Download - Institutional presentation_1_q15

Institutional PresentationInstitutional Presentation 1Q15

Profile and History

Pine

History

Business Strategy

Competitive Landscape

Focus Always on the Client

Corporate Credit

FICC

Summary

2/28Investor Relations | 1Q15 |

FICC

Pine Investimentos

Highlights and Results

Corporate Governance

Corporate Governance

Committees

Social Investment and Responsibility

Profile and History

PineSpecialized in providing financial solutions for corporate clients…

Credit Portfolio by Annual Client Revenues

December 30th, 2014

Over R$2 billion37%

R$500 million to R$2 billion

R$250 million to R$500 million

12%

Up to R$250 million

15%

4/28Investor Relations | 1Q15 |

Profile

Focused on establishing long-term relationships

Profound knowledge and product penetration

Business is structured along three primary business lines:

• Corporate Credit: credit and financing products

• FICC: instruments for hedging and riskmanagement

• Pine Investimentos: Capital Markets, FinancialAdvisory, Project & Structured Finance andResearch

R$2 billion36%

801 827 825

867

1.015

1.220

1.272 1.256 1.244

...with extensive knowledge of Brazil’s corporate credit cycle.

History

1939Pinheiro Family

foundsBanco Central do

Nordeste

1975Noberto Pinheiro becomes one of

End of 2007Focus on expanding the Corporate Banking franchise

Discontinuation of the payroll-deductible loan business

May, 2007Creation of Pine Investimentos products line and

opening of the Cayman branch

2005Noberto Pinheiro becomes Pine’s sole

shareholder

October, 2007Beginning of the FICC Business

October, 2011Subscription of Pine’s capital by DEG

August, 2012 Subscription of Pine’s capital by DEG, Proparco, Controlling Shareholder and Management

November, 2012Opening of the broker dealer in New York, Pine Securities USA LLC

5/28Investor Relations | 1Q15 |

184 222 341 521 620 755 663 761 1.214

2.854 3.108

4.195

5.763

6.963

7.911

9.920 9.826 9.657

62

121 126 140 136 152 171 209

335

Dec-9

8

Dec-9

9

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

Mar

-15

Corporate Credit Portfolio (R$ Million)

Shareholders' Equity (R$ Million)

1997Noberto and Nelson Pinheiro sell their stake in BMC and

found Pine

becomes one of BMC’s controlling

shareholders

Devaluationof the real

Nasdaq Sept. 11 Brazilian Elections

(Lula)

SubprimeAsian Crisis

Russian Crisis

European Community

shareholder

March, 2007

IPO

May, 2015

18 years

Business Strategy

Competitive LandscapePine serves a niche market of companies with few options for banks.

100% Corporate

Large Multi-Services banks

Market

Consolidation of the banking sector has decreasedthe supply of credit lines and financial instrumentsfor corporate

Foreign banks are in a deleveraging process

PINE

Full service Bank – Credit, Hedging, and Investment

7/28Investor Relations | 1Q15 |

100% focused on providing complete service to companies, offering customized products

Corporate & SME

SME & Retail

Retail

Full service Bank – Credit, Hedging, and InvestmentBank products – with room for growth

~15 clients per officer

Competitive Advantages:

� Focus

� Fast response: Strong relationship withclients, with the credit committee meetingtwice a week and response times to clients ofno more than one week

� Specialized services

� Tailor-made solutions

� Product diversity

Foreign and Investment Banks

Focus Always on the ClientProducts tailored to meet the needs of each individual client.

Working Capit

CDIs

OverdraftAccounts

Fixed Income

Currencies

Commodities

Equities

CDBs

CDs

RDBs

LCAs

LCIs

DebenturesCRIs

CCBs

Eurobonds

PrivatePlacements

Financial Letters

TreasuryDistribution

Capital Markets

Financial Advisory

Local Currency

Foreign Currency

Pricing of Assets and Liabilities

LiquidityManagement

Trading

Local Currency

Working CapitalUnderwriting

8/28Investor Relations | 1Q15 |

BankGuarantees

Exclusive Funds

Portfolio Management

Swap NDFsStructured Swaps

BNDES Onlending

Bank Guarantees

Compror

ACC/ACE

Export Finance

Finimp

Lettersof Credit

2,770 onlending

Accounts

Syndicated andStructured Loans

ClientsCorporate

Credit

FICC

PineInvestimentos

Capital Markets

Financial Advisory

Fixed Income Currencies

Commodities

Local Currency

Onlending

Foreign Currency

Trade FinanceParticipation

Funds

Options

Corporate & Structured

Finance

M&A

Project Finance

StructuredFinance

Private Credit Funds

Real Estate Funds

Rural Credits

AircraftFinancing

Investment Management

In addition to the

headquarters located in the

city of São Paulo, Pine has 10

branches throughout Brazil, in

the States of Ceará, Mato

Grosso, Minas Gerais, Paraná,

Pernambuco, Rio de Janeiro,

Rio Grande do Sul, and

São Paulo. The origination

network also counts with a

Cayman Branch and a broker

dealer in New York (USA).

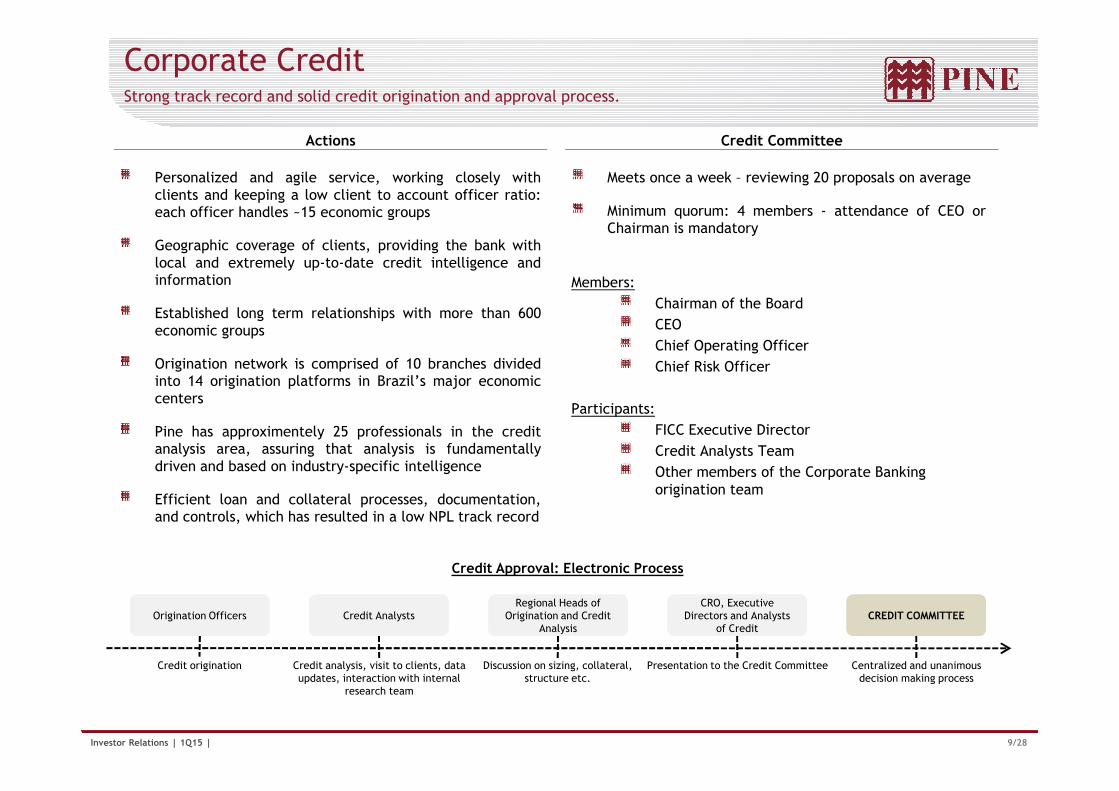

Corporate Credit

Actions Credit Committee

Strong track record and solid credit origination and approval process.

Meets once a week – reviewing 20 proposals on average

Minimum quorum: 4 members - attendance of CEO orChairman is mandatory

Members:

Chairman of the Board

CEO

Chief Operating Officer

Chief Risk Officer

Personalized and agile service, working closely withclients and keeping a low client to account officer ratio:each officer handles ~15 economic groups

Geographic coverage of clients, providing the bank withlocal and extremely up-to-date credit intelligence andinformation

Established long term relationships with more than 600economic groups

Origination network is comprised of 10 branches dividedinto 14 origination platforms in Brazil’s major economiccenters

9/28Investor Relations | 1Q15 |

Credit Approval: Electronic Process

Origination OfficersOrigination Officers

Credit origination Credit analysis, visit to clients, data updates, interaction with internal

research team

Credit AnalystsCredit AnalystsRegional Heads of

Origination and Credit Analysis

Regional Heads of Origination and Credit

Analysis

Presentation to the Credit Committee

CRO, Executive Directors and Analysts

of Credit

CRO, Executive Directors and Analysts

of Credit

Centralized and unanimous decision making process

CREDIT COMMITTEE CREDIT COMMITTEE

Participants:

FICC Executive Director

Credit Analysts Team

Other members of the Corporate Banking origination team

centers

Pine has approximentely 25 professionals in the creditanalysis area, assuring that analysis is fundamentallydriven and based on industry-specific intelligence

Efficient loan and collateral processes, documentation,and controls, which has resulted in a low NPL track record

Discussion on sizing, collateral, structure etc.

Commodities13%

Fixed Income7%

Currencies80%

March 31st, 2015 R$ million

FICCProven trackrecord: leadership largest bank in commodity hedging1

Client Notional Derivatives by Market Notional Value and MtM

11,268 14,382 8,376 7,703 7,482

482

354 288 221

349

(243)

(532)

(47)

(365)

(103)

Notional Amount

MtM

Stressed MtM

10/28Investor Relations | 1Q15 |

13%

Scenario on March 31st,2015:

Duration: 149 days

Mark-to-Market: R$349 million

Stress Scenario (Dollar: +31% and Commodities Prices: -30%):

Stressed MtM : (R$103 million)

Market Segments Portfolio Profile

1Source: Report Cetip, March 2015

Fixed Income: Fixed, Floating, Inflation, Libor

Currencies: Dollar, Euro, Yen, Pound, Canadian Dollar,Australian Dollar

Commodities: Sugar, Soybean (Grain, Meal and Oil), Corn,Cotton, Metals, Energy

Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Long Term Loan

US$25,000,000

Debentures

R$50,000,000R$45,200,000

Debentures

December, 2014

BNDES Onlending

R$630,000,000

Coordinator

February, 2015March, 2015

Project Finance

R$30,000,000

Lead Coordinator

Structuring CRP

R$24,000,000

Lead Coordinator

Pine Investimentos

Selected Transactions

Capital Markets: Structuring and Distribution of Fixed

Income Transactions.

Financial Advisory: Project & Structured Finance, M&A,

and hybrid capital transactions.

Research: Macro, Commodities, and Corporate.

11/28Investor Relations | 1Q15 |

August, 2014

Export Prepayment Finance

Structuring Agent

August, 2014

Financial Advisor

US$58,000,000 R$459,300,000

June, 2014

M&A

Advisor

September, 2014

Lead Coordinator

November, 2014

Lead Coordinator

July, 2014

Project Finance

R$391,459,000

Financial Advisor

2

3

4Q14 1Q15

R$ million

Fees

Highlights and Results

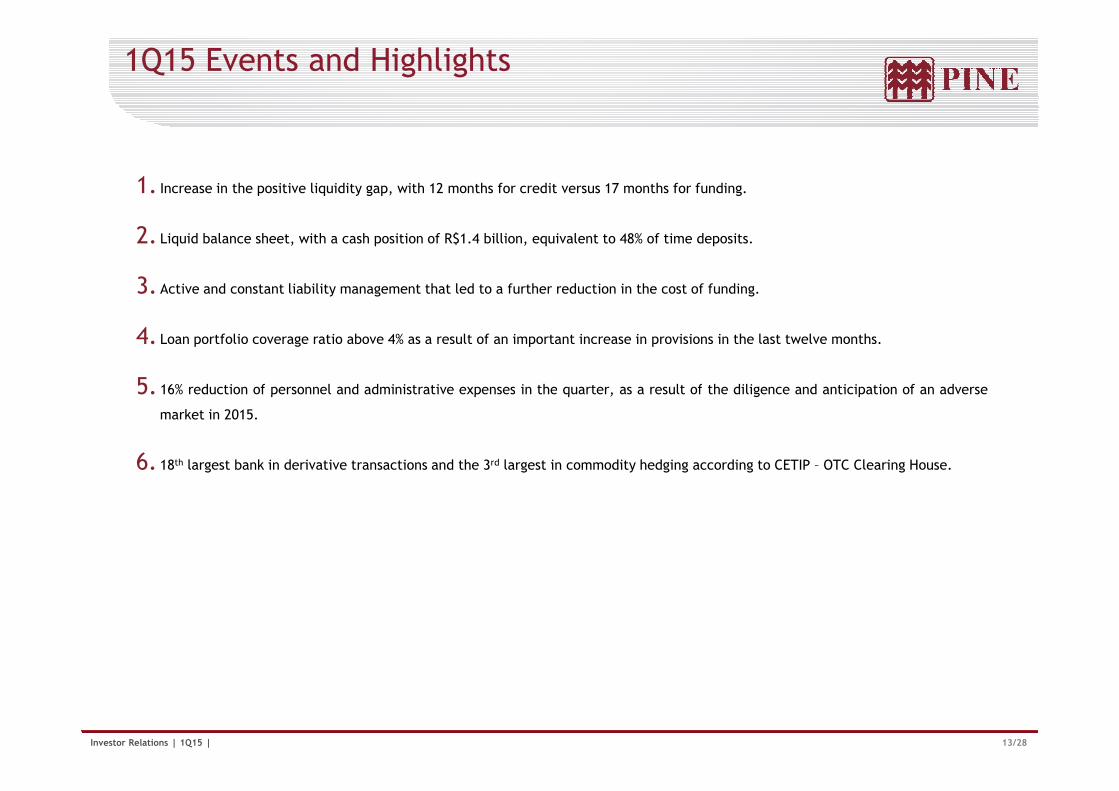

1Q15 Events and Highlights

1. Increase in the positive liquidity gap, with 12 months for credit versus 17 months for funding.

2. Liquid balance sheet, with a cash position of R$1.4 billion, equivalent to 48% of time deposits.

3. Active and constant liability management that led to a further reduction in the cost of funding.

4. Loan portfolio coverage ratio above 4% as a result of an important increase in provisions in the last twelve months.

5. 16% reduction of personnel and administrative expenses in the quarter, as a result of the diligence and anticipation of an adverse

13/28Investor Relations | 1Q15 |

5. 16% reduction of personnel and administrative expenses in the quarter, as a result of the diligence and anticipation of an adverse

market in 2015.

6. 18th largest bank in derivative transactions and the 3rd largest in commodity hedging according to CETIP – OTC Clearing House.

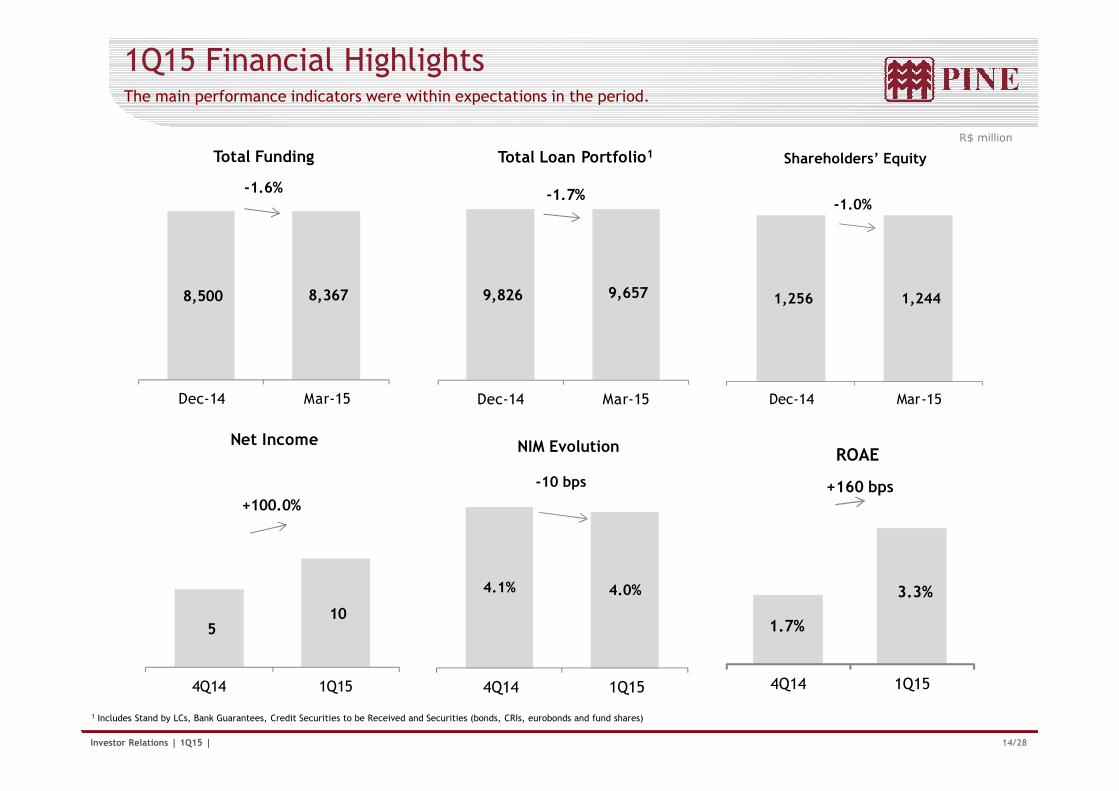

9,826 9,657

Dec-14 Mar-15

Total Loan Portfolio1

-1.7%

1Q15 Financial Highlights

R$ million

The main performance indicators were within expectations in the period.

8,500 8,367

Dec-14 Mar-15

Total Funding

-1.6%

1,256 1,244

Dec-14 Mar-15

Shareholders’ Equity

-1.0%

14/28Investor Relations | 1Q15 |

Dec-14 Mar-15

1 Includes Stand by LCs, Bank Guarantees, Credit Securities to be Received and Securities (bonds, CRIs, eurobonds and fund shares)

Dec-14 Mar-15

5 10

4Q14 1Q15

Net Income

+100.0%

Dec-14 Mar-15

4.1% 4.0%

4Q14 1Q15

NIM Evolution

-10 bps

1.7%

3.3%

4Q14 1Q15

ROAE

+160 bps

4.1% 4.0%

4Q14 1Q15

-10 bps

Net Interest Margin

NIM Evolution Impacts in Period

NIM in line with guidance.

Lower revenue contrinution from FICC and Treasury;

Mark to Market of securities; and

Increased spreads at origination.

15/28Investor Relations | 1Q15 |

4Q14 1Q15

NIM Breakdown

R$ million

1Q15 4Q14 1Q14 QoQ YoY

Recurring Financ ial Margin

Income from financial intermediation 54 83 109 -34.9% -50.5%

Overhedge effect 34 10 (3) 240.0% -1233.3%

Liabilities hedge effect - 1 (4) -100.0% -100.0%

Recurring Income from financial intermediation 88 94 102 -6.4% -13.7%

Expenses and Efficiency Ratio

Expenses

Cost control, better than the guidance range.

23

27

23

26

22

18

39.8% 42.2% 39.1%

- 8 0 . 0 %

- 6 0 . 0 %

- 4 0 . 0 %

- 2 0 . 0 %

0 . 0 %

2 0 . 0 %

4 0 . 0 %

6 0 . 0 %

5

1 0

1 5

2 0

2 5

3 0

3 5

4 0

4 5

5 0

Personnel Expenses

Other administrative expenses

Recurring Efficiency Ratio (%)

16/28Investor Relations | 1Q15 |

Efficiency Ratio

- 1 0 0 . 0 %0

1Q14 4Q14 1Q15

R$ million

1Q15 4Q14 1Q14 QoQ YoY

Operating expenses 1 45 52 53 -13.5% -15.1%

(-) Non-recurring expenses (1) (3) (4) -66.7% -75.0%

Recurring Operating Expenses (A) 43 49 49 -12.2% -12.2%

Recurring Revenues 2 (B) 110 116 123 -5.2% -10.6%

Recurring Efficiency Ratio (A/B) 39.1% 42.2% 39.8% -310 bps -70 bps

1 Other administrative expenses + tax expenses + personnel expenses2 Gross Income from financial intermediation - provision for loan losses + fee income + overhedge effect - hedge impact

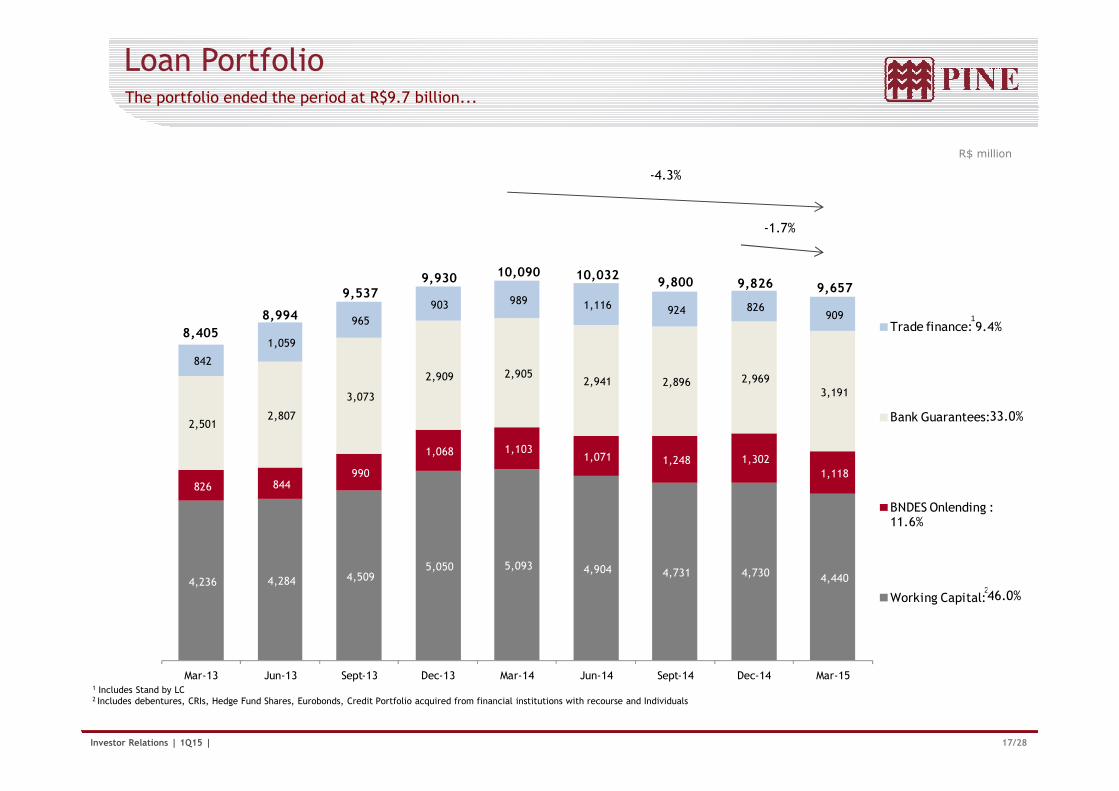

3,073

2,909 2,905 2,941 2,896 2,969

3,191

842

1,059

965

903 989 1,116 924 826 909

Trade finance: 9.4%

9,657

8,405

8,994

9,5379,930 10,090 10,032

9,800 9,826

R$ million

Loan PortfolioThe portfolio ended the period at R$9.7 billion...

-4.3%

-1.7%

1

17/28Investor Relations | 1Q15 |

4,236 4,284 4,509 5,050 5,093 4,904 4,731 4,730 4,440

826 844 990

1,068 1,103 1,071 1,248 1,302

1,118

2,501 2,807

3,073 3,191

Mar-13 Jun-13 Sept-13 Dec-13 Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Bank Guarantees: 33%

BNDES Onlending : 11.6%

Working Capital: 46%

1 Includes Stand by LC2 Includes debentures, CRIs, Hedge Fund Shares, Eurobonds, Credit Portfolio acquired from financial institutions with recourse and Individuals

2

33.0%

46.0%

43%42%

7%6%5%5%5%

8%8%8%7%8%

10%10%10%8%8%

12%10%12%12%8%

12%12%13%11%9%

13%14%12%15%20%

Sugar and

Ethanol

Real Estate

Energy

Agriculture

Engineering

Transportation

Continuous Loan Portfolio Management

Sectors Rebalance

...with improved sector diversification.

Sugar and Ethanol

13%

Real Estate

12%

Energy

12%

Chemicals

4%

Metallurgy

4%

Specialized

Services

3%

Vehicles and Parts

2%

Retail

2%

Meatpacking

2%

Food Industry

2%

Construction

Material

1%

Other

9%

18/28Investor Relations | 1Q15 |

38%40%40%43%42%

Mar-15Dec-14Mar-14Mar-13Mar-12

Transportation

and Logistics

Others

The composition of the portfolio of the 20 largest clients changed by over 15% in the past twelve months;

The total portfolio share of the 20 largest clients remained below 30%, in line with market peers.

Agriculture

10%

Engineering

8%Transportation

and Logistics

7%

Telecom

5%

Foreign Trade

4%

4%

Working Capital

77%

Guarantees23%

Residential Lots40%

Residential36%

Warehouse14%

Mall7%

Commercial3%

SP75%

MG17%

PR6%

GO2%

AL0%

MS0%

Working Capital

50%

Guarantees34%

Onlending9%

Trade Finance

7%

Main SectorsSugar and Ethanol | Real Estate | Agriculture

Sugar and Ethanol Real Estate

Exposure by Product Exposure by State Exposure by Product Exposure by Segment

19/28Investor Relations | 1Q15 |

Working Capital

73%

Trade Finance

14%Onlending

12%

Guarantees1%

Agriculture

Exposure by Product Exposure by State

MT32%

SP30%

PR10%

BA9%

ES5%

CE4%

MS2%

Others8%

Working Capital

Guarantees11%

Onlending3%

Main SectorsEnergy | Engineering

Energy Engineering

Exposure by Product Exposure by Product

Guarantees74%

Working Capital

18%

Onlending8%

20/28Investor Relations | 1Q15 |

Transporta-tion34%

Concession31%

Industrial22%

Oil and Gas7%

Sanitation5%

Energy1%

Capital86%

Exposure by SegmentExposure by Segment

Wind Energy

59%

UTE13%

Distributors10%

Transmitting

8%

Equipment

Supplier

6%

SHPs UHEs3%

Trader1%

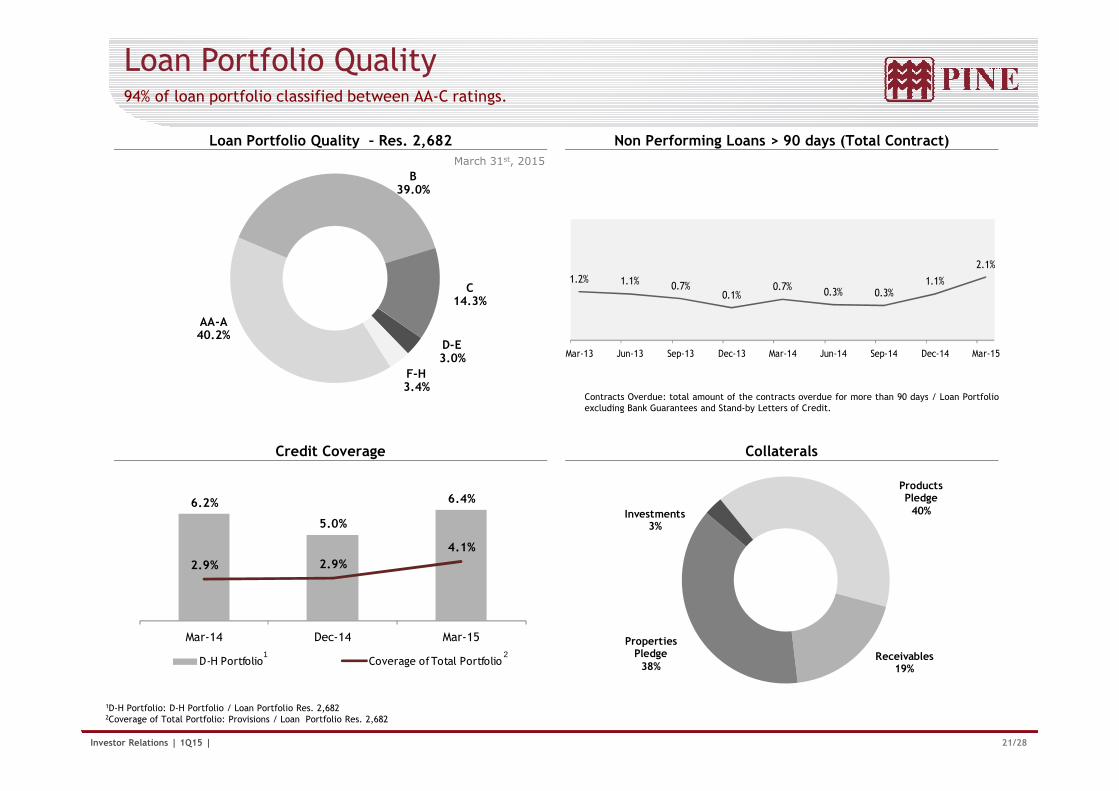

March 31st, 2015

Contracts Overdue: total amount of the contracts overdue for more than 90 days / Loan Portfolio

Loan Portfolio Quality94% of loan portfolio classified between AA-C ratings.

Loan Portfolio Quality – Res. 2,682 Non Performing Loans > 90 days (Total Contract)

1.2% 1.1% 0.7%0.1%

0.7%0.3% 0.3%

1.1%

2.1%

Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

AA-A40.2%

B39.0%

C14.3%

D-E3.0%

F-H3.4%

21/28Investor Relations | 1Q15 |

Contracts Overdue: total amount of the contracts overdue for more than 90 days / Loan Portfolioexcluding Bank Guarantees and Stand-by Letters of Credit.

1D-H Portfolio: D-H Portfolio / Loan Portfolio Res. 2,6822Coverage of Total Portfolio: Provisions / Loan Portfolio Res. 2,682

Credit Coverage Collaterals

6.2%

5.0%

6.4%

2.9% 2.9%

4.1%

Mar-14 Dec-14 Mar-15

D-H Portfolio Coverage of Total Portfolio

Products Pledge

40%

Receivables19%

Properties Pledge

38%

Investments3%

1 2

434 323

113 364

346 388

687 429

500

478

473 531 430

773 973

871

834 1,064

819 839 929

8,367

6,589

7,111

7,894

8,383

8,7978,559 8,638 8,500

Trade Finance: 11.1%

Private Placements: 9.2%

Multilateral Lines: 10%

International Capital Markets:

R$ million

FundingDiversified sources of funding...

58% 48%42% 44% 41%39% 41% 35% 48% Cash over Deposits

-4.9%

10.0%

22/28Investor Relations | 1Q15 |

2,087 2,185 1,944 2,175 2,314 2,271 1,905 1,720

1,209

972 1,013 1,048

1,112 1,022 761

731 545

361

225 254 372

475 659 908

920 1,122

1,273

110 110 93

90 76 80

98 69

157

126 19 20

23 27 41

30 27

24

859 862 1,099

1,141 1,174 1,086

1,292 1,333

1,161

154 286 649

632 582 594 709

635

509

642 689

762

792 833

508 892 747

796 402

435

437

459 434

427 323

347

338 78 80

69

113 346 687

837

171 181

429 773

762

997 6,589

Mar-13 Jun-13 Sept-13 Dec-13 Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

International Capital Markets: 4%

Financial Letter : 9.5%

Local Capital Markets: 6.1%

Onlending: 13.9%

Demand Deposits: 0.3%

Interbank Time Deposits: 1.9%

High Net Worth Individual Time Deposits: 15.2%

Corporate Time Deposits: 4.3%

Institutional Time Deposits: 14.5%

4.0%

Asset & Liability Management... keeping a positive gap between credit and funding.

Leverage Credit over Funding Ratio

82% 83%80% 80%

77%

Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

7.9x 7.9x 7.7x 7.8x 7.8x

5.6x 5.6x 5.4x 5.4x 5.2x

-

1 . 0

2 . 0

3 . 0

4 . 0

5 . 0

6 . 0

7 . 0

8 . 0

9 . 0

1 0 . 0

Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Expanded loan Porfolio

Loan Portfolio excluding Bank Guarantees

23/28Investor Relations | 1Q15 |

47% 47% 43% 41% 36%

53% 53% 57% 59% 64%

Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Total Deposits Others

Leverage: Expanded Loan Portfolio / Shareholders’ EquityExpanded Loan Portfolio excluding Bank Guarantees and Stand-by Letters of Credit /

Shareholders’ Equity

Credit over Funding ratio: Loan Portfolio excluding Bank Guarantees and Stand-by Letters ofCredit / Total Funding

ALM – Average Maturity Total Deposits over Total FundingR$ millionmonths

8,638 8,3678,797 8,559 8,500

16 16 16

16 17

14 14

13 12 12

Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Funding

Credit

Capital Adequacy Ratio (BIS), Basel III BIS ratio reached 13.0%.

15.0% 14.7% 13.7%

2.1% 2.3%2.2%

2.1% 1.5% 1.5% 1.4% 1.4%0.8%13.0%

17.1% 17.0%15.9%

14.1% 13.7% 13.7% 13.8% 13.9%

Tier II Tier I

Minimum Regulatory Capital (11%)

24/28Investor Relations | 1Q15 |

R$ Million BIS (%)

Tier I 1,232 12.2%

Tier II 85 0.8%

Total 1,317 13.0%

15.0% 14.7% 13.7%12.0% 12.2% 12.2% 12.4% 12.4% 12.2%

Mar-13 Jun-13 Sept-13 Dec-13 Mar-14 Jun-14 Sept-14 Dec-14 Mar-15

Corporate Governance

Corporate GovernancePine is committed to best corporate governance practices…

Two Independent Members and Two External Members on the Board of Directors

Mailson Ferreira da Nóbrega: Brazil’s Finance Minister from 1988 to 1990

Gustavo Junqueira: Former Head of Pine Investimentos, Member of the Board of Directors atEZTEC, Financial Advisor at Arsenal Investimentos and CFO at Gradiente Eletrônica

Harumi Susana Ueta Waldeck: Former CFO of Pine, with over 17 years of experience at thecompany. She brings the day-to-day experience to the Board.

São Paulo Stock Exchange (BM&FBOVESPA) Level 2 Corporate Governance

26/28Investor Relations | 1Q15 |

São Paulo Stock Exchange (BM&FBOVESPA) Level 2 Corporate Governance

Audit and Compensation Committee reporting directly to the Board of Directors

100% tag along rights for all shareholders, including non-voting shares

Arbitration procedures for fast settlement of litigation cases

Social Investment and ResponsibilityFocus on the short, medium and long term.

Partnerships

Responsible Credit

“Lists of Exceptions”: the Bank does not finance projects or thoseorganizations that damage the environment, are involved in illegallabor practices or produce, sell or use products, substances or activitiesconsidered prejudicial to society.

System of environmental monitoring, financed by the IADB andcoordinated by FGV, and internally-produced sustainability reports forcorporate loans

Protocolo Verde – “Green Protocol”, an agreementbetween FEBRABAN and the Ministry of the Environmentto support development that does not compromise futuregenerations.

Sustainability Annual Report

Sixth consecutive year disclosing theSustainability Report in the GRIstandard. The 2014 report, with its highlevel of clarity, transparency and qualitywas recognized with the second place inthe Abrasca Annual Report Award,considering its category of companies

27/28Investor Relations | 1Q15 |

Social Investment Recognition

Most Green Bank

Recognized by the International Finance Corporation (IFC), privateagency programs of the World Bank as the most "green" bank as a resultof its transactions under the Global Trade Finance Program (GTFP) andits onlending to companies focused on renewable energy and ethanol

Efficiency Energy

Recognition by World Bank for support in the Energy Efficiency sector.

Exhibition and sponsorship of Brazilian artists, for instance Paulo von Poser and

Miguel Rio Branco, in addition to sponsoring and supporting films and

documentaries such as Quebrando o Tabu (Fernando Henrique Cardoso on the

drug war), O Brasil deu certo, e agora? (idealized by Mailson da Nóbrega), Além

da Estrada (Charly Braun) and others.

considering its category of companieswith net income to R$3 billion.

Noberto N. Pinheiro Junior

CEO

Raquel Varela BastosHead of Investor Relations

Luiz Maximo

Investor Relations Specialist

Ana LopesInvestor Relations Analyst

Investor Relations

28/28Investor Relations | 1Q15 |

This report may contain forward-looking statements concerning the business prospects, projections of operating and financial results and growth outlook of PINE. These are merely projections and as suchare based solely on management’s expectations regarding the future of the business. These statements depend substantially on market conditions, the performance of the sector and the Brazilian economy(political and economic changes, volatility in interest and exchange rates, technological changes, inflation, financial disintermediation, competitive pressures on products and prices and changes in taxlegislation) and therefore are subject to change without prior notice.

Gabriel NettoInvestor Relations Analyst

Fone: (55 11) 3372-5343

www.pine.com/[email protected]