A n n u a l R e p o r t 2 0 0 9G r o w i n gP a r t n e r s h i p sW o r l d w i d e

Fenner is a world leader in reinforced polymer technology.

Our strategy is to increase market share and target newvalue added product areas.

We will continue to concentrate on growing thosebusinesses where we already demonstrate leadershipthrough our skills in applications, design, materialstechnology and dedication to customer service as well asby carefully planned acquisitions.

G r o w i n gP a r t n e r s h i p sW o r l d w i d e

Contents

1 Financial Highlights

2 Chairman’s Statement

4 Business Review - ChiefExecutive Officer’s Review

1 2 Business Review - GroupFinance Director’s Review

1 5 Business Review - Definition ofKey Performance Indicators Used

1 6 The Board

1 7 Corporate Governance

2 2 Corporate Responsibility Report

2 7 Board Remuneration Report

3 4 Directors’ Report

3 8 Independent Auditors’ Report

3 9 Group Financial Statements

7 7 Independent Auditors’ Report- Company

7 8 Company Financial Statements

8 3 Five Year Summary of the Group

8 4 Annual General MeetingAdvisorsFinancial Calendar

F i n a n c i a l H i g h l i g h t s

F e n n e r p l c 1

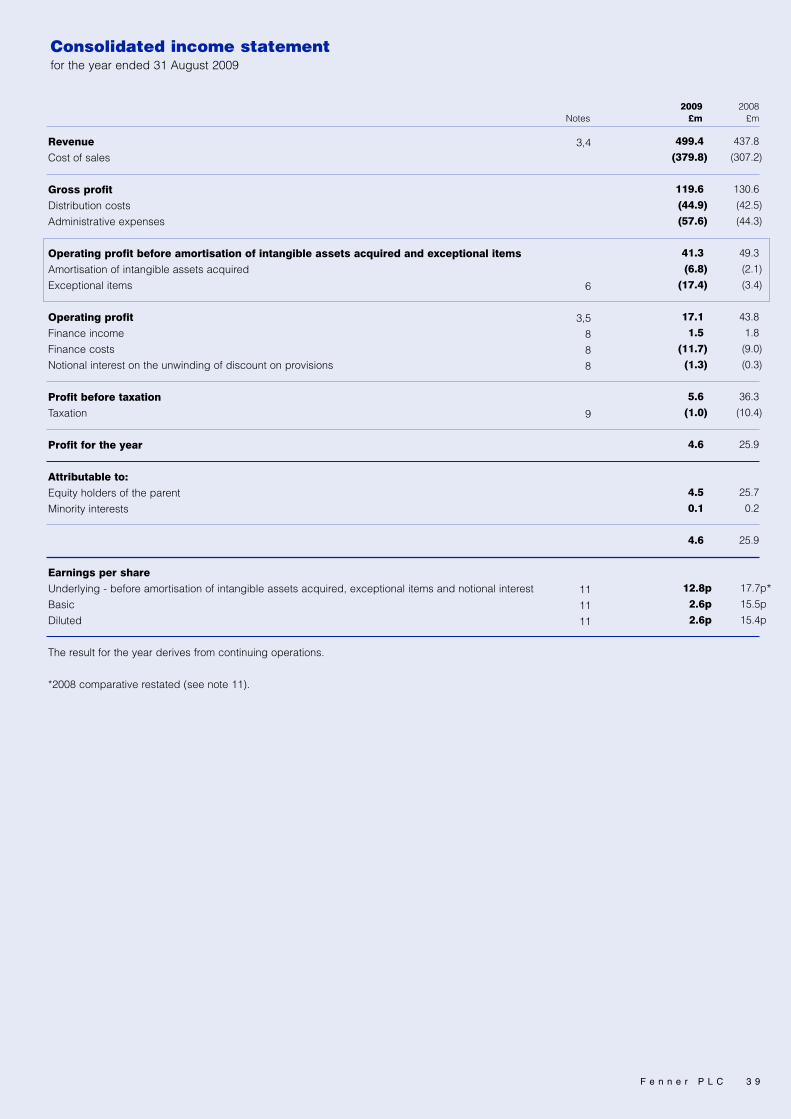

2009 2008£m £m

Revenue 499.4 437.8

Underlying operating profit 1 41.3 49.3

Exceptional items (17.4) (3.4)

Operating profit 17.1 43.8

Underlying profit before taxation 2 31.1 42.1

Profit before taxation 5.6 36.3

Underlying earnings per share 2 12.8p 17.7p

Basic earnings per share 2.6p 15.5p

Dividend per share 6.6p 6.6p

1 Underlying operating profit is before amortisation of intangible assets acquired and exceptional items

2 Underlying profit before taxation and underlying earnings per share are before amortisation of intangibleassets acquired, exceptional items and notional interest

O u r c o a l r e l a t e db u s i n e s s e s h a v ep e r f o r m e d e x t r e m e l yw e l l t o d e l i v e r g r o w t h

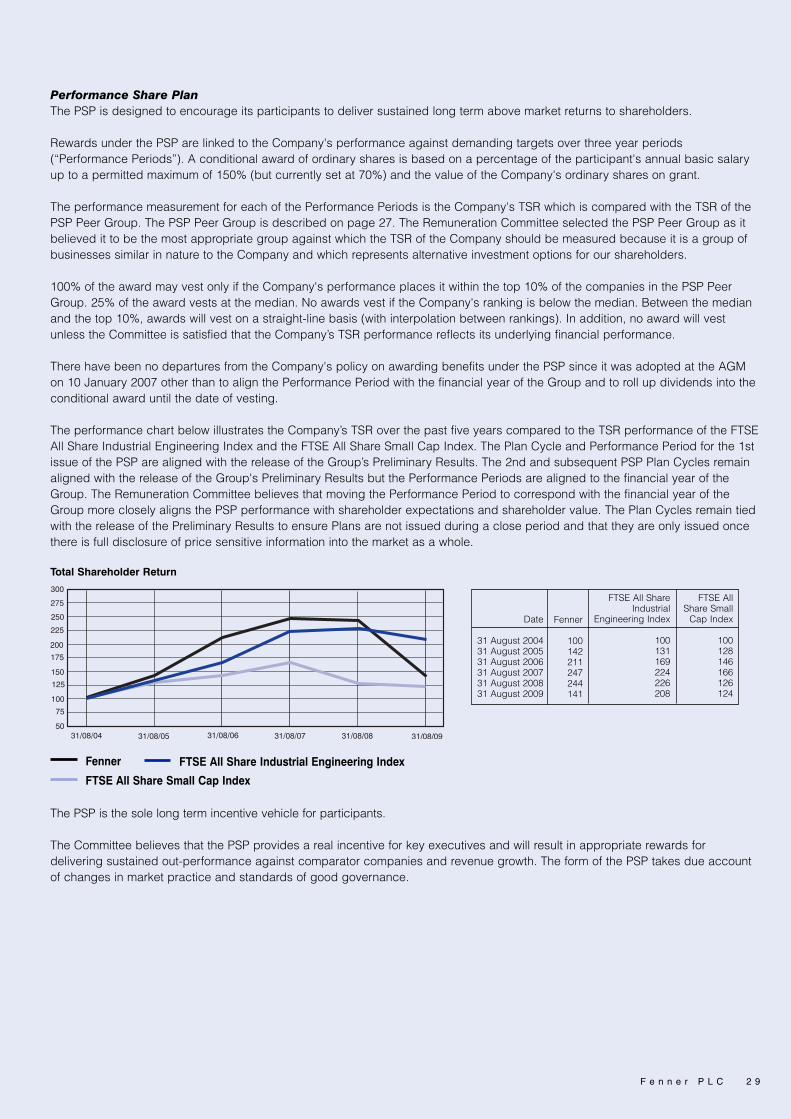

C h a i r m a n ’ s S t a t e m e n t

FINANCIAL HIGHLIGHTSRevenue increased by 14% to £499.4m(2008 £437.8m). This increase included£46.6m from the net effect of acquisitionsand disposals and £73.8m of favourablecurrency translation.

Underlying operating profit of £41.3m (2008£49.3m) held up well through the globaleconomic downturn, underpinned by thestrength of demand from the mining andmedical sectors, together with the earlyimplementation of cost reduction initiatives inthose parts of the Group which wereexposed to reduced demand levels. Thefavourable net effects of acquisitions anddisposals was £5.0m and currencytranslation was £8.5m.

Exceptional items of £17.4m (2008 £3.4m)principally comprised restructuring andreorganisation costs associated with ourmajor investment projects and downsizingcosts associated with the global economicdownturn. Regretfully, the effects of thedownturn resulted in a reduction in employeesof 832. The associated annual cost savingsare estimated to be in excess of £23.0m.Operating profit was £17.1m (2008 £43.8m).

Net finance costs increased to £11.5m (2008£7.5m), comprising £10.2m (2008 £7.2m) ofnet interest payable and a non-cash notionalcharge of £1.3m (2008 £0.3m) relating to theunwinding of discount on provisions. The

increase in interest was due to the plannedhigher level of borrowings from ourinvestment programmes and unfavourableexchange rate movements.

The headline and underlying tax rates were18% and 28% respectively. Underlyingearnings per share was 12.8p (2008 17.7p)and basic earnings per share was 2.6p(2008 15.5p).

Net cash from operating activities generated£36.4m (2008 £28.2m), assisted by stringentmanagement of working capital levels whichgenerated a cash inflow of £16.5m (2008outflow of £8.2m). Investing activities relatingto capital expenditure and acquisition ofbusinesses amounted to £71.4m (2008£104.2m). Of this amount, £37.6m wasinvested in acquisitions, principally theassets and liabilities of the ConveyorServices Corporation group of companies(Conveyor Services) and the entire sharecapital of Solid Systems Engineering, LLC(Solid Systems). Capital expenditureamounted to £34.3m of which £18.4mrelated to our recently commissioned steelcord facility in Western Australia. The effectof exchange rate movements gave rise to anincrease in debt of £21.2m. The resultant netdebt was in accordance with our forecasts at£165.4m (2008 £97.6m) which gave aheadroom of approximately £70m overavailable facilities. Interest cover was 4.0times (2008 6.8 times).

The strength of the Group’s businesses with their geographical spread has been

demonstrated throughout the year despite economic conditions unseen for many

years. Our coal related businesses have performed extremely well to deliver growth.

The industrial businesses were presented with many business challenges and

reacted swiftly where necessary to the changing environment to manage

performance levels, whilst protecting our core competencies.

2 F e n n e r p l c

None of the Group’s major committed debtfacilities are due for re-negotiation until 2012.

The Board is recommending a maintainedfinal dividend of 4.4p per share which givesa total dividend for the year of 6.6p per share(2008 6.6p).

OPERATIONSThe Conveyor Belting Division’s resultbenefited from robust demand from the coalsector, in particular the energy drivendemand for thermal coal. Our recentinvestment programmes across a network ofglobal business units has led to growth inour coal related businesses, increasedflexibility in our manufacturing choices andenhanced our ability to exceed ourcustomers’ expectations. In Asia Pacific, ourgrowth projections were exceeded throughthe continuing development of our productand service offerings across a widergeographical area. At the end of the year,another strategic milestone was completedin the development of the Division when ournew world-class manufacturing facility inWestern Australia was commissioned. Thiswill contribute to operational performance inthe current financial year. In North Americaand Europe, mining volumes were strongwhich somewhat mitigated the softerindustrial revenues experienced. In October2008, our service network was significantlyenhanced through the acquisitions ofConveyor Services and Solid Systems which,together with prior year acquisitions, are nowintegrated in the Americas as Fenner DunlopConveyor Services. These provide a platformfor growth through range extension andservice channels into both existing and newsectors.

In the Advanced Engineered ProductsDivision, the overall performance, in anenvironment severely depressed byeconomic conditions, was noteworthy withthe achievement of an underlying return onsales in excess of 11%. A strong result wasdelivered by our technical weaving businesswhich was made possible by furtherprogress in developments in the medical

sector. Elsewhere, the Division suffered fromthe effects of deteriorating economicconditions which filtered through the supplychain during the second half of the year.Downstream de-stocking activities furtherexacerbated the position with lows in thecycle seen around late spring beforelevelling out in the summer. Signs ofimprovement emerged around our financialyear end as enquiry levels started to pick up.With the cost reduction initiativesimplemented through the downturn and afocus on maintaining service levels, theDivision is well positioned to benefit from itsoperational gearing and ability to respond tocustomer demand.

PEOPLEOn behalf of the Board, I would like to thankall our employees for their continuing supportduring a period which has presented manychallenges to our businesses around theworld.

OUTLOOKEach of our businesses have restructuredcosts appropriately to meet demand levelsprevalent during the year, however, they haveretained the skills and ability to respond tothe current volume pick-up. We are seeingearly but clear signs of underlyingimprovements in our markets and thebenefits of market share gains in a numberof areas.

For several months our Advanced EngineeredProducts Division has seen benefits from theend of customer de-stocking. This iscombined with increasingly encouragingsigns that the worst effects of the recessionare behind us, although we expect growthand recovery to be slow.

Our Conveyor Belting businesses have madea positive start to the year with the prospectof Asia Pacific continuing its growth trend.

colin cooke

Chairman

F e n n e r p l c 3

Financial performance measures described as “underlying” within this statement are before amortisation ofintangible assets acquired and exceptional items and, where applicable, notional interest.

INTRODUCTION AND STRATEGYOur strategy is to increase market share andtarget new value added product areas. Wecontinue to concentrate on growing thosebusinesses where we already demonstrateleadership through our skills in applications,design, materials technology and dedicationto customer service as well as by carefullyplanned acquisitions. This common aimacross a wide range of industrial marketsgives Fenner a solid basis for long termgrowth, stability and shareholder value.Fenner is proud to be a world-class globalmanufacturer, with a strong commitment tohealth and safety, operating in key territoriesin established and emerging markets.

During the year under review, Fenner hasresponded to the global economic downturnin a swift, controlled and systematic manner.All operations that were impacted by thedownturn ensured that costs and cash werecontained by reducing headcount, strippingout non-essential expenditure, reducinginventory and ensuring both margin andmarket share were protected. None of ouroperations cut headcount beyond what wasessential to maintain a healthy business. Inmany cases we were able to retain key skillsby reducing employment costs throughsalary sacrifice, temporary lay-offs andshort-time working. This has ensured thatthe operations are well positioned to benefitfrom a subsequent improvement in theeconomy. New product developmentcontinued during the downturn as this is akey component of future growth andpositions the operations favourably againstcompetitors in our ability to servicecustomer expectations.

The Fenner Group consists of two Divisions,the Conveyor Belting (“CB”) Division and theAdvanced Engineered Products (“AEP”)Division.

Both CB and AEP provide high quality,comprehensive, whole life value products fortheir customers and both have a strongbrand and reputation in their chosenmarkets. These characteristics areconsidered to be key to the success of theGroup over its long history. Customersatisfaction is of importance to all businessunits, who ensure they are meeting theircustomer expectations which are specific toeach market. Experienced sales teamsmaintain close contact with customers,providing feedback on expectations andperformance. These qualitative indicatorsare complemented by quantitativemeasurements including customer surveysand “on time in full” performance.

As a diversified Group, Fenner uses a widerange of materials, from thousands of tonnesof rubber compound to a few hundredgrammes of metallic and polymericbiomaterials. Not only do we use significantvolumes of some materials, we also workclosely with selected suppliers to ensurethat our customers benefit from the latesttechnical developments in materials andprocesses. The majority of theserelationships are in the normal course ofbusiness, ensuring quality, continuity ofsupply and reasonable commercial terms.Where appropriate, and usually relating totechnical developments, relationships areformally documented. Operations remainvigilant to potential problems in the supplychain to ensure continued stability andcontinuity of supply.

CONVEYOR BELTINGThe CB Division is a recognised worldleader in the global conveyor belting market.It manufactures heavyweight ply, solidwoven and steel cord conveyor belting formining, power generation and industrialapplications and has growing servicebusinesses, mainly in Australia and the USA,

“We responded swiftly to the challenges of global recession whilst retaining, and in

carefully selected markets investing in, the capability and capacity to benefit fully from

the recovery.”

Mark Abrahams - Chief Executive Officer

R e s i l i e n t a n dr e s p o n s i v e

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w

4 F e n n e r p l c

F e n n e r p l c 5

Sept 09 Sept 07 Sept 08Sept 06

which install, monitor and service conveyorsystems for our mining customers.

In November 2008, following the acquisitionsof the businesses of the Conveyor ServicesCorporation group of companies and SolidSystems Engineering, LLC, Fenner DunlopConveyor Services was launched, providinga full service offering to our US coalcustomers on their conveyor systems. Inaddition to branch locations matching thoseof our US customers, we also acquired ourfirst CB business in South America which islocated in Antofagasta, Chile.

By December 2008, the two new belt lines inour Port Clinton, Ohio facility were fullycommissioned and January 2009 saw thecompletion of our weaving facility inLavonia, Georgia. These give Fennerunrivalled integrated facilities for theproduction of steel cord and rubber plyconveyor belting in the Americas.

The formal opening of our facility in Kwinananear Perth, Western Australia was in July2009. This purpose built plant houses theworld’s largest steel cord press, calenderand related equipment and is strategicallylocated to service the iron ore miners ofNorth Western Australia and elsewhere in theworld through the nearby port of Fremantle.

As expected, and illustrated by theMcCloskey graph below, energy coal pricesfell from the unsustainable levels seen in thefirst half of 2008. Whilst the fall wasprecipitous, prices did not fall below the“trigger” value at which coal companies buybelt. In recent months, prices for bothenergy coal and metallurgical coal appearto be firming. Australian export volumes inthe first eight months of the year are up onthe same period in 2008.

With the exception of those parts of theoperations which serve the industrialmarkets, CB experienced positive trading

conditions throughout the year under review;although all faced a variety of challengesincluding the effects of the lack of liquidityon customers and suppliers, competitivethreats and delays in new projects.

The Australian business has continued itsgrowth year on year. Much of this isattributable to a strong first half followed bythe implementation of the BHP Billiton ironore service contract in Western Australia.Coal and iron ore are the main tradingexports for the country and the biggestinfluence on the trading performance of ourAustralian operations and both of thesecommodities continue to have a positiveoutlook. It is widely reported that the recentround of iron ore contract negotiationsbetween Rio Tinto, Vale, BHP and Chinese /Asian steel mills are expected to set thepricing at higher levels than the long termaverage. Coking Coal with the lower pricingis once more at record production andexport levels. The Chinese have beenresponsible for much of the extra volumeuptake although India is expected to grow itscoal imports significantly.

The Australian service branches not alignedto coal and iron ore have experiencedtougher market conditions although we haveplaced our service operations in regions ofsignificant future mining growth and ensuredour belt supply offers are aligned with theneeds of our major clients. The sale ofbelting has been above budget overall and,whilst we expect competition to be tight,market share will be maintained.

The Western Australian business is now wellpositioned to be part of the fastest growingsector of the Australian economy. Theresources boom followed by the globalrecession stalled most major projects overrecent months but the second wave of newprojects is just recommencing with agrowing confidence for 2010, particularly thesecond half.

The economic downturn in the Americassignificantly impacted the trading volume inall market segments, in particular, theindustrial segment. The aggregate, cement,construction and wood products markets aredepressed by an estimated 30%-40% withlittle sign of recovery until mid 2010. Ourdistributors that service this market aretaking a conservative approach to re-stockingas cash flow is the critical component totheir survival. In this situation, our dedicationto rapid service will be a key differentiator.

NW EUROPE - STEAM COAL MARKER

MONTHLY AVERAGE

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

In the USA, most major coal miningcompanies reported strong earnings duringthe first quarter of 2009 but, due to mildweather and excessive coal stocks, havesubsequently experienced a slowdown incoal sales. Economic and meteorologicalfactors decreased electricity demandthroughout 2009, reducing demand forenergy coal which was further compoundedby historically high stocks. Together withreduced exports of metallurgical coal andlow natural gas pricing, this is expected tolead to a 5%-8% reduction in demand forcoal in the calendar year. Peabody, ArchCoal and Consol all cut production early andreport that their current capacities are soldout into 2010.

For over 50 years Fenner has manufacturedfire resistant belts to the highest standardsfor use in underground coal mines. Wewelcome the introduction in the USA of anew, higher standard of fire resistanceMSHA 30CFR14 (B.E.L.T.). From 31December 2009, conveyor belts installed inunderground mines in the USA need to bemanufactured to B.E.L.T. standard. We havesuccessfully launched the new Firebossrange of belts, including belts reinforcedwith our superior UsFlex fabric made at ourLavonia plant. The combination of the newFireboss compound and UsFlex fabric willgreatly improve the safety of the belt andimprove its durability.

Despite a drop in sales volume of industrialbelts, market share was maintained.European distributors, largely serving thesteel, cement and automotive industries,have seen a substantial drop in sales whichhas resulted in a similar drop in sales fromstock at Dunlop Conveyor Belting, based inDrachten, Netherlands. This drop was offsetto a degree by a better than averageperformance in Africa and the Middle Eastwhich, when combined with tight costmanagement initiatives, minimised theimpact.

The solid woven businesses have performedwell this year, largely due to high demandfrom both coal and potash producers in theirtarget markets. Raw material prices wereextremely volatile in the early part of theyear; in some areas the financial crisiscaused suppliers to offer large discounts,but signs towards the end of the year werepointing to a resumption of price increases.Spare capacity in India has been used tohelp meet demand elsewhere. Solid wovenbelting remains the core of the business

although the new steel cord offering in SouthAfrica is progressing well, building on theincreasing recognition of belt quality by itscustomers.

In India and China, there will be a continuedeffort to introduce heavy duty belts toappropriate customers. The Indian operationwill initially source these products from ourUK plant, leaving spare capacity which willbe used to facilitate a stronger exportoffering. In the latter case, Fenner India hasthe advantage of the ability to produce PVCbelts that meet all the relevant safetystandards throughout the world. In SouthAfrica, entry into Black EconomicEmpowerment mining juniors and non-coalapplications remains important. Theexpansion of the conveyor service offer willprove significant in a market which isincreasingly looking for total conveyormaintenance.

With ten locations throughout the USA andone in Chile, the newly formed FennerDunlop Conveyor Services offers allconveyor related needs including: conveyorbelting, conveyor components, conveyorstructures, installation, vulcanized splicing,system repairs, contract maintenance,transfer point technology, conveyor systemdesign, belt scanning, coal transport andengineering services. In addition, under thename of Classic Conveyor Components, wemanufacture and supply conveyor idlers,scrapers and structure. Based in Paonia,Colorado, LoadOut Services offers contractlabour and management to run coal washplants and train loading facilities.

ADVANCED ENGINEERED PRODUCTSThe AEP Division is divided into five productgroup businesses which are managed on aglobal basis. These businesses are:• Fenner Precision, which is a leading

supplier of performance critical polymercomponents to the office automationindustry;

• Fenner Drives, which designs,manufactures and sells an extensiverange of bespoke solutions formechanical power transmission andmotion transfer applications;

• The supply of silicone and EPDMspeciality hoses for the diesel engine,truck, bus and off-road equipment OEMmarket, trading as James Dawson;

• Fenner Advanced Sealing Technologies("FAST"), which comprises performancecritical hydraulic and pneumatic seals forthe global fluid power industry, trading

6 F e n n e r p l c

F e n n e r p l c 7

as Hallite and bespoke sealing productsfor process applications including oil andgas, electronics, pumps, valves,compressors and aerospaceapplications, trading as CDI/EGC; and

• Secant Medical, a leading developer andmanufacturer of custom-engineeredbiomedical textile structures for medicaldevices and Prodesco, providingspecialist industrial fabrics.

All operations within AEP aim to providehigh value added solutions to theircustomers’ needs using advancedpolymeric materials, expertise in applicationdesign, effective manufacturing design skillsand timely delivery. Expansion into furthermission critical applications is a key part ofthe AEP strategy as this supports the highadded value, niche nature of the productrange across the various AEP businessesand provides added protection against thefull effects of economic volatility.

All the AEP operations benefited from anoticeable flight to quality as customersbecame increasingly focused on quality,reliability and stability in the supply chainduring the year under review. Service levelshave been maintained throughout thetrading period with some of the AEPbusinesses continuing to invest in improvingcustomer service and infrastructure duringthe downturn.

The Hose business at James Dawson wasthe first of the AEP businesses to beimpacted by the global downturn as its OEMcustomer base experienced a severecontraction in the construction industry, witha subsequent and immediate reduction inthe number of off-road vehicles beingmanufactured using Dawson hoses. Thiscontraction was exacerbated by de-stockingin the supply chain, causing order levels tofall even further. Dawson responded to theslow down by controlling costs, reducing thework force and consolidating its satelliteoperation to the main facility in Lincoln,thereby streamlining production andimproving capability and efficiencies. Theproduct development team continued to bebusy throughout the period meaning thatDawson is well placed to promote hosesthat are compliant with changing emissionsregulations worldwide.

Fenner Drives and Fenner Precision werealso impacted by rapid de-stocking in theircustomer supply chains, with only a fewserved markets remaining unaffected. Both

businesses were fleet enough to counter theworst effects of the downturn by proactivelymanaging costs to enable variable marginsto be maintained. Fenner Drives enhancedits online trading capabilities andgeographic coverage, including the openingof a branch in Dubai; demonstratingcommitment behind their slogan “solvingmore problems in more places for morecustomers”. Fenner Precision completed theintegration of the Winfield acquisition,increased its Asian sales force anddeveloped new products, some for newmarkets like offshore wind farms.

The FAST businesses have enjoyed sixyears of continuous growth but saw areduction in demand for hydraulic and oiland gas equipment in the first quarter.However, the work of the preceding years toimprove production efficiencies, expand theproduct offering and increase service levelsmeant that FAST had gained market shareand did not suffer as marked a contractionin sales as many of its competitors. FASTreacted quickly to the downturn by cuttingcosts, overheads and employee numberswhilst still protecting its core businesscapability. The strategic aim of FASTcontinues to be to generate a healthy returnon sales whilst using the most advancedmaterials and technology to supply bettersolutions for performance criticalapplications ahead of its competitors. FASTcontinues to expand its global presence andmaintain its reputation for high qualityproducts.

The medical and technical textilebusinesses represented by Secant Medicaland Prodesco were not impacted as sharplyby the economic downturn and continued totrade well during the year. Furtherinvestment in the medical business tobroaden the technical capability andproduct platform is seen as a key strategyfor these businesses and continues to beprogressed as a priority. Whilst not having asignificant impact, the potential changes inUS healthcare are creating someuncertainty, however demographic trendswill inexorably increase demand over thenext 10 to 20 years.

By the end of the fiscal year, order levelshad stabilised and there are increasingsigns that de-stocking by the customer baseis coming to an end. All the businesses arepoised to take advantage of opportunities asthey arise.

SALES PER EMPLOYEE

YEAR

£’00

0

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

SUMMARY AND OUTLOOKThe last year has been one of the mostchallenging ever experienced in the face ofrapidly deteriorating economies around theworld. However, the robustness of ourstrategy has enabled us to demonstrate ourresilience with roughly half of the Group stillgrowing in this tough environment. Theother half, which was adversely impacted bythe economy, responded incisively andswiftly to realign its cost base whilstretaining our long term values of safety,customer service and product development.

This has left the Group very stronglypositioned to benefit from the recovery,although we expect the speed of anyimprovement in demand will vary across ourend markets.

EMPLOYEESIn this period of economic uncertainty, allbusiness units have managed costsproactively throughout the year. Difficultdecisions have been made promptly whichhas, unfortunately, led to the elimination ofmore than 800 jobs, approximately 20% ofthe total workforce. In addition, a largeproportion of the remaining workforce hasparticipated in short-time working, salarysacrifice or temporary lay-off programmes.These actions made a significantcontribution to maintaining variable marginsclose to prior year levels across the Groupas a whole.

By the end of 2009, our North AmericanService business had increased itsheadcount by almost 400 through theacquisition of the Conveyor ServicesCorporation group of companies and SolidSystems Engineering, LLC.

Overall, the Group headcount fell by closeto 400 during the year.

Productivity is a key factor to success. Dueto the increasing diversity of our operations,productivity for the Group as a whole is bestmeasured by total sales per employee.

The graph shows that, despite the growth inour service businesses, which generateslower sales per employee than ourmanufacturing businesses, and the globalrecession, sales per employee has beenmaintained at last year’s level.

All our businesses have processes thatrequire high levels of proficiency andtechnical expertise and Fenner continues tobenefit from a skilled and committedworkforce in both our acquired and existingbusinesses. We acknowledge theimportance of our employees’ contribution tothe performance of the Group.

HEALTH AND SAFETYThe Group is growing. That growth bringswith it greater responsibilities and greaterexpectations from our customers,employees and neighbours. We live in aworld of continuous improvement and healthand safety is no different in this regard; toachieve our goals we need to embed rigourand continuous improvement in the way weapproach health and safety. Fenner looksfor, and promotes, health and safety as akey element in the culture of each of itsbusinesses. The Health & SafetyManagement System Framework (“TheFramework”) is a set of Expectations whichwill help both individuals, business units andnew acquisitions understand what isrequired of them. It provides structure andguidance to all operations, irrespective ofsize, to deliver outstanding performance,protecting their unique culture andautonomy.

In order to implement The Framework, eachbusiness unit initially assesses its currentlevel of compliance with the Expectations,taking into account their operational riskprofile and the applicable regulatoryrequirements. The unit then develops animprovement plan which can incorporateand build on their existing health and safetymanagement programmes. Plans, and theprogress against those plans, are monitoredand updated annually and will be subject toindependent assessment.

Given the challenges set by the 89Expectations, it is envisioned that our wellestablished operations will take two to threeyears to fully implement The Framework andup to five years for some of our acquiredbusinesses.

An increasing number of our employeeswork on customers' sites and job safetyassessments are mandatory prior to work

8 F e n n e r p l c

100

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

105

110

115

120

125

130

F e n n e r p l c 9

commencing. For these businesses, ourhealth and safety management systems area significant unique selling proposition. Accidents and near misses are recordedand reviewed operationally and safesystems of work updated if necessary.Accidents involving lost time are reportedthrough divisional management and up tothe main Board. The process for sharing thedetails of an incident and the measurestaken around Group operations to preventsimilar accidents elsewhere has beenformalised and extended to includeguidance on wider health issues with abusiness impact, including swine flu.

The absolute number of lost time incidents("LTIs") is the KPI chosen to measure thesuccess of our health and safety policy. Theselection of an absolute measure across thewhole Group, which does not reflectchanges in employee numbers or hoursworked, demonstrates our belief thateveryone who works for Fenner shouldreturn home in the same fit and healthy statein which they came to work. We aredelighted to report that in such a difficultyear our LTIs have fallen to 81. The followinggraph shows the results over the last sixyears:

Also shown by the blue line is the number ofLTIs per 200,000 hours worked (“LTIFR”).Even with The Framework maintaining focuson health and safety, delivering continuousimprovement year on year is challenging,particularly as our operations respond toincreasing demand with higher output andadditional working hours.

ENVIRONMENTThe Group is committed to identifying andassessing the risks of pollution and otherforms of environmental impairment arisingout of its activities. We seek to reduce ourimpact on the environment to the lowestpractical levels and with each newinvestment, ensure that we exemplify thebest contemporary practice in respect of theenvironment. At Board level, the ChiefExecutive Officer has specific responsibility

for the development of policy andmanagement systems. Responsibility forenvironmental matters in each operatingdivision is designated to the DivisionalManaging Director and, at a local level, to asenior manager on each site. EachDivisional Managing Director is required toreport to the Board on a regular basis and toadvise the Board immediately of anyenvironmental risks or other incidents likelyto be significant to the business. No newrisks or incidents were reported to the Boardin the last year.

All acquisitions are subject to appropriateenvironmental due diligence which isspecifically extended to includeenvironmental management systems andoperational compliance. Given that therecent acquisition activity has given us anadditional 15 sites in the USA of a size thatcannot support specialist environmentalknowledge, we have, with our advisors,devised an assessment questionnaire toensure any issues identified at acquisitionare addressed and continuing compliance isensured.

Compliance with applicable regulatorystandards is a minimum which is subject toofficial audit; larger facilities validate theirmanagement systems by independent audit.Despite restraints on cost and staffreductions, progress continues onenvironmental management systems and wenow have eight sites implementing ISO14001 with one already accredited and theother seven scheduled for accreditation overthe next two years.

A small number of business units continueto assess their carbon footprint with a viewto seeing if some meaningful actions canresult from such measures and to preparefor, or comply with, local requirements.Although within the UK and other jurisdictionsa local consensus is developing, carbonfootprint estimates are not yet a validconsistent measure comparable across thewide range of sizes, technologies andlocations of the Group’s units. However, wehave now established a baseline for allenergy sources used in manufacturing at alevel of detail which will enable theintroduction of an appropriate standardwhen identified.

In the UK, work has been undertaken inresponse to the Carbon ReductionCommitment scheme (“CRC”), a keycomponent of the Climate Change Act. TheCRC is a UK based carbon trading scheme

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

40

20 0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

60

80

100

120

LTIs

LTI LTIFR

LTIF

R

LOST TIME INCIDENTS

YEAR

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

affecting large organisations that willcommence in 2010. We have undertakensite surveys at our major UK manufacturingfacilities to determine the energy baselinefor the trading scheme. We are alsopursuing an application to join a ClimateChange Agreement hosted by the BritishPlastics Federation, which will identifyenergy saving potential in each location anddraw up a plan for implementation.

In addition to our environmentalresponsibilities, there are sound commercialreasons to minimise and recycle waste. As amanufacturing Group, the obvious focus is onraw materials as the reduction opportunitiesare well known and, for the residual waste,recycling is well understood. We are workingto develop consistent and comparablereporting to capture data on all significantwaste generated throughout the Group. Air quality can be adversely affected bysome of our processes and significantinvestment and maintenance costs areincurred to ensure this does not happen.A number of locations use processes whichinvolve a range of chemicals which aregenerically referred to as volatile organiccompounds (“VOCs”). These chemicals aresubject to strict regulation with their storageand use carefully controlled. In addition tominimising any emissions to air of VOCs,potential substitutes are assessed as soonas they become commercially available.

The majority of the Group’s businesses haveoccupied their sites for many years, somefor over 100 years. The Group thereforerecognises and manages risk of exposure toenvironmental legacy issues.

Fenner continues to be committed toundertaking regular reviews of its activitiesand the workings of the environmental policyto ensure that it is comprehensive andeffective, identifying objectives andstandards that will enable a demonstrablecontinuous improvement in environmentalmatters.

PRINCIPAL RISKS AND UNCERTAINTIES Fenner considers the following to be themost significant risk factors for Fenner toconsider, but the risk factors listed do notnecessarily comprise all those associatedwith Fenner and are not set out in anyparticular order of priority.

Additional risks and uncertainties notpresently known to Fenner or that Fennercurrently deems immaterial may also havean adverse effect on its business.

Strength of key marketsAlthough there are signs that the globalrecession may be over, many marketsremain weak and we expect the recovery tobe slow. However, Fenner is well positionedto benefit from the underlying volume growthin energy markets, particularly oil and coaland recovery in industrial markets. AlthoughFenner has successfully traded throughprevious cycles, a substantial downturn inone or more of these key markets couldhave a material adverse impact on thebusiness. Fenner continues to look foropportunities that are counter cyclical tohelp balance out any market downturn.

Fluctuations in raw material costs andavailabilityVolatility in raw material costs continues tobe a key risk for the Group as there is adirect impact on the costs of production andmanaging customer expectation. The Groupcontinues to manage raw material costs. Forexample, where materials are a significantcost of sale, we have long term supplyagreements and arrangements which aredriven by the constraints of the markets intowhich we sell. However, increases in suchcosts could have a material adverse impactupon the Group’s profitability and cash flowif such increases cannot be recoveredthrough increased sales prices.

In addition, liquidity problems can adverselyaffect the availability of materials with limitedsources of supply. All business units havebeen assessing their exposure and, wherenecessary, have approved, or continue towork on approving, alternative sources.

Climate changeIn the run up to the United Nations ClimateChange Conference in Copenhagen,increasing media attention is being given toclimate change and the political will to actappears to be responding to that coverage.Fenner takes full account of the substantivepublicised research in evaluating itsstrategic projects. In advance of theCopenhagen negotiations, the InternationalEnergy Agency recently released their 450Scenario which sets out a policy frameworkand the impact on power generation todeliver a long term greenhouse gasconcentration of 450ppm CO2 equivalent,less than half the level that would be emittedunder current policies. Even under the 450Scenario, coal fired power generation willincrease over the next 20 years.

1 0 F e n n e r p l c

F e n n e r p l c 1 1

Fluctuations in foreign currencyDue to the global nature of the Group,Fenner derives a large proportion of itsrevenues from overseas and hence has anexposure to foreign currency fluctuations.Whilst the Group seeks to reduce this riskthrough formal contracts and borrowings,adverse movements in foreign currencies,particularly the US dollar relative to sterling,could lead to material adverse movementsin reported earnings.

CompetitionProducts are available which competedirectly or indirectly with the Group’sproducts. New technology, changingcommercial circumstances and new entrantsto the markets in which the Group operatesmay adversely affect the Group’s business.One source of competition comes from thelow cost economies but whilst these cancompete on price, they cannot alwayscompete on quality or service. Aggressive orpredatory pricing from competitors couldlead to a reduction in margin or volume.

Dependence on key personnelThe future success of Fenner is dependenton the continued services of key personnel.Although the Group has succession plansand seeks to develop and promote fromwithin, the loss of the services of theexecutive officers of the Group and otherkey employees could have a materialadverse affect on the business.

Fluctuations of revenues, expenses andoperating resultsFenner’s revenues, expenses and operatingresults could vary from period to period as aresult of a variety of factors, some of whichare outside Fenner’s control. These factors,which are actively monitored andconsidered in all relevant managementdecisions, include general economicconditions, adverse movements in interestrates, conditions specific to the energymarkets, seasonal trends in revenues,capital expenditure, other costs and theintroduction of new products by Fenner or itscompetitors.

In response to a changing competitiveenvironment, Fenner may elect from time totime to make certain pricing, service ormarketing decisions or acquisitions thatcould have a material adverse effect on theGroup’s revenues, results of operations andfinancial condition.

Employee benefit schemesThe Group has a number of employeebenefit schemes, including defined benefitpension schemes and US healthcareprogrammes. These schemes expose theGroup to changes in interest rates, otherinvestment returns and inflation as well asthe effects of the longevity of schememembers. Developments in medical scienceand changes in healthcare managementcan significantly increase the cost ofmaintaining benefits in the future.Appropriate financial and legal advice istaken on the rules and funding of all suchschemes. Changes in regulatory oversighthave resulted in increased costs andmanagement time without any real benefitsfor our employees.

FORWARD-LOOKING STATEMENTSCertain statements contained in thisdocument, including those under thecaptions “Summary and Outlook” and“Principal Risks and Uncertainties”,constitute forward-looking statements. Suchforward-looking statements involve risks,uncertainties and other factors which maycause the actual results, performance orachievements of Fenner, or industry results,to be materially different from any futureresults, performance or achievementsexpressed or implied by such statements.Such risks, uncertainties and other factorsinclude, among others: growth in the energymarkets, general economic conditions andthe business environment.

Mark Abrahams

Chief Executive Officer

B u s i n e s s R e v i e wG r o u p F i n a n c e D i r e c t o r ’ s R e v i e w

ACCOUNTING POLICIESThe Group financial statements have beenprepared in accordance with the accountingpolicies described in note 1 to the Groupfinancial statements, in accordance withIFRS as adopted by the European Union.

The Company financial statements havebeen prepared in accordance with theaccounting policies described in note 1 tothe Company financial statements, inaccordance with UK GAAP.

REVENUE AND OPERATING PROFITGroup revenue increased by 14% to£499.4m (2008 £437.8m). Of this increase,£46.6m was generated from the full yeareffect of prior year acquisitions and disposalsand current year acquisitions. The effect offavourable exchange rate movementsamounted to £73.8m, the largest componentrelating to the weakening of sterling againstthe US dollar.

In the CB Division, revenue increased to£361.8m (2008 £292.2m). Mining marketsremained strong and our service networkwas significantly enhanced throughacquisition activity in North America.

In the AEP Division, revenue decreased to£137.6m (2008 £145.6m) due to its greaterexposure to industrial segments and theimpact upon them from the global economicdownturn.

Underlying operating profit reduced to£41.3m (2008 £49.3m). The net effect ofacquisition and disposal activity contributed£5.0m and the favourable translation effectof exchange rate movements was £8.5m.Divisional profits contributed were £30.8m(2008 £29.1m) from the CB Division and£15.8m (2008 £26.1m) from the AEPDivision.

Exceptional items incurred amounted to£17.4m (2008 £3.4m), the largest componentrelating to global restructuring activitiesassociated with the economic downturn. Seenote 6 to the Group financial statements forfurther details of exceptional items.

Amortisation of intangible assets acquiredincreased to £6.8m (2008 £2.1m) due to thefull year effect of acquisitions in the prior yearand acquisitions completed during the year.

Group operating profit reduced to £17.1m(2008 £43.8m).

INTERESTNet interest payable was £10.2m (2008£7.2m). The increase in the net chargereflected the growth in net debt as a resultof the planned acquisitions and capitalexpenditure. The weakening of sterlingduring the year increased the cost on thetranslation of foreign currency denominatedinterest, albeit mitigated by reductions inshort-term interest rates.

In addition, notional interest on theunwinding of discount on provisionsincreased to £1.3m (2008 £0.3m) due to theincrease in contingent deferredconsideration on acquisitions.

TAXATIONThe underlying tax rate was 28% (200830%). The reduction in the rate reflected agreater proportion of profits generatedoutside the USA where tax rates aregenerally lower and tax assets, includinglosses, and tax holidays have been utilised.

The headline rate of tax of 18% (2008 29%)principally reflected the higher rate of taxrelief in the USA for exceptional itemsincurred in that territory.

EARNINGS PER SHARE AND DIVIDENDSUnderlying earnings per share was 12.8p(2008 17.7p) and basic earnings per sharewas 2.6p (2008 15.5p).

The interim dividend of 2.2p per share (20082.2p) was paid on 7 September 2009. TheBoard is recommending a final dividend of4.4p per share (2008 4.4p) to make a totaldividend for the year of 6.6p per share(2008 6.6p).

ACQUISITIONS AND DISPOSALSThe Group completed two acquisitionsduring the year and one after the year end.One non-core product line was divestedduring the year.

In October 2008, the assets and liabilities ofthe Conveyor Services Corporation group ofcompanies, including LoadOut Services,were acquired. The consideration paidduring the year amounted to £30.1m,including acquisition costs, and outstandingcontingent and deferred considerationpayable is estimated at £17.3m.

Also in October 2008, the entire sharecapital of Solid Systems Engineering, LLCwas acquired for £5.4m plus deferredconsideration estimated at £1.3m.

1 2 F e n n e r p l c

F e n n e r p l c 1 3

As required under IFRS, a review of the fairvalue of assets and liabilities wasundertaken at the dates of acquisition. Thisresulted in a provisional fair value of netassets acquired of £42.8m. This amountcomprises the valuation of separatelyidentifiable intangible assets of £31.0m,which include trade names and customerrelationships that will be amortised over theireconomic lives, and other net assetsacquired of £11.8m. Goodwill of £9.1m hasbeen recorded which comprises £11.4m foracquisitions in the year less £2.3m from there-assessment of contingent deferredconsideration on prior year acquisitions.

Further acquisition disclosures are given innote 33 to the Group financial statements.

In March 2009, a non-core product line inAEP which generated small revenue streamswas disposed of for an initial considerationof £0.1m with deferred amounts of £0.4m.

In September 2009, after the year end,certain business assets and liabilities of BeltService Srl were acquired for an initialconsideration of £0.2m with deferredamounts of £0.5m. The business, located inItaly, further strengthens our conveyorbelting service network in Europe.

CASH FLOW, NET DEBT AND FINANCINGNet cash from operating activities increasedto £36.4m (2008 £28.2m), benefiting fromstringent working capital controls throughthe economic downturn. The reduction inworking capital levels generated cash of£16.5m (2008 cash outflow of £8.2m).

Capital expenditure reduced to £34.3m(2008 £63.7m). The major spend during theyear related to the strategic investment in anew steel cord facility in Western Australia.This compares to a depreciation charge of£15.0m (2008 £10.1m). After disposing ofplant and equipment of £0.1m (2008 £0.5m),the free cash inflow was £2.2m (2008outflow of £35.0m).

The net outflow on acquisition and disposalactivity was £37.2m (2008 £41.0m). Dividendspaid of £11.5m (2008 £9.9m) and an outflowfrom other financing activities of £0.1m(2008 inflow of £35.5m, principally relating toa share placing) gave an increase in netdebt before the effects of exchange ratemovements of £46.6m (2008 £50.4m). Thetranslation effect of a weakening of sterlingincreased this amount by £21.2m (2008£10.9m) which resulted in an increase in netdebt of £67.8m to £165.4m (2008 £97.6m).

Gross debt at the year end amounted to£200.4m (2008 £141.2m). Cash andshort-term deposits at the year end were£35.0m (2008 £43.6m).

The Group is financed principally by a mixof equity, retained earnings, US dollarprivate placement loan notes and committedbank facilities. The principal loan facilitiesare raised centrally whilst operatingcompanies supplement this funding withlocal overdraft and working capital facilities.

At the year end, the Group's committedbank facilities primarily consisted of a£100m revolving credit facility with three UKbanks which expires in June 2012. Inaddition, the Group's Australian operationshad committed bank borrowings ofAustralian $35m (£18.1m) which expire inMay 2013.

The Group's other principal source ofcommitted debt financing remain two USdollar private placements. $90.0m (£55.2m)of Senior Notes repayable in June 2017carry a fixed interest coupon of 5.78% and$20.4m (£12.5m) of Senior Notes repayablebetween 2010 and 2012 carry a fixedinterest coupon of 7.29%.

In addition to its undrawn committedfacilities at the year end of £12.4m (2008£51.3m), the Group has access toapproximately £50m of uncommittedworking capital facilities.

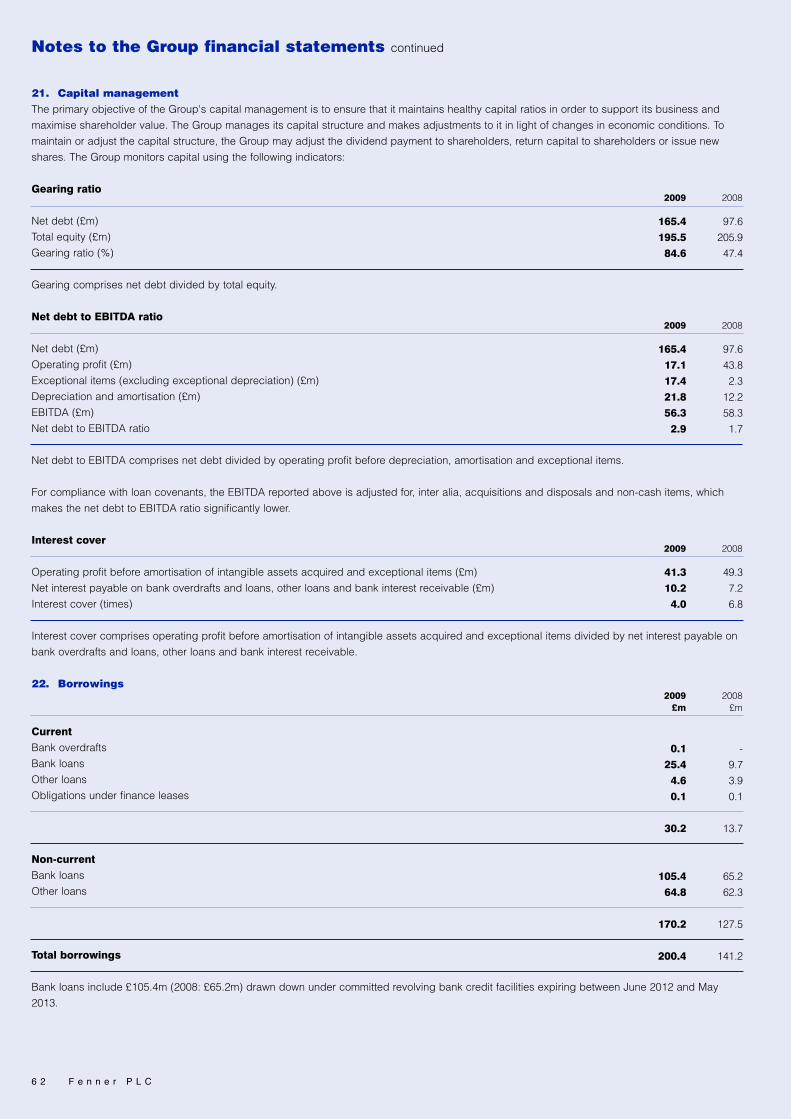

The financial covenants relating to thecommitted bank facilities and the 2017private placement are aligned. The principalcovenants are interest cover - underlyingoperating profit being at least 2 times thenet interest charge, and the net debt toEBITDA ratio - net debt being less than 3.5times adjusted EBITDA.

At 31 August 2009, the Group comfortablycomplied with its loan covenants. Interestcover was 4.0 times (2008 6.8 times) whilstnet debt to reported EBITDA was 2.9 times(2008 1.7 times). In addition, for compliancewith loan covenants, reported EBITDA isadjusted for, inter alia, acquisitions andnon-cash items, thus the net debt toadjusted EBITDA ratio is significantly lowerwhen adjusted for these items.

The Group remains well placed to fund andsupport its operations, with continuingaccess to medium and long term debtfinance, cash resources and, wherenecessary, shorter term facilities.

B u s i n e s s R e v i e wG r o u p F i n a n c e D i r e c t o r ’ s R e v i e w c o n t i n u e d

1 4 F e n n e r p l c

FINANCIAL RISK MANAGEMENTIn the normal course of business, the Groupis exposed to certain financial risks,principally foreign exchange risk, interestrate risk, liquidity risk and credit risk. Theserisks are managed by the central treasuryfunction in conjunction with the operatingunits, in accordance with risk managementpolicies that are designed to minimise thepotential adverse effects of these risks onfinancial performance. The policies arereviewed and approved by the Board.

The exposures are managed through theuse of foreign currency and sterlingborrowings, derivatives and creditmanagement procedures. The use ofderivatives is undertaken only where theunderlying interest or currency risk arisesfrom the Group’s operations or sources offinance. No speculative trading inderivatives is permitted.

In the normal course of business, derivativeshave been used to hedge future non-functionalcurrency cash flows arising from tradingtransactions relating to the sale and purchaseof goods and services. The Group haschosen not to hedge account for suchtransactions under the requirements of IAS39 ‘Financial Instruments: Recognition andMeasurement’, recognising that cash flowsthrough to the maturity of the derivative areunaffected. In compliance with IAS 39, allfinancial instruments have been measuredat their fair value as at the balance sheetdate. A charge or credit to the incomestatement has been recognised for the lossor gain on these instruments. In addition, inaccordance with IAS 21 ‘The Effects ofChanges in Foreign Exchange Rates’, allforeign currency monetary items have beenre-translated at the closing rate, withchanges in value charged or credited to theincome statement.

The interest rate swap to hedge interest ratecash flows, entered into in 2006, continuedduring the year. This instrument fixes theinterest rate on $40m of floating rate bankborrowings until 2011. At 31 August 2009,the fair value of this instrument was a liabilityof £2.5m (2008 £1.5m). In 2007, the Groupalso swapped $27.2m of the 2017 privateplacement into €20.0m, with cash flowsmirroring the private placement at a fixedrate of 5.05%. This swap matures in June2017 when the private placement isrepayable. At 31 August 2009, the fair valueof this instrument was a liability of £0.9m

(2008 £0.3m). These swaps have beenaccounted for as hedges in accordance withIAS 39, with the charge or credit recogniseddirectly in equity.

RETURN ON GROSS CAPITAL EMPLOYEDThe average gross capital employedincreased due to the effect of the Group’sstrategic expansion plans to £379.2m (2008£266.9m) and underlying operating profitamounted to £41.3m (2008 £49.3m),adversely affected by the economicdownturn. As a consequence, the return ongross capital employed reduced to 11%(2008 18%).

POST-RETIREMENT BENEFITSThe Group operates a number of definedbenefit post-retirement schemes for qualifyingemployees in operations around the world.

The principal scheme is the Fenner PensionScheme which is based in the UK. The mostrecent triennial valuation of the FennerPension Scheme was carried out as at 31March 2008. The total defined benefitpost-retirement liability, as calculated by theschemes' actuaries in accordance with IAS19 'Employee Benefits' and recorded on thebalance sheet at 31 August 2009, increasedto £42.1m (2008 £19.1m). Of this amount, theFenner Pension Scheme represents £37.6m(2008 £15.5m) and the overseas schemestotalled £4.5m (2008 £3.6m). During the year,the fair value of assets of the schemesreduced by £5.8m and the present value ofrecognised obligations increased by £17.2m,principally as a result of a reduction incorporate bond yields used to discountobligations. Further details of post-retirementbenefits are disclosed in note 25 to the Groupfinancial statements.

KEY FINANCIAL PERFORMANCEINDICATORS

Richard perry

Group Finance Director

2009 2008

Adjusted earnings per share 12.8p 17.7p

Interest cover (times) 4.0 6.8

Net debt to EBITDA (ratio) 2.9 1.7

Return on gross capital employed 11% 18%

Financial performance measures described as “underlying” within this statement are before amortisation ofintangible assets acquired and exceptional items and, where applicable, notional interest.

. F e n n e r p l c 1 5

B u s i n e s s R e v i e wD e f i n i t i o n o f K e y P e r f o r m a n c e I n d i c a t o r s U s e d

INTERNATIONALLY TRADED COAL PRICESAs published by, and used with thepermission of, the McCloskey GroupLimited, the coal industry recognised marketanalysis and trade reporting company.These bi-weekly prices reflect the deliveredto port price of coal for the two major coalimporting markets.

SALES PER EMPLOYEETotal annual third party revenue at constantexchange rates divided by the averagenumber of employees derived from a simpletotal head count with no distinction betweenfull time, part time, temporary or casualemployees. Where employees are employedfor part of a year, the average number iscalculated on a pro-rata basis.

LOST TIME INCIDENTSThe number of incidents connected withwork which results in an injured personbeing away from work or unable to do thefull range of their normal duties, notincluding the day of the incident.

LOST TIME INCIDENT FREQUENCYThe Lost Time Incident Frequency Rate(“LTIFR”) is the number of Lost TimeIncidents per 200,000 hours worked.

UNDERLYING EARNINGS PER SHAREThis is a measure of performance andgrowth. It is calculated by dividing theunderlying profit for the year by theweighted average number of shares in issueand ranking for dividend.

INTEREST COVERThis measure provides an indication ofwhether the Group’s profit is sufficient tocover its interest obligations. It is calculatedby dividing the underlying operating profitby net interest payable on bank overdraftsand loans, other loans and bank interestreceivable.

NET DEBT TO EBITDAThis is a measure of the Group’s ability toservice its debt obligations. It is calculatedby dividing net debt, defined as short andlong term borrowings less cash andshort-term deposits, by the profit for the yearafter adding back net finance costs,taxation, depreciation, amortisation andexceptional items.

RETURN ON GROSS CAPITAL EMPLOYEDThis is a measure of performance relative toamounts invested. It is calculated bydividing underlying operating profit by grosscapital employed. Gross capital employed isdefined as the average of the opening andclosing non-current assets (excludingdeferred tax), inventories, trade and otherreceivables and trade and other payables.

T h e B o a r d

Appointed in May 1993 as executive Chairmanand became non-executive Chairman in May1994. He is also non-executive Chairman ofAltitude Group plc and non-executiveChairman of Energybuild Group Plc.

Appointed to the Board as Group FinanceDirector in 1990 and became Chief ExecutiveOfficer in May 1994. He is also non-executiveChairman of Inditherm plc and non-executivedirector of The Leeds Teaching HospitalsNHS Trust.

Appointed to the Board in September 1994.He is also a non-executive director of ScapaGroup plc.

Appointed to the Board in January 2003, hewas formerly an executive director ofD S Smith Plc.

Appointed to the Board in November 2005,he was formerly Chief Executive of BritishVita plc and is a non-executive director ofZotefoams Plc.

Joined the Company in 2001 and wasappointed Company Secretary in July 2002.

COLIN COOKE (69)* r n

Chairman

MarK abrahaMs (54) n

Chief Executive Officer

rIChard PErry (59)

Group Finance Director

daVId bUTTFIELd (63)* a r n

Senior Independent Director

daVId CaMPbELL (59)* a r n

dEbra bradbUry (44)

Company Secretary

* Non-executive a Audit Committeer Remuneration Committeen Nomination Committee

1 6 F e n n e r p l c

F e n n e r p l c 1 7

The Group remains committed to maintaining high standards of corporate governance as set out in the Combined Code onCorporate Governance (“Combined Code”), revised in June 2008. A copy of the Combined Code is available from the FinancialReporting Council or online at www.frc.org.uk.

Compliance with the Combined CodeThe Group has complied with the provisions of the Combined Code during the year ended 31 August 2009 and this statementexplains how the Principles of Corporate Governance are applied within the Group. It should be read in conjunction with theBusiness Review and the Board Remuneration Report on pages 4 to 15 and pages 27 to 33 respectively.

The BoardAs at 31 August 2009, the Board comprised a non-executive Chairman, two executive directors and two non-executive directorsand is collectively responsible to shareholders for the proper management of the Group. Biographical details of the directors areset out on page 16.

The roles of the Chairman and Chief Executive Officer are separate and distinct from one another in accordance with best practice.

The Board is satisfied that it has met the Combined Code’s requirements for its effective operation. Specific matters are reserved forthe Board’s consideration under a formal schedule. These include developing Group strategy, reviewing trading performance,considering senior management appointments, formulating policy on key issues (including the approval of significant capitalexpenditure, acquisitions and disposals) and reporting to shareholders. The schedule is reviewed at least annually. Various othermatters are delegated to duly authorised sub-committees of the Board consisting of directors and senior executives. Details of theircomposition and purpose are outlined below. In addition, the Chairman and non-executive directors meet several times a yearwithout the executive directors being present.

All directors are subject to election by shareholders at the first Annual General Meeting ("AGM") following their appointment and tore-election thereafter at intervals of no more than three years. Due to his length of tenure, the Chairman seeks annual re-election inaccordance with best practice.

The Group holds appropriate Director’s and Officer’s liability insurance.

Board balance and independenceThe Board is satisfied that the current balance of skills and experience continues to be appropriate for the requirements of thebusiness. Over half of the Board comprises non-executive directors, inclusive of the Chairman, and they are deemed by the Board tobe independent of management and do not have any business relationships which could interfere with the exercise of their judgement.

The Senior Independent Director is David Buttfield.

Information and professional developmentPrior to each Board, Committee or General Meeting, the Board is provided with timely, appropriate and sufficient information toenable it to discharge its duties proficiently. The Board also receives appropriate documentation, financial information, regulatoryupdates and briefing notes on a regular basis to ensure it is kept fully informed and up to date.

Non-executive directors receive an induction to the Group and its operations when they are appointed to the Board. They are alsoencouraged to visit the Group’s offices and factories whenever the opportunity presents itself, where they meet management andare briefed on local business operations. At least one Board meeting during the year is held at an operational site outside of theUK, although this was deemed inappropriate in the year under review whilst the operations were rationalising costs in response tothe global economic downturn.

All directors have access to the Company Secretary, who is responsible for ensuring that Board procedures are followed and thatthe Group complies with all applicable rules, regulations and obligations governing its operations. A procedure exists for directorsto take independent professional advice, if necessary, at the Group’s expense, in the furtherance of their duties.

Performance evaluationA Board performance evaluation was carried out in the year which comprised of a questionnaire. The review looked at Boardresponsibilities, duties, strategy, information flows, monitoring, Board structure including sucession planning and the effectivenessof the whole Board and its committees. The performance of the Chairman was also evaluated by the Senior Independent Directorafter a review with the other members of the Board. The Chairman evaluated the performance of the individual directors as part ofthe review. It was concluded that the composition, experience and effectiveness of the Board was appropriate and robust and nosignificant issues were raised during the evaluation.

Corporate Governance

ConflictsThe Company amended its Articles in January 2009 to deal with, amongst other things, the provisions on conflicts of interest in theCompanies Act 2006 which came into force in October 2008. No conflicts arose during the year and the Board continues to monitorevents with a view to ensuring any conflicts are handled appropriately.

Audit CommitteeThe Audit Committee comprises the two non-executive directors and is chaired by David Buttfield, who has recent and relevantfinancial experience. The Company Secretary acts as a secretary to the Committee. In undertaking its duties, the Committee hasaccess to the services of the Group Finance Director and the Company Secretary as well as access to external professional advice.The Committee has the power to request the attendance at meetings of any director, external auditor, internal auditor or Groupemployee as considered appropriate. The Committee also meets external auditors without the executive directors being present.

The principal duties of the Committee are to monitor the integrity of the financial statements, to review the internal controls and riskmanagement systems, to review the work of internal audit and to consider all aspects of the relationship with the external auditors.The Committee has the authority to obtain external legal or other professional advice on any matter within its terms of reference.

The work of the Audit CommitteeDuring the year, the Committee carried out the following work:

- review, prior to Board approval, of the Preliminary and Half Year Results, the Annual Report and the Half Yearly FinancialReport;

- consideration of the Group’s key business risks, including the arrangements for the identification and management of risk;- overseeing the implementation of a Group-wide risk management system;- receive the reports on internal control and review the effectiveness of the internal control function and arrangements, monitor

progress and evaluate the internal control reports at least twice a year, including a meeting with the Head of Internal Control;- meet with the external auditors, both with and without the executive management being present, to discuss audit issues;- approve the external auditors' terms of engagement and associated fees;- monitor the level of non-audit work of the external auditors;- review the terms of reference of the Audit Committee and the Whistleblowing Policy; and- review the financial statements of the UK Fenner Pension Scheme.

No non-routine matters of concern were drawn to the Committee’s attention by either the external or internal auditors during theyear. Matters of material concern are immediately drawn to the Committee’s attention if and when they arise.

There is a policy on the provision of non-audit services by the external auditors. Certain services such as due diligence in relationto acquisitions and disposals, taxation services and actuarial advice are permitted but others, for example, internal audit,information technology and HR consultancy are generally considered inappropriate. Non-audit fees are reported to the Committee.

The Committee has received and reviewed written confirmation from the external auditors on all relationships that, in theirjudgement, may bear on their independence. The external auditors have also confirmed that they consider themselves independentwithin the meaning of UK regulatory and professional requirements.

Audit Committee and internal controlThe Audit Committee reviews the effectiveness of the Group’s system of internal control and receives a report on internal control atleast twice a year. This review covers all controls, including operational, financial, compliance and risk management.

In accordance with the requirements of the Combined Code and the recommendations of the Turnbull Guidance on internal control,the directors have reviewed the effectiveness of the internal control system and arrangements. During the period under review, nosignificant changes to the material risks were identified and no control failings or weaknesses were identified that resulted inunforeseen material losses.

The directors are responsible for the Group’s system of internal control which, like any system of internal control, can only providereasonable and not absolute assurance against material misstatement or loss.

The key procedures within the control structure are: - the identification of major business and insurance risks faced by the Group’s operations, by both the Board and senior

management, and the determination of the most appropriate course of action to deal with these risks; - central review and approval procedures in respect of major areas of risk such as acquisitions and disposals, litigation,

treasury management, taxation and environmental issues; - a clear management structure with well defined lines of responsibility and the appropriate levels of delegation; - regular review of the Group’s business units by operational and executive management and monthly reports from the

Divisional Directors;

1 8 F e n n e r p l c

Corporate Governance continued

F e n n e r p l c 1 9

- a structured process for appraising and authorising capital projects, which includes clearly defined authorisation levels.Projects are subject to post-investment appraisals;

- well established consolidation and reporting systems for both the statutory and monthly management accounts, with allBoard members receiving a monthly statement of the financial results;

- comprehensive budgeting systems with an annual budget approved by the Board. Monthly results are reported againstbudget and revised forecasts for the year are prepared regularly;

- an internal programme of monitoring visits by the internal audit team, as agreed with the Audit Committee, reviews thecompliance of each business unit with the Group's standard internal financial control procedures;

- competition compliance programmes are in place in several jurisdictions and the Group-wide Whistleblowing Policycontinues to be applied; and

- a programme of business risk reviews with operational management focusing on non-financial controls and riskmanagement.

Remuneration CommitteeThe Remuneration Committee comprises the Chairman and the non-executive directors and is chaired by David Campbell. TheChief Executive Officer also attends the meetings by invitation but does not participate in any decision in relation to his ownremuneration. The Committee has the power to request the attendance at meetings of any director or Group employee asconsidered appropriate.

The Committee is responsible to the Board for determining the remuneration packages of the executive directors and other seniorexecutives and advises on executive remuneration policy issues. The Committee administers the long term Performance Share Plan(“PSP”) and the expired Long Term Share Incentive Plan (“LTIP”). It also approves the granting to certain employees of a long termShadow Performance Share Plan which is a cash incentive scheme with performance aligned to the PSP.

The Remuneration Committee received advice during the year from Hewitt New Bridge Street Consultants LLP (“HNBSC”), whoadvised the Committee in relation to director and senior executive remuneration and the PSP. MM&K Ltd assisted the Committee inconsideration of matters in relation to the expired LTIP which ended in November 2008.

Nomination CommitteeThe Nomination Committee comprises the Chairman, the non-executive directors and the Chief Executive Officer. The Committee ischaired by the Chairman and generally meets at least annually and/or as required. The Committee has the power to request theattendance at meetings of any director or Group employee as considered appropriate.

Terms of reference set out the Committee’s role and duties which include reviewing the composition of the Board, havingresponsibility for the identification and nomination of candidates to fill Board vacancies and considering succession planning for allBoard positions and senior executives.

Candidates for appointment to the Board are considered by the Committee, taking advice from external consultants whereappropriate.

Meetings of the BoardThe attendance of each director at Board, Audit Committee, Remuneration Committee and Nomination Committee meetings is setout below.

Number of meetings during the year

Chairman C I Cooke

Executive directorsM S Abrahams

R J Perry

Non-executive directorsD F Buttfield

D A Campbell

* By invitation

6

6

6

6

6

6

Board

3

3*

3*

3*

3

3

Audit Committee

RemunerationCommittee

2

2

2*

0

2

2

1

1

1

1*

1

1

NominationCommittee

Terms of referenceThe terms of reference of the Audit, Remuneration and Nomination Committees are reviewed at least annually and are available toview on the Group’s website at www.fenner.com or upon request to the Company Secretary.

Executive CommitteeThe Executive Committee is chaired by the Chief Executive Officer and consists of the two executive directors, the CompanySecretary and five members of the Group’s senior management including senior executives from the operations. The ExecutiveCommittee meets at least six times a year and deals with the daily management of the Group through powers delegated to it by theBoard. Two strategic planning days were held in the year in addition to the routine Executive Committee meetings.

Directors' remunerationPolicy and procedure are set out in the Board Remuneration Report on pages 27 to 33.

Relations with shareholdersThe Company encourages regular dialogue with its institutional shareholders inclusive of client brokers and also with privateinvestors at the AGM. The Chief Executive Officer and Group Finance Director hold update meetings with institutional shareholdersand private client brokers following the announcement of Preliminary and Half Yearly Results and as requested throughout the year.The Chairman and non-executive directors are offered the opportunity to attend meetings with major shareholders and attend ifrequested. There were no requests received from shareholders for meetings with the Chairman or non-executive directors in theyear.

The Board is provided with broker reports and feedback from shareholder meetings on a regular basis.

The Group’s website provides comprehensive investor relations information for shareholders to view. The website includes analystpresentations, the current share price, regulatory announcements, financial performance information, shareholder information andan investor relations contact address.

Annual General MeetingIn relation to the Company’s AGM:

- proxy forms allow for voting either for a resolution, against a resolution or for a vote to be withheld;- a separate resolution is proposed for each substantially separate issue, including the receipt of the Annual Report;- the proxy count in respect of each resolution is announced after it has been dealt with on a show of hands;- all executive and non-executive Board members normally attend the meeting;- the Notice of Meeting, the Annual Report and any other related papers are normally sent to shareholders more than one

month before the meeting; and- shareholders are invited to ask questions during the AGM and have an opportunity to meet the Board directors before and

after the formal meeting.

Statement of directors’ responsibilitiesThe directors are responsible for preparing the Annual Report, the Board Remuneration Report and the financial statements inaccordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Under that law the directors haveelected to prepare the Group financial statements in accordance with International Financial Reporting Standards (“IFRS”) asadopted by the European Union and the parent company financial statements in accordance with United Kingdom GenerallyAccepted Accounting Practice (United Kingdom Accounting Standards and applicable law). Under company law the directors mustnot approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Groupand the Company and of the profit or loss of the Group for that period. In preparing these financial statements, the directors arerequired to:

- select suitable accounting policies and then apply them consistently;- make judgements and accounting estimates that are reasonable and prudent;- state whether IFRS as adopted by the European Union and applicable United Kingdom Accounting Standards have been

followed, subject to any material departures disclosed and explained in the Group and parent company financial statementsrespectively; and

- prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company willcontinue in business.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Company’stransactions and disclose with reasonable accuracy at any time the financial position of the Company and the Group and enablethem to ensure that the financial statements and the Board Remuneration Report comply with the Companies Act 2006 and, as

Corporate Governance continued

2 0 F e n n e r p l c

F e n n e r p l c 2 1

regards the Group financial statements, Article 4 of the IAS Regulation. They are also responsible for safeguarding the assets of theCompany and the Group and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the Company’s website. Legislation in the United Kingdomgoverning the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

Each of the directors, whose names and functions are listed in The Board on page 16 confirm that, to the best of their knowledge:

- the Group financial statements, which have been prepared in accordance with IFRS as adopted by the European Union give a true and fair view of the assets, liabilities, financial position and profit of the Group; and

- the Business Review contained on pages 4 to 15 includes a fair review of the development and performance of the businessand the position of the Group, together with a description of the principal risks and uncertainties that it faces.

Going concernAfter making enquiries, the directors have formed a judgment at the time of approving the financial statements that there is areasonable expectation that the Company and Group have adequate resources to continue in operational existence for theforeseeable future. For this reason, the directors continue to adopt the going concern basis in preparing the financial statements.

C I Cooke Chairman11 November 2009

2 2 F e n n e r p l c