IFRS 17 Insurance ContractsBreakfast Briefing Series Launch event30 May 2017

2 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Agenda

.

Agenda Items Speaker

Introduction Eimear McCarthy

Scope of IFRS 17 Maaz Mushir

Measurement Maaz Mushir

Presentation and disclosures Carla Dunne

Transition Carla Dunne

IFRS 4 and IFRS 9 considerations Carla Dunne

Programme Delivery David Walsh

Closing remarks Ciara Regan

Introduction

4 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Meet our team

Welcome and Introduction

Eimear McCarthyPartner - Audit and AssuranceE: [email protected]: +353 1 417 2685

Donal LehanePartner – ConsultingE: [email protected]: +353 1 417 2807

David WalshManager – ConsultingE: [email protected]: +353 1 417 3943

Carla DunneManager - Audit and AssuranceE: [email protected]: +353 (0) 1 417 3863

Ciara ReganPartner - Audit and AssuranceE: [email protected]: +353 1 407 4856

Angela McNallyDirector - Audit and AssuranceE: [email protected]: +353 1 417 2279

Maaz MushirManager - Audit and AssuranceE: [email protected]: +353 1 417 2234

Actuarial

Accounting Processes, People and Technology

5 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

1999

Welcome and Introduction

Baby One More Time!

6 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

IASB’s insurance contracts project

25 Oct 2013Comment deadline

2014 and H1 2016Board re-deliberations

16 Nov 2016Approval of post-field test staff recommendations

April 1999

Project commenced

12 Sep 2016IFRS 9 “decoupling” – Deferral possible for some insurers to 1/1/2021

20 Jun 2013

ED Issued

16 Feb 2016IFRS 17 deliberations complete, balloting begins

23 Sep 2016Completion of field testing

18 May 2017Publication date for IFRS 17

1 Jan 2020 *Comparatives and IAS 8 disclosures – Transition date IFRS 17 & IFRS 9

1 Jan 2021Effective date IFRS 17 and IFRS 9 (deferral approach)

1 Jan 2018Effective date IFRS 9 (full application or overlay approach)

* Illustrative for entities with 31 December year-end

7 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Key objectives of IFRS 17

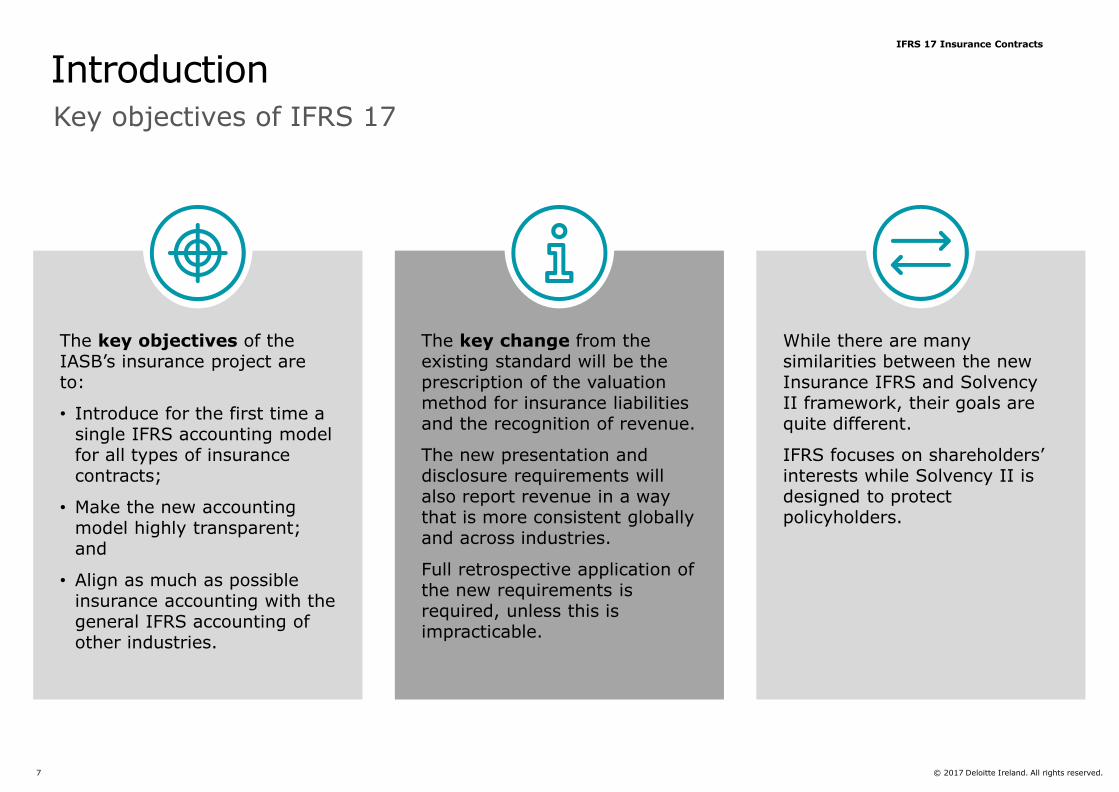

Introduction

The key objectives of the IASB’s insurance project are to:

• Introduce for the first time a single IFRS accounting model for all types of insurance contracts;

• Make the new accounting model highly transparent; and

• Align as much as possible insurance accounting with the general IFRS accounting of other industries.

The key change from the existing standard will be the prescription of the valuation method for insurance liabilities and the recognition of revenue.

The new presentation and disclosure requirements will also report revenue in a way that is more consistent globally and across industries.

Full retrospective application of the new requirements is required, unless this is impracticable.

While there are many similarities between the new Insurance IFRS and Solvency II framework, their goals are quite different.

IFRS focuses on shareholders’ interests while Solvency II is designed to protect policyholders.

8 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Solvency II vs IFRS 17 Balance Sheet

Assets

Best estimate

liability

(“BEL”)

Risk

Adjustment

(“RA”)

Contractual

Services

Margin

(“CSM”)

Assets

BEL

Risk Margin

Other liabilities

Subordinated

liabilities

Excess of assets

over liabilities

Callable capital

instruments Goodwill

Changes in cash flows

related to past & current

services

Income statement

(underwriting result)

Income statement

(investment result)

Other comprehensive

income (“OCI”)

Release of CSM

Release of RA related to

current period

Interest on Insurance

liability

Changes in discount rates

Technical

provisions

Basic Own

Funds

Ancillary Own

Funds

Shareholder

equity

Solvency II IFRS 17

Typical balance sheet Typical balance sheet Income statement

Other liabilities

9 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Fact sheet

OneOne accounting model for all insurance

contracts in all IFRS jurisdictions.

450listed insurers using IFRS Standards

$13 trilliontotal assets of those listed insurers

Betterinformation about profitability

2021mandatory effective date of the new Standard

3.5years for companies to implement the new requirements

900meetings, roundtables and discussion forums

Moreuseful and transparent information

600comment letters

❷Who is affected?

❶ IFRS 17 Insurance Contracts

❸When?

❹What changes?

❺ How was industry feedback collated?

Scope of IFRS 17

11 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

What has improved under IFRS 17?

1Valuation of technical provisions

• Use of current assumptions.

• Consideration of time value of money.

• Use of consistent discount rates.

2Profitability

• Consistent recognition of profit about current and future profitability.

• Profit will be earned in a consistent manner as insurance services are provided to insurance clients.

• Reporting of onerous contracts.

3Comparability among companies

IFRS 17 increases comparability between insurance companies in the same jurisdiction or across different jurisdictions.

4Comparability between insurance contracts

IFRS 17 increases comparability between insurance companies issued by the same company or companies within a group. Several multi nationals consolidate their subsidiaries using non-uniform accounting policies.

5Comparability among industries

The principles of revenue and profit recognition under IFRS 17 make it consistent with other industries.

12 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Scope of IFRS 17

IFRS 17 will apply to a range of different contracts, which fall under the following categories:

• Insurance and reinsurance contracts issued;

• Reinsurance contracts that an entity holds (“ceded reinsurance”); and

• An investment contract with a discretionary participation feature (“DPF”) that it issues, provided that the entity also issues insurance contracts

Remaining contracts which are typically issued by insurance companies are those which comprise investment components, normally referred to as investment contracts. These are financial instruments in substance and thus are accounted for in accordance with IFRS 9.

Measurement

14 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Three approaches to the measurement of insurance contracts

Premium Allocation Approach

• Short-term general insurance

• Short-term life and certain group contracts

Building Block Approach

Variable Fee Approach

• Long-term business• Whole life insurance• Term assurances• Protection business• Annuity Contracts• Reinsurance written• Certain general insurance

contracts

• Unit-linked contracts,• Variable annuities and

equity index-linked contracts• Continental European 90/10

contract• UK with profits contracts• Unitised with profits

15 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Building Blocks Approach (BBA)

Principles

• Measurement model uses a “building block” approach

• Measurement objective is to quantify the notion of the insurer’s “fulfilment of obligations under the contract”

• Measurement is current –assumptions must not be “locked-in”, except the discount rate used to calculate CSM

• Discount rate can be developed from market interest rates using either a “top down” or “bottom up” approach

• Discount rates based on market interest rates whose characteristics match those of the liability (currency, duration, liquidity)

• Contractual service margin (CSM) eliminates the recognition of any future accounting profit at inception

Obligation to provide service, measured at inception as the expected contract profit.

Compensation for uncertainty for certain liability cash flows. Similar to Risk Margin concept in Solvency II.

Use a market discount rate that considers the currency, timing and liquidity of liability cashflows.

Expected cash flows from premiums and claims and benefits.

Block 1: Expected Future Cash

Flows (unbiased probability-

weighted mean)

Block 4:Contractual Service

Margin

Block 3:Risk Adjustment

‘Fulfilment cash flows’

Total IFRS Insurance Liability

Block 2:Time value of money

16 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Building Blocks Approach (BBA)

Principles

• Measurement model uses a “building block” approach

• Measurement objective is to quantify the notion of the insurer’s “fulfilment of obligations under the contract”

• Measurement is current –assumptions must not be “locked-in”, except the discount rate used to calculate CSM

• Discount rate can be developed from market interest rates using either a “top down” or “bottom up” approach

• Discount rates based on market interest rates whose characteristics match those of the liability (currency, duration, liquidity)

• Contractual service margin (CSM) eliminates the recognition of any future accounting profit at inception

Obligation to provide service, measured at inception as the expected contract profit.

Compensation for uncertainty for certain liability cash flows. Similar to Risk Margin concept in Solvency II.

Use a market discount rate that considers the currency, timing and liquidity of liability cashflows.

Expected cash flows from premiums and claims and benefits.

Block 1: Expected Future Cash

Flows (unbiased probability-

weighted mean)

Block 4:Contractual Service

Margin

Block 3:Risk Adjustment

‘Fulfilment cash flows’

Total IFRS Insurance Liability

Block 2:Time value of money

How it works Read the overview

Forced

Hedging

0

1

Allocation of

share class

specific

expenses

0

2

Hedging

Ratio

0

3

Class

Specific

Transactions

0

4

Rounding of

shareholder

transactions

0

5Divergence

from

Benchmark

0

7

Design of

performance

fee

methodology

0

6

The CSM represents the most fundamental change in the measurement of insurance contract liability from the current accounting and solvency standards.

If fulfillment cash flows <0, CSM = –(Block 1 + Block 2 + Block 3).

If fulfillment cash flows >0, CSM = 0

The level of aggregation (unit of account) applied in the calculation of CSM is going to be a key challenge for insurers in the implementation of the standard.

17 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Recognition of changes in estimates and assumptions

Subsequent measurement under BBA

Block 1: Expected Future Cash

Flows (unbiased probability-

weighted mean)

Block 4:Contractual Service

Margin

Block 3:Risk Adjustment

‘Fulfilment cash flows’

Total IFRS Insurance Liability

Block 2:Time value of money

• CSM is adjusted by changes in estimates and is allocated to profit or loss on basis of passage of time.

• For some contracts, changes in estimate include entity share of policyholder’s assets.

In each reporting period, an entity re-measures the fulfilment cash flows using updated assumptions about cash flows, discount rate and risk.

18 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

There are four broad categories to “adjust” SII contract value to that defined under IFRS 17. However, the devil is always in the details.

An extremely simplistic illustration of the differences in SII and IFRS 17 Insurance Liabilities

SolvencyII

TechnicalProvisions

SIIcontract

boundaries

RiskMargin

DiscountRates

CSM IFRS 17InsuranceLiabilities

Best Estimate Liabilities

Risk margin

PV of Fulfilment Cashflows

Risk adjustment

Contractual Service margin

19 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Evolution of IFRS 17 vs Local GAAP profits over time (measured under BBA)

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

12000

1 3 5 7 9 11 13 15 17 19

Term Assurance

Local GAAP IFRS 17

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1 2 3 4 5 6 7 8 9 1011121314151617181920

Annuities

Local GAAP IFRS 17

20 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Evolution of IFRS 17 vs Local GAAP profits over time (measured under VFA)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

21 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Premium Allocation Approach

PAA is the option to use premium as proxy for the valuation of insurance contracts for short term incepted

but unexpired risks

Discounted probability weighted average of expected

future cash flows

Risk Adjustment

Premium Allocation Approach

(PAA)

Onerous

Discounted probability weighted

average of expected

future cash flows

Risk Adjustment

CSM

Incurred Liability Liability prior to date when claims are incurred

Fulfilment CF value for claims reserves

Fulfilment CF value for unexpired and unincepted risks

Minimum liability for unincepted contracts

or unexpired coverage.

AND

Premium Allocation Approach

(PAA)OR OR

Building Blocks Approach/ General Model

Presentation and disclosures

23 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Significant changes to the balance sheet

New IFRS balance sheet

1. Liabilities under insurance contracts(including unallocated surplus) willchange with the underlying valuation basis

2. Reinsurer’s share of liabilities willchange in line with underlying inwardsvaluation basis

3. Deferred acquisition costs will no longerexist

4. Other assets / payables and otherfinancial liabilities will no longer includeinwards and outwards future premiums

5. Intangible assets that relate to futureprofits will be deferred as part of the CSM

6. Retained earnings will differ due to:

Retrospective application of Standardsat inception

Different emergence of profit

KPIs will change as a result

24 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Fundamentally different

New IFRS Income Statement

KPIs will change as a result

1. Gross written premiums - replaced byInsurance Revenue comprising of:

Release of CSM

+/- Change in Risk Adjustment

+ Expected net cash flows

2. Claims and change in insurance liabilitieswill include actual net cash outflow,fundamentally changing to reflect themeasurement basis

3. Acquisition costs:

Attributable expenses included in BEL

Non-attributable expenses recognised inincome statement immediately

4. Finance costs:

Unwind of initial discount – a cost in eachperiod based on discount rates at inception

New discount rate – option to take theimpact of changes through profit/loss orother comprehensive income

25 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Disclosures overview

An entity shall disclose qualitative and quantitative information about:

• The amounts recognised in its financial statements that arise from insurance contracts; (explanation of recognised amounts)

• The significant judgements, and changes in those judgements; and (significant judgements)

• The nature and extent of the risks that arise from contracts within the scope of the Standard. (risks)

There are also extensive disclosures relating to transition.

Transition

27 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Overview

IFRS 17 – Transition

Three possible approaches to be applied

The retrospective approach should be applied to groups of insurance contracts, unless it is impracticableor if groups at inception of contracts in force on transition cannot be identified.

An entity is then permitted to choose between the modified retrospective approachand the fair value approach.

Where impracticable to apply the modified retrospective approach, a fair value approach is applied from the date of transition.

Key definitions in transition

Impracticable: Applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so. (IAS 8.5)

Fair value: The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. (IFRS 13.A)

28 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Illustration (effective date: 1/1/2021)

IFRS 17 – Transition

The objective of the modified retrospective approach is to approximate full restatement

The use should be only to the extent the entity does not have reasonable and supportable information to restate

Retrospective approach

Modified retrospective approach

Fair value approach

BS3BS2BS11

/1

/2

02

0

1/

1/

20

21

(eff

ecti

ve d

ate

)

31

/1

2/

20

21

IS1 IS2

Maximum Comparative Periods

Each bar represents all of the groups of contracts issued in those years and part of the different portfolios

BS = Balance SheetIS = Statement of Comprehensive Income

- 1 yr

- 2 yr

- 3 yr

- 4 yr

- 5 yr

- 6 yr

- 7 yr

- 12 yr

- 13 yr

- 14 yr

IMPRACTICABILITY ARISES

IMPRACTICABILITY ARISES

- 11 yr

- 8 yr

- 9 yr

- 10 yr

IFRS 4 and IFRS 9 considerations

30 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Key Principles

IFRS 9

AC FVTOCIFVTPL/

FVTOCI Option for certain equity instruments

Within the scope of the impairment model

Outside the scope of the

impairment model

Financial assets in the scope of IFRS 9Loan

commit-ments

(unless @ FVTPL)

Financial guarantees

(unless @ FVTPL)

Lease receivables

Contract assets

(IFRS 15)

Subsequent measurement …

1. Classification and Measurement

2. Impairment

3. Hedge Accounting

31 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Overview

IFRS 4 – Interaction with IFRS 9

1. Overlay Approach

• apply IFRS 9, but adjust profit or loss to remove volatility for designated assets arising from the accounting mismatches

• available to all insurers

• effective when an insurer first applies IFRS 9

• apply IAS 39 in the financial statements

• available to insurers whose activities are predominantly connected with insurance

• eligible at reporting entity level

• deferral option to 2021

2. The Temporary Exemption

IFRS 9 Financial Instruments is effective from 1 January 2018. As such, IFRS 17 will have a later implementation date than that of IFRS 9 which may cause:• additional accounting mismatches; and • volatility in profit or loss that may arise in this ‘gap’ period.

As a result, the IASB amended IFRS 4 to introduce two options for insurers:

32 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

The Overlay approach

IFRS 4 – Interaction with IFRS 9

• IFRS 9 is applied in full.

• Reclassify between P&L and OCI the difference between amounts reported applying IFRS 9 and amounts that would have been reported applying IAS 39.

• For financial assets:

measured at FVTPL under IFRS 9 but would not have been measured at FVTPL in their entirety under IAS 39; and

that relate to contracts within the scope of IFRS 4.

Statement of Comprehensive Income

Insurance contracts revenue X

Incurred claims and expenses (X)

Operating result X

Investment income ‘IFRS 9’ X

Interest on insurance liability (X)

Overlay approach-adjustment (X)

Investment result X

Profit / (Loss) X

Overlay approach-adjustment X

Effect of discount rate changes on insurance liability

(X)

Other comprehensive income X

Total comprehensive income X

33 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

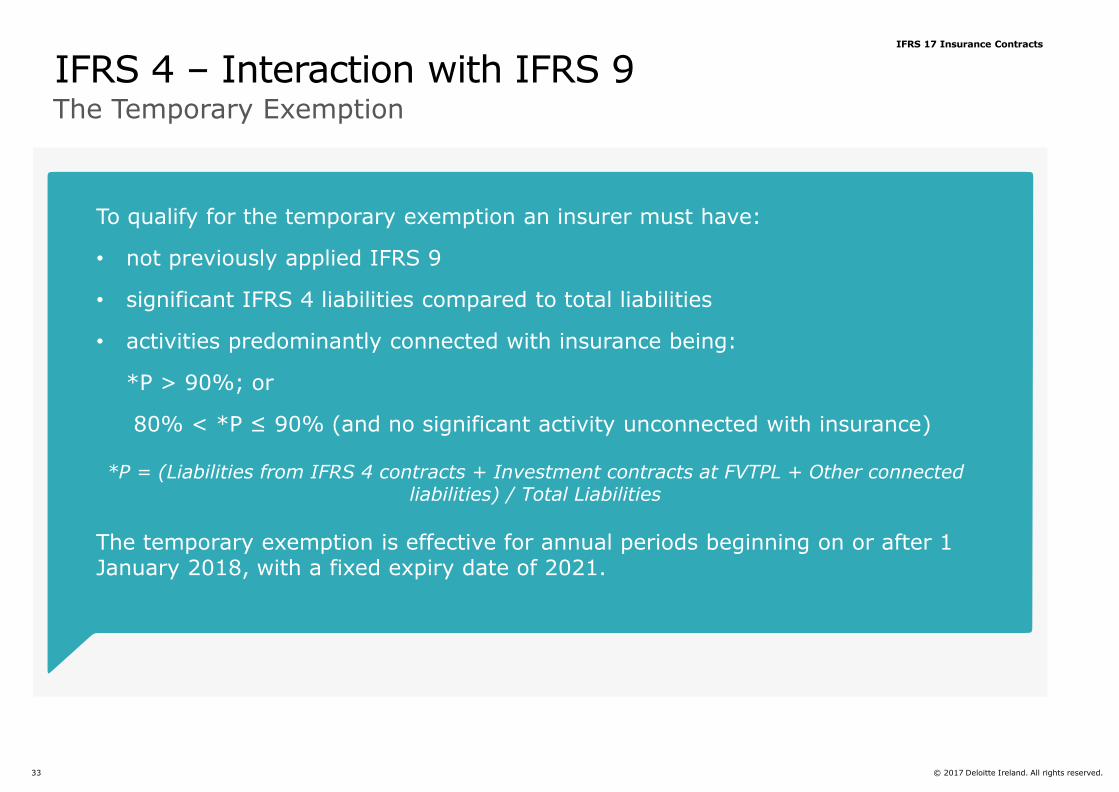

The Temporary Exemption

IFRS 4 – Interaction with IFRS 9

To qualify for the temporary exemption an insurer must have:

• not previously applied IFRS 9

• significant IFRS 4 liabilities compared to total liabilities

• activities predominantly connected with insurance being:

*P > 90%; or

80% < *P ≤ 90% (and no significant activity unconnected with insurance)

*P = (Liabilities from IFRS 4 contracts + Investment contracts at FVTPL + Other connected liabilities) / Total Liabilities

The temporary exemption is effective for annual periods beginning on or after 1 January 2018, with a fixed expiry date of 2021.

34 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Key considerations

IFRS 4 – Interaction with IFRS 9

IFRS reporter

• Do you qualify for the temporary exemption? Judgement involved. Need to consider both qualitative and quantitative factors.

• Are you are planning to early adopt IFRS 17 before 1 January 2021? If so, you must also apply IFRS 9 Financial Instruments and IFRS 15 Revenue from Contracts with Customers.

IGAAP reporter with IFRS group reporting

• Have you considered the implications on your group reporting requirements? Need to consider the costs and complexities of preparing financial information under both IAS 39 and IFRS 9.

IGAAP reporter with no IFRS group reporting

• What is the timing for FRS 102 to change?

Programme Delivery

36 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

IFRS 17 Programme Delivery

Project Planning

• Resource Planning• Budget Planning• Workstream identification• Programme structure• Programme governance• Implementation Roadmap

IT Solutions

• Data Requirements• System Requirements• Vendor Benchmarking• System Build V Buy analysis

Operating Model

• Day 2 readiness – Processes, people and technology• Management Information (MI) • Month End• KPIs• Internal Controls – Transition & Post Go Live Controls

Communications• Internal Comms• Investor Relation Comms• Treasury Comms

Kicking off your IFRS 17 project

Closing remarks

38 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

What should you do next?

Understand the impact of IFRS 17 and IFRS 9 changes on your business

Understand the impact on your profit profiles, accounts and KPIs

Early planning, resources and training

Complete a business case and secure budget

Educate senior management and the market

Future-proof in-flight initiatives

Start early, start small and keep it simple

39 © 2017 Deloitte Ireland. All rights reserved.

IFRS 17 Insurance Contracts

Deloitte Next Steps

JULY 11 AUGUST 2 SEPTEMBER 5

Deep dive of the new

Insurance Contracts

Standard, IFRS 17

Understanding the

financial and practical

impacts for reserving

Understanding the

impact across the

entire business: from

IT to actuarial and

finance

Series of upcoming breakfast briefings:

• Launch of new series of “on demand webcasts” and eminence papers on topical issues that will follow the insurers’ IFRS 17 journey to implementation

• Publication of an IFRS 17 practical guide

• Deloitte interpretative guidance on IFRS 17 will be released continuously on our online accounting research tool IASPlus.com

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its

network of member firms, each of which is a legally separate and independent entity. Please see

www.deloitte.com/ie/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its

member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance to public and private clients

spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings

world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex

business challenges. With over 210,000 professionals globally, Deloitte is committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global Services Limited, Deloitte Global Services Holdings Limited, the Deloitte Touche Tohmatsu Verein, any of their member firms, or any of the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your finances or your business. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2017 Deloitte & Touche. All rights reserved