International Competitiveness of Botswana’s beef industry

Tebogo B. Seleka

Pinkie G. KebakileBotswana Institute for Development Policy Analysis

Conference on Policies for Competitive Smallholder Livestock ProductionGaborone, Botswana, 4-6 March 2015

Outline

• Introduction

• Measuring international Competitiveness

• Results

- Against SADC countries

- Against leading beef exporters

• Factors underlying Botswana’s beef industry competitiveness

Introduction

• Beef industry in Botswana plays a key role in the economy.

- It accounts for a large proportion of agricultural value added.

- It is the second leading source of export revenue after minerals.

- It is one of the key sources of livelihood among rural dwellers – as a source of income and employment (including self-employment).

• However;

- Its share of agricultural value added has declined over time.

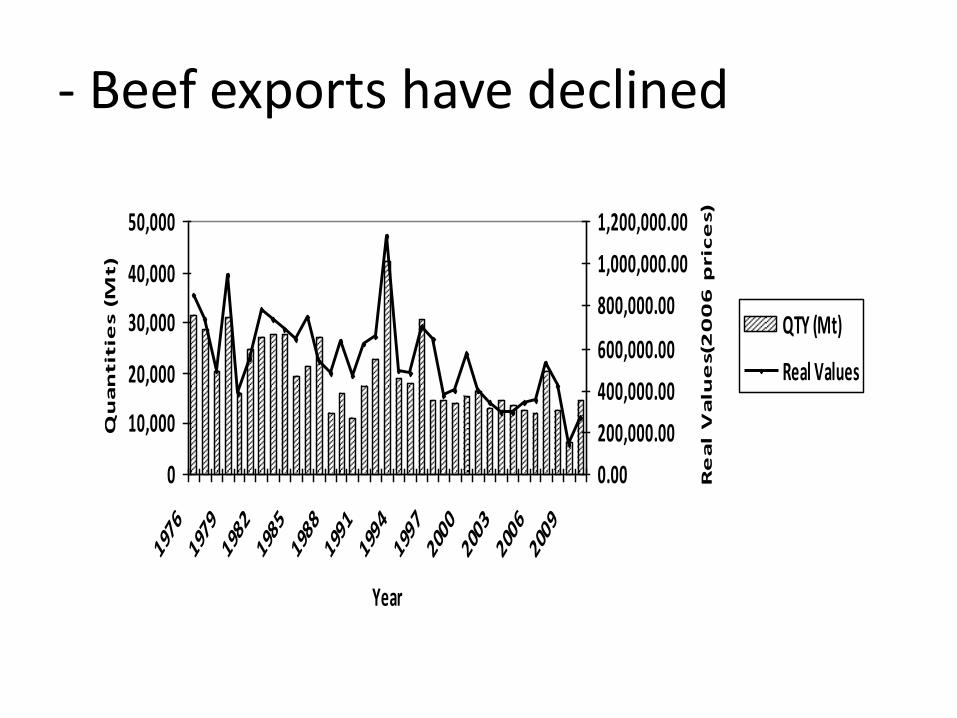

- Beef exports have declined

0

10,000

20,000

30,000

40,000

50,000

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

Year

Qu

an

tit

ies (

Mt)

0.00

200,000.00

400,000.00

600,000.00

800,000.00

1,000,000.00

1,200,000.00

Re

al

Va

lue

s(2

00

6 p

ric

es)

QTY (Mt)

Real Values

Measuring international competitiveness

• RCA1ij= xij/xnj

• RCA2ij=(xij/xnj)/(xik/xnk)

• RCA3ij=(xij-mij)/(xij+mij)

• NPij=(xij-mij)/pij

• PCij=pij/cij

- RCA=Revealed comparative advantage, x= exports, m=imports, I= country I, j = beef, k= all agricultural commodities, n=set of countries (SADC or leading beef exporters), NP = ratio of net trade to production, PC=ratio of production to consumption, p = production, c= consumption.

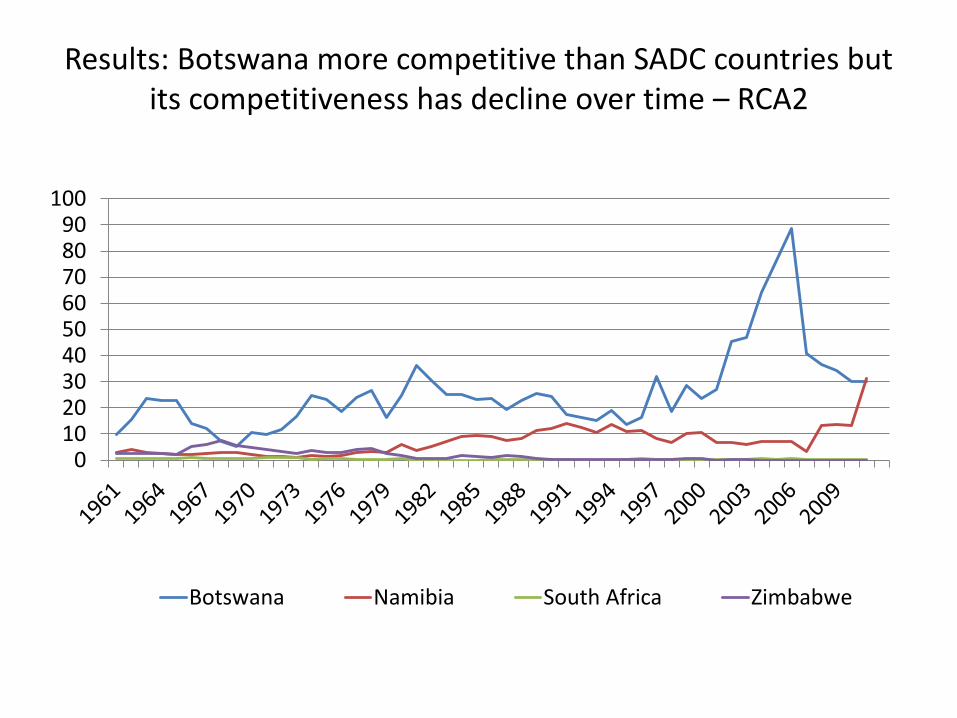

Results: Botswana more competitive than SADC countries but its competitiveness has decline over time – RCA2

0102030405060708090

100

Botswana Namibia South Africa Zimbabwe

Ratio of net trade to production

-0.2

0

0.2

0.4

0.6

0.8

1

Botswana Namibia South Africa Zimbabwe

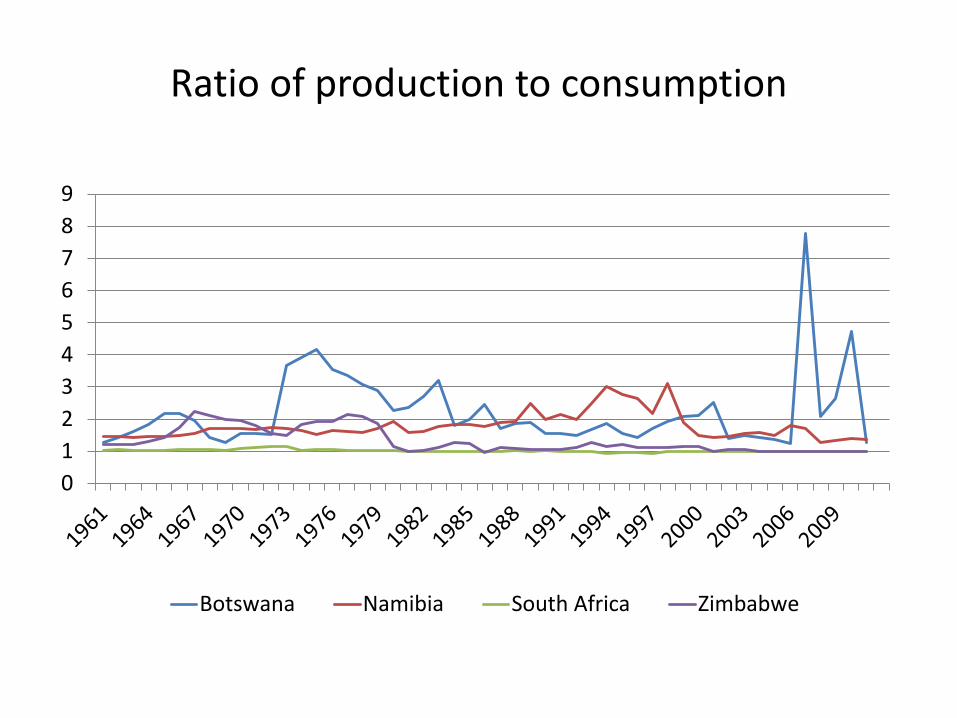

Ratio of production to consumption

0

1

2

3

4

5

6

7

8

9

Botswana Namibia South Africa Zimbabwe

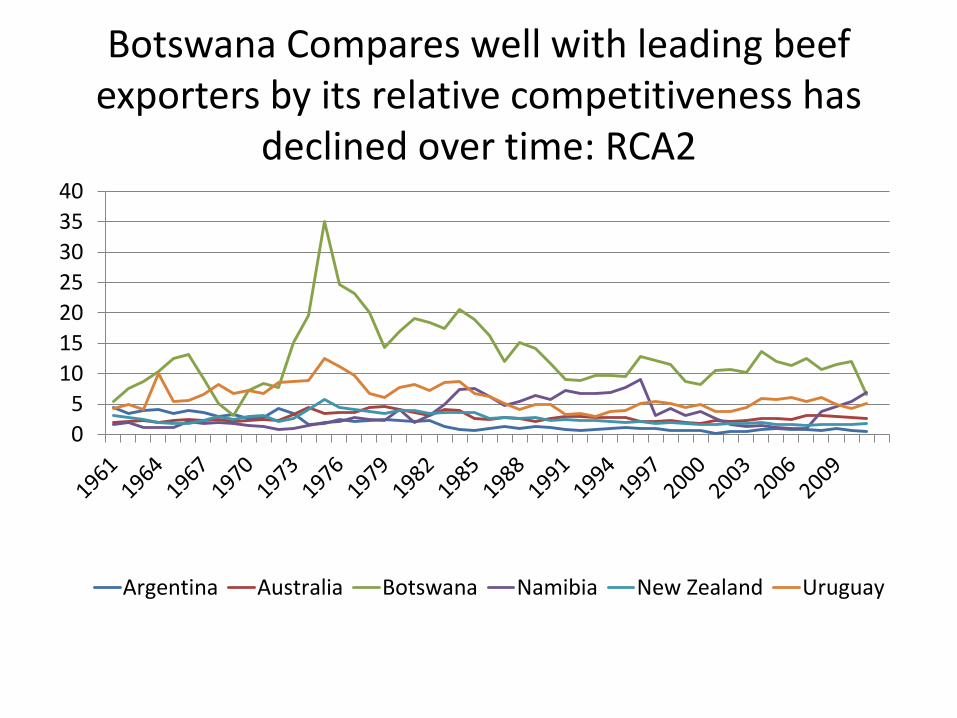

Botswana Compares well with leading beef exporters by its relative competitiveness has

declined over time: RCA2

0

5

10

15

20

25

30

35

40

Argentina Australia Botswana Namibia New Zealand Uruguay

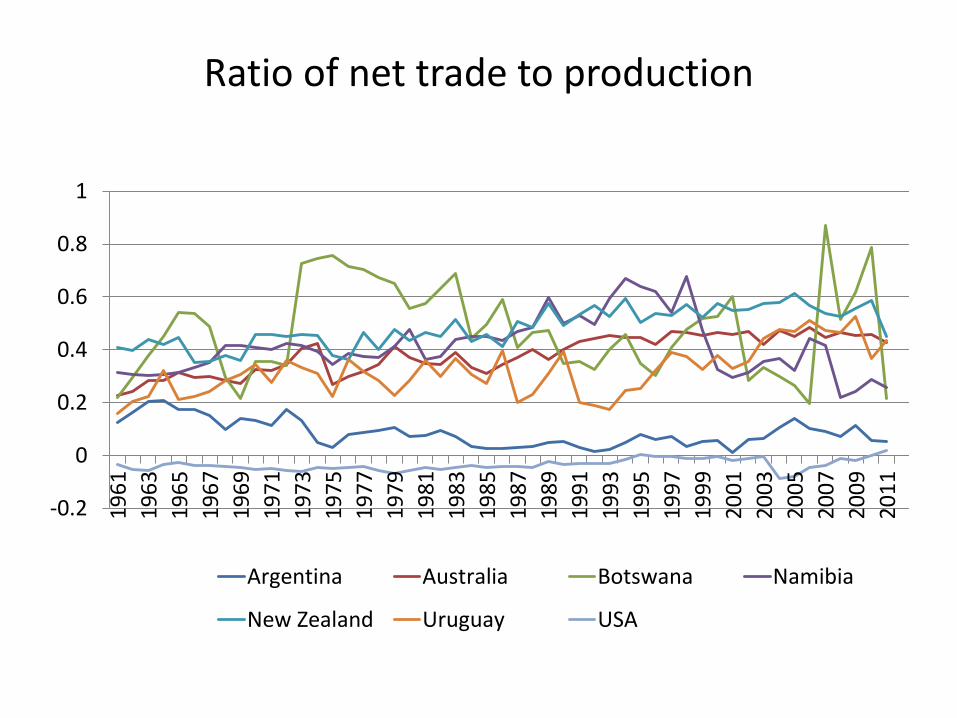

Ratio of net trade to production

-0.2

0

0.2

0.4

0.6

0.8

1

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

Argentina Australia Botswana Namibia

New Zealand Uruguay USA

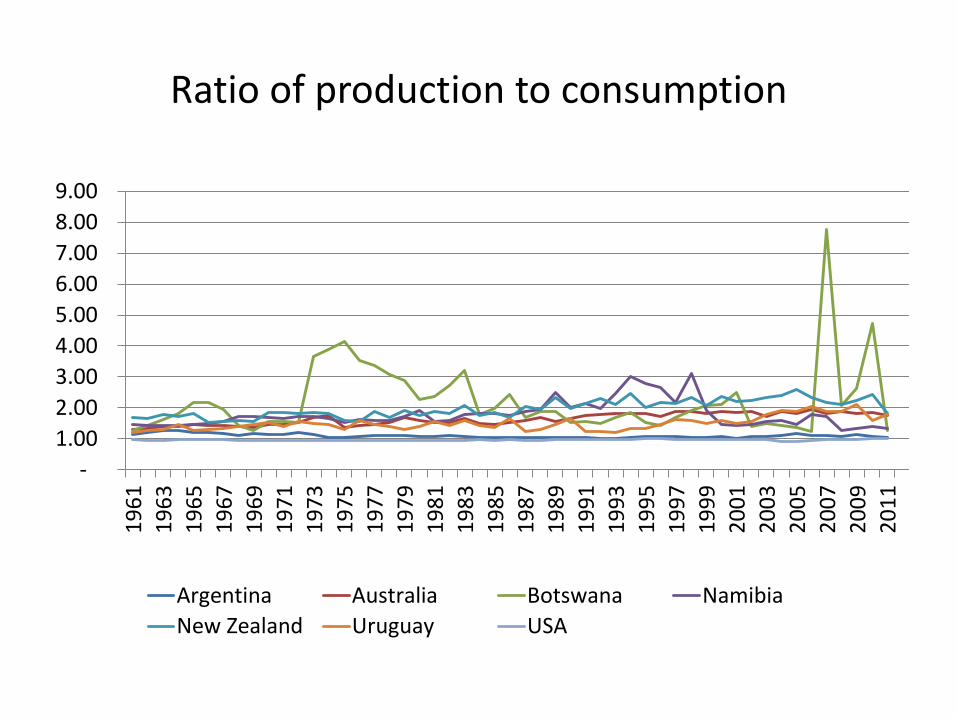

Ratio of production to consumption

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

Argentina Australia Botswana Namibia

New Zealand Uruguay USA

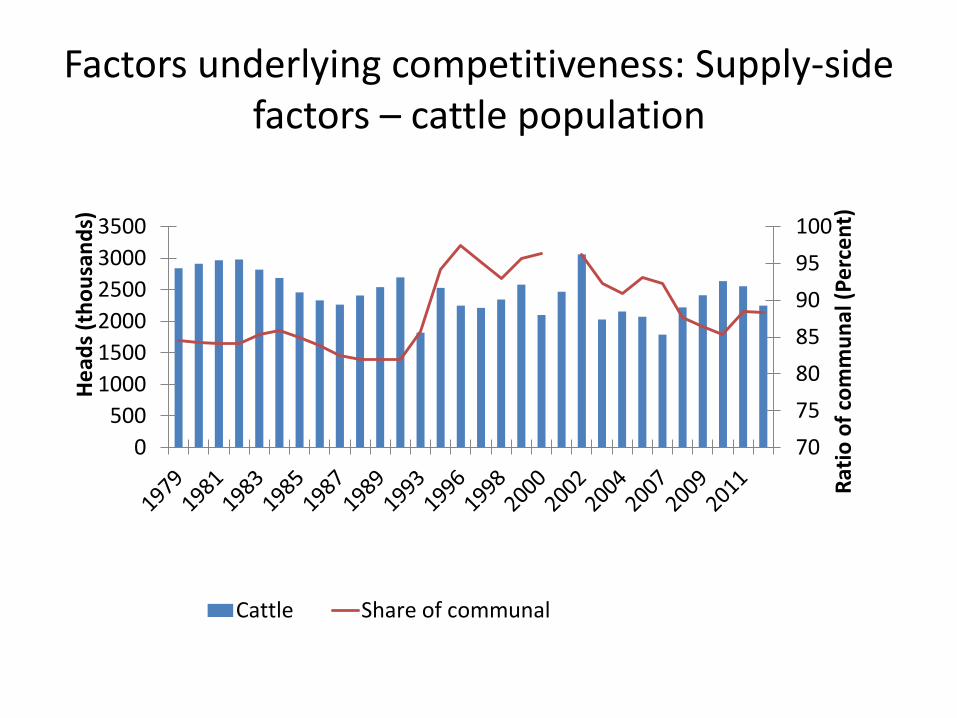

Factors underlying competitiveness: Supply-side factors – cattle population

70

75

80

85

90

95

100

0

500

1000

1500

2000

2500

3000

3500

Rat

io o

f co

mm

un

al (

Pe

rce

nt)

He

ads

(th

ou

san

ds)

Cattle Share of communal

• Poor productivity indicators

- Mortality rates averages 12 percent in communal system – although they have improved over time

- Off-take rates averaged 8 percent under communal arrangements

- Calving rates averaged 57 percent and have stagnated over time.

- Cattle prices declined consistently from 1974 to 2006.

- Disease outbreak (FMD).

- Recurrent drought

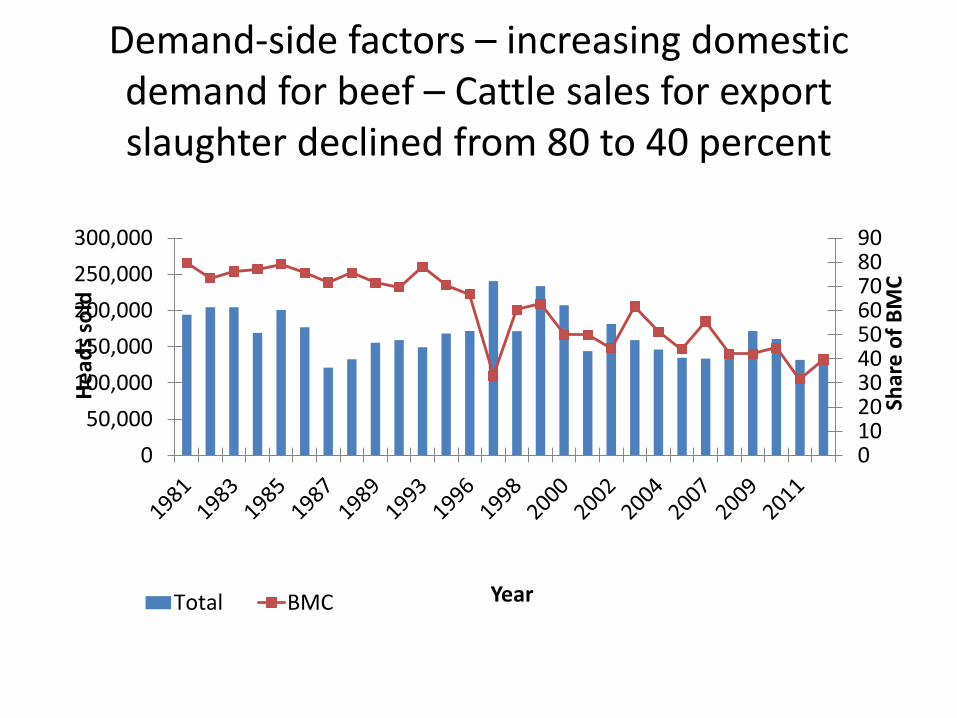

Demand-side factors – increasing domestic demand for beef – Cattle sales for export slaughter declined from 80 to 40 percent

0102030405060708090

0

50,000

100,000

150,000

200,000

250,000

300,000

Shar

e o

f B

MC

He

ads

sold

YearTotal BMC

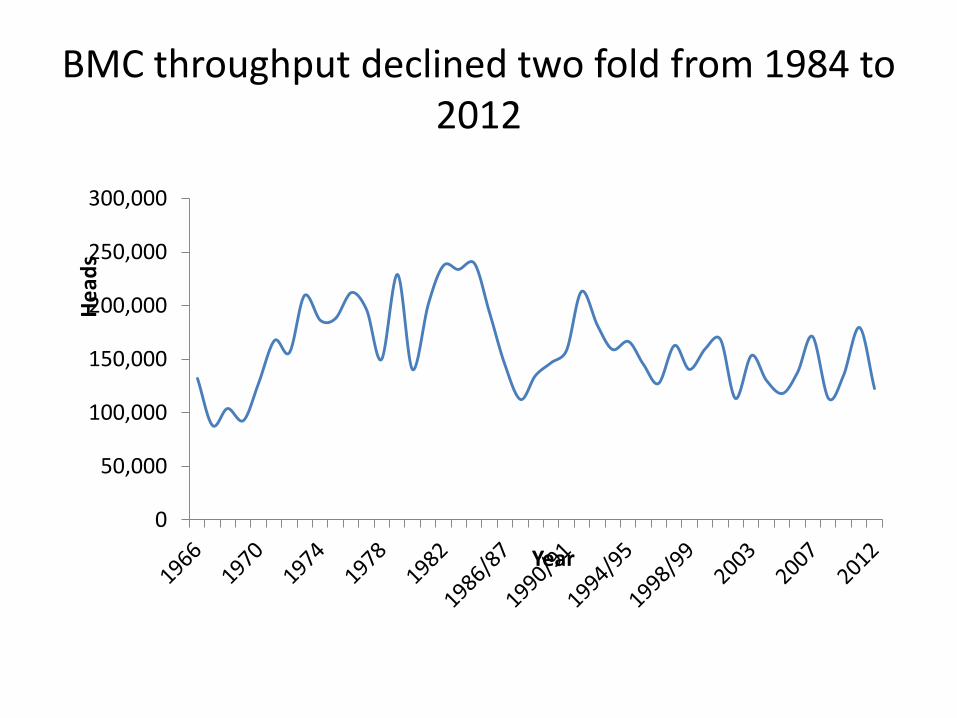

BMC throughput declined two fold from 1984 to 2012

0

50,000

100,000

150,000

200,000

250,000

300,000

He

ads

Year

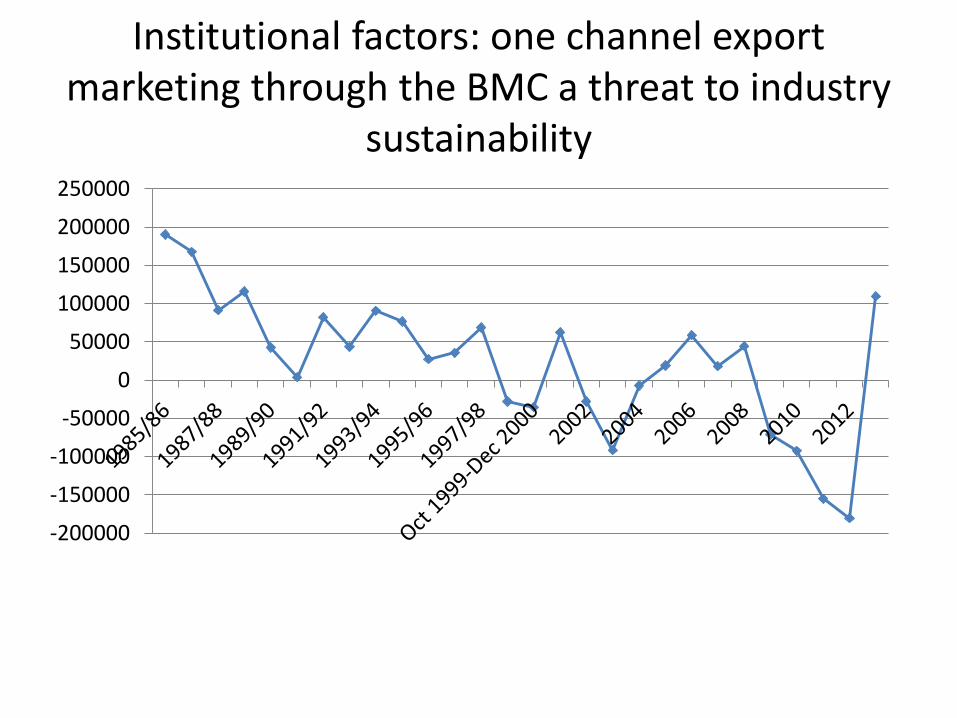

Institutional factors: one channel export marketing through the BMC a threat to industry

sustainability

-200000

-150000

-100000

-50000

0

50000

100000

150000

200000

250000

• Preference erosion in the EU market due to future policy reforms.

Conclusions• Botswana’s beef industry is more competitive

than other SADC countries, but compares well with leading beef exporters.

• Declining competitiveness levels are due to low and stagnant productivity.

• Increasing domestic demand for beef in Botswana, which has resulted in declining exports.

• Future threats include single channel export marketing and possible preference erosion in the EU market.