September 28, 2016 | 8:30 AM

New Mexico Solid Waste & Recycling Conference

Full Cost Accounting and Solid Waste Rate Structuring

Presenter:

Mr. David S. Yanke

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Workshop Agenda

A. Background

B. Full Cost Accounting methodology

C. Detailed example

D. Summary

E. Questions and answers

2

A. Background

NEWGEN STRATEGIES AND SOLUTIONS, LLC

NewGen Strategies & Solutions, LLC

• NewGen is a management consulting firm specializing in providing economic, strategic, stakeholder, and sustainability services

• 37 person firm with offices in Austin, Dallas, Denver, and Nashville

Solid WasteWater/

Wastewater

Energy Gas

4

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Full Cost Accounting History

5

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Full Cost Accounting History (cont’d)

6

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Full Cost Accounting History (cont’d)

7

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Goals of this Workshop

Aid cities, counties, etc. in identifying all

solid waste costs

Help to establish solid waste rates

Assist in their solid waste

planning

8

B. Full Cost Accounting Methodology

NEWGEN STRATEGIES AND SOLUTIONS, LLC

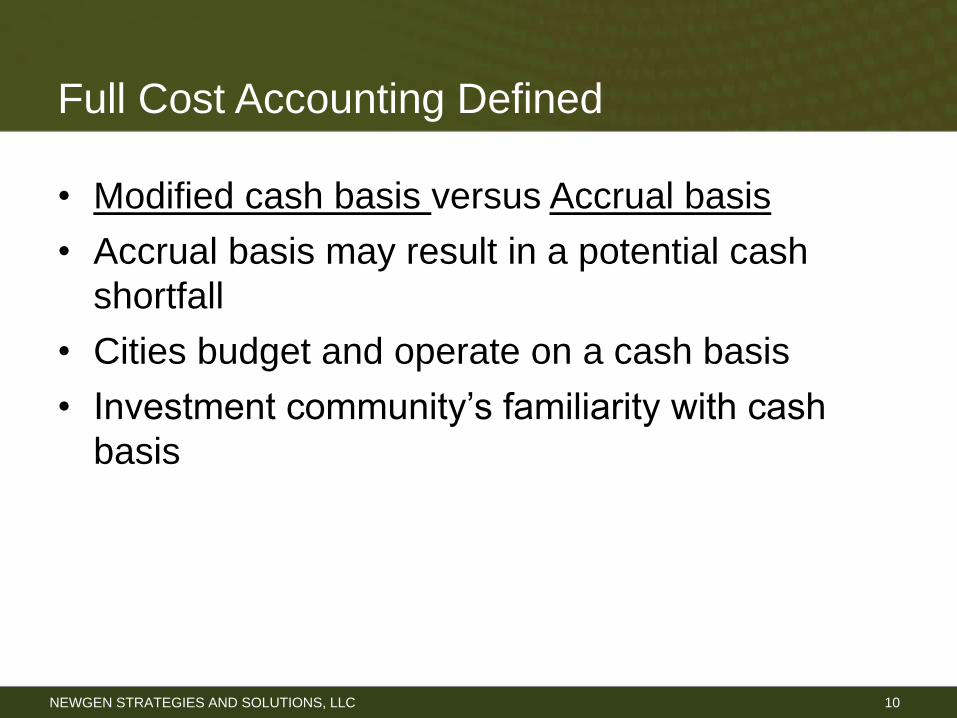

Full Cost Accounting Defined

• Modified cash basis versus Accrual basis

• Accrual basis may result in a potential cash

shortfall

• Cities budget and operate on a cash basis

• Investment community’s familiarity with cash

basis

10

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Modified Cash Basis

• Salaries, wages, and

benefits

• O&M costs

• Predevelopment costs

• Closure/Post-Closure

care costs

• Principal payments

• Interest expense

• Cash capital outlays

Accrual Basis

• Salaries, wages, and

benefits

• O&M costs

• Predevelopment costs

• Closure/Post-Closure

care costs

• Depreciation expense

• Interest expense

Comparison

11

NEWGEN STRATEGIES AND SOLUTIONS, LLC

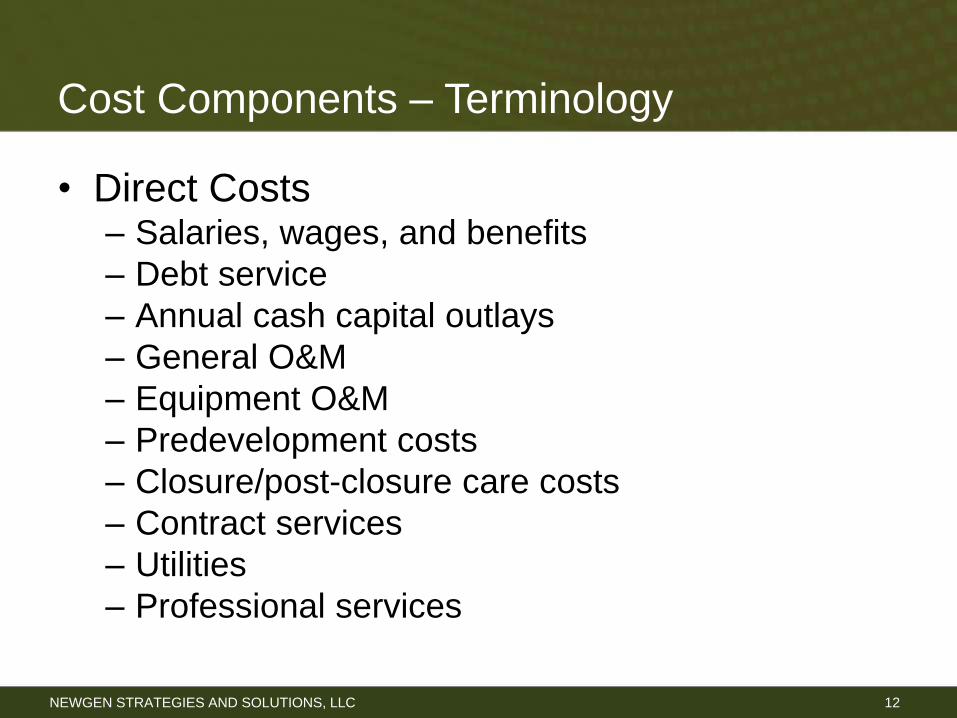

Cost Components – Terminology

• Direct Costs– Salaries, wages, and benefits

– Debt service

– Annual cash capital outlays

– General O&M

– Equipment O&M

– Predevelopment costs

– Closure/post-closure care costs

– Contract services

– Utilities

– Professional services

12

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Cost Components – Terminology (cont’d)

• Indirect Costs

– Administration/City Manager

– Purchasing department

– Finance department

– HR department

– City Council

– Legal department

– City engineer

– Management information systems

– General insurance

13

NEWGEN STRATEGIES AND SOLUTIONS, LLC

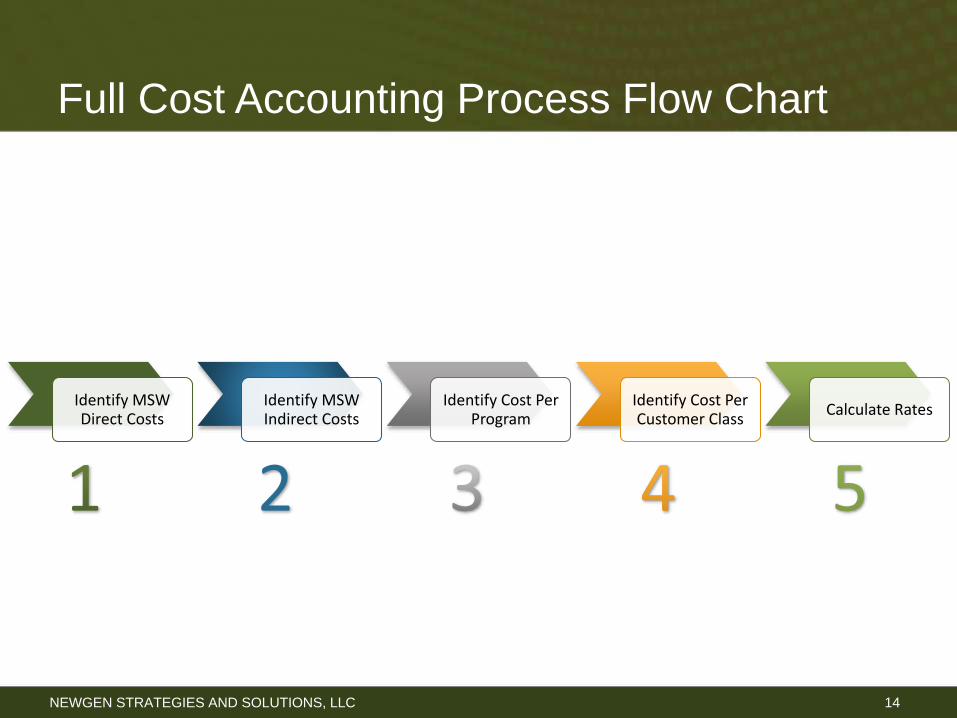

Full Cost Accounting Process Flow Chart

Identify MSW Direct Costs

Identify MSW Indirect Costs

Identify Cost Per Program

Identify Cost Per Customer Class

Calculate Rates

14

NEWGEN STRATEGIES AND SOLUTIONS, LLC

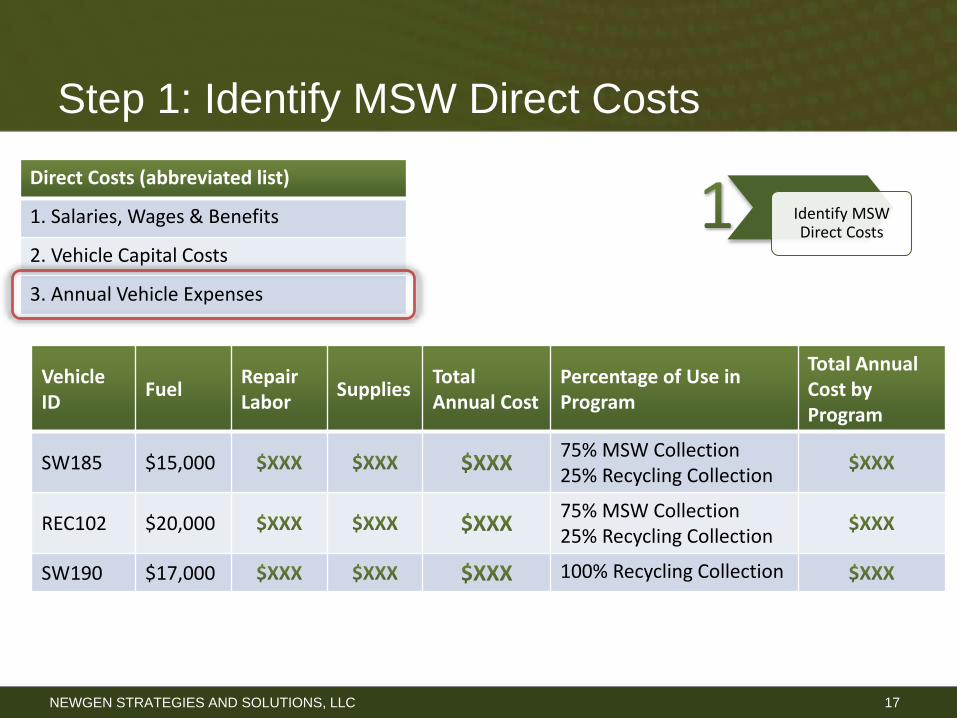

Step 1: Identify MSW Direct Costs

Direct Costs (abbreviated list)

1. Salaries, Wages & Benefits

2. Vehicle Capital Costs

3. Annual Vehicle Expenses

15

Employee Salary Benefits Percentage of ProgramAmount to Program

Mandy Sines $40,000 $10,00075% MSW Collection25% Recycling Collection

$37,500$12,500

Robert Recycler $50,000 $10,00050% MSW Collection50% Recycling Collection

$30,000$30,000

Identify MSW Direct Costs

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 1: Identify MSW Direct Costs

Direct Costs (abbreviated list)

1. Salaries, Wages & Benefits

2. Vehicle Capital Costs

3. Annual Vehicle Expenses

16

VehicleVehiclePrice

Amortized Life

Amortized Cost

Percentage of Use in Program

Annual Cost by Program

Front-Load $350,000 10 $35,00075% MSW Collection25% Recycling Collection

$26,250$8,750

Side-Load $300,000 7 $42,85775% MSW Collection25% Recycling Collection

$32,143$10,714

Rear-Load $175,000 7 $25,000 100% Recycling Collection $25,000

Identify MSW Direct Costs

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 1: Identify MSW Direct Costs

Direct Costs (abbreviated list)

1. Salaries, Wages & Benefits

2. Vehicle Capital Costs

3. Annual Vehicle Expenses

17

Vehicle ID

FuelRepair Labor

SuppliesTotal Annual Cost

Percentage of Use in Program

Total Annual Cost by Program

SW185 $15,00075% MSW Collection25% Recycling Collection

REC102 $20,00075% MSW Collection25% Recycling Collection

SW190 $17,000 100% Recycling Collection

Identify MSW Direct Costs

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Cost Components

• Indirect cost allocation methodologies

18

Internal Assessment

EmployeeBased

Other

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 2: Identify MSW Indirect Costs

19

Identify MSW Indirect Costs

Indirect Costs (abbreviated list)

1. Administration/City Manager

2. Purchasing Department

3. Finance Department

2

DepartmentDept.Budget

% Attributable to MSW Dept.

$ Attributable to MSW Dept.

Purchasing $500,000 25% $125,000

Finance $700,000 30% $210,000

TOTAL $335,000

Internal Assessment Method

Part 1

* Oftentimes indirect cost allocation to Environmental Services Department is already done!

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 2: Identify MSW Indirect Costs

20

Identify MSW Indirect Costs

2

MSW Program% of TotalMSW Direct Costs

Total fromPart 1 Table

Indirect Cost to Program (% of Total MSW x Total from Part 1)

MSW Collection 50% $335,000 $167,500

Disposal 25% $335,000 $83,750

Recycling Collection 15% $335,000 $50,250

Yard Waste 10% $335,000 $33,500

100% $335,000

Internal Assessment Method

Part 2

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 2: Identify MSW Indirect Costs

21

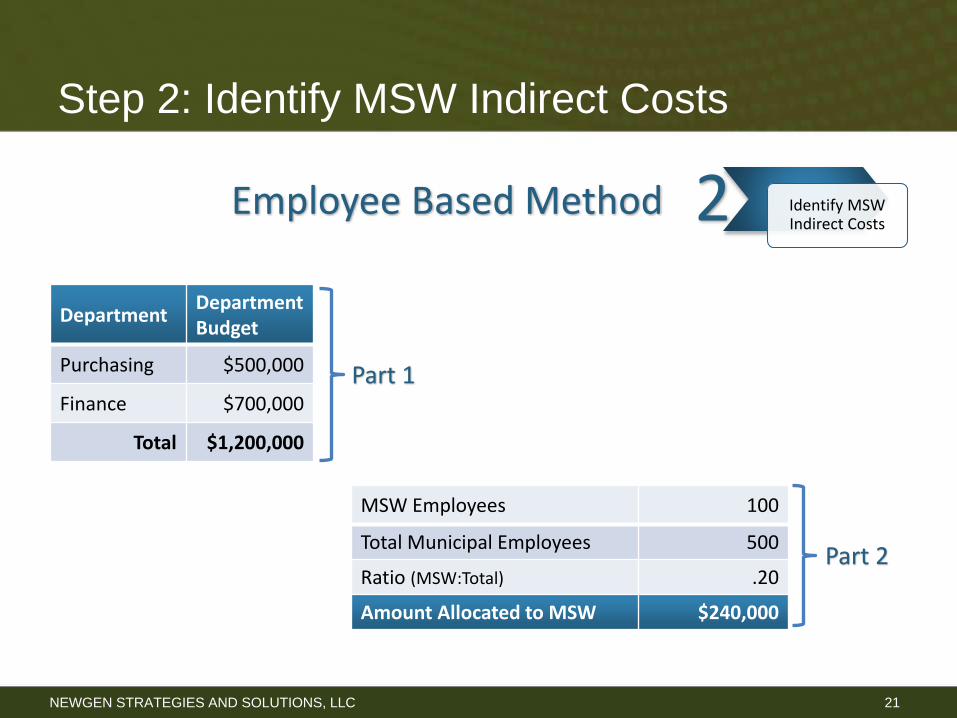

Identify MSW Indirect Costs

2

DepartmentDepartment Budget

Purchasing $500,000

Finance $700,000

Total $1,200,000

Employee Based Method

Part 2

MSW Employees 100

Total Municipal Employees 500

Ratio (MSW:Total) .20

Amount Allocated to MSW $240,000

Part 1

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 2: Identify MSW Indirect Costs

22

Identify MSW Indirect Costs

2

Employee Based Method

Part 3

MSW ProgramSW Employeesby Program

% of TotalMSW Employees

$ Amountfrom Part 2

Indirect Cost to Program (% of Total MSW x Total from Part 1)

MSW Collection 40 40% $240,000 $96,000

Disposal 25 25% $240,000 $60,000

Recycling Collection 32 32% $240,000 $76,800

Yard Waste 3 3% $240,000 $7,200

100 100% $240,000

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Direct costs

• Directly assigned whenever

possible (example: salaries,

debt issues, etc.); or

• Allocated based on

professional judgement or

estimate by City Staff

(example: public education

program); or

• Allocate based on composite

of “directly assigned” costs

Indirect costs

• Allocated based on

composite of “directly

assigned costs”

Allocation of Costs by Program

23

NEWGEN STRATEGIES AND SOLUTIONS, LLC

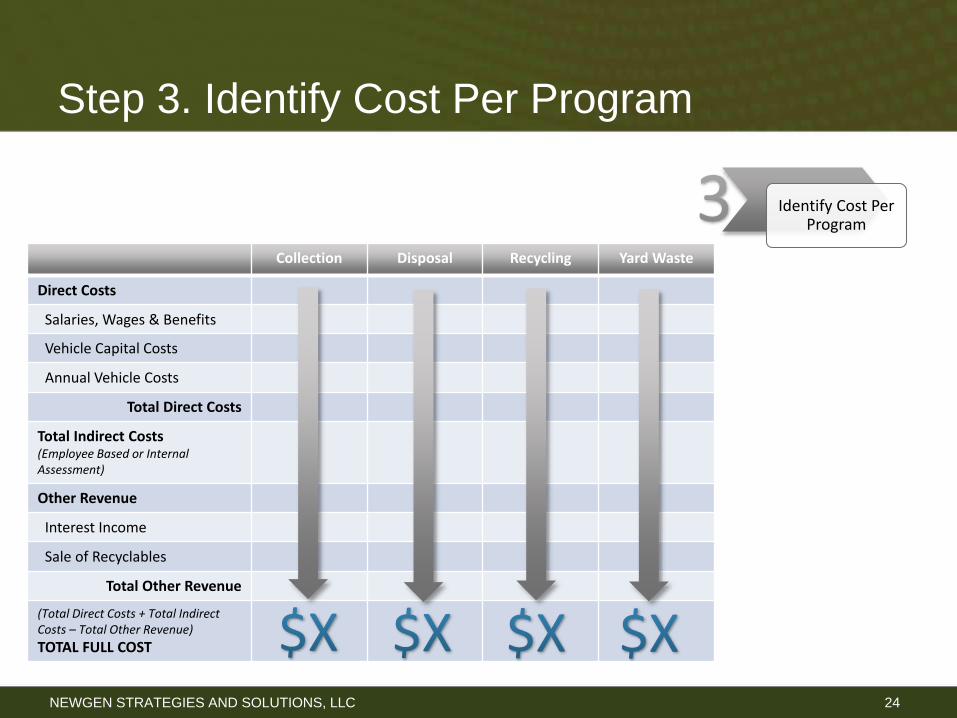

Step 3. Identify Cost Per Program

Collection Disposal Recycling Yard Waste

Direct Costs

Salaries, Wages & Benefits

Vehicle Capital Costs

Annual Vehicle Costs

Total Direct Costs

Total Indirect Costs(Employee Based or Internal Assessment)

Other Revenue

Interest Income

Sale of Recyclables

Total Other Revenue

(Total Direct Costs + Total Indirect Costs – Total Other Revenue)

TOTAL FULL COST

24

Identify Cost Per Program

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Allocation of Program Costs by Customer

Class

• This step is not necessary for all cities

• Typically two customer classes

• Same allocation methodology used

– Directly assign; or

– Allocate based on professional judgement; or

– Allocate based on composite

25

Residential

Commercial

Customer Classes

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 4. Identify Cost Per Customer Class

26

Identify Cost Per Customer Class

Program Cost Residential Commercial Other

Direct Costs

Salaries, Wages & Benefits

Annual Vehicle Expense

Vehicle Capital Costs

Total Direct Costs

Total Indirect Costs(Employee Based or Internal Assessment)

Other Revenue

Interest Income

Sale of Recyclables

Total Other Revenue

(Total Direct Costs + Total Indirect Costs – Total Other Revenue)

TOTAL FULL COST

NEWGEN STRATEGIES AND SOLUTIONS, LLC

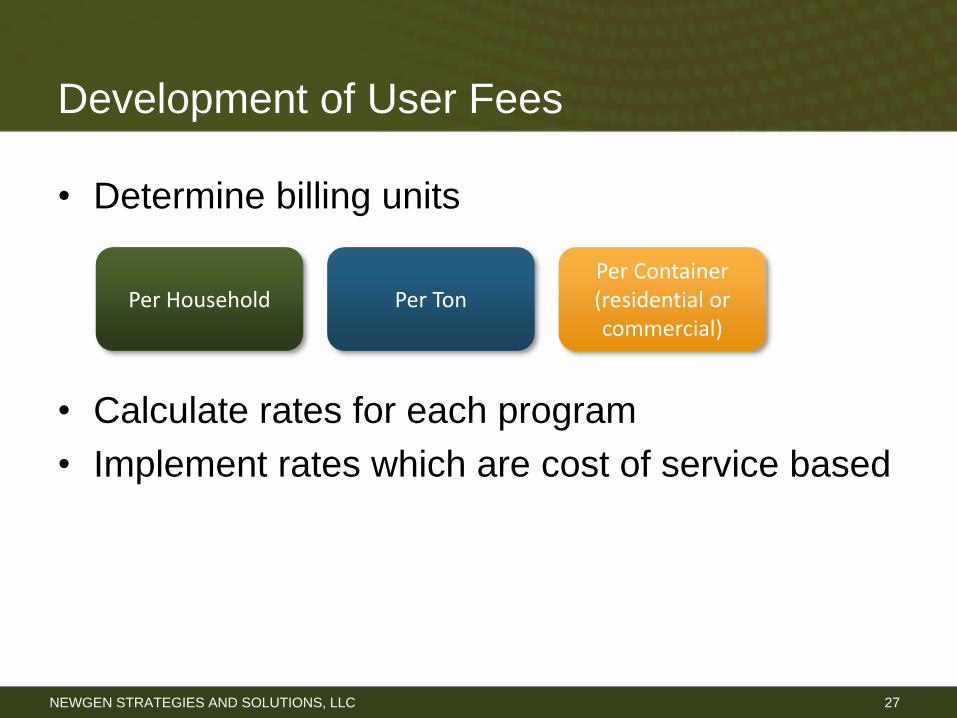

Development of User Fees

• Determine billing units

• Calculate rates for each program

• Implement rates which are cost of service based

27

Per Household Per TonPer Container(residential or commercial)

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Step 5. Calculate Rates

28

Calculate Rates

Program RatesMSW

CollectionDisposal

RecyclingCollection

Yard Waste

Total

Total Full Cost

Billing Units (households, dumpster “lifts”, tons, etc.)

Cost per Billing Unit

C. Example

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Overview

• City in Texas

• Population of

approximately

40,000

• ~$4.7 million

revenue requirement

• Various solid waste

services

TransferStation

Commercial

Residential

30

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Solid Waste Services Offered

Residential

• Refuse collection (weekly collection via side-load trucks)

• Curbside recycling (included in monthly fee)

• Heavy trash/Large waste collection (on-call service)

• Yard waste (2-3 times per month)

Commercial

• Front load dumpster (2, 4, 6, 8 CY – up to five days per week)

• Roll-off (20, 30, or 40 CY – up to five days per week)

Transfer Station (7:30 am – 5:00 pm, Mon-Sat)

31

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Project Approach

1. Methodology overview

2. Development of the “Test Year”

3. Allocation of costs to service categories (programs)

4. Allocation to customer classes

5. Determination of billing units

6. Calculation of the cost of service

7. Current rate recovery

8. Proposed rates for consideration

9. Projected revenue with rate increases

10. Policy issues and recommendations

32

NEWGEN STRATEGIES AND SOLUTIONS, LLC

1. Methodology Overview

• Development of the “Test Year”

– Total revenue the utility will need to recover to fund all

expenses associated with the provision of services.

• Development of revenue requirement forecast

– Revenue requirement adjusted to project changes in

costs due to inflation, salary increases, new

equipment, etc.

33

NEWGEN STRATEGIES AND SOLUTIONS, LLC

1. Methodology Overview (cont’d)

• Allocation of costs to service categories

– Represent the primary solid waste services provided

by the city

• Allocation to customer classes

– Grouped based on the customer classes that will

recover each category’s costs. (residential refuse and

recycling, commercial front load, etc.)

34

NEWGEN STRATEGIES AND SOLUTIONS, LLC

1. Methodology Overview (cont’d)

• Determination of billing units

– Example: cart rate charged by customer

• Calculation of the cost of service

– Distribute costs for each customer class utilizing the

appropriate billing units

35

NEWGEN STRATEGIES AND SOLUTIONS, LLC

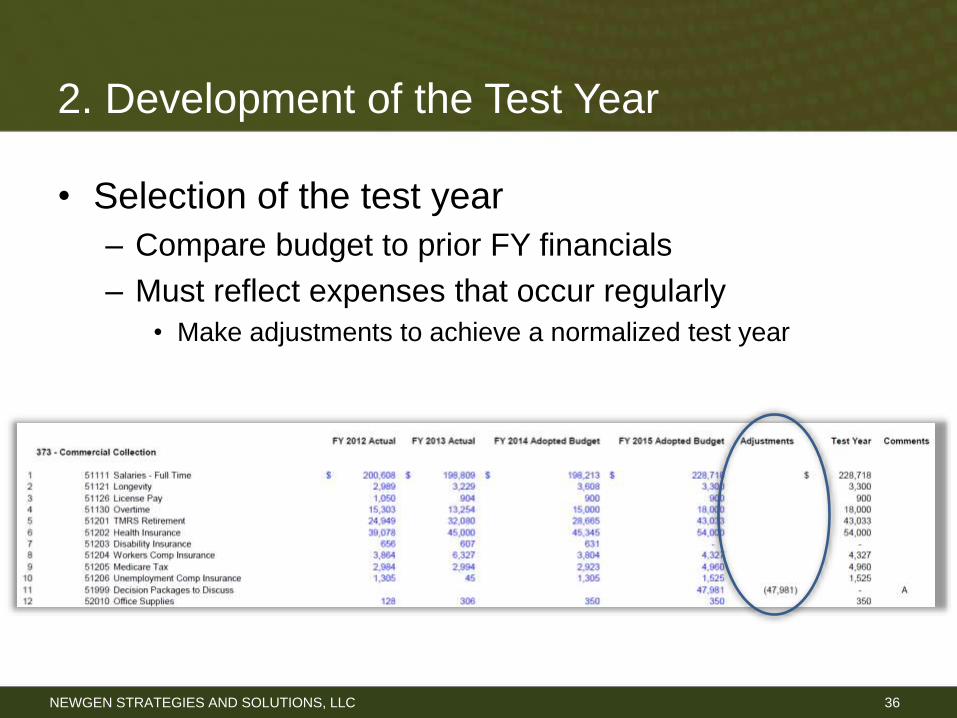

2. Development of the Test Year

• Selection of the test year

– Compare budget to prior FY financials

– Must reflect expenses that occur regularly

• Make adjustments to achieve a normalized test year

36

NEWGEN STRATEGIES AND SOLUTIONS, LLC

2. Development of the Test Year

• Develop the revenue requirement forecast

– Inflationary assumptions used to develop the forecast

37

NEWGEN STRATEGIES AND SOLUTIONS, LLC

3. Allocation of Costs to Service Categories

• Critical step in determining adequate rates to

reflect the cost of providing service

38

Residential Refuse

• Solid Waste

• Yard Waste

• Heavy Trash

Commercial Refuse

• Front Load Dumpster

• Roll-Off

• Non-Profit

Recycling Collection

• Residential Curbside

• Recycling Drop-off Center

Transfer Station

• Transfer Station

• Brush

• Disposal

• Administration

NEWGEN STRATEGIES AND SOLUTIONS, LLC

3. Allocation of Costs to Service Categories

39

• Allocations to “Commercial Collection”

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Summary – by Category

40

NEWGEN STRATEGIES AND SOLUTIONS, LLC

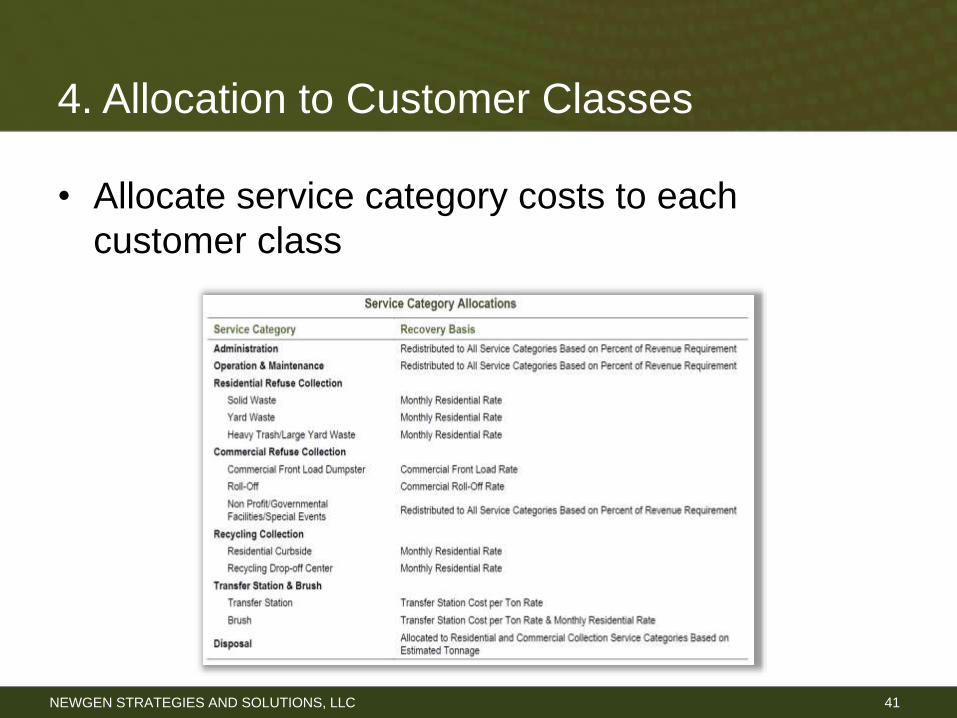

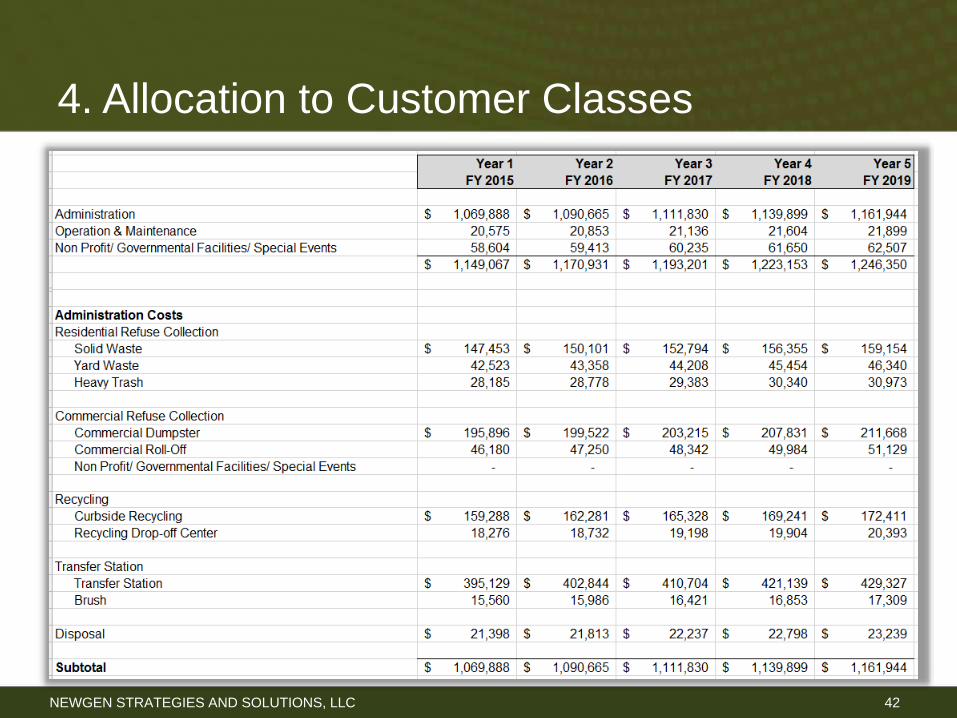

4. Allocation to Customer Classes

• Allocate service category costs to each

customer class

41

NEWGEN STRATEGIES AND SOLUTIONS, LLC

4. Allocation to Customer Classes

42

NEWGEN STRATEGIES AND SOLUTIONS, LLC

4. Allocation to Customer Classes

43

NEWGEN STRATEGIES AND SOLUTIONS, LLC

4. Allocation to Customer Classes

44

NEWGEN STRATEGIES AND SOLUTIONS, LLC

5. Determination of Billing Units

• Determine cost of service by dividing the cost of

service by the appropriate billing units

• Cart billing units

– Flat monthly fee for each cart account

– Zero percent growth for conservative analysis

45

NEWGEN STRATEGIES AND SOLUTIONS, LLC

5. Determination of Billing Units

• Commercial Front Load (3 components)

– Frequency of collection

– Volume of disposal capacity

– Number of containers

46

NEWGEN STRATEGIES AND SOLUTIONS, LLC

5. Determination of Billing Units

• Commercial Roll-Off Collection

– Conservative analysis (zero percent growth)

47

NEWGEN STRATEGIES AND SOLUTIONS, LLC

6. Calculation of the Cost of Service

48

NEWGEN STRATEGIES AND SOLUTIONS, LLC

6. Calculation of the Cost of Service

49

NEWGEN STRATEGIES AND SOLUTIONS, LLC

6. Calculation of the Cost of Service

50

NEWGEN STRATEGIES AND SOLUTIONS, LLC

6. Calculation of the Cost of Service –

Example Calculation

51

In FY 2015, a six-cubic yard container collected

three times per week (13 collections per month)

would result in the following monthly rate:

$25.08 + $7.53 × 13 + $2.57 × 6 × 13 = $323.43

Container Fee

Cost Per Collection

Cost Per CYMonthly Charge

NEWGEN STRATEGIES AND SOLUTIONS, LLC

7. Current Rate Recovery

• Forecasts projected revenue recovered using

current rates

52

NEWGEN STRATEGIES AND SOLUTIONS, LLC

8. Proposed Rates for Consideration

• Consultant expertise guides the proposed rates

53

NEWGEN STRATEGIES AND SOLUTIONS, LLC

9. Projected Revenue with Rate Increases

• Revenue projection assumes the proposed rates

are effective at the beginning of each fiscal year

54

D. Summary

NEWGEN STRATEGIES AND SOLUTIONS, LLC

Summary

• Full cost accounting is a systematic method for

identifying, summing, and reporting costs

incurred in providing services

• Can use to determine the true costs of MSW

management

56

E. Questions and Answers

Mr. David S. Yanke

Direct: (512) 649-1254

Cell: (512) 773-5494

3420 Executive Center Drive

Suite 165

Austin, TX 78731

Phone: (512) 479-7900

Fax: (512) 479-7905