ICRA LIMITED P a g e | 1

Financial Sector Ratings Contacts: Karthik Srinivasan +91 22 3047 0028 [email protected]

Vibha Batra +91 124 4545 302

[email protected] Viral Shah +91 22 3047 0035

[email protected] Harsh Vardhan Babel +91 22 3047 0040

ICRA RESEARCH SERVICES

ICRA RATING FEATURE

INDIAN BROKERAGE INDUSTRY

“Headwinds tailing off for the brokerage houses; structural challenges remain”

March 2013

ICRA LIMITED P a g e | 2

Executive Summary

Buoyed by the global flows into the Indian market in the later part of CY2012, we witnessed strong traction in index movement both on the BSE and NSE. However the

9MFY12-13 continued to be weak for the Indian equity capital markets. In ICRA’s estimation, the brokerage revenue pool has remained flat at ~Rs 105 billion for FY12-13

when compared with FY11-12 despite the strong growth in Options volumes as the Cash volumes and Futures continued to slide and were lower even in absolute number

during this period as compared to the previous fiscal.

In 9M FY12-13, while the burden of collapsed retail participation has completely weighed down the retail broking operations, the combination of regulatory changes such

as capping of commission rates for domestic mutual funds as well as increasing and seemingly irreversible penetration of DMAs have been a heavy drag on its institutional

broking piece. In ICRA’s view, were these trends to continue, they could test the resilience of the industry and trigger significant structural changes especially in the

institutional broking segment.

Capital market ancillary businesses too continued to remain moribund. Slow demand for margin funding also impacted interest income while increasing penetration of high

frequency trading has led many medium to small sized broking houses to close arbitrage trading operations. While a few relatively large ticket public issuances kept

brokerage houses interested, fee income from the advisory piece has remained lacklustre. The difficult economic conditions ensured that revenues from the investment

banking operations for companies were a casualty. Fewer public issuances meant that distribution income remained weak, though was propped up by retail debt

issuances. While PMS operations continued to provide steady run rate for some large brokerage houses, at industry level equity PMS AUMs have only declined.

A brightening outlook for the commodities and currencies broking segment stands out against the dark tones of the beleaguered equity broking industry. While for the

commodities segment, traded turnover declined nominally, ICRA has observed a more broad based increase in market participation and robust increase in customer

addition aided by increased investor awareness. The currencies segment on the other hand too continued to gain traction.

There are reasons for optimism as the dispiriting mood which pervaded the industry is now slowly giving way to newfound hope and optimism. Equity cash volumes have

shown signs of improvement in Q3FY12-13 and beyond. Broader based retail participation is showing the early signs of returning to the markets. The cash volumes

recorded for the month of January 2013 were the highest since February 2012. Equity options, largely understood to be the forte of the more savvy institutional investors

are attracting a steady trickle of the higher end retail investors. The commodities and currencies segment are emerging as dependable avenues for diversification for

brokers. The government stepping on the gas with regard to reforms initiative and declining interest rate scenario is doing much for improving investor sentiment. The

month of January 2013 saw very strong FII inflows into the country. The disinvestment plans and planned public offerings may provide the much needed boost to

investment banking and distribution operations.

In H1FY12-13, ICRA has observed that total capital market related revenues for select top brokers who account for ~35% market share has remained almost flat in H1FY12-

13 (annualized) when compared to FY11-12. However, costs have declined more sharply by ~7-8% (annualized) over the same period leading to improvement in cost-

INDIAN BROKERAGE INDUSTRY

Headwinds tailing off for brokerage houses; structural challenges remain March 2013

ICRA RESEARCH SERVICES

ICRA LIMITED P a g e | 3

income ratio and other profitability indicators. Early indicators for Q3FY12-13 indicate growth in the quarter – revenue for 9MFY12-13 (annualized) has grown by 3-5%

when compared to FY 11-12 and profitability has improved further.

The Union Budget 2013, amongst other proposals, has reduced Securities Transaction Tax (STT) on equity futures contracts to 0.01% from 0.017%, introduced

commodities transaction tax (CTT) on non-agriculture commodities futures trading and allowed participation of FIIs in the currencies derivative segment. In ICRA’s view,

while these proposals could provide a fillip to equity derivative volumes as well as currency derivative volumes, the imposition of the CTT could impact the gross returns of

the arbitrageurs by 20-30% and consequently significantly impede the growth of the segment at least over the short term. Also, arbitrage activity could return to the

equities segment or move to the currencies segment, which could help growth of these segments.

However, in ICRA’s view the underlying economic picture remains uncertain. In the absence of any strong global economic recovery, this phase of cautious optimism is

largely contingent upon government delivery of the reforms programme. Any let up in execution could mean that this build up of hope could unravel very quickly.

At the same time, ICRA has noted that the industry brokerage revenue pool has been stabilizing. Commodities and currencies have emerged as dependable sources of

diversification and the brokers have re-aligned their business models vigorously to contain costs. Consequently, in ICRA’s view, brokers are better tuned to face the

challenges ahead. ICRA revises its outlook on the sector to “Stable” from “Negative”.

This note covers the financials of 151 entities constituting ~35% of equity broking revenue market share

1 The 15 brokerage houses analyzed in the note are Angel Broking Limited, Bonanza Portfolio Limited, Edelweiss Financial Services Limited, Emkay Global Financial Services Limited,

Geojit BNP Paribas Limited, HDFC Securities Limited, Indiabulls Securities Limited, India Infoline Limited, JM Financial Limited , Kotak Securities Limited, Motilal Oswal Financial Services Limited, Reliance Securities Limited, Sharekhan Limited, Religare Enterprises Limited and Globe Capital Market Limited

ICRA LIMITED P a g e | 4

The report includes an update on the…

I. Equity markets update in 9MFY12-13……………………………………………………………………………………………………………………….…………………………….………………………………………6 a. Trends in cash, futures and options volumes b. Trends in trading activity by investor class c. Trends in transaction size and number on the exchanges d. Trends in trading activity on the BSE and NSE and impact of entry of MCX-SX e. ICRA’s estimation of the equity brokerage revenue pool

II. Commodities markets update in 9MFY12-13………………………………………………………………………………………………………………………….………………..……………………………………11

a. Trends in exchange traded volumes b. Trends in spot exchange activity c. Trends in exchange wise traded volumes market share d. Impact of possible regulatory diktats on the commodities markets e. ICRA’s estimation of the commodities brokerage revenue pool f. Analysis of operating risks in commodities trading

III. Currencies markets update in 9MFY12-13……………………………………………………………………………………………………………..…………….………………………………………………………15

a. Trends in exchange traded volumes b. Trends in exchange wise traded volumes market share c. ICRA’s estimation of the currencies brokerage revenue pool

IV. Other capital markets related businesses……………………………………………………………………………………………………………………….………………………………………………………….…16

a. Key trends investment banking operations and outlook b. Key trends in capital market lending operations c. Key trends in other capital markets businesses d. Key trends in non-capital markets related forays and ICRA’s outlook

V. Key Industry trends in 9MFY12-13………………………………………………………………………………………………………………………………….……………………………………………………………19

a. Key trends to watch out for in the institutional broking space Impact of capping of brokerage commissions for domestic institutional investors Impact of increased penetration of Direct Market Access (DMAa) ICRA’s views on industry consolidation

b. Key trends to watch out for in the retail broking space

Trends in customer addition Other initiatives taken by brokers to re-invigorate activity levels Trends in online trading Trends of options trading

ICRA LIMITED P a g e | 5

VI. Performance update for H1FY12-13 for 15 top brokers ………………………………………………………………………………………………………………………………………….…….………………23 a. Trends in capital markets related revenue b. Trends in operating costs c. Analysis of profitability and profitability linked ratios d. Initial impressions for 9MFY12-13 performance

VII. ICRA’s outlook for the Brokerage Sector for FY13-14……………………………………………………………………………………………………………………………………………………………………24

ICRA LIMITED P a g e | 6

EQUITY MARKETS UPDATE IN 9MFY 12-13

Strong growth in overall market turnover in 9MFY12-13; however cash and futures volumes continue to slide

9MFY12-13 continued to remain challenging for the Indian equity markets. With

the domestic capital markets bound quite tightly with the global markets, the

combination of weak developed markets recovery, slowing growth in emerging

economies and closer to home – persistently high inflation, slowing economy,

weakening public finances, depreciating rupee, slowing exports and deteriorating

current account deficit dampened investor sentiment. In Q3FY12-13 however, a

slew of reforms, proposed legislations and possible bottoming out of economic

cycle buoyed investor outlook and brought some life back into the equity

markets.

The domestic equity brokerage turnover (BSE and NSE combined) registered an

increase of 16% (annualized) in 9MFY12-13 to Rs 309 trillion (Rs 356 trillion in

FY11-12). This strong increase continued to be fueled mainly by equity derivative

volumes with cash volumes declining by 9% (annualized) in 9MFY12-13 when

compared with FY 11-12 while equity derivative volumes grew by 19% over the

same period.

Within the equity derivative segment, futures volumes continued their

downward trend and declined by 13% (annualized) in 9MFY12-13 when

compared to FY 11-12 while options volumes increased by a further 29%

(annualized) over the same period.

In terms of volume composition, cash market trades accounted for 8% of overall

volumes in 9MFY12-13 as compared to 10% in FY 11-12 and 13% in FY10-11.

Were the same trends to continue, cash volumes are likely to decline even in

absolute number in FY12-13 when compared to the already battered volumes of

FY11-12. Similarly, futures volumes constituted ~16% of overall volumes in

9MFY12-13 when compared to 22% for FY 11-12 and 29% for FY 10-11. Again, on

the current trajectory, it looks unlikely for the futures volumes in FY 12-13 to

upstage the FY 11-12 levels in absolute numbers. Options volumes constitute the

remainder 76% of overall volumes in FY12-13. Consequently, equity derivative volumes, led by options volumes have continued their upward surge and now account

for 92% of overall exchange traded volumes in 9MFY12-13 as compared to 90% in FY 11-12 and 87% in FY 10-11.

Chart 1: Common size analysis of equity volumes

Source: ICRA analysis, NSE and BSE website

Chart 2: Common size analysis of equity volumes

Source: ICRA analysis, NSE and BSE website

0%

20%

40%

60%

80%

100%

Q1F

Y09

Q2F

Y09

Q3F

Y09

Q4F

Y09

Q1F

Y10

Q2F

Y10

Q3F

Y10

Q4F

Y10

Q1F

Y11

Q2F

Y11

Q3F

Y11

Q4F

Y11

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Common size analysis of equity volumes

Turnover - Cash Total F&O

ICRA LIMITED P a g e | 7

Within the year, cash volumes as a percentage of overall volumes have largely

remained stable. Cash volumes seen at ~7.4% of overall volumes for Q1FY12-13

improved marginally to 7.6% in Q2FY12-13 and 8% in Q3FY12-13. However,

within specific time frames within the year - last fortnight of September 2012,

early weeks of October 2012 as well as smaller pockets in November 2012, the

cash volumes as a percentage of overall volumes were reported upward of 10%

as markets rallied to efforts of the government to institute the much awaited

reforms.

Within the Options segment, the index option based on NIFTY accounted for

nearly 93% of the total options volume in 9MFY12-13 as compared to 96% for FY

11-12, providing adequate liquidity and further fueling investor appetite.

However in 9MFY12-13, stock options have gathered momentum with traded

volume growth of 81% (annualized) when compared to FY11-12 albeit on a

smaller base. Also, based on anecdotal evidence, ICRA has learnt that penetration of options as an asset class is slowly tricking down to the higher end retail

investors who are increasingly getting comfortable delving into this area. In ICRAs’ view, strong growth of stock options and options segment in general could be an

indicator of increased investor comfort with newer segments within the equity capital markets space and a indicator that the traction in the options trading may

continue.

Average daily volumes (ADV) in 9MFY 12-13 (Rs 1.65 trillion) increased by 15%

when compared to FY 11-12 (~Rs 1.43 trillion). ADV grew at a faster clip in

Q3FY12-13 (Rs. 1.70 trillion) as compared to Q1FY12-13 (Rs 1.59 trillion).

For the month of January 2013, ADV of unprecedented Rs 1.84 trillion was

recorded, which is higher by ~11% when compared to 9MFY11-12. Cash volumes

ADV was strong at ~Rs. 153 billion, higher by ~22% when compared to ADV of Rs

126 billion for 9MFY12-13.

Anecdotal evidence suggests that proprietary trading segment participation

increased in 9MFY12-13 by ~500 bps to ~25-30%, share of institutions segment

has remained stable at ~20-25% while retail contribution has declined to ~45-50%.

Chart 3: Y-o-Y growth – Equity Brokerage Turnover

Source: NSE and BSE website, ICRA analysis

Chart 4: Equity Brokerage Turnover - Yearwise

Source: ICRA analysis

ICRA LIMITED P a g e | 8

Within the institutional segment, contribution of the DII segment over the past 7

quarters remains between 40-50% of FII volumes. However, the nature of trading

has differed significantly. While over this time frame FIIs have been net buyers of

Indian equities to the tune of ~Rs. 1 trillion, the DIIs have been net sellers to the

tune of Rs 500 billion. In the month of January 2013, FIIs have pumped in more than

USD 4 billion into Indian equity markets. For many, this remains a pre-cursor to

capital markets revival.

Dip in number of transactions in the cash segment; increase in number of trades

and trading size for the derivatives segment

In terms of trading activity in the market, the number of trades in the cash segment

declined by ~17% (annualized) while average trade size remained flat when

compared to FY11-12. The average trade size stood at Rs 18,950 in 9MFY12-13 as

compared to Rs. 19,009 in FY11-12. Number of trades reported a decline to 1.12

billion in 9MFY 12-13.

In the derivatives segment at the exchanges, number of contracts continued to increase by ~14% (annualized) in 9MFY12-13 as compared to FY 11-12. Average trade

size also reported a marginal 4% increase to ~Rs. 0.27 million per trade in 9MFY12-13 as compared to Rs 0.26 million per trade in FY 11-12.

Chart 5:Institutional participation in Indian equities

Source: ICRA Analysis, moneycontrol

Chart 6:Total number of trades – cash segment

Source: ICRA Analysis, NSE and BSE website

Chart 7:Total number of trades – derivative segment

Source: ICRA Analysis, NSE and BSE website

ICRA LIMITED P a g e | 9

Industry revenue pool from equity broking remains stagnant at Rs 105 bn; flat when compared to FY 11-12

Gross brokerage yields remained largely stable in 9MFY11-12 when compared to FY 11-12. However, the decline in cash volumes as well as the futures volume at the

expense of options volumes impacted overall gross blended yield which in ICRA’s estimation has declined by ~15-20% when compared to FY 11-12. ICRA has also

noted increasing penetration of proprietary options volumes, which do not have any brokerage revenue potential. However, ICRA has also noted increased delivery

based buying especially in Q3FY11-12, which remain very lucrative from brokerage industry perspective. Consequently, the decline in cash and futures volumes as

well increased proprietary activity in options trading has been offset by increased delivery based buying by clients and increased options trading in general. Hence,

in ICRA’s estimation, the annual brokerage revenue pool remains at Rs 100 - 105 billion, flat when compared to FY 11-12. For the purpose of this estimation, ICRA

has not considered the increase in overall volumes as seen in the month of January 2013.

In ICRA’s view, if the trajectory of cash volumes as well as overall market activity levels as seen in the month of January 2013 were to continue, the brokerage

revenue pool could expand by as much as 15-20% in the near term.

Derivative volumes on the Bombay Stock Exchange (BSE) primarily dependent on incentives doled out and lower transaction fees

In a bid to revive its sagging fortunes, the BSE launched a derivate trading incentive scheme in September 2011. According to Securities and Exchange Board of India

(SEBI) directive, an exchange can run the scheme for six months to bring in liquidity in the underlying instrument. Accordingly, brokers generating the liquidity would

be paid out of the BSE’s own resources. The scheme would be discontinued when

average trading volumes at the exchange during the previous 60 days reaches 1%

of the market capitalization of the underlying.

Predictably, the BSE got a strong response to its market making activities.

Arbitrageurs thrived and proprietary trades got a fillip as incentives doled out and

significantly lower transaction charges made it a compelling case to trade. Volumes

soared in response. ADV have been seen in the range of Rs 250 bn - 350 bn for

9MFY12-13 – almost 20-30% of those seen on the NSE. However, more than 90% of

the trades have been contributed by proprietary trades. Most brokers interviewed

by ICRA have conceded that FIIs have largely remained conspicuously absent.

The jury remains out on whether this points to more sustainable and broad based

participation. While build up in open interest has been strong, bulk of it has been in

the out of the money options which cannot be construed as sustainable market

participation. Out of the money options open interest is again not indicative of

retail participation. Also, whenever the BSE has withdrawn the incentive scheme, volumes have nosedived.

In ICRA’s view, the task is cut out for BSE. While it has the deep pockets to keep the programme running, it can not run an incentive programme, at least in the

current form indefinitely. Before the exchange starts withdrawing or reducing incentives, non-incentive-linked volumes need to rise to meaningful levels. Else, when

market-making activity reduces, spreads could widen to such an extent that genuine traders will find little reason to continue trading.

Chart 8: BSE and NSE Derivative Volumes

Source: ICRA Analysis, NSE and BSE website

ICRA LIMITED P a g e | 10

Entry of MCX-SX could queer the pitch for BSE and NSE

Following the conclusion of the long tussle with SEBI, MCX-SX obtained the license to become a full-fledged bourse. The exchange has been allowed to start trading

in equity, equity derivatives and other asset classes just like its rivals – BSE and NSE. MCX-SX had also started an aggressive campaign to add members in the months

of October – November 2012 and has been successful in adding about 700 members.

While the NSE has strong market leadership in both the cash and futures market trading, BSE has been trying hard to wrest some influence back. The entry of MCX-

SX could queer the pitch for BSE and NSE. MCX has made strong progress as a commodity exchange and boasts of upward of 85% market share. Commodity volumes

on the MCX account for ~35-40% of equity volumes. While MCX-SX could try to woo their commodity broking customers into equity trading through their MCX-SX

platform, ICRA believes that getting commodity customers into the equity fold may not be easy owing to difference in mindsets of these two customer segments.

Consequently, liquidity on the MCX-SX at least in the early life of the exchange may be dependent largely on account of volumes poached from rival exchanges.

While it would be premature to judge, the activity on the initial few days at the MCX-SX has been rather tepid. ICRA believes growing and sustaining the volumes

over the medium term would largely dependent on the newer product introduction as well as strong technological platform innovation.

ICRA LIMITED P a g e | 11

COMMODITIES AND CURRENCIES SEGMENT UPDATE IN 9MFY12-13

COMMODITY MARKET

Commodity prices have seen a decline in recent past, affected by global economic slowdown and slowing growth rate in China, one of the largest consumers of

commodities. However, declining commodity prices were partially offset by a weakening rupee which softened the hard landing for commodities markets in India.

Lower volatility in the bullion market (the largest constituent of commodities market in India) impacted investor interest, thereby leading to lower trading volumes.

Better performance in Equity capital markets in 2012 may have also attracted portfolio reallocation away from commodities. Subsequently the volumes in

commodity markets remained flat in 9MFY12-13 when compared to FY11-12.

Growth in Exchange traded commodity volumes stagnates after seeing healthy growth for last couple of years

Commodities broking turnover, which saw healthy growth in the last few years, peaked in Q2FY12 and the volumes have stagnated since then with an Average Daily

Volume (ADV) of ~ Rs 0.6 trillion. However, 9MFY12-13 saw easing of commodity demand, leading to lower growth in their prices. Bullion which constitutes the

largest turnover volumes within the commodity segment saw returns and volatility in gold and silver reducing compared to previous years. The precious metals

segment, which is the largest contributor to exchange traded volumes (in value) in commodity futures markets, saw a decline on annualized basis of ~ 21% during

9MFY12-13. Both, gold and silver saw decline in volumes traded (in quantity) by 27 – 28% on an annualized basis in 9MFY12-13.

Chart 9: Commodity Market Turnover – Quarter wise Chart 10: Gold & Silver – Quarterly Trading Volume

Source: FMC website, NCDEX and MCX website, ICRA Analysis Source: FMC website, ICRA Analysis

0.1 0.2

0.1 0.2 0.2

0.2 0.3 0.3 0.3

0.3 0.4

0.49 0.51

0.70

0.57 0.59 0.55

0.60 0.56

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

-

10

20

30

40

50

60

Q1

FY0

9

Q2

FY0

9

Q3

FY0

9

Q4

FY0

9

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Av

era

ge

Da

ily T

urn

ov

er (

Rs

Tri

llio

n)

To

tal M

ark

et

Tu

rno

ve

r (R

s T

rilli

on

)

Commodities Brokerage Turnover - Quarterwise

Total Market Turnover Average Daily turnover (RHS)

-

1

2

3

4

5

6

7

-

50

100

150

200

250

300

350

(in

'00

0 T

on

ne

s)

(in

'00

0 T

on

ne

s)

Quarterly Trading Volume

Silver Gold (RHS)

ICRA LIMITED P a g e | 12

CY2012 also saw better performance from equity capital markets with the Nifty

gaining ~ 27.7% in 2012 compared to a decline of ~ 24.9% in 2011. So the

performance difference in commodity market and equity market has reduced.

Consequently, exchange traded commodity volumes (by value), which had grown

by ~49% to Rs 182 trillion in FY11-12 (ADV of ~Rs 0.59 trillion) declined ~ 5% on

an annualized basis during 9MFY12-13 to Rs. 130 trillion (ADV of Rs 0.57 trillion).

Precious metals, non-precious metal products, agricultural commodities and

energy products in aggregate contribute to more than 99% of the overall

exchange traded commodity volumes (by value). Amongst these asset classes,

during 9MFY12-13, precious metals (gold, silver) contributed to ~ 46% overall

value traded followed by energy products which contribute to ~ 22% of value

traded in 9MFY12-13 (56% and 16% respectively in FY 2011-12). Within precious

metals, trading in silver contributed to 53% of the overall value traded with gold

contributing to the remaining 47% in 9MFY12-13 (57% for silver and 43% for gold

in FY 2011-12). Non precious metal products contribute to 19% of overall value

traded in 9MFY12-13 (16% in FY11-12) and agriculture products contribute to

13% of the overall value traded in 9MFY12-13 (12% in FY11-12).

For 9MFY 12-13, commodity ADV is observed at ~35-40% of equity volumes.

However since currently, commodity trading on the exchanges does not allow

‘options’ trades, in value terms commodity futures market volumes are higher by

more than 200% when compared to futures volumes on equity markets.

Spot market activity beginning to take shape in commodity segment

The commodity spot exchange market has started picking up volumes in the last

2 years, albeit a very small fraction of the commodity futures market volumes.

The ADV at National Spot Exchange Limited (NSEL), the dominant exchange in this

segment, has been ~ Rs 9.50 billion in 9MFY12-13. E-series products constitute

the majority volumes in the spot market, which functions just like cash segment

in equities, but offering commodities like gold, silver and copper in the demat

form in smaller denominations. NSDL and CDSL act as the depository for holding

commodity units in the electronic form. Investors can take physical delivery of

accumulated demat units at multiple centers. The spot exchange is widely used

by arbitragers to combine spot and futures transactions on commodities.

Chart 11: Commodity Turnover – Asset Class wise

Source: FMC website, NCDEX and MCX website, ICRA Analysis

Chart 12: National Spot Exchange Volumes – Quarter wise

Source: NSEL website, ICRA Analysis

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY08-09 FY09-10 FY10-11 FY11-12 9MFY13

Ave

rage

Dai

ly T

urn

ove

r ( R

s tr

illio

n)

Turo

ver

Commodity Brokerage Turnover - Yearwise

Agricultural Commodities Bullion Metals

Energy Others Average daily turnover

-

2

4

6

8

10

12

14

-

200

400

600

800

1,000

1,200

Rs

in b

illio

n

Rs

in b

illio

n

National Spot Exchange Volumes

Total Turnover Average Daily Volume (RHS)

ICRA LIMITED P a g e | 13

MCX remains the market leader with more than 85% market share despite decline in bullion turnover

With the grant of recognition to the Universal Commodity Exchange, Navi

Mumbai the total number of Recognized Commodity Exchanges has become 22

(16 Regional and 6 National Exchanges). The five National Commodity Exchanges

contributed 99.76 % to the total value of trade in the Commodity Futures Market

in Q2FY12-13 as per FMC.

These are MCX, Mumbai (85.63 %), NCDEX, Mumbai (11.56 %), ACE Derivatives

and Commodity Exchange Ltd., Mumbai (1.35%), NMCE, Ahmedabad (0.73 %)

and ICEX, Mumbai (0.49 %). As compared to the equities broking segment which

only has two major exchanges with a third national exchange just started, the

commodities segment, depending on the asset class has multiple national

exchanges. MCX remains the market leader with most of the other exchanges

focusing on agricultural commodities. Many of the regional commodity

exchanges specialize in trading of few specific agri products based on local

markets. However, more number of national commodity exchanges will provide

better competition.

There is interest shown from large institutions in the commodity market, as they

are setting up new commodity exchanges based on the potential seen in the commodity markets. As compared to global standards, where generally commodity

markets are bigger than equity markets by many folds, the Indian commodity market is yet to be developed.

Institutional participation and trading in commodity options awaits parliamentary approval

Currently regulations only allow Indian corporate and agricultural houses to trade in the commodity markets apart from the retail investors. All other institutional

investors are not allowed to participate in the Indian exchange based commodity markets.

The cabinet has approved the Forward Contract Regulation Act (Amendment) Bill, 2010 in Oct-12 to amend the Forward Contract Regulation Act, 1952. However it

needs to be passed by both Houses of Parliament and was not done in the Winter Session of Parliament. It may be taken up in the Budget session of the Parliament,

though it is not very high on priority list for the government. The amended bill will make the commodity futures market regulator, Forward Markets Commission

(FMC), an autonomous regulator from one overseen by a ministry of Consumer Affairs.

The Bill also seeks to facilitate entry of institutional investors and pave the way for introduction of new category of products, like Options. Globally, commodity

options account for ~ 50% of the overall exchange based commodity volumes on the major commodity exchanges. If the proposal is accepted, ICRA expects the

commodity markets to gain with wider participation and higher liquidity.

Chart 13: National Spot Exchange Volumes – Quarter wise

Source: FMC website, ICRA Analysis

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13

Others

ACE

ICEX

NMCE

NCDEX

MCX

ICRA LIMITED P a g e | 14

The government had to remove the controversial clause allowing banks to participate in commodities futures from the Banking Regulation Amendment Bill, to

secure its passage in Q3FY12-13. So bank participation in commodity trading market may not be seen in the near future. The FMC is asking bankers to ask their

borrowers to hedge themselves for their commodity exposure, which should help increase participation in exchange traded commodity market.

Introduction of Commodity Transaction Tax of 0.01% on Non-agricultural commodity futures: to have marginally negative impact on the commodity segment

The Union Budget 2013 has introduced the Commodity Transaction Tax of 0.01% on Non-agricultural commodity futures, (similar to STT levied on equity futures

transactions). CTT was first proposed in the 2008 Budget, but was not implemented due to opposition by traders, brokers and commodity exchanges over concerns

of it potentially impeding the growth of a nascent segment. With huge proprietary volumes on the exchange, imposition of CTT is expected to reduce the spreads

available for commodity arbitrage trades in cash to future transactions by ~ 20 – 30% and in future to future transactions by ~ 40% to 50%. However, the wider

effect on the client volumes would remain to be seen.

However, short term concerns notwithstanding, market players believe that the long term prospects of this segment remains strong.

Commodities broking revenue pool estimated at Rs 17-23 billion per annum

As per ICRA estimates (based on segment wise market volumes and segment wise average yields of the industry adjusted for the proprietary volumes), the flat

commodity market volumes along with marginal reduction of commodity brokerage yields by 5-10% has led to the commodity brokerage revenue pool in the range

of ~ Rs 17 – 23 billion. At 9MFY 12-13 levels, the commodities brokerage revenue pool as a percentage of equity brokerage revenue pool stands at 16-22% (~17-23%

in FY 11-12) representing a increasing source of revenue diversification for brokerage houses.

Commodities market involve higher operating risk compared to equity markets

Compared to equity markets, the operating risk is higher in the commodity segment with physical holding of the commodity at exchange warehouses and various

classes of the same commodity based on quality. The liquidity is also low for some of the agricultural based commodities, which may lead higher price fluctuations

and malpractices of artificial pressure in prices. ICRA has seen few cases of commodity brokers incurring operating losses on account of these risks.

Commodity segment provides diversification opportunity for Indian brokerage houses

As a lot of regulatory changes may take place in the near future, the near term performance of commodity brokerage market may be dependent on government’s

actions. However, the commodity segment is still in a developing stage in India and expected to grow in the long run. The commodity broking business provides a

source for diversification of revenue for the equity brokerage houses. There are expectations that the gush of liquidity caused by quantitative easing III in the US

may once again find its way into commodities asset classes. Any increase in volatility could then mean good news for brokers. ICRA takes note of the strong

customer addition and increased investor awareness for the commodity markets. Consequently, ICRA believes that commodity trading is steadily emerging as a

sustainable mode of diversification for capital market intermediaries.

ICRA LIMITED P a g e | 15

CURRENCIES:

Currency segment growing at a steady pace; first mover advantage in currency options makes NSE the market leader

In 9MFY12-13, the exchange traded currencies segment has been growing at a

steady pace. Turnover on all the exchanges together was recorded at Rs. 61.22

trillion, indicating a decline of ~18% on an annualized basis. This was explained by

high turnover recorded in H1FY11-12 before the Competition Commission of India

ruling which mandated transaction charges on trades done by the exchanges.

Predictably, this ruling impacted volumes and volumes recorded in H2FY11-12 were

much lower at Rs. 35.48 trillion. Hence when compared to volumes recorded in

H2FY11-12, market turnover in 9MFY12-13 recorded an increase of 15%. ADV was

reported at Rs 33 billion in 9MFY12-13 as compared to Rs 40 billion in FY11-12 and

Rs 29 billion in H2FY11-12.

As an outcome of the two year long dispute between MCX-SX and SEBI, it was not

accorded the license to trade in currency options while NSE and the USE led the race.

NSE seems to have benefitted significantly. What started out as a two-horse race for

market share has ended up with NSE much ahead with a market share of between

58-63% in 9MFY12-13 as compared to MCX-SX, which has lagged behind with a

market share in the range of 35-42% over the same period.

In terms of currency pairs traded, USD-INR currency pair trading accounts for more

than 95% of overall trading with other three currency pairs - EURO-INR, GBP-INR and

JPY-INR in that order. Options’ trading continues to be allowed only in the USD-INR

pair. Market participants have reported a steady increase of clients – both genuine

hedgers as well as arbitrageurs. Market participants have noted that globally

currency OTC segment have been much lower than exchange traded segment.

Consequently, as the regulatory regime for this segment evolves as well as more

clients get enlisted, this segment is expected to gain significant traction. Market

participants have however conceded that growth of this segment is expected to face

a bottleneck on account of unavailability of experienced executives.

Currency brokerage revenue pool pegged at ~Rs 4-5 billion

As per ICRA estimates, currency broking yields have remained in the range of 0.5 –

0.6 bps in 9MFY12-13. The steady increase in currency market volumes as well as

currency brokerage yields has led to an expansion of the currency brokerage revenue pool to Rs 4-5 billion, an increase of ~8-12% when compared to FY11-12.

Chart 14:Currency market turnover -Quarterly

Source: ICRA Analysis, USE, NSE, MCX-SX website

Chart 15:Currency exchange market share

Source: ICRA Analysis, USE, NSE, MCX-SX website

ICRA LIMITED P a g e | 16

OTHER CAPITAL MARKETS LINKED BUSINESSES

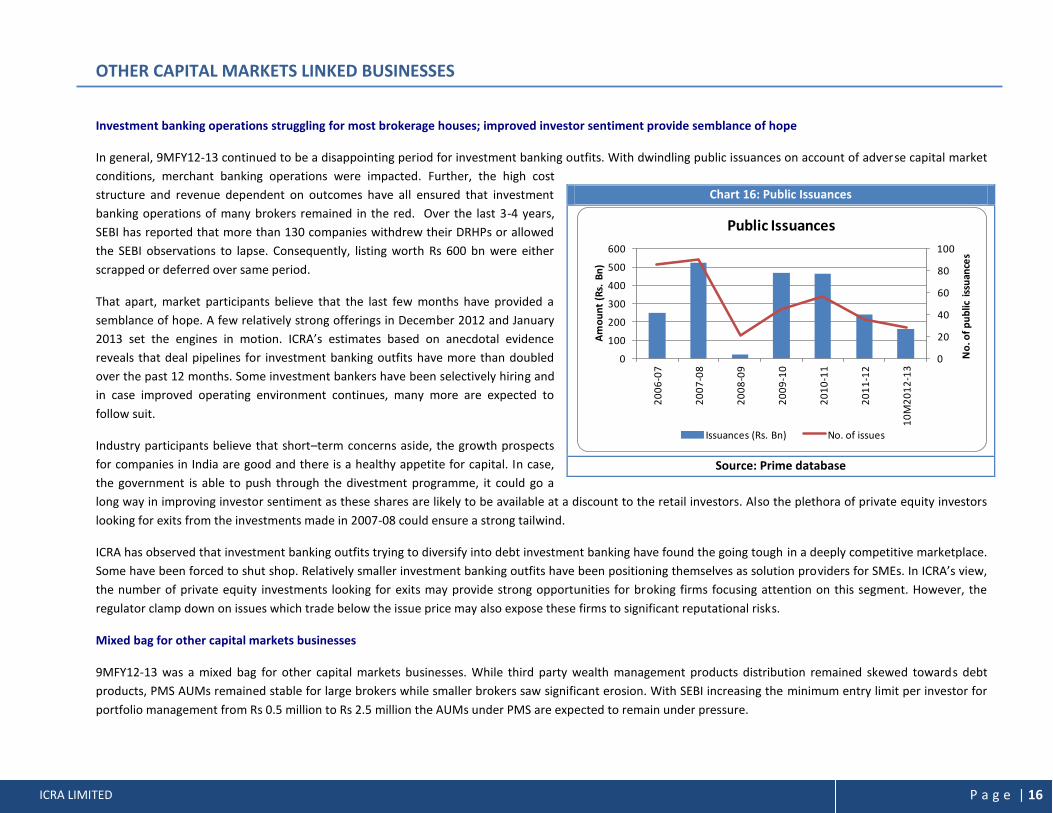

Investment banking operations struggling for most brokerage houses; improved investor sentiment provide semblance of hope

In general, 9MFY12-13 continued to be a disappointing period for investment banking outfits. With dwindling public issuances on account of adverse capital market

conditions, merchant banking operations were impacted. Further, the high cost

structure and revenue dependent on outcomes have all ensured that investment

banking operations of many brokers remained in the red. Over the last 3-4 years,

SEBI has reported that more than 130 companies withdrew their DRHPs or allowed

the SEBI observations to lapse. Consequently, listing worth Rs 600 bn were either

scrapped or deferred over same period.

That apart, market participants believe that the last few months have provided a

semblance of hope. A few relatively strong offerings in December 2012 and January

2013 set the engines in motion. ICRA’s estimates based on anecdotal evidence

reveals that deal pipelines for investment banking outfits have more than doubled

over the past 12 months. Some investment bankers have been selectively hiring and

in case improved operating environment continues, many more are expected to

follow suit.

Industry participants believe that short–term concerns aside, the growth prospects

for companies in India are good and there is a healthy appetite for capital. In case,

the government is able to push through the divestment programme, it could go a

long way in improving investor sentiment as these shares are likely to be available at a discount to the retail investors. Also the plethora of private equity investors

looking for exits from the investments made in 2007-08 could ensure a strong tailwind.

ICRA has observed that investment banking outfits trying to diversify into debt investment banking have found the going tough in a deeply competitive marketplace.

Some have been forced to shut shop. Relatively smaller investment banking outfits have been positioning themselves as solution providers for SMEs. In ICRA’s view,

the number of private equity investments looking for exits may provide strong opportunities for broking firms focusing attention on this segment. However, the

regulator clamp down on issues which trade below the issue price may also expose these firms to significant reputational risks.

Mixed bag for other capital markets businesses

9MFY12-13 was a mixed bag for other capital markets businesses. While third party wealth management products distribution remained skewed towards debt

products, PMS AUMs remained stable for large brokers while smaller brokers saw significant erosion. With SEBI increasing the minimum entry limit per investor for

portfolio management from Rs 0.5 million to Rs 2.5 million the AUMs under PMS are expected to remain under pressure.

Chart 16: Public Issuances

Source: Prime database

0

20

40

60

80

100

0

100

200

300

400

500

600

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

10

M2

01

2-1

3

No

. of

pu

blic

iss

uan

ces

Am

ou

nt

(Rs.

Bn

)

Public Issuances

Issuances (Rs. Bn) No. of issues

ICRA LIMITED P a g e | 17

Smaller retail brokers continued to close down equity markets proprietary arbitrage operations as increased penetration of algorithmic trading have thinned the

spreads and made operations unviable. The mediocrity of the recent performance in proprietary arbitrage trading is in part the result of massive growth. Whereas in

the past it was plausible for smart managers to spot market anomalies, several hundred managers in a large industry would be unlikely to earn spectacular returns.

However, with algorithms not yet written for commodities trading, brokers have shifted attention to this segment. Larger brokers have ramped up fund allocation

for proprietary commodities arbitrage. ICRA estimates, based on anecdotal evidence suggest that gross returns in commodity proprietary arbitrage operations (pre-

interest and tax) remained in the 15-17% p.a range. Warehousing as well as other related costs set returns back by 2.5-3.0%, allowing net returns (pre-interest and

tax) in the 12-14% range. However, with the proposed imposition of the commodities transaction tax on non-agriculture futures trading in the Union Budget 2013,

ICRA estimates the gross returns to be impacted by 20-30%. With MCX-SX starting equity trading in the second week of February 2013, market participants are

hopeful of revival of the “exchange to exchange” arbitrage opportunities returning as volumes pick up on MCX-SX. Also, reduction of STT on futures transactions on

the equity markets may lead to renewed interest into this segment.

Brokers looking to scale up their margin funding book

For a large part of FY12-13, margin funding books were in scale down mode for many capital market entities. With borrowing costs averaging between 12-18% and

outlook for equity markets bleak, returns looked uncertain. Also, the mid-caps and the small caps stock prices beaten down, demand for margin funding was

impacted.

Increasing retail participation in the equity capital markets have also led to a return of the demand for margin funding. Consequently, brokers have been turning

their attention to ramping up their margin funding book. As per anecdotal evidence in the last 2-3 months, margin funding / LAS book sizes for brokers have

increased by 20-30%. Industry participants believe that if equity markets hold up, sustained demand is likely to continue. Declining interest rates may also aid

demand. However, initial signs point that brokers have also been careful about scaling up this book. Industry participants have insisted for collateral preferable from

the BSE-200 category, beefed up security cover, insisted for transfer of shares to broker accounts rather than create a pledge in investor accounts and only extended

these loans to clients with existing relationships. ICRA has also observed some initial traction in the funding against commodities for clients. Brokers insist that

demand for funding against commodities remains a huge opportunity. However, proposed imposition of CTT in the Union Budget 2013 may temper this optimism, at

least for funding against non-agricultural commodities.

Non capital market related lines of diversification for few capital market players gain traction; some contemplating entering into other NBFC lending segments

Some brokerage entities having access to capital had forayed into non-capital market related businesses – consumer funding, mortgage financing and SME loans. In

FY12-13, the books continue to be in scale up mode with no significant asset quality concerns surfacing. Some of these players are also contemplating entering into

other asset classes where they have been able to find opportunities exciting. Also, buoyed by the apparent success in scaling up NBFC operations of these few

players, some other larger capital markets players are bucking the trend and now exploring non-capital markets related forays.

While these entities are funding long tenured assets and also been able to tie up long maturity bank loans, the pace of their growth has been such that there has

been no discernable reduction in their dependence on short term borrowings, which inherently is not a stable source of borrowing. Consequently, in ICRA’s view,

these entities remain vulnerable to ALM mismatches.

ICRA LIMITED P a g e | 18

ICRA continues to watch this space closely. In ICRA’s view, while these players have been successfully scaling up operations in these businesses over last 3-4 years,

they have yet to withstand the test of business cycles. While asset quality for these lines of businesses remains at comfortable levels at present, the ability to

maintain the same through business cycles would remain a key sensitivity.

ICRA LIMITED P a g e | 19

KEY INDUSTRY TRENDS IN 9MFY 12-13 Capping of brokerage yields to DIIs and increased penetration of Direct Market Access (DMAs) could point to a significant structural change for institutional

equity brokers; consolidation possible

The SEBI in its Press Release dated August 16, 2012 capped brokerage commission fees at 12 basis points for the cash segment and at five basis points for the

futures and options (F&O) segment for mutual funds. This development has benefitted the domestic mutual fund industry, which has been through difficult times

over the last few years with abolition of entry loads and ebbing of long term money flows. In ICRA’s view, this development along with the increased penetration of

DMAs is expected to have a profound impact on landscape of institutional broking in India.

The institutional brokerage segment in India is largely dominated by the foreign brokerage houses. From the investors perspective, the activity ratio of the FIIs (who

have a strong preference for foreign brokerage houses) by far outnumber the DIIs. In ICRA’s estimates, the overall annual institutional brokerage revenue pool is

reckoned between Rs 22-25 billion. Of this revenue pool, foreign brokerage houses account for between 66-75%, while the rest is accounted by domestic brokerage

houses. These numbers change by ~3-5% depending on the state of the capital markets. In adverse capital market situations, the scramble for safety ensures more

volumes go to foreign brokerage houses while in strong bull markets, the domestic brokerage houses’ relatively stronger corporate access ensures more volumes to

them.

Before these regulations, in ICRA’s estimate gross brokerage yields on cash market transactions for institutional investors were in the range of 5-20 bps, contingent

on volume generation. In general FIIs paid lesser than DIIs on account of large volume generation. However, over the past few years, institutional brokers have

conceded that protecting their yields has been difficult. Anecdotal evidence suggests that gross cash yields are lower by 15 - 25% as compared to three years into

the past. Institutional brokers have also conceded that while the capping of yields is applicable only to mutual funds, they have been under increasing pressure from

their other clients – namely the FIIs and the insurance companies to reduce the yields for them. To add to their cup of woes, high competitive intensity has also

ensured high customer attrition. Consequently, these new regulations are only expected to bite more.

Over the last few years, while the penetration of DMAs has been generally increasing, over the past few quarters, this trend is becoming increasingly pronounced.

Two factors largely influence the demand for DMAs – cost and confidentiality. Over the past few years while costs were always an issue, confidentiality was the

primary focus area for investors. Clients - especially FIIs have since long patronized foreign brokerage houses on account of greater degree of trust regarding

confidentiality of their trades. However, lackluster performance of the Indian capital markets have impacted their returns and hence caused these investors to pivot

and focus on costs as well. While there are different kinds of DMAs, in general DMAs price brokerage yields at anywhere between 20-40% of full service brokerage

commission. In certain select instances pricing has been seen at even lower. However, the lower yields also necessitate extremely limited client servicing.

From the demand perspective – different kind of investors have been buying into Indian equities. On the FII side, the biggest FIIs are those with emerging market

funds with specific allocation to India. These funds are largely Exchange Traded Funds and consequently research offered by Institutional investors is of limited

importance. For these investors DMAs are a boon.

The other kind of investors has been the hedge funds – usually buying both index as well as individual stocks. For these investors, investment horizon could be as

little as a few weeks or a few months at best. Also, their continued presence in the Indian capital markets horizon cannot be taken for granted. Due to their largely

fickle nature, the cost-benefit of servicing them has always been a focal discussion area for institutional brokers with some large institutional brokers making a

deliberate attempt to stay away.

ICRA LIMITED P a g e | 20

The other investors – India long only funds are funds which require access to research as well as corporate access. These include FIIs with India dedicated funds,

Indian DIIs – including insurance companies and mutual funds. However uncertainty in the global economic scenario has built strong risk averseness leading to lower

incremental flows for the foreign long only funds. The domestic mutual funds industry in itself has been facing dwindling long dated funds, cost containment issues

and redemption pressures. As already mentioned earlier, they have been net sellers in Indian equities in 9MFY12-13. Insurance companies, with the exception of LIC

have been relatively smaller players. Also tight regulations by IRDA on investment norms have ensured that participation from insurance players may remain at

lower levels.

It is here that the new regulations and the advent of DMAs would bite. ICRA notes that at an average, for ICRA rated entities, ~20-30% of institutional broking

volumes are now through DMAs. Institutional brokers rated have been split in their view regarding the future of DMAs. While some strongly believe that this is a

trend here to stay, others differ on the premise that at some stage capital markets may revive and newer growth stories may emerge. At such times they believe,

Indian equity markets may be inundated by fresh portfolio inflows and these investors would require servicing. The remunerative potential from these flows could

be very large.

All this presents a quandary for institutional brokers. Institutional broking unlike retail broking entails a higher entry and exit barrier. Also, due to weak global

economic outlook, institutional broking allied segments such as investment banking have also remained in the red for many brokers. Also, with retail participation

muted, profits from retail broking operations have not been able to subsidize costs for institutional broking. FII flows have been volatile and DIIs have been net

sellers. Consequently, many of them have been forced to cut costs. Employee spending and that on making market presence constitute bulk of the costs for

institutional brokers. Conferences have been the high impact but high cost format for brokers aspiring to further their market presence. Cost per conference,

depending on venue, location, guests could range from Rs. 2 – 10 million. Consequently, expenditure on conferences have been on the wane. Brokers have

embarked upon the relatively inexpensive road-shows and webinars to touch base with their clients. Many brokerage houses have realigned their analyst teams and

tried to bring on board lower cost resources.

The problem is particularly acute for smaller institutional brokers but hardly restricted to them alone. Unsurprisingly some brokers have found the going tough. A

few have closed down institutional broking operations while many others are only pulling along in hope for a turnaround. Unless Indian equity markets turnaround

in the next few quarters, ICRA expects smaller domestic institutional brokers to shut shop. ICRA also believes that acquisitions in the institutional broking space may

remain elusive. Institutional brokers do not generally benefit by increased allocation from FIIs or DIIs in the event or a merger between two institutional brokers.

Also, benefits such as client acquisitions generally can be got by customary acquiring large teams from competing brokerage houses. Hence, in ICRA’s view, while

current state of institutional broking may force players to put their shops on the block, takers for the same may only be limited.

Muted retail participation showing early signs of improvement; retail brokers further cut costs by going slow on offline customer addition

ICRA has observed that in the wake of weak retail segment participation, the pressures on profitability have only got more severe for retail brokers. Some small

retail brokers have been making losses even the larger ones have been facing significant pressures on profitability.

Their fingers already burnt in 2008 and its aftermath, broad based retail participation in the equity markets remained conspicuously absent. Even the prolonged

range bound index movement for bulk of the last year could not entice the retail segment back into the markets. In fact, the number of demat accounts even

showed some decline below 20 million as at March 2012. Consequently the sudden sharp uptick in the indices did not go unnoticed, but was “too soon, to sharp”

for many investors. Hence, retail brokers remain cautiously optimistic for a full-scale return of the retail investor. Nevertheless, announcements of reforms

ICRA LIMITED P a g e | 21

programme as well as initiatives for easing the pressure on public finances has helped improve sentiment. A few relatively well performing IPOs in the early part of

December 2012, also brought back some confidence. Consequently, the retail segment slowly trickled back into the broader market. ICRA has observed a sharp

decline in market share for the top-10 brokers while moderate decline in the market share of the top-100 brokers indicative of return in interest levels for the retail

segment, who generally patronizes the smaller retail brokers.

Retail brokers have long argued the merits of adding customers in difficult times to take the benefits of the upside when good times return. Consequently, while

market conditions remained adverse over the last few years, customer addition by retail brokers continued unabated. In ICRA’s view, now this phenomenon has run

its course. ICRA has also observed that retail brokers tweaked their business model by pulling the plug on offline client acquisition. With low activity levels and the

relatively high customer acquisition cost (Rs 3000-4000 one-time cost) not

paying off by client activity levels, retail brokers have also rationalized on

their client acquisition teams. Consequently, many retail brokers are now

concentrating their energies on improving client activity levels. Efforts have

been made by many retail brokers to understand their client trading habits

and customize their client engagement initiatives to suit their mindsets.

For example, if a retail broker has observed that over a period of time, their

client has only bought shares of “A” category stocks, the trading calls sent out

to the investor would be more fundamental research based. Conversely, if a

client has historically delved into intra-day trading, such customized calls are

being sent to them. In case of select retail brokers, specific conferences have

been held with clients to understand their mindsets and engage with them to

build portfolios that could perfectly suit their risk-taking abilities. All this has

helped retail brokers cut their costs further, while improving customer

engagement.

Conversely, increased thrust has been placed on adding online trading clients. Consequently, select brokers have been upgrading their technology platforms as well

as their sales force to push their online trading offering. In ICRA’s view, providing an online trading platform has given brokers better pricing power as compared to

offline clients. Also, once the initial set-up costs are complete, online trading requires much lower client servicing costs as compared to offline clients. Consequently,

online trading is more profitable for brokers. However, ICRA notes that with select exceptions, bank owned brokerage houses have largely established themselves as

pioneers in online broking. Consequently, for non-bank owned brokerage houses, adding online customers has remained a challenge on account of greater

resistance for the average retail investor to shift from the more trusted bank portals towards the relatively unknown. Also, bulk of the retail investors have online

broking accounts linked to their bank accounts making it difficult for non-bank owned retail brokers to wean away these clients to them, despite most of them

having payment gateway tie-ups with 30-35 banks. Consequently, retail brokers have conceded that most of their online broking clients are conversions from offline

clients and not genuine online broking customers.

Chart 17: Top Brokers equity broking market share

Source: NSE, ICRA Analysis

-

10

20

30

40

50

60

70

80

FY07-08 FY08-09 FY09-10 FY10-11 FY11-12 9MFY12-13

Perc

enta

ge

Equity Broking Market Share

Top 5 Top 10 Top 25 Top 50 Top 100

ICRA LIMITED P a g e | 22

In ICRA’s opinion, with heavy clouds still hanging over the sustainable retail participation, this approach from retail brokers could help somewhat ease pressures on

profitability. However, while the larger retail brokers have been able to adapt to the changed market dynamics, the smaller retail brokers could continue to lose

money. ICRA expects some consolidation action in the retail broking space over the medium to near term.

Retail brokers seen educating clients on options trading; activity levels amongst retail clients on the rise

ICRA has observed a few interesting trends for the retail customer behavioral pattern over the past 3-4 quarters. Retail brokers have taken to the classroom to

educate the retail investor about options trading. Many retail brokers have reported that while getting the retail investor to the classroom has been tough, the get

him acquainted with the nitty-gritty of options has been easier and that the average retail investor in showing increasing intrigue regarding this asset class.

Consequently, pockets within the retail investor have been realizing the benefits of options trading and also using equity stock options to reduce the holding cost of

holding delivery stock. Increasing proportion of equity stock options trading to 8% of total options trading for 9MFY12-13 from 5% in FY 11-12 provides evidence of

the manifestation of this phenomenon. This has also helped retail brokers re-invigorate their client activity levels. Brokers have also been aiding the trend by sending

out periodic options trading calls to their retail clients ICRA estimates based on anecdotal evidence that client activity levels (based on one trade per quarter) has

improved by an average of 4-5% in the last quarter.

Consequently, as retail investors are getting educated about options trading, the futures segment has lost significant momentum. As already mentioned earlier,

futures volumes on the exchanges have declined even in absolute number in 9MFY11-12. This can be part explained by the strong traction in the options segment.

Options volumes have led to decline of futures volumes in two ways. The first is pricing. Trading in one lot into options is far cheaper than that for futures. Also, the

perception that buying options limits the overall losses, while buying futures can theoretically entail unlimited loss has been to the detriment of futures volumes.

Consequently, futures volumes have fallen off the radar.

ICRA LIMITED P a g e | 23

PERFORMANCE UPDATE: H1FY12-13 ICRA has attempted to plot the financial performance of brokerage entities for H1FY12-13. For this objective, ICRA has analyzed the quarterly results of 15

prominent entities in the brokerage sector taken largely from public domain. In ICRA’s estimation, these entities account for ~35% of overall equity broking market

share.

ICRA has noted that some brokerage houses have ventured outside the capital markets

domain such as consumer funding, mortgages, insurance etc. Consequently, in terms of

methodology, ICRA has used the standalone financials of entities and weeded out the

impact of non-capital markets businesses on financial performance. The net results

reflect ICRA’s best estimates.

Overall revenue remains flat in H1FY12-13 (annualized) compared to FY 11-12…

In line with ICRA’s estimation that the equity brokerage revenue pool has remained flat

in FY12-13 when compared to FY 11-12 and minor decline in the commodities broking

revenue pool, the total revenues for the entities covered by ICRA remained almost flat

(minor de-growth of ~1%) (annualized) in H1FY12-13 when compared to FY 11-12. In

ICRA’s estimation, while the revenue pool has remained stagnant, increased market

share for the top brokers (covered in the earlier section) would have ensured slightly

higher revenues In ICRA’s estimation which would have been off-set by lost traction in

other capital markets ancillary activities.

In ICRA’s estimation, overall operating expenses also declined by ~7-8% in H1FY12-13.

Over the past couple of years, while there has been some rationalization in the

employee expenses – both on account of rationalization of pay structures as well as

overall headcount, reduction in public offerings ensured lower printing and stationary

expenses, consolidation of branches, renegotiation of rental expenses have all ensured

that brokerage entities have been able to keep a firm lid on costs and further tighten it

over a period of time. In ICRA’s view, while brokers have cut costs aggressively, in ICRA’s

view, the scope for further cost rationalization could be limited.

However, with decline in expenses being more pronounced than that for revenues, cost-

income ratio for the entities covered decreased by 500 bps to 77% in H1FY12-13 from

82% in FY11-12. The increase in cost-income ratio once again reinforces that despite

severe cost cutting measures, the sharper decline in revenues for brokerage entities has

exerted significant pressure on profitability.

Chart 18: Return on Net Worth

Source: ICRA Analysis

Chart 19: Cost-income ratio

Source: ICRA Analysis

12.30%

13.1%

8.9%

10.1%

0%

2%

4%

6%

8%

10%

12%

14%

FY10 FY11 FY12 H1FY13

RONW

RONW

86%

77%

82%

77%

72%

74%

76%

78%

80%

82%

84%

86%

88%

FY10 FY11 FY12 H1FY13

Cost-income ratio

Cost-income ratio

ICRA LIMITED P a g e | 24

Consequently, profitability indicators improved for the brokerage companies. Profitability as a percentage of total revenues improved to ~15% in H1FY12-13 as

compared to 13% in FY11-12. Return to assets improved to 3.6% in H1FY12-13 from 3.3% in FY11-12.

Initial impressions for Q3FY12-13 have been positive. While ICRA has not been able to analyse the results for all the entities enlisted above, revenue growth in

Q3FY12-13 (annualized) of 3-5% (annualized) has been observed when compared to FY11-12 which implies relatively strong performance in the quarter. Costs have

have not grown, consequently profitability has been strong in Q3FY12-13 on the back of increased cash volume led revenue growth

ICRA’S OUTLOOK FOR FY13-14 FOR THE SECTOR Old troubles may continue to plague the industry ahead. Retail participation remains uncertain, regulatory changes mean institutional equities business could face

significant structural challenges and other capital markets businesses may remain morose. While brokers have cut costs aggressively, in ICRA’s view, the scope for

further cost rationalization could be limited. Also, the Indian capital markets remain largely entwined with the global and domestic economy. As long as strong signs

of recovery do not emerge in the global economy, uncertain times may continue for the domestic capital markets.

However, the past 3-4 months have generally provided more good news than bad. The interest rate cycle seems to have peaked, liquidity flows in the country have

been strong, retail participation giving signs of returning to life and positive noises by the government have all in aggregate helped dispel some gloom that beset the

industry.

ICRA has noted that the industry brokerage revenue pool has been stabilizing. Commodities and currencies have emerged as dependable sources of diversification.

Brokers have re-aligned their business models vigorously to contain costs. Competitive pressures exist but have abated somewhat. Consequently, in ICRA’s view,

brokers are better tuned to face the challenges ahead. ICRA revises its outlook on the sector to “Stable” from “Negative”.

ICRA LIMITED P a g e | 25

Please contact ICRA to get a copy of the report

CORPORATE OFFICE Building No. 8, 2nd Floor, Tower A, DLF Cyber City, Phase II, Gurgaon 122002 Ph: +91-124-4545300, 4545800 Fax; +91-124-4545350 REGISTERED OFFICE 1105, Kailash Building, 11

th Floor,

26, Kasturba Gandhi Marg, New Delhi – 110 001 Tel: +91-11-23357940-50 Fax: +91-11-23357014

CHENNAI Mr. Jayanta Chatterjee Mobile: 9845022459 Mr. Leander Rayen Mobile: 9952615551 5th Floor, Karumuttu Centre, 498 Anna Salai, Nandanam, Chennai – 600035 Tel: +91-44-45964300 Fax: +91-44-24343663 E-mail: [email protected] [email protected]

HYDERABAD Mr. M.S.K. Aditya Mobile: 9963253777 301, CONCOURSE, 3rd Floor, No. 7-1-58, Ameerpet, Hyderabad 500 016. Tel: +91-40-23735061, 23737251 Fax: +91-40- 2373 5152 E-mail: [email protected]

MUMBAI Mr. L. Shivakumar Mobile: 9821086490 3rd Floor, Electric Mansion, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025 Ph : +91-22-30470000, 24331046/53/62/74/86/87 Fax : +91-22-2433 1390 E-mail: [email protected]

KOLKATA Ms. Vinita Baid Mobile: 9007884229 A-10 & 11, 3rd Floor, FMC Fortuna, 234/ 3A, A.J.C. Bose Road, Kolkata - 700020 Tel: +91-33-22876617/ 8839, 22800008, 22831411 Fax: +91-33-2287 0728 E-mail: [email protected]

PUNE Mr. Amit Khare Mobile: 9763200633 5A, 5th Floor, Symphony, S. No. 210, CTS 3202, Range Hills Road, Shivajinagar, Pune-411 020 Tel : +91- 20- 25561194, 25560195/196, Fax : +91- 20- 2553 9231 E-mail: [email protected]

GURGAON Mr. Vivek Mathur Mobile: 9871221122 Building No. 8, 2nd Floor, Tower A, DLF Cyber City, Phase II, Gurgaon 122002 Ph: +91-124-4545300, 4545800 Fax; +91-124-4545350 E-mail: [email protected]

AHMEDABAD Mr. Animesh Bhabhalia Mobile: 9824029432 907 & 908 Sakar -II, Ellisbridge, Ahmedabad- 380006 Tel: +91-79-26585049/2008/5494, Fax:+91-79- 2648 4924 E-mail: [email protected]

BANGALORE Mr. Jayanta Chatterjee Mobile: 9845022459 'The Millenia', Tower B, Unit No. 1004, 10th Floor, Level 2, 12-14, 1 & 2, Murphy Road, Bangalore - 560 008 Tel: +91-80-43326400, Fax: +91-80-43326409 E-mail: [email protected]

ICRA LIMITED P a g e | 26

ICRA Limited

An Associate of Moody's Investors Service

CORPORATE OFFICE

Building No. 8, 2nd

Floor, Tower A; DLF Cyber City, Phase II; Gurgaon 122 002

Tel: +91 124 4545300; Fax: +91 124 4545350

Email: [email protected], Website: www.icra.in

REGISTERED OFFICE

1105, Kailash Building, 11th

Floor; 26 Kasturba Gandhi Marg; New Delhi 110001

Tel: +91 11 23357940-50; Fax: +91 11 23357014

Branches: Mumbai: Tel.: + (91 22) 24331046/53/62/74/86/87, Fax: + (91 22) 2433 1390 Chennai: Tel + (91 44) 2434 0043/9659/8080, 2433 0724/ 3293/3294, Fax +

(91 44) 2434 3663 Kolkata: Tel + (91 33) 2287 8839 /2287 6617/ 2283 1411/ 2280 0008, Fax + (91 33) 2287 0728 Bangalore: Tel + (91 80) 2559 7401/4049 Fax + (91

80) 559 4065 Ahmedabad: Tel + (91 79) 2658 4924/5049/2008, Fax + (91 79) 2658 4924 Hyderabad: Tel +(91 40) 2373 5061/7251, Fax + (91 40) 2373 5152 Pune: Tel

+ (91 20) 2552 0194/95/96, Fax + (91 20) 553 9231

© Copyright, 2013 ICRA Limited. All Rights Reserved.

All information contained herein has been obtained by ICRA from sources believed by it to be accurate and reliable. Although reasonable care has been taken to

ensure that the information herein is true, such information is provided 'as is' without any warranty of any kind, and ICRA in particular, makes no representation or

warranty, express or implied, as to the accuracy, timeliness or completeness of any such information. All information contained herein must be construed solely as

statements of opinion, and ICRA shall not be liable for any losses incurred by users from any use of this publication or its contents.