assessment process of risks and solvency, known as the ORSA, is the

centrepiece of this plan.

In an operational way, the ORSA is part of the global process of Enterprise Risk

Management (ERM).

Figure 1: Potential Stakeholders of the Insurance Industry

It is part of a cyclical and iterative system involving the board of directors,

internal audit, senior management, internal control and all employees of the

company. It aims to provide a reasonable assurance of compliance with the strategy of

the company against risks.

Introduction

1. International Approach to Risk Management

ORSASolvency II

Insurers

Regulators

Rating Agencies

Investors

Policy- holders

10

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

The General conditions in the guidelines on ORSA described by European

Insurance and Occupational Pensions Authority EIOPA (EIOPA-CP-11/008) state

that: “The undertaking should develop its own processes for the ORSA, tailored to fit

into its organisational structure and risk management system with appropriate and

adequate techniques to assess its overall solvency needs, taking into consideration the

nature, scale and complexity of the risks inherent to the business.”

But what are these “appropriate” and “adequate” techniques to assess the

solvency needs?

Although there are many ways to achieve a specific view of risk, it is possible to

group them in three main areas.

• Data Quality & Benchmarking

• Modelling

• Adjustments

(1) Data Quality & Benchmarking The first stage towards achieving a consistent view of risk is to have good quality

data and reliable quality control procedures on this data. Regardless of the line of

business, it is very difficult to have an accurate understanding of modelling outputs

without knowing the inputs provided.

The concept of GIGO (Garbage In Garbage Out) is as applicable in the computing

world as it is in the insurance sector. No model or tool will deliver an accurate and

reliable output unless the inputs provided have a minimum standard of quality.

It is very complicated to have a clear and defined risk strategy when there is no

control on the exposure underwritten. The higher the resolution and granularity of

the insurance portfolios, the lesser the uncertainty around the assessment of the risk.

Standards of quality can vary by region, peril and line of business, but anyone

aiming to have their own view of risk should strive towards the highest quality

exposure data possible.

Data quality control alone is sometimes not enough. To achieve a comprehensive

view of risk, a second process is often required.

Data benchmarking provides an objective perspective towards the consistency

and accuracy of the data. Regardless of the quality of the records and procedures used

to compile them, it is important to have an opinion on how that data looks, and to

compare it against data from other sources.

For example an insurance company might have gone through an intense process

of increasing the quality of its portfolio risk types (occupancies and construction types

within the exposure). Although this guarantees a high standard of data quality, it is

equally important to compare this data set against a general market view. If that

insurance company has a 90% portfolio weighting of industrial exposures versus a

50% average in the market, we can assume that their property diversification is low,

hence heavily biased towards a single line of business, which would not be considered

best risk management practice.

2. General Concepts Involved in a “View of Risk”

11

(2) Modelling Modelling is a valuable (but not the only) way to assess the risk a company might

be subject to, and entails a large number of disciplines and products available for risk

assessment.

From catastrophe to capital models they all share the same core idea: “The

process of using computer-assisted calculations to estimate the expected loss

associated to events with a distinct frequency and severity”.

All models are based on a historical catalogue of events and the completeness of

such catalogues is key when assessing the quality and suitability of the models.

Once the historical catalogue has been settled, each model will treat the historical

data in the most appropriate way possible depending on the purpose of the model.

Although models used in different areas of the insurance company may use very

diverse sources of data, they all strongly rely on them.

For example, a catalogue in a catastrophe model will be implemented in the

hazard module, but there are other components as important as the hazard, mostly the

vulnerability and financial modules which have as much relevance in the calculation of

the losses as the hazard. Vulnerability and Financial modules are separate and

independent elements of a catastrophe model and fulfil very specific functions,

designed to be able to assess losses due to natural and man-made catastrophes.

In general users do not have access to the component parts of such models,

especially if they have been provided by a third party, but they can work on

understanding the different constituent parts of such models.

Reaching an understanding of these parts is a step towards fulfilling what regulators

see as “owning a view of risk” when they refer to modelling. Being able to identify the

strengths and weaknesses of these models through a thorough study of their component

parts and outputs, provides extremely valuable information on the reliability of the tools

and their suitability to be able to represent an accurate view of risk.

(3) Adjustments There is a different kind of modelling also available which does not rely on

historical catalogues of events, but rather on loss experience.

This approach has the advantage of being independent of the mathematical

models, but is still linked to the events suffered in a region and the lines of business

relevant to each company.

The largest benefit of this approach is that it allows adjustments reflecting the

real loss history suffered by a company based on the actual claims collected, rather

than estimating physical properties of the events and then estimating a loss from it.

The main disadvantage is that is very dependent on the time span covered by

the loss experience and subject to exposure variation, claims collection uncertainty,

policy condition changes and other factors which can sometimes be very hard to

control and quantify.

There is of course the possibility of combining both approaches. When the loss

records do not provide a complete or partial picture, the results from the models can

be blended with the data to achieve a more accurate (or less uncertain) result.

2. General Concepts Applied to a Proprietary View of Risk

12

(4) Reaching a View of Risk As we have seen, there are several ways to reach a “view of risk” and each of them

feeds from the others, but there is a basic hierarchy to it (Figure 2).

Figure 2: Basic Components of a Proprietary View of Risk

Companies should not address Adjustments without a clear picture of the models

and the data used, and companies should not blindly take the modelling results

without a critical examination of their constituent parts and a strong control of the

exposures modelled.

Under Solvency II and ORSA requirements, any technique or tool capable of

providing a clear picture and addressing any of the issues involved in the aforementioned

components’ view of risk, should be accepted as an appropriate and adequate one.

Insurers, reinsurers and brokers on behalf of their clients, all use a wide variety of

tools, procedures and models to best estimate the risk their portfolios are subject to.

The range of complexity is quite wide, but there is always a tool which will suit

the purpose set by a company to reach a higher level of understanding of their risks,

which is by all means and purposes a step forward towards reaching their own view.

Here we will show a couple of examples which hopefully illustrate the variety and

flexibility of tools available to anyone in the insurance sector with a basic analytical

knowledge.

(1) Exposure Data Control One of the inherent issues always present in insurance and reinsurance is lack of

knowledge, regardless of the potential hazard affecting a book of business.

The concerns of companies are sometimes limited to the regions and perils

available in the catastrophe models, based on the assumption that commercial models

cover the main liabilities in the globe, but there are many countries and perils in the

world that have not been implemented in catastrophe models so far, and yet have

caused large losses at the time of their occurrence (for example, the Thai floods).

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

View of Risk

Adjustments 03

02

01Using & Understanding Models

Data Quality & Benchmark

3. State of the Art Products for Risk Assessment

13

The idea behind exposure data control tools is a very basic and old one. What

hazards are my portfolios exposed to? And can they cause large losses?

There are several tools available in the market that allow companies to overlay

exposure information with hazard maps. These are known as Mapping or

Geographical Information Systems (GIS) and their ultimate goal is to provide a

reference (either visual or numerical) capable to help underwriters and risk managers

to better control their exposure and risk (Figure 3).

Figure 3: A hypothetical exposure overlaid on top of a seismic hazard map (left). On the right, the same seismic hazard map from the Global Seismic Hazard Assessment Program (GSHAP) showing areas exposed to earth-quake in Asia. Such simple exhibits are very useful for risk management purposes as they provide a clear picture between the risk underwritten and the perils they are exposed to.

Some of the commercial software available is highly innovative and runs on very

versatile platforms that enable users to visualize and quantify their exposures to a

given risk, in addition to performing sophisticated, detailed data analysis capable of

driving insightful business decisions.

Such packages can assist users in global or individual risk mapping, pre-binding

underwriting analysis, risk driver analysis, claims planning and preparedness, post-

catastrophe analysis, identifying exposure accumulations around terrorist targets, and

a host of other functions.

Some of them even enable users to view and track exposures worldwide by

providing global mapping capabilities and portfolio analysis as well as up-to-date (real

time) information on catastrophes including earthquakes, hurricanes, wildfires,

tornados and hail events, volcanic eruptions, and other ad hoc events.

Sometimes, such level of complexity is not really needed. Commercially available

GIS software is capable of plotting maps like the ones in Figure 3 and can provide

equally powerful insights to support making underwriting decisions and growth

exposure management.

2. General Concepts Applied to a Proprietary View of Risk

14

(2) Models and Adjustments Although catastrophe models are very powerful tools, they lack the capabilities to

assess some lines of business, for example life and motor, outside the natural

catastrophe world.

So, how is a company supposed to manage the risk linked to a line of business

not covered by catastrophe models?

One way is to use a Dynamic Financial Analysis (DFA) tool to create loss

distributions representative of the loss experience suffered by a company.

A good example is a process followed by insurance companies or brokers with

access to a significant loss history record of the risks exposed.

The first step is to assess the quality of the loss data and establish the assumptions

to be applied. Transparency is a paramount feature in these kinds of procedures and

although such techniques are not always replicable they have to be at least caveated.

Knowing the limitations of a model or a tool is as important as understanding its

results.

Once the data quality control is done, the second step is to fit a statistical

distribution to the loss history. The mathematics behind are not straight forward, but

the concept is. From a suite of available mathematical distributions, we have to find

the best match to the experienced loss (Figure 4). The match is never perfect and the

convergence in the tail can sometimes be poor, but actuaries and catastrophe

modellers who work on a daily basis with such methods, will reach the most adequate

compromise between data and modelling.

Figure 4: Loss frequency distribution of historical losses and the best fitting distribu-tions. In our example a distribution (Pareto2 (MLE)) was chosen as the best fit for severity distribution.

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

Original Set Pareto 2 LogNormal

0%

20%

40%

60%

80%

100%

15

Once a distribution is found, the last step is to use a probabilistic tool (as in a

DFA model) to simulate losses based on some basic parameters like an underwriting

limit or attachment. The events experienced in the loss data need to be assigned a rate

of occurrence. Most of the data related to insurance losses follows a random

behaviour, which can be represented by a Poisson distribution with a mean based on

the time span of the historical data.

Figure 5: Per Risk Aggregate Ground-up Loss Curve Comparing the Historical Records with the Modelled Records Using a DFA

The final output is a distribution of modelled losses matching the historical data

and capable to forecast losses for further return periods than the ones in the loss

records (Figure 5).

But as mentioned already, there are several things to be considered in such an

analysis if it has to be used as an adjustment tool. For example the original loss data

might have to be compensated by indexation, loss records completeness, loss

thresholds and changing financial conditions or other factors, but as long as there is a

good understanding of the raw data (loss records benchmark), the data inputs to the

model (rectified loss data) and the processes behind the tools used (model evaluation),

such an exercise is extremely useful for underwriting purposes.

How can all these tools and concepts benefit the Japanese market?

The Japanese insurance market does not yet have a disclosed schedule of

implementation of a strict regulatory framework like Solvency II, but many Japanese

insurance companies, aware of the work carried on in Europe and the US, have

started to address their risk management strategies in a more comprehensive and

robust way.

The larger Japanese insurance groups have a significant contribution of risk

coming from international exposures, mainly in Asia, the US and Western Europe.

These groups are aware of international regulatory demands, ERM procedures and

the importance of a healthy risk management strategy.

2. General Concepts Applied to a Proprietary View of Risk

Return Period (years)403020100

Loss

Experienced Loss Modelled Loss

4. Japan Perspective

16

The General Insurance Rating Organisation of Japan (GIROJ), through its work

in data collection, statistical analysis and modelling, has a significant role in solvency

and the capital requirement in Japan. The treatment of cat reserves and the criteria

driving them have been evolving in Japan for several decades and more recently there

is a movement towards implementing a more ERM driven perspective.

In a different approach to Solvency II’s Standard Formula in Europe, insurance

companies use GIROJ probabilistic model outputs to meet the solvency requirements

in Japan, but they are not universally benchmarked against other catastrophe models

to assess internal views of risk.

Generally speaking, the probabilistic nature of the GIROJ models may make

them a more accurate regulatory tool to assess the risk insurance companies are

exposed to than the Standard Formula. Effectively, what GIROJ does is to bring its

own view of risk to the meeting of capital requirements in Japan.

This approach creates a dichotomy between Solvency needs and the internal view

of risk, which can lead a Japanese insurance company to have two very different views

of risk: one complying with the Solvency requirements established by GIROJ, and

another one poles apart, as an internal interpretation of risk based on internal models,

but both views are equally valid.

A meticulous capital management strategy requires a balance between capital and

risk as well as a sustainable growth approach, but how is it possible to have a sound

strategy when there is such an apparent contrast between the capital required by the

Solvency regulation and the internal capital requirements estimated by the internal

models (Figure 6)?

Figure 6: Hypothetical Gap Between an Internal View of Risk and the Solvency Requirements

How is an insurance company supposed to apply a sustainable growth strategy

without a tight control of the capital buffer between different views of risk or without

a fitted regulation around them both?

If, for example, GIROJ became the reference for solvency and internal risk

management requirements in Japan, Japanese insurers might face a tougher test than

the Solvency II Standard Formula when justifying a different view of risk from the

one established by GIROJ.

Suddenly that capital buffer would disappear, with a cascade effect on other fields

involved in the whole ERM framework.

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

Capital requirement based on solvency regulations

Capital buffer

Capital requirement based on an internal model

17

One must consider the fact that proactive pre-emptive measures towards

achieving a sound proprietary view of risk will help in the future to face tougher and

stricter regulatory requirements.

Here is where the international experience and all the tools available in the

market can help those who are ready to face such a challenge.

No insurance company is the same, and they all have very different internal and

external risk management strategies in place, but the sooner they get familiar with all

the general concepts applied to “a proprietary” view of risk, the better prepared will

they be to establish the “appropriate and adequate techniques” to assess their own

solvency and risk prerequisites.

Risk management is a very complex field, which involves many different

disciplines and large amounts of uncertainty.

In this paper, we have only described a handful of concepts and tools available in

the market used to create a “view of risk”. Whenever an insurance or reinsurance

company takes on the task to create such a view, they will face many challenges, from

understanding their exposures to how best to diversify their risk while following a

suitable growth strategy.

But like any large and complex operation, once the constituent parts and largest

drivers are identified, then the main issues can be tackled using the right tools in

hand. Such tools are already available and have been used for several years in the

international environment.

Every day the insurance market is becoming more and more technical and

demanding. Everyone has a need to allocate key people or resources towards

understanding the inputs and outputs of the tools and processes used in the creation

of a view of risk. They also need to make sure that knowledge is well communicated

and no information is lost in translation when shared among all the stakeholders.

A good ERM plan requires for all stakeholders to be aware of the main issues

faced so a sound strategy can be placed for both internal and external purposes.

Conclusions

2. General Concepts Applied to a Proprietary View of Risk

18

Preparing for a Japan Typhoon Megadisaster

Milan Simic, Ph.D., SVP

Managing Director of International Operations, AIR Worldwide

Ruilong Li, Ph.D.

Senior Engineer, AIR Worldwide3. Using model scenarios to probe your portfolio’s strengths and weaknesses is

responsible risk management practice. It is important to prepare for a wide range of

scenarios in order to respond effectively when disaster strikes. The scenario described

in this article is just one example of the extensive and widespread damage a typhoon

could produce in Japan and around Tokyo. The insured loss for this event has a

modeled annual exceedance probability of about 1.3% (a 75-year return period) for

all of Japan, and about 1.3% (75-year return period) for Tokyo. This is not an

extreme tail event; far greater losses are possible.

It is well into December when a Category 4 typhoon, the seventh typhoon

landfall of the year, slams into Japan. The slow-moving storm brings fierce winds,

some in excess of 160 km/h, to the coastal regions of Mie, Aichi, and Shizuoka

prefectures. A high storm surge plows into the levees surrounding Ise Bay, testing

flood defenses. Weakening as it moves inland over colder and more mountainous

terrain, the storm passes north and west of Tokyo, causing extensive wind damage to

the low-lying coastal areas around Tokyo Bay and higher elevations west of the city.

The storm, which makes a total of five landfalls in Japan, continues to weaken as it

moves across northern Honshu and Hokkaido.

Strong winds disrupt surface transportation, cause the cancellation of hundreds of

flights, and prompt officials to issue evacuation orders or advisories to hundreds of

thousands of residents. Heavy precipitation increases the risk of landslides. In Tokyo,

officials suspend public transit and close down schools. Production along the highly

industrialized southern coast is halted as vulnerable light metal roofing and siding are

either heavily damaged or destroyed.

AIR estimates that if such an event were to actually happen today, insured losses

would be 2.8 trillion yen (23.2 billion U.S. dollars)* for all of Japan and 630.7 billion

yen (5.2 billion U.S. dollars) for the Tokyo metropolitan area. The heaviest losses are

found in Shizuoka Prefecture and result from damage to industrial assets. Figure 1

shows the wind intensity footprint for this simulated storm.

* All U.S. dollar amounts are based on an exchange rate of JPY 1 = USD 0.00829, current as of

May 1, 2015.

1. Event Overview

Foreword

19

Figure 1: Wind Intensity Footprint (1-Minute Maximum Sustained Winds) of

the Typhoon Megadisaster Scenario from the AIR Typhoon Model for Japan

Source: AIR

The Northwest Pacific Basin produces more tropical cyclones than anywhere else

in the world. Since 1951, an average of four typhoons per year have made landfall on

one of Japan’s four islands – and another five come within 500 km of the coastline.

While typhoons can occur during any month of the year, most strike Japan between

May and October, with July through September being peak season.

2. Japan’s Typhoon Setting and History

3. Preparing for a Japan Typhoon Megadisaster

20

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

Wind drives most typhoon-related loss in Japan, but flooding is also a significant

threat because of Japan’s orientation, location, and terrain. After the destruction caused

in 1959 by Typhoon Vera – the costliest weather-related disaster in Japan’s history – the

government undertook a massive effort to strengthen coastal and inland defenses, and

most major cities are now protected by sophisticated flood defense systems.

Typhoon Vera was accompanied by an exceptionally destructive storm surge that

destroyed a levee and dyke system and inundated the city of Nagoya. More than 5,000

people were killed, and more than 834,000 buildings were damaged or destroyed in

Japan. Other significant historical storms include Typhoon Kathleen (1947) and

Typhoon Ida (1958). A more recent storm, Typhoon Tokage (2004), affected some of

the same areas as our Megadisaster scenario, but was far less powerful.

Throughout Japan, building codes are stringent and reflect the country’s exposure

to both wind and earthquake hazards, but many existing structures predate the

existence of these codes. Wood construction dominates residential exposures in Japan,

and modern wood-frame houses exhibit good lateral resistance to wind loads; thus,

major structural damage is expected to be limited at the wind speeds of the modeled

storm. However, damage to roof coverings and windows can allow wind-driven rain to

enter a building’s interior and cause extensive damage to building contents.

Furthermore, dislodged external components can become wind-borne debris that can

cause extensive damage to surrounding structures.

Larger multi-family apartment buildings and commercial and industrial structures

are generally engineered and made of reinforced concrete or steel. Damage is usually

confined to nonstructural components, such as mechanical equipment, roofing,

cladding, and windows.

A significant portion of Japan’s industrial stock is of non-engineered light metal

construction, which is one of the construction types most vulnerable to high winds.

These buildings can experience extensive structural damage, and even collapse.

Figure 2: Japan’s Insurable Exposure by Construction Type

Source: AIR

Agricultural

Commercial

Apartment Unit

Industrial

Single-Family Homes

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Masonry Steel WoodConcrete

3. Affected Exposure

21

AIR estimates that the simulated event featured here would cause insured losses of

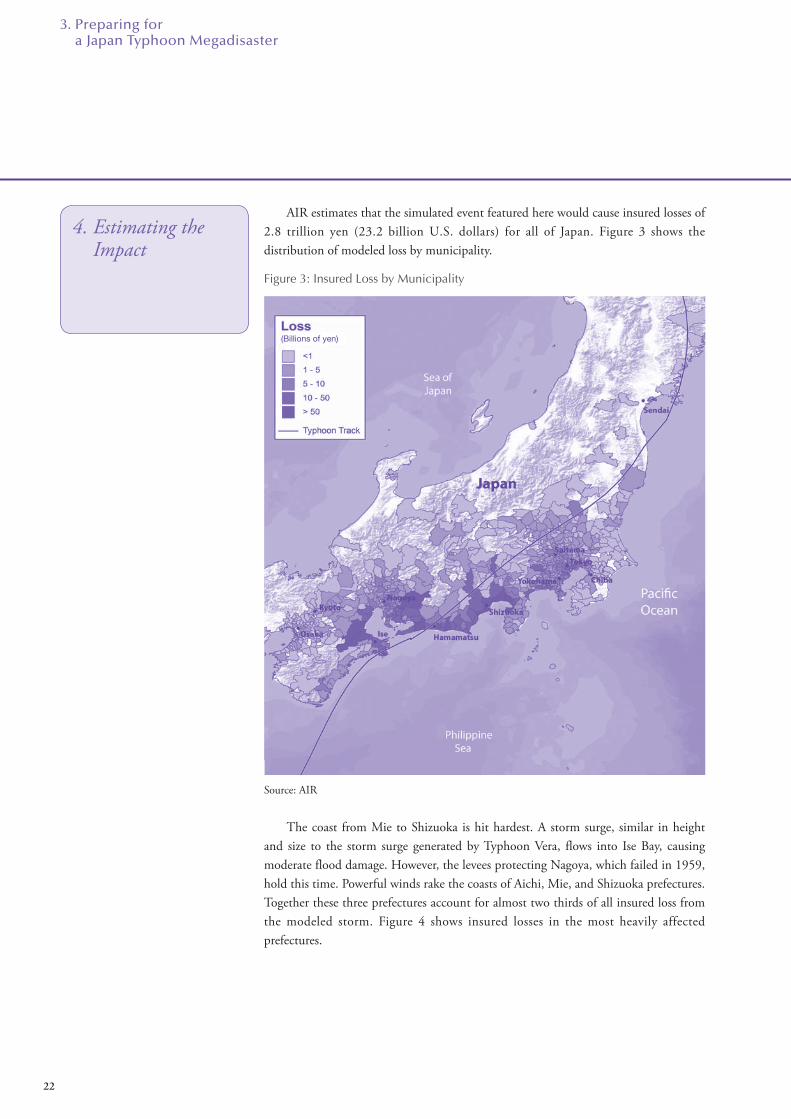

2.8 trillion yen (23.2 billion U.S. dollars) for all of Japan. Figure 3 shows the

distribution of modeled loss by municipality.

Figure 3: Insured Loss by Municipality

Source: AIR

The coast from Mie to Shizuoka is hit hardest. A storm surge, similar in height

and size to the storm surge generated by Typhoon Vera, flows into Ise Bay, causing

moderate flood damage. However, the levees protecting Nagoya, which failed in 1959,

hold this time. Powerful winds rake the coasts of Aichi, Mie, and Shizuoka prefectures.

Together these three prefectures account for almost two thirds of all insured loss from

the modeled storm. Figure 4 shows insured losses in the most heavily affected

prefectures.

(Billions of yen)

3. Preparing for a Japan Typhoon Megadisaster

4. Estimating the Impact

22

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

Figure 4: Insured Loss in the Most Heavily Affected Prefectures

Source: AIR

Much of this loss is industrial because this region is a manufacturing hub and

home to companies like Toyota, Brother Industries, Makita, Yamaha, and Suzuki.

Note that insurance penetration for industrial and commercial lines is typically much

higher than for residential lines, which is another contributing factor to high insured

industrial losses. On an insurable loss basis, residential losses exceed industrial losses.

Shizuoka Prefecture alone sustains over 891.6 billion yen (7.4 billion U.S. dollars)

in insured loss. Most of this loss is to industrial exposures in Hamamatsu and around

the northern portions of Suruga Bay. Shizuoka’s residential loss, at 257.5 billion yen

(2.8 billion U.S. dollars), is also the highest of any prefecture. To the west, most of the

529.6 billion yen (5.8 billion U.S. dollars) in Aichi prefecture is to industrial

exposures on Atsumi Peninsula and in and around the city of Toyota.

With 630.7 billion yen (5.2 billion U.S. dollars) in insured loss, the densely

populated Tokyo metropolitan area (consisting of the prefectures of Chiba, Kanagawa,

Saitama, and Tokyo Metropolis) accounts for 22% of the event’s total insured loss,

most of which is to residential properties. Strong winds affect all areas around Tokyo

Bay and areas to the west, such as Hachioji, Machida, Suginami, and Nerima, but

Edogawa and Ota are hit especially hard.

Figure 5: Insured Loss by Line of Business for Japan

Source: AIR

Automobile

Industrial

Commercial

Residential

1,000

900

800

700

600

500

400

300

200

100

0KanagawaShizuoka Aichi Mie Tokyo Saitama Chiba

(Billions of yen)

Insu

red

Loss

23

A few modeling best practices can help ensure that your model produces the most

realistic loss estimates:

• Building response to potentially damaging winds is highly dependent on its

location and attributes. Accordingly, collect accurate, detailed information for the

properties that make up your portfolio – including location and all primary

building characteristics such as construction type, occupancy, building age, height

– and a true replacement value. Relying solely on coarse resolution address data

can lead to significant over- or underestimations of risk.

• Be aware that typhoons in Japan can result in high flood losses. While

precipitation was not a significant source of loss in this Megadisaster scenario, the

AIR model provides the ability to separate wind and flood losses, which have

different policy conditions in Japan.

• Note that losses from extra cleanup expenses and debris removal can be a

significant source of additional insured losses (more than 30% for some policies).

While not included in the industry losses in this scenario, clients can explicitly

model these losses for their own portfolios.

• Consider the potential for business interruption losses. While not included in this

scenario, clients can use the AIR model to calculate business interruption losses as

a function of downtime, the level of damage sustained, the size of the building,

and its architectural complexity.

• Note that highly concentrated losses can trigger demand surge, which is an

increase in the cost of materials and labor after a large catastrophe due to limited

supply. This event triggers demand surge of about 10% for building damage,

which is included in the industry modeled losses.

• Finally, consider your loss ratio, or how your estimated losses compare to the

“total insured value” in each affected area. While your losses may at first appear to

be high, the loss ratio they reflect (typically less than 10% even in the worst

affected region of this Megadisaster analysis) should be entirely consistent with an

infrequent but thoroughly plausible catastrophic event.

AIR’s models capture the behavior of physical phenomena and how those

phenomena impact the built environment. They have been thoroughly validated using

data from a wide variety of sources.

But no model can predict what the next megadisaster will actually be or when it

will occur. This fundamental uncertainty makes it all the more important for

companies to use catastrophe models to prepare for such losses. The full range of

scenarios the models generate – simulating so many perils that impact so many places

– provide a unique and important global perspective on an organization’s overall risk.

The careful analysis of model results can help risk managers prepare for many

contingencies – thus ensuring that scenarios like the one presented here will not be

entirely unexpected.

Extreme Disaster Scenarios

To help risk managers think about events that are unlikely to be captured by traditional catastrophe

modeling techniques, AIR has created Extreme Disaster Scenarios (EDS) that can be analyzed using

AIR’s Touchstone® platform. These events are plausible but highly uncertain, and no attempt has

been made to assign them loss exceedance probabilities. Two EDS are available for the AIR Typhoon

Model for Japan that affect an area similar to the one in this Megadisaster scenario.

3. Preparing for a Japan Typhoon Megadisaster

5. Are You Prepared?

6. Closing Comments

24

Recent Developments in Enterprise Risk Management among Japanese Insurance Companies

Nobuyoshi YamoriProfessor, Research Institute for Economics and Business Administration Kobe University

Recent Developments in Enterprise Risk Management among Japanese Insurance Companies

Nobuyoshi YamoriProfessor, Research Institute for Economics and Business Administration Kobe University4.4. Many large financial institutions in the United States and Europe experienced

difficulties following the financial crisis in autumn 2008, forcing national

governments to provide large amounts of financial support in order to stabilize the

financial system. Naturally, people in each country rebelled against government

decisions to rescue the very financial institutions that had caused the crisis.

Governments therefore strengthened financial institution regulation and supervision

to preclude similar crises in the future. While Japan’s financial system was not

disrupted significantly, Japanese regulatory authorities revamped the financial

regulation framework in step with international trends.

Strengthening risk management and limiting the amount of risk in accordance

with the tightened regulations, however, does not equate to “management” of financial

institutions. Rather than limiting risk, financial institutions are now required to

manage the types and amounts of risk they bear in accordance with their capacities

and management philosophies in order to consistently increase corporate value over

the long term. Given this perspective, Enterprise Risk Management (ERM) has

naturally gained currency among Japanese insurance companies.

(1) The Challenging Environment of the Non-Life Insurance Business Underwriting profit and investment profit are the primary sources of earnings for

non-life insurance companies. Figure 1 shows profit and loss for Japan’s non-life

insurance companies according to each type of profit. Surprisingly, the industry

experienced underwriting losses in seven of the twelve fiscal years from fiscal 2002

through fiscal 2013, and notably had underwriting losses for the four consecutive

fiscal years from fiscal 2010.1 In particular, underwriting losses were a significant

339.1 billion yen for fiscal 2011.

Analysis of the deterioration of underwriting profits in terms of the three main

factors of premium income, insurance claims, and operating expenses (operating and

administrative expenses associated with underwriting) is instructive. Insurance

companies reduced operating expenses by improving efficiency, but lower premium

income obviated these efforts.2 In addition, insurance claims increased. Fiscal 2011

exemplifies this analysis. As a result of unexpected large-scale natural disasters

including the Great East Japan Earthquake in March 2011 and floods in Thailand in

summer 2011, the amount of net claims paid increased 1.2 trillion yen to 5.5 trillion

yen from 4.3 trillion yen in the previous fiscal year. Notably, greater weather-related

uncertainty resulting from climate change such as global warming is not the only

factor increasing risk for Japan’s insurance companies. The flooding in Thailand clearly

showed that Japan’s insurance companies are subject to global risks beyond the borders

of Japan, because the activities of non-life insurance companies and their clients have

become international. This shows that management of insurance risk has become

much more difficult than ever before.

Notes: 1. In fiscal 2014, underwriting is expected to become profitable because automobile insurance

cash flow improved, due largely to the revision of automobile insurance premiums.

2. Premium income totaled 9.3 trillion yen for fiscal 2002, but decreased to 8.7 trillion yen

in fiscal 2013.

1. The Importance of ERM

1. The Importance of ERM

2. The Current Situation of Japanese Non-Life Insurance Companies

2. The Current Situation of Japanese Non-Life Insurance Companies

25

Nonetheless, non-life insurance companies have recorded positive pretax net

earnings in all but one of the past twelve fiscal years. This was due to the contribution

from investment income. Figure 1 shows that investment profit has averaged about

500 billion yen annually, which has compensated for reduced underwriting profits.

However, there is still the risk of significant swings in investment income, as the direct

impact of the financial crisis resulted in investment losses in 2008. Financial market

volatility has increased amid structural changes in the global economy. It is obvious

that management of investment risk has become increasingly difficult as a result.

Figure 1: Underwriting Profit and Investment Profit of Japanese Non-Life

Insurance Companies*

* Based on data available from the General Insurance Association of Japan (GIAJ; aggregate non-

consolidated data for GIAJ members).

Underwriting profit = underwriting income – underwriting expense – operating, general and

administrative expenses associated with underwriting ± other income (expenses).

Investment profit = investment income – investment expenses.

(2) Pressure from Capital Markets to Increase Profitability In the past, shareholders rarely pressured management of insurance companies

under the system of cross-shareholdings among closely related banks and companies

within the same financial group. The shareholder composition of Japan’s large non-life

insurance groups, however, shows that foreigners have come to account for about 40%

of shareholders over the past several years. Foreign institutional investors with larger

stakes are insisting on profitability and dividends to shareholders. In addition,

Japanese institutional investors such as life insurance companies and pension funds

have come to aggressively demand improvement in management from their investees

because they need to improve their own performance.

FY2013FY2012FY2011FY2010FY2009FY2008FY2007FY2006FY2005FY2004FY2003FY2002

(Fiscal years)

(Billions of yen)

Underwriting profit Investment profit

-400

-200

0

200

400

600

800

4. Recent Developments in Enterprise Risk Management among Japanese Insurance Companies

26

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2015

These changes in shareholder composition and behavior have put intense pressure

on insurance company executives for strong profitability. The management targets of

all the major insurance groups include increased return on equity (ROE)3. For

example, Sompo Japan Nipponkoa Holdings, Inc. (SJNK) announced at an investor

relations meeting in May 2014 that a target for fiscal 2015 was to increase ROE to 7%

or more from 4.3% in fiscal 2013. MS&AD Insurance Group Holdings, Inc.

(MS&AD) has the goal of increasing ROE from 4.5% in fiscal 2013 to 7% in fiscal

2017, the final year of its new medium-term management plan, “Next Challenge

2017.” Similarly, Tokio Marine Holdings, Inc. set an ROE target of 7% or higher in

its medium-term management plan, “Innovation and Execution 2014;” ROE was

7.6% for fiscal 2013.

Note: 3. Simple comparison of percentages of ROE is not appropriate as insurance companies have

different ROE targets according to their strategies and circumstances.

The author has conducted joint research with ERM managers from Japan’s major

insurance companies since 2013. Through the joint research, the author concluded

that the ERM that Japanese insurance companies aim to achieve is management

targeting consistent increases in corporate value to ensure soundness while

maintaining and increasing profitability by determining the risks they should take and

the losses they could accept, premised on their own management philosophies and

missions.

Actually, the use of ERM as a key term in medium-term management plans has

become the norm for Japan’s major insurance companies. These companies have

transitioned from building the ERM system to fully employing it in management.

Many small and medium-sized insurance companies, however, are still building their

ERM systems. Moreover, even major insurance companies still have issues they must

resolve to raise the sophistication of their ERM.

The first issue is identifying and measuring risk. Each company is enhancing the

sophistication of its methods for identifying and measuring risk. However, companies

must constantly raise the sophistication of risk measurement because risk has become

more complicated and new types of risk have emerged.

The second issue is enhancing risk control technology. If management cannot

control risk appropriately, measuring risk is worthless to management.

The third issue is structuring ERM in terms of each company’s management

philosophy and mission. Soundness and profitability involve a trade-off that must be

balanced, but the desirable balance must be determined in accordance with each

company’s management philosophy and mission, rather than ad hoc. For example,

Japan is integrally subject to accumulated earthquake risk. It would be inappropriate

and against its mission for a Japanese insurance company to refuse to underwrite

earthquake risk from a risk management perspective. Japanese insurance companies

are expected to consider how to handle earthquake risk in a manner that ensures peace

of mind for the people of Japan, and then follow through.

3. Issues in the Sophistication of ERM

27

The fourth issue is the strong determination of management executives to actually

employ ERM in their management. For modern Japanese management executives,

corporate management is tantamount to the extreme difficulty of driving a car at night

in torrential rain. With the risk model as the headlights, risk control as the steering

wheel, and the management philosophy as the map, the management executive is the

person who actually uses all of these to navigate the deplorable roads that symbolize

risk. Risk control sometimes involves painful reforms such as business portfolio

restructuring. Companies need management executives who have the ability and the

will to implement such reforms.

The final issue is the need for an ERM culture. All employees, not just

management executives, must share an understanding of ERM for it to truly take root.

For example, ERM would be ineffective if a company cannot develop a large number

of employees who think and operate in terms of risk-based underwriting and

investment in their daily activities. Moreover, companies must construct a framework

that enables the continuity of ERM even if the top management changes.

When an emphasis on profitability was not as necessary because of low pressure

from shareholders, management executives could succeed by keeping the ratio of risk

to equity (= risk/equity) low to avoid risk. These days, however, the number of

shareholders who emphasize ROE (= earnings/equity) is increasing.

Management executives cannot be allowed to manage inefficiently, but at the

same time, an excessive emphasis on earnings by powerful shareholders can

compromise soundness and damage the interests of policyholders. Insurance company

management has a greater need for balance in the trade-off between soundness and

profitability than corporate management in general. Insurance company management

executives are now responsible for ensuring an appropriate return on risk (= earnings/

risk) in order to achieve higher ROE by balancing capital and risk.

Establishing ERM in accordance with a company’s management philosophy and

mission involves clarifying the risks the company should take and engendering a deep,

shared understanding of the company’s risk appetite among shareholders, management

executives, policyholders, regulatory authorities, and other stakeholders. This

approach enables an insurance company to keep its management strategy including

risk management without accepting inappropriate pressure from shareholders with a

short-term perspective. This means that management executives of insurance

companies must use ERM as a tool for communicating with stakeholders.

While ERM certainly evolved in response to international regulatory trends,

Japanese insurance companies are expected to proactively employ the ERM framework

to enhance their management capabilities.

4. Recent Developments in Enterprise Risk Management among Japanese Insurance Companies

4. Conclusions

28

Trends in Japan’s Non-Life Insurance Industry

Underwriting & Planning DepartmentThe Toa Reinsurance Company, Limited5. Fiscal 2014 results for Japan’s non-life insurance companies were solid. An

overview of the results of the 26 non-life insurers follows.

Net premium income in all lines of business increased to 8,083.1 billion yen, up

311.8 billion yen from the previous fiscal year, due to factors including higher

premium income from automobile insurance due to the effect of revised premium

rates and also the increase of household insurance premium. On the other hand, the

loss ratio improved by 1.8 percentage points to 62.3%. Despite an increase in payout

of claims associated with heavy snowfall in the Kanto region, claims paid due to

natural disasters decreased in fiscal 2014 and automobile claims paid decreased as a

result of fewer automobile accident claims. Expenses rose by 96.8 billion yen to

2,605.8 billion yen because higher premium income increased agency commissions.

Net expense ratio decreased slightly by 0.1 percentage points to 32.2%. The

underwriting result improved by 277.7 billion yen to an underwriting profit of 143.3

billion yen, because premium income increased and loss ratio improved. Major non-

life companies enjoyed better combined ratios compared with the previous year,

reflecting profit for the year.

Investment profit was solid, increasing 48.9 billion yen to 644.0 billion yen.

Although an environment of low interest rates continued, a weaker yen and high stock

prices contributed to the solid investment profit.

As a result of the above, results for both underwriting and investment were strong,

supporting an increase in ordinary profits of 332.2 billion yen to 746.8 billion yen.

While the reduction of the corporate tax rate resulted in the reversal of deferred

tax assets, net income increased 164.5 billion yen year on year to 378.8 billion yen.

(1) Overview of the Non-Life Insurance Industry The integration of four companies in 2010 – Mitsui Sumitomo Insurance Co.,

Ltd. with Aioi Nissay Dowa Insurance Co., Ltd., and Sompo Japan Insurance Inc.

with NIPPONKOA Insurance Co., Ltd. – began a cycle of business integration that

established an oligopoly in Japan’s non-life insurance market. As of March 31, 2015,

the top three non-life insurance groups (MS&AD Insurance Group Holdings, Inc.,

Tokio Marine Holdings, Inc., and Sompo Japan Nipponkoa Holdings, Inc.

(hereinafter abbreviated to “SOMPO HOLDINGS”)) account for approximately

85% of net premium income for the industry as a whole.

In addition, AIU Insurance Company, Ltd. and The Fuji Fire and Marine

Insurance Company, Ltd. of the American International Group, Inc. are integrating

their businesses through a merger that will establish a new company, AIG General

Insurance Co., Ltd., in July 2016 or later.

Thus, the non-life insurance industry is promoting increased operating efficiency

through mergers, functional consolidation and cost reductions. At the same time, the

industry is seeing initiatives to secure profits from new sources through business

collaboration with non-insurance companies. In addition, non-life insurers are

targeting increased earnings by investing in growth areas other than domestic non-life

insurance, including the life insurance business and overseas operations such as those

discussed below.

1. Trends in Business Results of Non-Life Insurance Companies for Fiscal 2014

2. Trends in the Non-Life Insurance Industry

2. Trends in the Non-Life Insurance Industry

29

Changes and trends among the top three non-life insurance groups are as follows.

MS&AD Holdings was created through the 2010 business integration of two

companies, Mitsui Sumitomo Insurance and Aioi Nissay Dowa Insurance. Since fiscal

2014, MS&AD Holdings has been implementing full-scale reorganization by

function. For example, Mitsui Sumitomo Insurance is handling the Group’s aviation

and marine insurance. While maintaining the framework of two core non-life

insurance companies, MS&AD Holdings is promoting growth and enhanced

efficiency by taking full advantage of their unique characteristics.

Tokio Marine Holdings did not execute major mergers in Japan after Tokio

Marine & Nichido Fire Insurance Co., Ltd. and Nisshin Fire & Marine Insurance

Co., Ltd. integrated their businesses in 2006. More recently, in 2013 the Tokio

Marine Group reached on an alliance agreement with National Mutual Insurance

Federation of Agricultural Cooperatives (Zenkyoren). This alliance is pursuing

opportunities through broad business ties that go beyond the boundaries of the

mutual aid business and the insurance business, such as business collaboration in the

field of agricultural risk.

With respect to SOMPO HOLDINGS, Sompo Japan Insurance and Nipponkoa

Insurance, both of which focus on the non-life insurance business in Japan, were

merged into Sompo Japan Nipponkoa Insurance Inc., on September 1, 2014, forming

the largest non-life insurance company in Japan in terms of non-consolidated

premium income.