INTERMEDIATE ACCOUNTING

Chapter 19Accounting for Postretirement Benefits

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

What Types of Pensions Plans Are There?(Slide 1 of 3)

There are two types of pension plans that employers tend to provide their employees: A defined benefit plan is a type of plan in which

the future employee benefit is defined by a formula and the amount that the company contributes into the plan depends on the future needs of the plan.

A defined contribution plan is a type of plan in which the employer’s contribution into the pension fund is based on a formula, so that the future benefits are limited to an amount that can be provided by: The contributions made during the employee’s service to

the company. The return earned on the investment of those

contributions.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

In addition, companies’ pension plans can be: A noncontributory plan where the entire pension

cost is born by the employer (company) A contributory plan where employees bear part

of the cost of the plan and make contributions from their salaries into the pension fund

What Types of Pensions Plans Are There?(Slide 2 of 3)

With respect to Internal Revenue Code (IRC) rules and regulations, pension plans may be either: A qualified pension plan is a type of pension plan

that covers the majority of the company’s employees and limits contributions to certain amounts.

A nonqualified pension plan is a type of pension plan that is not governed by the IRC rules and regulations.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Estimates that the company must make for a defined benefit pension plan include: How many employees will remain with the company

until retirement? What will employees’ retirement benefits will be at

the time? What pension fund assets will be available to pay

retirement benefits? What will be the length of time the employee will

draw retirement benefits? Actuaries are certified professionals who are trained to determine future risk, estimate probabilities of future events, make price decision, estimate present and future values, and formulate investment strategies.

What Types of Pensions Plans Are There?(Slide 3 of 3)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

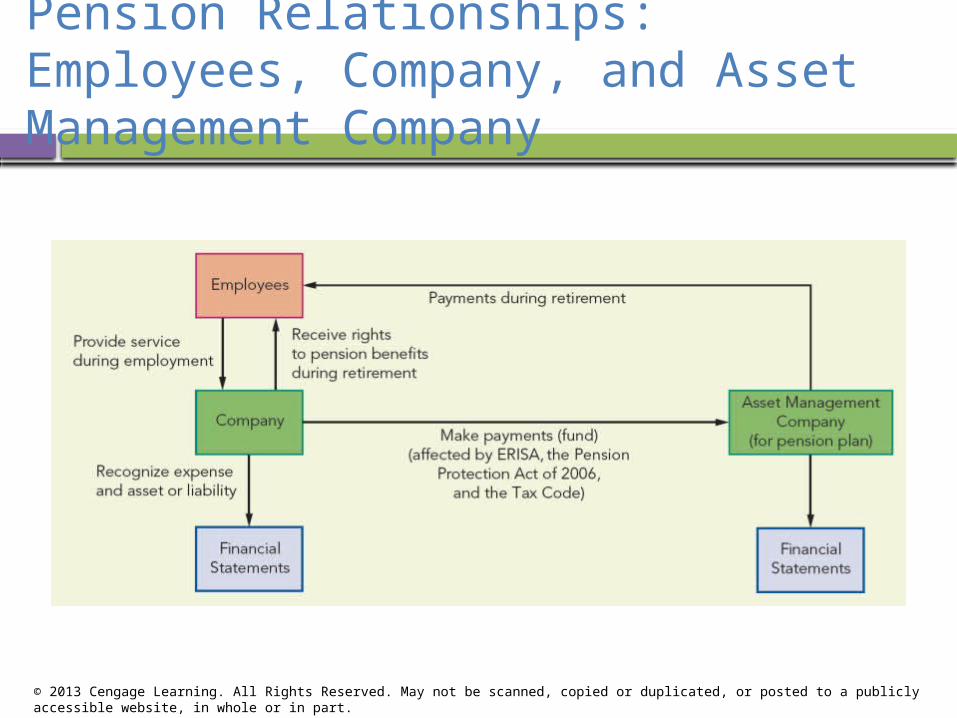

Pension Relationships: Employees, Company, and Asset Management Company

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

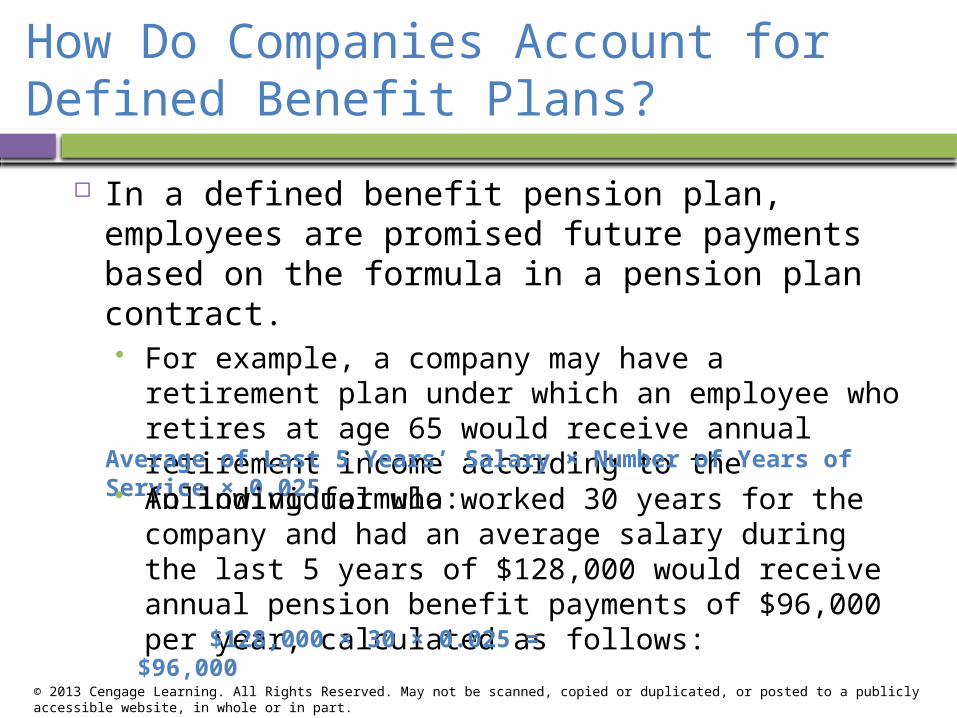

In a defined benefit pension plan, employees are promised future payments based on the formula in a pension plan contract. For example, a company may have a retirement

plan under which an employee who retires at age 65 would receive annual retirement income according to the following formula:

How Do Companies Account for Defined Benefit Plans?

Average of Last 5 Years’ Salary × Number of Years of Service × 0.025

An individual who worked 30 years for the company and had an average salary during the last 5 years of $128,000 would receive annual pension benefit payments of $96,000 per year, calculated as follows: $128,000 × 30 × 0.025 = $96,000

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

What Are the Components of Pension Expense?

GAAP uses the term net periodic pension cost when discussing the cost of a pension plan that is recognized in an employer’s financial statements during an accounting period. This term is used as opposed to pension expense

because a company may capitalize some of its net periodic pension costs as part of an asset.

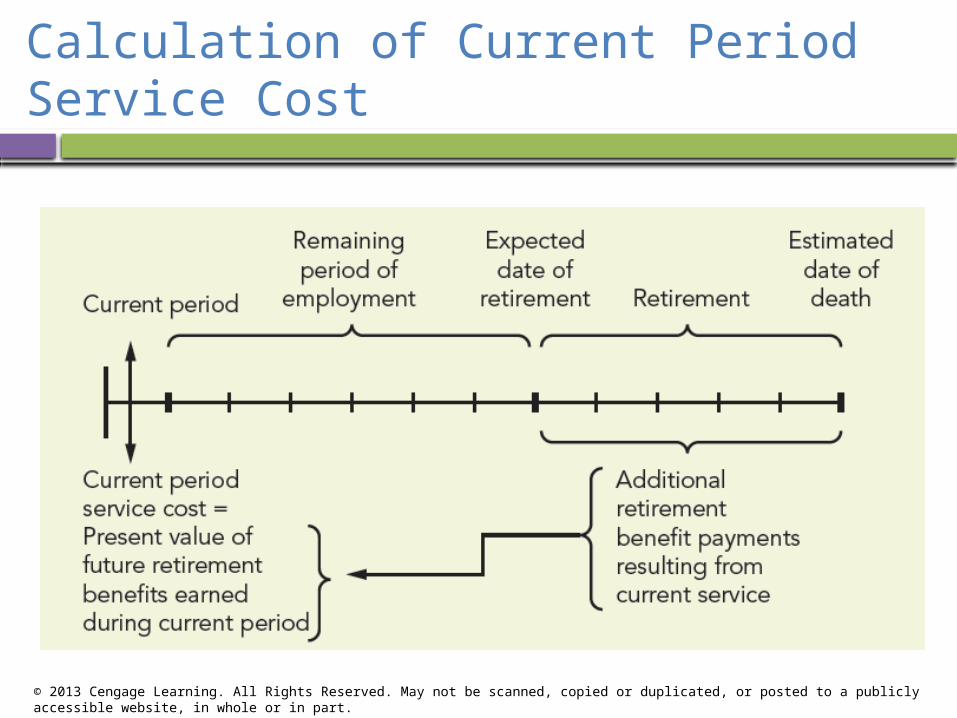

For simplicity, we will use the term pension expense and assume none of the pension costs are capitalized. The service cost is the increase in the

projected benefit obligation due to employees providing service to the company during the current period.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Calculation of Current Period Service Cost

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

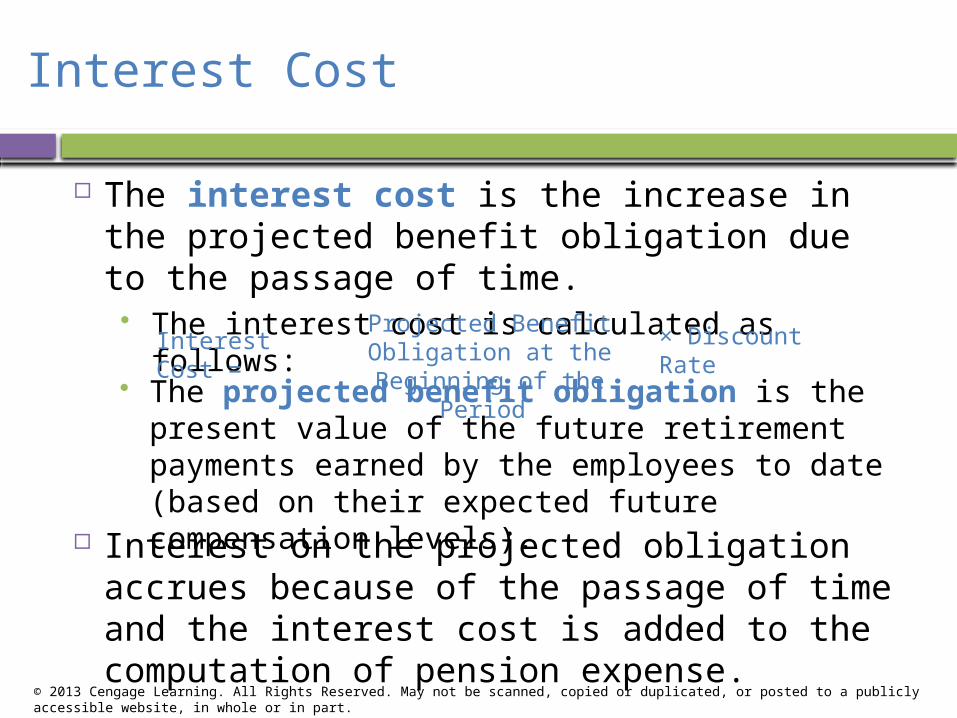

Interest Cost

The interest cost is the increase in the projected benefit obligation due to the passage of time.

The interest cost is calculated as follows:Interest Cost =

Projected Benefit Obligation at the Beginning of the Period

× Discount Rate

Interest on the projected obligation accrues because of the passage of time and the interest cost is added to the computation of pension expense.

The projected benefit obligation is the present value of the future retirement payments earned by the employees to date (based on their expected future compensation levels).

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

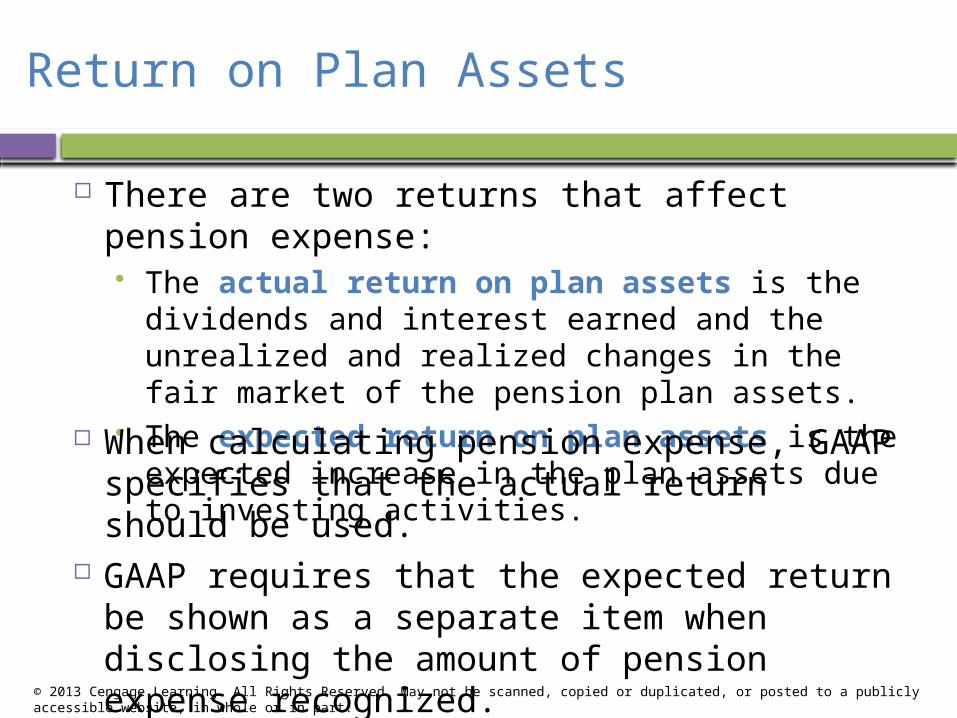

Return on Plan Assets

There are two returns that affect pension expense: The actual return on plan assets is the

dividends and interest earned and the unrealized and realized changes in the fair market of the pension plan assets.

The expected return on plan assets is the expected increase in the plan assets due to investing activities.

When calculating pension expense, GAAP specifies that the actual return should be used.

GAAP requires that the expected return be shown as a separate item when disclosing the amount of pension expense recognized.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Amortization of Prior Service Cost

Often a company will amend its pension plan and this results in an increase in the projected benefit obligation.

Retroactive benefits may also be granted at the initial adoption of a plan.

The cost of these retroactive benefits is the prior service cost.

Amortization of prior service cost assigns an equal amount to each future service period of each active employee who, at the date of the amendment, is expected to receive future benefits under the plan.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Gain or Loss(Slide 1 of 2)

The gain or loss arises because estimates and assumptions are made about many of the items included in the computation of pension costs and benefits.

Current accounting guidance provide three methods for companies to recognize gains and losses in pension expense: Immediate recognition in pension expense Minimum amortization using the corridor

approach Any systematic and rational approach that

results in faster amortization than the corridor approach

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

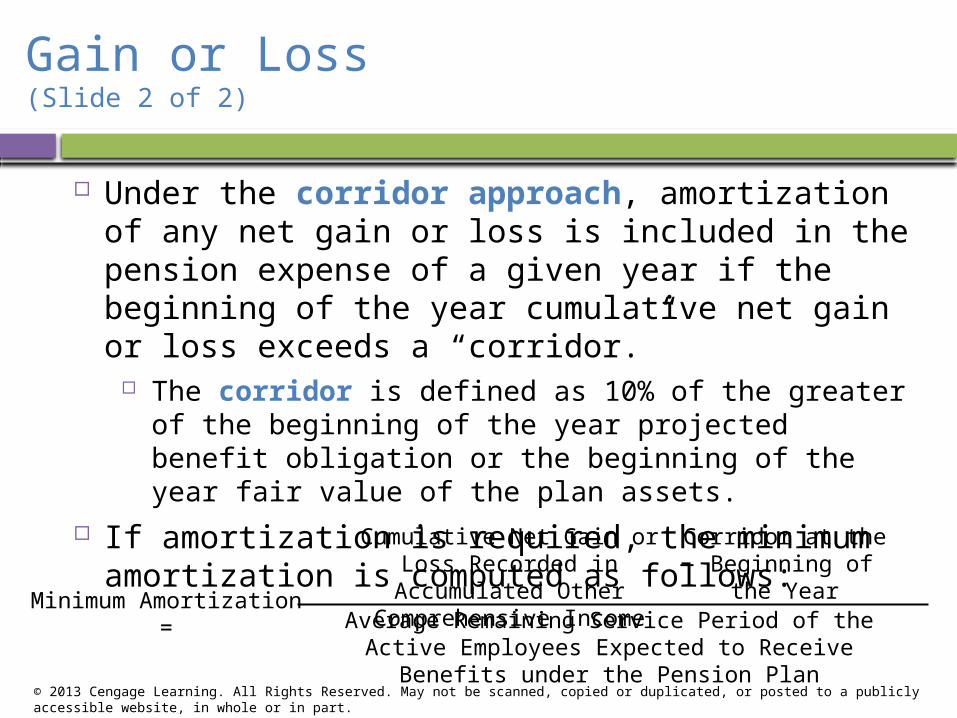

Gain or Loss(Slide 2 of 2)

Under the corridor approach, amortization of any net gain or loss is included in the pension expense of a given year if the beginning of the year cumulative net gain or loss exceeds a “corridor.”

The corridor is defined as 10% of the greater of the beginning of the year projected benefit obligation or the beginning of the year fair value of the plan assets.

If amortization is required, the minimum amortization is computed as follows:

Cumulative Net Gain or Loss Recorded in Accumulated

Other Comprehensive Income

Corridor at the Beginning of the

YearMinimum Amortization =

‒

Average Remaining Service Period of the Active Employees Expected to Receive Benefits under the

Pension Plan

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

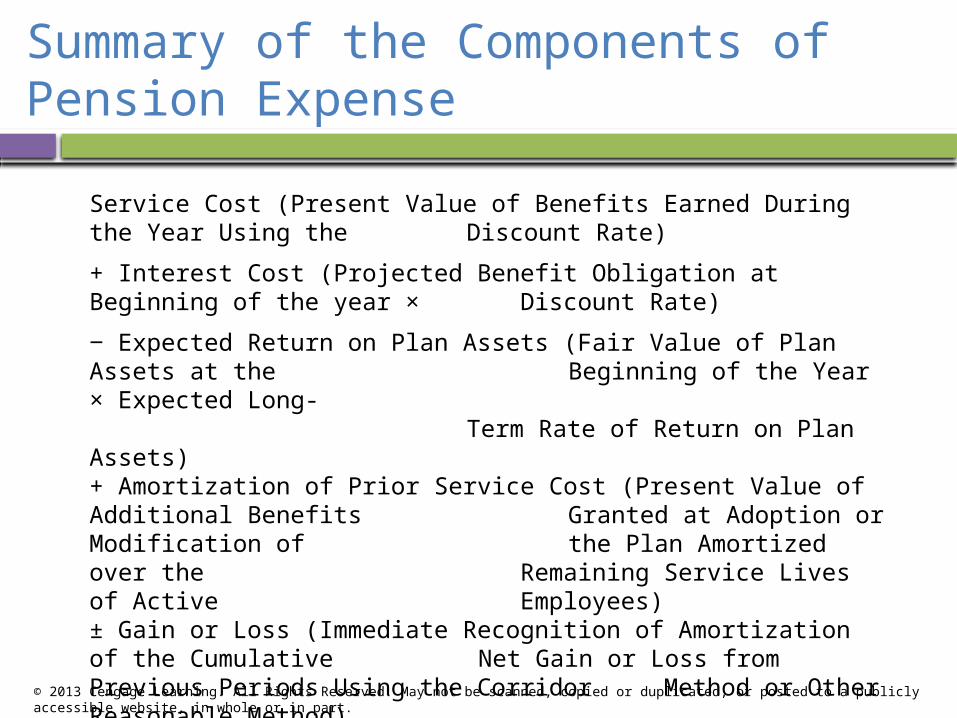

Summary of the Components of Pension Expense

Service Cost (Present Value of Benefits Earned During the Year Using the Discount Rate)

+ Interest Cost (Projected Benefit Obligation at Beginning of the year × Discount Rate)

‒ Expected Return on Plan Assets (Fair Value of Plan Assets at the Beginning of the Year × Expected

Long-Term Rate of Return on Plan

Assets)+ Amortization of Prior Service Cost (Present Value of Additional Benefits Granted at Adoption or Modification of the Plan Amortized over the Remaining Service Lives of Active Employees)± Gain or Loss (Immediate Recognition of Amortization of the Cumulative Net Gain or Loss from Previous Periods Using the Corridor Method or Other Reasonable Method)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

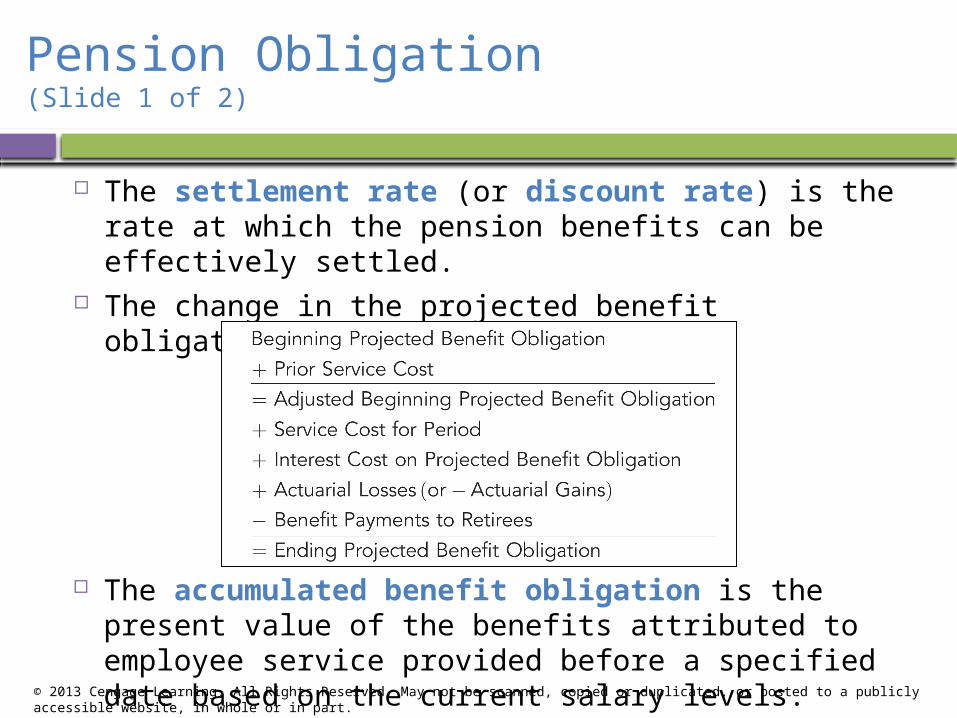

Pension Obligation(Slide 1 of 2)

The settlement rate (or discount rate) is the rate at which the pension benefits can be effectively settled.

The change in the projected benefit obligation is determined as follows:

The accumulated benefit obligation is the present value of the benefits attributed to employee service provided before a specified date based on the current salary levels.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The vested benefit obligation is the actuarial present value of the vested benefits, which are those benefits that the employee have the right to receive if the employee no longer works for the employer.

The projected benefit obligation will provide the largest and most conservative measure of the pension obligation while the vested benefit will be the smallest measure.

Pension Obligation(Slide 2 of 2)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pension Assets

The actuarial funding method is a method to determine the amounts and timing of employer contributions that will be needed over time to provide for current and future pension benefits.

The market-related value is either the fair market value at the end of each accounting period or a calculated value that recognizes changes in fair value in a systematic or rational manner over not more than 5 years.Beginning Fair Value of Pension Plan Assets

+ Actual Return on Plan Assets

+ Contributions (Amount Funded) by the Company

‒ Payments to Retirees

= Ending Fair Value of Pension Plan Assets

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Accrued/Prepaid Pension Cost(Slide 1 of 3)

When a company recognizes pension expense, the between pension expense and the amount contributed to the pension fund is recorded in the Accrued/Prepaid Pension Cost account.

The difference between the projected benefit obligation and the fair value of the pension plan assets at the end of the period is the funded status of the pension plan.

If the projected benefit obligation is greater than the fair value of the pension plan assets (the plan is underfunded), the accrued/prepaid pension cost is reported as a liability.

If the projected benefit obligation is less than the fair value of the pension plan assets (the plan is overfunded), the accrued/prepaid pension cost is reported as an asset.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The adjustment to Other Comprehensive Income can be separated into two components: Retroactive benefits (prior service cost)

that have been granted and are amortized into pension expense

Gains or losses (which include the difference between the actual and expected return on plan assets, as well as any actuarial gains or losses)

Accrued/Prepaid Pension Cost(Slide 2 of 3)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

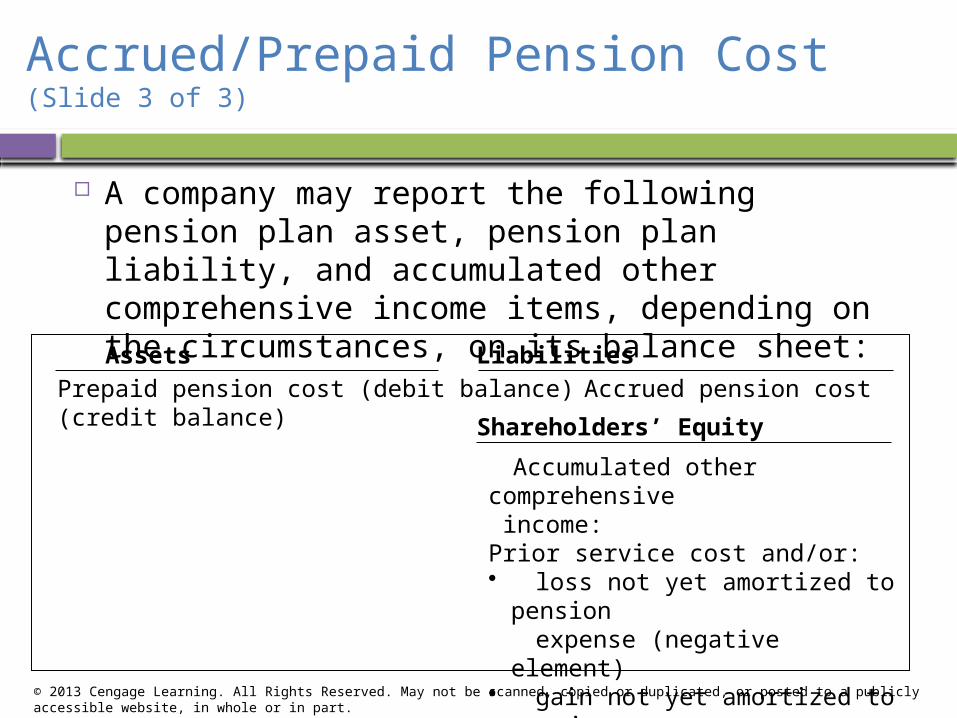

A company may report the following pension plan asset, pension plan liability, and accumulated other comprehensive income items, depending on the circumstances, on its balance sheet:

Accrued/Prepaid Pension Cost(Slide 3 of 3)

Assets LiabilitiesPrepaid pension cost (debit balance) Accrued pension cost (credit balance) Shareholders’ Equity

Accumulated other comprehensive income:Prior service cost and/or:• loss not yet amortized to

pension expense (negative element)

• gain not yet amortized to pension

expense (positive element)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Conceptual Issues: Prior Service Cost

Accounting regulators considered four alternative methods for how the prior service cost should be initially considered:

Account for it prospectively. Recognize the total amount as an expense in the

period in which it arises (i.e., the current period) and record a liability.

Recognize the liability and reduce other comprehensive income, and then amortize the prior service coast as a component of pension expense. In addition, the liability is reduced and other comprehensive income is increased as the prior service amount is amortized.

Decrease retained earnings (as a retrospective adjustment because they reflect prior service) and record a liability.

(GAAP)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Conceptual Issues: Presentation of Pension Plan Assets

There are two alternative views for accounting by the employer for pension assets:

Funding is a discharge of the pension liability. The pension liability is not discharged until the

retiree receives the pension payment. The second approach is required by GAAP, except

that the projected benefit obligation is netted against the pension plan assets to determine the underfunding (liability) or overfunding (asset).

If a company has multiple defined benefit pension plans, the plans cannot be netted against each and must be reported separately on the balance sheet.

(GAAP)

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Conceptual Issue: Pension Liabilities

In making the decision on what liability should be used in pension accounting, regulators examined five alternatives to determine which best met the recognition measure criteria of a liability:

Contribution based on an actuarial funding method Amount attributed to employee service to date Termination liability Amount of vested benefits Amount payable to retirees

Accounting regulators settled on the second alternative. The only exception made is the projected benefit obligation is netted against the pension plan assets to determine underfunding (liability) or overfunding (asset).

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Reporting Issues

Statement of cash flows disclosures A company reports the cash it paid to fund its

pension plan as a cash outflow in the operating activities section of its statement of cash flows.

If a company uses the indirect method, the adjustment is only for the amount of the accrual for the difference between the expense and the funding. It does not include the amount of the adjustment for over- or underfunding because that amount did not affect income. Vested benefits

ERISA specifies the minimum vesting requirements that companies must follow.

A company must disclose the vested portion of the accumulated benefit obligation.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Multiemployer Plans

In our examples, we assumed that the pension plan is a single-employer plan. That is, the plan is maintained by one

company for its employees. In contrast, a multiemployer plan

involves two or more unrelated companies in which assets contributed by each company are available to pay benefits to the employees of all the involved companies.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Other Postemployment Benefits

Other postemployment benefits (OPEB) are provided to former employees after employment but before retirement.

Under GAAP, a company must accrue the cost of these benefits during employment and recognize the amount as an expense and a liability if the four criteria for the recognition of compensated absences are met.

Other postemployment benefits include all forms of benefits provided to former employees after their retirement, other than pensions.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

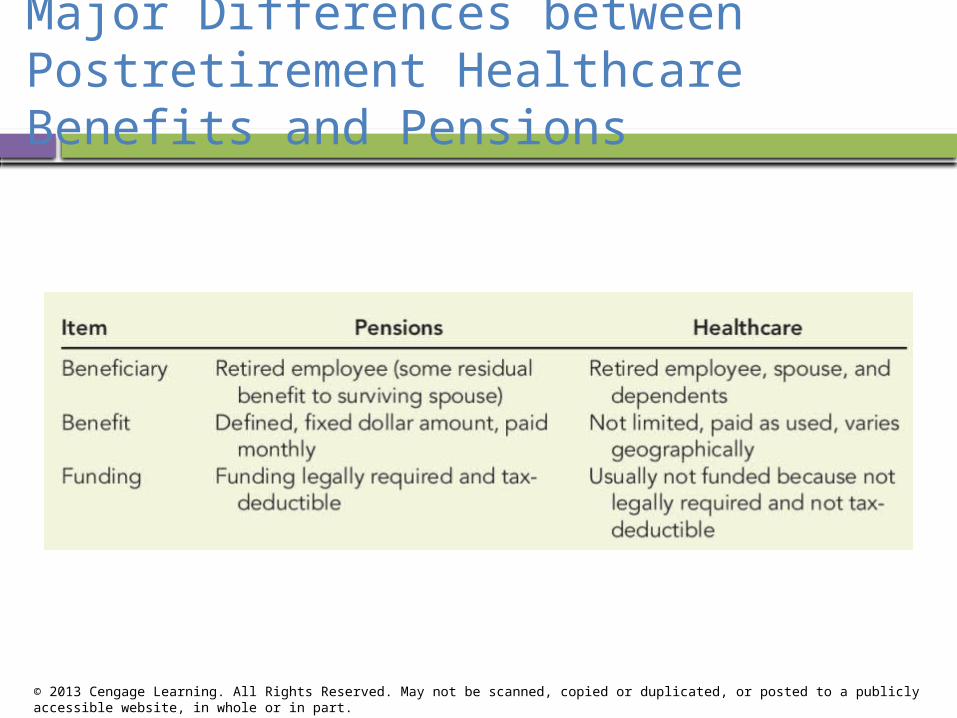

Major Differences between Postretirement Healthcare Benefits and Pensions

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Accounting Principles

The expected postretirement benefit obligation (EPBO) is the actuarial present value of the benefits a company expects to pay under the terms of the postretirement benefit plan. The present value amount is measured as of the

balance sheet date. It is based on the benefits that employees will

receive after their expected retirement dates. The accumulated postretirement benefit

obligation (APBO) is the actuarial present value of the benefits attributed to employee service rendered to a specific date.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

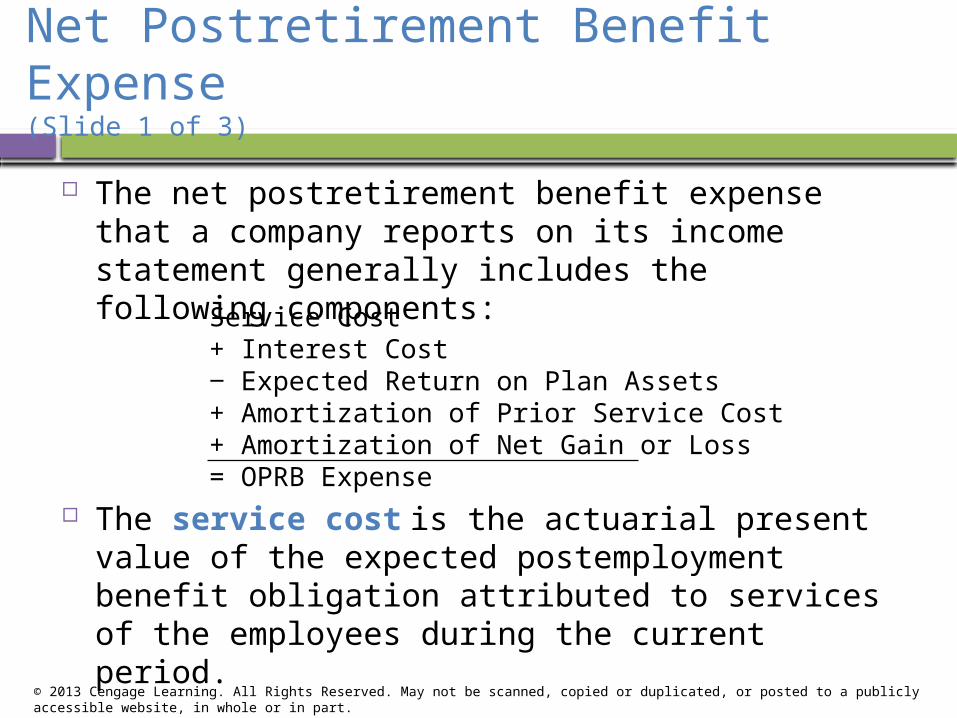

Net Postretirement Benefit Expense(Slide 1 of 3)

The net postretirement benefit expense that a company reports on its income statement generally includes the following components:

Service Cost+ Interest Cost‒ Expected Return on Plan Assets+ Amortization of Prior Service Cost+ Amortization of Net Gain or Loss= OPRB Expense

The service cost is the actuarial present value of the expected postemployment benefit obligation attributed to services of the employees during the current period.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

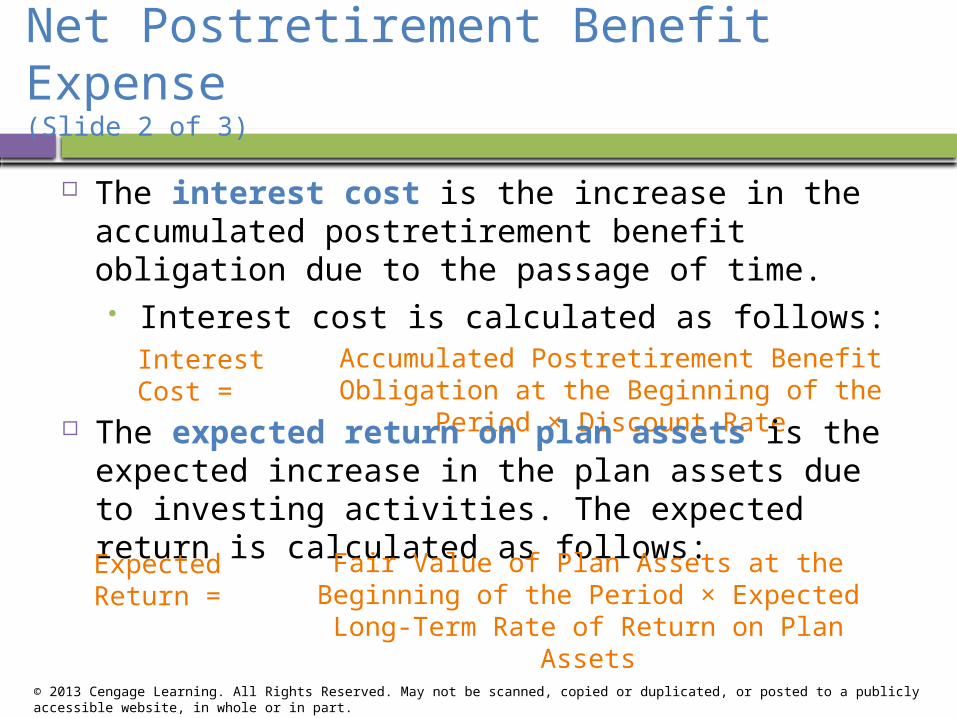

Net Postretirement Benefit Expense(Slide 2 of 3)

The interest cost is the increase in the accumulated postretirement benefit obligation due to the passage of time.

Interest cost is calculated as follows:Interest Cost =

Accumulated Postretirement Benefit Obligation at the Beginning of the Period ×

Discount Rate The expected return on plan assets is the expected increase in the plan assets due to investing activities. The expected return is calculated as follows:Expected Return =

Fair Value of Plan Assets at the Beginning of the Period × Expected

Long-Term Rate of Return on Plan Assets

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

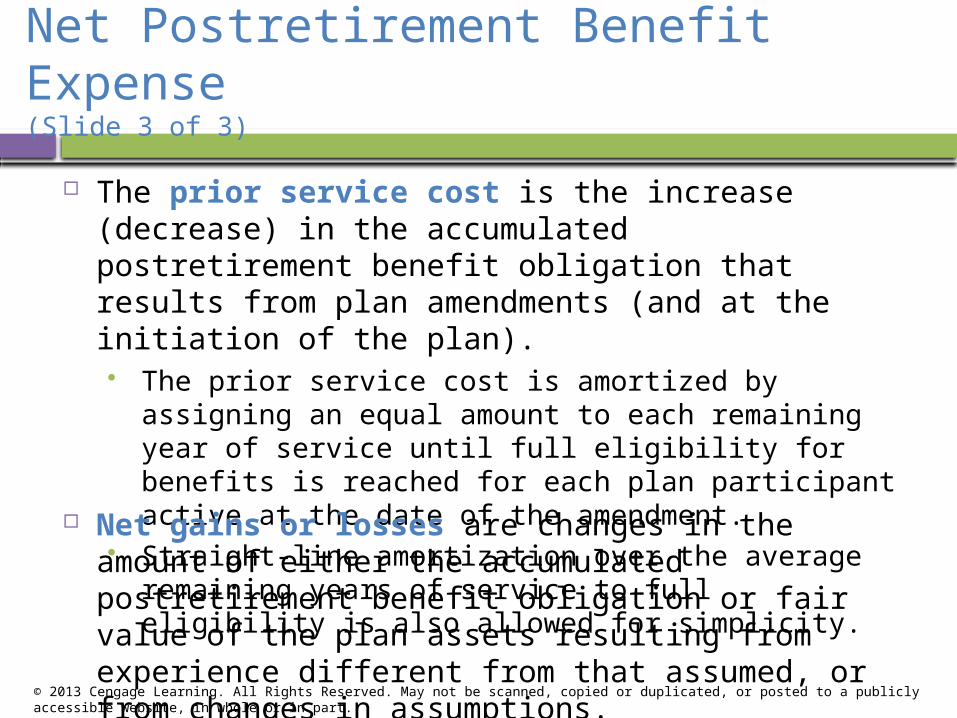

Net Postretirement Benefit Expense(Slide 3 of 3)

The prior service cost is the increase (decrease) in the accumulated postretirement benefit obligation that results from plan amendments (and at the initiation of the plan). The prior service cost is amortized by assigning an

equal amount to each remaining year of service until full eligibility for benefits is reached for each plan participant active at the date of the amendment.

Straight-line amortization over the average remaining years of service to full eligibility is also allowed for simplicity.

Net gains or losses are changes in the amount of either the accumulated postretirement benefit obligation or fair value of the plan assets resulting from experience different from that assumed, or from changes in assumptions.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Other Pension Terminology

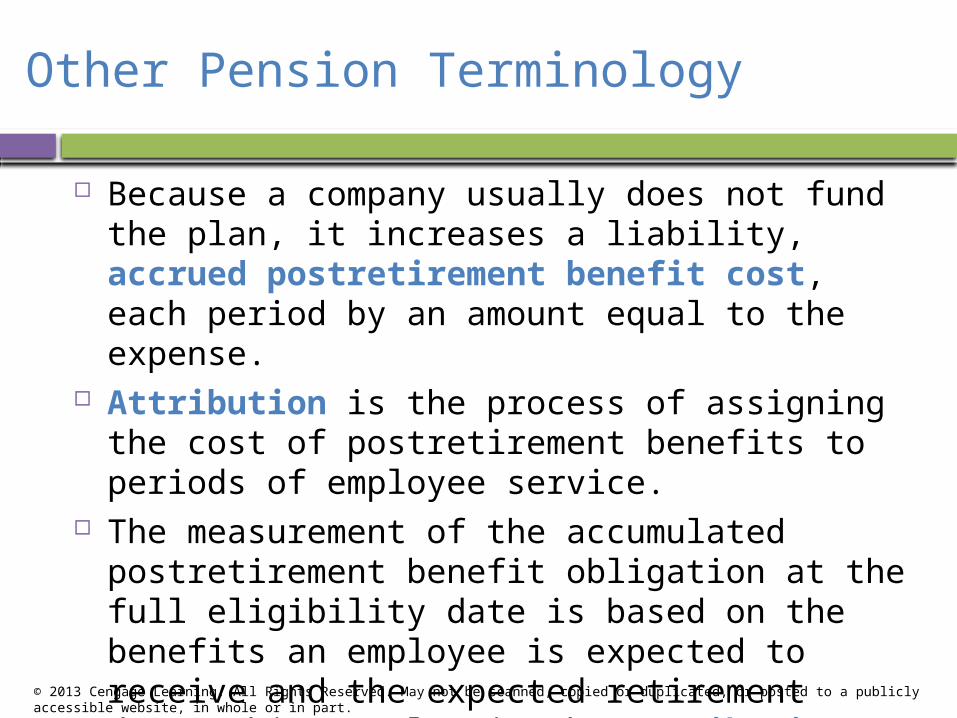

Because a company usually does not fund the plan, it increases a liability, accrued postretirement benefit cost, each period by an amount equal to the expense.

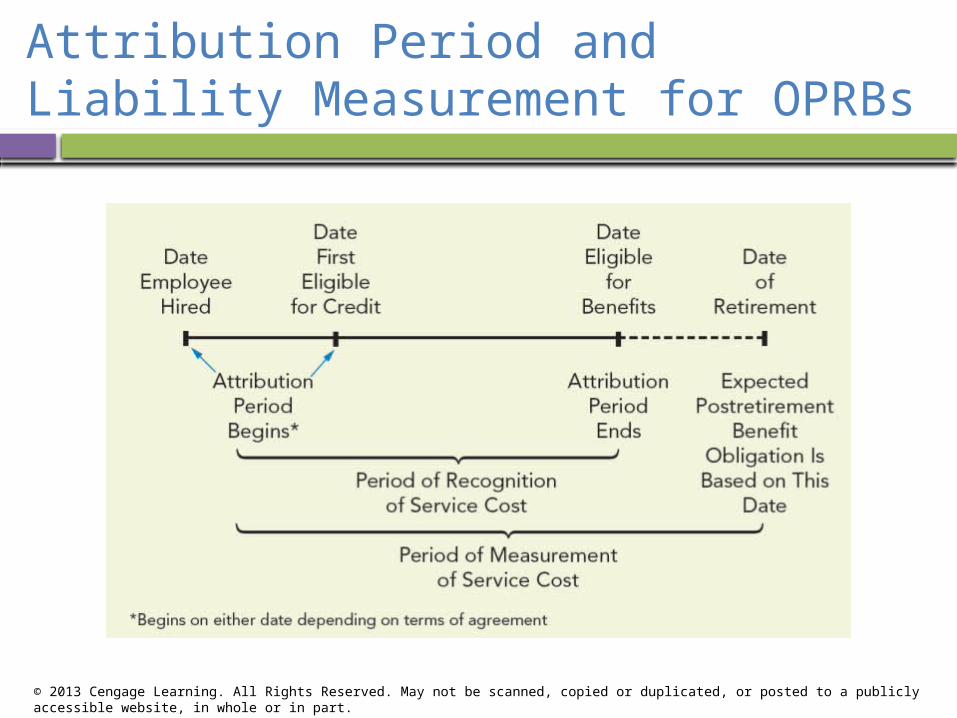

Attribution is the process of assigning the cost of postretirement benefits to periods of employee service.

The measurement of the accumulated postretirement benefit obligation at the full eligibility date is based on the benefits an employee is expected to receive and the expected retirement date. This results in the attribution period (recognition period) and the measurement period being different.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Attribution Period and Liability Measurement for OPRBs