Download - GlobalOutlook

Page 1 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

14 January 2014

Financial Markets Research

Monthly Outlook January 2014

Beginning of the end / Jan Lambregts +44 207 664 9669 An increasingly positive macro backdrop and a bit more cooperation between Democrats and Republicans, finally saw

the Fed confident enough to commence tapering last month. It was a cautious first reduction of only USD 10 billion, so

the Fed’s still pushing USD 75 billion a month into the market, but it was a beginning nevertheless.

The market’s reaction, including emerging markets, has been rather subdued. In particular when compared to the fall-

out earlier last year. That will have a lot to do with the extensive campaign the Fed’s been waging to explain the

difference between tapering and tightening, as well as the firm forward guidance that rates are to remain low for the

foreseeable future. Even the tapering itself is likely to be a very gradual affair. Indeed, working off the base of an

ongoing moderate recovery, we think the Fed will not conclude tapering until year-end 2014.

It’s hard to see the Fed easily diverge from this gradual path. Various Fed speakers have begun to talk about economic

growth hitting 3% or higher in 2014 (Rabobank forecast: 2.8%), so if that’s the basic scenario in their mind, growth

would have to overshoot/undershoot considerably to speed things up/slow things down.

The good news for the ECB is that policymakers can finally emerge from the shadows of Fed tapering speculation and

find it easier to differentiate themselves in the eyes of the market as the central bank that hasn’t embarked on a

“tightening” course, mostly using beefed up forward guidance. We saw a first start of that at the January press

conference and it could be more successful this time around, in particular if the ECB is able to juxtapose it with an

improving economic backdrop.

Page 2 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Contents United States 3

Cautious taper steps 3 Well past the time… 3

Eurozone 4

Beefed-up forward guidance… 4 … as the domestic economy shows more signs of

recovery 4 Further disinflation remains a risk 4

Japan 5

12 months of Abenomics and what do we get? 5 ...another year older and further in debt? 5 2014 is likely to be a critical year for Japan 5

United Kingdom 6

Gaining momentum 6 Housing market remains strong 6 Bank of England outlook 6

Switzerland 7

A good year for the Swiss economy 7 SNB still struggling with internal and external

factors 7

The Netherlands 8

A strong start of 2014 8 Household consumption keeps falling 8 Manufacturing production declines 8

Poland 9

Non-inflationary economic recovery continues 9 Zloty at risk at New Year opening, medium-term

prospects remaining upbeat 9

Hungary 10

Back on the growth path 10 Forint remains under pressure at the year opening 10

Russia 11

Economic slowdown may continue in 2014 11 Ruble ends the year with annual losses although

with a more optimistic outlook at 2014 opening 11

China 12

Debt data suggest hangover to follow the party 12 The provinces are in the red even despite huge

fiscal transfers 12 When the music stops, so will a lot of investment

spending 12

Australia 13

RBA putting the house on a recovery... 13 ...and it may well need to... 13 ...as The Year of the Horse presents its hurdles 13

Brazil 14

Why Ms Rousseff will probably be re-elected 14

Foreign Exchange 15

EUR/USD: battle of the Titans 15 EUR/JPY: further gains in store 15 EUR/GBP: Carney confidence 15

Fixed Income 16

Significant peripheral spread narrowing... 16 ...but how far could this move go? 16 And a trade? 16

Credit Markets 17

The temptation to follow the herd 17

Financial Forecasts 18

Page 3 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

United States

Cautious taper steps

Now that the impact of the fiscal cliff and the sequester is fading and

the two main political parties appear to have signed a truce, at least

until the November elections, the economic outlook has improved.

Employment growth shifted into higher gear, unemployment fell

substantially, and that induced the Fed to announce the first taper of

USD 10bn at the December meeting. At the same time, the central bank

stressed that it is in no hurry to terminate QE3 altogether or to hike the

fed funds target rate. Bernanke said that the FOMC expects similar

moderate taper steps at further meetings. What’s more, if economic

data are disappointing, the Committee may skip a meeting or two.

However, the tapering process could also be speeded up on the back of

stronger-than-expected data. Currently, Bernanke expects QE3 to end

late in the year. Our baseline forecast is that the FOMC will decide to

end QE3 in December 2014, after tapering by USD 10bn at each

meeting (except for a final USD 5bn at the December meeting). Last

Friday’s disappointing nonfarm payrolls may have raised the risk of a

slower taper schedule, but we think that one data point is not sufficient

to throw the FOMC off course. What’s more, it is also a rather unclear

data point, because the exact impact of the bad weather remains

uncertain.

Well past the time…

Meanwhile, the Fed seems to have been successful in convincing the

markets that the decision to start tapering does not mean that the first

policy rate hike is around the corner of 2014, dampening the upward

impact on longer-term rates of its December decision. In fact, the

forward guidance on the federal funds target rate was strengthened:

the FOMC now expects to start hiking well past the time the

unemployment rate declines below 6.5%, especially if inflation remains

below the 2.0% target. In fact, the Committee discussed lowering the

unemployment threshold to 6.0%, but the majority decided against it

because that would hurt the Fed’s credibility. But in practice, we should

probably pay more attention to the 6.0% level than the 6.5%. Our

forecast is that the unemployment rate will drop below 6.0% in 2015Q3

and that the FOMC will decide to announce its first hike in December

2015. The next FOMC meeting on 28-29 January will be Ben Bernanke’s

last. His term expires at the end of the month and in February his

number two, Janet Yellen, will take over. While Bernanke has managed

to launch the taper before his departure, the actual exit strategy will be

left for Yellen. A major challenge is to keep the markets convinced that

there will be a substantial delay between the end of QE3 and the start

of the hiking trail. This may require further strengthening of forward

guidance.

Chart 1: Inflation

Source: Macrobond

Chart 2: Unemployment

Source: Macrobond

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 2.8 1.9 2.8 2.5 4.1 2.6 2.9

Consumption 2.2 2.0 2.2 1.8 2.0 2.5 2.0

Business inv. 7.3 2.7 5.2 4.7 4.8 4.9 5.0

Residential inv. 12.9 13.6 10.9 14.2 10.3 12.0 11.0

Government -1.0 -2.2 -0.6 -0.4 0.4 -4.0 2.0

Trade 0.1 0.2 0.2 -0.1 0.1 0.9 0.1

Inventories 0.2 0.1 0.2 0.4 1.7 -0.2 0.1

CPI (% YoY) 2.1 1.5 1.6

Unemp. %rate 8.1 7.4 6.6

Yearly ("in") Quarterly (ar)

Source: Rabobank

/ Philip Marey +31 30 216 9721

Page 4 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Eurozone

Beefed-up forward guidance… In the January press conference, ECB President Draghi firmed up the

forward guidance language: “[…] the Governing Council strongly

emphasises that it will maintain an accommodative stance of monetary

policy for as long as necessary […] Accordingly, we firmly reiterate our

forward guidance that we continue to expect the key ECB interest rates to

remain at present or lower levels for an extended period of time.” He then

underscored that the Governing Council “remain[s] determined to

maintain the high degree of monetary accommodation and to take further

decisive action if required.” The timing for this change in language did

not come entirely unexpected. Now that the Fed has initiated a

tapering cycle and economic data are slowly improving, a firming up of

its language is likely to be more successful than during much of 2013

when it was ill striving against the stream for the ECB. This is largely

because the ECB’s forward guidance is conditional and asymmetric in

nature. By talking dovish amidst improving conditions the ECB can

finally distinguish itself from other central banks, the Federal Reserve in

particular, even as the latter has retained a dovish stance. Overall, we

expect the ECB to maintain policy in the coming months. But it is likely

to act quickly if there is any discernible deterioration in either the

growth, inflation or money market outlook. The March meeting (when

it publishes fresh staff projections) is likely to be our next reality check.

… as the domestic economy shows more signs of recovery

Draghi has clearly indicated that the Governing Council will resist

tightening action even when the economy continues to recover. On

that note, perhaps the most encouraging news is that it is domestic

demand that appears to be strengthening, notably in the periphery.

Figure 1 shows the impressive acceleration in retail sales growth in the

periphery, albeit from a low base. Recent data for retail sales, consumer

confidence and retail surveys suggest that overall eurozone

consumption expanded at a pace of around 0.2% QoQ in Q4.

Unemployment remains at a high level, but appears close to stabilising.

In the medium-term the low inflation environment should support a

gradual recovery in consumer spending. Meanwhile, business surveys

also point to a somewhat stronger pickup in investment spending

growth than we had previously pencilled in. The credit environment,

deleveraging pressures and government finances are likely to keep a lid

on the economy’s growth potential for a protracted period of time,

however. We have slightly upped our 2013Q4 growth forecast.

Further disinflation remains a risk

The elephant in the room is inflation and President Draghi has signalled

that the Governing Council will not accept a significant deterioration in

the medium-term outlook. We would stress that recent declines in core

inflation have been partly driven by technical factors and indirect taxes

falling out of the comparison base. Super-core inflation (Figure 2) has

not shown a discernible downward trend since end-2012. We expect

headline inflation to move within a fairly narrow range over the next six

months (between 0.8% to 1%), but a persistent fall below it may spur

the ECB into action again. Initially this would likely be a combination of

liquidity measures and a further beefing-up of the forward guidance.

We remain sceptical of negative deposit rates, conditional LTROs and

asset purchases (particularly at his stage), but – clearly - nothing can be

excluded should deflation risks be seen as being on the up.

Chart 1: Retail sales growth: core vs. periphery

-10

-8

-6

-4

-2

0

2

4

6

05 06 07 08 09 10 11 12 13

%Y

oY

core periphery

Source: Macrobond, Rabobank

Chart 2: Core and super-core inflation

Source: Macrobond, Rabobank

Table 1: Economic forecasts

2012 2013 2014 Q3/13 Q4/13 Q1/14 Q2/14

GDP -0.6 -0.4 1.0 0.1 0.3 0.3 0.2

Consumption -1.4 -0.5 0.5 0.1 0.2 0.1 0.1

Investment -3.9 -3.1 1.6 0.4 0.5 0.3 0.4

Government -0.6 0.2 0.3 0.2 -0.1 0.1 0.2

Trade 1.7 0.6 0.2 -0.4 0.1 0.1 0.0

Inventories -0.6 -0.1 0.2 0.3 0.0 0.0 0.1

CPI (%y-o-y) 2.5 1.4 1.2 1.3 0.8 0.9 1.0

Unemp. %rate 11.4 12.1 12.2 12.1 12.2 12.2 12.2

Yearly Quarterly

Source: Rabobank

/ Elwin de Groot +31 30 216 9012

Page 5 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Japan

12 months of Abenomics and what do we get? The start of 2014 is a good time to assess what the “Abenomics

revolution” has actually delivered after 12 months. The short answer is

some growth, but not a sustainable economic recovery. Let’s start with

the good news. Chart 1, which rebases its key data series back to 100 in

January 2005 (with the exception of CPI on the right axis), shows that

the Nikkei is much higher than it was at the start of 2013 (it was up

72.5% in 2013); moreover the JPY, in nominal effective terms, is hugely

weaker (USD/JPY was down 21.5% in the year). That momentum has

also led to a positive momentum in some sectors of the real economy:

the Tankan survey for large manufacturers is now rising steadily and is

at a level as last seen back in 2007. Perhaps most encouragingly for the

BoJ, however, is that CPI has also leaped higher on the back of the weak

JPY: in November headline CPI was 1.6% YoY – higher than in the

Eurozone - while even core CPI was up 0.5% YoY (again catching up

with Europe). So, if we were to finish the story there we could conclude

that massive QE and massive fiscal deficits, together with currency

depreciation, still work as an economic panacea.

...another year older and further in debt?

Except they don’t. Crucially, despite a weak JPY the trade deficit

continues to widen. This is not just due to a “J-curve” (where a weak

currency pushes up the import bill before a substitution effect kicks in)

as there are no real alternatives for Japan’s imports of energy and raw

materials. Instead there is a strong correlation between FDI outflows

from Japan and the trade deficit. In short, Japan’s industrial base is

gradually shifting to mainland Asia to chase the expanding market

there. Unless the JPY makes Japan cheaper to produce than Indonesia

and Thailand, for example, that trend is unlikely to be reversed. As a

parallel, while machine orders have picked up they still remain far

below their 2005 level, let alone the peak they reached in 2007, and the

same is also true for industrial production. However, perhaps most

concerning is the continued decline in real wages. While inflation is to

be welcomed in a deflation-prone economy it does little good to

households unless they receive pay rises to match – and so far they

clearly are not doing so. Those consumers lucky enough to be able to

live on their equity portfolios are seeing a huge boost to their wealth;

those living on their salaries are seeing their incomes reduced. (In a

recent discussion I was asked if higher CPI would not be beneficial for

households, in that it would help deflate away their mortgage debts. I

replied that it doesn’t make one feel better off if the mortgage only

seems smaller measured against a basket of consumer goods that are

also increasingly unaffordable!) Meanwhile, Abenomics has also done

nothing yet to reduce the public sector’s perilous overhang of debt.

2014 is likely to be a critical year for Japan

As such, 2014 is likely to prove a critical year for Japan. Can Mr Abe

deliver on his reform promises? Will consumers be able to shrug off the

looming hike in the sales tax? There is certainly room for scepticism on

both matters. Of course, if key data start to soften the BoJ will certainly

opt to up the ante on QE once again. After all, if all you have is a

hammer, then everything starts to look like a nail. Whether that is

enough to build a real recovery with remains to be seen, however.

Chart 1: Here’s the good news on Abenomics to date...

-3

-2

-1

0

1

2

3

40

60

80

100

120

140

160

180

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Jan

-5 =

10

0

NIKKEINOMINAL EFFECTIVE XR (INVERTED)TANKAN (rebased 0 = 100)CPI - RHS

Source: CEIC, Rabobank

Chart 2: ...and here’s the not so good news; look at real wages and the trade deficit

-100

-50

0

50

100

150

70

80

90

100

110

120

130

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Jan

-05

=1

00

Jan

-05

= 1

00

REAL WAGE INDEXMACHINE ORDERSINDUSTRIAL PRODUCTIONTRADE DEFICIT 12MMA - RHS

Source: CEIC

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 1.4 1.6 1.0 1.3 2.4 2.8 2.0

Consumption 2.1 1.9 0.4 1.7 2.5 2.0 1.5

Investment 3.3 1.9 2.6 0.6 4.1 3.9 4.6

Government 1.7 2.2 2.1 2.5 2.3 2.7 2.2

Trade -0.7 0.0 0.0 -0.1 0.0 0.5 0.1

Inventories 0.1 -0.3 -0.2 -0.2 -0.4 -0.3 -0.4

CPI (% YoY) 0.0 0.4 2.4 -0.3 0.9 1.5 2.3

Unemp. %rate 4.3 4.0 4.0 3.9 4.0 3.9 3.9

Yearly Quarterly

Source: Rabobank

/ Michael Every +852 2103 2612

Page 6 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

United Kingdom

Gaining momentum

In the revision of the quarterly national accounts, economic growth in

the third quarter of 2013 remained the same (0.8% QoQ). On a positive

note, the GDP growth figures of past quarters of 2012 and 2013 have

been revised up (in total 0.5%). The expenditure break-down of GDP,

again, indicated that the recovery is domestically driven. Especially

private consumption got a strong upward revision. However, with real

income growth still being negative, it is questionable whether

consumption can remain the primary growth driver. Moreover, exports

were revised negatively (from -2.4% to -3.0%). Together with the

disappointing latest trade figures, this indicates that the recovery is not

broad based. Going forward, leading indicators keep pointing at a

strong economic expansion in the fourth quarter. The manufacturing

PMI eased back to 57.3 in December, and the services PMI went down

to 58.8. Both are however far above the neutral, no-change level (50.0).

Housing market remains strong

Private consumption growth seems to be partially fuelled by the still

buoyant housing market. According to the Nationwide lender, house

prices rose 1.4% MoM (8.4% YoY) in December. What’s more, the BoE

reported that mortgage approvals in the same month increased to a

70-month high, though the level (70,759 in November 2013) is still

below the long-term average (84,511 approvals a month since 1993).

The housing market developments seem to be partially caused by the

government support through the Help-to-Buy scheme. Together with

low mortgage rates, lower unemployment and an improved economic

outlook, the housing market is expected to remain strong in 2014.

However, the risk of a housing market bubble is growing, with the BoE

commenting that they are watching the developments closely. The end

of Funding for Lending (FLS) support for home loans as per January 1st

will probably not hamper the housing market much, since take-up of

FLS funds has been low so far. The refocus of FLS support towards

business lending is sensible, since in November, lending to non-

financial corporates had their biggest drop since the start of the data

series in 2011. With the improving economic outlook, it is expected that

credit demand from companies will increase. Hopefully, FLS can

support banks in servicing these credit demands.

Bank of England outlook

Although the UK economy has shifted up a gear, at the end of Q3 2013,

it was still smaller than its 2007 high. An improvement in exports,

investment and consumer confidence would be welcome to ensure the

recovery is broad based. The BoE is set to retain dovish tone in the

months ahead particularly given its greater confidence that CPI

inflation can refrain from returning to elevated levels. To prevent the

market from speculating about a rate hike in 2014 we expect the MPC

to alter its forward guidance. The unemployment rate has fallen at a

faster rate than anticipated in recent months to 7.4%. We expect the

Bank to indicate that it will not start to consider a rate hike until the

unemployment rate has dropped to a much lower level, potentially

6.4%. This could be announced as part of the February Inflation Report.

Chart 1: Past GDP growth revised upwards

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

12 Q1 12 Q2 12 Q3 12 Q4 13 Q1 13 Q2 13 Q3

Latest estimate 2nd estimate

% Q-o-Q % Q-o-Q

Source: Office for National Statistics (ONS)

Chart 2: PMIs point at a continued expansion

-3

-2

-1

0

1

2

3

30

35

40

45

50

55

60

65

70

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Manufacturing sector (l) Services sector (l) GDP (r)

Index % Q-o-QPurchasing Managers' Indices* (PMI) vs GDP growth

* Above 50 denotes expansion and below 50 denotes contraction.

Source: Reuters EcoWin

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 0.3 1.8 2.0 0.8 0.8 0.6 0.4

Consumption 1.5 2.3 1.7 0.4 0.8 0.4 0.4

Investment 1.2 -0.9 5.1 -1.3 2.1 2.2 1.1

Government 1.5 -0.4 0.6 2.4 0.6 0.1 0.0

Trade 1.2 -0.7 -0.2 0.2 -1.2 0.0 0.0

Inventories 0.4 -0.2 0.8 -0.1 1.0 0.0 0.0

CPI (%y-o-y) 2.8 2.7 2.4

Unemp. %rate 8.1 7.8 7.3

Yearly Quarterly

Source: Rabobank

/ Marcel Weernink +31 30 216 0973 & Jane Foley +44 20 7809 4776

Page 7 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Switzerland

A good year for the Swiss economy

It has been a good year for Switzerland, with the economy growing by

approximately 2% in 2013. Although there seem to be no immediate

threats, there are some signs of fatigue as the Swiss purchasing

managers index disappointed in December. This came as a surprise as

European purchasing managers indices advanced after a weak third

quarter. In Switzerland, most components contributed to the decline,

with the largest impact coming from a decline in the output

component. The employment sub-component was also sharply lower

than in November, indicating that the unemployment rate might

increase a little bit going forward. At the same time, recent export

readings indicate that the country’s exporters are still receiving support

from the weakening of the Swiss franc. Swiss consumer prices increased

by 0.2% in December, probably a reflection of higher energy prices in

the last two months of 2013. We expect eurozone fundamentals to

improve further next year and foresee a growth rate of more than 2%

for the Swiss economy. The low interest rate environment, also on the

capital markets, is probably the main challenge this year as a property

bubble is looming, despite the introduction of the so called anti-cyclical

buffer to be held by banks.

SNB still struggling with internal and external factors

The Swiss National Bank announced that it incurred a loss of CHF 9bn in

2013. The Swiss National Bank said that it lost CHF 15bn on the value of

its gold holdings, but that this was partly offset by a gain of CHF 3bn on

the foreign currency portfolio and more than CHF 3bn in profit from

selling its stabilization fund that bailed out Swiss bank UBS. As the

reserve component turned negative, shareholders and governments

will not receive any dividends this year. This should be “old” news to

the shareholders of the SNB as the gold price and the gold holdings of

the SNB are public information, but the share price fell by 5% after the

announcement. The negative news seems a little bit conflicting with

the central bank forecasts as it upgraded its growth forecasts for 2013

from 1.8% to 1.9% and for 2014 from 1.9% to 2.1% at the meeting in

December. At the same time the central bank said that the cap on the

franc remains essential even as risks to the economy have receded. SNB

President Thomas Jordan strengthened his remarks by saying that

“there is no reason to discuss an exit of the cap”. On the housing

market: “We’re of course watching this market closely and are

concerned about the imbalances”. The SNB has repeatedly warned of

overheating; the SNB may call on the government to raise the capital

reserve requirements for commercial banks even further. In summary,

the SNB is struggling with internal and external factors.

Chart 1: First signs of fatigue?

Source: Bloomberg, Macrobond

Chart 2: An annual loss for the SNB

-25

-20

-15

-10

-5

0

5

10

15

2009 2010 2011 2012 2013

Bill

ion

CH

F

Source: SNB

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 1.0 1.8 2.2 0.5 0.4 0.5 0.6

Consumption 2.4 2.4 0.4 0.7 0.4 0.2 0.3

Investment -0.4 0.8 0.6 1.4 0.5 0.2 0.4

Government 3.2 1.6 0.1 0.1 0.1 0.0 0.1

Trade -0.7 -0.1 1.4 -0.9 -0.3 0.1 0.2

Inventories 0.0 0.0 0.3 0.7 0.3 0.2 0.1

CPI (%y-o-y) -0.7 0.0 1.1 -0.1 -0.1 0.9 1.1

Unemp. %rate 2.9 2.8 2.8 2.8 2.7 2.6 2.5

Yearly Quarterly

Source: Rabobank

/ Emile Cardon +31 30 216 9013

Page 8 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

The Netherlands

A strong start of 2014

Statistics Netherlands (CBS) has upwardly revised third quarter GDP

growth from 0.1% QoQ to 0.2% in its second estimate. Furthermore,

recent economic indicators are pointing towards an acceleration of

growth in 13Q4. The positive carry-over from last year is making for a

relatively strong start of the Dutch economy in 2014. Considering this,

we have upwardly revised our 2014 GDP growth forecast to 0.5%.

Throughout the year, however, quarterly growth is expected to be

limited owing to a continuing decline in domestic spending.

Household consumption keeps falling

Real household consumption declined by 0.5% 3m/3m in October

(based on our own seasonal adjustment), after an equal decline in the

month before. With the exception of January 2012, the consumption

momentum has declined for almost three years now. Durable goods

have been particularly hard-hit (Chart 1). Consumption of durable

goods contracted strongly in 2012 and 2013 in YoY terms, although in

recent months the magnitude of the decline has moderated somewhat.

Consumer confidence improved substantially in recent months. In

December the confidence level equalled -16, a 2 point increase from

November. There are a number of reasons behind the more benign

consumer mood. There will be fewer pension cuts this year compared

to 2013. A temporary tax break in the first tax bracket of income taxes

will increase purchasing power in 2014. The same holds true for the

expected decline in the inflation rate in 2014, which is largely because a

number of indirect tax hikes have fallen out the YoY CPI comparison.

Furthermore, the unemployment rate dropped in November and on

the housing market the number of transactions have increased in

recent quarters. Yet consumers remain cautious when it comes to

making large purchases. The balance of consumers who think it is a

favourable time for large purchases is still at a low level. Moreover, we

expect the previous declines in disposable income and house prices to

lead to a further decline in private consumption volume in 2014.

Manufacturing production declines

Manufacturing production fell 0.6% MoM in November after a 0.6%

increase in October (Chart 2). The 3m/3m growth of production was

1.1% in November, but this was mostly the result of the strong

production growth in September. The drop in manufacturing

production does not match the much stronger rise in sentiment that is

visible in recent months. Producer confidence in the manufacturing

industry improved to -0.1 in December from -0.4 in November, largely

owing to a more favourable stock position. Employment expectations,

however, deteriorated. The balance of employers who expect an

increase in the workforce declined from -12.4 in November to -14.8 in

December. In the manufacturing industry, but also in the overall

economy, we expect employment to decline further in 2014.

Chart 1: Low demand for durable goods

-10

-8

-6

-4

-2

0

2

4

6

8

10

-15

-10

-5

0

5

10

03 04 05 06 07 08 09 10 11 12 13

Total Food, beverages & tobaccoDurables Other, including energyServices

% %

Household consumption, trading-day corrected,

volumes, year on year change, 3-month average

Source: Statistics Netherlands (CBS)

Chart 2: Manufacturing production disappoints

-15

-10

-5

0

5

10

15

-15

-10

-5

0

5

10

15

03 04 05 06 07 08 09 10 11 12 13

Manufacturing 3m/3m IP 3m/3m Manufacturing y-o-y

%%

Dutch Manufacturing production and Industrial

Production, seasonally adjusted

Source: Statistics Netherlands (CBS)

Table 1: Economic forecasts

2012 2013 2014 Q3/13 Q4/13 Q1/14 Q2/14

GDP -1.3 -0.9 0.5 0.2 0.4 0.0 0.1

Consumption -1.6 -2.2 -1.4 -0.8 -0.3 -0.2 -0.4

Investment -4.6 -7.2 1.2 0.0 -0.1 -0.1 -0.1

Government -0.8 -1.2 -0.3 1.3 2.2 -2.3 0.6

Trade 0.2 1.8 0.8 0.0 0.3 0.4 0.2

Inventories 0.2 -0.4 0.0 -0.3 0.0 0.0 0.0

CPI (% YoY) 2.8 2.6 1.0 2.8 1.3 1.0 1.0

Unemp. %rate 5.3 6.7 7.4 7.0 7.0 7.1 7.3

Yearly Quarterly

Source: Rabobank

/ Theo Smid +31 30 216 7599

Page 9 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Poland

Non-inflationary economic recovery continues The gradual economic recovery in Poland has continued and according

to the short-term forecasts it even accelerated at the end of 2013. Data

for industrial output and retail sales suggest that activity in the industry

and retail sectors has remained on an upward trend. At the same time,

the decline in construction and assembly output narrowed in

November, which may indicate some improvement in this sector.

Recent favourable weather conditions could even help annual growth

in production in this sector to return to positive territory in December.

Business climate indicators are also signalling further growth in

economic activity, albeit at a more modest rate in the coming months.

The ongoing economic recovery has translated into an improvement in

labour market conditions. The annual rate of growth in unemployment

is in systematic decline and, according to the Ministry of Labour

estimates, even stopped in December.

CPI inflation edged down for the fourth time in a row to 0.6% YoY in

November from 0.8% YoY in October. This was accompanied by a

decrease in most core inflation indices. Therefore at its January

meeting, the MPC left interest rates unchanged, which was in line with

the November Council declaration on maintaining interest rates at

current levels until mid-2014. It also seems that in the coming months,

the Council will have no grounds to break this commitment, as the

accelerating rate of economic recovery in Poland is still not increasing

inflationary pressure. In line with forecasts, in December, the current

and expected inflation rates most probably stabilized although they

continue to significantly undershoot the lower limit of the inflation

target. It should also be noted that the growth rate of producer prices

still remains below zero (-1.5% YoY in November). However, in the face

of clear signs of economic recovery in Poland –particularly in the field

of domestic demand– a discussion about the need to raise interest

rates is expected to begin in the second quarter, especially if the

recovery is found to have accelerated at the same rate as in recent

months. This would inevitably lead to higher inflation. Inflationary

pressure intensified at the start of the new year with an increase in

excise duty on alcohol and cigarettes and the increase in natural gas

prices and the prices of municipal services. However, persistent low

commodity prices may prevent inflation from rising above the inflation

target even by the end of 2014. Therefore, interest rates are likely to

remain unchanged until at least November 2014.

Zloty at risk at New Year opening, medium-term prospects

remaining upbeat

The economic recovery and strong exports helped the zloty to

appreciate for almost the whole of December. Nevertheless, negative

investor sentiment towards emerging markets as well as local risk

factors, mainly related to pension system reform, weakened the zloty at

the start of the New Year. This situation is unlikely to improve in the rest

of Q1, so further zloty depreciation in the coming weeks is the most

likely scenario. Nevertheless, as the domestic macroeconomic situation

is expected to improve markedly in coming quarters and monetary

tightening is certain to come earlier in Poland than in the Eurozone.

Therefore, on a longer horizon, namely the second half of the year, the

zloty is likely to be one of the top gainers among CEE currencies.

Chart 1: Wages, inflation and unemployment

11

12

13

14

15

0

1

2

3

4

5

6

11 12 13

Pe

rce

nt

Yo

Y c

ha

ng

e (%

)

Inflation Wages (3m MA) Unemployment (RHS)

Source: Reuters, BGZ

Chart 2: Money market outlook

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2.5

3.0

3.5

4.0

4.5

5.0

5.5

11 12 13 14

Pe

rce

nt

Pe

rce

nt

WIBOR 3M WIBOR 3M (forecast)

Source: Reuters, BGZ

Table 1: Economic forecasts

2012 2013 2014 Q3/13 Q4/13 Q1/14 Q2/14

GDP 1.9 1.4 3.1 1.9 2.3 2.7 3.0

Consumption 0.8 0.7 2.4 1.0 1.5 1.7 2.2

Investment -0.8 -0.4 3.2 0.6 1.1 1.9 2.8

Government 0.0 -0.1 0.4

CPI (% YoY) 3.7 1.0 1.9 1.1 0.7 1.1 1.7

Unemp. %rate 13.4 13.4 13.3 13.1 13.4 14.1 13.2

Yearly Quarterly (YoY)

Source: BGZ

/ Dariusz Winek, BGZ +48 22 860 4356 & Piotr Poplawski , BGZ+48 22 860 5869

Page 10 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Hungary

Back on the growth path

The Hungarian economy seems to be following the path to sustained

recovery. After GDP grew by 1.8% (YoY) in Q3 2013, economic data

since then have confirmed the positive outlook. Industrial output

increased by 6% YoY in October, which has placed Hungary among the

top three countries in the EU in industrial output performance. This was

possible mainly thanks to the performance of the vehicle

manufacturing sector, but related supplier divisions and higher food

industry sales were also among the key drivers behind the progress.

The positive Q3 GDP growth figure has also been supported by an

improvement in exports as well as by a significant acceleration in public

investment (co-financed by EU funds). In Q3 2013, the volume of public

sector investment increased by 31.5% (YoY). At the same time, private

investment also improved, stimulated by the Funding for Growth

Scheme implemented by the Hungarian central bank (MNB) in June.

The purpose of this was to boost lending to SMEs and has resulted in

higher amounts of loans and lower borrowing costs.

Positive trends are also noticeable on the labour market. The real

average wage showed a monthly increase for the tenth consecutive

month, improving household purchasing power. In H1 2014, this

should help to revive household consumption, which until now still

remains subdued. The expansion is also confirmed by the decrease in

the unemployment rate – which remained flat in November at 9.3%,

having fallen in October from the 9.8% registered in September. The

current level is the lowest since February 2009.

The inflation rate remained flat in November at 0.9% YoY staying at

historically low levels. As a consequence of low price pressure, the MNB

Monetary Council decided, at its meeting on 17 December, to reduce

the central bank rate –for the seventeenth time in a row– by a further

20 bps, from 3.20% to 3.00%. In its minutes, the central bank indicated

however, that “further easing of monetary policy may follow, but a

reduction in the pace of easing is likely to be warranted in the future.”

This could suggest that the room for further cuts in interest rates in

2014 is rather limited, however an additional cut of a further 20 bps in

January or February, is still quite likely, especially as further decline in

CPI in 2014 is predicted, assuming the lowering of VAT on pork and a

reduction in public transport prices.

Forint remains under pressure at the year opening

The forint weakened in late November and early December, paring

some of its losses at the end of the year. However, generally poor

investor sentiment towards emerging markets, the probability of

further monetary easing, and the feeding of liquidity into the system by

the central bank through the FGS program, increase the risk of a

depreciation in the value of the forint, at least at the beginning of 2014.

In the medium term, the gaining momentum of the economic recovery

in Hungary boosted by exports (as well as a brighter situation in the

euro area) should help the forint to revert back to appreciation against

the euro in second half of the year.

Chart 1: Wages, inflation and unemployment

8

9

10

11

12

-2

-1

0

1

2

3

4

5

6

7

8

11 12 13

Pe

rce

nt

Yo

Y c

ha

ng

e (%

)

Wages (3m MA) Inflation Unemployment (RHS)

Source: Reuters, BGZ

Chart 2: Money market outlook

2

3

4

5

6

7

8

2

3

4

5

6

7

8

11 12 13 14

Pe

rce

nt

Pe

rce

nt

BUBOR 3M BUBOR 3M (forecast)

Source: Reuters, BGZ

Table 1: Economic forecasts

2012 2013 2014 Q3/13 Q4/13 Q1/14 Q2/14

GDP -1.7 1.0 2.4 1.8 2.3 2.1 2.2

Consumption -1.9 -0.1 1.4 0.1 0.3 0.6 0.9

Investment -3.8 4.4 3.0 8.2 6.8 5.6 4.9

Government 0.0 1.9 2.2 0.1

Trade

CPI (% YoY) 5.7 1.3 2.6 1.5 0.9 1.2 1.4

Unemp. %rate 10.7 9.4 9.1 9.8 9.4 10.4 9.8

Yearly Quarterly (YoY)

Source: BGZ

/ Dariusz Winek, BGZ +48 22 860 4356 & Piotr Poplawski , BGZ+48 22 860 5869

Page 11 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Russia

Economic slowdown may continue in 2014

After disappointing economic growth data in Q3 (1.2% YoY), due to

subdued government expenditure and declines in inventories, the

latest macroeconomic data releases show only little improvement,

mainly driven by an improvement in private consumption. Retail sales

increased by 4.5% YoY in November after 3.6% growth in October. The

falling unemployment rate (to 5.4% in November from 5.5% in October)

might also support household spending. It is important to bear in mind,

however, that demographic estimates show a decline in numbers in the

labour force by around 3% a year in the period 2013-2016.

Furthermore, industrial production fell by 1% YoY in November after

declining by 0.1% YoY in October and business confidence dropped

further to -8.0 in December from -6.0 in November.

Despite the continued economic slowdown, inflation remained

unchanged at 6.5% YoY in December, staying for the sixteenth time in a

row above the CBR inflation target, set at a range of 5-6%. As price

growth is higher than was assumed by the monetary authority, with its

new chairwoman still building her credibility as a responsible policy

maker, the CBR decided to keep the key interest rate unchanged at

5.5% at its December meeting. In such circumstances any stimulation of

the economy by reducing borrowing costs is rather unlikely in the near

future. Official CB forecasts show that “inflation will resume the

declining trend in the first half of 2014 and achieve the target at 5

percent in the second half of the year”. If this condition is met and the

economic slowdown continues, it will allow the monetary authorities

room for monetary easing.

Ruble ends the year with annual losses although with a more

optimistic outlook at 2014 opening

Net capital outflows (USD 48bn in the first nine months of 2013,

compared to USD 46bn in the corresponding period of 2012) as well as

low oil prices transforming into a deterioration in the current account

surplus undermined the ruble throughout last year. Even the large-

scale currency intervention undertaken by the CBR, especially in H2 of

2013, were insufficient to prevent the ruble from weakening from its

end-2012 level. The ruble finished the year nearly 7.7% lower against

the dollar (YoY on a closing basis). However, the ruble is one of the few

best performing currencies among emerging markets in the last six

months. Considering the improvement in current account data in Q1

2014 due to the coming Winter Olympics Games in Sochi, as well as

possible further interventions by the central bank on currency markets,

the short-term prospects for the ruble are positive. The medium-term

outlook is rather mixed due to further outflows of capital, possible

monetary easing and falling oil prices.

Chart 1: Wages, inflation and unemployment

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

0

2

4

6

8

10

12

14

16

18

11 12 13

Pe

rce

nt

Yo

Y c

ha

ng

e (%

)

Wages (3m MA) Inflation Unemployment (RHS)

Source: Reuters, BGZ

Chart 2: Money market outlook

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

11 12 13 14

Pe

rce

nt

MOSPRIME 3M MOSPRIME 3M (forecast)

Source: Reuters, BGZ

Table 1: Economic forecasts

2012 2013 2014 Q3/13 Q4/13 Q1/14 Q2/14

GDP 3.6 1.3 1.4 1.2 1.2 1.8 1.4

Consumption 6.8 4.1 3.5 5.3 4.2 4.4 4.1

Investment 6.6 0.1 -1.3 -0.9 0.1 -0.1 -0.3

Government -0.2 0.0 0.1 0.1

Inventories

CPI (% YoY) 5.1 6.5 5.5 6.4 6.4 6.2 5.9

Unemp. %rate 5.7 5.5 4.8 5.8 5.4 5.2 5.0

Yearly Quarterly (YoY)

Source: BGZ

/ Dariusz Winek, BGZ +48 22 860 4356 & Piotr Poplawski , BGZ+48 22 860 5869

Page 12 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

China

Debt data suggest hangover to follow the party On 30 December China finally released local government debt data.

The last official estimates of such liabilities for 2010 stood at CNY

10.7trn (USD 1.7trn); as of end-Q2 2013 these had multiplied to CNY

17.9trn (USD 2.9 trn) including contingent debt guarantees. In short,

debt has jumped 67% in just 10 quarters, an average rise of CNY 600bn

(nearly USD 100bn) per quarter. Indeed, China’s local government debt

is now close to the sum of its central government debt and total public-

sector debt, including contingent liabilities, were CNY 30.3trn (USD

5trn), equivalent to 55.9% of GDP vs. 34% in 2005. Moreover, if we

include Policy Bank bonds as liabilities too, which we should, then

public-sector debt was 72% of GDP, up from 44% in 2005. Of course,

China’s debt is still lower than in most OECD economies. Moreover,

with a 10-year government bond yield of around 4.6% and nominal

GDP growth over 9%, China can effectively deflate away its debt ratio

simply by growing the denominator in the equation. Conversely,

however, it needs to be recalled that exactly because China has been

growing so fast it should have allowed for lower debt ratios rather than

higher. Yet worryingly, the ratio has pushed upwards even despite

nominal GDP growth of 9-10% YoY: were we to see lower nominal GDP

growth and/or higher borrowing costs – both of which are probable

ahead – then the debt ratio would look even worse.

The provinces are in the red even despite huge fiscal transfers

What is even more remarkable about the rise in local government debt

is that on paper it shouldn’t be necessary at all. True, China’s provinces

mostly run huge structural fiscal deficits. Qinghai has a deficit equal to

51.4% of its own local GDP, while even economically dynamic regions

such as Shanghai and Guangdong run deficits of 2.0% and 2.2%,

respectively. However, these shortfalls are compensated for by fiscal

transfers from the central government: once these are included then

total local expenditures only slightly exceed the total revenue stream,

obviating the need to borrow at the kind of levels that could result in a

USD2.9 trillion debt mountain. Clearly there must be vast off-book

spending going on by local governments: but why and how? The

answers to those respective questions are: “To invest in construction

projects to maintain rapid provincial GDP growth”; and “However they

can” – often via opaque Local Government Financing Vehicles (LGFVs).

We can estimate the impact of this off-book expenditure as follows: the

central government fiscal deficit in 2012 was 1.5% of GDP; if we include

the tiny deficits run by the provinces that increases to 1.8% of GDP;

however, if we also suppose the yearly increase in off-book local

government debt is another form of state spending we end up with a fiscal

deficit of nearly 12% of GDP! Of course, not all of that debt went into the

economy: some of it was used to roll over maturing loans, while we are

looking at the total debts including contingent liabilities.

When the music stops, so will a lot of investment spending

Nonetheless, it seems clear that if/when local government borrowing

slows there is likely to be a significant negative impact on investment,

and hence GDP growth. Even in true market economies in Europe

recent government austerity programmes have revealed the extent to

which the private sector often relies on the public sector for its orders –

in China that problem is now greater by orders of magnitude. It is

telling that as aggregate credit expansion has slowed (in November

total system financing was down 12.6% YoY 3MMA), the manufacturing

and services PMIs have also turned down – the HSBC/Markit series were

just 50.5 and 50.9 respectively in December, only just in expansionary

territory.

Chart 1: Local government debt is now close to total central government liabilities

0

10

20

30

40

50

60

70

80

% G

DP

CNY FX Policy bank bonds Railways Local

05 06 07 08 09 10 11 12 13Q3

Source: CEIC

Chart 2: The actual fiscal deficit is much larger than the official figure if we include LGFVs

-14-12

-10

-8

-6

-4

-2

02

42

00

2

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

% G

DP

Total public-sector deficit (official)

Plus change in total local-government debt

Source: CEIC, Rabobank

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 7.7 7.6 7.3 7.6 7.7 7.6 7.4

- Primary 4.5 4.3 4.1 3.0 3.4 3.2 2.7

- Secondary 7.9 8.0 7.9 7.6 7.8 7.6 7.6

- Tertiary 8.1 8.0 8.0 8.3 8.4 8.3 8.0

Retail sales 14.2 12.7 11.8 13.0 13.2 12.2 12.0

Exports USD

YoY%

8.3 7.7 4.6 4.1 3.9 4.0 4.2

Imports USD

YoY%

5.3 6.9 4.5 5.2 8.4 4.6 4.7

CPI (% YoY) 2.7 2.5 2.2 2.4 2.8 2.5 2.4

Yearly Quarterly (%, YoY)

Source: Rabobank

/ Michael Every +852 2103 2614

Page 13 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Australia

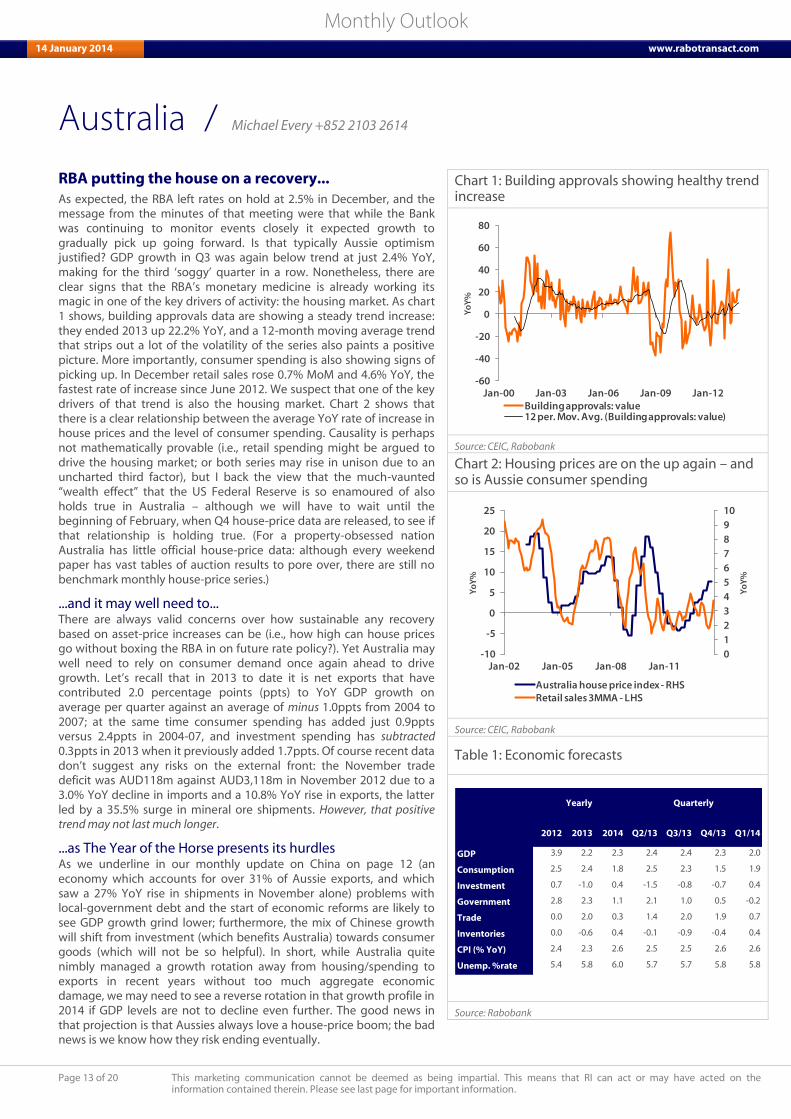

RBA putting the house on a recovery... As expected, the RBA left rates on hold at 2.5% in December, and the

message from the minutes of that meeting were that while the Bank

was continuing to monitor events closely it expected growth to

gradually pick up going forward. Is that typically Aussie optimism

justified? GDP growth in Q3 was again below trend at just 2.4% YoY,

making for the third ‘soggy’ quarter in a row. Nonetheless, there are

clear signs that the RBA’s monetary medicine is already working its

magic in one of the key drivers of activity: the housing market. As chart

1 shows, building approvals data are showing a steady trend increase:

they ended 2013 up 22.2% YoY, and a 12-month moving average trend

that strips out a lot of the volatility of the series also paints a positive

picture. More importantly, consumer spending is also showing signs of

picking up. In December retail sales rose 0.7% MoM and 4.6% YoY, the

fastest rate of increase since June 2012. We suspect that one of the key

drivers of that trend is also the housing market. Chart 2 shows that

there is a clear relationship between the average YoY rate of increase in

house prices and the level of consumer spending. Causality is perhaps

not mathematically provable (i.e., retail spending might be argued to

drive the housing market; or both series may rise in unison due to an

uncharted third factor), but I back the view that the much-vaunted

“wealth effect” that the US Federal Reserve is so enamoured of also

holds true in Australia – although we will have to wait until the

beginning of February, when Q4 house-price data are released, to see if

that relationship is holding true. (For a property-obsessed nation

Australia has little official house-price data: although every weekend

paper has vast tables of auction results to pore over, there are still no

benchmark monthly house-price series.)

...and it may well need to... There are always valid concerns over how sustainable any recovery

based on asset-price increases can be (i.e., how high can house prices

go without boxing the RBA in on future rate policy?). Yet Australia may

well need to rely on consumer demand once again ahead to drive

growth. Let’s recall that in 2013 to date it is net exports that have

contributed 2.0 percentage points (ppts) to YoY GDP growth on

average per quarter against an average of minus 1.0ppts from 2004 to

2007; at the same time consumer spending has added just 0.9ppts

versus 2.4ppts in 2004-07, and investment spending has subtracted

0.3ppts in 2013 when it previously added 1.7ppts. Of course recent data

don’t suggest any risks on the external front: the November trade

deficit was AUD118m against AUD3,118m in November 2012 due to a

3.0% YoY decline in imports and a 10.8% YoY rise in exports, the latter

led by a 35.5% surge in mineral ore shipments. However, that positive

trend may not last much longer.

...as The Year of the Horse presents its hurdles

As we underline in our monthly update on China on page 12 (an

economy which accounts for over 31% of Aussie exports, and which

saw a 27% YoY rise in shipments in November alone) problems with

local-government debt and the start of economic reforms are likely to

see GDP growth grind lower; furthermore, the mix of Chinese growth

will shift from investment (which benefits Australia) towards consumer

goods (which will not be so helpful). In short, while Australia quite

nimbly managed a growth rotation away from housing/spending to

exports in recent years without too much aggregate economic

damage, we may need to see a reverse rotation in that growth profile in

2014 if GDP levels are not to decline even further. The good news in

that projection is that Aussies always love a house-price boom; the bad

news is we know how they risk ending eventually.

Chart 1: Building approvals showing healthy trend increase

-60

-40

-20

0

20

40

60

80

Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

Yo

Y%

Building approvals: value12 per. Mov. Avg. (Building approvals: value)

Source: CEIC, Rabobank

Chart 2: Housing prices are on the up again – and so is Aussie consumer spending

0

1

2

3

4

5

6

7

8

9

10

-10

-5

0

5

10

15

20

25

Jan-02 Jan-05 Jan-08 Jan-11

Yo

Y%

Yo

Y%

Australia house price index - RHSRetail sales 3MMA - LHS

Source: CEIC, Rabobank

Table 1: Economic forecasts

2012 2013 2014 Q2/13 Q3/13 Q4/13 Q1/14

GDP 3.9 2.2 2.3 2.4 2.4 2.3 2.0

Consumption 2.5 2.4 1.8 2.5 2.3 1.5 1.9

Investment 0.7 -1.0 0.4 -1.5 -0.8 -0.7 0.4

Government 2.8 2.3 1.1 2.1 1.0 0.5 -0.2

Trade 0.0 2.0 0.3 1.4 2.0 1.9 0.7

Inventories 0.0 -0.6 0.4 -0.1 -0.9 -0.4 0.4

CPI (% YoY) 2.4 2.3 2.6 2.5 2.5 2.6 2.6

Unemp. %rate 5.4 5.8 6.0 5.7 5.7 5.8 5.8

Yearly Quarterly

Source: Rabobank

/ Michael Every +852 2103 2614

Page 14 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Brazil

Why Ms Rousseff will probably be re-elected Since Mr Luis Inacio Lula da Silva (popularly known as Lula) was first

inaugurated as president in 2003, the importance of politics to the

markets has declined, as a consensus on basic policy has been

consolidated. This consensus has included agreements on fiscal

responsibility, an inflation target and a floating BRL. As his pupil, Ms

Rousseff has imposed her interventionist style since 2011 and markets

are now anticipating the debate about the 2014 general elections.

Here we point to ten reasons why, in our opinion, Ms Rousseff is

favorite to win the forthcoming Presidential election:

(1) The incumbent always starts ahead; (2) The republican system in

Brazil is very concentrated. States and municipalities, and their

representatives, are financially dependent on Central Government; (3)

Upgrades in social policy in recent years are still yielding political

dividends in the form of votes for the PT (Labour Party); (4) Recent

public expenses directed at consumers have further raised the short-

term welfare perception; (5) The unemployment rate is at its lowest

ever level; (6) Party alliances should give Ms Rousseff’s coalition some

50% of free time on open TV; (7) The opposition has been unable to

exploit the government’s weaknesses; (8) Only two candidates are

viable opponents, reducing the chances of a second round; (9) The

most likely scenario, in case of a second round, is that a slice of

opposition support will migrate to Ms Rousseff; (10) All the polls predict

a victory for Ms Rousseff.

Of course, many things could happen to change this reasoning and

alter the eventual outcome, but all of them would lie at the thin end of

the Bell curve. What is for sure today is that, statistically, Ms Rousseff

has a higher chance of winning the elections than Brazil has of winning

the World Cup.

The implications of the outcome of this election are crucial for the

country. Supposing that Ms Rousseff remains in office until 2018, we

should expect minor changes in her policy agenda. In infrastructure

auctions, for instance, some adjustment in the contracts could be

considered to boost their attractiveness to the private sector.

Unfortunately, we have to acknowledge that major changes in

economic policy are unlikely to happen. Monetary policy tends to avoid

direct confrontation with Government guidelines and usually reacts to

the outcomes of such policies. The Central Bank (CB) complies only

artificially with inflation target limits, even taking repressed publicly

monitored prices into account. Finally, the BRL is entering into

dangerous territory. After touching 4% of GDP last year, the current

account deficit should continue to grow. If that turns out to be the case,

the pressure on the BRL should complicate inflation control even

further. All in all, that would require courageous action, such as higher

interest rates, lower economic growth or higher unemployment to curb

inflation and adjust the currency in real terms. If the economy gets

close to the edge of the cliff, Ms Rousseff may give up some of her

ideological convictions. A better global economy, including a recovery

in commodity prices, could reduce the rate of the deterioration in her

probable second term. But the opposite is also true. A frustrated

recovery across the globe should require a quick return to basic

policies. Would Ms Rousseff be pragmatic enough to do that?

Chart 1: Voter intention polls, after Marina Silva and Eduardo Campos’ political alliance

Source: Datafolha

Chart 2: Current account deficit

-6

-4

-2

0

2

4

-100-80-60-40-20

020 20

03

200

4

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013(e)

2014(f)

(%)

Current Account (USD billion)

CAD / GDP (%)

Source: Central Bank

Table 1: Brazil basic rate and inflation (IPCA)

Source: IBGE, Rabobank (f)

/ Robério Costa +55 11 5503 7315

Page 15 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Foreign Exchange

EUR/USD: battle of the Titans The USD has started the year on a firm footing. It is not uncommon for

the greenback to start the year well. At the start of 2013 and 2012 there

was a great deal of hope about the outlook for the USD. In both of

these years the USD index disappointed the consensus by ending the

year close to where it started. The lacklustre performance of the USD in

the past couple of years can be whittled down to the slow pace of the

economic recovery which in turn resulted in a longer phase of QE from

the Federal Reserve than many had anticipated.

This year we expect the US economy recovery to accelerate allowing

the USD to win back lost ground. However, the Fed has indicated that

QE could persist through the whole of 2014 and that the Fed funds rate

will remain at its record low level for some time after that. This means

that upside potential for the USD this year is likely to remain moderate.

In addition, we do not expect the EUR to concede ground easily.

The move away from the height of the crisis, coupled with a significant

current account surplus in the Eurozone (EUR 26.2bn in Oct) and signs

of economic recovery continue to lend good support to the EUR.

We expect that EUR/USD can return to the EUR/USD1.28 level by the

end of 2014. However, we see risk that 1.30 could hold until the final

months of the year.

EUR/JPY: further gains in store The ECB is likely to remain committed to keeping the short-term money

market rates under pressure this year. However, the monetary policy of

the BoJ is set to remain even more accommodative and EUR/JPY is

likely to be drawn to higher levels. There are concerns that wage

inflation in Japan is not keeping pace with CPI inflation. This factor

coupled with the consumption tax increased scheduled for April this

could put the recovery under pressure from Q2 onwards. As a

consequence there is talk that the BoJ could extent its policy stimulus

in the coming months and we expect that this will further undermine

the yen. We have further weakened our yen forecasts and anticipate

that EUR/USD edge towards EUR/JPY144.5 on a 3-month view.

EUR/GBP: Carney confidence Both BoE and ECB policies are currently oriented around keeping short-

term rates pressured lower. This can be expected to remain the case

well into next year. Although the business cycle of the UK and the

Eurozone are closely linked, the UK economy has outperformed in

recent quarters. The better news has led to a strengthening in the UK’s

effective exchange rate. Although the recent good news from the UK

economy is welcome, the recovery is not yet broad based. In the

minutes of its December policy meeting, the MPC protested against the

strength of the pound and these sentiments could be repeated; Even

though sterling remains well below its long-term averages vs. the EUR

and the USD a stronger pound could risk a recovery in the very weak

external sector. While we expect that the pound can strengthen vs. the

EUR during the course of the year, with a lot of good news in the price,

we expect the gains to be measured. Our 12 month EUR/USD forecast

stands at 0.81.

Chart 1: ECB would favour a softer EUR

Source: Macrobond

Chart 2: BoJ: protracting the recovery

Source: Macrobond

Chart 3: BoE: changing forward guidance

Source: Macrobond

/ Jane Foley +44 20 7809 4776

Page 16 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Fixed Income

Significant peripheral spread narrowing... The start of 2014 has seen a very strong narrowing of peripheral

spreads in the Eurozone with Spain, Italy and Portugal all in particular

benefiting. In terms of looking for the immediate driver behind this

move, we would point to what we were hearing from numerous clients

towards the end of last year – this being that, despite favouring further

spread tightening in the Eurozone, they were looking to protect

performance heading into year end and therefore were staying fairly

neutral in relation to benchmark. It would therefore seem that the new

financial year has heralded a rush to express this spread tightening

view. The rally that we have seen in peripherals drove a very strong

performance of our own long 10yr Spain vs. 10yr France trade (see

Chart 1) and, having entered at a level of 197.5bp on October 9, we

exited the position on January 3 at a spread of 159.5bp – booking a

profit of 38bp. The strength of the market rally has also seen both

Ireland and Portugal conducting bond issuance this year (at tenors of

2024 and 2019 respectively) which is earlier than had originally been

suggested.

...but how far could this move go?

On a medium-term basis we continue to look for a broad compression

of Eurozone spreads either “from below” or “from above”. The former

refers to a scenario in which we see a quickening of the global recovery

thereby allowing the Fed to continue dialling down its unconventional

stimulus. This stands to underpin a “Great Rotation” which, in the

context of the EZ bond market, will result in lower-beta markets

underperforming. Meanwhile convergence “from above” would occur if

such a recovery proves elusive, this being because in such a situation

we would expect the Fed to pursue a gradualist approach to tapering

which will ensure the liquidity outlook remains constructive. This will

stand to perpetuate a liquidity phase we term as the “Great Flotation” –

this being where all asset classes are supported by the same tide of

central bank stimulus. The ongoing hunt for yield caused by this stands

to see higher-beta EZ sovereigns outperform.

However, given the sizeable tightening moves seen at the outset of

2014, there is a question mark over how much additional gains might

be expected near term. Chart 2 shows the performance of a basket of

peripheral 10-year spreads over Germany in the opening sessions of

2013 and thus far in 2014. This simple analysis points to some

possibility that the recent pronounced peripheral rally may lose steam

in the coming few sessions (but with this reflecting a dissipation of New

Year liquidity effects rather than challenging our longer term bullish

thematic view). That said, this slowing of bullish momentum may be

more a development regarding Spain and Italy near term rather than

Portugal – where the still decidedly elevated 10-year spread (350bp)

sees it stand out as a candidate in the current yield hungry

environment. In addition sentiment looks to set to continue to improve

on the back of Ireland’s positive demonstration effect (Ireland clearly

showing there to be light at the end of the bailout tunnel).

And a trade?

We have looked to express our bullish Portuguese view versus France

(see Chart 3) in order to capture the theme of a relative outperformance

of the periphery vs. France but with the former reaping the benefits of

recent reform but the latter conspicuous for the lack of progress it has

enjoyed in terms of addressing its own competitiveness issues.

Chart 1: 10yr Spain vs. France

140

150

160

170

180

190

200

210

Oct-13 Oct-13 Oct-13 Nov-13 Nov-13 Dec-13 Dec-13 Jan-14

SPGB 4.4% 2023 vs. FRTR 1.75% 2023

bp

Entry Level

Exit Level

Source: Bloomberg, Rabobank

Chart 2: Peripheral spread compression – 2013/2014 comparison

80

85

90

95

100

105

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

2013 2014

Dec 31 = 100

GDP-weighted composite 10y peripheral spread over Germany

Number of sessions after Dec 31

Source: Rabobank

Chart 3: A tapering hedge?

270

290

310

330

350

370

390

410

430

Oct-13 Oct-13 Nov-13 Nov-13 Dec-13 Dec-13 Jan-14

PGB 5.65% 2024 vs. FRTR 1.75% 2023

bp

Source: Bloomberg, Rabobank

/ Richard McGuire +44 20 7664 9730 & Lyn Graham-Taylor +44 20 7664 9732

Page 17 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Credit Markets

The temptation to follow the herd

In the corporate world the new year has started with a flow pattern very

similar to that prevailing towards the end of 2013, but possibly even

more accentuated. The credit rally has been relatively slow-moving,

driven more by momentum rather than large flows. The absence of a

compelling reason to sell corporate bonds means that real money

customers are retaining large positions, with apparent low volatility.

Their preference is to re-invest the coupons received, principal

redemptions and any surplus cash arising in to new issues. Amongst a

welter of new issues (SSA, Financials) the corporate issue volume has

been moderate, but with longer duration (e.g. from German autos) and

hybrid debt (ENEL) on offer. Seemingly the market has a one-directional

view, therefore spread tightening is the path of least resistance.

Bond valuations now reflect the benefit of several months of improving

economic data and strong technical factors. This is clearly evident from

the European credit indices, with the iTraxx Europe Crossover index

trading below 280bps in early January; the Series 20 version

commenced last September at just below 400bps. In cash markets

turnover has been somewhat limited, at least in the corporate world.

Real money managers are not inclined to sell, while market makers’

inventories are low, perpetuating the inertia. Nor are investors adding

much via secondary markets. We can expect some alleviation, or at

least more activity once primary markets spring to life. But as we stated

in our Outlook piece in December we expect net issuance to decline

this year, partly as a result of hefty bond redemptions (some dating

back to 2009) and partly due to per-emptive refinancing activity by

corporates last year.

The trading pattern of recent months has been very much skewed

towards primary, rather than secondary activity due to the benefits of

liquidity and pricing. We do not see this pattern changing in the near

term. In fact compared to 2011, when the USD/EUR currency basis

favoured issuance in US dollars the funding disadvantage (of issuing in

Euro) has diminished. Foreign companies such as IBM, Sinopec and

Korea Gas have recently completed Euro denominated issues. Brazil’s

energy behemoth Petrobras has just tapped Euro and Sterling markets

with a multi-tranche issue, including some long dated bonds. It is

tempting for corporates to fund themselves before politics intervene,

either in Europe, or the US. However the successful fund-raising by the

Republic of Ireland (EUR 3.75bn of 10-year bonds) last week has already

set a positive tone.

Investors face a more challenging financial environment this year, as

the scope for spread compression is modest, while a) the effects of US

bond tapering will become evident and b) the monetary policy of large

economies is likely to diverge. Until recently the monetary policies of

key economies were largely synchronized, or biased similarly. Gradually

rising US dollar rates may not destabilise Euro credit markets, but there

may be second order effects (e.g. in emerging markets, or from fund

outflows) to contend with.

Chart 1: Clear preference for high yield

300

320

340

360

380

400

420

440

460

480

500

80

90

100

110

120

130

140

150

160

170

180

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14

bp

s

bp

s

iBoxx EUR FinancialsiBoxx EUR Non-FinancialsiBoxx EUR High Yield core cum crossover (rhs)

Source: Markit

Chart 2: On the back of a broadly based rally

250

300

350

400

450

500

550

50

70

90

110

130

150

170

190

210

230

250

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14

bp

s

bp

s

iTraxx Europe MainiTraxx SovX WEiTraxx Europe X/O (rhs)

Source: Markit

Chart 3: Redemptions in 2014 are significant

0

50

100

150

200

250

300

EU

R b

illio

n

Non-financial issuance Non-financial redemptionsRedemptions outstanding Net-non financial

Notes: Euro currency only. Non-financials only. Issued amount above

€500 m. Excludes subordinated and convertible bonds. Redemption is

based on maturity dates of the bonds. Source: Bloomberg

/ Eddie Clarke +44 20 7664 9842

Page 18 of 20 This marketing communication cannot be deemed as being impartial. This means that RI can act or may have acted on the

information contained therein. Please see last page for important information.

Monthly Outlook 14 January 2014 www.rabotransact.com

Financial Forecasts

Table 1 – Economic forecast overview

2012 2013 2014 2012 2013 2014 2012 2013 2014

United States 2.8 1.9 2.8 2.1 1.5 1.6 8.1 7.4 6.6

Eurozone -0.6 -0.4 1.0 2.5 1.4 1.2 11.4 12.1 12.2

United Kingdom 0.3 1.8 2.0 2.8 2.7 2.4 8.1 7.8 7.3

Japan 1.4 1.6 1.0 0.0 0.4 2.4 4.3 4.0 4.0

China 7.7 7.6 7.3 2.7 2.5 2.2 na na na

Netherlands -1.3 -0.9 0.5 2.8 2.6 1.0 5.3 6.7 7.4

GDP Inflation Unemployment rate

Source: Rabobank International

Table 2 – Foreign exchange forecasts

Majors 14/01/2014 +3M +6M +12M Emerging 14/01/2014 +3M +6M +12M

EUR/USD 1.37 1.35 1.33 1.28 EUR/PLN 4.16 4.20 4.16 4.10

EUR/JPY 141 144 144 143 EUR/HUF 299.20 302.00 302.00 295.00

EUR/GBP 0.83 0.83 0.82 0.81 EUR/CZK 27.38 27.50 27.50 27.00

EUR/CHF 1.23 1.23 1.23 1.24 EUR/TRY 3.00 2.81 2.79 2.75

USD/JPY 103.4 107 108 112 EUR/RUB 45.53 45.20 44.40 43.50

GBP/USD 1.64 1.63 1.62 1.58 USD/BRL 2.36 2.40 2.50 2.60

AUD/USD 0.90 0.89 0.88 0.86 USD/MXN 13.11 13.00 12.80 12.40

NZD/USD 0.84 0.84 0.84 0.83 USD/ZAR 10.87 10.60 10.80 11.00

Source: Rabobank International

Table 3 – Swap rate forecasts

U S D 14/01/2014 +3M +6M +12M E U R 14/01/2014 +3M +6M +12M