FACILITATOR: SANDRA TURNER, EU AND INTERNATIONAL MANAGER, NCVO

CHAIR: ANITA PROSSER, CHAIR OF EUROPEAN FUNDING NETWORK

SPEAKERS: NICK DEXTER, DEPUTY DIRECTOR, DEPARTMENT FOR COMMUNITIES AND LOCAL GOVERNMENT

SUE ORMISTON, BIG LOTTERY FUND

S9: GETTING READY FOR £600 MILLION INVESTMENT FROM THE EU

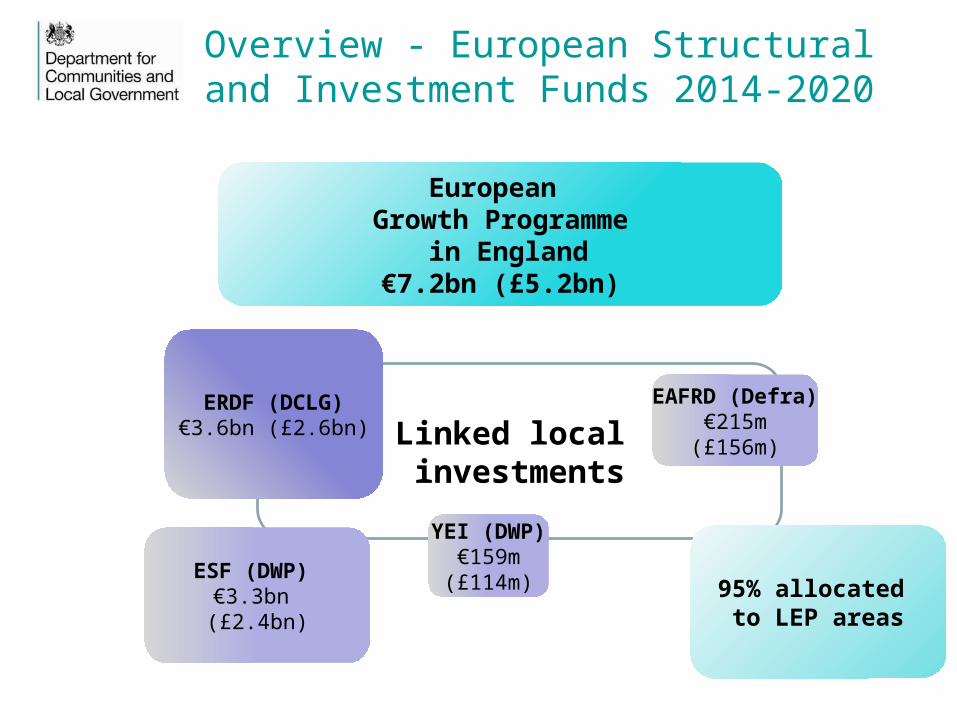

Overview - European Structural and Investment Funds 2014-2020

Linked local investments

European Growth Programme

in England€7.2bn (£5.2bn)

95% allocated to LEP areas

ERDF (DCLG)€3.6bn (£2.6bn)

EAFRD (Defra) €215m (£156m)

ESF (DWP) €3.3bn (£2.4bn)

YEI (DWP) €159m (£114m)

Priorities for ERDF spending in 2014-20

1. Research & Innovation – 21%

2. ICT - 3.4 %

3. SME Competitiveness - 40%

4. Low Carbon economy - 22%

• 95% of ERDF will be spent across 8 objectives• 5% on Technical Assistance• 80% of investments will support objectives 1 to 4

Financial Instruments (FIs) are business loans and equities finance available under ERDF.

There are 4 FI models supporting objectives across 3 of the 8 priority areas: innovation, SMEs and low carbon economy.

5. Environmental Protection - 3 %

6. Climate change adaptation -2 %

7. Sustainable transport in Cornwall & Isles of Scilly – 1.6%

8. Social Inclusion – 1.4%

Technical Assistance – 5%

Priorities for ERDF spending in 2014-20

£2.6bn for 2014-20 Programme allocated to:

• SME competitiveness: £1,095m

• Low carbon approaches: £605m

• Research and innovation: £585m

• ICT and broadband: £103m

• Environmental protection: £81m

• Climate change adaptation: £52m

• Transport for Cornwall/IoS: £43m

• Social inclusion: £38m

Priorities for ERDF spending in 2014-20

SME competitiveness: £1,095m

• Access to finance through grants, loans and equity to help

businesses grow where some groups of Local Enterprise Partnership

areas are looking to build on current financial instruments to improve

access to finance for small businesses while others look to collaborate

to set up new financial instruments

• Business support including advice services for

entrepreneurship, commercialisation, and exports;

• Business support for new business start-ups;

• Premises for SMEs including managed workspaces and

business incubators where demand is shown to exceed supply.

Priorities for ERDF spending in 2014-20

Environmental protection: £81mCoastal resilience (indicative 40%):

• managed realignment and mitigation of coastal squeeze

• shoreline re-nourishment, cliff and dune system stabilisation

• harbour, port and waterfront enhanced protection and adaptations not linked to transport

• improvements to coastal frontages and seawalls

• strengthening and extensions to estuary embankments

Fluvial risk management (indicative 30%):

• onsite or upstream attenuation and slowing the flow measures

• diversion channels

• raising strengthening and/or extending river walls and frontages

• fixed and temporary barriers and gates

• stepped back embankments

• resilience measures for business infrastructure, including for example dry or wet flood-proofing

• river restoration and improved conveyance measures

Surface water run-off and drainage systems (indicative 30%):

• integration, including retrofitting, of surface water and run off management measures into urban and

commercial redevelopments

• innovative measures in contexts where flood risk and land management relies on pumping and interrelates

with drainage

Priorities for ERDF spending in 2014-20

£2.6bn for 2014-20 Programme allocated to:

Environmental protection: £81m

• Investment in green and blue infrastructure such as green

corridors in urban areas and waterways

• Sustainable drainage to improve water quality and in some

cases local air quality.

• Provision of support and advice for businesses in the adoption

of innovative technologies and processes for the management and reuse

of energy, materials, water and waste (including recycling and recovery)

• Provision of support for the development, testing and

demonstration of innovative technologies to promote resource efficiency

Priorities for ERDF spending in 2014-20

Community-Led Local Development (CLLD): £38m

• Targeted on specific geographic areas of need and opportunity.

• Prioritising the needs of areas as identified by reference to the 20%

most deprived areas using the Index of Multiple Deprivation (IMD).

• Cornwall and the Isles of Scilly, area 70% of resource available will

target the 30% most deprived areas according to the IMD. The

remaining 30% of resource may target areas outside of these where

they are adjacent

• Aim to overcome persistent barriers to growth and employment in

lagging areas or deprived communities, reduce the risk of poverty and

social exclusion, through improved access to economic growth and

development opportunities.

Better education, training

Social inclusion

Employment and Mobility

ESF spends against 3 thematic objectives

8

9

10

9

• TO 8 – Promoting sustainable and quality employment and supporting labour mobility – 917m ESF

• TO 9 – Promoting social inclusion, combating poverty and any discrimination - 751m ESF

• TO 10 – Investing in Education, training and vocational training for skills and lifelong learning – 1084m ESF

Differences in focus between 2007-13 and 2014-20

10

The 2014-2020 ERDF programme differs from previous programmes because it has:

• A flexible, single programme across England – rather than 10 programmes

• A highly localised model built around functional geographies (LEP areas)

• Stronger focus on results rather than just spend

• Financial focus on top priorities – SMEs, innovation and low carbon economy

• More segmented menu of policy priorities such as environment, flood

prevention and broadband

• A stronger geographic agenda with an emphasis on cities and local

communities (e.g. Sustainable Urban Development)

11

EU categories of region mapped

against LEP areas in England 2014-20

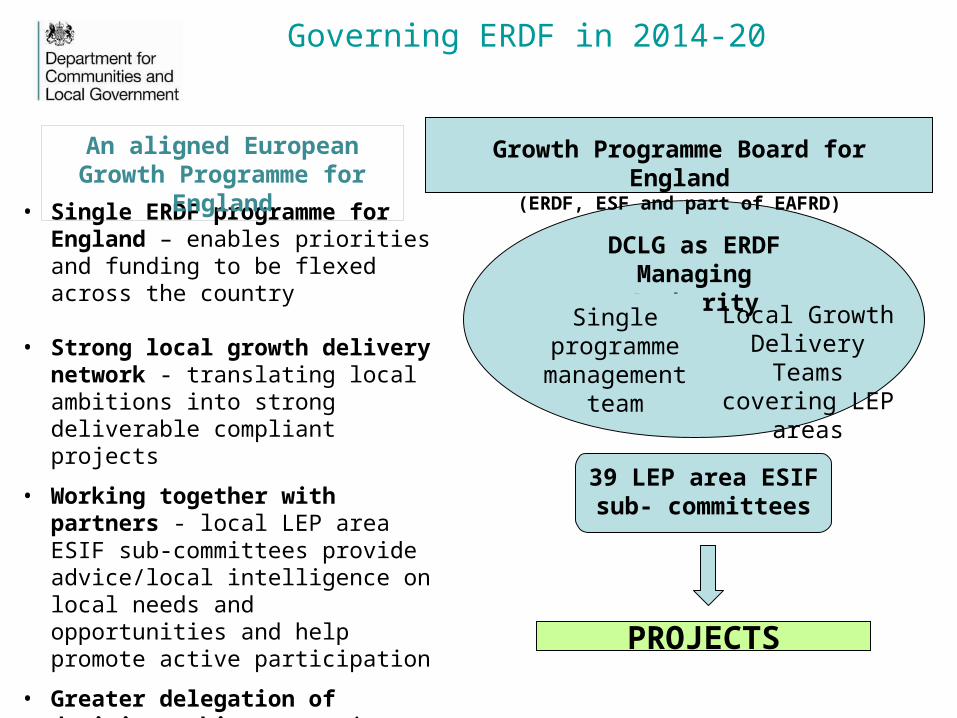

Governing ERDF in 2014-20

Growth Programme Board for England(ERDF, ESF and part of EAFRD)

PROJECTS

• Single ERDF programme for England – enables priorities and funding to be flexed across the country

• Strong local growth delivery network - translating local ambitions into strong deliverable compliant projects

• Working together with partners - local LEP area ESIF sub-committees provide advice/local intelligence on local needs and opportunities and help promote active participation

• Greater delegation of decision making on projects in London (through GLA) and to a lesser extent in 8 core cities (up to 10% of local ERDF allocations)

Local Growth Delivery Teams covering LEP

areas

39 LEP area ESIF sub- committees

DCLG as ERDF Managing Authority

Single programme

management team

An aligned European Growth Programme for England

LEP areas

How do we work with wider growth initiatives ?

LEPs

EZ funding

European Structural and Investment Funds

Growing Places Fund

Regional Growth Fund

programmes

Coastal Communities Fund

Strategic Economic

Plan

Local Plans and planning decisions

Further Education College

Investment

GROWTH

Jobs

Housing

Skills

Infrastructure

Regeneration

Transport links

Local authority assets and spending

Public private partnerships

Private Sector Investment

Growth Deals

National policy initiatives and strategic drivers

Enterprise

14

Key Messages

• The Big Lottery Fund’s Opt in Offer

• The Application Process

• Role of the ESIF Committee

• Next Steps

• Questions and Answers

INTRODUCTION

Photo:Learning through LandscapesNCVO member since 2000

www.biglotteryfund.org

.uk

15

OUR MISSION

Making a real difference to communities and the lives

of people most in need

ESF TO9 Promoting

social inclusion and

combating poverty

OUTCOME 1 To maximise the impact of

funding

OUTCOME 2To improve access to

European Funds by VCSE

organisations

OVERALL VISION FOR BUILDING BETTER OPPORTUNITIES

www.biglotteryfund.org

.uk

16

• Building Better Opportunities is now live

• 37 Local Enterprise Partnership (LEP) areas are expected

to opt-in

• 71 projects in 25 LEP areas are now open for application

• £300m investment over 3 years to tackle poverty and

promote social inclusion

KEY MESSAGES

www.biglotteryfund.org

.uk

17

Baker Tilly / Ecorys are offering support and advice

regarding monitoring, audit and reporting

requirements.

www.bboesfsupport.com

SUPPORT TO APPLICANTS

www.biglotteryfund.org

.uk

18

1. Supporting those furthest from the labour market

2. Meet local needs and priorities

3. Actual costs

4. Grants, not contracts

5. Support available

A SUMMARYTHE BIG LOTTERY OPT IN OFFER

www.biglotteryfund.org

.uk

19

2-STAGE COMPETITIVE GRANTS PROCESSAPPLICATION PROCESS

www.biglotteryfund.org

.uk

Stage 1 Outline Proposal

Stage 2 Detailed Proposal

20

BIG LOTTERY DEVELOPMENT GRANTSAPPLICATION PROCESS

www.biglotteryfund.org

.uk

Stage 1 Outline Proposal

Development Funding

Lottery Money

Stage 2 Detailed Proposal

21

• June / July 2015 – Stage 1 Application• August / September 2015 – Stage 1 Assessment • October 2015 – Stage 1 Decision Making• November / December 2015 – Stage 2 Application• January / February 2016 – Stage 2 Assessment

(there are multiple assessment windows so this is the earliest)

• March 2016 – Stage 2 decisions & award

All dates are subject to minor change

TRANCHE 1 KEY DATES

www.biglotteryfund.org

.uk

22

• October / November 2015 – Stage 1 Application• December / January & February 2016 – Stage 1 Assessment • March 2016 – Stage 1 Decision Making• March / April 2016 – Stage 2 Application• May / June 2016 – Stage 2 Assessment

(there are multiple assessment windows so this is the earliest)

• July 2016 – Stage 2 decisions & award

All dates are subject to minor change

TRANCHE 2 KEY DATES

www.biglotteryfund.org

.uk

23

ROLE OF THE ESIF COMMITTEE

www.biglotteryfund.org

.uk

ESIF Committee

Advice on strategic fit

24

1. Assessment and decision making for Tranche 1 Applications

2. Development of Tranche 2 project outlines

3. BBO programme management and evaluation

NEXT STEPS

www.biglotteryfund.org

.uk

25

Feedback and Questions

www.biglotteryfund.org

.uk

www.biglotteryfund.org.uk

26