Gaming and Leisure Properties, Inc.

February 25, 2014

1 Gaming & Leisure Properties Inc.

In addition to historical facts or statements of current conditions, this presentation contains forward-looking statements that involve risk and uncertainties within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the company’s current expectations and beliefs but are not guarantees of future performance. As such actual results may vary materially from expectations.

The risks and uncertainties associated with the forward-looking statements are described in the company’s filings with the Securities and Exchange Commission, including the Company’s reports on Form 8-K, Form 10-K, Form 10-Q and Form S-11.

GLPI assumes no obligation to publicly update or revise any forward-looking statements.

This presentation includes “Non-GAAP financial measures” within the meaning of SEC Regulation G. A reconciliation of all Non-GAAP financial measures to the most directly comparable financial measure calculated and presented in accordance with GAAP can be found at www.glpropinc.com in the Recent News section and financial schedules available on the Company’s website.

Safe Harbor

2 Gaming & Leisure Properties Inc.

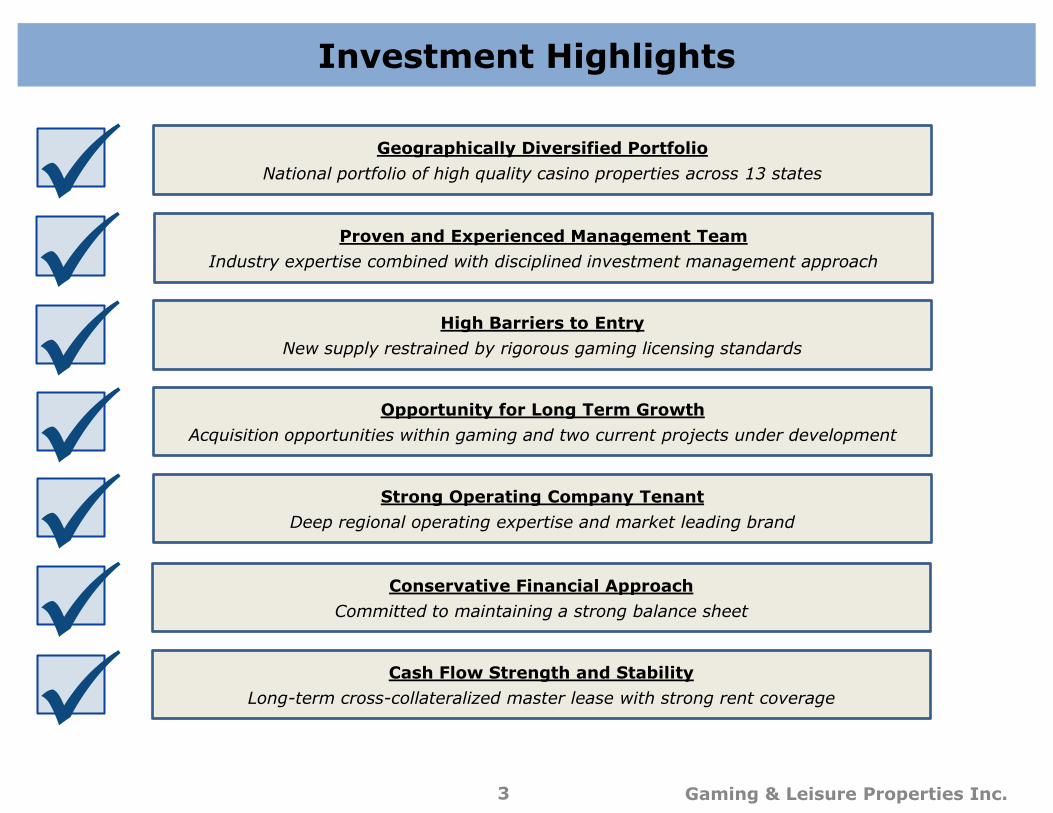

Geographically Diversified Portfolio

National portfolio of high quality casino properties across 13 states

Cash Flow Strength and Stability

Long-term cross-collateralized master lease with strong rent coverage

Strong Operating Company Tenant

Deep regional operating expertise and market leading brand

High Barriers to Entry

New supply restrained by rigorous gaming licensing standards

Proven and Experienced Management Team

Industry expertise combined with disciplined investment management approach

Conservative Financial Approach

Committed to maintaining a strong balance sheet

Investment Highlights

Opportunity for Long Term Growth

Acquisition opportunities within gaming and two current projects under development

3 Gaming & Leisure Properties Inc.

First real estate company focused on gaming assets

Spun-off from Penn National Gaming (NYSE:PENN) November 2013

REIT election expected effective for the 2014 tax year

17 Properties leased back to PENN though a triple-net master lease

Approximately 6.5 million total square feet of building space owned

Over 3,000 acres of land and 2,600 hotel rooms

Two properties owned and operated in a taxable REIT subsidiary

Casino Queen in East St. Louis, IL recently acquired and leased back to its existing operators

Focus on growth and diversification

Two facilities under construction in Ohio; expected to open in the fall of 2014

Intention to actively pursue acquisition and development opportunities in regional gaming and adjacent leisure markets

Disciplined, market-tested management team

Significant development and acquisition track record

Management has over 45 years of combined gaming & leisure real estate experience

Company Overview

4 Gaming & Leisure Properties Inc.

Experienced Management Team…

Peter Carlino – Chairman of the Board and Chief Executive Officer •Serves as the Chairman and CEO of GLPI in addition to the Chairman of Penn National Gaming’s Board of Directors •Served as Penn's Chairman since April 1994 •CEO of Penn from April 1994 until GLPI was spun out to shareholders on November 1, 2013

William Clifford – Chief Financial Officer, Secretary and Treasurer •Serves as GLPI’s Chief Financial Officer, Secretary and Treasurer •Served as Penn National Gaming’s Senior Vice President-Finance and Chief Financial Officer since October 2001 •Served as the Chief Financial Officer and Senior Vice President of Finance for Sun International Resorts, Inc., Paradise Island, Bahamas, the Financial, Hotel and Operations Controller for Treasure Island Hotel and Casino in Las Vegas, the Controller for Golden Nugget Hotel and Casino, Las Vegas, and the Controller for the Dunes Hotel and Casino, Las Vegas

45 years of combined Gaming, Lodging & Leisure experience in numerous industry cycles

Able to leverage industry relationships to source acquisitions

Hold ~15% of shares outstanding – fully aligned with shareholders

5 Gaming & Leisure Properties Inc.

…With a Proven Track Record of Growth…

6 Gaming & Leisure Properties Inc.

1972

Grand Opening

of Penn National

Race Course

2003

Acquired

Hollywood

Casino Corp.

2001

Acquired Casino

Rouge and Casino

Rama Mgt.

Contract

2000

Acquired Casino

Magic and

Boomtown Biloxi

1997

Acquired Charles

Town Races

1996

Acquired Pocono

Downs Racetrack 2005

Acquired Argosy

Gaming

2004

Acquired Bangor

Historic Track

2007

Acquired Zia

Park Casino

1994

PENN Initial

Public Offering

…And an Eye Towards Creating Shareholder Value…

7 Gaming & Leisure Properties Inc.

In 2007 PENN entered into agreement to sell the Company to Fortress Investment Group and Centerbridge Partners for $67 per share

The all-cash transaction represented a total value of approximately $8.9 billion including repayment of debt

Sale price would have resulted in a 30% premium to shareholders

Macro events led to the termination of the agreement in July 2008

PENN received a $225 million termination fee and well as a $1.25 billion

investment in the form of zero-coupon preferred equity

Preferred equity, which was to have been redeemed in July 2015, was repurchased / converted in the recent spin transaction

…Through Even the Toughest Periods

8 Gaming & Leisure Properties Inc.

2008

Grand Opening

of Hollywood

Casino PNRC

Grantville, PA

2009

Grand Opening of

New Hollywood

Casino

Lawrenceburg, IN

2008

Grand Opening

of Slot Operations

at Bangor, ME

2010

Grand Opening of

Hollywood Casino

Perryville, MD

2011

Acquired M Resort

Las Vegas, NV

2012

Grand Opening of

Hollywood Casino

Kansas Speedway

2012

Grand Opening of

Hollywood Casino

Toledo, OH

2012

Grand Opening of

Hollywood Casino

Columbus, OH

2012

Acquired Hollywood

Casino St. Louis,

MO

Fall 2014

Expected Grand

Opening of

Hollywood at

Mahoning Valley

Race Track

Fall 2014

Expected Grand

Opening of

Hollywood at

Dayton Raceway

In light of the termination of the private equity transaction, PENN explored alternatives to create shareholder value including a spin-off of assets into a PROPCO “REIT”

Despite challenging economic circumstances, PENN continued to grow through acquisition and development while pursing the REIT spin-off

2013 GLPI

Completes

Spin off

from

PENN

Spin-off Transaction Overview & Highlights

Separated real estate and non-real estate holdings in tax free spin-off

Entered into master lease agreement with PENN to operate the assets

Exchanged $975 million of Series B Redeemable Preferred Stock at $67 per

share into non-voting PENN common shares

Following the exchange, PENN purchased $397 million of the non-voting PENN

common stock at $67 per share and redeemed $252 million other Preferred

Stock at par in order to satisfy related party tenant rules

GLPI declared and paid a dividend of $11.84 per share to purge historical

earnings and profits as required to achieve REIT status

Reduces Cost of Capital

Facilitates Acquisitions

Improves Financial Efficiency (Margins,

ROE)

9 Gaming & Leisure Properties Inc.

¹ Based on Total Debt / Adjusted EBITDA ² Based on Adjusted EBITDA / Interest Expense

Transaction Rationale

Premium REIT valuation / Lower Cost of Capital

GLPI trades at EBITDA multiple premium to regional gaming companies and has a lower cost of capital

Regulatory Concentration Contraint Removed

GLPI faces reduced FTC/Regulatory constraints in owning properties in same jurisdiction

Access to Diverse Capital

GLPI has access multiple sources to fund growth including preferred, equity/linked, secured & unsecured instruments

Opportunity to Grow Portfolio

First mover and balance sheet advantage allow GLPI to source meaningfully accretive deals quickly

Diversification Opportunities Exist

Potential to work with multiple gaming operators to expand tenant base

Enhanced Credit Profile

Through spin-off GLPI has a greatly enhanced credit profile

10 Gaming & Leisure Properties Inc.

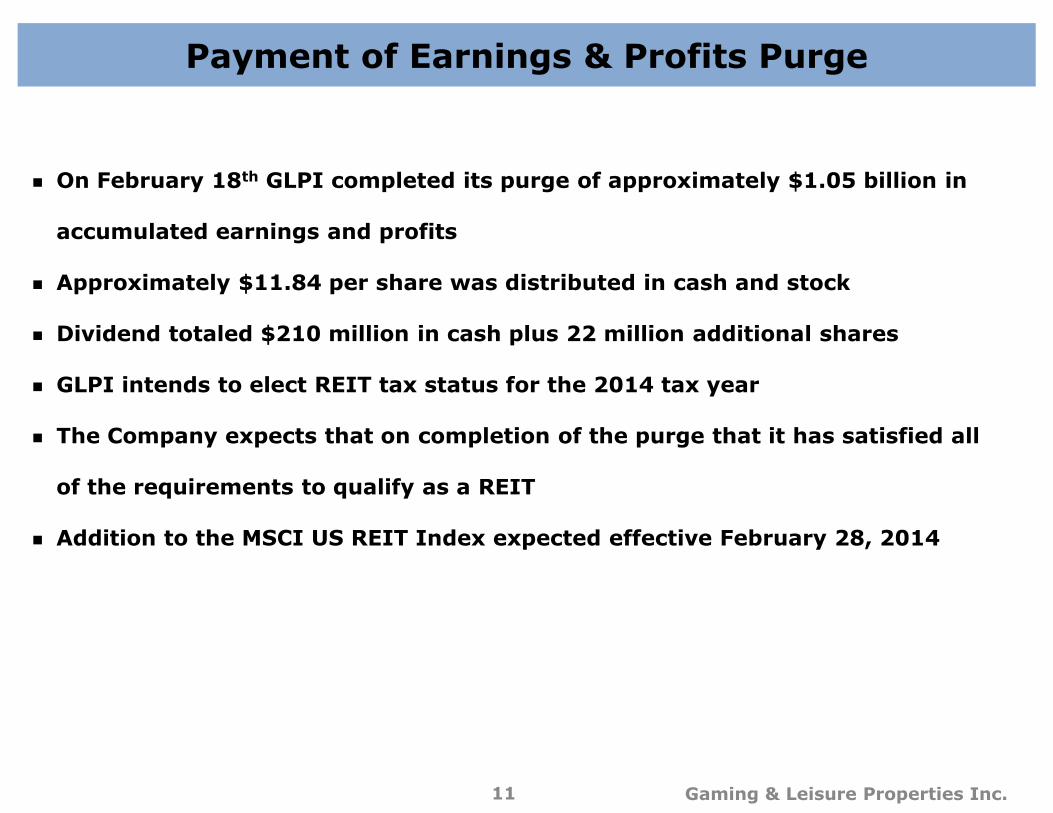

Payment of Earnings & Profits Purge

11 Gaming & Leisure Properties Inc.

On February 18th GLPI completed its purge of approximately $1.05 billion in

accumulated earnings and profits

Approximately $11.84 per share was distributed in cash and stock

Dividend totaled $210 million in cash plus 22 million additional shares

GLPI intends to elect REIT tax status for the 2014 tax year

The Company expects that on completion of the purge that it has satisfied all

of the requirements to qualify as a REIT

Addition to the MSCI US REIT Index expected effective February 28, 2014

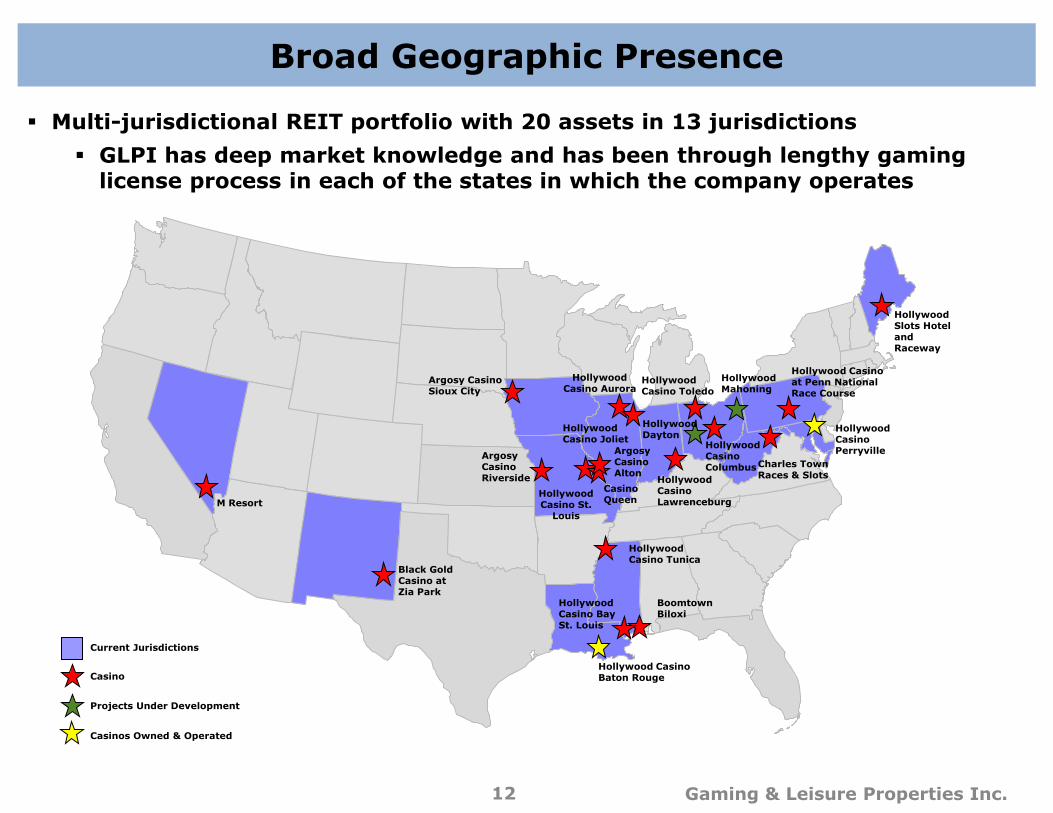

Broad Geographic Presence

Multi-jurisdictional REIT portfolio with 20 assets in 13 jurisdictions

GLPI has deep market knowledge and has been through lengthy gaming license process in each of the states in which the company operates

12 Gaming & Leisure Properties Inc.

Hollywood Mahoning

Argosy Casino Sioux City

Hollywood Casino Aurora

Argosy Casino Alton

Hollywood Casino Bay St. Louis

Boomtown Biloxi

Charles Town Races & Slots

Hollywood Casino Lawrenceburg

Hollywood Casino Toledo

Hollywood Casino at Penn National Race Course

Hollywood Slots Hotel and Raceway

Argosy Casino Riverside

Hollywood Casino Tunica

Hollywood Casino Perryville

Hollywood Casino Columbus

Hollywood Casino St.

Louis

Casino Queen

Black Gold Casino at Zia Park

Hollywood Casino Joliet

Hollywood Casino Baton Rouge

Hollywood Dayton

M Resort

Casinos Owned & Operated

Casino

Current Jurisdictions

Projects Under Development

High Barriers to Entry

Capital Intensive Assets

Extensive Management Experience

Creates first mover advantage in real estate asset class

Access to Capital

REIT status allows lower cost of capital

Regulatory Advantage

Only REIT with regulatory approval in multiple gaming jurisdictions

13 Gaming & Leisure Properties Inc.

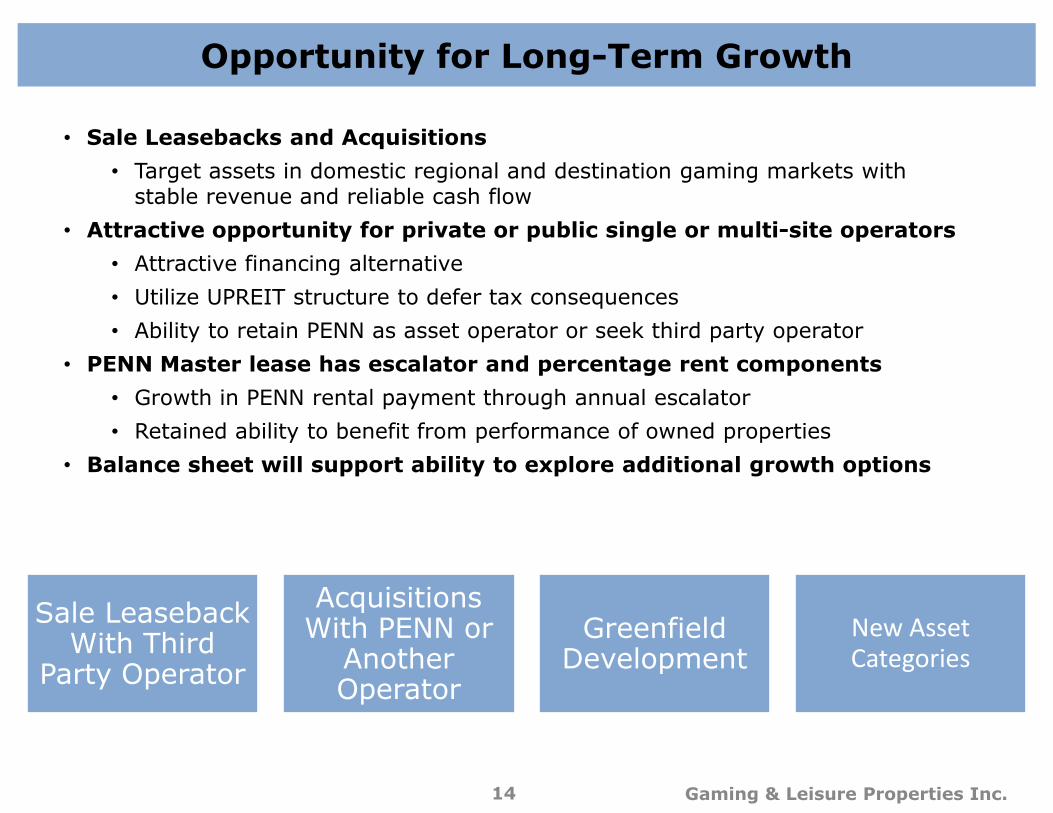

Opportunity for Long-Term Growth

• Sale Leasebacks and Acquisitions

• Target assets in domestic regional and destination gaming markets with stable revenue and reliable cash flow

• Attractive opportunity for private or public single or multi-site operators

• Attractive financing alternative

• Utilize UPREIT structure to defer tax consequences

• Ability to retain PENN as asset operator or seek third party operator

• PENN Master lease has escalator and percentage rent components

• Growth in PENN rental payment through annual escalator

• Retained ability to benefit from performance of owned properties

• Balance sheet will support ability to explore additional growth options

Sale Leaseback

With Third Party Operator

Acquisitions With PENN or

Another Operator

Greenfield Development

New Asset Categories

14 Gaming & Leisure Properties Inc.

Opportunity to Consolidate Existing Casino Assets

139

118

257

0

50

100

150

200

250

Commercial Gaming Assets

Held by Publicly Traded Companies

Commercial Gaming Assets

Held by Privately Held Companies

Total

Commercial Gaming Assets

The only REIT focused on the casino market, with considerable industry expertise

Significant market opportunity

Over 250(1,2) commercial gaming facilities in the United States

Approximately 140 are owned by public companies, that may consider monetizing the

assets to focus on operating opportunities

Many gaming facilities are located in areas where regulatory constraints limit operator

expansion

¹ American Gaming Association, company websites, SEC filings and state gaming regulatory boards. ² Represents only domestic gaming (and excludes Native American) properties. Figures exclude assets owned by Penn

and properties in South Dakota due to their small size. Nevada property count only includes publicly traded companies (equity and debt) with $12 million or more of gaming revenue.

15 Gaming & Leisure Properties Inc.

Casino Queen Highlights Robust Acquisition Opportunity

16 Gaming & Leisure Properties Inc.

Approximately one month after spin-off, GLPI announced its first acquisition Casino Queen in East St. Louis was acquired for $140 million

Property is leased back on a triple-net basis for approximately $14 million in rent per year

GLPI provided a new five year $43 million term loan at 7%

Adds a quality asset with stable market share to GLPI portfolio

Provides further diversification and strengthens cash flows

Demonstrates GLPI’s ability to become consolidator and provider of financing solutions to

highly levered regional gaming operators

Development Pipeline

(1) $ in millions

Project Scope Planned Capital

Spend(1)

Amount Spent to Date

(12/31/13) (1)

Completion Date

Hollywood at Mahoning Valley Race Track

Austintown, OH

$100 $25.9 Fall

2014

Hollywood at Dayton Raceway

Dayton, OH

$89.5 $26.2 Fall

2014

Pipeline:

$190M of development coming on line in the fall of 2014

Management targets a 9-11% yield on cost for development projects

17 Gaming & Leisure Properties Inc.

Strong Operating Company Tenant

High quality, capital intensive assets with recognized brand and loyal customer base

Hollywood Casino at Lawrenceburg ~634,000 property square footage

2,907 gaming machines and 80 table games

Hollywood Casino Columbus ~354,075 property square footage

3,015 gaming machines and 78 table games

Hollywood Casino at Penn National RC ~451,758 property square footage

2,469 gaming machines and 53 table games

Hollywood Casino at Charles Town ~511,249 property square footage

3,500 gaming machines and 110 table games

18 Gaming & Leisure Properties Inc.

Strong Operating Company Tenants

Disciplined capital investments & improvements = Strong ROICs

Young Portfolio – 12 of 20 assets are less than 10 years old(1)

(1) Includes properties which have undergone significant renovation

19 Gaming & Leisure Properties Inc.

Cash Flow Strength & Stability With PENN Lease

Lease Structure:

“Triple Net” Master Lease: PENN will be responsible for maintenance capital expenditures, property taxes, insurance and other expenses

All properties subject to the lease will be cross-defaulted / guaranteed

PENN will remain responsible for acquisition, maintenance, operation and disposition of all (including gaming) FF&E and personal property required for operations

Term and Termination:

15 years, with four 5-year extensions at PENN’s option

Causes for termination by lessor include lease payment default, bankruptcy and/or loss of gaming licenses

At the end of lease term, PENN will be required to transfer the gaming assets (including the gaming licenses) to successor tenant for fair market value, subject to regulatory approval

Provisions for orderly auction-based transition to new operator at the end of the lease term if not extended

Rent:

Fixed base rent component with annual escalators (subject to minimum rent coverage of 1.8x) plus:

Fixed percentage rent component for the facilities (other than Hollywood Casino Toledo and Hollywood Casino Columbus) reset every 5 years to equal 4% of the average net revenue for such facilities for the trailing 5 years

Ohio’s (Toledo and Columbus) performance components will be established monthly with land rent set at 20% of monthly net revenues (represents less than 10% of PENN rent)

Capital Expenditures:

PENN required to maintain properties and spend a minimum of 1% of net revenues on maintenance capital (including FF&E and capitalized personal property required for operations) annually

Structural projects will generally require GLPI consent

Other: Obligations under the Master Lease will be guaranteed by PNG and certain of its subsidiaries

Certain rights of first offer as well as radius restrictions on competition

20 Gaming & Leisure Properties Inc.

Low Cost Rated Debt

Ratings on company’s credit facility and bonds are currently BBB-/Ba1 with stated goal of investment grade rating

Attractive, Stable Yield

Targeted 80% AFFO payout ratio, with growth coming from acquisitions and percentage rent components

Ample Capacity on Credit Facility to Fund Growth

At 12/31/13 the company has $700 million available on its revolver

Manageable Debt Maturity Schedule

First tranche of maturities in 2018

Measured Financial Approach To Support Growth

21 Gaming & Leisure Properties Inc.

Fully Leased /Movement Away From Single Tennant Risk

100% Tenant Occupancy / Recent Acquisition of Casino Queen highlights effort to move away from single tenant concentration in portfolio

Strong Financial Flexibility and Balance Sheet (2)

Low leverage and ample liquidity to

fund growth

$700 million available under revolving

credit facility

$285 million cash

Attractive in-place debt

4.7 % weighted average cost of debt

Manageable maturity schedule with

no maturities until 2018

(1) Effective January 28, 2014 the interest rate on the Revolver and Term Loan A decreased to L + 150 (2) Data as of 12/31/2013. (3) 2014 projection per press release dated 2/20/14 (4) Pro Forma for OH tracks set to open in the fall of 2014

22 Gaming & Leisure Properties Inc.

Projected

EBITDA (3)

Projected

Adjusted Funds From Operations (3)

First Quarter Dividend Per Share

Debt to Adjusted EBITDA (4)

$432.6 $301.3 $0.52 5.7X

December 31, 2013

Interest Rate Balance

Unsecured Term Loan A (1) L + 175 300,000

Unsecured $700m Revolver (1) L+ 175 -

Senior Notes Due 2018 4.375% 550,000

Senior Notes Due 2020 4.875% 1,000,000

Senior Notes Due 2023 5.375% 500,000

2,350,000$

Structure Promotes Stable Cash Flow

23 Gaming & Leisure Properties Inc.

Master lease provides for cross collateralization and cross default protection

Leases are ‘triple-net’

Current rent coverage is in excess of 1.8x

Exposure to regional gaming trends mitigated

- Approx. 80% of PENN rent is permanently fixed

- Approx. 10% of PENN rent is fixed for five years

- Less than 10% of PENN rent is variable monthly

Diverse asset ownership across multiple markets

Geographically Diversified Portfolio

National portfolio of high quality casino properties across 13 states

Cash Flow Strength and Stability

Long-term cross-collateralized master lease with tenant parent guarantee and strong rent coverage

Strong Operating Company Tenant

Deep regional operating expertise and market leading brand

High Barriers to Entry

New supply restrained by rigorous gaming licensing standards

Proven and Experienced Management Team

Industry expertise combined with disciplined investment management approach

Conservative Financial Approach

Committed to maintaining a strong balance sheet

Investment Highlights

Opportunity for Long Term Growth

Large target opportunity within gaming and in adjacent markets / Current projects under development

24 Gaming & Leisure Properties Inc.

Appendix

25 Gaming & Leisure Properties Inc.

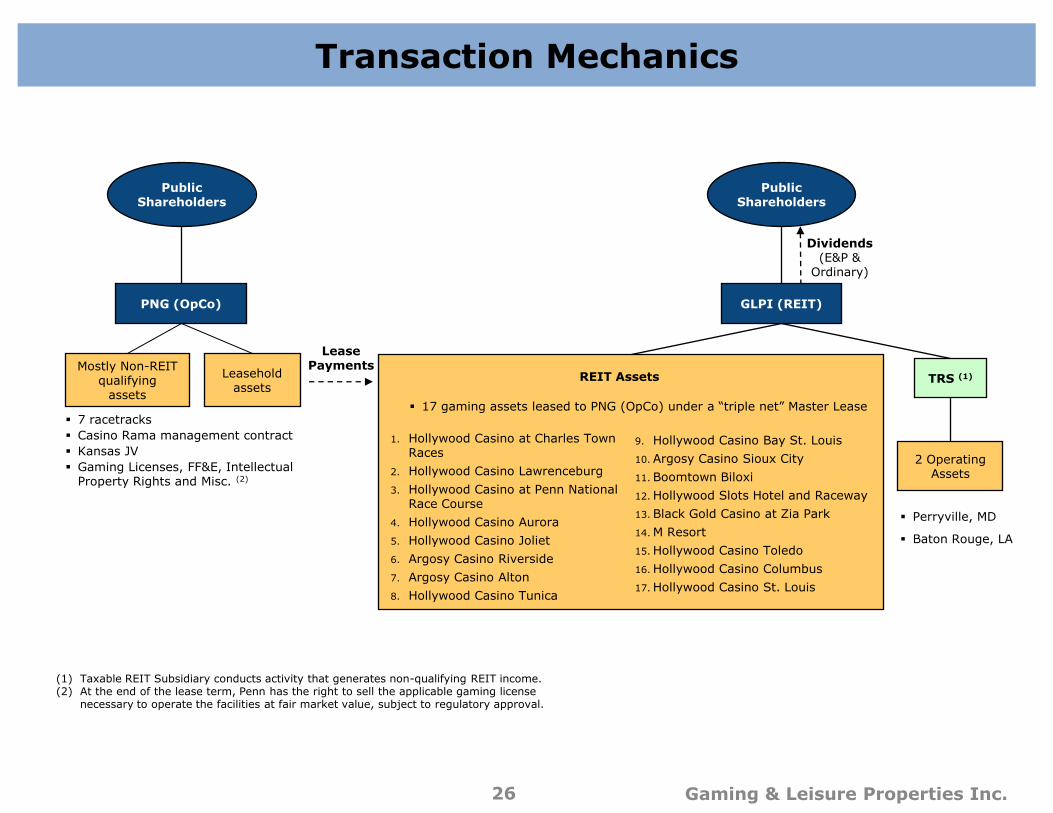

Transaction Mechanics

(1) Taxable REIT Subsidiary conducts activity that generates non-qualifying REIT income. (2) At the end of the lease term, Penn has the right to sell the applicable gaming license

necessary to operate the facilities at fair market value, subject to regulatory approval.

Public Shareholders

GLPI (REIT) PNG (OpCo)

Dividends (E&P &

Ordinary)

Lease Payments Mostly Non-REIT

qualifying assets

7 racetracks

Casino Rama management contract

Kansas JV

Gaming Licenses, FF&E, Intellectual Property Rights and Misc. (2)

REIT Assets

17 gaming assets leased to PNG (OpCo) under a “triple net” Master Lease

TRS (1)

2 Operating Assets

Perryville, MD

Baton Rouge, LA

Public Shareholders

1. Hollywood Casino at Charles Town Races

2. Hollywood Casino Lawrenceburg

3. Hollywood Casino at Penn National Race Course

4. Hollywood Casino Aurora

5. Hollywood Casino Joliet

6. Argosy Casino Riverside

7. Argosy Casino Alton

8. Hollywood Casino Tunica

9. Hollywood Casino Bay St. Louis

10. Argosy Casino Sioux City

11. Boomtown Biloxi

12. Hollywood Slots Hotel and Raceway

13. Black Gold Casino at Zia Park

14. M Resort

15. Hollywood Casino Toledo

16. Hollywood Casino Columbus

17. Hollywood Casino St. Louis

Leasehold assets

26 Gaming & Leisure Properties Inc.

Definitions and Reconciliation of Non-GAAP Measures to GAAP

Adjusted EBITDA, or earnings before interest, taxes, stock compensation, insurance recoveries and deductible charges, depreciation and amortization, gain or loss on disposal of assets, and other income or expenses, and inclusive of gain or loss from unconsolidated affiliates, is not a measure of performance or liquidity calculated in accordance with GAAP Adjusted EBITDA information is presented as a supplemental disclosure. Adjusted EBITDA should not be construed

as an alternative to operating income, as an indicator of the Company's operating performance, as an alternative to cash flows from operating activities, as a measure of liquidity, or as any other measure of performance determined in accordance with GAAP.

The Company has significant uses of cash flows, including capital expenditures, interest payments, taxes and debt principal repayments, which are not reflected in adjusted EBITDA.

Adjusted EBITDA is presented as a supplemental disclosure as this measure is considered by many to be a better indicator of the Company’s operating results than diluted net income (loss) per GAAP. A reconciliation of the Company’s adjusted EBITDA to net income (loss) per GAAP, as well as the Company’s adjusted EBITDA to income (loss) from operations per GAAP, is included in the Company’s news announcements and financial schedules available on the Company’s website.

Funds From Operations (“FFO”) is equal to net income, excluding gains or losses from sales of property, plus real estate depreciation FFO is defined by NAREIT (the National Association of Real Estate Investment Trusts, the trade organization for

REITs) as “the most commonly accepted and reported measure of REIT operating performance.” Adjusted Funds From Operations (“AFFO”) is defined as FFO plus stock based compensation expense reduced by

maintenance capex. A reconciliation of FFO and AFFO to net income (loss) per GAAP is included in the news announcements and

financial schedules available on the Company’s website. FFO and AFFO do not represent cash flow from operations as defined by GAAP, should not be considered as an

alternative to net income as defined by GAAP and is not indicative of cash available to fund all cash flow needs.

Notwithstanding the foregoing, GLPI’s measures of adjusted EBITDA, adjusted EBITDAR, FFO and AFFO may not be comparable to similarly titled measures used by other companies

27 Gaming & Leisure Properties Inc.

Gaming and Leisure Properties, Inc.

February 25, 2014