Download - Investment Opportunity Study

Project Description Report (In conjunction with Main Report)

Department of Industry

Ministry of Economic Affairs

Investment Opportunity Study

2020

Consulting Assignment Background This study titled “Investment Opportunity in Bhutan” was carried out by APECS Consultancy. The assignment was

awarded vide work order No. MoEA/DoI/IDD-13(a)/2019-2020/669 dated 27th January 2020. The assignment was for a

period of 5 months.

Consulting Team

Rohit Adhikari, Team Leader

Novin Darlami, Policy Expert

HN Adhikari, Quality Infrastructure Expert

BN Bhattarai, Supply/Value Chain Expert

Bishnulal Gurung, Financial Expert

Sangay Gyeltshen, GIS and Data Management Expert

Tandin Dorji, Business Analyst

Tashi Dorji, Editor

Official Counterpart and Technical Reviewer/Adviser:

Copyright

Industrial Development Division, Department of Industry, MoEA.

Suggested Citation

Department of Industry (2020). Investment Opportunity Study Bhutan 2020. Thimphu, Bhutan.

Disclaimer

Various statements contained in this document, including those that express a belief, expectation or intention, as well

as those that are not statements of historical fact, are forward-looking statements. The forward-looking statements

have been based on the current expectations and assumptions about future events. These assumptions include,

among others, analysis of operating industries, resources inventory, market trends and demand, investment

opportunities, financial projections.

While it is considered that these expectations and assumptions to be reasonably true, they are inherently subject to

significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which

are difficult to predict and the actual results with regard to investment opportunities could differ.

This information is not offered as legal or any other advice on any particular matter. The Department and contributing

authors expressly disclaim all liability to any person in respect of anything, and in respect of the consequences of

anything, done or omitted to be done wholly or partly in reliance upon the whole or any part of the contents. No

reader should act or refrain from acting on the basis of any matter contained in this report without first seeking the

appropriate legal or other professional advice on the particular facts and circumstances.

Tashi Dorji (Mr.)

Chief Industries Officer

Dakpa Gyeltsen (Mr.)

Senior Industries Officer

Industrial Development Division

Department of Industry, MoEA

Page | i

Preface

Industrial development is key for

expansion of the economy, creation of

employment opportunities, value addition

to resources and revenue generation

among others. Towards promoting

industrial development, relevant policies

have been realigned and specific programs

such as CSI Flagship Development Program

and development of business infrastructure

are being taken up. To complement the

various programmes that are being

undertaken to foster economic

diversification, the current study was

proposed.

Considering the current

availability of resources and the business

development environment in the country,

this study had become imperative. Further,

the investment opportunities have

considerably changed over the period of

time due to advancement in technology,

methods of production and availability of

resources. This study takes stock of the

resources, assesses business potential and

identifies project ideas to stimulate

investment in the country.

The study is expected to provide

comprehensive information on business

opportunities in the country with the aim to

guide and encourage prospective investors

to take up business activities. The study

contains list of potential activities that

investors could further explore and take up.

The findings of the study will also serve as

a basis for policy recommendations to

promote industrial development.

Jiten Bansal

Retrieved from:

https://www.tripoto.com/trip/my-solo-trek-to-tiger-s-nest-or-paro-taktsang-5965efd268442

Investment Opportunity Study 2020

Page | ii

Acknowledgements

APECS Consultancy would like to

thank the Department of Industry for selecting

the firm to carry out this study. The firm thanks

the Director General, Officiating Director

General, the Specialist of DoI, industry officers

from Industrial Planning and Coordination

Division, Company Registration Division,

Foreign Direct Investment Division, Industrial

Infrastructure Development Division and

Environment Unit for their valuable comments

and suggestions. Further, the Chief Industries

Officer and Project Focal from the executing

agency, the Industrial Development Division,

continuously rendered their support in

procuring relevant data, facilitating meetings

and reviewing the reports; the firm is very

thankful for their support.

The consulting team is also grateful

for all the inputs received from various

business establishments as well as other

government and non-government agencies

who provided us their valuable time, shared

expert opinion and knowledge on investment

climate and opportunities in the country.

Page | iii

Abbreviations

Abbreviation Definition

ADB Asian Development Bank

ADO Asian Development Outlook

BCAA Bhutan Civil Aviation Authority

BDBL Bhutan Development Bank Limited

BHU Basic Health Unit

BICMA Bhutan InfoComm and Media Authority

BLDCL Bhutan Livestock Development Corporation Limited

BTBP Bhutan Telecommunications and Broadband Policy

CBR Crude Birth Rate

CF Community Forest

CFT Cubic Feet

COTI Countries Other Than India

CSI Cottage and Small Industries

CSO Civil Society Organization

DCCL Dungsam Cement Corporation Limited

DGPC Druk Green Power Corporation

DOAT Department of Air Transport

DoFPS Department of Forest and Park Services

EA Economic Activity

ECCD Early Childhood Care and Development

EDP Economic Development Policy

FAO Food and Agriculture Organization

FDI Foreign Direct Investment

FMU Forest Management Unit

FTA Free Trade Agreement

FYP Five Year Plan

G2C Government to Citizen

GDP Gross Domestic Product

GNHCS Gross National Happiness Commission Secretariat

GST Goods and Service Tax

HEP Hydro Electric Plant

HSS Higher Secondary School

ICT Information and Communication Technology

IOS Investment Opportunity Study

ISIC International Standard for Industrial Classification

ISP Internet Service Provider

ITC International Trade Centre

JDWNRH Jigme Dorji Wangchuck National Referral Hospital

KG Kilogram

LDC Least Developed Country

LSS Lower Secondary School

LULC Land Use and Land Cover

M&L Medium and Large

MoAF Ministry of Agriculture and Forest

MoEA Ministry of Economic Affairs

MoH Ministry of Health

MSE Micro and Small Enterprise

MSO Multi-Service Operator

Investment Opportunity Study 2020

Page | iv

Abbreviation Definition

MSS Middle Secondary School

M2 Metre Square

MT Metric Tones

NEC National Environment Commission

n.e.c. Not Elsewhere Classified

NFI National Forest Inventory

NFIS National Financial Inclusion Strategy

NICS National Industrial Classification System of India

NPL Non-Performing Loans

NPV Net Present Value

NRDCL Natural Resources Development Corporation Limited

NWFP Non-wood Forest Product

P&M Production and Manufacturing

PA Protected Area

PHCB Population Housing and Census of Bhutan

PHPA Punatsangchhu Hydroelectric Project Authority

PNH Primary National Highway

PPP Purchasing Power Parity

PPP Public Private Partnerships

PS Primary School

RGoB Royal Government of Bhutan

RICBL Royal Insurance Corporation of Bhutan Ltd.

RMA Royal Monetary Authority

S&C Small and Cottage

SAARC South Asian Association for Regional Corporation

SDG Sustainable Development Goals

SNH Secondary National Highway

SoE State Owned Enterprise

SWOT Strength, Weakness, Threats and Opportunities

TFR Total Fertility Rate

ToR Terms of Reference

UNCTAD United Nation Conference on Trade and Development

UNESCAP United Nation Economic and Social Commission for Asia and the Pacific

WGI Worldwide Governance Indicators

Page | v

Conversions and Units

Currency

1 USD= 76.1 Ngultrum (June 2020)

1 Pound sterling= 94.17 Ngultrum (June 2020)

1 INR= 1 Ngultrum

Measurements

m= metre

ft. = feet

Sq. m= Square meter

Cu. m= Cubic meter

C. ft= Cubic feet

Sq. ft= Square feet

Kg= kilogram

lbs= Pounds

kw= kilowatt

1 m= 3.28 foot

1 Sq. m= 10.76 Sq. ft

1 Decimal= 435.6 Sq. ft

1 kg= 2.20 lbs

Investment Opportunity Study 2020

Page | vi

Contents

Preface……………………………………………………………………………………………………………………….i

Acknowledgement…………………………………………………………………………………………………….ii

Abbreviation……………………………………………………………………………………………………………..iii

Conversion and Units………………………………………………………………………………………………..v

Executive Summary…………………………………………………………………………………………………..vii

Methodology…………………………………………………………………………………………………………….ix

1. Manufacturing of Beauty Care Products ............................................................................... 3

2. Manufacturing of Mouth freshener ....................................................................................... 27

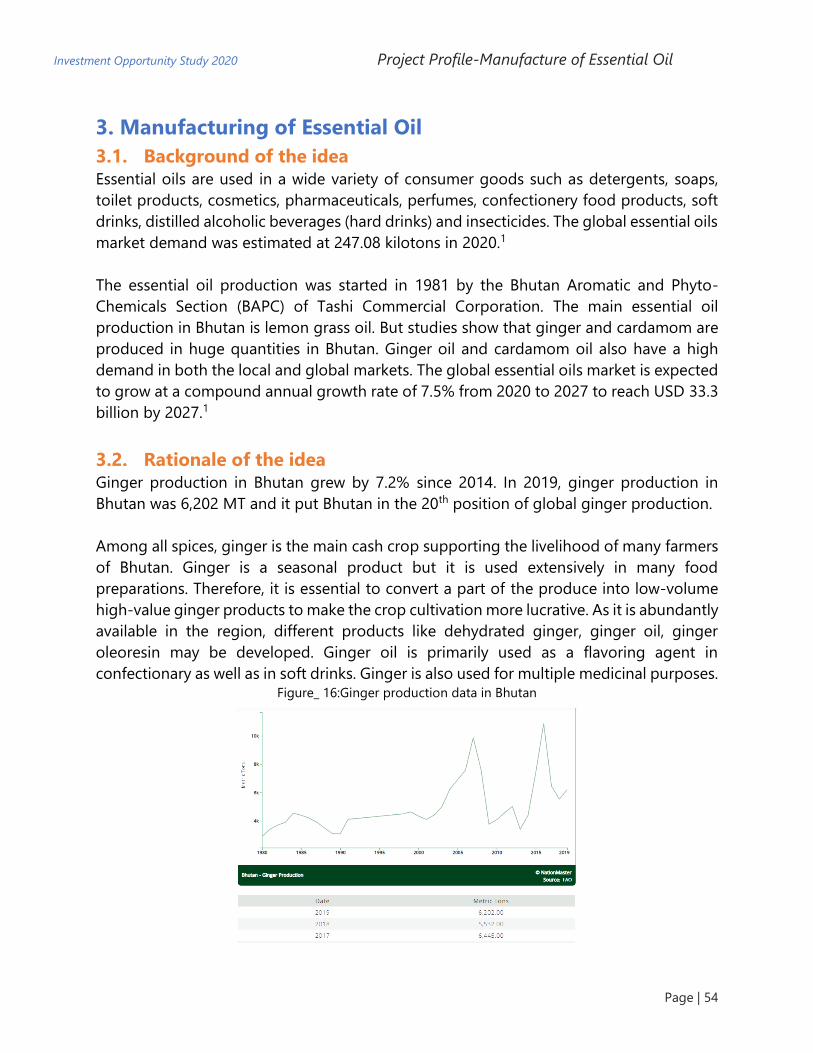

3. Manufacturing of Essential Oil ................................................................................................ 54

4. Manufacturing of Gypsum Board/Panel .............................................................................. 81

5. Manufacturing of Chewing Gum ......................................................................................... 104

6. Manufacturing of Corrugated Paper Board Containers ............................................. 112

7. Manufacturing of Bamboo Toothpick and Ear Buds .................................................... 120

8. Manufacturing of Bio-Liquid and Talc Based Fertilizers ............................................. 128

9. Manufacturing of Prefabricated Wooden Building Components............................ 139

10. Manufacturing of Packaging Aluminium Foil .............................................................. 149

11. Hydroponic Farming ……………………………………………………………………………………….156

12. High Tech Geophysical and Mining Exploration Services ……………………………….179

13. Multi-product Kiosks Services………………………………………………………………………. .209

14. Car Detailing and Resell…………………………………………………………………………………...227

15. Financial Consulting for Investments and Market Research ……………………………236

16. Domestic Tourism Company…………………………………………………………………………….243

17. Outdoor Sporting Organizer…………………………………………………………………………….253

18. Childcare Agency for Children under 3 years……………………………………………………258

19. Branding and Marketing Intermediary Services………………………………………………..268

Page | vii

Executive Summary This report is on Investment Opportunity Study for Bhutan. The study comprises of

analysing the existing economic activities and business establishments, reviewing

available resources in the country under various domains, assessing the 12th Five Year

Plan to incorporate major new developments, identifying the surplus resources for

utilization, analysing accessibility for resources, identification of possible opportunities

under various sub-sectors and in different parts of the country and providing a list of

potential industries under manufacturing and service sectors.

Rationale for the Assignment

The current assignment is an offspring of the statements from the Economic

Development Policy 2016. Few relevant clauses of the Policy are outlined below:

7.3.1 The MoEA shall continue to create an enabling environment by

adopting policies and regulations for promotion of investments in the

country.

7.3.18 National Resource Inventories shall be updated periodically beginning

from 2018 and made available to prospective entrepreneurs to enable

identification of areas of opportunities for investment.

7.3.19 The MoEA shall identify scope of subcontracting/outsourcing

opportunities by large and medium industries to small and cottage

industries and initiate such business linkages and partnerships by 2018.

Objective

The objective of the study is to review national resources and prepare a report on

investment opportunities in the country.

Due to technical issues with regard to report binding, the consultants had to print the

report as two documents. This second document, titled ‘Project Descriptions’ and

contains descriptions of potential investment ideas under Production &

Manufacturing, and Service sector. The background and rationale, market outlook,

equipment and resources requirements, and financial analysis are presented for the

projects.

The first document, titled ‘Main Report’ is to be read in conjunction with this report. It

contains the following Chapters:

Chapter 1: The first chapter describes Bhutan with regard to geography, population,

economy and trade. It is a brief introduction to set the context for this report.

Chapter 2: This chapter describes the operating business establishments in Bhutan as

of March 2020. Based on the data obtained from Department of Industry and

Department of Cottage and Small Industry, a detailed analysis based on the investment

size and classification as per International Standard for Industrial Classification (ISIC)

Investment Opportunity Study 2020

Page | viii

version 3.1 has been prepared. Apart from the description on these two categories, a

separate compendium of all the 280 economic activities Bhutanese establishments are

currently engaged in has also been prepared as a stand-alone document.

Chapter 3: This chapter describes the resources available in Bhutan under the various

topic of Agriculture, Horticulture, Livestock, Forest based products, Minerals,

Education, Health and other infrastructure. Wherever applicable, forecasts have been

made on the growth considering the projections made in the 12th Five Year Plan

document. For resources that were not covered in the document, projection is based

on historical data.

Chapter 4: This chapter is in continuation to the resource inventory and analyses the

availability, consumption and surplus with review of 12th Five Year Plan and salient

features that could result in enhanced connectivity, accessibility and production.

Chapter 5: This chapter presents a detailed Strength, Weakness, Threats and

Opportunities (SWOT) analysis of Bhutan in relation to investment climate and

resources. Comparisons have been made with SAARC countries, lower-middle income

countries and land locked lower middle-income countries where applicable.

Chapter 6: This chapter encompasses the review of relevant policies that impacts

trade and investment in the country to identify possible conflicts and gaps that could

affect investors’ confidence. Recommendations are provided along with the review.

Chapter 7: This chapter assesses investment opportunities under ten sectors of Agro,

Forest, Mineral, ICT and other professional services, Hospitality, Education and Health,

Transport and Logistics, Construction, Finance and Insurance and Energy. The

investment ideas are also accompanied by recommended Dzongkhags for its

establishment.

An action plan for preparation of detailed project reports for these ideas is also

attached.

Page | ix

Methodology In economics literature, there is no universally accepted methodology or tool to be

used for a study of this nature and scope. At the heart of it, it is a scoping study: a

method used to comprehensively map evidence across a range of study designs in an

area, with the aim of informing future research practice, programs and policy.

Several authors such as Myers (1977), Smith and Watts refer investment opportunity

set (or IOS) as the component of firm value resulting from options to make future

investments. Typically, the study on a particular investment opportunity is carried out

by firms for product or the firm diversification while this study has been carried out at

a larger scale i.e. at a national level and information has been considered accordingly.

This study employed reference from various sources of similar nature in order to select

the most appropriate methodology some of which are mentioned in table below:

Sl.

No

Title Country Author Retrieved from

1. Investment

Opportunity Study

Bhutan 2006

Bhutan Ministry of Economic

Affairs, RGoB

https://www.moea.gov.bt/wp-

content/uploads/2017/07/Ch

apters-C-F_Vol_I.pdf

2. Understanding the

Investment Potential

of the Bangladesh

Diaspora

Bangladesh Commonwealth

Secretariat, UK

https://thecommonwealth.org

/sites/default/files/inline/Und

erstanding%20the%20Invest

ment%20Potential%20of%20t

he%20Bangladesh%20Diaspo

ra.pdf

3. Climate Investment

Opportunities in

Cities - 2018

East Asia and the Pacific,

South Asia, Europe and

Central Asia, Middle East

and North Africa, Sub-

Saharan Africa, and Latin

America and the

Caribbean

International Finance

Corporation

http://www.njtod.org/climate-

investment-opportunities-in-

cities/

4. Investment Climate

Assessment

Bhutan World Bank http://siteresources.worldban

k.org/BHUTANEXTN/Resourc

es/306148-

1288813971336/BhutanICAVo

lume1.pdf

5. Investment Guide

Study

Bhutan UNCTAD https://theiguides.org/guides

/bhutan.pdf

6. Investment

opportunity study for

Ethiopia, Kenya,

Mozambique and

Zambia

Ethiopia, Kenya,

Mozambique and Zambia

International Trade

Centre (ITC)

http://www.intracen.org/uplo

adedFiles/intracenorg/Conten

t/Redesign/Projects/PIGA/PIG

A_Investment%20opportunity

%20study_final.pdf

7. Nepal: Market Study

Identifying Foreign

Direct Investment

Opportunities in

Nepal

Nepal Ministry of Foreign

Affairs, The

Netherlands

https://www.rvo.nl/sites/defa

ult/files/2018/10/Nepal-

Market-Study.pdf

Investment Opportunity Study 2020

Page | x

Framework

This study employs a methodology of desk research and field surveys. The desk

research was carried out through review and analysis of the data from published

sources and government database. After thorough research and preliminary

assessment of key areas for investment exploration, further data collection employing

a mix of the quantitative and qualitative questions was used to interview relevant

government, corporate, autonomous, CSOs and private organisations.

Understanding Bhutan’s

Economy

Baseline Study of

Operating Industries

Based on Economic

Activity Based on Scale

Resources Inventory

Agriculture

Livestock

Horticulture

Non-Wood Forest

Products

Education

ICT, Transportation

Health

Human Resources

Minerals

Review of 12th

FYP

Acc

ou

nti

ng

fo

r C

han

ges

Identification of Investment

Opportunities

For Cottage and Small-

Scale Investment

For Medium and Large-

Scale Investment

Overall Longlist based

on Economic Sector

Synopsis Detailed Project Profiles

Policy Recommendations

to foster Investments

Page | xi

The report makes inferences through SWOT matrix for Bhutan. Along with this, a

compendium of the available resources inventory was documented. The third aspect

was listing specific business avenues which was also considered based on the global

and regional demand and forecasts, existing business climate and resources. Using the

multi criteria decision analysis (MCDA) technique, economic activities were selected

for detailed study.

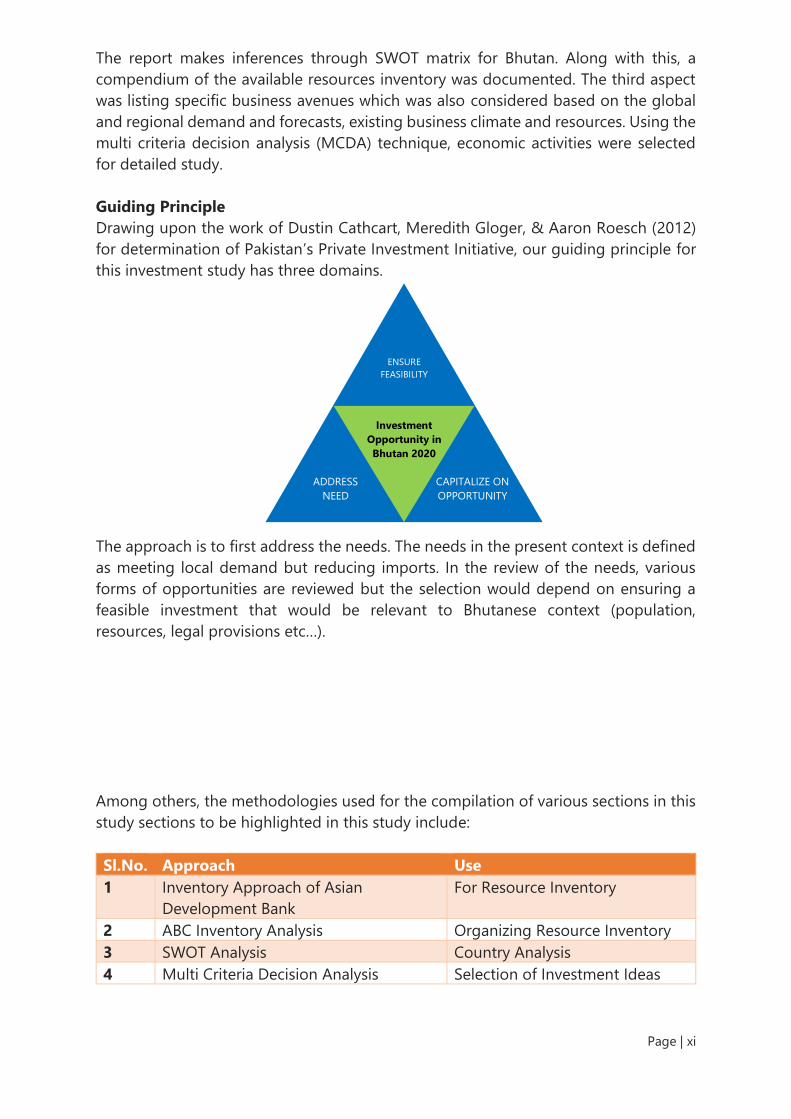

Guiding Principle

Drawing upon the work of Dustin Cathcart, Meredith Gloger, & Aaron Roesch (2012)

for determination of Pakistan’s Private Investment Initiative, our guiding principle for

this investment study has three domains.

The approach is to first address the needs. The needs in the present context is defined

as meeting local demand but reducing imports. In the review of the needs, various

forms of opportunities are reviewed but the selection would depend on ensuring a

feasible investment that would be relevant to Bhutanese context (population,

resources, legal provisions etc…).

Among others, the methodologies used for the compilation of various sections in this

study sections to be highlighted in this study include:

Sl.No. Approach Use

1 Inventory Approach of Asian

Development Bank

For Resource Inventory

2 ABC Inventory Analysis Organizing Resource Inventory

3 SWOT Analysis Country Analysis

4 Multi Criteria Decision Analysis Selection of Investment Ideas

Investment

Opportunity in

Bhutan 2020

ENSURE

FEASIBILITY

ADDRESS

NEED

CAPITALIZE ON

OPPORTUNITY

Investment Opportunity Study 2020

Page | xii

Methodology for investment selection

This approach is developed to systematically select the investment opportunities in a

rationalized manner and employs MCDA at two levels;

• Long-Listing

• Short-Listing

Identification of Economic Activities

Overall, the list of industries is selected from the following sources:

i. List of economic activities mentioned in the National Industrial Classification

System 2008 of India.

ii. Current operational economic activities with less than 5 establishments.

iii. Potential economic activities based on consultant’s knowledge.

iv. Government reports describing economic activities that could substitute

imports.

v. List of top 50 products imported in the country.

Long listing of Economic Activities

The identified economic activities are longlisted based on five criteria as mentioned

below:

i. Relevance to Bhutan: economic activities such as tobacco or drug related

items or complex ideas such as manufacture of aircraft are discarded based

on its irrelevance to Bhutan.

ii. Environmental Friendliness: economic activities that could endanger the

ecology have been discarded in line with Bhutan’s stand for environmental

conservation.

iii. Market Potential: overall ease of marketability of the product at regional and

international market is considered instead of limiting it only to Bhutan.

Page | xiii

iv. Resource Availability: overall ease of purchase of raw material from India

and Bangladesh is also considered along with resource availability within

Bhutan

v. Employment Generation: ideas offering limited or single employment are

discarded.

Rejection Criteria: any economic activity that does not score a full five point is rejected.

Grouping into Sectors

The longlisted ideas are grouped under ten sectors (shown in Table 1) which can be

explored by individuals who may find specific and relevant opportunities for

consideration in the future.

Table 1: Grouping of longlisted economic activities

Production and

Manufacturing

Services Trade

Agro Agro Agro

Forest Forest Forest

Mineral Mineral Mineral

Information Communication

and Technology and

Information

Technology

Information Technology

Hospitality Sector Hospitality Sector Hospitality Sector

Construction Construction Construction

Education and Health Education and Health Education and Health

Finance and Insurance Finance and Insurance Finance and Insurance

Energy Energy Energy

Transport and Logistics Transport and Logistics Transport and Logistics

The above list is also characterized based on the Dzongkhag where it is most

applicable.

Shortlisting of Economic Activities

Shortlisting of economic activities for recommendation was carried out based on the

following criteria: return on investment, market size, main market, new

product/services (value), economic diversification, energy intensive, domestically

available resources, cost of imported raw material, time taken to operationalise, import

substitution, sensitivity of policies and regulations.

Each criterion was scored using a Likert scale of 1-5 with 5 indicating the most

favourable terms with regard to that criteria. The top twenty activities scoring the

highest was chosen for recommendation.

Manufacturing Sectors

Page | 2

Project Title: Manufacturing of

Beauty Care Products

(Soaps, Shampoo and Allied Products)

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 3

1. Manufacturing of Beauty Care Products

1.1. Background of the Idea The demand for organic cosmetic products is strong. The global natural cosmetics

market size is expected to reach a value of USD 48.04 billion by 2025, increasing by

5.01% from 2019 to 2025, according to a recent report published by Grand View

Research.

A product is considered "natural" when it contains ingredients that are sourced from

nature rather than created synthetically. Given that Brand Bhutan is associated with

organic culture, manufacturing and exporting of organic soaps is quite promising.

1.2. Rationale of the Idea

1.2.1. Local Demand

The beauty care products currently in the market is largely synthetic based. The

imports have been consistent over the past five years accounting to almost Nu 350

million.

Table_ 1: Beauty Care Products Average Import Trends in Bhutan

Items Average Import

in 4 years (Nu. Millions)

Soaps 140

Other agents for washing skin 33

Organic surface-active agents (other than soap) 144

Shampoos 31

Personal Hair and Skin Care 10

Figure_ 1: Import of Beauty Care Products (in Millions)

-

50

100

150

200

2015 2016 2017 2018 2019Soaps

Other agents for washing skin

Organic surface-active agents (other than soap

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 4

An article in Kuensel covered the story on the successful start-ups manufacturing soaps

in Bhutan1. Firms interviewed expressed the satisfaction with market response to the

products.

However, it must be noted that the cost of production of synthetic products outside

Bhutan is much cheaper owing to economies of scale. Therefore, this business idea

considers only offsetting products worth Nu. 20 million annually.

1.2.2. Export Demand

Bhutan has been making a good progress in the export market with regard to soap.

Exports in the past few years have been increasing at 50% each year. Almost all of the

export is to Germany.

Figure_ 2: Export of Soaps from Bhutan

A research by Centre for the Promotion of Imports mentions of the following key

points:

• European imports of soap increased from €1.4 billion in 2012 to €1.6 billion in

2016. This resulted in an average annual growth rate of 3.8%.

• In the coming years, European imports are expected to keep growing

moderately.

• Developing countries supply around 14% of European soap imports amounting

to €231 million. This share is predicted to be fairly stable in the coming years.

• Germany is Europe’s leading importer of soap by far with €248 million in 2016.

France (€222 million) and the United Kingdom (€203 million) follow.

• When it comes to imports from developing countries, the United Kingdom leads

with €68 million. This is one third of its total soap imports.

• The strong performance of developing country soap suppliers in the United

Kingdom is evidenced further by a €14 million increase between 2012 and 2016.

1 https://kuenselonline.com/handmade-soaps-find-market-in-the-country/

1.46

41.47

60.28

86.30

-

20

40

60

80

100

2015 2016 2017 2018

India COTI

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 5

Figure_ 3: European Imports of Soaps in £ million

Source 1: Centre for the Promotion of Imports, Netherlands Enterprise Agency

For this business idea, the net import from Bhutan is considered as 1% of the total

import which makes around Nu. 230 million. Assuming a market share of 10% by one

firm, it accounts to Nu. 23 million.

1.2.3. Market Outlook International2

Skincare maintains the top billing in the global organic beauty market and is expected

to emerge as the most attractive segment, closely followed by haircare. This means

that natural and organic skincare, combined with organic haircare, will form half of the

total global organic beauty market3.

The Global Organic Soap market is projected to register a CAGR of 7.2% over the

forecast period (2020-2025).

• The growing concerns regarding the impact of synthetic ingredients such

as parabens and sulphates in synthetic soaps are driving the market for organic

soap.

• Furthermore, awareness towards a sustainable environment, by reducing the

impact of chemicals coupled with the government initiatives to support organic

products are also fuelling the market growth.

1.3. The Concept The strategy to penetrate the beauty products market suggested to offer multiple

products to customers under one brand name to leverage Brand Bhutan. To follow this

2 Information from: https://www.mordorintelligence.com/industry-reports/organic-soap-market and

https://www.statista.com/statistics/673641/global-market-value-for-natural-cosmetics/ 3 https://formulabotanica.com/global-organic-beauty-market-22bn-2024/

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 6

concept, multiple products manufacturing is suggested which can be started from

making soap and shampoo.

The product group is as follows:

• Herbal and Organic Bathing Soap: 10g, 20gm, 50gm, 75gm, 100gm, 125gm

• Herbal Hair Shampoo: Pouch 5-10 ml, 30ml, 50ml, 100ml, 150ml, 200ml, 400ml

• Body Wash Lotion: 50ml, 100ml, 200ml, 400ml, 1lt

• Skin Moisturizer Cream: 50ml, 100ml, 200ml, 400ml, 1lt

• Hair Conditioners: 20ml, 50ml, 100ml, 150ml, 200ml

• Hair Cream: 50ml and 100ml

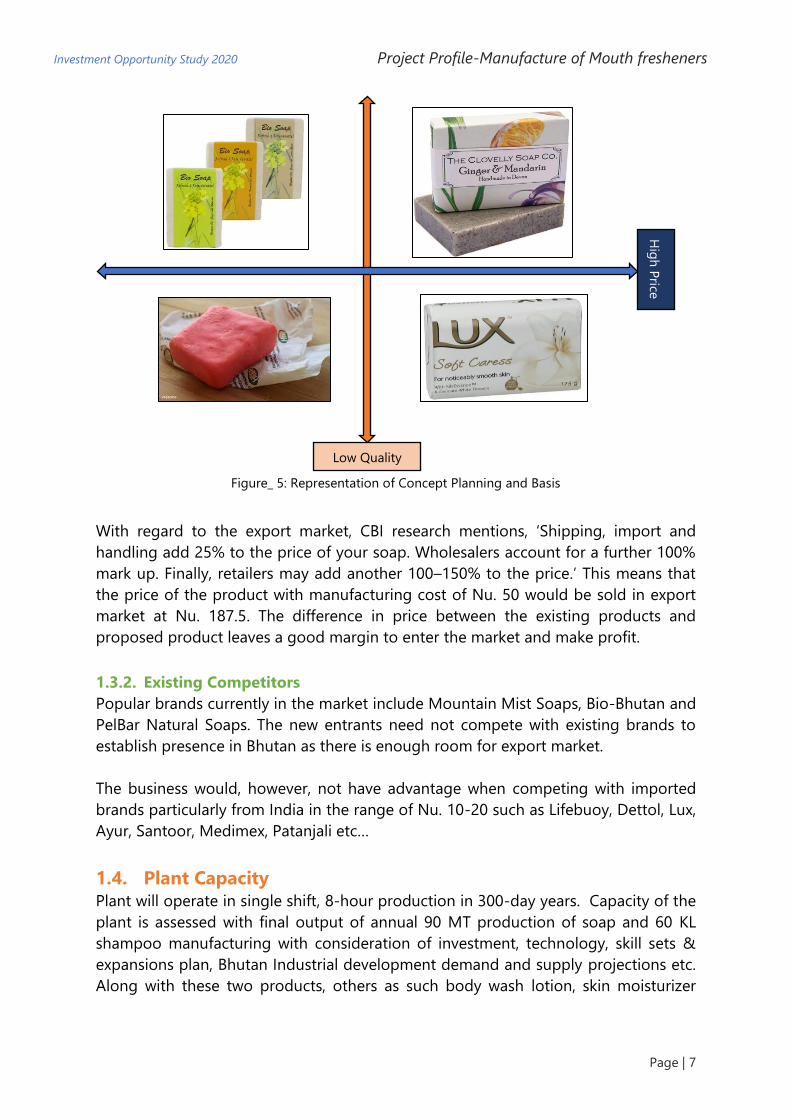

1.3.1. Perceptual Mapping

In comparison to the price of a natural organic ingredient-based soap, the price is 5

times higher in the UK. For example, a 100g bar of Bio Soap costs Nu. 1104, a similar

product (based on packaging and ingredients) costs Nu. 512 in the UK5. This provides

an excellent opportunity for Bhutanese products to find a place in the European export

market.

Figure_ 4: Price Changes over the Period (Nu./Kg)

When comparing within the local market, there is stiff competition from imported

products which has been about Nu. 100 per kg, making the price as low as Nu. 10 for

100g. Therefore, this business idea must seek to find a niche market in Bhutan and

concentrate largely on the export market. A Representation of Concept Planning and

Basis is given in figure no. 5 below:

4 https://druksell.bt/search?type=article%2Cpage%2Cproduct&q=soap* 5 https://www.amazon.co.uk/s?k=ginger+soap&ref=nb_sb_noss

0

100

200

300

400

500

600

700

2015 2016 2017 2018 2019

Soap Shampoo Deodrants

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 7

Figure_ 5: Representation of Concept Planning and Basis

With regard to the export market, CBI research mentions, ‘Shipping, import and

handling add 25% to the price of your soap. Wholesalers account for a further 100%

mark up. Finally, retailers may add another 100–150% to the price.’ This means that

the price of the product with manufacturing cost of Nu. 50 would be sold in export

market at Nu. 187.5. The difference in price between the existing products and

proposed product leaves a good margin to enter the market and make profit.

1.3.2. Existing Competitors

Popular brands currently in the market include Mountain Mist Soaps, Bio-Bhutan and

PelBar Natural Soaps. The new entrants need not compete with existing brands to

establish presence in Bhutan as there is enough room for export market.

The business would, however, not have advantage when competing with imported

brands particularly from India in the range of Nu. 10-20 such as Lifebuoy, Dettol, Lux,

Ayur, Santoor, Medimex, Patanjali etc…

1.4. Plant Capacity Plant will operate in single shift, 8-hour production in 300-day years. Capacity of the

plant is assessed with final output of annual 90 MT production of soap and 60 KL

shampoo manufacturing with consideration of investment, technology, skill sets &

expansions plan, Bhutan Industrial development demand and supply projections etc.

Along with these two products, others as such body wash lotion, skin moisturizer

Hig

h P

rice

Low Quality

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 8

cream, hair conditioners and hair cream will also be produced in the proposed plant.

The detail plant capacity planning is as follows given below:

# Product Plant Capacity Annual Capacity

(MT)

1. Premium Quality Herbal Soap 100Kg per Hr. 90 MT

2. Shampoo 100 Lt per Hr. 60 KL

3. Body Wash Lotion 100 Lt per Hr. 30 KL

4. Skin Moisturizer Cream 50Lt. per Hr. 20 KL

5. Hair Conditioners 50Lt. per Hr. 20 KL

6. Hair Cream 50Lt. per Hr. 20 KL

Table 2: Plant Capacity and Planning

1.5. Manufacturing Process

1.5.1. Soap Manufacturing6

Glycerine is a humectant meaning that it helps retain, or reduce the loss of moisture.

The manufacturing of soap consists preparation of herbs, mixing with glycerine, and

coconut oil with pure potassium hydroxide. After that heating and shaping is done in

moulds. Cooling is done after moulding and soaps are ready for finally sizing and

packaging. The raw ingredients are herbal fats, herbal oils and their fatty acids, soluble

olive oil and cocoa oils, palm, coconut oil, kernel oils etc. Manufacturing process for

soap production is detailed in figure no.5 given below:

The soap manufacturing process follows the following steps:

6 https://www.diynatural.com/how-to-make-glycerin-soap-base-recipe/

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 9

Step 1: Melt the glycerine

Step 2: Add the herbs (add the minced herbs, citrus zest and two drops of

essential oils (if used) and mixing).

Step 3: Pour the mixture into the mould

Step 4: Cooling, cutting, sizing and packaging

1.5.2. Shampoo Manufacturing7

The ingredients are prepared according the above process. Water is metered into the

process vessel and it is often heated to around 130-140℉ (55-60℃) to aid

dilution/hydration of other ingredients. Conditioners and other ingredients are added.

This solution cooled and packed in PET Bottles.

Figure_ 6: Shampoo Manufacturing Process Flow Chart

Water, surfactants (surface active agents – or cleansing agents), thickeners or viscosity

builders, conditioning agents, foam boosters, preservatives, active ingredients,

fragrance and colour are the main ingredients for shampoo manufacturing.

Body Wash Lotion, Skin Moisturizer Cream, Hair Conditioners and Hair Cream are the

emulsion-based products and mainly mixing, boiling and cooling are the main process

activities. The equipment used for manufacturing these products are mixers, SS vessels

and kettles, filling machines etc. These allied products are also packed in HDPE bottle

shape containers.

7 https://www.slideshare.net/waliseu/shampoo-44457202

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 10

1.5.3. Equipment Requirement

Equipment used for manufacturing of soap, shampoo and other products mainly

consist of mixtures equipment, SS vessels, and kettles. The required machines and

equipment for this plant can be sourced from Kolkata (West Bengal), Guwahati (Assam)

and Rajkot (Gujarat). The list of equipment suppliers is attached as Annex A.

Some of the required equipment include pre-cleaning machines and mixing

equipment, glycerin soap plant - (MOC SS 316), soap cutting machine – manual,

stamping machine, shampoo making machine (reactor vessel), lotion & cream making

machine, SS vessels and kettles, trays and tanks, soap bar packaging machines,

shampoo/liquid bottle filling machine - bottle manual, body lotion filling and

packaging machine, shampoo pouch filling machine and bottle cap sealing machine,

weighing machine, conveyors and packaging machine etc.

1.5.4. Required Systems and Licenses

• Land requirement: about 1,000 m2 and built up area of about 465 m2 for

production hall, storage, packaging, office and utilities.

• Manpower of 25 people including:

▪ Manager

▪ Accounts and Administration,

▪ Advertising and Marketing

▪ Quality assurance and Lab In-charge

▪ 12 factory front line workers

▪ Support staff (on contract basis)

1.6. Required Licenses and Certification

Table_ 2: Required Licenses and Certification

Quality Management ISO 9001:2015

Environment Management ISO 14001

GMP Certification for Export Good Manufacturing Practice

Products Cover in Indian Act Drugs and Cosmetics Act by the Act 68 of

1982 - 1983

BIS Number – India IS 7669, BIS IS 2888: 2004(R2016)

Bhutan Approval Environment Clearance and Other

Regulatory Act Registration and Certificates

Export Requirement to US & Europe WHO- GMP (Good manufacturing practices)

Export – Import Duty to India Trade between India and Bhutan is not

subject to customs duties

The proposed business idea is based on providing a range of beauty care products.

More details on the process can be found from the following sources and videos for

better understanding.

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 11

Reading Materials Videos

https://www.diynatural.com/how-to-make-

glycerin-soap-base-recipe/

https://www.youtube.com/watc

h?v=rPckDJP9GLY

http://www.madehow.com/Volume-2/Soap.html https://www.youtube.com/watc

h?v=qSXbZ52r7IY

https://my.msme.gov.in/MyMsmeMob/MsmePro

jectProfile/Pages/2_6.html

https://www.youtube.com/watc

h?v=lQ6fCZgYc8g

1.7. Estimated Project Cost and Financials The total cost of the project has been considered at Nu. 13.5 million. The payback

period is 21 months. D.S.C.R value is 4.51 which show that the project will generate

sufficient income to pay back loans. Other financial trends are as follows:

Table_ 3: Project Trends and Financial Ratio

# Description Amount (Nu. In Lacs)

1. Plant Capacity ▪ 90 MT for Soap

▪ 150KL Shampoo and Other Items

2. Land Area (On Lease) 1000 m2

3. Proposed Location in Bhutan Thimphu, Samtse, Phuentsholing, and

Gelephu

4. Establishment Cost 134.59

5. Cost of Operation at 100%

capacity utilization

2.1 Fixed Cost 78.22

a. Salary & Wages 57.00

b. Overhead Cost 21.22

6. Variable Costs at 100% capacity

utilization

42.63

a. Raw Material 534.60

b. Other Variable

Cost

34.28

7. Break Even Point 52.83%

8. Payback Period 21 Months

9. D.S.C.R. 4.51

10. NPR 14.24%

11. Return on Investment 44.53%

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 12

1.8. Means of Finance

Table_ 4: Means of Finance

# Particulars Value (Nu. in Lacs)

1. Promoters Equity 37.21

2. Term Loan from Bank 97.40

Total 134.61

3. Margin Money for Working Capital 28.84

4. Working Capital Loan from Bank 49.82

Total 78.66

1.9. Project Cost The cost of project is estimated as a total value of land, building and civil construction,

plant and machinery, MFA, preliminary expenses, pre-operative expenses and

contingency. The required land is around 1000 m2 on lease for 30 years.

The Plant & Machinery shared maximum project cost of around 41.85% with Nu. 5.6

million followed by Building & Civil Construction cost of Nu. 3.8 million constituting

28.19% of the project cost. Margin Money for working capital is not considered as part

of the project cost.

The summary of the project cost is as follows: Table_ 5: Head Wise Project Cost and Sharing Percentage

# Particulars Value (Nu. in Lacs) Cost

Sharing

1. Building & Civil Construction 37.95 28.19%

2. Plant & Machinery 56.34 41.85%

3. Misc. Fixed Assets 14.75 10.96%

4. Preliminary Expenses 1.00 0.74%

5. Pre-operative Expenses 21.30 15.82%

6. Contingencies 3% 3.27 2.43%

Total 134.61 100%

1.9.1. Estimation of Building and Civil Work and Cost

Based on the requirement of processing area, raw material and finished goods store

and office space, the following building area is planned. The building civil construction

cost is considered as per the Bhutan Schedule of Rates (Civil Works)8 - 2018 - issued

by Ministry of Works and Human Settlement, Bhutan. Pre-fabricated building structure

will be used for construction of building amenities.

8 Source: https://www.mowhs.gov.bt/wp-content/uploads/2018/04/BSR-2018-civil.pdf

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 13

Total estimated building construction cost is Nu.3.8 million which is around 28% of the

total project cost. The detail Building and Civil Work cost estimation is as follows:

Table_ 6: Estimation of Building and Civil Work and Cost

# Particular Dimensions (Mt.)

Area (Sq. Mt.)

Rate (Nu./ Sq. Mt.)

Amount (Nu. in Lacs)

1. Production area -

main shed height

16 feet (5Mt.)

60 50 3000 750 22.50

2. Raw material

storage

25 18 450 600 2.70

3. Packaging section 20 16 320 600 1.92

4. Finished goods

storage

25 18 450 600 2.70

5. Laboratory 20 15 300 600 1.80

6. Office space 20 15 300 600 1.80

7. Facilities + utility +

canteen

20 18 360 600 2.16

8. Security & time

office

10 10 100 600 0.60

9. Boundary wall (130

RM with height of 3m

(10Ft) and 1ft thickness)

412 1 412 150 0.62

10. Parking area 60 30 1800

0.50

11. Green belt

development and

open space

70 50 3500

0.30

12. Entrance gate - 15

feet wide and sign

board

1 35000 0.35

Total 37.95

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 14

1.9.2. Plant and Machinery Cost9

The cost estimates for plant & machinery have been worked out based on the cost

figures received from the Indian plant machinery suppliers.

The prices are considered without Indian GST which is exempted under supply of trade

agreement between India and Bhutan (Category Export). Installation and

commissioning of equipment are considered separately in the total plant and

machinery cost estimation. Freight and insurance have been considered with the

assumption that all goods are transported by road. Goods of imported origin would

be handled at the Kolkata port.

Total estimated cost of the plant and machinery is Nu. 5.6 million including the cost of

packaging and forwarding @7.5% and erection and commissioning @10% of

equipment billing cost of Nu. 4.8 million. The equipment list with cost is given in table

below:

Table_ 7: Plant & Machinery with Cost

# Plant & Machinery Qty. Rate Amount (Nu. in Lacs)

1. Pre cleaning Machines and Processing equipment's

(100 Kg. per Hr.)

1 250000 2.50

2. Glycerine Soap Plant - (SS 316) (100Kg per Hr.) 1 950000 9.50

3. Soap Cutting Machine - Manual (500 cuts per Hr.) 2 40000 0.80

4. Stamping Machine 2 80000 1.60

5. Shampoo Making Machine-Reactor vessel (100Lt.) 1 635000 6.35

6. Lotion & Cream Making Machine (100Lt. Capacity) 1 1125000 11.25

7. SS vessels and kettles, Trays and Tanks

(100Lt, 200Lt. 500 Lt and 1000 Lt.)

1 250000 2.50

8. Soap Bar Packaging Machines 1 100000 1.00

9. Shampoo Filling Machine - Bottle Manual

(Upto 5Lt)

1 35000 0.35

10. Body Lotion Filling and Packaging Machine

(Upto 5Lt)

1 190000 1.90

11. Shampoo Pouch Filling Machine (10ml to 50ml) 1 100000 1.00

12. Bottle Cap sealing machine (upto 4” Dia) 1 75000 0.75

13. Corrugated box wrapping machine

(Box weight Capacity 100Kg)

1 135000 1.35

14. Weighing Machine (500Kg) 1 20000 0.20

15. Small Hand Tools and Laboratory Equipment 0.5

16. Laboratory Equipment's and Measuring Devices 6.00

17. Miscellaneous Items i.e. Jigs and Fixtures 0.40

9 Equipment Supplier List is given under annexure A.

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 15

Total 47.95

18. Packaging and Forwarding @7.50% 3.60

19. Erection and Commissioning @10% 4.80

Grand Total 56.34

1.9.3. Misc. Fixed Assets

A miscellaneous fixed asset includes office equipment & furniture, computer and

peripherals, firefighting equipment, vehicle etc. Nu.1.5 million has been estimated

under this head “MFA” and is presented in the below table:

Table_ 8: Misc. Fixed Assets Cost Estimation

# Particulars Qty. Amount (Nu.in lacs)

1. Office Equipment, Laptop, Printer & Software's 1 2.50

2. Furniture & Fixture with Interior Items 1 3.50

3. Fire Fighting Equipment's (1set of 10 pcs each) 1 0.60

4. Ventilation - Exhaust fans 5 0.15

5. Tata Mini Truck 1 8.00

Total 14.75

1.9.4. Preliminary Expenses

Preliminary expenses are those expenses which are incurred before the incorporation

and commencement of the business. This expense is treated as deferred

revenue expenditure. These expenses are marked write off in next ten years in

estimation of profitability.

The Preliminary Expenses details are as follows:

Table_ 9: Preliminary Expenses

# Particular Amount (Nu.in Lacs)

1. Company formation, Approvals and Setup

expenses

1.00

Total 1.05

1.9.5. Pre-operative Expenses

These expenses are incurred prior to commencement of commercial production. A

total of amount Nu. 2.13 million is estimated under this project cost head. It is written

off in the next 10 years and exempted in the first year.

The details are given in the table below:

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 16

Table_ 10: Pre-operative Expenses

# Particular Amount (Nu.in Lacs)

1. Interest up to production 1.99

2. Insurance during construction period 0.56

3. Electricity charges construction period 1.50

4. Salary during construction period 3.40

5. Marketing launch expenses 2.00

6. Quality, GMP and Environment Management System 5.00

7. Project consultancy fees @5% of project cost 5.45

8. Travelling Expenses for Project Implementation 1.00

9. Registration of Trade Mark and patent 0.40

Total 21.30

1.9.6. Cost of Raw Material

The cost of raw material consists of the cost of the main ingredients, raw material and

cost of packaging. The annual raw material cost is based on the present average

market prices in Bhutan. A total of Nu. 53.46 million has been estimated as raw material

cost. The details are given in the table below:

Table_ 11: Cost of Raw Material

# Raw Material Annual

Requirem

ent

Rate (Nu/Unit )

Total Amount (Nu.in Lacs)

1. Refined Glycerine 73 KL 110 Lt 80.3

2. Coconut oil, fats, olive oil, wax

esters and ester oils, essential

oils etc.

112 KL 140 Lt 156.8

3. Surfactants, Thickeners or

Viscosity Builders,

Conditioning Agents, Foam

Boosters, preservatives, active

ingredients, fragrance and

colour.

25 MT 350 Kg 87.5

4. Herbs Ingredients as such

amla, sweet almond oil, methi,

almonds oil, flowers, Shea,

cocoa, kokum butter etc.

30 MT 600 Lt 180

5. Packaging Material - PP

Sheets, Pouches, HDPE

Bottles, Carton Box,

Packaging's Taps etc.

Set

30

Total Raw Material requirement at 100% capacity Utilisation 534.60

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 17

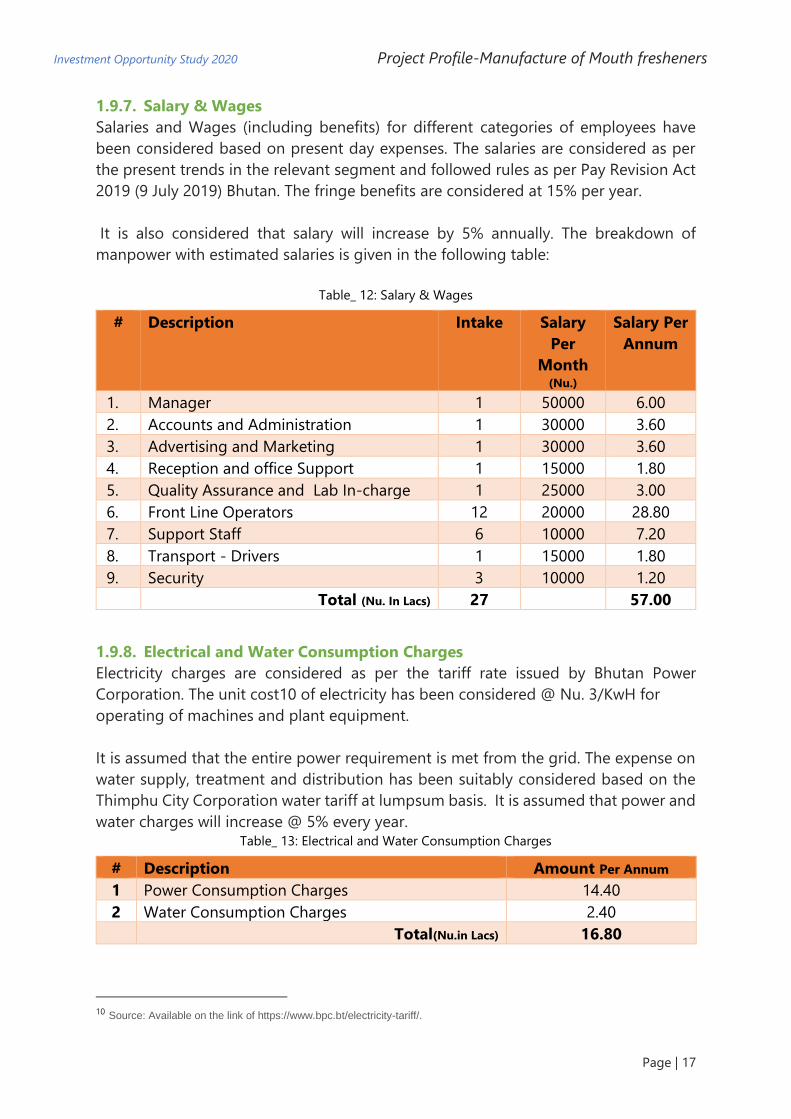

1.9.7. Salary & Wages

Salaries and Wages (including benefits) for different categories of employees have

been considered based on present day expenses. The salaries are considered as per

the present trends in the relevant segment and followed rules as per Pay Revision Act

2019 (9 July 2019) Bhutan. The fringe benefits are considered at 15% per year.

It is also considered that salary will increase by 5% annually. The breakdown of

manpower with estimated salaries is given in the following table:

Table_ 12: Salary & Wages

# Description Intake Salary

Per

Month (Nu.)

Salary Per

Annum

1. Manager 1 50000 6.00

2. Accounts and Administration 1 30000 3.60

3. Advertising and Marketing 1 30000 3.60

4. Reception and office Support 1 15000 1.80

5. Quality Assurance and Lab In-charge 1 25000 3.00

6. Front Line Operators 12 20000 28.80

7. Support Staff 6 10000 7.20

8. Transport - Drivers 1 15000 1.80

9. Security 3 10000 1.20

Total (Nu. In Lacs) 27 57.00

1.9.8. Electrical and Water Consumption Charges

Electricity charges are considered as per the tariff rate issued by Bhutan Power

Corporation. The unit cost10 of electricity has been considered @ Nu. 3/KwH for

operating of machines and plant equipment.

It is assumed that the entire power requirement is met from the grid. The expense on

water supply, treatment and distribution has been suitably considered based on the

Thimphu City Corporation water tariff at lumpsum basis. It is assumed that power and

water charges will increase @ 5% every year. Table_ 13: Electrical and Water Consumption Charges

# Description Amount Per Annum

1 Power Consumption Charges 14.40

2 Water Consumption Charges 2.40

Total(Nu.in Lacs) 16.80

10 Source: Available on the link of https://www.bpc.bt/electricity-tariff/.

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 18

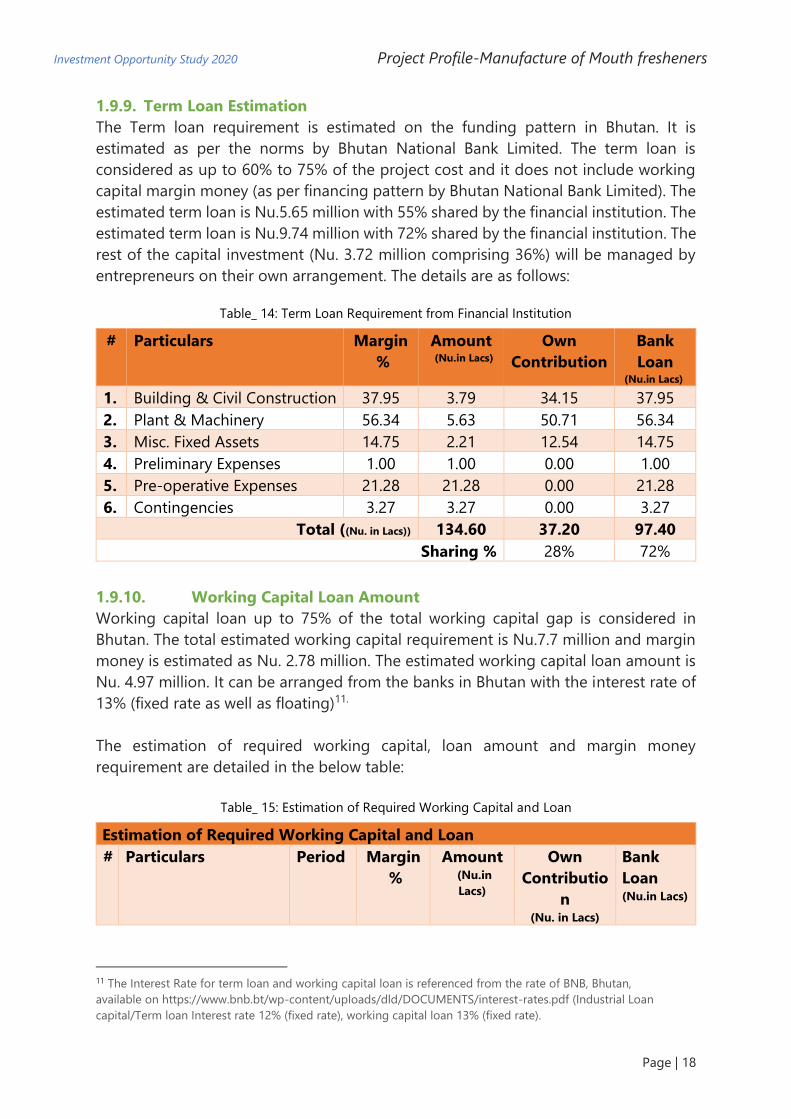

1.9.9. Term Loan Estimation

The Term loan requirement is estimated on the funding pattern in Bhutan. It is

estimated as per the norms by Bhutan National Bank Limited. The term loan is

considered as up to 60% to 75% of the project cost and it does not include working

capital margin money (as per financing pattern by Bhutan National Bank Limited). The

estimated term loan is Nu.5.65 million with 55% shared by the financial institution. The

estimated term loan is Nu.9.74 million with 72% shared by the financial institution. The

rest of the capital investment (Nu. 3.72 million comprising 36%) will be managed by

entrepreneurs on their own arrangement. The details are as follows:

Table_ 14: Term Loan Requirement from Financial Institution

# Particulars Margin

%

Amount (Nu.in Lacs)

Own

Contribution

Bank

Loan (Nu.in Lacs)

1. Building & Civil Construction 37.95 3.79 34.15 37.95

2. Plant & Machinery 56.34 5.63 50.71 56.34

3. Misc. Fixed Assets 14.75 2.21 12.54 14.75

4. Preliminary Expenses 1.00 1.00 0.00 1.00

5. Pre-operative Expenses 21.28 21.28 0.00 21.28

6. Contingencies 3.27 3.27 0.00 3.27

Total ((Nu. in Lacs)) 134.60 37.20 97.40

Sharing % 28% 72%

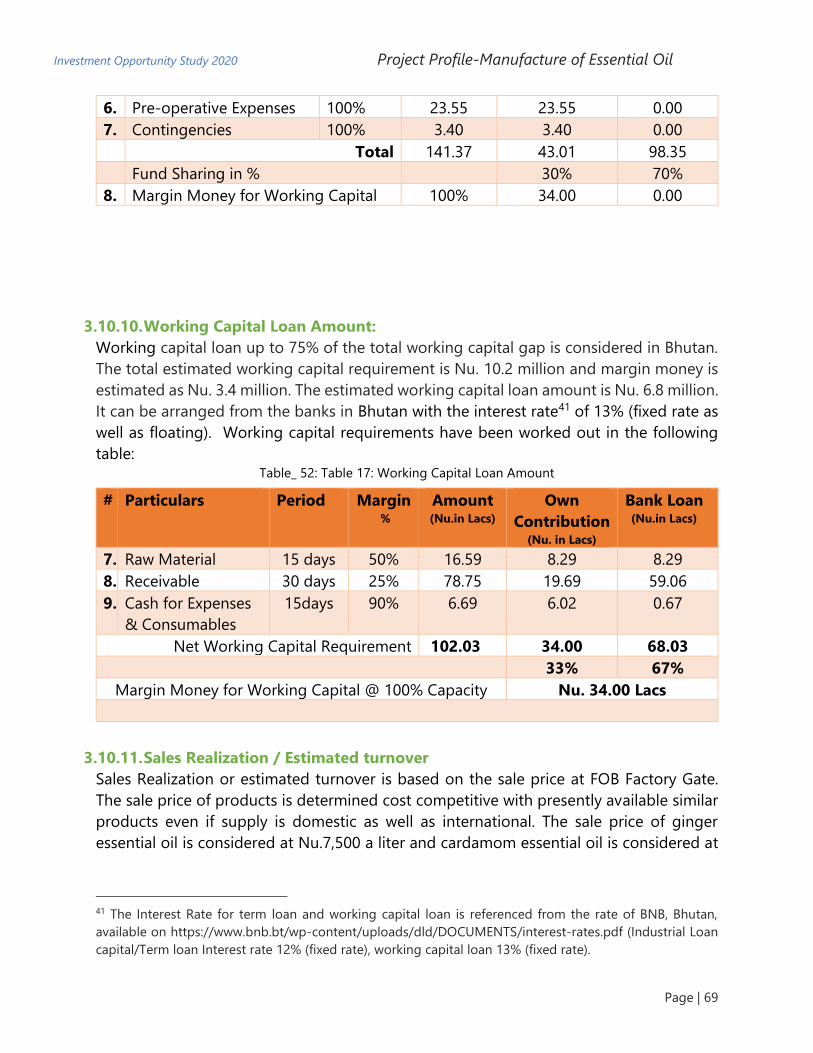

1.9.10. Working Capital Loan Amount

Working capital loan up to 75% of the total working capital gap is considered in

Bhutan. The total estimated working capital requirement is Nu.7.7 million and margin

money is estimated as Nu. 2.78 million. The estimated working capital loan amount is

Nu. 4.97 million. It can be arranged from the banks in Bhutan with the interest rate of

13% (fixed rate as well as floating)11.

The estimation of required working capital, loan amount and margin money

requirement are detailed in the below table:

Table_ 15: Estimation of Required Working Capital and Loan

Estimation of Required Working Capital and Loan

# Particulars Period Margin

%

Amount (Nu.in

Lacs)

Own

Contributio

n (Nu. in Lacs)

Bank

Loan (Nu.in Lacs)

11 The Interest Rate for term loan and working capital loan is referenced from the rate of BNB, Bhutan,

available on https://www.bnb.bt/wp-content/uploads/dld/DOCUMENTS/interest-rates.pdf (Industrial Loan

capital/Term loan Interest rate 12% (fixed rate), working capital loan 13% (fixed rate).

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 19

1. Raw Material 15

days

50% 15.40 7.70 7.70

2. Receivable 30

days

25% 55.07 13.77 41.30

3. Cash for Expenses &

Consumables

15days 90% 7.02 6.32 0.70

Net Working Capital Requirement 77.49 27.79 49.70

Margin Money for working Capital Nu. 27.79Lacs

1.9.11. Sales Realisation/Estimated Turnover

Sales Realisation or estimated turnover is based on the sale price at FOB Factory Gate.

The sale price of products is determined as cost competitive with present available

similar product by domestic as well as international supply. The sale price of Premium

Quality Herbal Soap is considered as average 160kg for 10gm to 125gm packing.

The total amount of Nu. 94.4 million is estimated as sales realization (turnover) at 100%

production capacity. The sale price of each item is detailed in the table below with

production capacity:

Table_ 16: Sales Realization/Estimated Turnover

# Product Sale

Quantity

Annual

Rate (Nu. per Unit)

Total Amount

per Annum (Nu. in Lacs )

1. Premium Quality Herbal Soap 90 MT 160 Kg. 144

2. Shampoo 60 KL 350 Lt. 210

3. Body Wash Location 30 KL 700 Lt. 210

4. Skin Moisturizer Cream 20 KL 700 Lt. 140

5. Hair Cream 20 KL 600 Lt. 120

Total 944

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 20

1.9.12. Estimated Cost of Production and Profitability

As per the above estimated economic parameters, finance can be arranged by sharing

28% by investor and 72% by loan through financial institutions. Working capital mainly

consists of the amount required to purchase raw material. Required margin money for

this project is Nu. 2.72 million. For profitability estimation, analysis of loan repayment

capacity and analysis of financial ratios for this project, the following assumptions and

relevant basis applicable to Bhutan have been considered:

• Industrial land12 in Bhutan is available on lease for up to maximum of 30 years and

could be renewed further. The plots for industrial use are available in the

government developed industrial parks and estates at prominent locations such as

Thimphu, Samtse, Phuentsholing, Gelephu etc. Charges are considered as Nu. 4 per

square feet per annum for the first three years. In the fourth year, the rate is Nu. 6

(i.e. 50% increase). Subsequently, it increases @3% every year.

• The profitability projection has been worked out for 10 years at 70% capacity

utilization to be achieved during the first to the third year and 80% from the fourth

year and 90% from the seventh year and onwards.

• Repair & maintenance have been taken at @1% p.a. on plant & machinery & misc.

fixed assets.

• Bank interest rate13 has been calculated @12% p.a. on term loan & @13% working

capital loan.

• Insurance charges is @ 0.25% on all assets in the first year. Then it is @ 5% decrease

every year.

• Power & water charges are increased @ 5% every year.

• Administrative expenses have been increased @ 5% every year.

• Margin money has been considered @ 40% on building, @ 25% on plant &

machinery and @ 25% on misc. fixed assets.

• Bank loan has been considered for repayment in 7 years with one-year moratorium.

• Preliminary expenditure will be written off every year in the next 10 years.

• Pre-operative expenditure will be written off from the second year.

• Depreciation has been charged on Straight-Line Method.

• Insurance, lease rent & interest has been taken as fixed cost for calculating B.E.P.

• Income tax14 has been charged @ 30% every year as per Bhutan's tax rates.

• DSCR - debt service coverage ratio - is defined as net operating income divided by

total debt service.

12https://www.bhutanenterprise.com/2018/06/03/investment-climate-in-bhutan/#:~:text=Lease%20rate%20for %20Industrial

%20Estate&text=4%20per%20square%20feet%20peri.e%2050%25%20increase%20on%20Nu. 13 The Interest Rate for term loan and working capital loan is referenced from the rate of BNB, Bhutan, available on

https://www.bnb.bt/wp-content/uploads/dld/DOCUMENTS/interest-rates.pdf (Industrial Loan capital/Term loan Interest rate 12%

(fixed rate), working capital loan 13% (fixed rate). 14 Ministry of Finance - https://www.mof.gov.bt/faq/)

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 21

1.10. Estimation of Project Profitability: (Nu.in Lacs) # Particulars 1st Yr. 2nd Yr. 3rd Yr. 4th Yr. 5th Yr. 6th Yr. 7th Yr. 8th Yr. 9th Yr. 10th Yr.

1 Installed Capacity@100% 944.00 944.00 944.00 944.00 944.00 944.00 944.00 944.00 944.00 944.00

2 Capacity Utilisation 70% 70% 70% 80% 80% 80% 90% 90% 90% 100%

3 Actual Sales (Nu. in Lacs) 660.80 660.80 660.80 755.20 755.20 755.20 849.60 849.60 849.60 944.00

4 Cost of Operation

4.1 Land Lease Charges 5.17 5.17 5.43 7.75 7.98 8.22 8.47 8.72 8.98 9.25

4.2 Raw Material 374.22 374.22 374.22 427.68 427.68 427.68 481.14 481.14 481.14 534.60

4.3 Consumables @ 3% 11.23 11.23 11.23 12.83 12.83 12.83 14.43 14.43 14.43 16.04

4.4 Power and Utility 16.80 17.64 18.52 19.45 20.42 21.44 22.51 23.64 24.82 26.06

4.5 Repair & Maintenance @3% 1.44 1.44 1.44 1.44 1.44 1.44 1.44 1.44 1.44 1.44

4.6 Salary & Wages 57.00 59.85 62.84 65.98 69.28 72.75 76.39 80.20 84.21 88.43

4.7 Fringe Benefits @10% 8.55 8.98 9.43 9.90 10.39 10.91 11.46 12.03 12.63 13.26

4.8 Insurance 0.50 0.45 0.41 0.36 0.33 0.30 0.27 0.24 0.22 0.19

4.9 Administration Expenses 7.00 7.35 7.72 8.10 8.51 8.93 9.38 9.85 10.34 10.86

Total 476.74 481.15 485.80 545.75 550.88 556.28 617.02 622.98 629.24 690.88

5 Marketing Expenses @10%

(Sales)

66.08 66.08 66.08 75.52 75.52 75.52 84.96 84.96 84.96 94.40

6 Cost of Production 542.82 547.23 551.88 621.27 626.40 631.80 701.98 707.94 714.20 785.28

7 Sale (Estimated Turn Over) 660.80 660.80 660.80 755.20 755.20 755.20 849.60 849.60 849.60 944.00

8 Profit Before Interest

and Depp.

117.98 113.57 108.92 133.93 128.80 123.40 147.62 141.66 135.40 158.72

9 Interest on Term Loan @12% 11.69 10.70 8.74 6.77 4.80 2.83 0.88 0.00 0.00 0.00

10 On Working Capital @13 % 6.46 6.46 6.46 6.46 6.46 6.46 6.46 6.46 6.46 6.46

11 Total Interest 18.15 17.16 15.20 13.23 11.26 9.29 7.34 6.46 6.46 6.46

12 Profit Before Depreciation. 99.84 96.40 93.73 120.70 117.54 114.11 140.29 135.20 128.94 152.26

13 Depreciation 11.48 9.91 8.58 7.44 6.47 5.64 4.93 4.32 3.80 3.35

14 Profit After Depreciation 88.36 86.49 85.15 113.27 111.07 108.47 135.36 130.88 125.15 148.91

15 Pre-operative Exp. W. Off 0.00 2.36 2.36 2.36 2.36 2.36 2.36 2.36 2.36 2.36

16 Preliminary Exp. W .Off 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10

17 Profit before Taxation 88.26 84.03 82.68 110.80 108.61 106.01 132.89 128.42 122.68 146.45

18 Taxation @30% of Net Profit 26.48 25.21 24.81 33.24 32.58 31.80 39.87 38.53 36.80 43.93

19 Accumulated Profit 61.78 120.60 178.48 256.04 332.07 406.27 499.29 589.19 675.06 777.58

20 Profit after Taxation 61.78 58.82 57.88 77.56 76.02 74.20 93.03 89.89 85.88 102.51

21 Add: Depreciation 11.48 9.91 8.58 7.44 6.47 5.64 4.93 4.32 3.80 3.35

22 Add: Interest on Term Loan 11.69 10.70 8.74 6.77 4.80 2.83 0.00 0.00 0.00 0.00

Total (A) 84.95 79.43 75.19 91.77 87.29 82.67 97.95 94.21 89.67 105.86

23 Interest on Term Loan 11.69 10.70 8.74 6.77 4.80 2.83 0.88 0.00 0.00 0.00

24 Repayment on Term Loan 0 16.40 16.40 16.40 16.40 16.40 15.40 0.00 0.00

Total (B) 11.69 27.10 25.14 23.17 21.20 19.23 16.28 0.00 0.00 0.00

Surplus (A) - (B) 73.26 52.33 50.06 68.60 66.09 63.44 81.68 94.21 89.67 105.86

DSCR (A/B) 7.27 2.93 2.99 3.96 4.12 4.30 6.02 0.00 0.00 0.00

Average DSCR 4.51

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 22

1.11. Calculation of Interest on Term Loan and Repayment (Nu. in

Lacs) # Year Opening Balance Repayment Closing

Balance

Interest

1 1st year 97.40 0 97.40 11.69 11.69

2 2nd year

1st Qtr. 97.40 4.10 93.30 2.86

2nd Qtr. 93.30 4.10 89.20 2.74

3rd Qtr. 89.20 4.10 85.10 2.61

4th Qtr. 85.10 4.10 81.00 2.49 10.70

3 3rd year

1st Qtr. 81.00 4.10 76.90 2.37

2nd Qtr. 76.90 4.10 72.80 2.25

3rd Qtr. 72.80 4.10 68.70 2.12

4th Qtr. 68.70 4.10 64.60 2.00 8.74

4 4th year

1st Qtr. 64.60 4.10 60.50 1.88

2nd Qtr. 60.50 4.10 56.40 1.75

3rd Qtr. 56.40 4.10 52.30 1.63

4th Qtr. 52.30 4.10 48.20 1.51 6.77

5 5th year

1st Qtr. 48.20 4.10 44.10 1.38

2nd Qtr. 44.10 4.10 40.00 1.26

3rd Qtr. 40.00 4.10 35.90 1.14

4th Qtr. 35.90 4.10 31.80 1.02 4.80

6 6th year

1st Qtr. 31.80 4.10 27.70 0.89

2nd Qtr. 27.70 4.10 23.60 0.77

3rd Qtr. 23.60 4.10 19.50 0.65

4th Qtr. 19.50 4.10 15.40 0.52 2.83

7 7th year

1st Qtr. 15.40 4.10 11.30 0.40

2nd Qtr. 11.30 4.10 7.20 0.28

3rd Qtr. 7.20 4.10 3.10 0.15

4th Qtr. 3.10 3.10 0.00 0.05 0.88

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 23

1.12. Break Even Point

# Particulars

1st

Yr.

2nd

Yr.

3rd

Yr.

4th

Yr.

5th

Yr.

6th

Yr.

7th

Yr.

8th

Yr.

9th

Yr.

10th

Yr.

1 Calculation of B.E.P.

Variable Cost

469.7

7

470.6

1

471.4

9

536.9

2

537.8

9

538.9

1

604.4

9

605.6

1

606.7

9 672.54

Fixed Cost

107.8

4

108.8

7

109.5

9

112.7

7

114.2

2

116.0

4

118.2

2

121.8

3

126.6

5 131.80

2

Break Even Point

(B.E.P.)

56.45

%

57.24

%

57.89

%

51.66

%

52.56

%

53.65

%

48.23

%

49.93

%

52.16

%

48.55

%

Average B.E.P. 52.83%

1.13. Projected Balance Sheet for the Project (10 Year) # Description Construc

tion

Period

Operation Period in Years

0 1st

Yr.

2nd

Yr

3rd

Yr

4th

Yr

5th

Yr

6th

Yr

7th

Yr

8th

Yr

9th

Yr

10th

Yr

1 Liabilities

1.

1 Equity 37.20

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

37.2

0

1.

2 General reserves 0

61.7

8

120.

60

178.

48

256.

04

332.

07

406.

27

499.

29

589.

19

675.

06

777.

58

1.

3 Debt 97.40

97.4

0

81.0

0

64.6

0

48.2

0

31.8

0

15.4

0 0.00 0.00 0.00 0.00

1.

4 Current Liabilities 0.00 0.46 0.51 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50

1.

5

Working Capital

Loan 0.00

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

49.6

9

Total Liabilities 134.59

246.

53

289.

00

330.

47

391.

63

451.

26

509.

06

586.

69

676.

58

762.

46

864.

97

2 Assets

2.

1 Gross Fixed Assets 112.31

112.

31

112.

31

112.

31

112.

31

112.

31

112.

31

112.

31

112.

31

112.

31

112.

31

2.

2

Accumulated

Depreciation 0

11.4

8

21.3

9

29.9

6

37.4

0

43.8

7

49.5

1

54.4

4

58.7

5

62.5

5

65.9

0

2.

3

Net fixed assets

(2.01-2.02) 112.31

100.

83

90.9

2

82.3

5

74.9

1

68.4

4

62.8

0

57.8

8

53.5

6

49.7

6

46.4

1

2.

4

Preliminary

Expenses 1.00 0.90 0.80 0.70 0.60 0.50 0.40 0.30 0.20 0.10 0.00

2.

5

Pre-Operative

Expenses 21.28

21.2

8

18.9

2

16.5

5

14.1

9

11.8

2 9.46 7.09 4.73 2.36 0.00

2.

6 Current Assets 0.00

14.4

9

16.5

6

16.5

6

16.5

6

16.5

6

16.5

6

16.5

6

16.5

6

16.5

6

16.5

6

2.

7

Profit & Loss

Account 0.00 0.00 0 0 0 0 0 0 0 0 0

2.

8

Cash & Bank

Balance 0.00

109.

03

161.

80

214.

32

285.

38

353.

94

419.

84

504.

86

601.

54

693.

68

802.

00

Total Assets 134.59

246.

53

289.

00

330.

47

391.

63

451.

26

509.

06

586.

69

676.

58

762.

46

864.

97

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 24

1.14. Environment Consideration Maintaining and sustaining the environment is of paramount importance for this

project. The manufacturing process contains no harmful ingredient. It will not create

any effluent and chemical waste. However, the plant is designed to be environment

friendly and prioritises to maintain neat and clean atmosphere through its industrial

process activities.

It’s an eco-plant and environment management system ISO 14001 will be

implemented and followed strictly to ensure that there is no compromise in

environment management.

1.15. Conclusion Beauty products like soap, shampoo and body care cater to the daily needs of people.

Some entrepreneurs have started manufacturing herbal glycerine-based soap to know

the liking of users “keeping away the chemicals normally used in these products”. The

demand is ample and it has wide scope in the domestic as well as the international

market and the main focus country is Germany. It is covered under small industry

segment and can be managed through technical collaboration with companies from

India and Thailand.

The project is financially viable with Net Profit Ratio of 14.24%. It needs around 25

employees including managerial staff, and skilled and unskilled staff to operate the

plant. The financial ratios are positive during the first 7 years of operation. The average

DSCR is 4.51which implies that the project generates sufficient funds to cover its cost,

including loan repayments and interest payments during the period. This also indicates

that the project can continue making profits even after 7 years.

The required machinery and equipment for the production of soap and allied products

can be imported from India, Thailand and Italy.

Based on the estimation of project cost and financial analysis, the production of Beauty

Care product manufacturing unit is financially viable, profitable with a good rate of

return. It is recommended to entrepreneurs to scale up to industrial level.

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 25

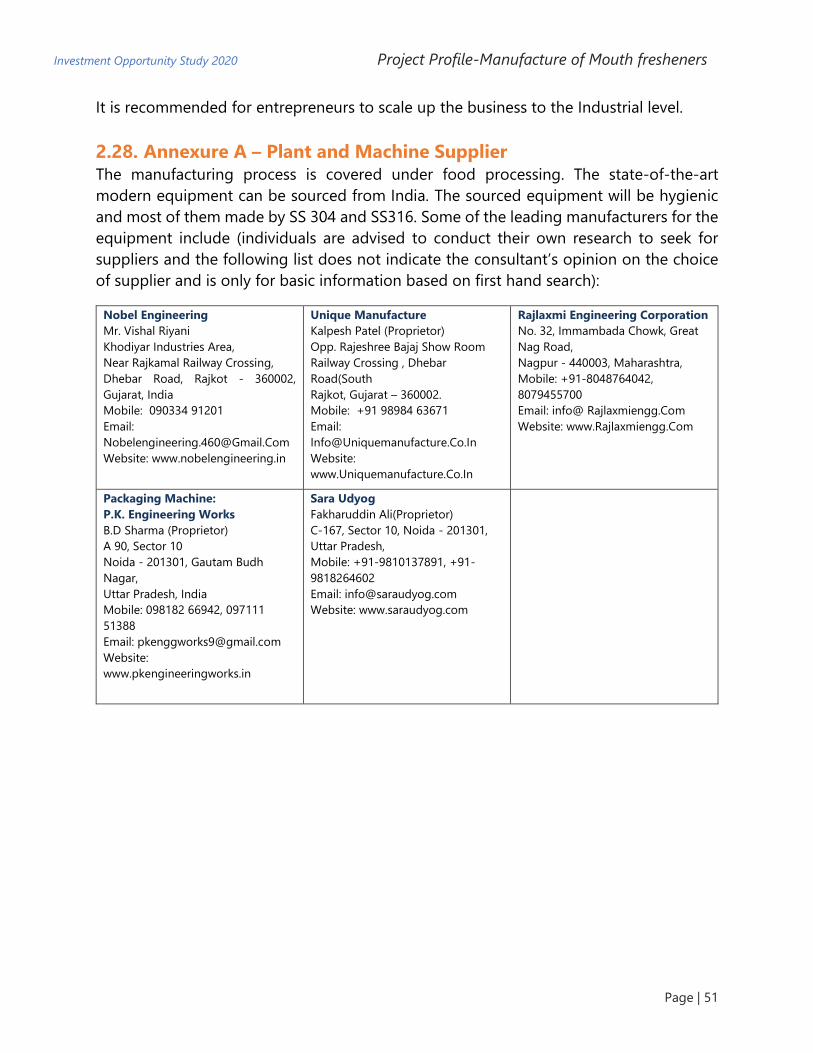

1.16. Annex A: List of Equipment Suppliers The manufacturing process is covered under engineering sector. The state-of-the-art modern

equipment can be sourced from India. Some of the leading manufacturers of equipment

include (individuals are advised to conduct their own research to look for suppliers, the

following list does not indicate the consultant’s opinion on the choice of supplier and is

provided only for basic information based on first hand search):

▪ RSB Equipment’s Private Limited

Mr. Atanu Sarkar

435, Jessore Rd, Shyam Nagar, Amarpalli,

Dum Dum, Kolkata, West Bengal 700055

Mobile: 098302 78600,

Email: [email protected],

Website: www.rsbpumps.com

▪ Kishori Kripa Enterprises

Mr. Naveen Bhalla

27, Pandit Park, Shivaji Gali

Krishna Nagar, Delhi - 110051, India

Mobile: +91 9811114589

Email: [email protected]

Website: www.kishorikirpa.com

▪ Golden Engineering Co.

Mr. Tarun Preet Singh

63/27, Opposite Lakhbir Complex,

Chd road, Khanna - 141407 (Punjab) India.

Mobile: +91-88721-77000, 08909241371

Email: [email protected]

Website: www.goldenengineeringcompany.com

▪ Adhisakthi Projects Private Limited

Senthil Kannan (CEO)

No. 20/10, Ganesh Nagar Main Road, G. K. Industrial Estate, Alappakkam,

Porur, Chennai - 600116, Tamil Nadu, India

Mobile: +91 9443203221, 9442255639

Email: [email protected]

Website: www.adhisakthi.com

▪ Sakun Engineers

Mr. Hiten (Proprietor)

33/A, New Arbuda Estate, New Ranip

Ahmedabad - 382470, Gujarat, India

Mobile: +91 9443203221, 9442255639

Email: [email protected]

Website: www.sakunengineers.in

References

▪ BhutanTradeStatistics2019260320201.pdf

▪ www.businesswire.com

▪ www.mof.gov.bt

▪ https://www.equitymaster.com/research-it/sector-info/consprds/consprds-

products.html#:~:text=The%20popular%20and%20economy%20segments,at%201%2C100%20gms%20p

er%20annum.

▪ https://my.msme.gov.in/MyMsmeMob/MsmeProjectProfile/Pages/2_6.html

▪ https://www.diynatural.com/how-to-make-glycerin-soap-base-recipe/

▪ http://www.madehow.com/Volume-2/Soap.html

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 26

Project Title:

Manufacturing of Mouth freshener

(Flavoured Areca nut and Cardamom)

Tobacco Free Product

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 27

2. Manufacturing of Mouth freshener

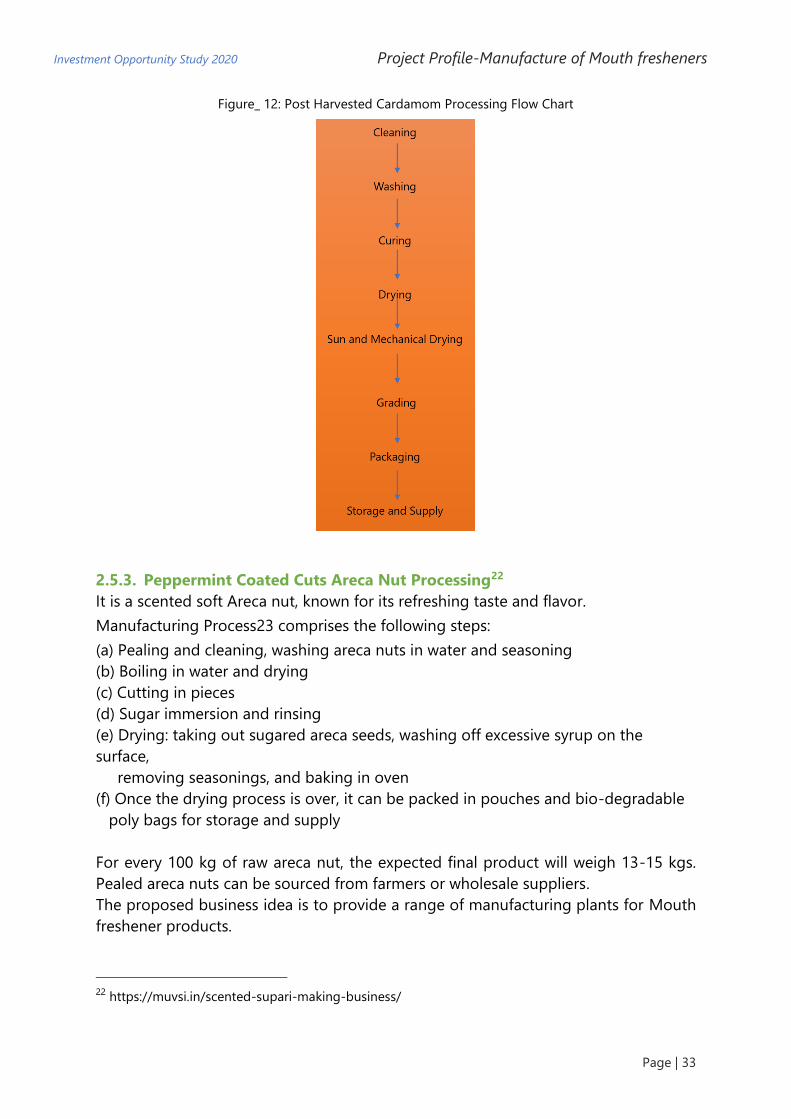

2.1. Background of the Idea People consume mouth fresheners for various reasons but mostly for good breath.

Known as ‘Pan Masala’, it is a very popular product in India and could be described as

a Bhutanese equivalent to Doma-pani.

Popular brands in the Bhutanese market include Rajnigandha, Rajnigandha Pearls,

Shakila, Shikar. None of these contain tobacco. The basic composition can vary based

on the brand and product but could consist of a balanced mixture of areca nuts (also

known as supari), catechu, cardamom, lime, flavoring agents and some natural

perfuming materials.

In reference to the Bhutan Trade Statistics, following highlights are presented;

i. Some types of pan masala are produced in Bhutan.

ii. Exports have plummeted possibly on the account of India’s GST.

iii. Import has still increased by 72% in 2019 as compared to 2018 indicating that

either the demand has substantially increased15.

On the supply side, Bhutan is having a rich production of Cardamom and Areca nut.

The southern Dzongkhags of Sarpang and Samtse lead the production. While the

production of Areca nut has been on the rise, cardamom production has been

▪ 15 BhutanTradeStatistics2019260320201.pdf

2014 2015 2016 2017 2018 2019

Imp_Pan masala 21 26 21 23 16 28

Exp_Pan masala 43 20 21 17 3 0

21

26

21 23

16

28

43

20

21

17

3

0 -

5

10

15

20

25

30

35

40

45

50

Imp_Pan masala Exp_Pan masala

Figure_ 7: Trade Statistics of Pan Masala (Nu. in Millions)

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 28

declining on the account of poor market price (or rather poorer price as compared to

few years ago).

Figure_ 8: Cardamom and Arecanut Production in Bhutan (MT)

2014 2015 2016 2017 2018

Arecanut 7468 9406 9467 9342 11681

Cardamom 1781 2091 2736 2245 1542

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Cardamom Arecanut

Investment Opportunity Study 2020 Project Profile-Manufacture of Mouth fresheners

Page | 29

2.2. Market Outlook International16

India is the major producer and consumer of areca nut in the world17. Production is

concentrated in six states, namely Karnataka, Kerala, Assam, Meghalaya, Tamil Nadu

and West Bengal. There is an ever-increasing demand for mouth freshener products.

Among the various types of pan masala available in the Indian market, pan masala

containing tobacco represents the dominating type accounting for more than 50% of

the entire market. Pan masala containing tobacco is followed by plain pan masala and

flavoured pan masala. Exports also represent a major driver of the Indian pan masala

market.

The biggest export market for Indian pan masala is the UAE accounting to one-third

of the total export. UAE is followed by USA, Singapore, Afghanistan, South Africa, Saudi

Arabia and Malaysia.

The majority of the Indian pan masala market is highly disorganised and is surrounded

by few players, namely, DS GROUP, Manikchand Group, Godfrey Phillips India Ltd,

Kothari Product Limited, Trimurti Fragrances Pvt. Ltd, Sugandha Exports, Dharampal

Premchand Limited, and Red Rose Group, among others. Among these players,

Rajnigandha represented the largest manufacturer of pan masala accounting for the

majority of the market share. It was followed by RMD, Pan Vilas, Pan Parag and others.

Factors like its immense popularity, constantly increasing disposable incomes,