Download - IABM Industry Update Industry Update Peter White, CEO, IABM Peter Bruce, APAC Director, IABM

IABM Industry UpdatePeter White, CEO, IABM

Peter Bruce, APAC Director, IABM

Regional Focus: Asia-Pacific• Peter Bruce, APAC Director, IABM

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

An Overview

Asia-Pacific

• The market in APAC is varied as it includes countries at very different stages of broadcast industry development

• Some countries are in the midst of transitioning to digital/HD broadcasting with a great deal of spending going into digital transmission, infrastructure and monitoring equipment

• Others have already migrated to digital/HD broadcasting and are pioneering the adoption of cutting-edge technologies such as UHD and ATSC 3.0

Source: Statista

2015 2016 2017 2018 2019 2020 2021 CAGR (2015-2021)Population 3421m 3450m 3477m 3504m 3530m 3555m 3579m 0.8%GDP / Capita US$ $6,200 $6,433 $6,799 $7,209 $7,705 $8,288 $8,897 6.2%Internet Penetration (%) 43.2% 45.5% 48.0% 50.5% 53.1% 55.9% 58.7% 5.3%Smartphone Penetration (%) 29.1% 32.4% 35.3% 37.9% 40.1% 42.0% 43.6% 7.0%

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

An Overview

Asia-Pacific

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Economic growth in APAC remains the highest in the world, mostly driven by India and China – India > China

• The slowdown in the Chinese economy during 2015 softened in 2016 and 2017 as a result of a renewed increase in infrastructure investment

• Growth in Southeast Asia will average 4.8% in the next three years driven by the Philippines, Vietnam, Cambodia, Lao and Myanmar

Asia-Pacific Economic Outlook: Stronger than the rest of the world

Business Environment

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2015 2016 2017* 2018*

GDP Growth in Major World regions, 2015-2018

World Output

Advanced Economies

Emerging and DevelopingAsia

Emerging and DevelopingEurope

Latin America and theCaribbean

Middle East, North Africa,Afghanistan, and Pakistan

Sub-Saharan Africa

Source: IMF

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Most economies are dependent on China

Business Environment

0%

5%

10%

15%

20%

25%

30%

35%

Singapore Korea Malaysia Chile Thailand SaudiArabia

Australia NewZealand

Philippines Japan

Trade Linkages with China (Export and Import Ratios), Top 10 countries

Export ratio Import ratio Slowdown in China has affected economic activity in other countries as well!

Source: OECD (Organization for Economic Co-operation and Development)

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Indonesia: GDP and manufacturing PMI are both rising. Economic conditions are still very positive. Infrastructure spending is though slowing

• Thailand: Strength of the baht undermining local export sector –imports have soared at the beginning of 2017 due to the currency’s appreciation. Infrastructure spending is accelerating

• Malaysia: Economy still suffering from low oil prices and lower global trade – this situation should improve in 2017 (more trade)

• Lao & Myanmar: the region’s fastest growing economies (growing 7% or higher)

• Singapore: will grow the lowest as it is the more mature economy (and it is more dependent on China’s growth)

Southeast Asia Economic Outlook: Generally Stronger

Business Environment

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

Myanmar

Lao

Cambodia

Vietnam

Philippines

Indonesia

Malaysia

Thailand

Singapore

Brunei

GDP Growth Forecasts

2016 2017

Source: IMF

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

In the first part of 2017, most currencies have appreciated Vs USD

Business Environment

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

AUD/USD CNY/USD INR/USD IDR/USD JPY/USD MYR/USD NZD/USD PHP/USD SGD/USD KRW/USD TWD/USD VND/USD THB/USD

Selected APAC currencies, Gain/Loss Vs USD January-May 2017

Appreciation Vs USD

Depreciation Vs USD

Source: PACIFIC Exchange Rate Services

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• China imposes a trade tariffs and other export restraints such as quotas and licences on a variety of products

• Weak Intellectual Property Rights (IPR) protection & lack of trade transparency: trade secrets theft, registration of trademarks in bad faith, procurement preferences for local companies, excessively subsidization of local companies

• “Onerous requirements on the use of encryption, including intrusive approval processes and, in many cases, mandatory use of indigenous encryption algorithms continue to be cited as a significant trade barrier” says USTR report

• New Cybersecurity Law issued at the end of 2016 restricts market access for cloud computing and internet-enabled services

Trade barriers in China & India

Business Environment

China

• India imposes tariff and non-tariff barriers. The tariff structure is composed by basic customs duty, an “additional duty,” a “special additional duty,” an education assessment (“cess”) and, possibly, a landing fee

• In 2009, India initiated a web-based Indian Customs Electronic Commerce/Electronic Data Interchange Gateway, known as ICEGATE (http://icegate.gov.in) more info on the BI Digest

• Tariffs on a variety of products (including telecommunications equipment) were increased recently

• 2014 policy mandates Electronics and Information Technology Equipment Manufacturers register their products with laboratories affiliated or certified by the Bureau of Indian Standards (BIS) even if these have already been certified by accredited international laboratories higher compliance costs

India

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Positive operational performance at constant exchange rates. This changes when accounting for variance in exchange rates (between 2015 and 2016) – most currencies have lost ground Vs. USD

• Growing Pay-TV market – rising revenues and profits across the whole region

• Pay-TV threatened by online piracy – it is rife in Asia-Pacific

• Advertising picture varies depending on the country considered

Both Revenues and Profits are up!

End-Users’ Performance

5%

3%

0%

1%

2%

3%

4%

5%

6%

Revenue Change Profit Change

Asia-Pacific

Source: IABM End-User Index(Constant Exchange Rates)

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

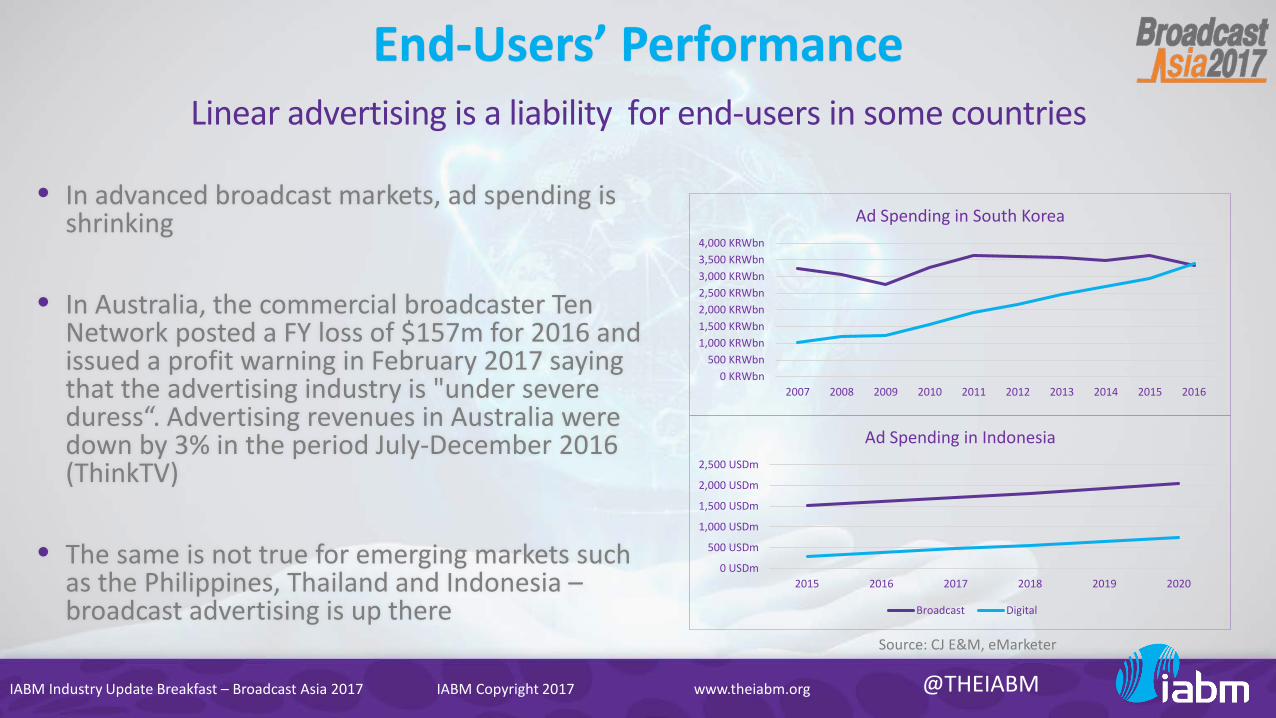

• In advanced broadcast markets, ad spending is shrinking

• In Australia, the commercial broadcaster Ten Network posted a FY loss of $157m for 2016 and issued a profit warning in February 2017 saying that the advertising industry is "under severe duress“. Advertising revenues in Australia were down by 3% in the period July-December 2016 (ThinkTV)

• The same is not true for emerging markets such as the Philippines, Thailand and Indonesia –broadcast advertising is up there

Linear advertising is a liability for end-users in some countries

End-Users’ Performance

Source: CJ E&M, eMarketer

0 KRWbn500 KRWbn

1,000 KRWbn1,500 KRWbn2,000 KRWbn2,500 KRWbn3,000 KRWbn3,500 KRWbn4,000 KRWbn

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ad Spending in South Korea

0 USDm

500 USDm

1,000 USDm

1,500 USDm

2,000 USDm

2,500 USDm

2015 2016 2017 2018 2019 2020

Ad Spending in Indonesia

Broadcast Digital

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Pay-TV is expected to grow by 5.8% in the period 2016-2021. This is slower than before due to piracy – opportunity for conditional access & DRM vendors

• Subscriber growth is expected to slow down in Southeast Asia although ARPU is set to remain healthy

• Ad-blocking software is highly concentrated in Asia. For instance, the Asia-Pacific region contains 55% of global smartphone users but 93% of ad-blocking browser usage!

• In India and Indonesia, more than half the smartphone population use ad-blocking browsers. Pop-up ads appearing on browsers reduce page loading speed and this is exacerbated in emerging countries as mobile broadband infrastructure is less developed

Piracy & Ad-Blocking are major issues in APAC

End-Users’ Performance

Source: Pagefair

0 20 40 60 80 100 120 140 160 180

Egypt

Germany

Great Britain

France

UAE

Nigeria

Philippines

Vietnam

Malaysia

United States

Brazil

Saudi Arabia

Russian Federation

Pakistan

Indonesia

India

China

Active Users of Adblocking Browsers by Country, March 2016 (millions)

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

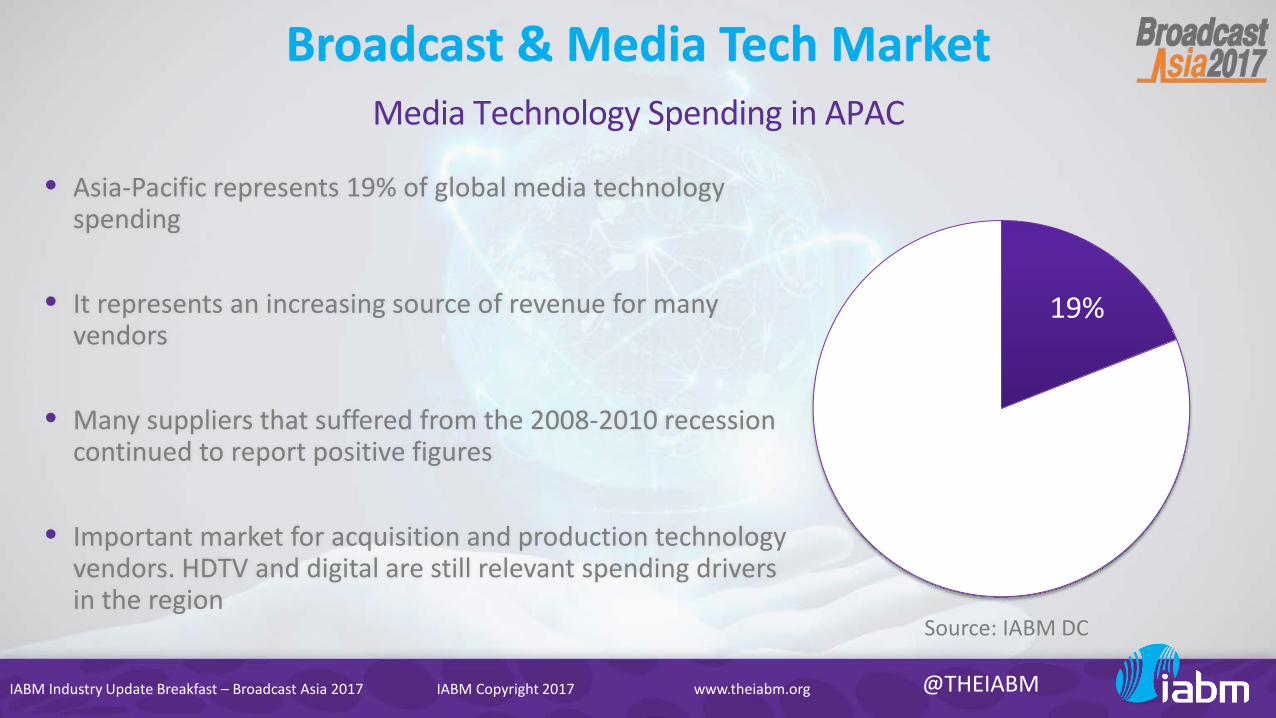

• Asia-Pacific represents 19% of global media technology spending

• It represents an increasing source of revenue for many vendors

• Many suppliers that suffered from the 2008-2010 recession continued to report positive figures

• Important market for acquisition and production technology vendors. HDTV and digital are still relevant spending drivers in the region

Media Technology Spending in APAC

Broadcast & Media Tech Market

19%

Source: IABM DC

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Only five countries have completed the digital transition in APAC (12.5%), the rest is either going through the transition or has not started it yet. Major constraint to completing the transition is: lack of government funding to household and broadcasters

• One of the few exceptions is Thailand (where the transition is ongoing): the communications regulator has distributed millions of vouchers to buy digital equipment. Eligible households include those living in social housing and “state enterprise” officials. The expected DSO date is 2020

• In Myanmar, the original DSO plan entails the analogue switch-off of over 200 stations between 2017 and 2019. The expected DSO date is 2020. . The Myanmar government has recently issued five new free-to-air licences (DVB-T2) in April 2017 to the following broadcasters: DVB Multi Media, Fortune International, KuangMyanmar Aung, Mizzima Media, and Young Investment Group

Status of Digital Transition in APAC

Digital Transition

0%

10%

20%

30%

40%

50%

60%

70%

Completed Ongoing Not Started Unknown

Status of Digital Transition in APAC

Source: ITU

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Vietnam intends to complete the transition to digital by 2020. Between 2017 and 2018 over 20 provinces will switch to digital

• The two most populous Southeast Asian countries, Indonesia and the Philippines, should complete their transitions by 2018 and 2023 respectively

• In Indonesia, DTT has been tested in 20 cities including Jakarta since 2016 – Indonesia is set to become the third-largest digital TV market by the end of the decade

• In the Philippines, GMA network has already invested in digital equipment. ABS-CBN has begun testing the technology in major cities. The government has recently unveiled its plan for transmission via the Japanese system ISBD-T

Status of Digital Transition in APAC

Digital Transition█ Not Started

█ Unknown

█ Completed

█ Ongoing

Source: ITU

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• South East Asia’s potential for increased HDTV channel deployment is big

• In China there is 1 HD channel for every 9.4m TV households. In the US there is 1 HD channel for every 197K TV households

• Other countries (except from Japan, South Korea etc.) have very low HD penetration rates as well

• Satellite broadcasting is important to the development of HD in Asia-Pacific. Many satellite service providers have expanded their capacity in the region to allow for a more extensive coverage

• In the next three years, the digital dividend in countries transitioning to digital will allow for more efficient delivery more HD channels

HD Deployment in APAC

HD Spending

0

100

200

300

400

500

600

700

US China

No. of HD Channels

Source: Statista

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• S Korea ATSC 3.0 UHD transmission to start the 31st May 2017 (beating USA). ATSC 3.0 will aid the further growth of 4K/UHD channels in the country

• The transition to 4K/UHD is underway in Japan, South Korea and India, where some local Pay-TV operators have already started broadcasting in the new format

• In Japan, some operators such as Sky Perfect JSAT have already launched 4K/UHD channels in 2015-2016. Japan’s Ministry of Internal Affairs & Communications announced that it aims at having 19-22 4K/UHD channels (operated by both FTA and Pay-TV broadcasters) on air by 2018 to focus on 8K deployment ahead of 2020 Tokyo Summer Games

• There have not been any noteworthy initiatives in Southeast Asia except from a few cases. First Media, an Indonesian Pay-TV provider, launched 4K/UHD in mid-2016

4K/UHD Adoption in APAC

4K/UHD Spending

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• The transition to file-based technology is still relevant in Asia-Pacific. According to our End-User data, about 20% of our APAC respondents have transitioned less than 50% of their operations to from tape to file – “file-based workflows” ranks high in the tech priorities’ index. This, along with digitization of workflows, is being adopted to make operations more efficient

• Media asset management ranks very high as well in the tech priorities’ index although primary priority remains multi-platform delivery – same in all other regions

File-Base Workflows & Media Asset Management

Other Spending Drivers

Facilis Technology partnered with local resellers in India,Hong Kong and The Philippines to help Asianbroadcasters such as ABS-CBN and Powervision TVmigrate to non-linear workflows

Telestream and Vizrt have partnered to integrate MAMand transcode solutions for media customers in theAPAC region

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

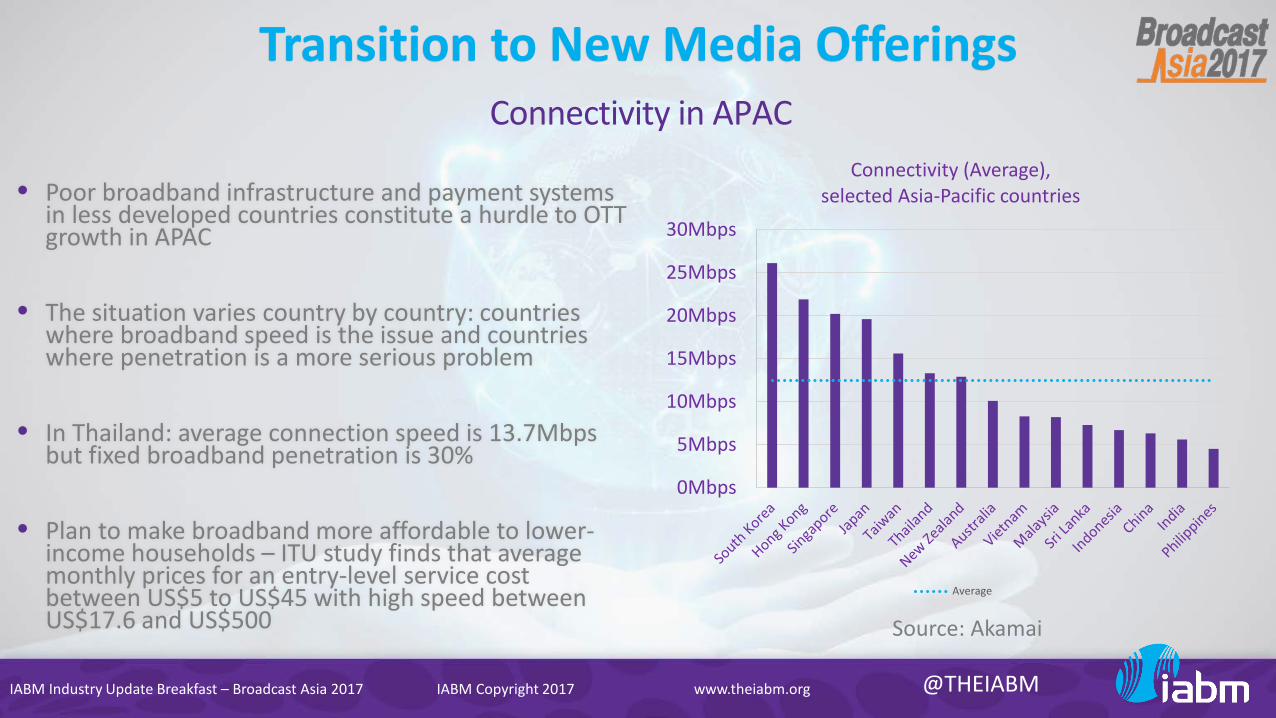

• Poor broadband infrastructure and payment systems in less developed countries constitute a hurdle to OTT growth in APAC

• The situation varies country by country: countries where broadband speed is the issue and countries where penetration is a more serious problem

• In Thailand: average connection speed is 13.7Mbps but fixed broadband penetration is 30%

• Plan to make broadband more affordable to lower-income households – ITU study finds that average monthly prices for an entry-level service cost between US$5 to US$45 with high speed between US$17.6 and US$500

Connectivity in APAC

Transition to New Media Offerings

0Mbps

5Mbps

10Mbps

15Mbps

20Mbps

25Mbps

30Mbps

Connectivity (Average),selected Asia-Pacific countries

Average

Source: Akamai

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• In most Southeast Asian countries, bank account penetration is very low

• Singapore is the exception – 96% penetration, like Luxembourg

• The majority of people who have a bank account often do not engage with it:

• Indonesia: 36% bank account penetration and 26% debit card ownership. Only 1% and 8.5% of these accounts are engaged in credit card and debit card transactions respectively

• Philippines: 31% bank account penetration and 20.5% debit card ownership. Usage rates are 2% and 3.5% respectively

Financial sector development in Southeast Asia

Transition to New Media Offerings

Source: World Bank

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Singapore Malaysia Thailand Indonesia Philippines Vietnam Myanmar Cambodia

Bank account penetration in Southeast Asia

Average

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

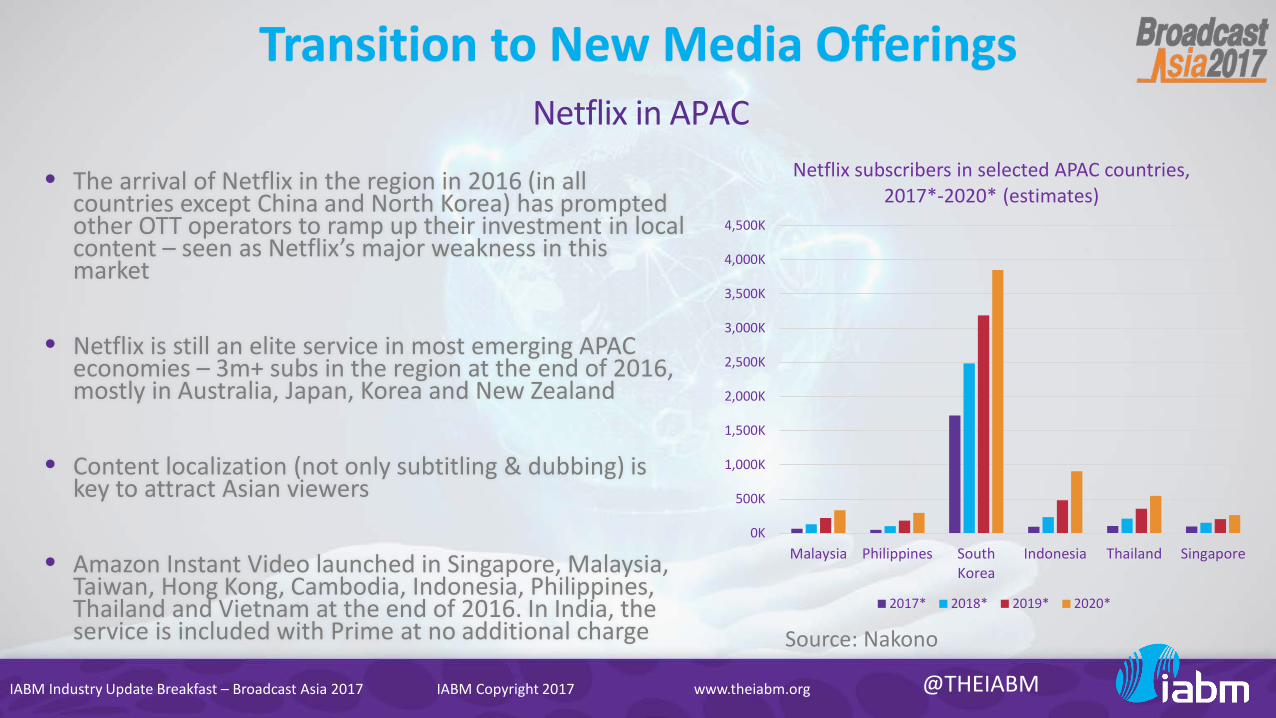

• The arrival of Netflix in the region in 2016 (in all countries except China and North Korea) has prompted other OTT operators to ramp up their investment in local content – seen as Netflix’s major weakness in this market

• Netflix is still an elite service in most emerging APAC economies – 3m+ subs in the region at the end of 2016, mostly in Australia, Japan, Korea and New Zealand

• Content localization (not only subtitling & dubbing) is key to attract Asian viewers

• Amazon Instant Video launched in Singapore, Malaysia, Taiwan, Hong Kong, Cambodia, Indonesia, Philippines, Thailand and Vietnam at the end of 2016. In India, the service is included with Prime at no additional charge

Netflix in APAC

Transition to New Media Offerings

Source: Nakono

0K

500K

1,000K

1,500K

2,000K

2,500K

3,000K

3,500K

4,000K

4,500K

Malaysia Philippines SouthKorea

Indonesia Thailand Singapore

Netflix subscribers in selected APAC countries, 2017*-2020* (estimates)

2017* 2018* 2019* 2020*

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

• Viu: launched by Hong Kong-based media behemoth PCCW in 2015. It boasts over 9m subscribers in over 10 countries and is Netflix’s main competitor in the region. It offers both free and paid subscriptions

• LeEco: is the leader in the Chinese OTT market. It is a technology provider offering integration of its OTT subscription with its smart devices and TVs. LeEco acquired the rights for broadcasting important sports events such as the English Premier League and the World Cup

• Iflix: provides a paid subscription service offering in countries such as Malaysia, Indonesia, The Philippines and Thailand. In 2016, it entered a strategic partnership with the European Pay-TV operator, Sky

• HOOQ: is offered in Indonesia, The Philippines, Thailand and India. It is a video streaming service provider backed by Sony, Warner Bros. and Singaporean telco Singtel

Other New Media offerings

Transition to New Media Offerings

The State of the GlobalBroadcast & Media Industry

Peter White, CEO, IABM

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

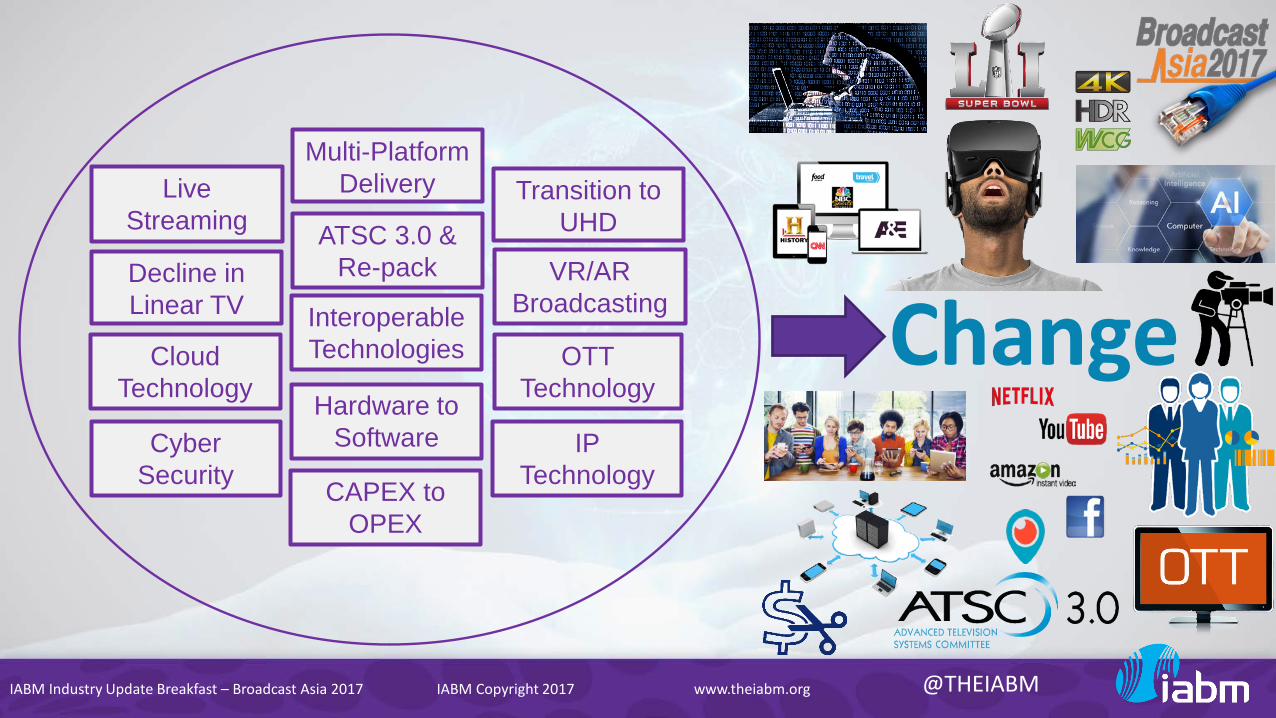

Multi-Platform DeliveryLive

Streaming

VR/ARBroadcasting

Transition toUHDATSC 3.0 &

Re-packDecline in Linear TV

CloudTechnology

CAPEX to OPEX

Hardware to Software

OTT Technology

InteroperableTechnologies Change

IPTechnology

Cyber Security

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

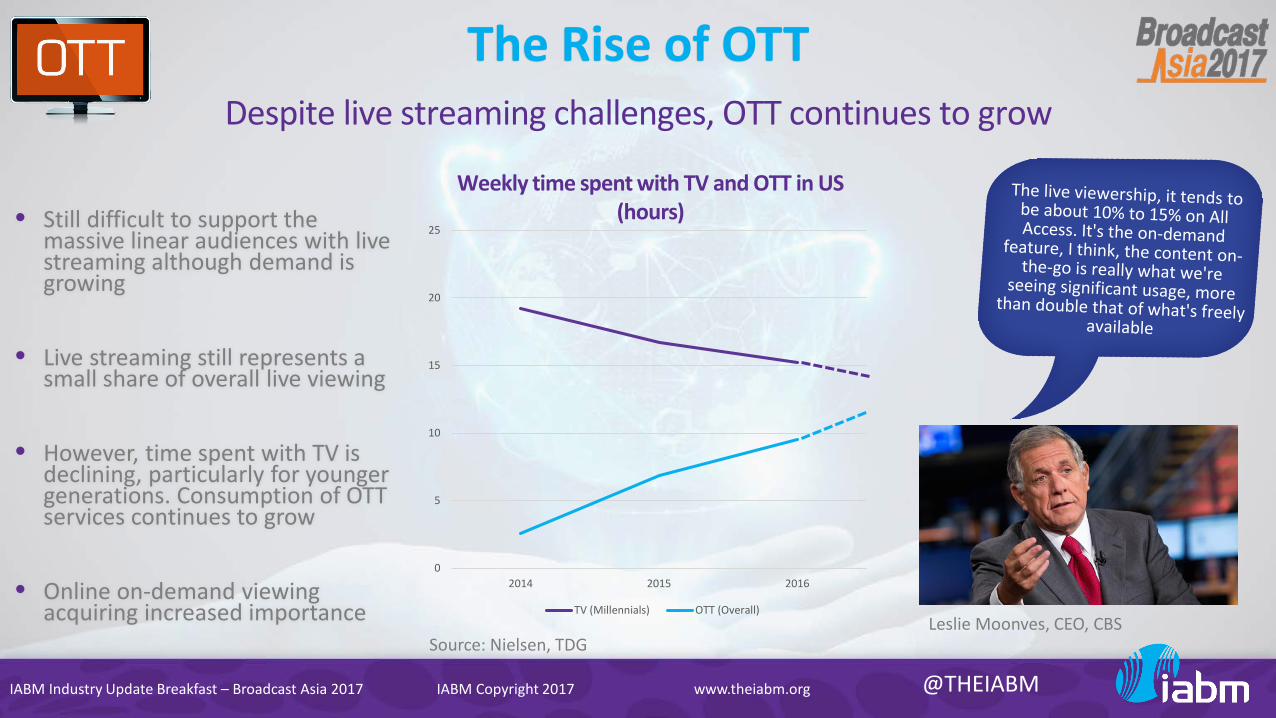

The Rise of OTTDespite live streaming challenges, OTT continues to grow

Weekly time spent with TV and OTT in US (hours)• Still difficult to support the

massive linear audiences with live streaming although demand is growing

• Live streaming still represents a small share of overall live viewing

• However, time spent with TV is declining, particularly for younger generations. Consumption of OTT services continues to grow

• Online on-demand viewing acquiring increased importance

Source: Nielsen, TDG

0

5

10

15

20

25

2014 2015 2016

TV (Millennials) OTT (Overall)Leslie Moonves, CEO, CBS

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

The Rise of OTTTraditional US Broadcast & Media Landscape

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

The Rise of OTTNew US Broadcast & Media Landscape

Traditional

New

Traditional

New

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

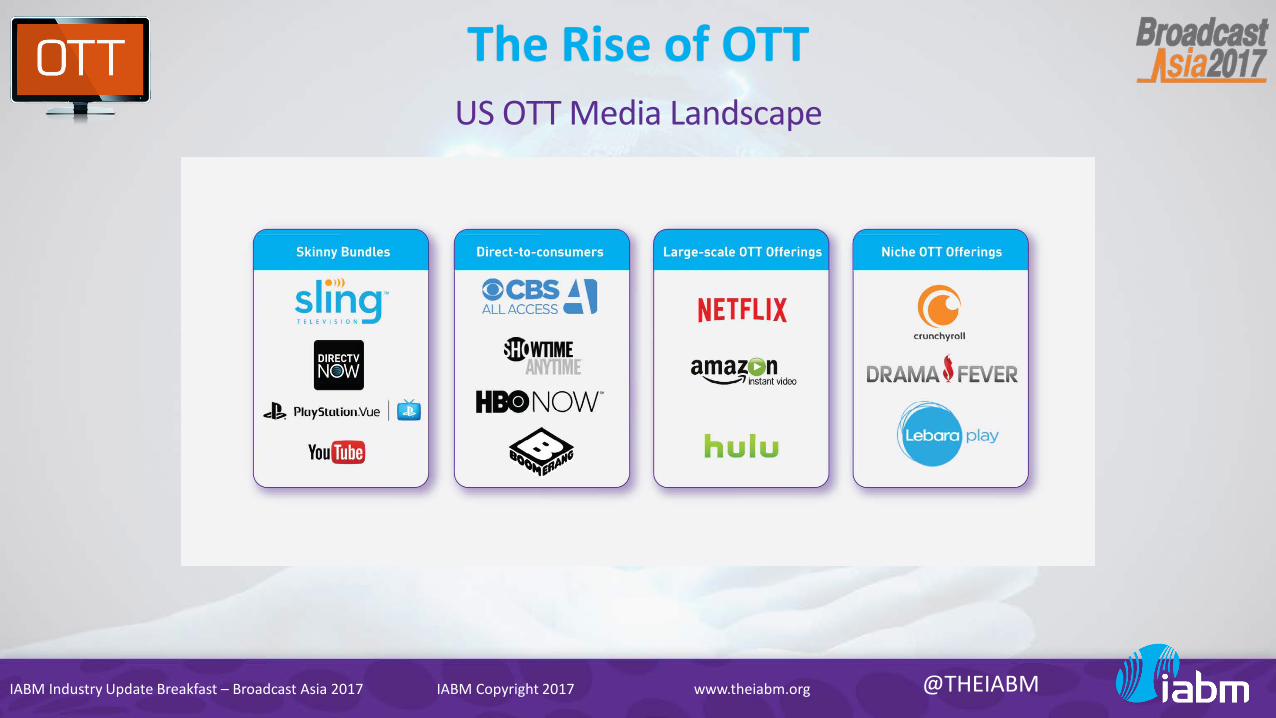

US OTT Media Landscape

The Rise of OTT

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

35%30%

38%

17%

39%

29%

48%

25%29%

9%11%

8%

9%

10%

11%

10%

17% 11%

9% 14% 11%

11%

11%

12%

9%

16% 16%

12%18% 16%

22%

16%19%

16% 22%17%

35% 28% 27% 40% 24% 29% 17% 20% 27%

0%

20%

40%

60%

80%

100%

2013 NAB 2013 IBC 2014 NAB 2014 IBC 2015 NAB 2015 IBC 2016 NAB 2016 IBC 2017 NAB

0-20 21-40 41-60 61-80 81-100

New

Traditional

The Rise of OTTPercentage revenue from traditional broadcast operations versus new activities such as web,

mobile, streaming, multi-platform content delivery?

Source: IABM Pre-NAB Show 2017 End-User Survey

CURR

ENT

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

34%29%

37%

18%

39%

30%

48%

22%26%

7% 14%9%

12%

11%15%

11%

18% 17%

13%

20% 16%

22%

16%18%

15%27%

17%

18%

21% 20%25%

20% 21%15% 22%

25%

27% 16% 17% 24% 14% 16% 11% 11% 15%

0%

20%

40%

60%

80%

100%

2013 NAB 2013 IBC 2014 NAB 2014 IBC 2015 NAB 2015 IBC 2016 NAB 2016 IBC 2017 NAB

0-20 21-40 41-60 61-80 81-100

New

Traditional

The Rise of OTTPercentage revenue from traditional broadcast operations versus new activities such as web,

mobile, streaming, multi-platform content delivery?

IN 2

–3

YEAR

S TI

ME

Source: IABM Pre-NAB Show 2017 End-User Survey

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

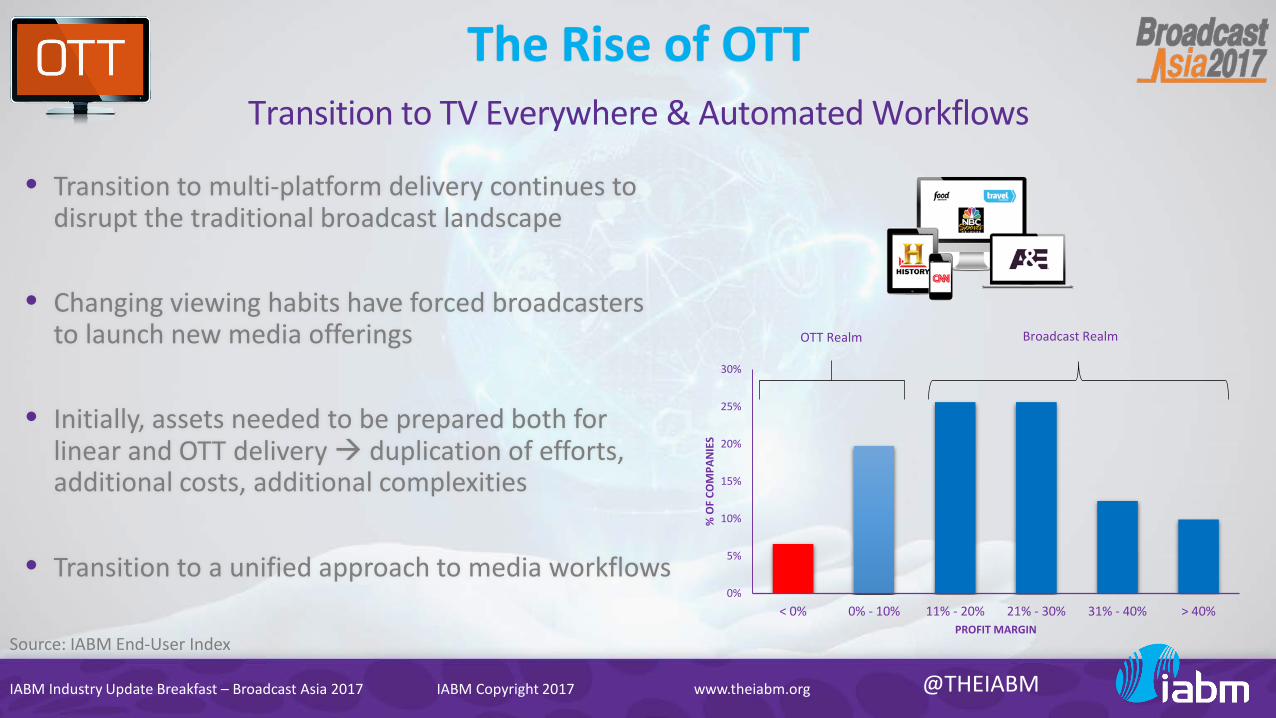

The Rise of OTT

• Transition to multi-platform delivery continues to disrupt the traditional broadcast landscape

• Changing viewing habits have forced broadcasters to launch new media offerings

• Initially, assets needed to be prepared both for linear and OTT delivery duplication of efforts, additional costs, additional complexities

• Transition to a unified approach to media workflows

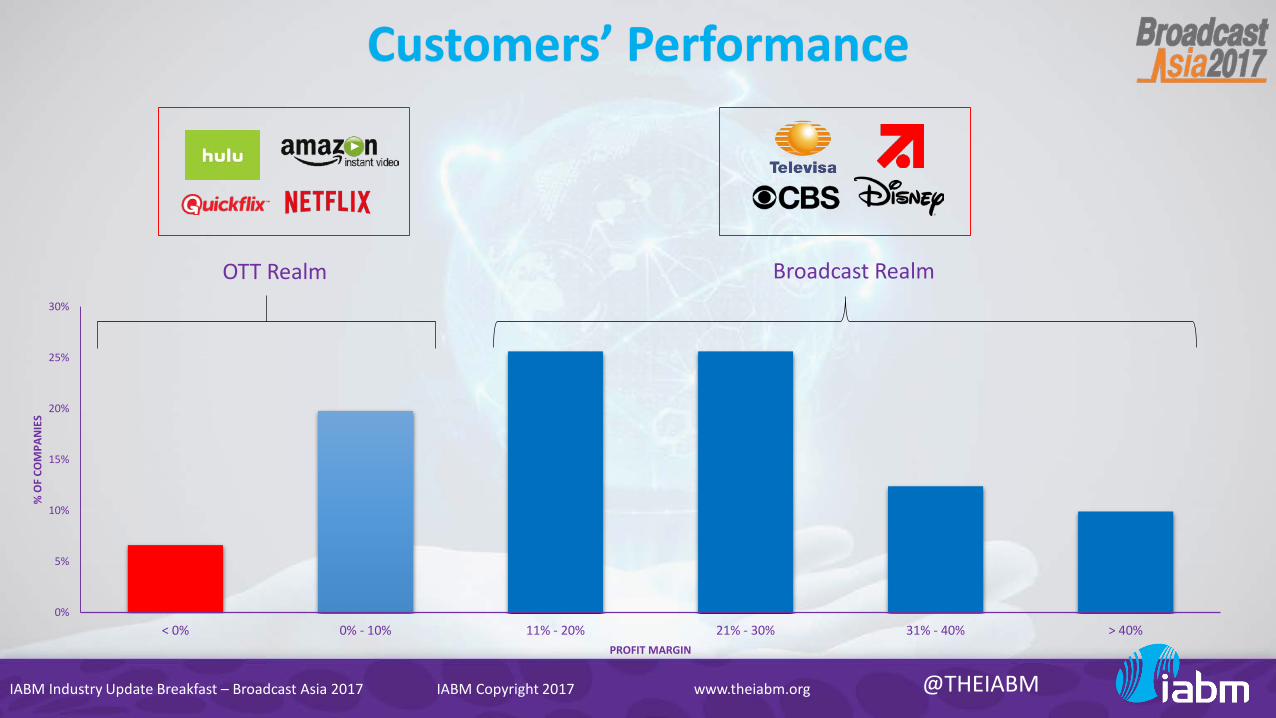

Transition to TV Everywhere & Automated Workflows

0%

5%

10%

15%

20%

25%

30%

< 0% 0% - 10% 11% - 20% 21% - 30% 31% - 40% > 40%

% O

F CO

MPA

NIE

S

PROFIT MARGIN

OTT Realm Broadcast Realm

Source: IABM End-User Index

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

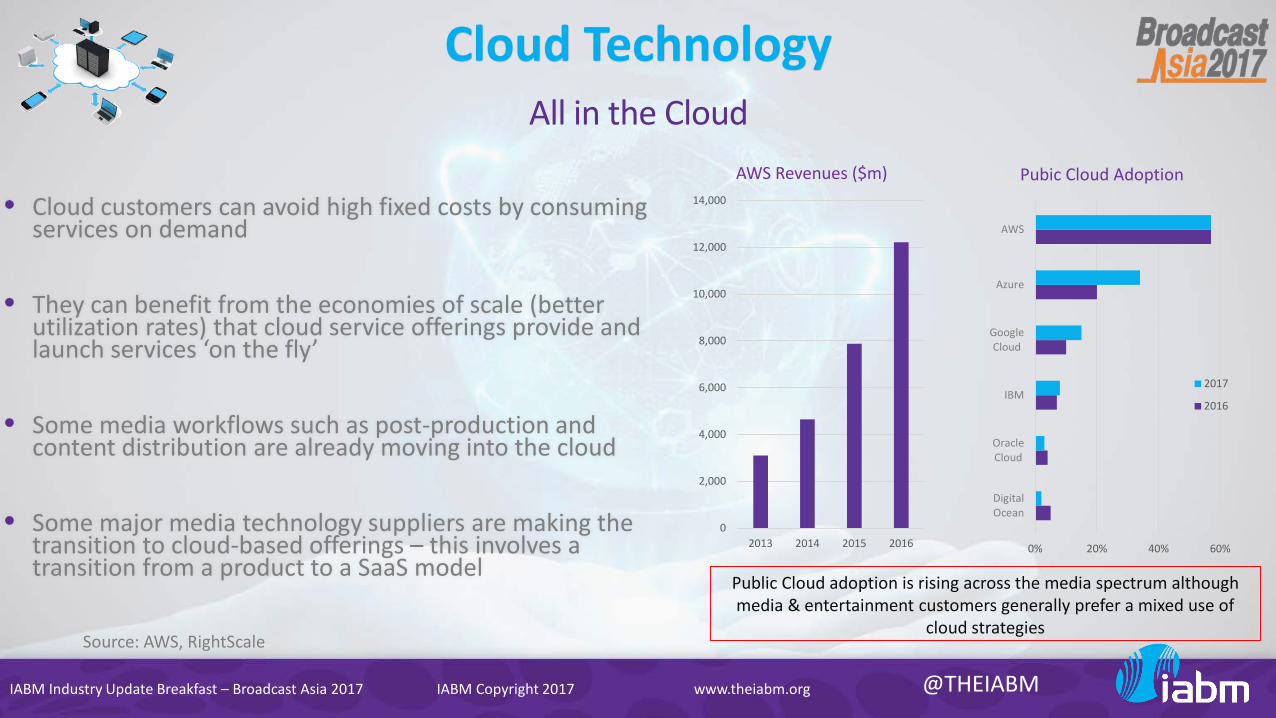

Cloud Technology

• Cloud customers can avoid high fixed costs by consuming services on demand

• They can benefit from the economies of scale (better utilization rates) that cloud service offerings provide and launch services ‘on the fly’

• Some media workflows such as post-production and content distribution are already moving into the cloud

• Some major media technology suppliers are making the transition to cloud-based offerings – this involves a transition from a product to a SaaS model

All in the Cloud

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2013 2014 2015 2016

AWS Revenues ($m)

0% 20% 40% 60%

DigitalOcean

OracleCloud

IBM

GoogleCloud

Azure

AWS

Pubic Cloud Adoption

2017

2016

Source: AWS, RightScale

Public Cloud adoption is rising across the media spectrum although media & entertainment customers generally prefer a mixed use of

cloud strategies

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

How likely are you to deploy some sort of cloud-based technology in the next 2-3 years?

What is the preferred deployment strategy for the adoption of cloud-based technology in your organisation?

4%

18%

19%

24%

35%

0% 10% 20% 30% 40% 50%

Other

Private Cloud (On-Premise)

Public Cloud

Private Cloud (Off-Premise)

Hybrid Cloud28%

0%

5%

10%

15%

20%

25%

30%

35%

Not at all likely Unlikely Somewhatlikely

Very likely We arealready doing

it today

15% 85%

Cloud Technology

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

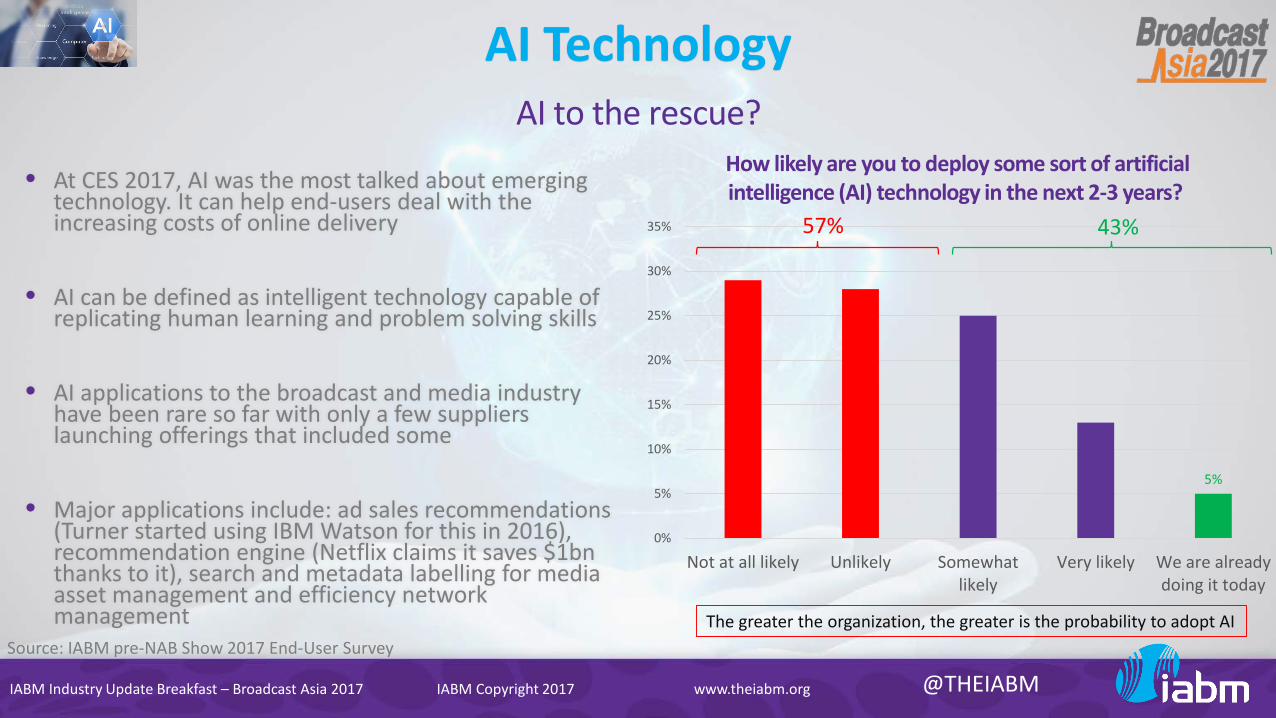

AI Technology

• At CES 2017, AI was the most talked about emerging technology. It can help end-users deal with the increasing costs of online delivery

• AI can be defined as intelligent technology capable of replicating human learning and problem solving skills

• AI applications to the broadcast and media industry have been rare so far with only a few suppliers launching offerings that included some

• Major applications include: ad sales recommendations (Turner started using IBM Watson for this in 2016), recommendation engine (Netflix claims it saves $1bn thanks to it), search and metadata labelling for media asset management and efficiency network management

AI to the rescue?How likely are you to deploy some sort of artificial intelligence (AI) technology in the next 2-3 years?

5%

0%

5%

10%

15%

20%

25%

30%

35%

Not at all likely Unlikely Somewhatlikely

Very likely We are alreadydoing it today

57% 43%

The greater the organization, the greater is the probability to adopt AISource: IABM pre-NAB Show 2017 End-User Survey

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Cyber Security CheckHackers continue to threaten media companies

40%

34%

16%

6%4%

Very high

Quite high

Quite low

Very low

Don't know

How high or low a priority is Cyber Security in your organization’s technology strategy?

IP-Networking, Cloud & Data Explosion create new vulnerabilities

Source: IABM pre-NAB Show 2017 End-User Survey

Has your organization experienced any Cyber Attacks in the last three years?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

From 1 to 50 from 51 to 500 from 500 to 10000 Over 10000Number of Employees

No

Yes

“The default assumption is that everything is vulnerable”Robert Watson, Computer Scientist, University of Cambridge

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Customers’ PerformanceBroadcast Revenue Sources

Source: IABM pre-NAB Show 2017 End-User Survey

53%

19%

28%

License Fee/Gov. Funding

30%

35%

35%

47%

37%

7%9%

SubscriptionsAdvertising

Increase Stay the SameDecline

Increase Stay the SameDecline Don’t Know

Increase Stay the SameDecline

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Customers’ PerformanceTraditional Broadcast & Media Technology Buyers

Next-Generation Broadcast & Media Technology Buyers

Other Broadcast & Media Technology Buyers

Demand

Workflow / Asset Management

Video Editing Tools

Routing & Networking Products

Production Switchers

Test & Measurement Tools

Playout Automation Products

Ingest / Transcoding / Streaming Products

Transmitters

Audio Mixers & Consoles

System cameras (Studio / Location)

Integrated Playout (Channel-in-a-Box)

Near-Line / Off-Line Storage Products

Service Providers

Demand Demand

Product Vendors

Production / Post-Production Outside Broadcast Transmission Services Equipment Rental OTT/OVP Platforms Content Delivery Networks

Med

ia O

rgan

izatio

nsNo

n-M

edia

O

rgan

izatio

ns

Focus

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Customers’ Performance

Media Networks Pay-TV Operators

75% 25%

10%

-9%

8% 9%

-15%

-10%

-5%

0%

5%

10%

15%

Revenue Change Profit Change Revenue Change Profit Change

Media Networks Pay-TV Operators

9%

-7%

-15%

-10%

-5%

0%

5%

10%

15%

Revenue Change Profit Change

Overall Industry

% o

f Tot

al

Indu

stry

Rev

enue

s

Source: IABM End-User Index

93%

7%

Profit-Making

Loss-Making

% o

f Tot

al

Indu

stry

Rev

enue

s

47 countries covered

187 companies included in the sample

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Customers’ Performance

5%

1%

11%

-10%

5%3%

-15%

-10%

-5%

0%

5%

10%

15%

Revenue Change Profit Change Revenue Change Profit Change Revenue Change Profit Change

EMEA Americas Asia-Pacific

% o

f Tot

al

Indu

stry

Rev

enue

s

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Customers’ Performance

0%

5%

10%

15%

20%

25%

30%

< 0% 0% - 10% 11% - 20% 21% - 30% 31% - 40% > 40%

% O

F CO

MPA

NIE

S

PROFIT MARGIN

OTT Realm Broadcast Realm

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Suppliers’ PerformanceYear on Year Sales Growth, last 24 months up to March 2017

-15%

-10%

-5%

0%

5%

10%

15% Global 3 mth mov avg. Large 3 mth mov avg. SME 3 mth mov avg.

13.5%

Source: IABM Industry Index – March 2017

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Suppliers’ PerformanceProfit Statistics: Profit Growth (left) & % of Companies in Profit and Loss (right)

-25%

-15%

-5%

5%

15%

25%

Apr-

15

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct

-15

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-

16

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct

-16

Nov

-16

Dec-

16

Jan-

17

Feb-

17

Mar

-17

Global 3 month mov avg.

Source: IABM Industry Index – March 2017

34.5%

65.5%

Profit Making Loss Making

Nov-16 Mar-17 Trend

In profit both years 53.4% 53.8% ↑

Moving from loss to profit 11.7% 11.7% =

In loss both years 24.3% 22.8% ↓

Moving from profit to loss 10.7% 11.7% ↑

Copyright @ 2013-2017 IABM DC

Total Market Size by Region

$b

$10b

$20b

$30b

$40b

$50b

$60b

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Americas EMEA Asia Pacific

Asia Pacific19%

EMEA43%

Americas38%

$50.1 billion

Helicopter view of the Broadcast & Media Technology Industry

IABM Industry Update Breakfast – Broadcast Asia 2017

Copyright @ 2013-2017 IABM DC

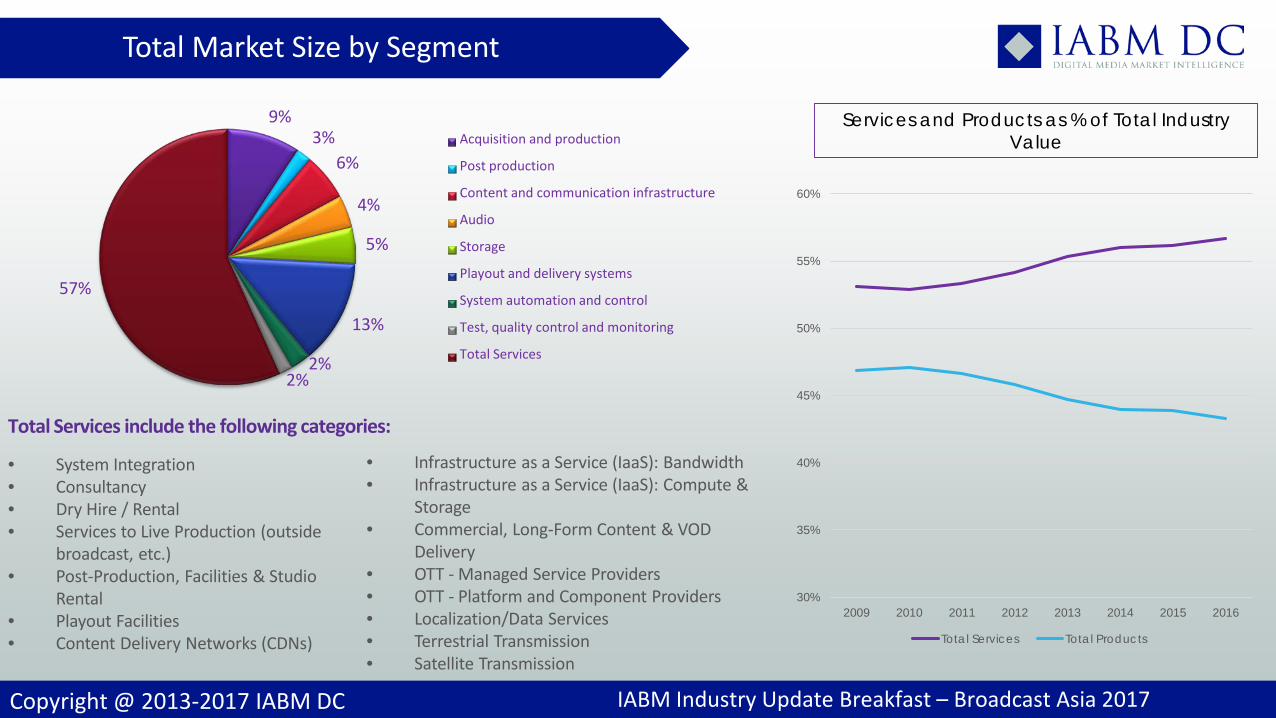

9%3%

6%

4%

5%

13%

2%2%

57%

Acquisition and production

Post production

Content and communication infrastructure

Audio

Storage

Playout and delivery systems

System automation and control

Test, quality control and monitoring

Total Services

Total Market Size by Segment

IABM Industry Update Breakfast – Broadcast Asia 2017

30%

35%

40%

45%

50%

55%

60%

2009 2010 2011 2012 2013 2014 2015 2016

Total Services Total Products

• System Integration• Consultancy• Dry Hire / Rental• Services to Live Production (outside

broadcast, etc.)• Post-Production, Facilities & Studio

Rental• Playout Facilities• Content Delivery Networks (CDNs)

Total Services include the following categories:

• Infrastructure as a Service (IaaS): Bandwidth• Infrastructure as a Service (IaaS): Compute &

Storage• Commercial, Long-Form Content & VOD

Delivery• OTT - Managed Service Providers• OTT - Platform and Component Providers• Localization/Data Services• Terrestrial Transmission• Satellite Transmission

Services and Products as % of Total Industry Value

Copyright @ 2013-2017 IABM DC

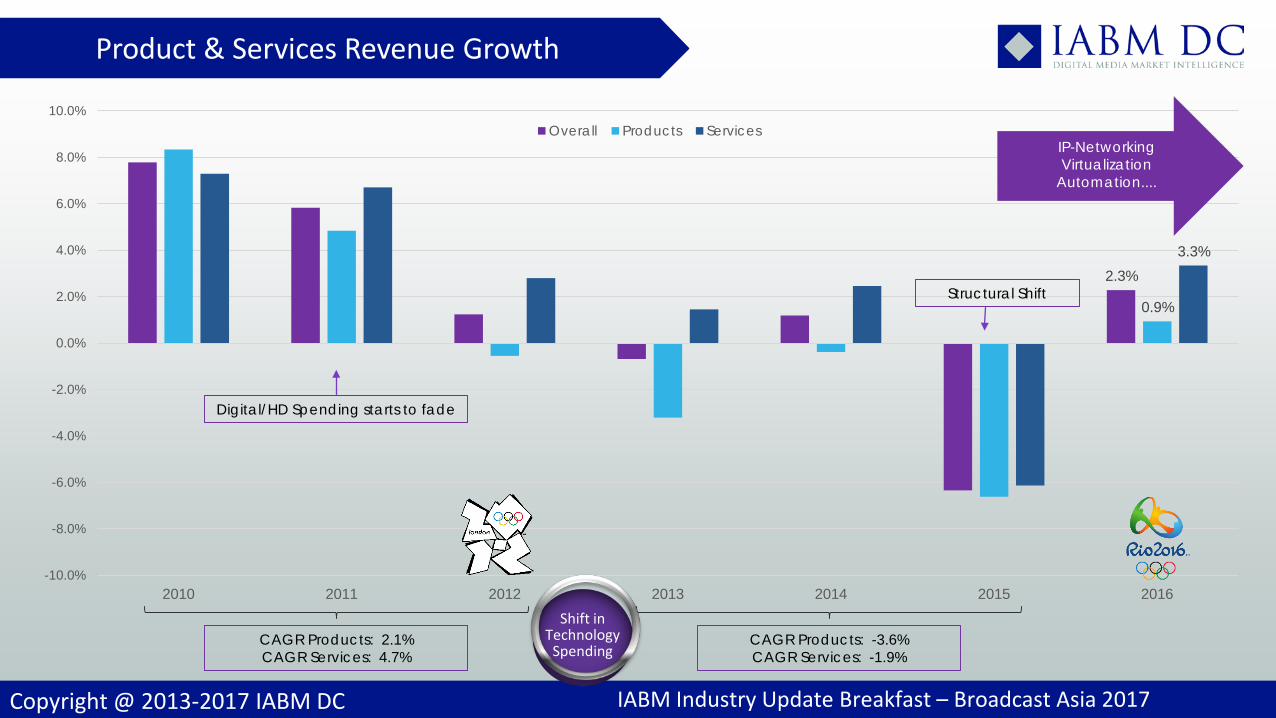

Product & Services Revenue Growth

2.3%

0.9%

3.3%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2010 2011 2012 2013 2014 2015 2016

Overall Products Services

Digital/HD Spending starts to fade

Structural Shift

CAGR Products: 2.1%CAGR Services: 4.7%

CAGR Products: -3.6%CAGR Services: -1.9%

IP-NetworkingVirtualization

Automation....

Shift inTechnology

Spending

IABM Industry Update Breakfast – Broadcast Asia 2017

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Suppliers’ View2 Important Transitions

• Broadcast and media technology users have traditionally relied on a CAPEX model with product upgrade cycles of up to 10 years

• The take-up of cloud computing in media & entertainment is favoring the transition to an OPEX model where costs flexibly vary on the basis of user demand

• Subscriptions guarantee steadier cash flows (and shorter product cycles) but suppliers are used to finance their high R&D expenditures with large money influxes (typical of licencefee/hardware model)

• Many traditional broadcast and media technology suppliers still rely on hardware as their primary source of revenues

• With end-users moving to software-defined infrastructures built on COTS equipment, bespoke hardware revenues are under pressure

• Traditional suppliers are therefore embarking on a difficult transition from purpose-built hardware to delivering software running on general-purpose equipment

From Hardware to Software From CAPEX to OPEX

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

State of 4K/UHD Adoption4K/UHD Adoption – A Timeline

What is the most likely timeline for the launch of UHD offerings in your organization?

55%

10%

35%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Alreadylaunched

1 to 3 years 4 to 6 years 7 to 10 years No plan tolaunch

Only 22% plan to launch UHD offerings in the next 3 years

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

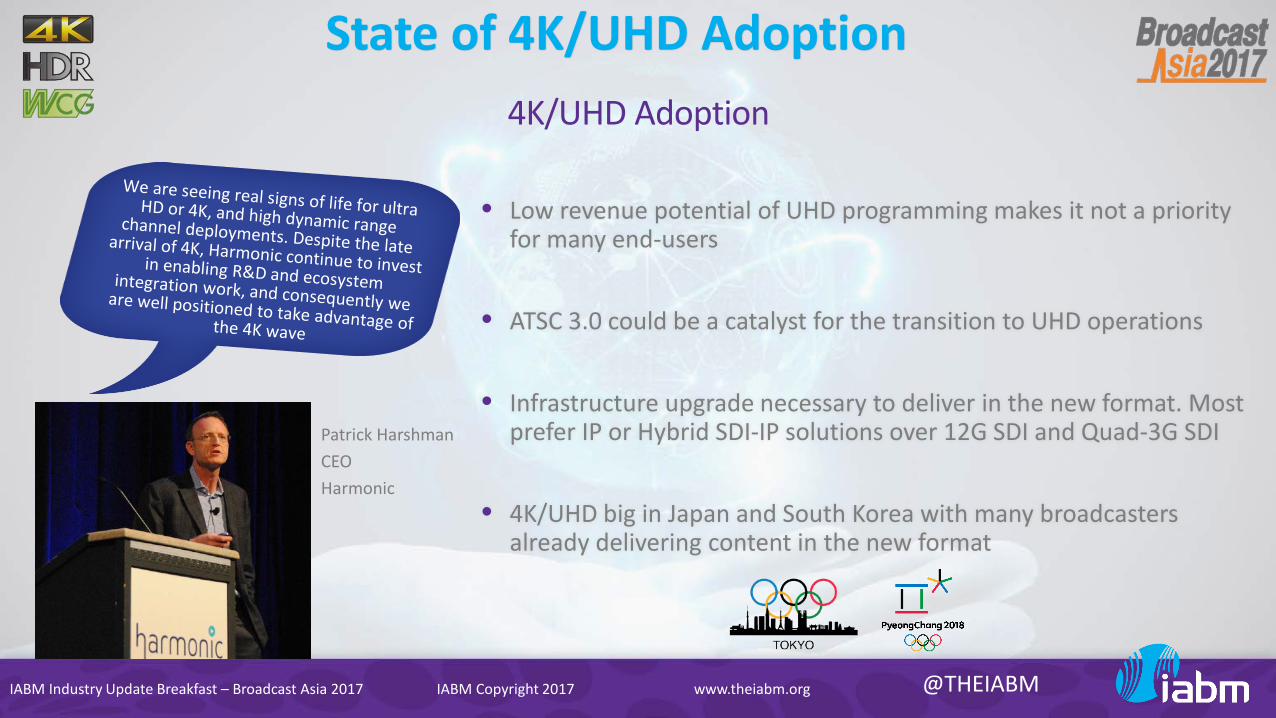

State of 4K/UHD Adoption

• Low revenue potential of UHD programming makes it not a priority for many end-users

• ATSC 3.0 could be a catalyst for the transition to UHD operations

• Infrastructure upgrade necessary to deliver in the new format. Most prefer IP or Hybrid SDI-IP solutions over 12G SDI and Quad-3G SDI

• 4K/UHD big in Japan and South Korea with many broadcasters already delivering content in the new format

4K/UHD Adoption

Patrick HarshmanCEOHarmonic

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

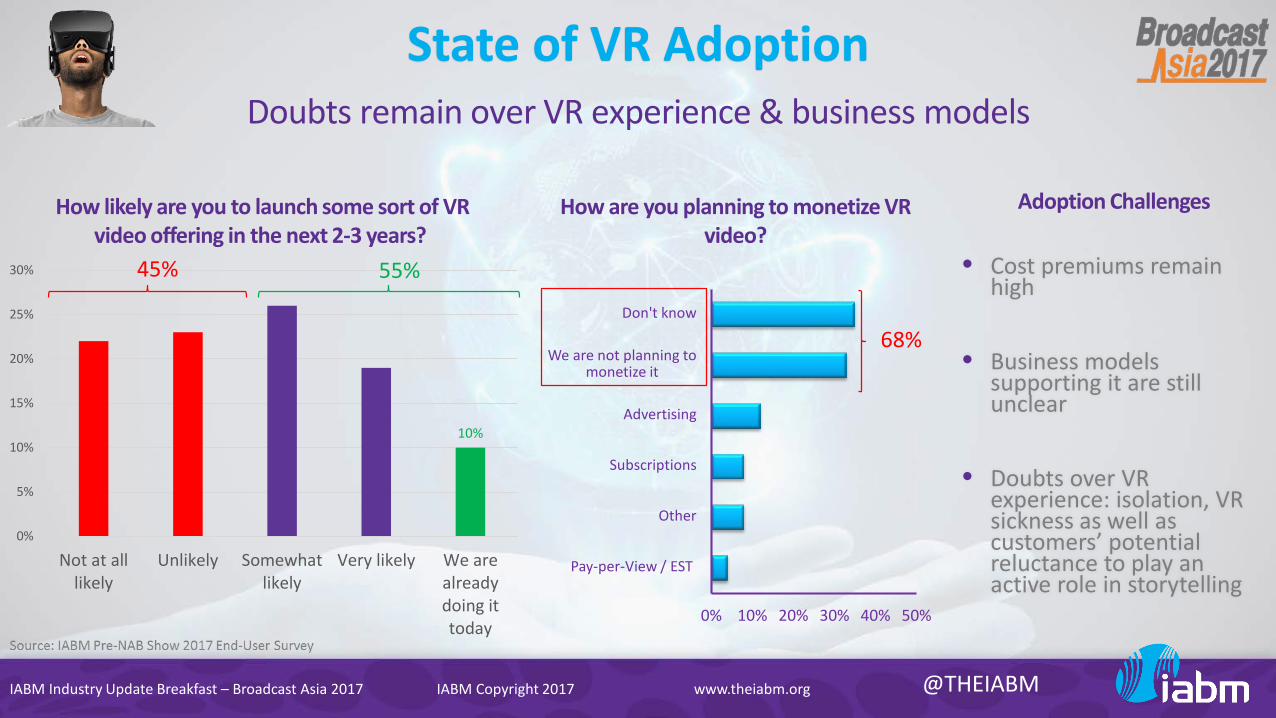

State of VR AdoptionDoubts remain over VR experience & business models

How are you planning to monetize VR video?

0% 10% 20% 30% 40% 50%

Pay-per-View / EST

Other

Subscriptions

Advertising

We are not planning to monetize it

Don't know

68%

How likely are you to launch some sort of VR video offering in the next 2-3 years?

10%

0%

5%

10%

15%

20%

25%

30%

Not at alllikely

Unlikely Somewhatlikely

Very likely We arealreadydoing ittoday

45% 55% • Cost premiums remain high

• Business models supporting it are still unclear

• Doubts over VR experience: isolation, VR sickness as well as customers’ potential reluctance to play an active role in storytelling

Adoption Challenges

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

Transition to IPTransition to IP Infrastructures

John StroupCEOBelden

Source: IABM pre-NAB Show 2017 End-User Survey

0% 5% 10% 15%

Transmitters

Production switchers

Camera lenses

Routing & networking products (IP)

Ingest / transcoding / streamingproducts

System cameras (studio / location)

Camera support & accessories

Camcorders

Workflow / asset managementsolutions

Video editing tools

0% 5% 10% 15%

Playout automation products

Library & storage managementproducts

Audio mixers & consoles

System cameras (studio / location)

Playout / transmission servers

Routing & networking products(baseband & hybrid)

Newsroom systems

Camera support & accessories

Workflow / asset managementsolutions

Routing & networking products (IP)

All Respondents Large Broadcasters

Of the products / solutions that you plan to purchase over the next 12 months, which is the most important priority? (Top 10)

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

The Importance of InteroperabilityCustomer preferences & Interoperability

Source: IABM pre-NAB Show 2017 End-User Survey

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

One stop shop "end to end" solution provider

Multiple suppliers for custom 'best of breed'

NAB 2017

IBC 2016

Customers still prefer ‘best-of-breed’ solutions

2%3%

Not at all important

Not Important

39%36%20%

Moderately Important Important Very

Important

Therefore, interoperability is important for most of them

Never, ever want to be locked in to one vendor

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

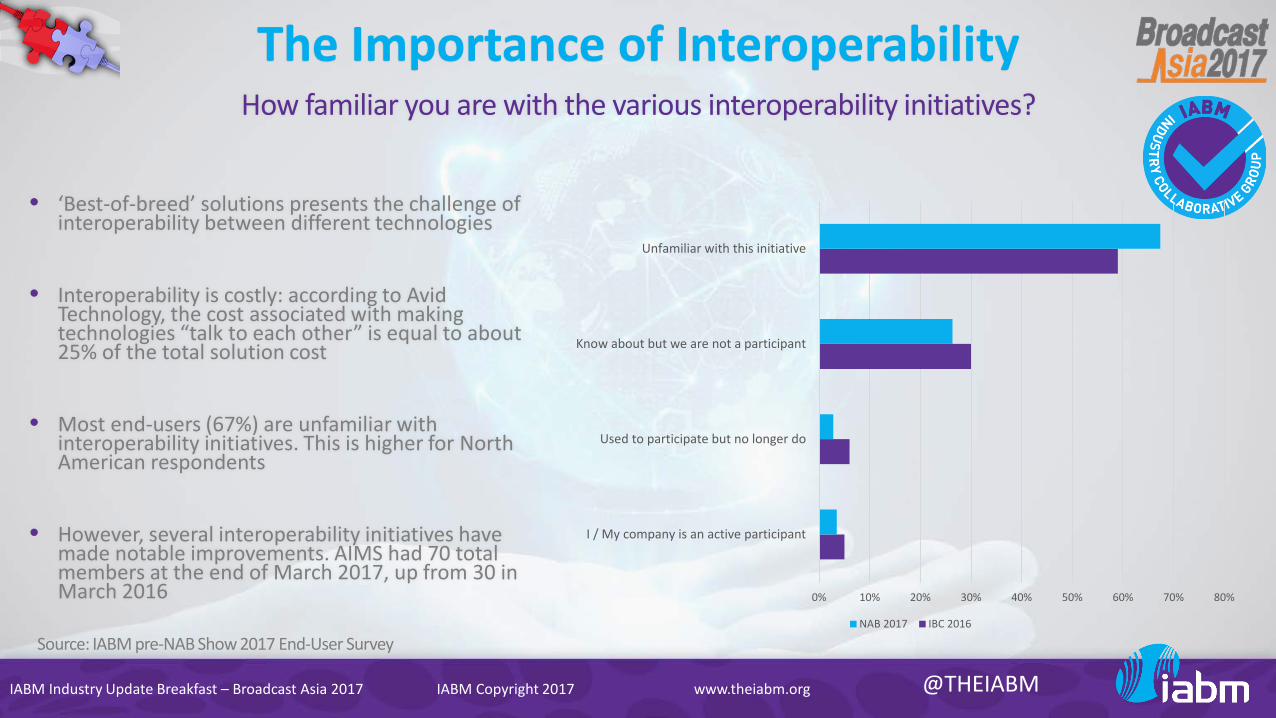

The Importance of InteroperabilityHow familiar you are with the various interoperability initiatives?

Source: IABM pre-NAB Show 2017 End-User Survey

• ‘Best-of-breed’ solutions presents the challenge of interoperability between different technologies

• Interoperability is costly: according to Avid Technology, the cost associated with making technologies “talk to each other” is equal to about 25% of the total solution cost

• Most end-users (67%) are unfamiliar with interoperability initiatives. This is higher for North American respondents

• However, several interoperability initiatives have made notable improvements. AIMS had 70 total members at the end of March 2017, up from 30 in March 2016 0% 10% 20% 30% 40% 50% 60% 70% 80%

I / My company is an active participant

Used to participate but no longer do

Know about but we are not a participant

Unfamiliar with this initiative

NAB 2017 IBC 2016

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

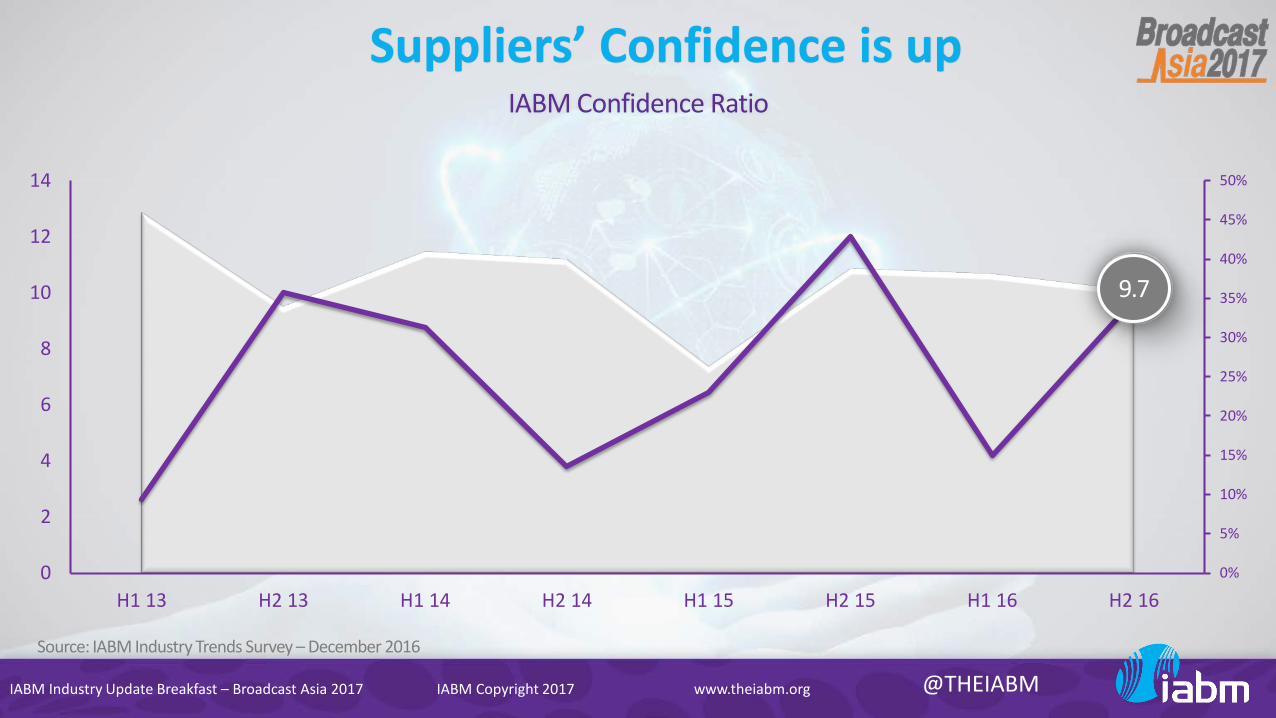

Suppliers’ Confidence is upIABM Confidence Ratio

Source: IABM Industry Trends Survey – December 2016

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2

4

6

8

10

12

14

H1 13 H2 13 H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

9.7

IABM Industry Update Breakfast – Broadcast Asia 2017 IABM Copyright 2017 @THEIABMwww.theiabm.org

But Customers remain more confidentOutlook for the business environment, Suppliers and End-Users

Source: IABM pre-NAB Show 2017 End-User Survey, IABM Industry Trends Survey – December 2016

15%

46%

33% 6%

Suppliers

25%

48%

22%4%

End-Users

Very Positive

Quite Positive

Neutral

Quite Negative

Very Negative

The State of the GlobalBroadcast & Media Industry

Peter White, CEO, IABM

IABM Industry UpdatePeter White, CEO, IABM

Peter Bruce, APAC Director, IABM