1

Imerys

Group Presentation

2Group presentation I September 2013

Table of contentsTable of contentsTable of contentsTable of contentsGroup presentation

� Imerys: the world leader of mineral-based specialty products

� A profitable and solid business model

� Development strategy: accelerating growth by enlarging

our business footprint

� Conclusion

3Group presentation I September 2013

Disclaimer

More comprehensive information about Imerys is available on the Company’s website

(www.imerys.com), under Regulated Information, including its Registration Document filed

under No. D.13-0195 on March 21, 2013 with Autorité des marchés financiers. Imerys draws

the attention of investors to the “Risk factors” set forth in section 4 of the Registration

Document.

This document contains projections and other forward-looking statements. Investors are

cautioned that such projections and forward-looking statements are subject to various risks

and uncertainties (many of which are difficult to predict and generally beyond the control of

Imerys) that could cause actual results and developments to differ materially from those

expressed or implied.

Photo credits: Imerys photo library, RR, X.

4Group presentation I September 2013

IMERYS

� 2012 Key figures

� Listed on NYSE Euronext Paris

�Market capitalization: 3.9 Bn€ (September 2013)

� 57% of capital held by GBL

� Indexes: SBF 120, DJ Eurostoxx, FTSE4Good

Revenue

3,885 M€

Operating margin

12.6%

ROCE

13.1%

More than 250

industrial sites

8 R&D centers

and 20 regional laboratories

16,026 employees

5Group presentation I September 2013

Imerys is the world leader of mineral-based specialty products

for the industry

… IN THOUSANDS OF APPLICATIONS…

PROCESS MINERALS INTO

SPECIALITY MINERALS…

Finished

product

Process

enabler

Mineral

component

Functional

additive

… ALL OVER THE GLOBE.

… FOR DIVERSIFIED END-MARKETS…

1

2

3

4

6Group presentation I September 2013

From functional properties to mineral-based specialty products

� Many well known products exist as a result of properties brought by Imerys specialties

MineralsProcess:

Beneficiate & Transform

7Group presentation I September 2013

FUNCTIONAL ADDITIVES – 45%Ingredient added to our customers’

product composition so as to enhance its properties, e.g.:

PROCESS ENABLERS – 20%Product used in the processes of our

customers but not present in the finished product, e.g.:

Monolithic refractories

for

industrial equipments

HIGH-TEMPERATURE,

HIGH WEAR RESISTANCE

Our products provide high-performance and key functionalities

MINERAL COMPONENTS – 25%Important constituent of a mineral

formula of our customers’ products, e.g.:

Clay, kaolin, feldspar

for

sanitaryware & tableware

WHITENESS, STRENGTH

Kaolin, mica, talc, feldspar

for paints or plastic parts

SHOCK ABSORPTION

AND LIGHTNESS

Paper RefractoryTiles Paints & coatingIron & Steel AbrasivesFiltration ThermalPlastics and polymers Floor and wall tilesSanitaryware BricksPerformance minerals specialties Board and PackagingCement Films & PackagingTableware FoundryOther RubberMobile Energy Adhesives & Caulks & SealantsAutomotive Electrical / electronicsPharma, health & beauty Technical ceramicsKiln Furniture Glass / fiber glassCarbon additives Chemical / petrochemicalsAggregates PhotovoltaicOther fine ceramics Agriculture / horticultureSlates Building & constructionHot metal forming Metal alloysInsulation Silanes & SiliconesEnergy Oilfield

FINISHED PRODUCTS – 10%Use as such and not further

transformed by our customers, e.g.:

Clay tiles

for housing

ENERGY EFFICIENCY,

DURABILITY

0

Wide range of applications

<2% each

3-5% each

20%

5-10% each

8Group presentation I September 2013

Diversity of applications

* Imerys estimates: 2012 sales

Consumption

40%

Durable goods

40%

Investment

20%

More

cyclical

Less

cyclical

12-15% of sales

each

<2% of sales each

2-5% of sales

each

5-8% of sales

each

Good balance between different economic cyclesNo end-market > 15% of sales*

Building

new

Iron & Steel

Building

Renovation

Commercial

printingAutomotive

Industrial

equipment

Publishing

Energy

Packaging

Food & Beverages

Other consumer goods

Other paper

Tableware

Infrastructure

Electrical

& électron. appliances

Pharma, Health &

BeautyOffice paper

Environment

Agriculture /

horticulture

OthersAerospace

9Group presentation I September 2013

Presence in 50 countries with more than 250 industrial facilities

Minerals for Ceramics

Energy Solutions & Specialites

Performance & Filtration Minerals

Filtration & Performance Additives

Kaolins

Ceramic Materials

Monolithic Refractories

High Resistance Minerals

Building Materials

Fused Minerals

Refractory Minerals

Graphite & Carbon

Carbonates

Oilfied Solutions

10Group presentation I September 2013

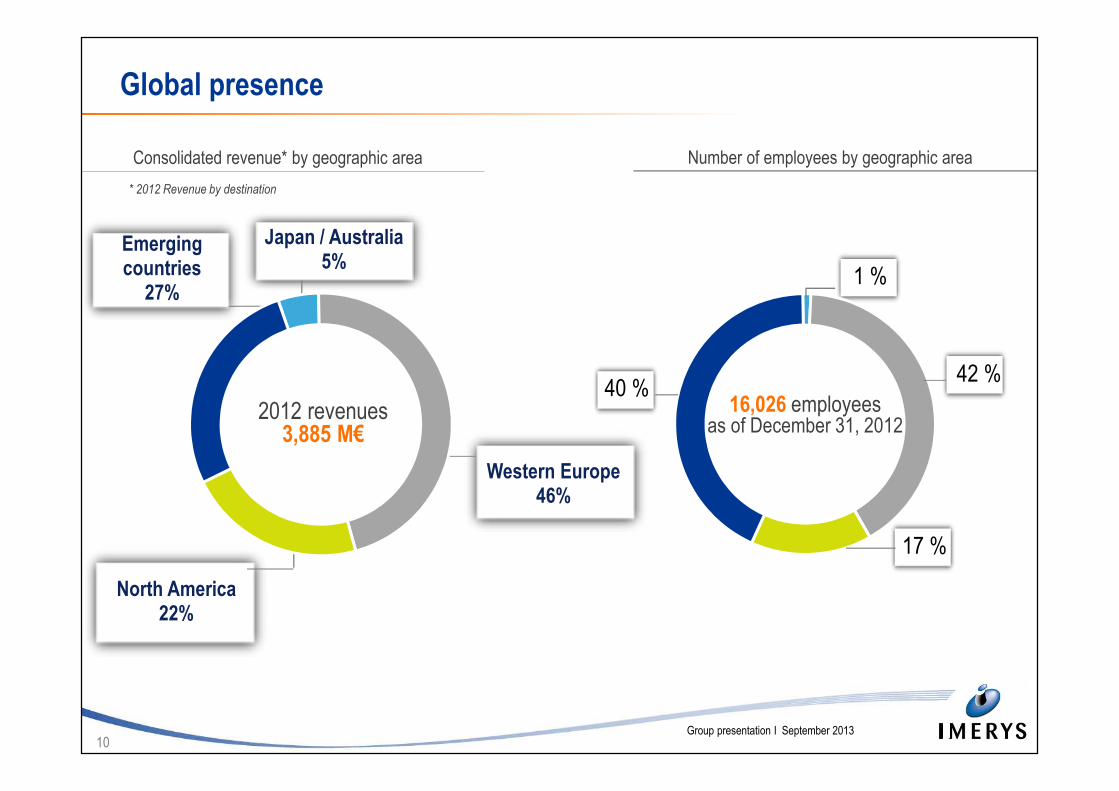

2012 revenues3,885 M€

1 %

42 %

17 %

40 %16,026 employees

as of December 31, 2012

Global presence

* 2012 Revenue by destination

Number of employees by geographic areaConsolidated revenue* by geographic area

Japan / Australia5%

Western Europe46%

North America22%

Emerging countries

27%

11Group presentation I September 2013

Table of contentsTable of contentsTable of contentsTable of contentsGroup presentation

� Imerys: the world leader of mineral-based specialty products

� A profitable and solid business model

� Development strategy: accelerating growth by enlarging

our business footprint

� Conclusion

12Group presentation I September 2013

Imerys positioned for high value

� Specialty products and services

� Products specified and engineered for value (not commodities)

� Important service dimension (logistics and supply chain,

integration into customer manufacturing process, reclaim of used products, etc.)

� Prices not subject to external markets evolutions, but negotiated bilaterally

� Sustained use

� Performance, functionalities essential to customer applications

� Cost to switch typically significant (qualification, process adjustments, etc.)

� Share of total customer cost typically low (< 4% in paper, < 1% in beer, < 2% in alkaline batteries)

� Strong commercial positions

� #1 or #2 on most markets

� Very diverse competitive environment across businesses without any dominant competitor

13Group presentation I September 2013

Leadership positions in all business groups

* 2012 consolidated sales

Market Positions Main Competitors

Energy Solutions

& Specialties(32% of sales*)

• World #1 in alumino-silicate monolithic refractories (Calderys)

• World #1 in graphite for alkaline batteries and conductive additives for Li-ion

batteries

• World #1 in in lubricants for seamless tube protection

• World #1 for large natural graphite powders

• World #1 in minerals for breathable polymer films (GCC)

• World #2 in ground calcium carbonate (GCC) for paper

Vesuvius, RHI, Nacional de Grafite,

Omya, SMI, Carbo Ceramics

Filtration

& Performance

Additives(28% of sales*)

• World #1 in kaolin for paper

• World #1 in talc for plastics, paints, paper, ceramics, health & beauty

• World #1 in mica and in mica for engineered plastics and high performance

coatings

• World #1 in diatomite and perlite for filtration

BASF, KaMin, AKW, Thiele, JM Huber,

Sibelco, Eagle Picher, CECA, S&B, Grefco,

Mondo, IMI Fabi

Ceramic Materials(20% of sales*)

• French #1 in clay roof tiles and for natural slates

• World #1 in raw materials and ceramic bodies for sanitaryware

• World #1 in kaolin for fiberglass

• World #1 in kiln furniture for roofing tiles

AKW, Sibelco, Unimin, Rio Tinto,

Terreal, Monnier, Wienerberger,

Saint-Gobain

High Resistance

Materials(20% of sales*)

• World #1 in fused silica

• World #1 in fused minerals for abrasives

• World #1 in fused zirconia

• World #1 in alumino-silicate minerals for refractories

Almatis, Washington Mills, 3M, Saint-Gobain,

Foskor, Kaolin AD, Minco

14Group presentation I September 2013

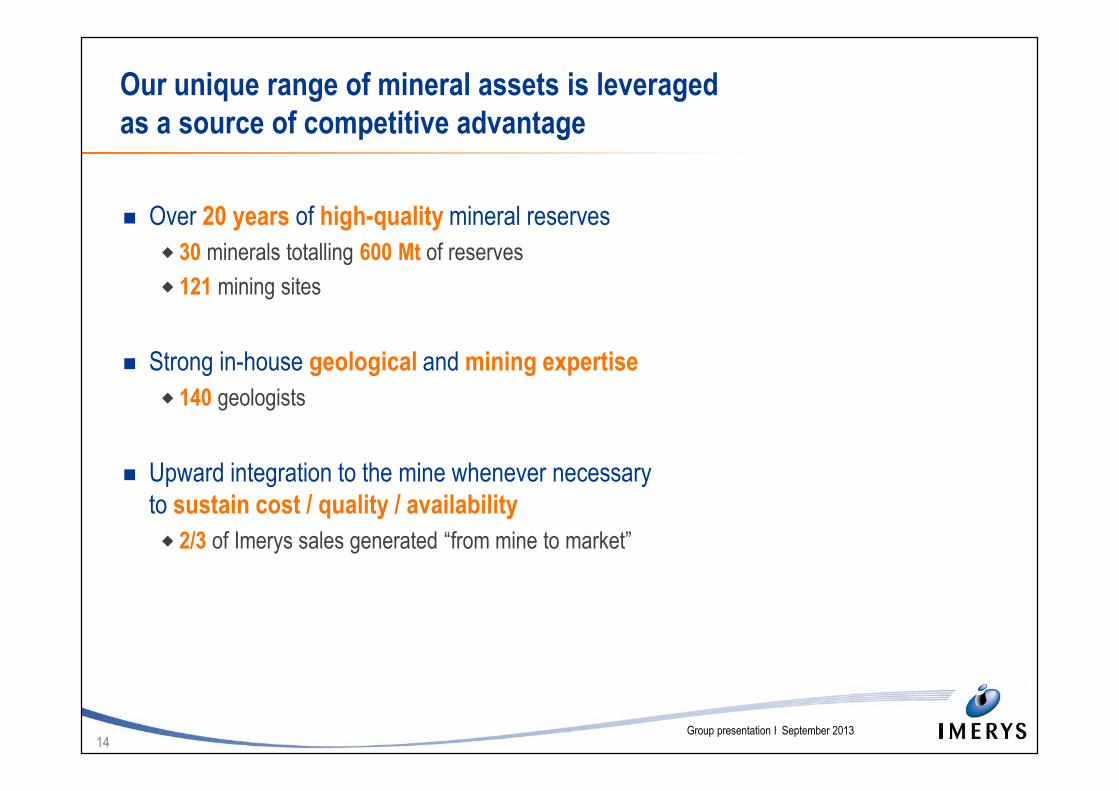

Our unique range of mineral assets is leveraged

as a source of competitive advantage

� Over 20 years of high-quality mineral reserves

� 30 minerals totalling 600 Mt of reserves

� 121 mining sites

� Strong in-house geological and mining expertise

� 140 geologists

� Upward integration to the mine whenever necessary

to sustain cost / quality / availability

� 2/3 of Imerys sales generated “from mine to market”

15Group presentation I September 2013

Our core competitive advantages include know-how, technology,

industrial efficiency

� Unique process know-how

� Mechanical treatment (sorting, shaping, sieving, cycloning, elutriation, etc.)

� Thermal treatment (fusion, calcination, sintering, etc.)

� Formulation of proprietary recipes

� High-volume production (tiles)

� Operational excellence

� Group-wide Key Performance Indicators

� Three-year Sustainable Development Plan to make further progress

across the Group (governance, human rights, environment, safety, communities, innovation,

purchasing, human resources)

16Group presentation I September 2013

Innovation & Sustainable Development

� Innovation: reinforcement of initiatives in 2012

� R&D and innovation: 56M€ i.e. + 30%

� 59 new products launched

� Sustainable Development: implementation of

three-year plan

� Further progress in safety performance

� Environment

‒ Almost 98% of Group facilities equipped with

environmental management systems

‒ Improvement in energy efficiency

* Net of electricity sold** Production sites only

* Number of lost time accidents x 1,000 ,000 / number of work hours

Energyproductivity**(base 100in 2009)

Combined accident frequency rate* (employees/subcontractors)

Total energy consumption* (in thousand of Gigajoules)

28,322

35,180 35,597 35,202 100

97.7 96.9 96.5

2009 2010 2011 2012

3.092.46

1.691.51

2009 2010 2011 2012

- 11 %

17Group presentation I September 2013

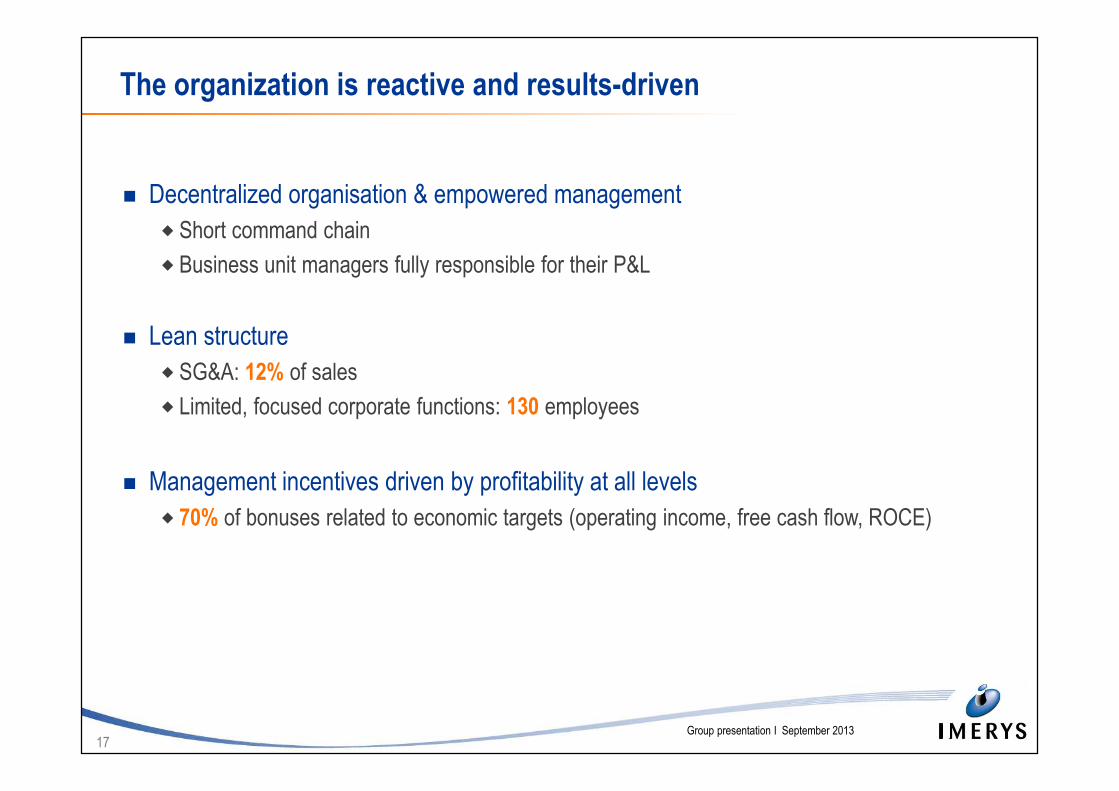

The organization is reactive and results-driven

� Decentralized organisation & empowered management

� Short command chain

� Business unit managers fully responsible for their P&L

� Lean structure

� SG&A: 12% of sales

� Limited, focused corporate functions: 130 employees

� Management incentives driven by profitability at all levels

� 70% of bonuses related to economic targets (operating income, free cash flow, ROCE)

18Group presentation I September 2013

Note: Exchange rates as at date of transaction. Acquisitions made in several steps

assumed to have taken place in full when we acquired control.

5

World Minerals: diversification

into filtration market

ACE: investment into

monolithic refractories in

India Astron China:

diversification

into fused

zirconia

business

Talc: major

complement

to white

pigment

portfolioTreibacher Schleifmittel:

diversification into abrasives

market

Lafarge Refractories:

diversification into monolithic

refractories business

More than 1.8 Bn € of investments and 73 acquisitions over 12 years

Asset disposals: ca. 0.4 Bn €

€396m

€94m€44m €49m €47m

€463m

€35m

€230m

€138m

€8m€59m

€232m

€49m

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Itatex : expansion of

product offering for

polymers, paints and

rubber markets

Goonvean : high purity

kaolin for ceramics and

performance products

Expansion supported by active external growth strategy

19Group presentation I September 2013

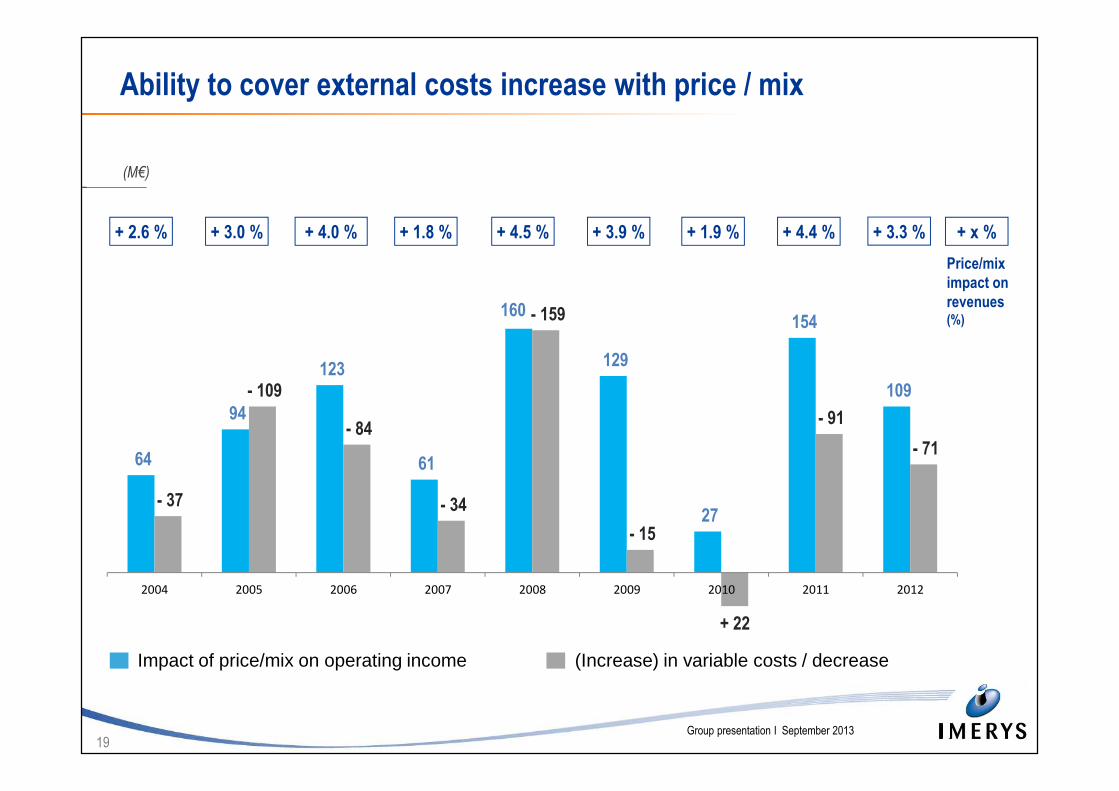

Ability to cover external costs increase with price / mix

(M€)

Price/mix

impact on

revenues(%)

+ 1.9 %+ 3.9 %+ 4.5 %+ 1.8 %+ 4.0 %+ 3.0 %+ 2.6 % + 4.4 % + x %

64

94

123

61

160

129

27

154

109

- 37

- 109

- 84

- 34

- 159

- 15

+ 22

- 91

- 71

2004 2005 2006 2007 2008 2009 2010 2011 2012

+ 3.3 %

Impact of price/mix on operating income (Increase) in variable costs / decrease

20Group presentation I September 2013

11,9%

12,6%13,6%

14,7%14,4%

14,0% 14,2%

12,0%

9,0%

12,5%

13,3%12,6%

10,8%

11,8%

13,6%

16,1%

14,9%14,5%

15,0%

12,0%

7,6%

13,0%

14,0%

13,1%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Value creation over time

ROCE before tax: Current operating income divided by average capital employed (including goodwill)

WACC before tax: Weighted Average Cost of Capital – source: Imerys annual reports between 2004 and 2012;

source: Imerys Registration Document between 2004 and 2012 and Imerys tax estimates

ROCE before tax Operating margin

WACC before tax estimated at 11.5%

Return on capital employed & operating margin

21Group presentation I September 2013

Sustained cash flow generation

Current Free Operating Cash Flow: EBITDA - notional tax – change in WCR – Capex paid

Current free operating cash flow* (M€)

255278

261

225 219

246

177

258

450

303

265287

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

22Group presentation I September 2013

Reduction of operating working capital requirement

� WCR as % of revenue: 22.8% in 2012

on comparable basis

� Effectiveness of targeted WCR reduction

plans (Talc, etc.)

� Management of third-party accounts,

inventory control

� Activity slowdown

� Continuation of factoring set up in

September 2009

(62 M€ in 2012, 74 M€ in 2011)

� Excluding factoring, 0.7 point improvement

in WCR in 2012

(24.5% of revenue in 2012

vs. 25.2% in 2011)

842 836

605

724

859833

24.8%24.2%

21.8% 21.8%

23.2%22.8%

15

17

19

21

23

25

27

2007 2008 2009 2010 2011 2012

Gross WCR WCR as a % of revenue

(M€)

23Group presentation I September 2013

123 %

65 %

79 %

110 %

124 %

0%

50%

100%

150%

200%

0

50

100

150

200

250

300

2008 2009 2010 2011 2012

238

119

169

229

267� Development capex doubled by value

in 2011+2012 vs. 2009+2010

� Further expansion of geographic

footprint and product offering, mainly: � 2011: proppant plant for oil and gas

exploration in the United States

� 2012:

‒ Carbon plant for Li-ion batteries in Belgium

‒ Fused alumina plant in Bahrain

‒ Lime production plant in Brazil

Booked capital expenditure

Maintenance Capex as %

of depreciation

Overburden (1)Development

(1) Mine overburden: i.e. works of removal of the top soil, to enable access to the deposit

Development capital expenditure accelerated in 2011 and 2012

to sustain the strategic plan

(M€)

24Group presentation I September 2013

1.50€1.65€ 1.80€ 1.90€

1.00€1.00€

1.20€

1.50€ 1.55€ (1)

36,9 % 37,6 % 36,6 % 37,8 %

23,5 %

63,2 %

37,4 % 37,2 % 37,6 %

2004 2005 2006 2007 2008 2009 2010 2011 2012

1. Based on the number of outstanding shares at the end of the year. Paid on May 13, 2013

Dividend

2012 2011 Change

Net income from current operations per share (€) 4.13 4.03 + 2.5%

Dividend per share (€) 1.55 1.50 + 3.3%

Total distribution(1) (€ millions) 116.8(1) 112.8 + 3.4%

Weighted average number of shares 75 165 743 75 272 854

Payout (% of net income from current operations)Dividend per share

25Group presentation I September 2013

Group strengths

� Operating margin at 12.6% despite adverse change in activity mix in 2012 and high cash flow

generation

� Stronger balance sheet as of Dec 31, 2012, historically low debt rations

� Net debt to EBITDA ratio at 1.3x vs. 2.7x in 2008

�Gearing down to 47% from 101% in 2008

�Financial flexibility to implement the development plan

� Higher exposure to emerging regions and to growth markets

� Business portfolio expanded with innovative products less than 5 years old

Imerys is well positioned to grow further

26Group presentation I September 2013

Table of contentsTable of contentsTable of contentsTable of contentsGroup presentation

� Imerys: the world leader of mineral-based specialty products

� A profitable and solid business model

� Development strategy: accelerating growth by enlarging

our business footprint

� Conclusion

27Group presentation I September 2013

Three directions to enhance our potential

for more profitable growth

Sources: Various economic databases and market studies – Brokers reports 2011/ 2012

< Worldwide GDP ≥ Worldwide GDP

Mature

end-

markets

52%

Emerging

countries

27%

Growth

end-markets

26%

Innovate

and

manage for cash

Enlarge business

portfolio:

innovate and invest

Grow presence

Imerys sales

2

1

3

28Group presentation I September 2013

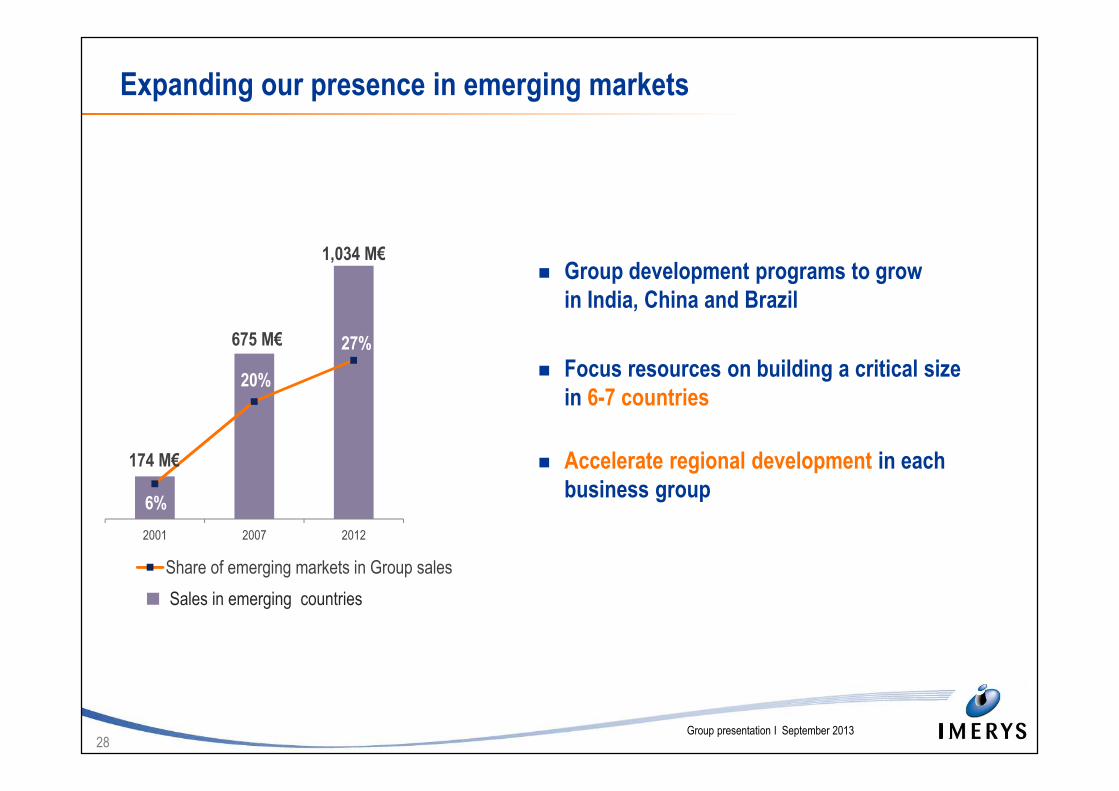

Sales in emerging countries

Expanding our presence in emerging markets

174 M€

675 M€

1,034 M€

6%

20%

27%

0

5

10

15

20

25

30

35

40

45

50

2001 2007 2012

Share of emerging markets in Group sales

� Group development programs to grow

in India, China and Brazil

� Focus resources on building a critical size

in 6-7 countries

� Accelerate regional development in each

business group

29Group presentation I September 2013

Main markets with growth potential above world

GDP for Imerys applications *

� Automotive

� Packaging

� Energy

� Electronics / semi-conductors

� Environment

� Cosmetics and healthcare

� Agriculture

� Aerospace

Capex and acquisitions to increase Group revenues in growth markets

Revenues in growth markets

* Sources : Various data bases, market studies and sell-side research 2011/2012

400 M€

1,026 M€14 %

26 %

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

0

100

200

300

400

500

600

700

800

900

1000

2005 2012

% of group revenues

30Group presentation I September 2013

2003 2004

Antiblocks

Carbon

for Li-Ion

Graphite

for Fuel

Cells

Silicone

rubber

fillers

2005 2006

Latex

gloves

carbonate

fillers

Carbonate

for Wood

fibers

composite

New alumina

abrasive:

Alodur Rod

2007

Astrafil K,

new filler

for fiber

replacement

(Canada)

Carbonate

for non

woven

2008

Natural DE

for Laminate

Cristal silica

controlled

Diatomite

Barrisurf

2009 2010

Carbon for

conductive

plastics

Nano

dimension

minerals

for UV

coating

Cynergy,

a chilled

proof filter

aid

Boosting innovation to play a major role in expansion plan

� In 2012, approx. 250 M€ of sales generated from products not in our portfolio 5 years ago (+ 25% vs. 2011)

2011 2012

Honey comb

structure for

solar

receiver

New spray

castable,

quick dry,

monolithic

refractory

Second

Generation

agglomerated

abrasives

Argical Pro

A crop

protection

natural

product

Low

temperature

porcelaine

body

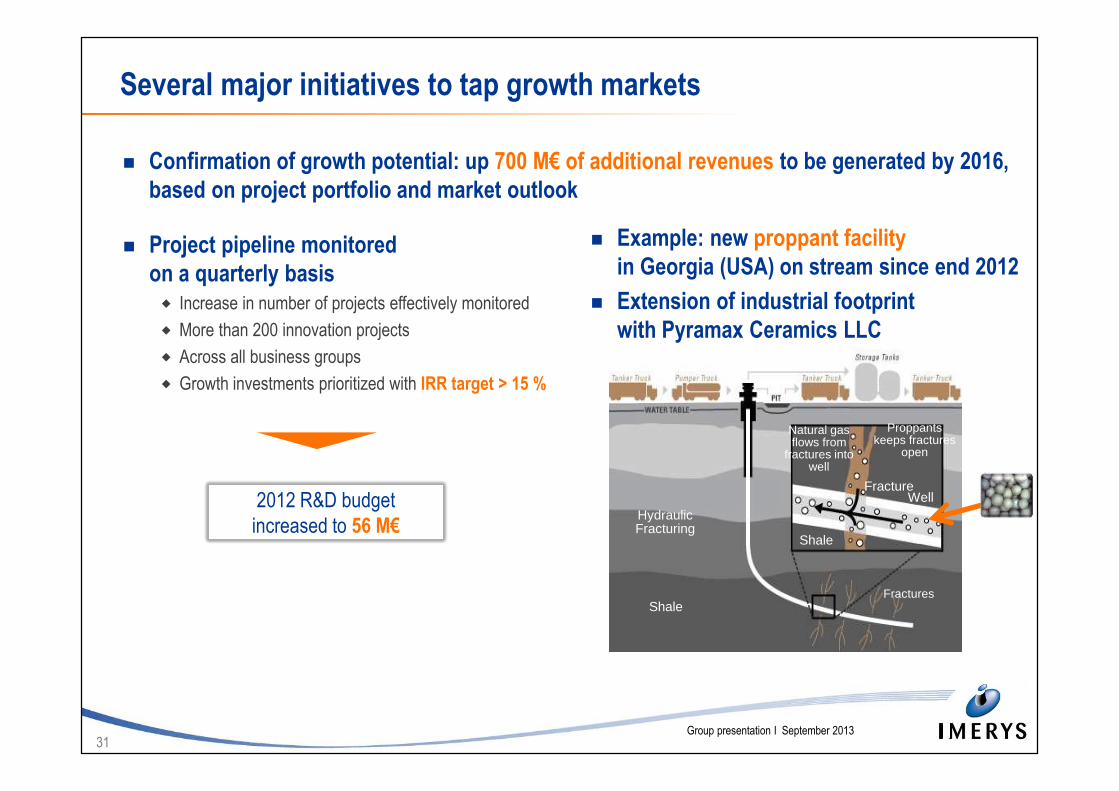

31Group presentation I September 2013

2012 R&D budget

increased to 56 M€

2012 R&D budget

increased to 56 M€

� Project pipeline monitored

on a quarterly basis� Increase in number of projects effectively monitored

� More than 200 innovation projects

� Across all business groups

� Growth investments prioritized with IRR target > 15 %

Several major initiatives to tap growth markets

� Example: new proppant facility

in Georgia (USA) on stream since end 2012

� Extension of industrial footprint

with Pyramax Ceramics LLC

� Confirmation of growth potential: up 700 M€ of additional revenues to be generated by 2016,

based on project portfolio and market outlook

HydraulicFracturing

Shale

Shale

Proppantskeeps fractures

open

Fractures

FractureWell

Natural gasflows from

fractures intowell

32Group presentation I September 2013

Acquisitions: an important driver to enlarge the Group’s business

portfolio

� Successful track-record

� Treibacher: entry into Abrasives applications, new competence in fusion

� World Minerals: entry into non-cyclical filtration business, new application competencies

� Lafarge Refractories: build-up from existing monolithic refractories business Plibrico

� Talc: a new mineral to strengthen current applications and increase presence

in attractive markets (additional competence in polymers applications used in automotive industry,

new applications in health & beauty)

� Business portfolio expansion will continue mainly through acquisitions

� With stringent return criteria: target ROCE of 15%

Growth potential of target a key decision factor

33Group presentation I September 2013

Table of contentsTable of contentsTable of contentsTable of contentsGroup presentation

� Imerys: the world leader of mineral-based specialty products

� A profitable and solid business model

� Development strategy: accelerating growth by enlarging

our business footprint

� Conclusion

34Group presentation I September 2013

Ambition 2012 – 2016 to increase value

� Generate organic growth* above worldwide GDP

� Increase resilience through additional products and geographical diversification

� Seize selective external growth opportunities

Maximize value creation for shareholders

* Excluding exchange rates and perimeter effects

35

� Imerys 154 rue de l’UniversitéF-75007 Paris + 33 (0) 1 49 55 63 00 www.imerys.com

� Analysts / Investors contactPascale Arnaud+ 33 (0) 1 49 55 63 [email protected]