Country update: Japan

www.pwc.com

Jack BirdPartner, PwC Japan

Yoko KawasakiPartner, PwC Japan

PwC

Agenda

2

Section one• Tax reform – basic plan

Section two• 2015 tax reform proposal highlights

- Corporate income tax - International tax- Consumption tax- Individual tax

Section three• Update on tax treaties

Global Tax Symposium – Asia 2015

PwC

Tax reform – basic plan

3Global Tax Symposium – Asia 2015

PwC

2015 tax reform fundamental principles

• Overcome deflation and regenerate economy• Energise the local economy• Delay the consumption tax rate hike• Enact anti-abuse rules related to international taxation (i.e. BEPS)• Enact legislation to help recover from the Tohoku Earthquake

4Global Tax Symposium – Asia 2015

PwC

2015 2016 2017 2018

Reduce corporate tax rate from 34.62%

Expand tax base • NOL limitations

Current: 80% of current income

• Limit dividend exclusion rules

• Enhance size-based enterprise tax Current: 2/8 of enterprise tax

• Special taxation measures

Corporate tax reform

32.11%

(▲ 2.51%)

31.33%

(▲3.29%)

less than 30%?

65% of current year income

50% of current year income

Reduce exclusion ratio

3/8 of total 4/8 of total

Revisit from scratch

5Global Tax Symposium – Asia 2015

PwC

Comparison of corporate effective tax rates

Current headline rates for countries other than Japan as of March 2014 except for the UK (April 2015). Japan rates are for Tokyo headquartered corporations.

6

45.00%

40.00%

35.00%

30.00%

25.00%

20.00%

15.00%

10.00%

5.00%

0.00%US France Germany UK China Korea Singapore

40.69% (-2011)40.75%

35.64%33.33%

38.36%(-2008)

30.00%(-2008)21.00%(-2014)

20.00%

33.00%(-2007)

25.00% 24.20% 20.00%(-2007)

17.00%

(2010-)

29.59%

Global changes in corporate effective tax rates

15.83%31.91%

21.00%33.33% 21.00%

22.00% 17.00%

38.01% (2012-)

23.71%

11.93%

22.47%

33.10%33.10%

5.75%

13.76%

2.20%

Japan2014

Japan 2015

10.63%Target rateNew rate

National taxes

Local taxes

Global Tax Symposium – Asia 2015

PwC

Comparison of corporate effective tax rates

Current headline rates for countries other than Japan as of March 2014 except for the UK (April 2015). Japan rates are for Tokyo headquartered corporations.

7

45.00%

40.00%

35.00%

30.00%

25.00%

20.00%

15.00%

10.00%

5.00%

0.00%US France Germany UK China Korea Singapore

40.75%

35.64%33.33%

20.00%

25.00% 24.20%

17.00%

29.59%

Current corporate effective tax rates

15.83%31.91%

21.00%33.33% 21.00%

22.00% 17.00%

23.71%

11.93%

22.47%

33.10%33.10%

5.75%

13.76%

2.20%

Japan2014

Japan 2015

10.63%Target rateNew rate

National taxes

Local taxes

Global Tax Symposium – Asia 2015

PwC

Corporate tax reform

Government is signalling future tax reform including:• Expand size-based enterprise tax• Change depreciation schedules• Change SME taxation

- ‘SMEs’, as defined, have a number of tax breaks compared to non-SMEs.

• Revisit special taxation measures• Change tax status of public interest corporations and cooperative

kumiais

8Global Tax Symposium – Asia 2015

PwC

2015 tax reform proposal highlights

9Global Tax Symposium – Asia 2015

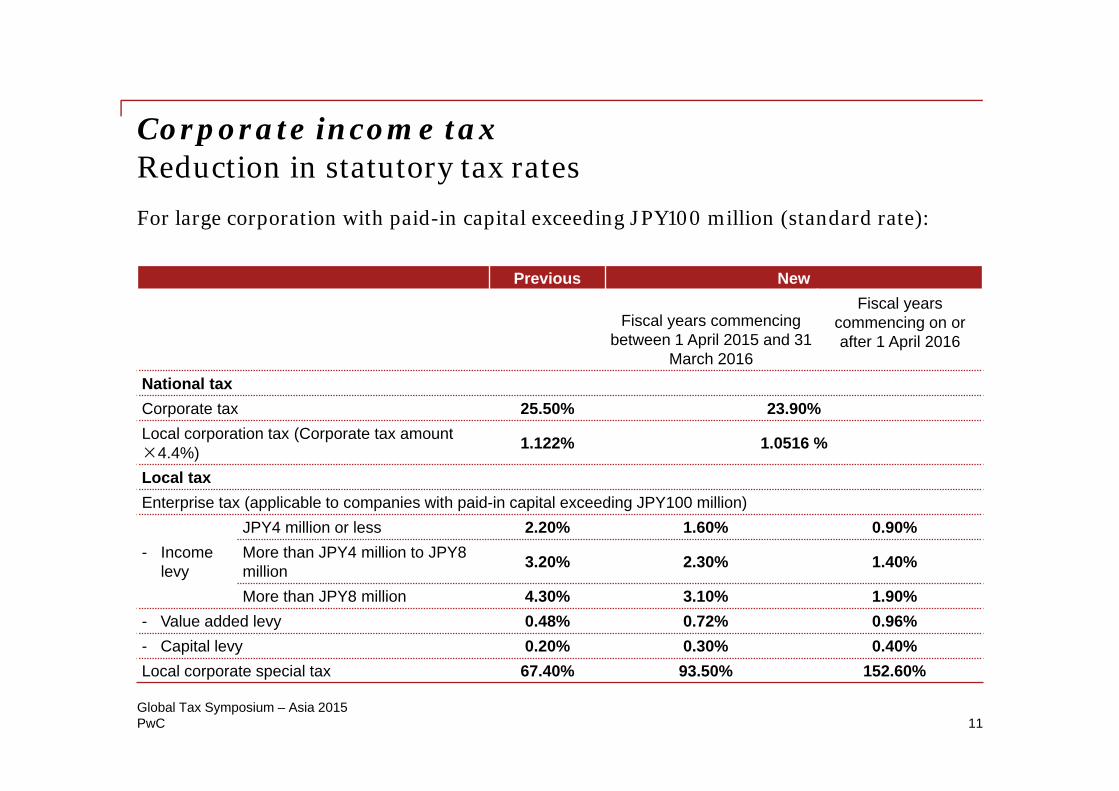

Corporate income tax

PwC

Previous New

Fiscal years commencing between 1 April 2015 and 31

March 2016

Fiscal years commencing on or after 1 April 2016

National taxCorporate tax 25.50% 23.90%Local corporation tax (Corporate tax amount ×4.4%) 1.122% 1.0516 %

Local taxEnterprise tax (applicable to companies with paid-in capital exceeding JPY100 million)

- Income levy

JPY4 million or less 2.20% 1.60% 0.90%More than JPY4 million to JPY8 million 3.20% 2.30% 1.40%

More than JPY8 million 4.30% 3.10% 1.90%- Value added levy 0.48% 0.72% 0.96%- Capital levy 0.20% 0.30% 0.40%Local corporate special tax 67.40% 93.50% 152.60%

For large corporation with paid-in capital exceeding JPY100 million (standard rate):

Corporate income taxReduction in statutory tax rates

11Global Tax Symposium – Asia 2015

PwC

For large corporation with paid-in capital exceeding JPY100 million headquarteredin Tokyo.

Corporate rate reduction

April 2013 April 2014 April 2015

Corporate tax reduced from 30% to 25.5% for fiscal years beginning on or after 1 April 2012

Effective tax rate for March year ends

38.01% 35.64% 33.10%

April 2015April 2014

Plus

Equals

10% tax uplift (25.5% x 10%)

Effective tax rate for December year ends

38.01% 35.64%

January 2015January 2013

New corporation surtax

April 2016

32.34%

33.10%

January 2016

April 2016

40.69%

January 2017

April 2017

32.34%

Corporate tax reduced from 25.5% to 23.9% for fiscal years

beginning on or after 1 April 2015

Corporate income taxReduction in effective corporate tax rate

12Global Tax Symposium – Asia 2015

PwC

Old NewFiscal years beginning

between 1 April 2015 and 31 March 2017

Fiscal years beginning on or after

1 April 2017

Percentage of current year income that may be offset by tax losses

Tax loss carry forward period

80%

9 years

65%

9 years

50%

10 years¹

1. Applicable to tax losses incurred in fiscal years beginning on or after 1 April 2017.

2. Newly established corporations will have seven years from establishment date in which full deduction is allowed, unless listed on a stock exchange.

Corporate income taxLimitation on utilisation of carried forward tax losses

13Global Tax Symposium – Asia 2015

PwC

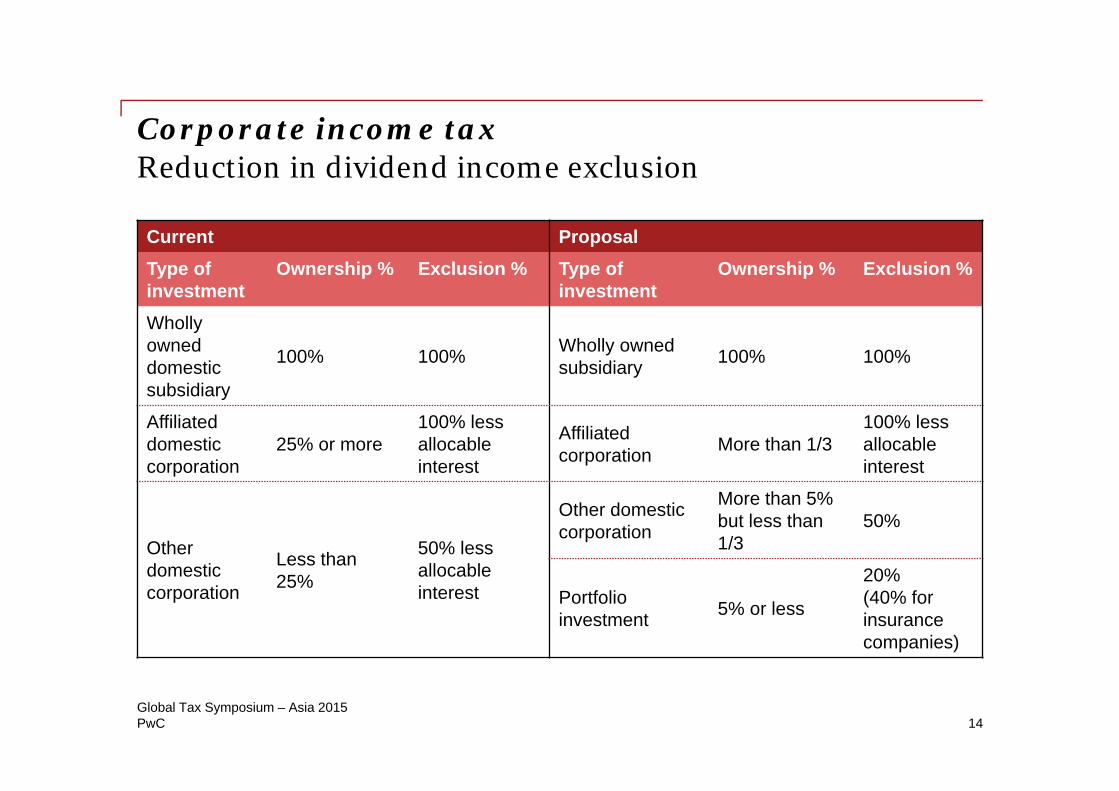

Current ProposalType of investment

Ownership % Exclusion % Type of investment

Ownership % Exclusion %

Wholly owned domestic subsidiary

100% 100% Wholly owned subsidiary 100% 100%

Affiliated domesticcorporation

25% or more100% lessallocable interest

Affiliated corporation More than 1/3

100% less allocable interest

Other domestic corporation

Less than 25%

50% less allocable interest

Other domestic corporation

More than 5% but less than 1/3

50%

Portfolio investment 5% or less

20%(40% for insurance companies)

Corporate income taxReduction in dividend income exclusion

14Global Tax Symposium – Asia 2015

PwC

Special taxation measures should be reviewed and limited to ‘necessary’ tax incentives.

1. Tax incentives which will be allowed to expire

• Investment incentive for increased investment in machinery

• Taxation of an accredited corporation engaged in R&D

• Reduced real estate registration tax upon a corporate bunkatsu (de-merger)

2. Tax incentives to be narrowed

• Rollover relief for newly acquired qualified assets

• Investment incentive granted to SMEs which acquire facilities and equipment for the improvement of operational efficiency

3. Certain high priority incentives to be enhanced

• R&D tax credit

• Reduced corporate tax rate applicable to SMEs (2 year extension)

Corporate income taxChanges to special taxation measures

15Global Tax Symposium – Asia 2015

PwC

Corporate income taxChanges to R&D tax credit

Amendment

High level typeR&D costs over 10% of the sales x creditable rate*

Increased typeIncreased amount of R&D costs x rate of increase (5-30%)

Elect

* (R&D ratio – 10%) X 0.2

Open innovation type tax creditSpecial R&D costs x 20% or 30%**

**Joint R&D with university or public research institution: 30%Joint R&D between corporations: 20%

Note – abolishment of the one year carry over rule

+ Significant increase of creditable rate (currently at 12%)

Creditable limit

10% of corporate tax amount

Total amount tax creditGross R&D costs X 8% to 10%

Note – abolishment of the one year carry over rule

12% of the gross R&D for SME

5% of corporate tax amount

25% of corporate tax amount

A combined credit limit of 30%

Creditable limit

16Global Tax Symposium – Asia 2015

+

PwCGlobal Tax Symposium – Asia 2015

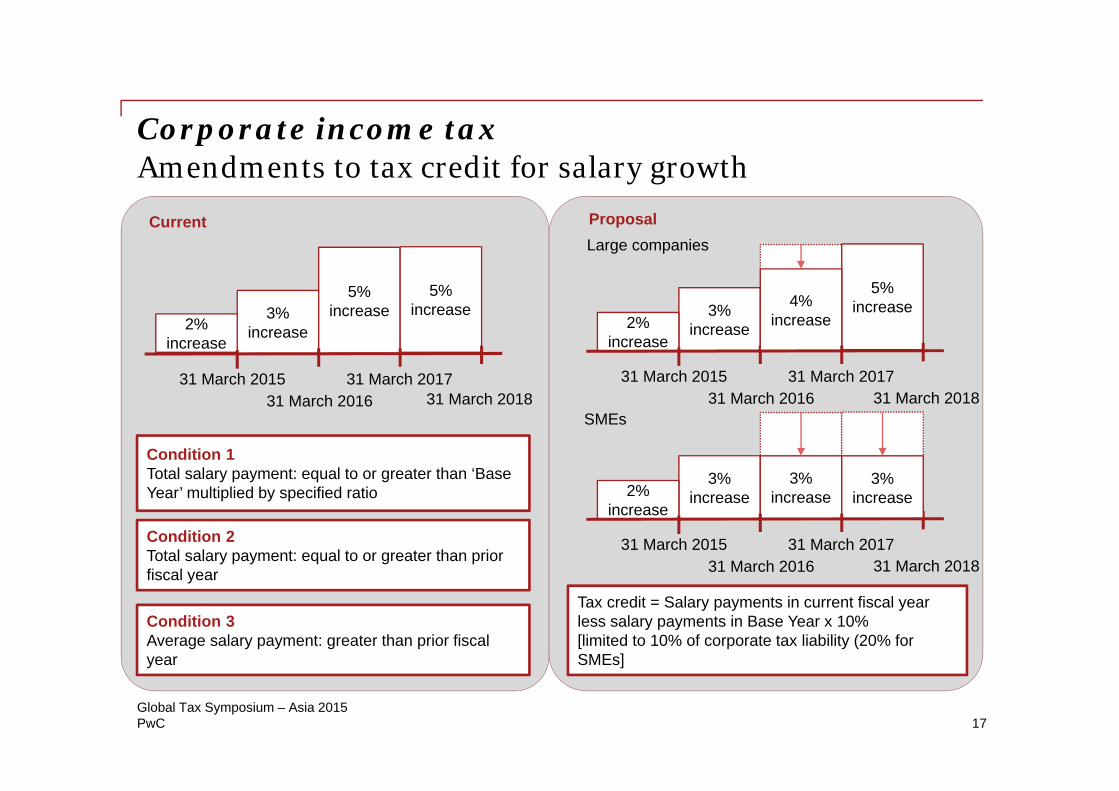

Corporate income taxAmendments to tax credit for salary growth

Tax credit = Salary payments in current fiscal year less salary payments in Base Year x 10%[limited to 10% of corporate tax liability (20% for SMEs]

Condition 1 Total salary payment: equal to or greater than ‘Base Year’ multiplied by specified ratio

Condition 2 Total salary payment: equal to or greater than prior fiscal year

Condition 3 Average salary payment: greater than prior fiscal year

ProposalLarge companies

SMEs

Current

3%increase

5%increase

5%increase

2%increase

31 March 201531 March 2016

31 March 201731 March 2018

3%increase2%

increase

31 March 201531 March 2016

31 March 201731 March 2018

3%increase

5%increase

5%increase

2%increase

31 March 201531 March 2016

31 March 201731 March 2018

4%increase

3%increase

3%increase

17

PwC

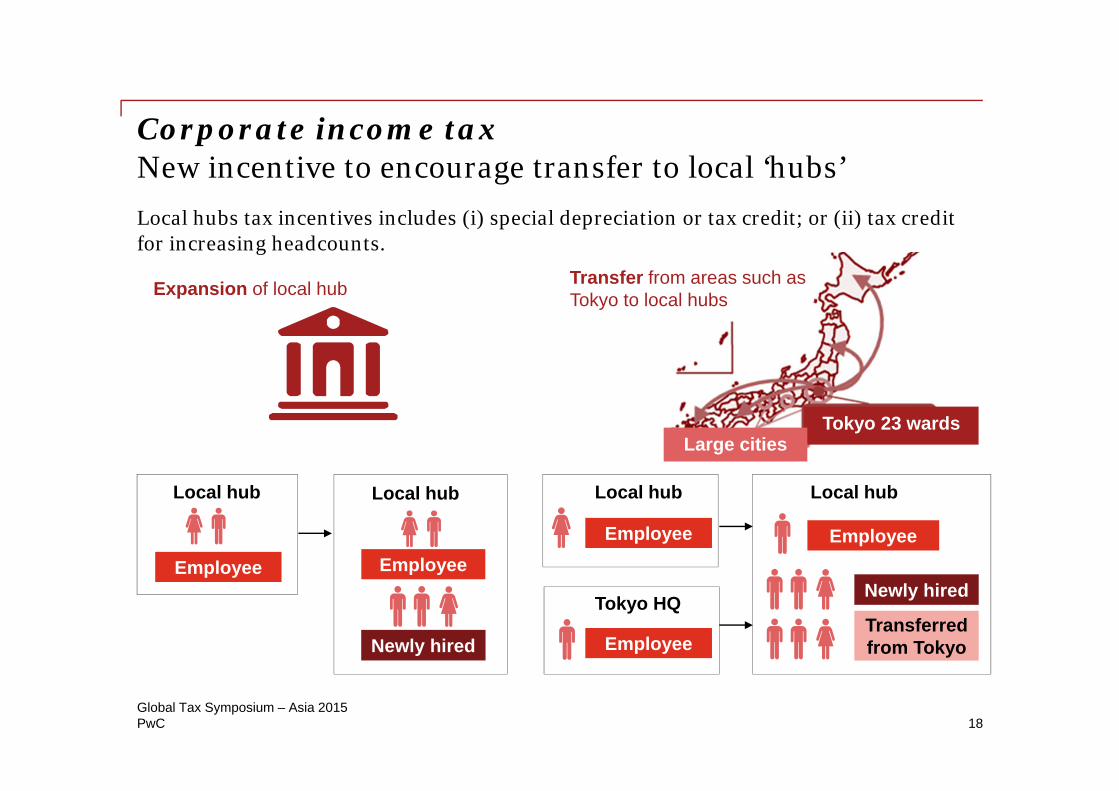

Corporate income taxNew incentive to encourage transfer to local ‘hubs’Local hubs tax incentives includes (i) special depreciation or tax credit; or (ii) tax credit for increasing headcounts.

Tokyo 23 wardsLarge cities

Local hub

Employee

Local hub

Employee

Newly hired

Local hub

Employee

Newly hired

Transferredfrom Tokyo

Local hub

Employee

Tokyo HQ

Employee

Expansion of local hub Transfer from areas such as Tokyo to local hubs

18Global Tax Symposium – Asia 2015

International tax

PwC

International taxEliminate dividend income exclusion for ‘hybrid’ financial instruments

20

Based upon the recommendation of BEPS Action Plan 2, the dividend received by a Japanese corporation from a foreign affiliate would be excluded from the dividend exclusion regime.

Japanese parent Foreign affiliate

Dividend exclusion

Equity

Dividend 60

Retainedearnings

32Corporate tax

8

Deductible dividend

Taxable income 40

Dividend 60

Deductibledividend

57

Non-deductibleDividend*

3

Dividend

No double taxation

Corporate tax rate at 30%**Tax cost in Japan is 0.9

(= 3 X 30%)

* Exclude from income tax calculation as expenses for receiving the dividend.** For simplicity, the corporate tax rate is 30% in the current case.

Corporate tax rate at 20%, withholding tax at 0%, domestic tax cost is 8

(= 40 X 20%)

Total tax cost is 8.9

Ordinary dividend

Foreign affiliate

Dividend 60

Retainedearnings

20Corporate tax

20

Corporate tax rate at 20%, withholding tax at 0%,

domestic tax cost is 20 (= 100 X 20%)

Total tax cost is 20.9

Global Tax Symposium – Asia 2015

PwC

International taxChanges to the controlled foreign corporation tax regime

• The changes proposed by the 2015 Tax Reform Proposal under the controlled foreign corporation (CFC) tax regime are as follows:

1. The trigger rate changed from ‘20% or less’ to ‘less than 20%’

2. Expand scope of holding companies

3. Relaxation of tax return filing requirements; and

4. Changes related to the amounts subject to tax related to tax deductible dividends from foreign corporation.

• The proposed changes in the trigger rate, the treatment of foreign holding companies, and the relaxation in the filing requirements will apply for foreign affiliates whose tax years begin on or after 1 April 2015.

• The proposed changes related to the definition (i.e. taxable income – including deductible dividends) will have an effective date of 1 April 2016 (with some grandfathering).

21Global Tax Symposium – Asia 2015

PwC

International taxChanges to the controlled foreign corporation tax regime

Resident/domesticcompany

Resident/domesticcompany

Specially related party (corporation/Individual)

Familyshareholdersgroup

Resident/ domestic company hold more than 50% (directly or indirectly)

Foreign affiliates

Foreign affiliates located in a jurisdiction with effective tax rate of 20% or less

Scope of taxable person(i) Resident or domestic corporate shareholder that owns, directly or indirectly, 10% or more equity interest (ii) Resident or domestic corporate shareholder as part of a family shareholder group that owns, directly or indirectly 10% or more equity interest

Specified foreign subsidiaries

Outside of CFC scope

Active business exemption

(corresponding to change in business form)

All conditions must be met1. Business Purpose TestThe main business should not be holding equity securities(excluding regional headquarter company whose main business is to hold the shares in the controlled company

Reform of business test for regional headquarter company, controlled corporation, holding corporation

Reform

Change the triggering tax rate from ‘20% or less’ to ‘less than 20%’

Reform2. Substance TestA place necessary to conduct its main business in the country where its head office is located

3. Admin & Control TestManages and controls its main business in the country where its head or main office is located

4. Local Country Test (for those industries other than 7 types referred to below)

Conducts its business mainly in the country where its head or main business is located

Unrelated Party Test (7 types of industry including wholesale)The corporation would be considered to conduct its business mainly with third parties if its conducts business with parties other than related party (capital relationship of more than 50%) (exclude transaction between a regional headquarter company, with wholesale as its main business, and its controlled subsidiaries)

ReformTransactions between regional headquarter company (with wholesale business as its main business) and its controlled Japanese subsidiary are considered to be with a related party

Aggregate income of sub

Fail to meet

Exempt

With investment income

No investment income

Aggregate investment income

No income aggregated

ReformRelaxation in the filing requirements

Meet all conditions

Global Tax Symposium – Asia 201522

PwC

International taxIntroduction of authorised OECD approachAOA Principles• Align Japanese domestic rules with 2010 version of OECD Model Tax Convention, which

attributes income to a PE using the ‘functionally separate approach’.

• Effect of change is that income attributable to a PE will be calculated based on functional and factual analysis of the PE by (i) allocating assets, risks and capital to the PE and (ii) recognising intra-entity dealings as if the PE were a separate enterprise.

• Definition of domestic source income will change to include income attributable to a PE, while income of the foreign entity not attributable to the PE will be excluded.

Current AOA

Principle Entire method Attribution method

Taxable domestic source income

All domestic source income of a foreign corporation with a PE is subject to Japanese corporate tax

1. Business (attributable) income of a PE2. Non-attributable income will be treated in

the same way as current taxation of a foreign corporation without a PE in Japan

23Global Tax Symposium – Asia 2015

PwC

2015 Tax Reform Proposal

• It will be clarified that interest received by a foreign corporation without Japanese branch related to accounts receivable for goods or services outstanding for less than 6 months will not be subject to corporation tax in Japan.

• Any Japan real estate owned by the head office of a foreign company with a PE in Japan shall be considered to have been transferred to the Japanese PE at the book value of the asset in the hands of the head office.

• In calculating the foreign tax credit for a Japanese company, rules will be issued to clarify the amount of foreign source income attributable to a foreign branch. Further, the amount of foreign taxes attributable to the foreign branches will be in a separate ‘basket’ for foreign tax credit calculation purposes.

International taxChanges to the ‘Attribution of Income’ method for a permanent establishment

Attribution Method (Standard)(attributable income of a PE)

Japan source

business income

Offshore Corporation (Headquarter)

OffshoreJapan

Third Country

Withholdableincome from

Third Country

Japan withholdable income not

attributable to Japan Branch

(Note 1, 2)

Japan Branch(PE)

Inter-company transaction recognised

Attributable to Japan Branch Attributable to

headquarter

Foreign tax credit available to

Japan Branch

Subject to filing

Subject to filing

Attributable to Japan Branch

Note 1 Headquarter invested in Japan directly (not through Japan Branch)Note 2 In general, withholding tax would be final tax (i.e., no further tax).

24Global Tax Symposium – Asia 2015

Consumption tax

PwC

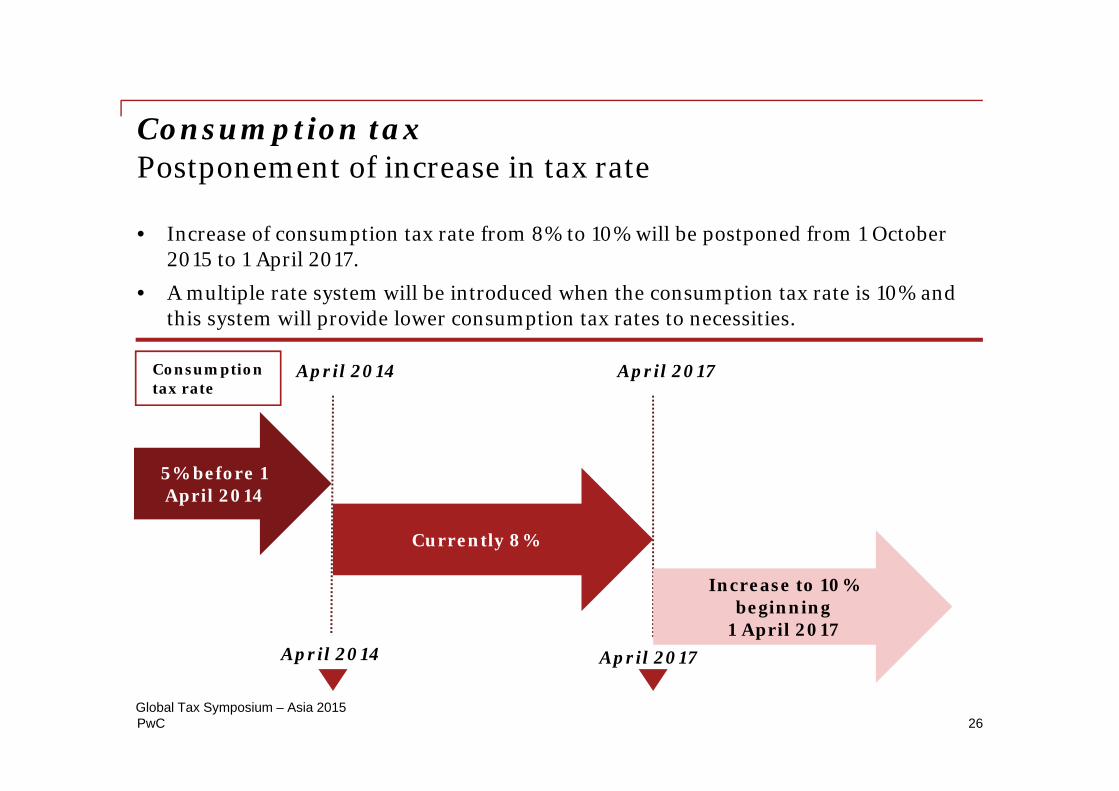

Consumption taxPostponement of increase in tax rate

• Increase of consumption tax rate from 8% to 10% will be postponed from 1 October 2015 to 1 April 2017.

• A multiple rate system will be introduced when the consumption tax rate is 10% and this system will provide lower consumption tax rates to necessities.

Consumption tax rate

April 2014 April 2017

April 2017

Currently 8%

April 2014

Increase to 10% beginning

1 April 2017

5% before 1 April 2014

26Global Tax Symposium – Asia 2015

PwC

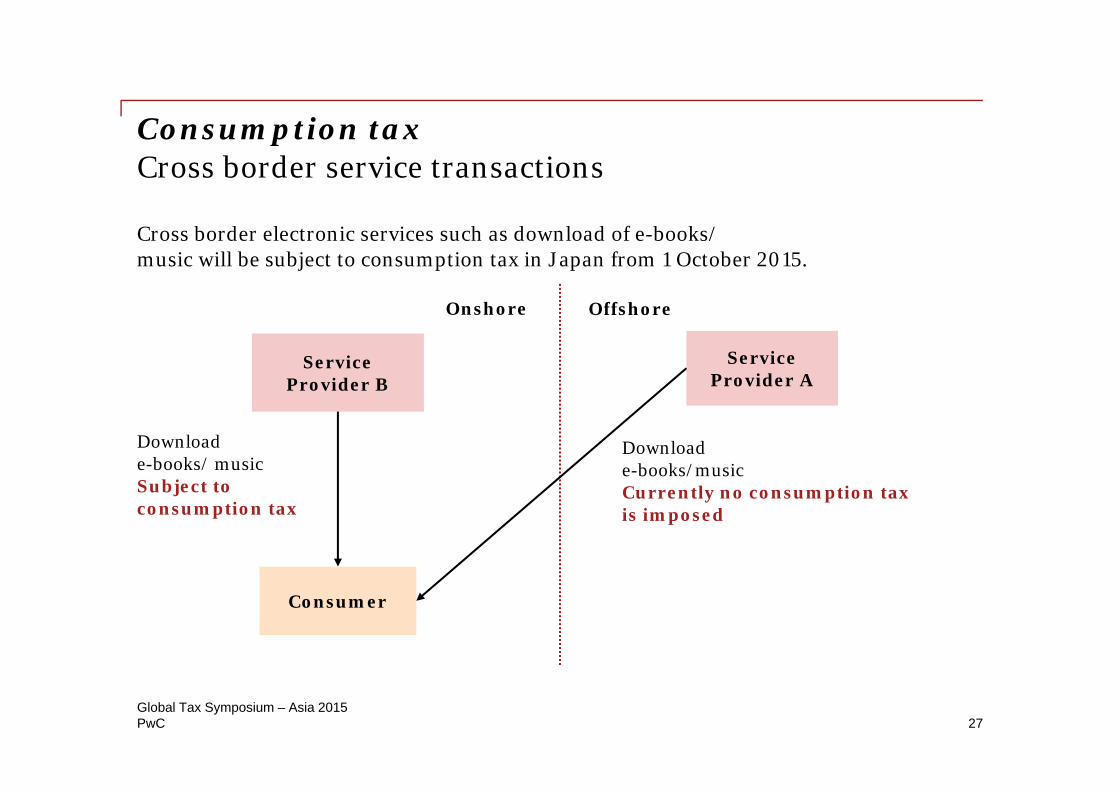

Consumption tax Cross border service transactions

Cross border electronic services such as download of e-books/music will be subject to consumption tax in Japan from 1 October 2015.

OffshoreOnshore

Service Provider A

Consumer

Service Provider B

Download e-books/ musicSubject to consumption tax

Download e-books/musicCurrently no consumption tax is imposed

27Global Tax Symposium – Asia 2015

PwC

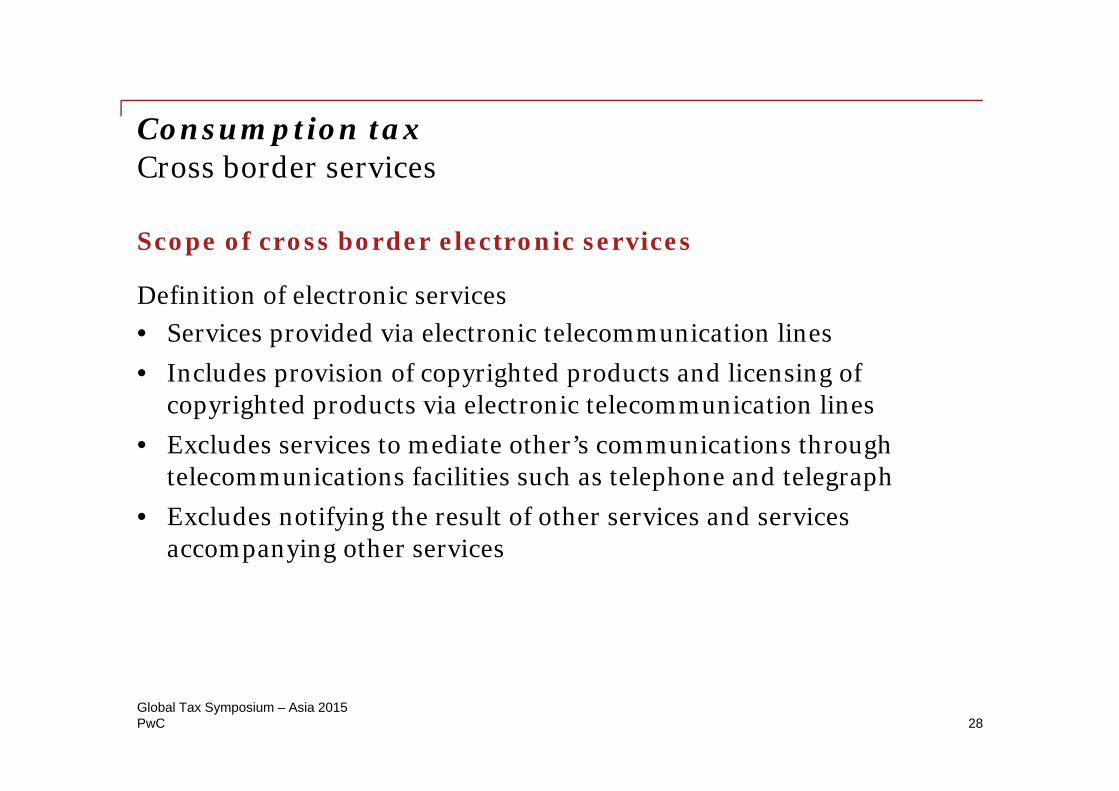

Consumption taxCross border services

Scope of cross border electronic services

Definition of electronic services• Services provided via electronic telecommunication lines• Includes provision of copyrighted products and licensing of

copyrighted products via electronic telecommunication lines• Excludes services to mediate other’s communications through

telecommunications facilities such as telephone and telegraph• Excludes notifying the result of other services and services

accompanying other services

28Global Tax Symposium – Asia 2015

PwC

Consumption tax Cross border services

• Service Provider A will collect consumption tax from Consumer. Service Provider A will file consumption tax return with the tax office and pay the tax.

• If business purchases the services, no input consumption tax credit is available, unless Service Provider A is a registered foreign service provider.

• The registration of foreign service provider will start from 1 July 2015.

Electronic services to consumers (B2C)

OffshoreOnshore

Service Provider A

Consumer(or business)

Electronic service

Tax Office

Tax filing and payment

29Global Tax Symposium – Asia 2015

PwC

Electronic services to business (B2B) Reverse charge mechanism

OffshoreOnshore

Service Provider ACompany B

Tax filing and payment

Input tax credit

Tax Office

Consumption tax Cross border services

• Service Provider A will not collect consumption tax. Company B will report the consumption tax and pay the tax. Company B may claim input consumption tax credit on the purchase. (Reverse Charge Mechanism)

• Service Provider A should notify Company B that the transaction is subject to the reverse charge.

• If the taxable sales ratio of Company B is 95% or more, no reporting is required for the time being.

• Electronic service will be B2B if it is clear from the nature or conditions of the services that the recipient is a business.

Electronic service

30Global Tax Symposium – Asia 2015

PwC

For provision of services such as performing arts and sports attractions in Japan by foreign entertainment providers, the Japanese sponsor will be subject to Japanese consumption tax via the reverse charge system from 1 October 2016.

Consumption tax Performing arts and sports attractions by foreign entertainment providers

Foreignentertainment

provider

Domestic sponsor

Receives revenue, net of consumption tax, from domestic business operator for provision of performing arts and sports attractions in Japan

Subject to consumption tax under the reverse charge system

31Global Tax Symposium – Asia 2015

Individual tax –Exit tax

PwC

Individual tax – exit tax

• The 2015 Tax Reform Proposals introduced a new exit tax for certain individuals leaving Japan.

• At the time of the exit, the individual will be subject to tax on gains on securities and derivative transactions as if the individual sold or settled the transactions at fair market value.

• The new rule will be applicable to exits and donations and inheritances of property made by a Japanese residents on or after 1 July 2015.

Global Tax Symposium – Asia 201533

PwC

Individual tax – exit tax (cont’d)

Proposed Rules

Taxpayer The resident would be subject to this tax if both of the following conditions are met:1. Value of assets subject to taxation at the time of the exit is JPY100 million or more; and2. Within 10 years of exit, the individual has been a Japanese resident for more than 5 years. For foreign nationals, the five out the last ten years ‘clock’ does not start until July 1, 2015. Time living in Japan under a visa status under ‘Table 1’ of the Immigration Control Law is not included (e.g. specialists in the humanities or international services, intra-company transferee, temporary visitor, etc.)

Assets subject to exit taxation

Securities as defined in the individual tax law, ownership of tokumei kumiai contracts and unsettled derivative transactions, credit transactions and hedging transactions of stock risks trading

Filing requirements for tax report

By the due date of the final tax return to be filed by a registered agent of the taxpayer (valuation date is the exit date); ORIn a ‘short period’ tax return which is due upon exit (if no tax agent is appointed) (valuation date is 3 months prior to the expected exit date)

Rescission of taxation by return to Japan within 5 years

If the taxpayer returns to Japan within 5 years of exit and retains assets continuously from the date of exit, taxation of such assets will be cancelled upon filing by the taxpayer within 4 months of the return date.

Transfer by donation or inheritance to a non-resident

Donor is deemed to sell or settle the derivative or transfer the securities on the date of transfer for purposes of the tax return filing.

34Global Tax Symposium – Asia 2015

PwC

Update on tax treaties

35Global Tax Symposium – Asia 2015

PwC

1. Japan-Oman Tax Treaty

2. Japan-UK Tax Treaty

Dividend Interest Royalties

New Convention 5% (shareholding of 10%)*10% (in all other cases)

10%Exemption (governmental or financial institution)

10%

Dividend Interest Royalties

Amended Convention 0% (shareholding of 10%)*10% (in all other cases)

Exempt in principle Out of scope

*If a dividend is tax deductible by a payer company, a 10% tax rate is applied.

Update on tax treaties

36Global Tax Symposium – Asia 2015

PwC

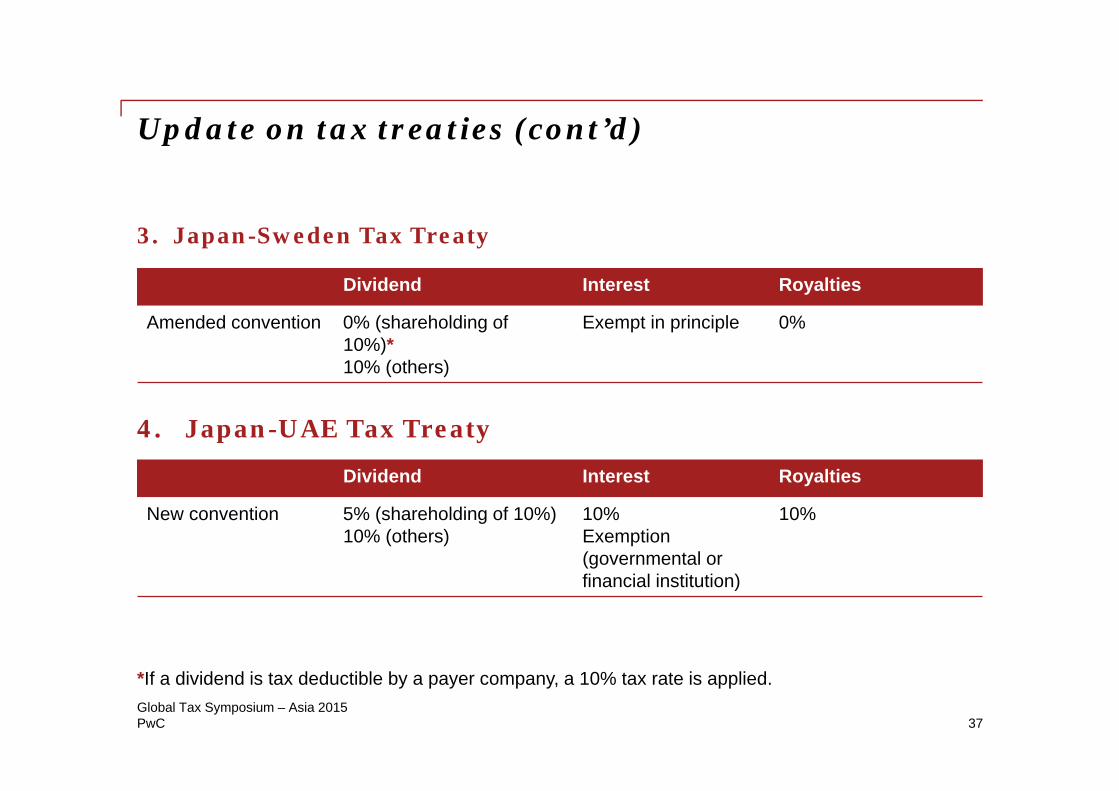

3. Japan-Sweden Tax Treaty

Dividend Interest Royalties

Amended convention 0% (shareholding of10%)*10% (others)

Exempt in principle 0%

*If a dividend is tax deductible by a payer company, a 10% tax rate is applied.

Dividend Interest Royalties

New convention 5% (shareholding of 10%)10% (others)

10%Exemption (governmental or financial institution)

10%

4. Japan-UAE Tax Treaty

Update on tax treaties (cont’d)

37Global Tax Symposium – Asia 2015

PwC

5. Japan-US Tax Treaty*

Dividend Interest Royalties

Protocol 0% (shareholding of at least 50%)**

Nil -

*Introduction of arbitration procedures.**Not applicable if a dividend is tax deductible by a payer company.

Update on tax treaties (cont’d)

38Global Tax Symposium – Asia 2015

PwC

Q&A

39Global Tax Symposium – Asia 2015

PwC

Contact us

Jack Bird

Partner, PwC Japan

+ 81 3 5251-2577

Yoko Kawasaki

Partner, PwC Japan

+ 81 3 5251-2450

40Global Tax Symposium – Asia 2015

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other professional advice or service by PricewaterhouseCoopers Ltd. ("PwC"). PwC has no obligation to update the information as law and practices change. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in May 2015 and were based on the law enforceable and information available at that time.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

![Volunteer Income Tax Assistance “VITA” Earned Income Tax ... · Volunteer Income Tax Assistance “VITA” Earned Income Tax Credit “EITC” Revised 1/28/19 [DOCUMENT TITLE]](https://cdn.vdocuments.mx/doc/165x107/5fa5a5c85aa0bb13122ce462/volunteer-income-tax-assistance-aoevitaa-earned-income-tax-volunteer-income.jpg)