Download - Hyflux Ltd 1H FY2014 Results Review

Hyflux Ltd1H FY2014 Results Review1H FY2014 Results Review

7 August 2014

Slide 1

FORWARD-LOOKING STATEMENT

This presentation has been prepared by Hyflux Ltd for the information of the attendees of this presentation.

The presentation may contain forward-looking statements which are based on current expectations, projections and

assumptions about future events. Although Hyflux believes that these expectations, projections and assumptions are

reasonable, these forward-looking statements are subject to risks, uncertainties and assumptions about Hyflux and its

business operations that could cause actual results to differ materially from those expressed or implied by these forward-

looking statements. Such risks include industry and economic conditions; currency fluctuations between the Singapore

dollar and other currencies; governmental, statutory, tax, public policy and regulatory changes; and the continued availability

of financing in the amounts and the terms necessary to support future business.

Investors are cautioned not to place undue reliance on these forward-looking statements which are based on current views

Disclaimer

Investors are cautioned not to place undue reliance on these forward-looking statements which are based on current views

of Hyflux’s management on future events.

Any forward-looking statement in this presentation is accurate only as of the date it is issued. Hyflux has no obligation to

publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise,

except as required by law.

The presentation is not and does not constitute or form part of any offer, invitation or recommendation to subscribe for orpurchase any security and neither this presentation nor anything contained in it shall form the basis of, or be relied upon inconnection with, any contract, commitment or investment decision.

No representation or warranty express or implied is made as to, and no reliance should be placed on, the fairness, accuracy,completeness or correctness of the information or opinions contained herein. None of Hyflux Ltd or any of its affiliates,advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arisingfrom any use of this document or its contents or otherwise arising in connection with this presentation.

Slide 2

• Record PATMI of S$99.3 million in 1HFY2014

• Slower 2H expected with continued weak growth in global capital

expenditure in water projects

• Actively pursuing opportunities for large-scale water projects in the

Middle East, Africa, Asia and Latin America

Executive highlights

Middle East, Africa, Asia and Latin America

Slide 3

Revenue & profit

S$ mil 1H14 1H13 % Change

Total Revenue 169.0 262.9 (36)

Other Income 142.2 6.4 > 100

PBT 98.7 30.4 > 100

PATMI 99.3 25.7 > 100

• Revenue declined in 1H14 in line with lower engineering, procurement and

Slide 4

• Revenue declined in 1H14 in line with lower engineering, procurement and construction (EPC) activities which reflected the timing of project commencement.

• Higher Other Income and PATMI contributed by divestment of joint venture with Marmon Water LLC group in March 2014 and sale and leaseback of Hyflux Innovation Centre in June 2014.

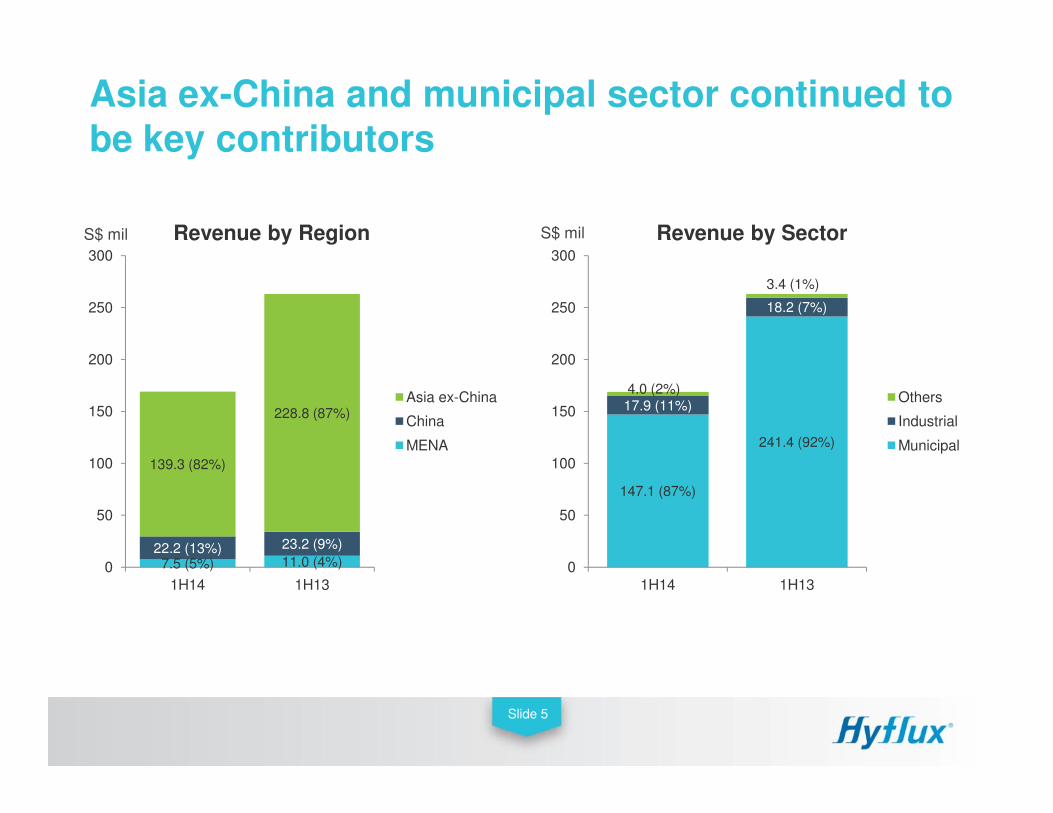

Asia ex-China and municipal sector continued to be key contributors

S$ mil S$ mil

228.8 (87%)150

200

250

300

Asia ex-China17.9 (11%)

18.2 (7%)

4.0 (2%)

3.4 (1%)

150

200

250

300

Others

Revenue by Region Revenue by Sector

Slide 5

7.5 (5%) 11.0 (4%)22.2 (13%) 23.2 (9%)

139.3 (82%)

228.8 (87%)

0

50

100

150

1H14 1H13

China

MENA

147.1 (87%)

241.4 (92%)

17.9 (11%)

0

50

100

150

1H14 1H13

Industrial

Municipal

Expenses

S$ mil 1H14 1H13 % Change

Raw Materials & Consumables 83 155 (47)

Staff Costs 38 35 10

Depreciation, Amortisation & Impairment 12 8 56

Other Expenses 55 25 > 100

Finance Costs 17 12 36

Total Operating & Finance Expenses 205 235 (13)

Slide 6

Total Operating & Finance Expenses 205 235 (13)

• Lower Raw Materials and Consumables used was in line with revenue trend.

• Increase in Depreciation, Amortisation and Impairment was mainly due to amortisation of Tuaspring Desalination Plant which commenced operations in September 2013.

• Increase in Other Expenses was primarily driven by higher utility charges from Tuaspring Desalination Plant due to the delay in the national grid connection to our power plant.

Balance sheet

S$ mil 30 Jun 2014 31 Dec 2013

Equity 1,229 886

Non-current Assets 1,814 1,776

Non-current Liabilities 978 1,150

Current Liabilities 456 360

Net Current Assets 394 261

Slide 7

Net Gearing 0.54x 1.15x

• Equity rose as a result of the S$300 million perpetual capital securities issue in January 2014 and the strong profit contribution from 1H2014.

• Shift from Non-current Liabilities to Current Liabilities due to the reclassification of a Medium Term Note that will become due in 2015.

• Net Gearing improved to 0.54 times as at 30 June 2014 from 1.15 times as at 31 Dec 2013.

Cash flow

S$ mil 1H14 1H13

Operating CF before SCA 24 10

Operating CF after SCA and tax paid (93) (222)

Investing CF 209 (7)

Financing CF 130 78

Net Cash Changes 246 (152)

Cash & Cash Equivalents 481 375

Slide 8

Cash & Cash Equivalents 481 375

SCA: Service concession arrangement

• Net cash from investing activities reflected divestment of joint venture with Marmon Water LLC in March 2014 and sale and leaseback of Hyflux Innovation Centre in June 2014.

• Cash generated from financing activities was largely from the proceeds of the perpetual capital securities issued in January 2014.

748

553

931

1,025732 682

1,500

2,000

2,500

3,000

EPC

O&M

Order book

S$ mil

2,897

2,670 2,592

1,874

1,508

1,848

1,480

1,117

30166 254 335

1,100955 943

1,872 1,938 1,910

435435

863

1,145

553

0

500

1,000

Dec 05 Dec 06 Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13 Jun 14

O&M

Slide 9

Note:

1. O&M order book is a summation of future revenues of our portfolio of plants over 20 – 30 year concession periods.

2. Jun-14 EPC order book includes Dahej Desalination project; WPA was signed in January 2013.

3. Jun-14 O&M order book includes Tuaspring and Magtaa projects.

601465

• Slower 2H expected with continued weak

growth in global capital expenditure in

water projects.

• Actively pursuing opportunities for large-

scale water projects in the Middle East,

Africa, Asia and Latin America.

Group outlook

Africa, Asia and Latin America.

• Leverage our strength across the water

value chain to pursue infrastructure

projects where water is integral to urban

planning.

Slide 10

New water projects worldwide

China

Trinidad

Slide 11

Saudi Arabia

Myanmar

India

Trinidad& Tobago

Potential projects in next 12 months in Hyflux’skey markets

Country Project Capacity (m3/day)

Saudi Arabia Al Khafji SWRO Desalination 30,000 x 2

Saudi Arabia Rabigh SWRO Phase 4 600,000

Saudi Arabia Yanbu 4 300,000

Saudi Arabia Yanbu 5 100,000

Saudi Arabia Shoaiba 4 IWPP 650,000

Saudi Arabia Khobar 4 IWPP 250,000

Saudi Arabia Khobar 5 220,000

Slide 12

Saudi Arabia Khobar 5 220,000

Saudi Arabia Jubail 4 320,000

Oman Qurayyat IWP 181,840

Oman Suwaiq IWP 227,300

Qatar Ras Laffan Industrial Desalination IWP 204,570

Kuwait Doha East 190,932

Kuwait Doha West 454,600

Source: GWI November 2013

Potential projects in next 12 months in Hyflux’skey markets

Country Project Capacity (m3/day)

Nigeria Yewa I 227,300

Nigeria Yewa II 227,300

Nigeria Ibeshe I 227,300

South Africa Cape Town SWRO 100,000

Significant opportunities in Hyflux’s key markets with estimated US$8 bn* worth of projects will be made available for tender

Slide 13

South Africa Durban SWRO 150,000 x 2

South Africa Saldanha Bay 25,500

India Chennai 3 200,000

India Chennai Nemmeli extension 150,000

Singapore Changi NEWater 228,000

Total 5,444,642

Source: GWI November 2013* Estimates based on GWI’s projected capacity, actual project value may vary.

• Raised S$475 million in perpetual capital securities in January and

July 2014

• Divested interests in joint venture with Marmon LLC and Hyflux

Innovation Centre

• Proceeds will be used for strategic investments in three main

Perpetual Capital Securities & Divestments

• Proceeds will be used for strategic investments in three main

areas:

1. Financing the Group's infrastructure projects

2. Acquiring new technology and investments in R&D

3. Expanding and automating the Group's membrane manufacturing

operations

Slide 14

0.67 0.670.70 0.70 0.70

1.0 Interim dividend per ordinary share (Singapore cents)

Interim dividend of 0.70 Singapore cents per ordinary share declared

0.0

0.5

2010 2011 2012 2013 2014

Slide 15

Slide 16

16

WATER SOLUTIONS

THAT IMPACT LIVES