Download - IMC notes (1)

Financial markets and Institutions Types of Investments

Debt – i.e. tradable bond, issued by a company or govt or non-‐tradable bank loan, bank deposit

Equity/share – tradable securities giving an ownership stake in a company

Other include commodities, property, derivatives, foreign exchange

Savers can invest in the above directly or indirectly (through an intermediary) – through insurance companies, pooled investment vehicles, or pensions schemes. The indirect method gives:

• Diversification • Reduction in transaction costs • Access to expertise • Access to assets that would otherwise not be available

UK banking system uses the universal bank model involves providing financial services of various kinds, including advisory services, in addition to deposit and lending services.

Types of Assets

Tangible assets such as land and buildings (property, or real estate), machinery, oil, sugar and gold, are all real assets. The utility of such an asset gives it an intrinsic value.

In a monetary economy, there are claims that may represent the right to a return, such as interest and the eventual repayment of principal (on a loan), or dividends payable out of a company’s profits (for shares in a company). Such claims are financial assets.

Shares

The ordinary shareholders of a company are the owners of the company. However, it is normal for ordinary shares to possess a vote.

Companies legally do not have to declare a dividend on ordinary shares, many of them do in order to maintain shareholder loyalty.

For public companies, this will not be paid until the shareholders have agreed it at the AGM.

Companies may only pay dividends out of post-‐tax profits – that is, from their distributable reserves.

In any single year, the dividend paid could exceed the profit for that year, because there may be distributable reserves brought forward from earlier years.

Bonds (fixed income securities)

A bond may be defined as a negotiable debt instrument for a fixed principal amount issued by a borrower for a specific period of time, making a regular payment of interest/coupon to the holder until it is redeemed at maturity, when the principal amount is repaid. Derivatives Derivative contracts is a term encompassing contracts such as futures, options and swaps which derive their value from the movement, up or down, in the price of an underlying asset. Derivatives contract enable investors to take a position in the price of an asset without actually taking delivery of the underlying asset. For example, a position can be taken on the price of oil, without participants in the related derivative contract taking physical delivery of oil at any point

Derivatives can be divided into exchange-‐traded and over-‐the-‐counter (OTC) types. • Exchange-‐traded derivatives are more standardised and offer greater liquidity • OTC contracts are tailor-‐made to meet the needs of buyers and sellers.

Currency transaction

Currency or foreign exchange trading (or FOREX as it is commonly known) is the dealing of the currencies of various countries. No formal market place for FOREX trades: in London, trading is over-‐the-‐counter (OTC). Prices are advertised on screens and deals are conducted over telephones. The major players are investment banks and specialist currency brokers FOREX transactions are described either as spot or forward.

• Spot means the trade is to meet immediate currency needs and will settle in two business days after the trade day (known as T + 2).

• Forward is when an exchange rate is agreed today for settlement at some future date

Pooled Funds

In order to minimise the risk involved in investment, it is often a good idea for the investor to spread invested money over a range of instruments, thereby diversifying risk. Individual investors’ investments to be grouped together and form a collective investment vehicle. Here they pool their money in a large fund, which is managed and invested for them by a fund manager. There are different types of ‘pooled’/collective investment vehicle:

• Unit trusts • Open-‐ended investment companies (OEICs) • Investment trusts.

There are also exchange traded funds (ETFs), which are typically designed to track an index. Authorised unit trusts and OEICs are Authorised Investment Funds (AIFs) and are often referred to simply as funds. Differences A unit trust differs from investment trusts and OEICs in the way it is set up, as a unit trust is not a company with shares. Pricing For unit trusts and OEICs, there is a direct relationship between the value of the underlying investments and the value of units. Units are priced according to Net Asset Value (NAV). Investment trust shares and also ETFs, however, are priced according to supply and demand in the stock market. Unit trusts are, like OEICs, called open-‐ended funds as there is no limit to the amount of money which can be invested. If no ‘second-‐hand’ units are available, the fund is permitted to create more units and expand the fund. Investment trusts, on the other hand, are closed-‐ended: except when new shares are issued – eg, on launch of the trust – the buyer of investment trust shares is buying them from existing holders of the shares. The function of securities market

• Raising of capital • Transfer of risk • Price discovery • Creation of liquidity

By short-‐term capital, we mean capital that is lent or borrowed for a period which might range from as short as overnight up to about one year, and sometimes longer.

By long-‐term capital, we mean capital invested or lent and borrowed for a period of about five years or more, but sometimes shorter.

Price transparency, liquidity, transaction costs

Price discovery

The process through which an equilibrium price for a financial instrument is revealed continuously through bid and offer prices, and trading

• Market establish equilibrium price • Markets disseminate the price to investors/the public

Price Transparency

Important that the investor knows the price before, during and after a deal in order to be satisfied that he has a good deal

• Pre-‐trade transparent (data on quotes and orders) vs post trade transparency (publication of sizes and prices of trades)

• Organised markets are transparent than OTC

Liquidity

• Liquidity measured by bid ask spread in quote driven market or by difference between the best sell and buy prices in order driven markets

• Liquid markets are those where large quantities are traded or where order need to be very large to have an impact on price

Factors contributing to liquidity are: • Effective and efficient IT • Settlement systems • Stock availability • Stock lending facilities • Diverse membership

Must calculate round trip transaction costs incorporating bid-‐ask spreads, dealing commission and transaction taxes, both in percentages and in absolute amounts

Transaction costs

Broker commissions (pay fee to broker because investor can’t invest directly), bid ask spreads and market impact

Costs of a share transaction for a UK investor can be broken down as follows:

Purchase cost. • The purchase cost includes a spread which is the difference between the bid and

offer price of the share. Broker's commission

• Brokers incur various costs for the resources they employ to fill orders, including costs for market data and order routing systems, exchange memberships and fees, regulatory fees, clearing fees, accounting systems, office space, and staff to manage the trading process.

• A typical charge could be, say, 1.5% on a deal up to £7,000 and 1.0% above that, with a minimum charge of £25

Stamp Duty and SDRT • Stamp Duty Reserve Tax (SDRT) is payable at 0.5% on the value of purchases of UK

equities settled through CREST (ie most transactions), rounded up to the nearest 1p and on equities not settled through CREST, at 0.5%, rounded up to the nearest £5. (There is no Stamp Duty if the charge so calculated would be £5 or less.)

Panel on Takeovers and Mergers Levy

• The PTM levy is a flat £1 on transactions (sales and purchases) that are in excess of £10,000

Market Impact

• Buyers putting through large buy orders may need to push up the price of the security up in order to make the trade.

• Sellers who want to put through a large sell order quickly may need to accept a lower price than is immediately available to a seller with a small order.

• The cost effect of this tendency for fluctuating order sizes to move prices is called the market impact or price impact, and is a significant component of transaction costs for large financial institutions.

Limit orders, which will be filled only if the price is better than the stated limit, provide a way of limiting transaction costs, Market orders are filled at whatever prices are available when the order is placed.

LSE trading platforms

Three domestic trading platforms at the LSE

Characteristics of these platforms can be summarized as whether or not they are:

• Order driven v quote driven

This is decided by:

• Depends on liquidity of share

The trading platforms for domestic securities are:

• SETS • SETSqx • SEAQ

LSE Settlement period T +2-‐ when all paper work and legal details are in place/money also moved between relevant bank accounts

Stock Exchange Electronic Trading Service (SETS)

• Automatic matching for trades in most liquid listed shares • Only LSE members can place orders • Only standard settlement permitted

o T+2 • Orders ranked by price then time of input • Change in order -‐> new input time • All trades anonymous due to LCH Clearnet acting as central counterparty service

(CCP) – process known as novation

SETS – Quote and crosses (SETSqx)

• Hybrid System – for less liquid stocks • Combines quote driven platform with periodic (orders) electronic auctions

(uncrossings) • Auctions at opening (8:00am), 11:00am, 3:00pm and closing (4:35pm) • If want to trade at other times of the day, Market makers must quote bid and offer

prices for transactions of at least 1* NMS (Normal market size) – per person or on a whole basis?

NMS is a minimum volume set by LSE

Stock Exchange Automated Quotation System

Price dissemination system

Pure quote driven

System used by the LSE to display market maker prices on AIM stocks (not traded through SETS or SETSqx)

• Minimum of two market makers input bid-‐ask spread into SEAQ • SEAQ displays two way prices to Public (brokers/dealers/investors) • Brokers Dealers deal by phone with market makers

Only market makers are able to quote prices on SEAQ

Gilt Market

The gilt-‐edged market is a further major capital market in the UK. The government borrows over the medium and longer term by issuing government stocks (called 'gilt-‐edged stock' or ‘gilts’).

Trade in second-‐hand gilts will continue until the debt eventually matures and the government redeems the stock.

Gilts settle T+1 via Euroclear UK & Ireland (using the CREST system)

Less liquid than shares, so will need quote driven system with market makers (investment banks)

Gilt Edged Market Makers (GEMMs):

• Required to make 2 way prices to customers • Must provide information on closing prices, market conditions and their turnover

and positions • Are expected to participate in Debt Management Office’s gilt issuance program • Must always participate when DMO issues further debt

Main holders: UK pension funds, insurance companies overseas investor + less extent wealthy private individuals

Quoted excluding interest (clean pricing), however settlement price includes accrued interest (dirty pricing)

Actual bond transaction prices reflect accrued interest based on actual/actual basis

Holders of gilts can now receive coupon payments gross

New Issues of gilts

Issued by Debt Management Office (DMO) to fund the public debt/Public Sector Net Cash requirement (PSNCR) or to refinance maturing debt

DMO typically issues gilts by auction (preferred method)

All bidder in market bid what prepared to pay for certain volume of gilts

Alternative arrangement is ‘tap’ method –issue announced, investors invited to tender. Smaller volume of gilts.

• If a part not take up at the required price – that part is withdrawn and released into the market later

Alternative trading venues

Set up outside of LSE

Dark Pools

• Price transparency does not need to be as high • Electronic trading platforms where neither price nor identity of trading firm is

revealed • Don’t know prices someone else is willing to buy or sell at • Post trade transparency is possible but not pre-‐trade

Multilateral trading facility

• Electronic trading platforms arranged in a similar manner to SETs but designed to be cheaper than SETs trading

• Lots of investment banks, get together cause LSE charges hefty fee to trade: BATS, CHIX, less than half blue-‐chip now trade on LSE

Systematic internalises

• Investment banks who execute client orders by trading for their own account rather than with an exchange or MTF

• Trade their own stock

Should know description to match to right platform for exam

Algorithmic trading

Algorithmic trading

A broad term describing all scenarios where electronic platforms:

• initiate orders or • decide on/ recommend aspects of orders (timing, price, quantity) generated by

humans

High frequency trading

• A subset of algorithmic trading where computers make decisions or initiate orders based on electronically received information before (human) traders get change to process what they observe.

Role of LSE member firms

Main market is London Stock Exchange whose members are:

Broker/Dealers

May act in dual capacity (Big bang in the 1980s made this possible)

• Broke a customer’s business (agent) • Deal directly or buy securities for own business (principal)

Equity market makers/Gilt Edged market makers

• Must quote two way prices • Make market

Interdealer brokers (IDB)

• Arrange matched anonymous principal to principal trades between market makers • Safety valve, esp. for gilt edg3d market makers who are obliged to follow through on

deal up to certain size, could find themselves loaded up with securities. If large stock cant shift on market directly as other members will lower price. To help them unwind large positions the IDB act as brokers to market makers to allow them to trade large positions anonymously.

The Stock Borrowing and Lending Intermediaries

• If market makers wish to take a short position in a stock, ie sell more than they currently have on their books, they will need to have stock in order to settle the trade.

• The Stock Borrowing and Lending Intermediaries (SBLIs) provide access to large pools of unused stock.

• The institutional investors in the UK buy large blocks of securities and often hold these blocks for a number of years. The SBLIs borrow stock on behalf of market makers from these

dormant positions. The stock is passed to the market maker who uses it to settle the trade, and in effect, to go short.

Central counterparty (Novation)

Clearing house (LCH:Clearnet)

Central counterparty stands between buyers and sellers

• Short seller to every buyer • Log buyer to every seller

Purpose: eliminates counter party-‐risk

When dealing directly with someone else there is risk that they won’t deliver on their promise (won’t pay before delivering security)

LCH.Clearnet Margining

Initial Margin

• Returnable good faith deposit paid on opening positions • Based on maximum probable one –day loss (amount security can fall in value in one

day)

Variation Margin

• Cash Settlement of daily profits or losses based on closing price each day • Paid to or received from LCH Clearnet the following morning. • If one side decides to default whole contract is void

UKLA and LSE

Companies have limited liability and can be private (cannot offer shares to public) or public

Public PLC can offer shares to public (majority do not)

If offer shares to public:

May choose to trade shares on exchange as will struggle to sell shares without secondary market for buyer to sell shares and realise profit.

To trade on exchange most commonly you have shares listed on full list of LSE, must satisfy req of UKLA (FCA) referred to as competent authority

• Listing: must satisfy UKLA listing requirements

Onerous requirement led to junior markets

• AIM: not regulated directly by FCA, is reg by LSE requirements • ISDX: UKLA requirements

UKLA listing Rules

Main conditions for full listing:

There are two tiers of listing:

• Premium listing (required for FTSE UK Index membership), involving the UKLA’s ‘super-‐equivalent’ requirements, which go beyond EU standards

• Standard listing, with less stringent requirements that are broadly similar to AIM requirements

Requirements:

• Minimum market capitalisation: o ≥£700,000 shares o ≥200,000 debt – if want debt to be traded

• Freely transferable -‐ cant restrict • 25% in public hands – free float/in public hands (excludes shares held by founders,

or huge blocks of shares)

Premium listing extras:

• Must have 3 years continuous trading record/ • 3 years of audited accounts (waived for innovative high growth companies and

investment companies. • Company must show that it has sufficient working capital to cover the next 12

months at least, • Must be a sponsor for the admission

Prospectus (prospects of company before they offer shares to public) has to be published unless the offer is made to:

• Qualified investor • Fewer than 150 persons (private placement) • Minimum amount you can invest per investor is high -‐ €100,000 • Total consideration of the offer less than €100,000 • Shares representing less than 10% of the shares already admitted for trading

UKLA Continuing obligations

Must allow market to have full understanding of company’s position

Disclose

• Price sensitive information • Significant transactions – plans to sell large chunk of buswiness • Changes in directors • Changes in registers – key shareholders • Dividend distributions – when they decide to distribute

Listed company discloses to -‐>

Primary Information providers (PIP)/Regulatory Information Service (RIS – part of LSE) (these entities are signed off by the FCA) tells -‐>

Quote vendors (Bloomberg and reuters etc.)

AIM/ICAP – ISDX markets rules

AIM

• Appoint NOMAD (nominated advisor) – expert financial services firm that ensure they fulfil obligation to aim rules

• Produce admission document • Securities must be freely transferable • Should have broker to support trading of the company shares • On-‐going obligations to publish price sensitive information immediately and

disclose significant transactions. • Lock in – companies with less than 2 years track record must agree to lock-‐in where

directors, significant shareholders and employees with 0.5% or more of the capital agree not to sell their shares for 1 year following admission.

• No minimum market capitalisation • NO minimum proportion of shares held by public

ICAP Securities and derivatives exchange (ISDX)

Applicants must:

• Appoint ISDX corporate advisor – specialists financial services firm • Demonstrate appropriate corp governance – how comp managed and directed • Have published audited accounts no more than 9months prior to date of admission

to trading • Adequate working capital – short term finance for business to run for next 12

months • Free transferability of shares – cant restrict ownership • No minimum market capitalization

Dual listed companies

Structure where two corporations function as single operating entity (e.g. Royal Dutch shell (UK & Netherlands))

• Separate legal entities and stock exchange listings – with supervisory board • Equalisation agreement – legal contract – describes how ownership is shared • Single board of directors, single management structure • May have tax advantaged • Arbitrage opportunities may arise-‐ risk free profit where two things should be the

same but are priced differently

Cross-‐Listing

A company may list its shares on more than one exchange – for example, a UK company may list in on the LSE in London while also making its shares available through American Depository Receipts (ADRs) (discussed further later in this Chapter) in New York. This is termed a cross listing.

Note characteristics for exam

Disclosure and Transparency Rules -‐ UK

Companies keep registers for all shareholders but sometimes shareholders could be hidden

Nominee broker deals on behalf.

Holders (including connected parties) of 3% and go up or down through a % point

• If holdings reach (3%), • falls below 3% • or moves through any percentage point above 3% • Notify company by T+2

Persons discharging managerial responsibilities (PDMR) (and their connected persons (family)) must inform company of any transactions in own company shares/derivatives

• Notify company by T+4 • Company tells market via regulatory information service (RIS)/Primary information

provider (PIP) by next business day. T+1

Not just shares but also any derivatives

Legal owner is anyone connected whether directly or indirectly

Settlement period

• From 6 October 2014, standard settlement in the UK is T + 2 for equities. • The ex-‐dividend date will always be a Thursday • These changes comes ahead of a proposed January 2015 start date for T + 2

settlement across the European Union. • Settlement of UK Government stocks (gilts) is normally T + 1, or on the same day

• Settlement in sterling or euros is made on a Delivery versus Payment (DVP) basis,

where both parties are ready to settle with each other at the same time, known as real time gross settlement.

Connected parties

Includes:

• Family stockholding • If you own a third or more of any company, that companies stockholdings are

included • Concert party = two or more persons who agree (formally to informally) to act in

agreement(e.g. investment club)

Each persons must notify that they are party to the agreement

Meetings

Annual general meetings (AGM)

• Must be held every calendar year (max gap 15 months) • Must be within 6 months of financial year end • ≥21 days notice required

• Members attend/send proxy • Standard tasks undertaken

o Approve accounts o Approve dividends o Approve (annual) reports of the directors and auditors o (Re)appoint directed o (Re)appoint auditors

All of these will be voted on.

Can be done via show of hands

• If more than 10% or at least 5 shareholders present request paper vote, company must do so

Proxy

Proxy power normally lasts for given meeting and any adjournments that may be created

• General proxy – flexibility in decision making, vote as they feel is appropriate • Special (two way proxy) – told how to vote

General Meetings

General meeting (any meeting other than AGM)

Can be requested by holders of > 5% in private company or 10% in public of paid up capital share.

If this happens:

• Directors must call general meeting within 21 days • Notice Period (≥ 14 days) -‐ notice to allow shareholders to come • Meeting must be held within 28 days of the notice calling to a meeting being sent

out.

Ordinary resolutions require > 50% votes cast

Special resolutions require >75% of votes cast

Corporate governance regulations (1)

UK Code on Corporate Governance

Main principles of the Code:

• Leadership -‐ Board is collectively responsible, lead by chairman • Effectiveness – board to have balance of skill, experience, knowledge • Accountability – board should present a balance assessment of firm position • Remuneration -‐ remuneration levels to be able to attract retain and motivate (NB

All Medium and late companies, irrespective of listed status are require to public remuneration report)

• Relations with stakeholders – dialogue and mutual understanding

Code applies to listed firms only, compliance non-‐mandatory, disclosure required or if they don’t they must explain in AGM why they did not

Stewardship Code

Financial reporting council also crated the stewardship code (2010) directed at (big shareholders) institutional investors, consisting of 7 principles:

1. Publicly disclose their policy on how discharge stewardship responsibilities 2. Have a robust policy on managing conflicts of interest 3. Monitor investee companies 4. Guidelines on when and how activities escalate to protect or enhance shareholder

value 5. Be wiling to act collectively with other investors 6. Clear policy on voting (and periodic disclosure of voting activity) 7. Report periodically on stewardship activities – to underlying clients using them as

investment manager

The Principal – agent problem

Small firms

• Owners = managers

Large firms

• Owners (principal) • Managers (agents)

This is Separation of ownership and control

The agency problem arises when large firms often owned by many shareholders appoint managers to run the firm.

The interests of the shareholders may be significantly different to the interests of the managers.

Possible solutions:

• Align the incentives – shares and stock options • Board of directors monitoring managers • External pressure (on managers) – if not being run well, it becomes a takeover target • Shareholder activism – turning up at AGM, grouping with other shareholders to

remove poor directors by voting them out

Functions of financial services industry

4 Function of financial services industry

Financial intermediation

• Linking those with capital to lend with those who need capital

Pooling and managing risk

• Pooled investment funds insurance or derivative products

Payment and settlement services

• Mechanisms for the transfer of money or assets

Portfolio management

• Allows investors to manage their wealth through advice and management services

The role of the government

• Production of services that the private sector is unwilling or unable to deliver • Regulation of firms (to ensure consumer protection) • Intervene in the distribution of income and wealth • Stabilization of the economy (reduce fluctuations of income employment and prices)

EU and UK

The European Union is an example of an international economic association.

It has a common market combining different aspects, including a free trade area and a customs union.

• A free trade area exists when there is no restriction on the movement of goods and services between countries.

• This may be extended into a customs union when there is a free trade area between all member countries of the union, and in addition, there are common external tariffs applying to imports from non-‐member countries into any part of the union.

A common market encompasses the idea of a customs union but has a number of additional features.

• Free markets in each of the factors of production. o E.g. A British citizen has the freedom to work in any other country of the

European Union. • Also aims to achieve stronger links between member countries

o e.g. by harmonising government economic policies and by establishing a closer political confederation

UK membership of the EU has restricted the previously unfettered power of Parliament. There is an obligation, imposed by the Treaty of Rome on which the EU is founded, to bring UK law into line with the Treaty itself and with EU Directives. Regulations, having the force of law in every member state, may be made under provisions of the Treaty of Rome Monetary Policy

The Monetary Policy Committee (MPC) of the Bank of England was charged with the responsibility of setting interest rates with the aim of meeting the government’s current inflation target

-‐ 2% measured by CPI, plus or minus 1% The MPC decides the short-‐term benchmark ‘repo’ rate at which the Bank of England deals in the money markets.

International securities markets

Why would investors want to invest in overseas securities?

Maybe Diversification, more return.

European Equity

• Typically done on electronic order matching systems (like SETS) • Operate under European directives from EU to make sure rules are broadly similar

US equities

• NYSE uses floor based specialist system – trading floor, individual trading directly on floor

• Presence of designated market makers – each stock that trades is run from central trading post-‐ more than one stock attached to trading post. Each trading post will have designated MMs assigned

• A lot trade by universal trading system (like SETS)

Emerging markets equity

Unique challenges due to often poor:

• corporate governance • Transparency • Regulation • Liquidity • Political risk=>volatility

Eurobonds

Eurobonds markets (international bond issue use by governments, corporations and banks)

Debt instrument issued by borrower normally outside of the country in whose currency it is denominated.

Companies issuing debt in the Eurobond market have their securities traded all around the world.

Since its Unsecured debt, the market only accepts highly rated companies.

• Pay coupons gross and annually/issued in bullet form • Bearer (form) instruments – issuer does not retain a formal register of ownership,

however to make sure settlement go through CCP will hold register (not open to government or tax authorities)

• Does not attract withholding tax for this reason (bearer form) • There is no formal market place • Market is telephone driven • Market Regulated by ICMA (international capital market association) • Gilts settle T +1 • Corporate bonds: confirm T+1, settle T+2 – requirement of ICMA

• 2 independent clearing houses do settlement: Euroclear or clearstream • These clearing houses immobilise the stocks in their vaults and then operate

electronic registers of ownership

Eurobond Process

• The most common form of issue used in the Eurobond market is a placing. • Issuer appoints a lead manager and award them the mandate. • Mandate gives lead manager power and responsibility to issue the bond on the

issuer's behalf. • Lead manager then creates management group of other Eurobond houses. • Each house then receives a portion of the deal and places it with its client base. • The lead manager may elect to run the entire book alone, and miss out the other

members of the management group.

Fixed price re-‐offer

• Lead manager can amend the terms of the issue as market conditions dictate. • Under fixed price reoffer, members of management group are prohibited from

selling bonds in secondary market at below the issue price until the syndicate is broken

• Syndicate breaks when lead manager believes the bulk of issue has been placed

Central Securities Depositories

Central Securities Depositories (CSD) hold securities. The fundamental objectives for the establishment of a CSD are for gains in efficiencies and for reduction in risk. Efficiency gained through:

• the elimination of manual errors

• lower costs • increased speed of processing through automation

Which all translate into lower risks. Almost all countries have some form of central depository where the securities are either immobilised or dematerialised

• In a 'dematerialised' system, there is no document, which physically embodies the claim.

o The system relies on a collection of securities accounts o instructions to financial institutions which maintain those accounts, and o confirmations of account entries

• Immobilisation is common in markets that previously relied on physical share certificates, but the certificates are now immobilised in a depository, which is the holder of record in the register. Access by investors to the depository is typically through financial institutions which are members of the depository

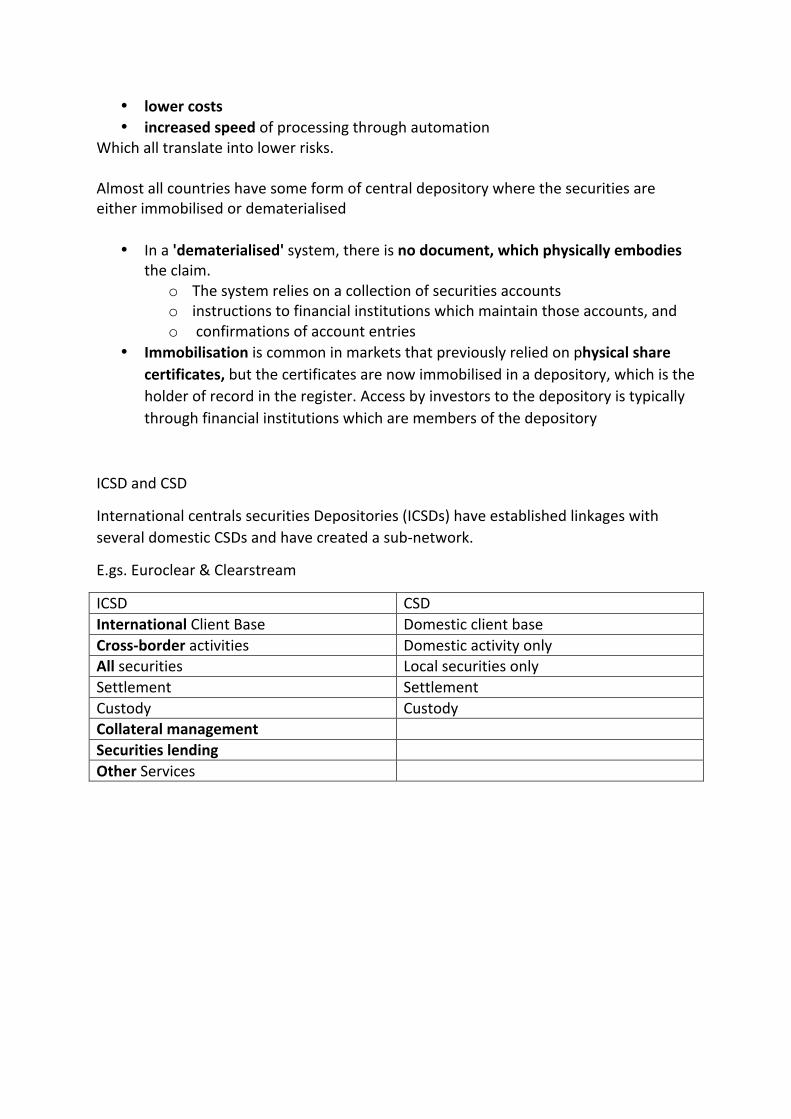

ICSD and CSD

International centrals securities Depositories (ICSDs) have established linkages with several domestic CSDs and have created a sub-‐network.

E.gs. Euroclear & Clearstream

ICSD CSD International Client Base Domestic client base Cross-‐border activities Domestic activity only All securities Local securities only Settlement Settlement Custody Custody Collateral management Securities lending Other Services

Regulatory Environment Eu Directives is an obligation for member states to ring their law in line with the directive.

Member states (UK)

• UK government – writes the laws in UK • HM Treasure

Acts

• Public interest disclosure act • Trustee Act 2000 • Data Protection Act 98 • Pensions Act 2004 • Financial Services & Markets Act (2000) -‐ most relevant for exam • Financial Services ACT -‐1021

Regulatory bodies

• FCA • Bank of England

o FPC o PRA

• Take Over Panel • Competition Markets Authority

Legislative Structure

Financial Services & Markets Act

Primary law – tend to deal with top level stuff, guidelines and principles

Enables secondary legislation

• (Regulated activities order, financial promotions order)

Enables the power of regulator to write detailed rules for industry and enforce those rules

Historically there was single regulator –FSA

Disbanded in 2000 and his power was handed to two regulators (FCA and PRA)

Prior to 2013

Single regulator FSA – covered botha spwcts of regulation which has two starnds

Conduct -‐ dsy day operations of company

Prudential – financial safety and soundness of cpmany – make sure company isn’t ging bust ensuring that if nees to payback debt can do without falling into default.

Problem with this was that it ws hard to keep eye on both aspects at once.

• Analysts felt UK felt credit crunch so badly because regulator took eye of the whole. Northern rock was looked into and made sure customers were being treated fairly, but didn’t see that it was about to go bust

Financial Services Act split FSA into:

• Conduct was taken on by FCA • Prudential take on by PRA

FCA -‐ accountable to government (Her majesty treasury)

• Regulates provision of financial services to consumers • Will aim to protect and enhance confidence in UK financial system • Deal with conduct of around >26,000 firms/every firm across the industry

PRA – division of the bank of England (Micro picture, individual firms and spotting if issues at the individual firm level)

• Objective to promote safety and soundness of regulated firms • Designed to minimise the adverse effects of firms failure • Only do checks on 3000 firms, those that are systemically important (firms that

would be too damaging to fail:

Includes:

• all banks • Insurers • And large firms

Leaves prudential bit for other 23,000 to FCA.

FPC – division of bank of England, looks at Macro across industry as a whole

• Responsible for macro prudential regulation • Aim to ensure the stability of financial system as a whole

FCA

FCA took legal structure of FSA in April 2013

Responsible for conduct supervision of all firms and for prudential supervision of non-‐pra firms

Supervises trading and market infrastructure

Competent authority for listing and prospectuses and is referred o as the UK listing Authority. UKLA and FCA – two separate roles, but conducted by same body.

UKLA responsible for approving companies seeking a listing and for writing and enforcing the listing rules (part of FCA handbook)

Responsibility for client assets oversight and countering financial crime

FCA has: 1 strategic, 3 operational objectives

Legal high level strategic objective to ensure relevant markets are functioning well

Operational objectives: PIC, protection, integrity, competition

• Secure and appropriate degree of protection for consumers o Keeping bad companies and products out of the industry o Compensation and redress in event of things going wrong

• Protect and enhance the integrity of the financial system • Promotion of effective competition in the interests of consumers

PRA

General objective: promotion the safety and soundness of regulated firms

• Uses resolution planning (companies version of living will – preparation for in case they go bust) to ensure that firms that fail do so in an orderly way

• The PRAs approach to supervision emphasises the importance of judgements made by supervisors. – is company at risk of going bust in the future, judging the firms to find at risk firms

FPC

• Responsible for identifying monitoring systematic risks, and taking action to address them

• Makes recommendations and gives directions to PRA and FCA

• FPC is required to take economic growth into account • FPC will publish two financial stability reports every 6 months.

Authorisation Requirement

Firms are required to be authorised – licensing program imposed by regulators on companies

Section 19 of FSMA 2000 – The general prohibition

• Company cannot conduct a regulated activity in the UK by way of a business (financial service main part of business) unless they are authorised or exempt.

If breached, then company taken to court

Civil court or criminal court – difference relies on evidence of guilt

Dual regulation

Banks and Insurers

• Systematically important so they are monitored by PRA for financial safety and soundness • They are also supervised by FCA who will be monitoring their day to day conduct.

All other firms – FCA is responsible for financial safe and soundness as well as conduct.

FCA/PRA Permission

Dual regulated firms will apply to the PRA for authorisation. However, the FCA will be consulted and will give or refuse consent to the PRA based on conduct implications. PRA will be bound by the decision.

What are regulators looking at when looking to authorise a firm:

Authorization is given by obtaining part 4a permission and fulfilling the relevant threshold conditions which depend on whether dual or FCA only regulated.

Threshold conditions depend on whether regulated by FCA or FCA and PRA

Threshold Conditions Application Location of Office (head office needs to be in UK so you can be sued by UK law if problems)

FCA & dual reg

Effective supervision (is business transparent enough for regulators to check your meeting requirements, FCA – business activities, (how/what selling) PRA – finances)

FCA and Dual Reg

Suitability (fitness and properness, are you going to be run well y good directors who will benefit customers)

FCA and Dual Reg

Business Model (what you have planned/is it sustainable)

FCA and Dual Reg

Appropriate resources (financial and non-‐fin) Need to see whether your human resources are good, people of right calibre. Financials are needed as FCA will be looking at soundness of these companies

FCA firms only

Business conducted in prudent manner (Reason for being of PRA, company must be prudent in how dealing are handled/ensure not about to go bust)

Dual regulated firms only

Appropriate non-‐financial resources (PRA interested in whether you have right people around to run the business)

Dual regulated firms only

Claims reps (insurers only) – claims reps

Dual regulated firms only

Legal status (insurers only) Dual regulated firms only

Need to know all 9 of these

Legislative structure

Does the firm need authorisation? – very examinable

1. Is it doing a regulated activity? If Yes, 2. Is it regarding a specified Investment? If Yes, 3. Is it an exempt person? If No

You would need Authorisation!

Regulated Activities

Regulated activities or (specified activities under the Regulated Activities Order) – there are 16

Can be divided into:

Wholesale financial services activities – big financial (investment banks -‐buyside) service firms (7)

• Dealing in investments (buying and selling assets)

• Dealing as an agent (executing orders/trading/broker for others (3td parties)) • Operating a MTF Multilateral trading Facility (alternative trading platform outside of

conventional stock exchange – institutions trade between themselves and allow some others to trade on their exchange too)

(Investment Management Community (sell side))

• Managing investments (managing money for clients) • Advising clients

(Back Office functions)

• Safeguarding of investments -‐ (custody, making sure legal title has ben correctly transferred, making assets have been bought legally and are safely kept and all legal title in clear)

• Sending de materialised instructions -‐ (Clearing houses perform this -‐ no longer have bits of paper floating about, information sent electronically via various dedicated systems (SWIFT) to make sure custodians know what has been dealt)

Insurance

• Offering/effecting insurance – selling or running insurance contracts to clients • Assisting in insurance – certain activities that may be carried out by legal 3rd party for

insurer (underwriting risk, claims handler – may not offer or handle insurance but are vital if you want to claim on insurance)

• Lloyds (of London) – specialised insurance market (original home of insurance) – specific insurance market for insuring big ticket risks ships sinking or office being attacked) on Lloyds trading floor these big things are insured then the risk is traded between the various Lloyd companies or members

Retail

• Deposits takers • Offering electronic money services (paypal) • Regulated Mortgage (on primary residence) mortgages on second homes or buy to let are

not necessarily regulated • collective investment schemes (CIS) – a fund

o Authorised unit trust o Open ended investment company (investment company with variable capital)

• Funeral plans -‐ really a form of collective investment scheme

Agreeing to provide regulated activities – process of becoming regulated is quite long, what firms do is while going through service they start legally committing to provide services by agreeing contracts with parties for the future.

MADAM LEASES ACAFE

• Multilateral trading ability • Advising on investments regulated mortgage/home finance contracts/stakeholder products

• Dealing in investments as principal or agent • Arranging regulated mortgages/deals in investments • Managing investments

• Lloyds insurance market related activities • Entering into/administering a regulated mortgage or home finance contract • Accepting deposits • Safeguarding/administering investments • Establishing/operating winding up a CIS or pensions scheme • Sending dematerialised instructions

• Agreeing to provide regulated activities • Carrying out or effecting contracts of insurance • Assisting in the administration and performance of a contract of insurance • Funeral plan contracts • Electronic money

What’s an Investment?

Specified investment:

Securities:

• Shares -‐ in any company • All tradable debt

o gilts o bonds o treasury bills (short term tradable debt issued by British government) o commercial papers (short term tradable debt issued by companies), o certificate of deposits (bank account that’s tradable), o FRNs (floating rate note-‐ bond with variable rate of interest. o Private loans are not tradable unless they are securitised. o Premium bonds are not tradable – they are like private loans between individual

and companies • Hybrids

• Depositor Receipts – don’t actually take ownership of share, share remains in hand of depositary investment banks, but you get any benefits of share like price appreciation or dividend s and votes – allows people who don’t want to trade directly to trade • Global depositary receipt • American depository receipt

• Warrant o Options right to buy shares are specified price

• Rights to or interest in investments

o Repos – sale and repossession agreement – investment bank sells bond cause it needs some short term money and when it sells bond it includes agreements to repurchase bond.

Derivatives – very examinable

• Options on investments (anything in securities) and on currencies, gold, silver, platinum and palladium (precious metals)

o Options on commodities are not specified investments (neither are commodities themselves)

• Futures for investment purposes -‐ obligation to buy or sell some underlying asset in the future (regardless of underlying asset, it is a specified investment)

• Contracts for difference, e.g. swaps, forward rate agreements, spread betting in general

Insurance

• Contracts of insurance – life and general • Lloyds investments

Retail

• Deposits • Rights under a regulated mortgage (primary residence) • Rights under a funeral plan • Units in CIS – unit trusts & OEICs • Personal and stakeholder pensions (private – personally made decision to take out which

differs form occupational investment) -‐ subset of above

Exempt persons – from formal regulation process

Reason recognised institutions are exempt is because they are recognised, recognition process is far more demanding

5 different classes of exempt people -‐ APRIL

Appointed representatives (Tied agent)

• Independent legal entity e.g. self-‐employed insurance salesman • If tied agent breaks any rule, the parent company will be punished

Professional People (regulated by designated professional body)

• Lawyers, accountants and actuaries

Recognised Institutions

• Recognised investment exchanges (LSE) • Recognised overseas investment exchanges (NASDAQ)

o Overseas exchange that can trade on form the UK with approporate terminal • Recognised Clearinghouses

o e.g. Euroclear (crest)

Intuitions (that are specifically exempt)

• e.g. IMF or Bank of England,

Lloyds members

• Made up for firms or syndicates/members that trade insurance on Lloyds of London trading floor.

• To do this trade you must be a formal Lloyds member • Lloyds itself is regulated but its member firms are not • If any firms breach FCA rules, Lloyds will punish (like appointed representatives)

Principles for Businesses (firms)

1. Integrity – acting without dishonesty, or intentionally misleading customer (1=I) 2. Skill care and diligence – you don’t mislead customer through lack of research (2=Due-‐

diligence) 3. Managements and control – CEO has sub managers and they have team managers reporting

to them, a clear tree of management control (3=tree) 4. Financial prudence – businesses does not overstretch itself (4=door=often see chancellor

standing outside door who should be most prudent person) 5. Market conduct – standards of conduct differ across markets (5=hive –full of honey and

money sells on market) 6. Customer interests – TCF-‐ always act in customers best interest (6-‐fixed (rate of

return/interest) 7. Communications with clients – clear fair and not misleading – (7=heaven, clients are gods) 8. Conflicts of interest – recognises and manage these conflicts (8=hate of conflict) 9. Customer relationships of trust -‐ (9-‐ wine, trusting relationship have a dinner and rink with

customers) 10. Clients assets – keep client assets safe and warm until mature into cash (10-‐hen (nurtures

eggs) 11. Relations with regulators (Open and honest with regulators (11-‐RR)

Individuals can sue firm if they are hurt because firms breached a rule

Hurt Individual cannot sue firm for breach of principle

Regulation of investment exchanged

FCA has recognised number of investment exchanges such as:

• LSE • NYSE Liffe • London metals exchange

Recognised exchanged are required to deliver a high standard of investor protection and market integrity

• Exchanges have to undergo higher level of checking out to become recognised

Recognised clearing houses that used to be recongised yb the FCAs predecessor the FSA, but are now regulated by the Bank of England

Off exchange derivatives (OTC)

• largely unregulated • but settlement and clearing now subject to new requirements* such as clearing through

central counterparty risk management procedures and reporting.

Regulation of derivatives

MiFID applies to firms carrying out activities in relation to any derivative instrument

UK market regulated by the FCA (only in relation to those derivatives covered under specified investments)

International accounting standards states that (non-‐hedge) derivatives must be rescored in the balance sheet at fair value.

• If fair value changes over companies accounting year, then that should be recognised as a gain or loss in income statement

• Except derivatives used a hedge where gains and losses are recognised in reserves

Approved Persons (individual)

Within an authorised firm, people carrying out ‘controlled functions’ must be approved

Must satisfy the FCA as to fitness and propriety

1. Honest, integrity and reputation (going to jail may exclude someone from this) 2. Competency and capability (including the need to pass approved exams and an internal

assessment) 3. Financial soundness (if ever been declared personally bankrupt you probably cannot look

after other peoples money)

Key issue is disclosure, of when apply you do not disclose any relevant details, this immediately makes you dishonest.

• Approved persons must comply with FCAs “Statements of Principle”

Controlled functions

(SIF)

Significant influence functions -‐ run whole departments, have influence on companies direction, policies and how the business is run

Governing functions

• Directors, partners if partnership

Required Functions

• Compliance oversight (head of compliance) officer • Money laundering officer

Systems and controls -‐ To have necessary control in business that regulator says you must have

• Finance officer (head of finance) • Head of audit • Head of risk

Significant management

• Trading company -‐ Heads of settlement • Bonds-‐ Head of bond trading

Majority of people performing controlled function:

Customer function -‐ Anyone who has influence on customer’s wealth

• Investment advisor • Trader – indirectly by trading with market

Who undertakes approval:

If only FCA regulated (majority of firms) not considered systematic risk – FCA signs of any individuals

If working for dual regulated firms, PRA approves however PRA needs consent from FCA before grants approval

• PRA checks individuals will handle businesses finance in right way • FCA will check persons follows correct conduct rules on day to day basis

Statements of principle (approved persons) – distinguish from principle of business

Apply to all approved persons – first 4

1. Integrity 2. Skill, care, diligence 3. Proper standard of market conduct 4. Deal with regulator in open way

Apply only to significant influence functions -‐

5. Proper organisation of business – must run area of business responsible, clear organisational structure, clear job descriptions communicated clearly

6. Skill care diligence in management -‐ delegating is not abdication of responsibility, must understand what you are delegating to understand if person delegating to is doing good job and not rogue trading

7. Comply with regulatory requirements – must be proactive, ensure that areas of business you are responsible for respond to changes in regulatory environment,

The code of practice for approved persons sets out descriptions of conduct that does not comply with the above principles.

FCA Handbook

5 Main books

High level standards

• Principle for business • Statements of principles • Threshold conditions • Fit and proper test • Training and competence • Senior manage arrangements • System and controls

Business standards

• Conduct of business • Client assets • Market conduct

Regulatory processes

• Supervision • Decision procedure and penalties manual

Redress

• Complaints handling • Compensation – not very examinable

Regulatory guides

• Enforcement guides

Knowledge of other books not required – just know they exist should be enough

(prudential standards, specialist sourcebooks and listing, prospectus and disclosure)

Senior manage arrangements system and controls (SYSC)

Purpose:

• System and controls are appropriate to the nature, scale and complexity of the firm o Outcomes based so different companies require different types of systems

• Effective compliance systems (especially countering financial crime) • Create common platform of requirements for firms subject to CRD and/or MiFID

o To achieve consistency across Europe – Common platform

Apportionment of senior management responsibilities

• CEO responsible for apportionment • Knowing and recording who does what (recorded kept for at least 5 years from

organisational structure changes – MiFID)

Training competence and professionalism

All staff (everyone) employed in authorised firms must be competent

If dealing with retail clients:

• Employee must be assessed as competent • Employee must be supervised

Retail distribution review – new requirements from Jan 2013 when giving retail investment sector:

• Retail investment advisor must hold statement of Professional standing –issued by an accredited body such as the CISI

• The SPS confirms that the advisors hold an appropriate level 4 qualification and has completed a minimum of 35 hours CPD per year / 21hours must be structured

In addition to the above advisors must subscribe to a code of ethics

Takeover Code

Regulated by the Takeover Panel

Takeover panel Funded by a £1 levy on LSE share transactions (buyer and sellers) above £10k

Regulates offers for shares in all UK public limited companies (plcs) that are listed on exchanges

Key points

• Promote fairness (note: the code does not consider competition issues or public interest) o Equal treatment for all shareholders of a particular class o Allow a reasonable period for the bid to be considered

• Reduce occurrence of defensive measures take by target co. Discourage financial structure that make it difficult for someone to launch a takeover bid, so they can be launched so the investors can then decide whether or not they wish to go forward

• Mandatory bid is required if shareholder acquires > 30% of the voting rights of a company. They must make a cash offer to all other shareholders at the highest price paid in 12 months before the offer was announced.

o Below 30% considered minority shareholder. • Offer must remain open for >21 days • If achieve >90% acceptance – can compulsorily purchase remaining 10% • Directors of target company should not deny shareholders the opportunity to consider the

bid.

The competition and Markets Authority (CMA)

The CMA was established under the Enterprise and Regulatory reform Act 2013.

Will investigate all mergers if :

• Proposed merger where turnover of company is at least >70 m in UK • Or when combined market share is at least 25% of total

If either of two tests are breached they will launch a Phase 1 Study (takes up to 40 days)

• To determine If the merger results in substantial lessening of competition

Phase 2 Investigations

Merger may be approved, prohibited or remedies/conditions imposed

• Statuary time of 12 weeks following phase 2 for remedies to be implemented.

Fines

CMA is empowered to impose fines up to 5% of the combined worldwide turnover of merging companies for breach of an order.

They can also impose fines for failure to provide requested information.

Data Protection Act 1998

Data protection act applies when processing personal data

Data controllers must register with the Information Commissions officer (ICO)

If in contravention of data protection, commissioner can serve enforcement notice. Failure to comply with enforcement notice could lead to a £500,000 fine

Eight principles to ensure personal information is:

• Fairly and lawfully processed • Processed for limited purposes • Adequate, relevant and not excessive

o Required to keep data on customers to satisfy rules (anti money laundering). Data protection act would say that if you asks for information that is not required for regulatory purposes then they are in breach

• Accurate and up to date • Not kept for longer than necessary • Processed in line with an individuals rights • Secure • Not transferred to other countries without adequate protection

o If data moved must be confident that data protection rules in that country are adequate enough

• Person whose data is held is entitled to ask for access to that information (subject access request) and has the right to correct where appropriate.

o They can be charged a maximum fee of £10 for access (max fee of £2 for credit reference agency records)

o The person entitles to be told the source, purpose and recipients of data. o DPA 1998 requires that subject access requests take place within 40 days of the

request (including fees) being received.

Breach is a criminal act resulting in fines but not jail

Whistleblowing procedure

• Whistle-‐blower interests stem from Public interest disclosure Act 1998 -‐ Law • Law is detailed in SYSC – part of FCA handbook -‐ regulation • Process whereby a worker seeks to make a disclosure to a regulator or law enforcement

agency relating to criminal offence or breach of rules (e.g. FCA rules) • No contractual restrictions for whistleblowing • Should be no discrimination for whistleblowing

Trustee Act 2000

When set up a trust, should be legal trust deed behind it which gives clear advice of how any money should be invested

If no trust deed, trust act 2000 would be default

Trustees are in power to invest in any appropriate asset and must review investments and obtain and consider advice.

Pension Act 2004

Introduced new regulatory authority – the pensions regulator

• For occupational pensions • Defined benefit Pensions only – promise certain % of your salary when you retire

New Pensions protection fund for where an employer who runs a scheme becomes insolvent and unable to pay liability

PPF provides compensation up to 100% of benefits to existing pensions and 90% to those not yet retired (funded by charges on companies that run these pensions on other defined benefit pension schemes)

Minimum funding requirement replaced by scheme specific objectives:

• Required trustees of defined benefit schemes to prepare a statement of funding principles which will clearly outline how necessary funding will be achieved – outlines what future liabilities will be and how much companies needs to put in to attain that target

• This must be reviewed every 3 years.

Conducts of Business Sourcebook (COBS)

Who?

Applies to Authorised firms

What?

Day to day activity rules in relation to:

• Client categorisation • Financial promotions • Investment research • Suitability and appropriateness • Dealing and managing • Client assets and client money

Rules on Client Assets are covered by a separate sourcebook (CASS)

Client Categorisation

Anyone you would be offering financial services to are potential clients

Look at the level of knowledge of financial services that clients have

High level

• Eligible counterparty (other authorised firms) • Level of protection will be low

Eligible Counterparty – must want following services:

• Receipt and transmission of orders • Execution of orders • Dealing on own account

Per se eligible counterparties

Authorised firms

National, central banks, international/supranational intuitions

Low level

• Retail client • Level of protection will be high

Retail

• Individuals and persons • Small businesses

Medium Level

• Professional Client • Medium level of protection

Professional

• Authorised firms when business they seek when business they is not in eligible counterparties risk

• Large undertakings in non finance

Per se Professional client

Authorised firms who are not eligible counter party

National, central banks, international/supranational institutors and regional government

Institutional investor whose main activity is to invest in financial instruments -‐ SPV

A large undertaking which meets two of the following :

If subject to MiFID • €20m balance sheet total • €40m net turnover • €2m own funds

Non-‐MiFID

• €12.5m balance sheet total • €25m turnover • 250 average employees in year

or (single test trumps all others:

• £5m share capital/net assets

Clients can elect to opt up, subject to certain criteria

• Protection costs money, so may end up with cheaper fees

• Retail clients may be deemed unable to handle risk of certain products so may have greater access to products

General notification

Firms must notify clients of their categorisation

Prior to the provision of services firms must inform the client

• Any right to request a different categorisation and • Any limitations to the level of client protection that such a different categorisation would

entail

Elective professional Clients

3 letters in this process

A firm can treat a retail client as an elective professional client if:

• Firm carries out a Qualitative test and for MiFID business also a and Quantitative tests • Clients requests this in writing and • Forms gives clear written warning of the protections and investor compensation rights lost • clients states in writing in a separate document that they are aware of the consequences.

Qualitative and Quantitative tests

Qualitative test

Firm undertakes adequate assessment of KNEES

• Knowledge and • Expertise • Experience of the clients

This assessment hives firms reasonable assurance that client is capable of making their own investment decision and understands the risks involved

Quantitative test – only if MiFID business (3 Rs: Regular, Rich, Resume)

At least two of three of following:

• Client has traded in significant size on the relevant market (that they are seeking business with you in) at an average frequency of 10 per quarter over previous 4 quarters

• Financial instrument portfolio > €500,000 • Client works/has worked in financial sector for at least 1 year in professional position which

requires knowledge of transactions/services

Financial Promotions

Must follow rules appropriate to type of client

Financial Promotions -‐ Invitation or inducement to engage in investment activity

Written promotions (non-‐real time)

• Adverts • Letter • Mailshots • Websites • Emails

Non-‐written (real time promotions) – potentially more aggressive

• Meetings • Telephone Calls

FSMA 2000

Financial promotion can only be issues by an authorised financial services firm, if not authorised would need approval by authorised financial firm

• e.g. Overseas financial firm not authorised would may seek to enter UK market

COBS Financial Promotion

Communication and financial promotions must be fair, clear and not misleading

Guidance:

A firm should ensure:

• It is clear if a clients capital is at risk • Any yield figure quotes gives a balanced impression of short/long term prospects

o If 1st year of investment gives bonus high rate, but drops in subsequent year must give balanced view of this

• Complex charging structures are explained • The FCA is named as regulator • A clear impression is given of any 3rd party packaged/stakeholders product provider

Exceptions

• Those communicated only to investment professionals (dragons den types) or eligible counterparties

• Excluded communications – if there are another set of rules that apply to communications. E.g. takeover rules take precedence over financial promotions rules

• A ‘one-‐off’ promotions (that is not a cold call) – communicated to a specific client or to one group of recipients -‐ could be a rich individual or family and promotion is tailored to their needs.

Communications with retail clients

Requirements for communications with retail clients

• Must be likely to be understood by an average member of the target group • Fair and prominent indication of relevant risks • Important items are not disguised, diminished or obscured • Must include the name of the firm

Comparisons of investments/businesses must be fair

• Specify information sources, key facts and assumptions o Comparisons must be fair – e.g. cant compare returns on bank deposit to equity

Past performance data

Past performance data should:

• Not be the most prominent feature of the communication • Contain a warning that pas performance is not a reliable indicator of future results • Cover at least 5 years immediately preceding consecutive 12 months • Include reference period and source • Contain a currency risk warning • Disclose the effect of charges if based on gross performance

Cold calls/unsolicited calls

Investment firms must not make a cold call unless:

• Existing relationship where recipient envisages the call • It relates to generally marketable packaged product

o We are allowed to sell to retail public, investment itself should be authorised and regulated by the FCA. Not just firms that are regulated, products must also be regulated

• It relates to a controlled activity/service carried out by an authorised firm/ or exempt person o involving readily realisable securities (other than warrants) o these are liquid and readily tradable

Definition of packaged product (CLIPS)

• Collective investment schemes (regulated) • Life policies

• Investment trust savings scheme – not collective investment because it is closed ended, finite number of shares. Like a company with shares trading on the market although all it does is own shares or stakes in other products.

o ITSS (savings scheme) You invest a regular sum of money with provider each month who n turn puts money into investment trust

o Investment directly into Investment trust is not a packaged product • Personal pensions • Stakeholder pensions

o Personal and stakeholder are private pensions. Stakeholder pensions have lower costs

Non-‐written financial promotions

A firm must not initiate a non-‐written financial promotion unless the persons communicating it:

• Does so at an appropriate time of day (for recipient) (must justify appropriate for specific person

• Identifies himself and the firm at the outset and makes the purpose of the communication clear

• Terminates the communication at any time if requested to do so • If signed up for communication; A contact point must be given, so that a future meeting if

arranged can be cancelled.

Investment adviser charging/remuneration

New rules since Jan. 2013 prevents firms making personal recommendations from earning commission set by product provider

Applies to retail investment products (broader than packaged product)

• Firms offering such service now charge for the advice they provide • Charges must be disclosed in writing in good time before advice given using clear and plain

language • Clients have the option of paying the charge upfront or may have it deducted from their

investment • Advisors can no longer receive commission from fund managers

Issues:

• Transparency • Conflict of Interest

Independent advice and restricted investment advice

Independent advice – you must cover all suitable retail investment products, relevant to the client base from relevant providers

• The RDR introduced a new definition of independent advice – which consider all suitable retail investment products

Restricted advice

• Advice which is not independent is described as restricted • Firms must disclose the nature of the restrictions (e.g. limited number of product providers

or specific types of product) to the client

Advising on packaged product

Advisers can choose to:

• Advise on the whole of the market (independent financial advisor) • Advise on limited product range (restricted) • Advise on a single providers products -‐ Appointed representative (exempt from

authorisation)

Key Feature Document must be given to a retail client when providing a recommendation on a packaged product including:

• Details on nature and complexity of the product • Complaints handling procedure • Compensations schemes (if provider goes bust) • Cancellation rights (if client invests but changes their mind)

Suitability and suitability reports

• For all Retail and professional clients: • Applies to personal recommendations and firms managing investments • Reasonable steps must be taken to ensure suitability • In order to do this firms must obtain necessary information regarding the clients:

o Relevant knowledge and experience o Financial situation o Investment objectives

• Retail clients must be sent a suitability report if recommendation related to an investment in a packaged product.

Appropriateness obligations

For all Retail and professional clients:

For investment services other than managing investments and personal recommendations (essentially execution only) – no advised service

• No need to assess appropriateness in relation to noncomplex financial instruments • Firms to assess appropriateness based on the clients relevant knowledge/experience

• If the product/service is not considered appropriate you must warn client • Where there is insufficient information to assess appropriateness the firm must notify the

client that we cannot do appropriateness check. It’s a firm’s discretion whether or not they execute order.

Best Execution

Applies to retail and professional clients

• When executing order a firm must take all reasonable steps to obtain the best possible results for its clients taking into account the execution factors

• A firm will satisfy this rule by executing a client order in accordance with the specific instructions of the client.

Churning and switching

Dealing with unjustified frequency/overtrading

Maybe due to racking up commissions

Firm should be acting in firms best interest

• Churning – relates to investments in general (switching between securities/assets) • Switching – if managing portfolio of packaged products (switching between funds)

Order Execution Policy

Clients must have prior consent to execution policy

For each class of financial instrument policy should include

• Information on different execution venues and • Factors affecting the choice of venue

For retail clients, the following information must be given in advance

• The relative importance of the execution factors • A list of execution venues • Warning that specific instructions may prevent firm form following its policy to obtain the

best possible results

Clients Order Handling

Retail and professional clients

• Firms must implement procedures and arrangement which provide for the prompt fair execution of client orders

• Comparable orders to be executed in accordance with the time of receipt by the firm

Aggregation and Allocation of Orders

• Could potentially aggregate orders as long as you believe it will not disadvantage either or clients and you disclose to clients that you will do this and that you have proper allocation policy (our systems and 3rd party systems clearly know about the allocations)

Inducements

A firm must act honestly, fairly and in best interest of their clients

Any fee commission or non monetary benefit paid to or provided by a 3rd party must be designed to enhance the quality of service to the client

A firm must disclose too the client any fees commissions or nonmonetary benefits in summary form.

Use of Dealing commission (Unbundling)

• Fund manager passes business to broker who they pay commission to execute the order • In return the broker executes and provides research + other goodies (subscription to

Bloomberg, invite analysts to training and education conference) • Problem is that fund managers customer is paying the commissions. Anything that

commission buys should give a benefit to the customer. • Rules now say that in return for payment of commission, no other goodies are acceptable.

Commission can only pay for execution of trades and research • Unbundle packages of returns form commission to make more transparent what customer is

paying for.

An investment manager must not execute customer orders through a broker and pass on charges to client unless the manage has reasonable ground to be satisfies that the goods services purchased with commission:

• Relate to the execution of trades • Comprise the provision of research • Will assist the manager in providing services to its customers • Do not impair compliance with the duty to act in clients best interest

Conflicts of Interest

Firms must identify conflicts of interest between

• The firms and its clients • One client and another

Maintain effective arrangements to manage conflicts

If the arrangements are not sufficient, and cannot manage conflict must disclose the nature of conflicts to firms and clients

Provide retail clients with a copy or summary of policy

Keep record of any conflicts

Conflicts of Interest Policy

The conflicts of interest’s policy must:

Set out the circumstances which gives rise to a conflict

State the procedure for managing conflicts, which could include:

• Information barriers such as ‘Chinese walls’ -‐ prevents information’s from following from the private (M+A advisory) to the public (advisors, analysts).

o Must prevent information from flowing between these two groups • Remuneration structures -‐ Avoid pay structures that create conflicts – if advisors paid by

commission they may not be working in best interest of clients • Independence -‐ analysts are independent to the private side. Stop one side from influencing

decision or research of the other (pressuring) • Segregation of duties – having a senior manager in charge of both public and private would

be bad. Need to segregate those duties

Investment research

Apply to investment research which is intended to be disseminated to clients/public

Covers written or oral material

Firms arrangements must manage conflicts of interest and cover

• No personal or firm transactions in unpublished research until clients have had reasonable opportunity to act.

• No personal transactions contrary to their current recommendation • No promises of favourable research to firm subject of research or will always have a conflict • No editorial control for the subject of the research

If significant shareholder of company we wirte share on, then we cannot get around conflict. In such cases:

• Disclose all relationships and circumstances which may impair objectivity of recommendation

Personal Account Dealing – requirements

Firms must establish implement and maintain adequate arrangements to:

• Prevent employees engaging in market abuse (insider dealings and related offenses) • Ensure all relevant persons are aware of restrictions

• Ensure any deals are notified promptly to the firm: post trade notification • Ensure adequate transactions record are kept:

Exceptions: discretionary fund management and nits in collective investment schemes (one information in one security held in fund (which generally has minimum of 16 securities)

Cancellation Rights

Life policies and pensions (stakeholder or personal) – you have 30 days to cancel without being charged any fees or commissions

Other products -‐ 14 days

• Consumer must be informed of a right to cancel • Cancellation date is the date of dispatch

Record Keeping

General rule

• MiFID – 5 years • Non-‐MiFID-‐ 3 Years

Records relating to pensions and life policies must be kept for 5 years.

Those relating to pension transfers, pension opt-‐outs or a free standing AVC must be kept indefinitely.

Record keeping re. financial promotions relating to life policies and pension must be kept for 6 years.

Reporting requirements

Occasional -‐ If executing order for client we must provide (occasional) reporting

Retail and professional clients

Retail clients to be sent an order confirmation by T+1

• Except when managing investments

Periodic – applies to investment managers

• Must provide periodic statements that gives information on content, value and performance of fund at regular periodic individual

• Default is every 6 months for normal securities (shares, bonds) • 3 months on request • If provide clients with order confirmations, the you only need to send report eervy 12

months • If portfolio is leveraged (or through derivatives) can create a lot of volatility in value of fund.

Because of this extreme volatility must report back to client on monthly basis

Holding of Client assets and client money

Make adequate arrangement to safeguard client’s ownership rights in event of:

• Insolvency of a firm – make sure that clients assets and money is separate from firms assets and money