Download - Fashion Buying Project Final

Prepared For: Anna Cappuccitti

Prepared By: Kati Wood

2

Table of Contents INTRODUCTION: ......................................................................................................................... 3

STORE LOCATION: ........................................................................................................................ 3 TARGET MARKET: ........................................................................................................................ 3 MISSION STATEMENT: .................................................................................................................. 4

ECONOMIC OVERVIEW: .......................................................................................................... 4 COMPETITIVE ANALYSIS: ....................................................................................................... 5

RETAIL INDUSTRY OVERVIEW: .................................................................................................... 5 COMPETITION: .............................................................................................................................. 7 POSITIONING MAP: ..................................................................................................................... 13 SWOT ANALYSIS: ...................................................................................................................... 14 STRATEGIC MOVES: ................................................................................................................... 16

PROMOTIONAL CALENDAR ................................................................................................. 17 PROMOTIONAL CALENDAR DETAILS BY MONTH: ...................................................... 24

FEBRUARY: ................................................................................................................................. 24 MARCH: ...................................................................................................................................... 25 APRIL: ......................................................................................................................................... 26 MAY: .......................................................................................................................................... 27 JUNE: .......................................................................................................................................... 28 JULY: .......................................................................................................................................... 29

MERCHANDISE PLAN .............................................................................................................. 31 MERCHANDISE PLAN JUSTIFICATIONS: .......................................................................... 34

SALES: ........................................................................................................................................ 34 MARKDOWNS: ............................................................................................................................ 36 MARKUP: .................................................................................................................................... 36

CLASSIFICATION LIST/INVESTMENT SUMMARY ......................................................... 38 MODEL STOCK PLANS ............................................................................................................ 40 MODEL STOCK PLAN EXPLANATION: .............................................................................. 45 WORKS CITED ........................................................................................................................... 46 APPENDIX ................................................................................................................................... 49

3

Introduction: Store Location: The Eaton Centre

Target Market: In an article for the Montreal Gazette, Zoe McKnight claims that while the

menswear line is, in fact, growing, the “target market remains women – from teens to

those in their mid-60s – who are interested in staying healthy and fit.” (McKnight B.4)

McKnight made an interesting point in noting the vast age range that lululemon targets.

Hollie Shaw, of the Edmonton Journal, solidified this point in her article about the up and

coming new brand that lululemon has put out for its younger market. They created this

new sister brand, called Ivivva, for the athletically inclined female aged four to fourteen.

(Shaw B.2) However, as McKnight points out, the original lululemon athletica brand is

designed with a very specific female customer in mind. Quoting Laura Klauberg, vice-

president of global brand and community, McKnight relays to us that the target customer

is “someone who is ‘super athletic, who is probably in (her) early 30s, who practices

yoga, who probably is a runner, [and is] very successful in her career.’” (Mcknight B.4)

With the average price point of lululemon goods falling between $80-130, it seems

necessary that the target market be relatively successful with a moderate-high income

level in order to adequately afford this price. (lululemon athletica, inc.) Looking at the

psychographic factors affecting lululemon’s target market, Klauberg, as relayed by

McKnight, gives a very insightful and apt description of the lifestyle and attitude one can

expect from a lululemon shopper: she values a healthy, balanced, and physically active

lifestyle and takes a positive attitude towards actively pursuing this state. (McKnight B.4)

4

Mission Statement: With an original intent to “elevate the world from mediocrity to greatness,”

lululemon athletica, inc. defines our mission as “creating components for people to live

longer, healthier, fun lives.” (“About Us”)

Economic Overview: For the majority of 2015, we have been hearing that the Canadian Economy has

been in crisis, with unemployment rates rising, consumer spending dropping alongside

consumer confidence, and a dollar that is lower than it has been in years. (Olive) Despite

this, economists are now recognizing a gradual switch back to the more stable economy

we are used to. We are seeing a rise in Canada’s real GDP projected at 1.2 per cent this

year, with growth rising to 2.2 per cent in 2016, our sales forecasting year. (“Good Signs

for Economy”) We have also seen a huge jump in Canadian retail sales in the second

quarter of 2015, with growth of 25% over the first quarter of 2015 according to Statistics

Canada. Given that there was not only growth between these two quarters, but also an

increase of 2.2% from the 2014 second quarter, we are confident that we will continue to

see this rise in retail sales for the 2016 Spring/Summer season. It must be noted that there

was a 0.8 per cent decrease in the sports and leisure sector, however. (“StatsCan”)

Though lululemon athletica, inc. does play a small role in this portion of retail sales, our

primary market of active-living apparel will remain largely unaffected. Despite these

areas of growth, there is one economic indicator that remains in jeopardy: Canada’s

unemployment rate. Unemployment rose to 7.1 per cent in September, the highest it has

been in over a year. (Younglai) This will have an important effect on consumer spending,

which we will consider closely when determining our planned sales. Overall, given that

5

the Canadian Economy is in a period of recovery, with second-quarter retail sales results

rising by 2.2%, it follows that a moderate increase in sales can be expected for lululemon

athletica, inc.

Competitive Analysis: Retail Industry Overview: Industry Size and Growth:

As of July 2015, clothing stores account for $1,978 million of the Canadian retail

sector, or 4.56% of Canadian retail trade as a whole. This demonstrates a 2.5% growth

from the previous month of June 2015, and a 6.5% growth historically from July 2014.

(StatsCan.)

Major Competitors and Their Impact on Retail Industry:

With consumer trends moving towards an active-living lifestyle more and more

each day, lululemon athletica, inc. has come up against some tough competition. Recent

years have brought a surplus of new entrants to the market ranging anywhere from

established brands, such as The Gap, diversifying their offerings to include yoga wear, to

new specialty companies, such as Soybu, who are focusing solely on active wear to

ensure high depth and breadth in their offering. (Lutz) This influx of entry to the market

will have an inevitable effect on lululemon. It has called into question their market share,

which had been dropping steadily through the last half of 2013. (Brooke) However,

market analysts are suggesting that lululemon is on the rise once more, with revenues

15.6% higher at the end of the fourth quarter of fiscal 2015. (Soni) Though competition

will always be an important factor to consider in any strategic decisions, at present

lululemon athletica, inc.’s competitors have not bridged the gap to becoming consumer’s

6

top-of-mind response to active-living wear, a position lululemon continues to hold dear.

Consumer Trends:

The biggest consumer trend to note right now is the move by Millennials towards

“low-cost, fast fashion retailers.” (Kopun) Millennials represent a huge share of the

market, accounting for upwards of 30% of total retail sales. (Accenture) While lululemon

has marketed themselves well to the Millennial market, they will need to continue to

monitor the level of importance that this integral customer places on the quality of their

active wear versus the price it costs to obtain. Another important consumer trend to note

is the move towards e-commerce. This switch from traditional ‘brick and mortar’

shopping towards the convenience of shopping online has been prevalent over the past

five years, however it is within the last year that e-commerce sales have truly begun to

soar. (FirstData) Lululemon has done an exceptionally good job at embracing this

omnichannel approach to retailing, investing heavily not only in their in-store experience,

but also making their consumer’s online experience integrated and satisfying. They

maintain the sense of community that is their point of differentiation amongst both

channels, a feat that few others have been able to replicate. (Shaw)

Industry Trends:

Lululemon has always been regarded as innovative, due largely in part to their

proprietary technical textiles. Having this advantage in a market where consumers are

constantly questioning what added value they will gain from purchasing your product

over a competitors’ has been crucial to lululemon’s success. (“About Us”) This level of

innovation has become an important industry trend in the development of products.

Consumers are demanding a product unlike any other on the market to ensure their

7

satisfaction, and our industry is dutifully responding to this demand with lululemon

athletica, inc. maintaining their position at the forefront of this movement. Another

important industry trend to note is the influx and growth of private label branding as a

point of differentiation. The best way to differentiate oneself in they eyes of consumers is

to carry a product that they cannot get anywhere else. Unfortunately, with the prevalence

of trade in our market, the only way to ensure exclusivity is to become vertically

integrated. (“Canada’s Changing Retail Market”)

Competition: Direct Competitors:

1. Athleta, by The Gap

2. Nike

3. Soybu

4. Zella, by Nordstrom

Positioning Strategies and Key Strengths by Competitor:

Athleta, by The Gap:

Athleta is the new moderately priced active-wear and lifestyle brand put forth by

The Gap and is one of lululemon’s biggest direct competitors. Similar to lululemon, their

merchandise assortment ranges from their yoga- and sport-wear offerings, to their

comfortable lifestyle apprel in the form of dresses, outerwear, and accessories. (Athleta)

Their pricing is reasonable, with comparable garments 20-30% less than their

counterparts at lululemon. For example, a pair of yoga pants from Athleta retail starting

at $50, where a similar pair at lululemon will start at $80 minimum. (Athleta)(lululemon

athletica, inc.) Athleta currently has 100 locations across North America, as well as a

strong online presence. Their customer service level remains high across both channels,

8

with live chat available online to ensure you find your perfect fit. Similar to lululemon,

they are striving to build a community by offering free fitness classes and a professional

discount for fitness instructors. (Athleta) Their in-store design and the environment of

their stores suggest an active-living culture, which their target market can appreciate.

The primary strength of Athleta is their association with the already successful

Gap brand. Clients of The Gap that are looking to make the switch to an active lifestyle,

or to try yoga for the first time, will be inclined to shop with a brand they already know

and trust. Athleta offers a wide variety of free fitness classes available through their

locations, limiting themselves not only to yoga, but including interval training and pilates

as well. (Athleta) Athleta has chosen to take on the plus-size market, which accounts for

67% of the apparel purchasing populace. (Lutz) Considering the negative backlash

lululemon has received in terms of its accessibility to female consumers over size 12,

Athleta stands to gain a huge following in this sector of the market. Finally, Athleta’s

customer service mentality remains a point of difference for them in a market that so

heavily values service. They do this through their one-of-a-kind return policy, boasting

the ability to return any garment, at any time, in any condition, and receive a full return if

you are in any way unsatisfied with the performance. They also ensure that if you cannot

find your desired size or style at one location, they will search other locations and their

online system to find it and ship it to you free of charge anywhere in the world. (Lutz) It

is these distinct strengths that make Athleta one of lululemon’s most dynamic

competitors.

9

Nike:

For decades Nike has been the go-to for athletes across the globe. Though

creating a name for themselves primarily with runners, Nike has never been shy about

showcasing their versatility amongst all athletic channels. One of their most recent

endeavours is their diversification into yoga-wear and accessories. (Nike) The

merchandise assortment of Nike stretches from the top and bottom aspect of yoga-wear,

to the accessories required for the activity such as mats, bags, and specialty footwear.

Their price point is comparable to lululemon with most offerings on par. For example, a

yoga mat with Nike starts at $60, with lululemon mats starting at $55. (Nike)(lululemon

athletica, inc) Nike communicates with their clientele through their already existing

community of sponsored athletes and athletic events. Nike products are available in

countless retail stores across the globe, as well as in their flagship locations across

Canada and the U.S. However, though they are currently in the process of developing an

online shopping experience for the Canadian consumer, at present their ecommerce site is

unavailable to Canadians. (Nike)

The yoga-wear sector of Nike has a similar key strength to Athleta in their

association to an already widely regarded brand. However, in this case it is due to the

athletic community Nike has already built for itself. Athletes of all kinds flock to Nike for

their apparel, footwear, and accessories. It is no wonder that when they introduced their

yoga line, they garnered followers that were already using other Nike products in their

respective athletic pursuits. Seen as perhaps a more serious athletics brand, consumers

who are highly involved in the active lifestyle may choose Nike over lululemon for their

more leisure activities, such as yoga. One of Nike’s main strengths, as mentioned before,

10

is the community that they have created with their products. Their main added value is

the idea of “hope” that they bring to people, whether it is those looking to start running

for the first time, or their sponsored athletes competing at in some of the world’s most

challenging marathons and events. (Nike) Nike also offers a wide assortment of specialty

accessories for yoga lovers, such as their Studio Wrap shoe, which is designed

specifically for precise control on otherwise slippery yoga mats. (Nike) This level of

innovation mixed with a product that is solely theirs puts Nike ahead of its competitors

when it comes to product comparison. Finally, Nike is one of the most accessible brands

for consumers, being found in countless retailers across the globe, whereas lululemon is

solely available in their own stores and online. (Nike)

Soybu:

Soybu is a relatively new competitor for lululemon, boasting a line of yoga-

centric apparel made entirely from soy, organic cotton, bamboo, and recycled materials.

(Lutz) Though their main focus is on yoga-wear, they do offer a small assortment of

dresses, outerwear, and swimwear, however it maintains the same athletic aesthetic. Their

price point is lower than that of lululemon, with one of their yoga tops retailing for $36

versus a comparable option at lululemon for $66. (Soybu)(lululemon athletica, inc.) Their

apparel is currently offered in select retail stores across Canada and the U.S., as well as

on their online shop. Though they are not as diversified as lululemon, they do appeal to

the same target of consumers who lead an active lifestyle and seek sustainable fashions.

Soybu’s key strength is their sustainability factor. Made from all-natural textiles,

the brand garners attraction from consumers who are environmentally minded. Since the

11

yoga lifestyle is often equated with peace, harmony, and a respect for ones environment,

it suggests that consumers who practice yoga will gravitate to a brand boasting these

features. (Soybu) Since Soybu is still relatively small and is only offered in specialty

stores and online, it creates an air of exclusivity to the product line, which is what

original followers of lululemon sought. With lululemon’s extreme growth, many of these

boutique shoppers have left to look elsewhere for their lifestyle fashions. (Lutz)

Considering the quality of the materials being used, as well as in comparison to their

direct competitors, Soybu is one of the most affordable yoga-wear alternatives on the

market. In a niche that is known for attracting a higher-end client, Soybu presents

themselves as an accessible and affordable alternative. (Soybu) Finally, since Soybu has

opted to focus solely on yoga wear, they’ve allowed themselves to develop a strong

assortment within their products, which allows customers to have repeat purchases on the

items they come to love most. (Soybu)

Zella, by Nordstrom:

Though Nordstorm is still in its infancy in the Canadian market, they are

forecasted to take it completely by storm. Known for their exceptionally high level of

customer service, it is no doubt that the brand and their kin, such as Zella, will represent a

new challenge for Canadian retailers like lululemon. (Nordstrom) The Zella brand offers

an assortment similar to that of lululemon, however they have branched off to include the

highly important plus-size market, as well as the children’s market. (Zella) Their pricing

strategy is moderate for the high quality of the brand, though it is still lower than that of

lululemon. For example, a zip-up sweatshirt from Zella retails at $130, where a similar

12

counterpart at lululemon starts at $170 and up. As mentioned previously the Nordstrom

brand is known primarily for customer service, which is important in the yoga

community. Though only available in Nordstrom stores which have yet to expand fully

into Canada, Zella is available online to the Canadian consumer with free shipping

Canada-wide. (Zella)

Diversifying away from their typical high-end department store offerings,

Nordstrom came up with their active-wear brand, Zella. Being associated with Nordstrom

is one of the biggest key strengths for Zella. The brand is offered on their website as well

as in stores, allowing the typical Nordstrom shopper to meet all their needs in one place.

Similarly to Athleta, Zella has decided to tackle both the plus size, as well as the

children’s market, making them more accessible to a wider range of consumers. (Zella)

Perhaps their biggest strength, however, is their developing connection to the fitness

community. One their website, Zella connects you to their “Zella PROs,” or the fitness

experts they’ve identified in your area that can assist you in achieving your athletic

pursuits. This level of integration with their consumer’s lives is what will set Zella apart

from their competitors. (Zella)

13

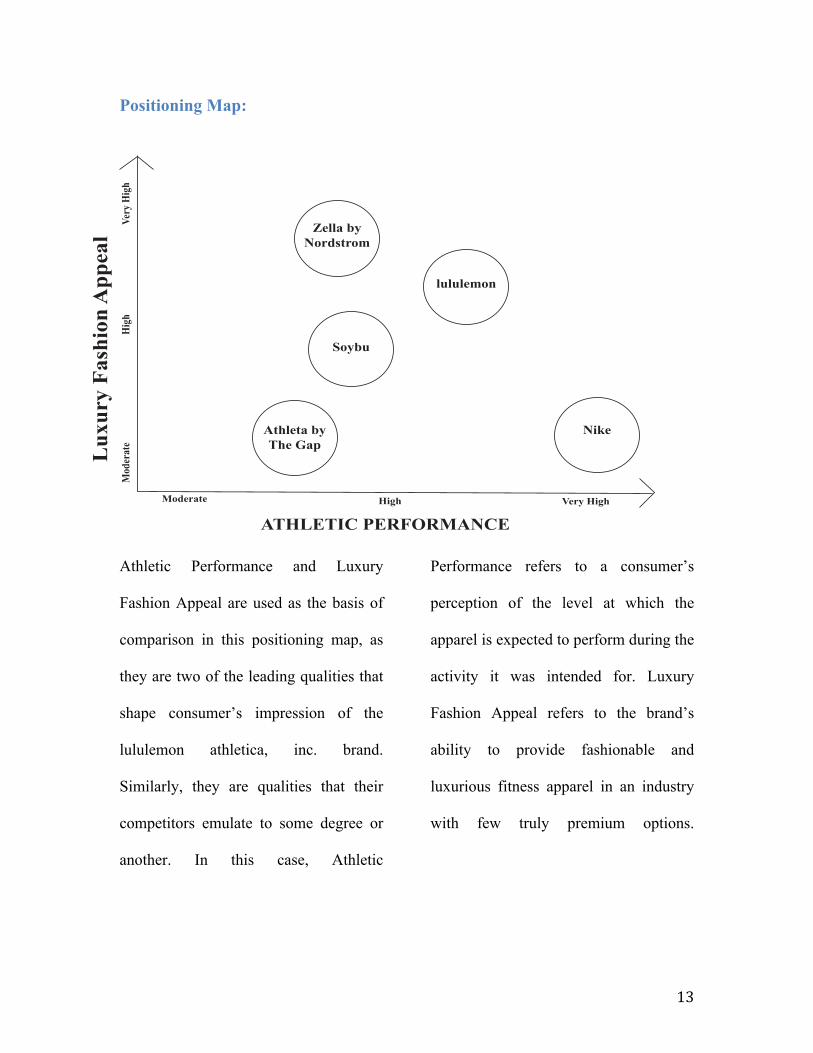

Positioning Map:

Athletic Performance and Luxury

Fashion Appeal are used as the basis of

comparison in this positioning map, as

they are two of the leading qualities that

shape consumer’s impression of the

lululemon athletica, inc. brand.

Similarly, they are qualities that their

competitors emulate to some degree or

another. In this case, Athletic

Performance refers to a consumer’s

perception of the level at which the

apparel is expected to perform during the

activity it was intended for. Luxury

Fashion Appeal refers to the brand’s

ability to provide fashionable and

luxurious fitness apparel in an industry

with few truly premium options.

ATHLETIC PERFORMANCE

Moderate High Very High

Lux

ury

Fash

ion

App

eal

Mod

erat

eH

igh

Very

Hig

h

lululemon

Nike

Zella by Nordstrom

Soybu

Athleta byThe Gap

14

SWOT Analysis: Strengths:

- Strong relationships with fitness professionals created through their fitness

ambassador program where feedback is then received to improve product (“Our

Ambassadors”)

- Ambassador program emphasizes community outreach through the offering of

free yoga classes that are open to the public, which in turn builds a community of

loyal lululemon followers (“Our Ambassadors”)

- lululemon athletica, inc. developed and copyrighted textiles such as “Luon” to

differentiate themselves from their competitors (“Textiles”)

- Strong brand identity within the yoga community, but the average consumer also

has top-of-mind recognition if they were to seek out active-wear or lifestyle

apparel

- The quality of the garments is backed up with a guarantee that if the product is not

performing to the extent you believed it would, you can bring it back to any

location at any time (“Our Quality Promise”)

Weaknesses:

- Widely perceived as overpriced with quality that does not match consumer’s

expectations (Peterson, 2014)

- Faced largely publicized criticism and controversy over “sheer pants” and the

subsequent comments made by founder and former CEO, Chip Wilson. It has

been hard for the brand to recover from these issues (Suddath) (Peterson, 2013)

- Limited sizing with no maternity or plus sizes, current size offering of 2-12 and

no differentiation between petite or tall (lululemon athletica, inc.)

15

- lululemon athletica, inc. encountered a number of supply chain issues due to

quality control, resulting in a shortage of inventory for sale (Lutz)

- lululemon is perceived as having a largely female focus, which leads them to miss

out on the men’s apparel market, which is growing exponentially (StatsCan)

Opportunities:

- Extended sizing to expand customer base

- Extend categories of active-wear outside of yoga and running

- Collaboration with non-athletic brands to increase their overall retail market share

- Extend the ambassador program to those who are indirectly involved in the fitness

community

- Manufacture products rather than relying on third-party manufacturing, thus

establishing consistent quality control through total quality management (TQM)

Threats:

- Stock prices have fallen dramatically in recent times, scaring off potential

investors (Caplinger)

- Competitors such as Nike offer a wider set of athletic apparel goods, such as

swimwear and skiing apparel which may entice consumers to shop with them for

all their athletic goods needs (Nike)

- Threat of new entrants to the market with similar products at a much more

competitive and affordable price-point, such as Athleta (Peterson, 2014)

- While the sporting goods industry is currently booming, this is largely an

unprecedented trend with risk associated that the trend will reach stagnancy at

some point, leaving lululemon with little to provide to their customers (StatsCan)

16

- Competition from not only new active-wear entrants, but also from established

luxury brands that introduce a higher-end client, such as that of Nordstrom and

their Zella subsidiary

Strategic Moves: lululemon athletica, inc. has made many strategic moves to get where they are

today, ranging from the development of proprietary textiles, to their ambassador initiative

mentioned above. However, it is their move towards the younger generation that is

garnering attention at present. With their introduction of Ivivva, lululemon has positioned

themselves to gain a greater market share, as well as to implant themselves in the entire

household of their consumer. (Shaw B.2)

Though lululemon is relatively accessible today with numerous locations across

major cities in North America, they are still cognizant of the fact that in order to retain

their market share, they must be as accessible as possible. As a result, they have made the

strategic decision to invest heavily in ecommerce, as well as to utilize warehouses,

showrooms, and temporary locations to broaden their sales avenues and increase brand

awareness. (Investopedia)

17

Promotional Calendar

18

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Friday

Saturday

78

910

1112

13

1415

1617

1819

20

2122

2324

2526

27

2829

12

34

5

Feb=16

Valen

@nesAA

DayA

SportsABraAP

romo@

onA

19

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Frida

ySaturday

67

89

1011

12

1314

1516

1718

19

2021

2223

2425

26

2728

2930

311

2

34

56

78

9

Mar<16

20

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Friday

Saturday

1011

1213

1415

16

1718

1920

2122

23

2425

2627

2829

30

12

34

56

7

Apr>1

6

Wom

en'sAAccessoriesAP

romoD

onA

21

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Friday

Saturday

89

1011

1213

14

1516

1718

1920

21

2223

2425

2627

28

2930

311

23

4

May<16

Mothe

r's>>

Day>

22

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Friday

Saturday

56

78

910

11

1213

1415

1617

18

1920

2122

2324

25

2627

2829

301

2

34

56

78

9

Jun=16

Father's?

Day?

Men

's?Yo

ga?Pant?P

romoE

on?

Semi=A

nnual?Sale:?Sp

ring/Summer?

23

Sund

ayMon

day

Tuesday

Wed

nesday

Thursday

Friday

Saturday

1011

1213

1415

16

1718

1920

2122

23

2425

2627

2829

30

311

23

45

6

Jul>1

6

24

Promotional Calendar Details by Month:

February: • Fashion must-haves for this month include our signature legging that has been

outfitted with a full fleece lining to keep you warm in the coldest months. We’re

also featuring our transitional parka designed in an Anorack style with a

removable hood.

• The above items have been bought in volume and will be featured during the

month as indicated by their position on the February calendar. We will also be

increasing our purchases for women’s sports bras for this month to accommodate

the needs of our Valentine’s Day promotion.

25

• The month of February will see our first promotion for the Spring/Summer 2016

season. We will be featuring all women’s sports bras in a “Buy One, Get One

Half Price” promotion. Limit of four sports bras per customer.

March: • Fashion must-haves for March include our top-selling convertible long-sleeve top.

This top can be worn in three styles: full long-sleeve, tank top, or long-sleeve

crop. The latter half of the month will see a feature on our cinched-waist rain

jacket with removable hood.

• Both styles shown above will be bought in volume for this month and will need to

be featured according to allocation shown March calendar.

• There will be no sales promotions for the month of March outside of regular

markdowns.

26

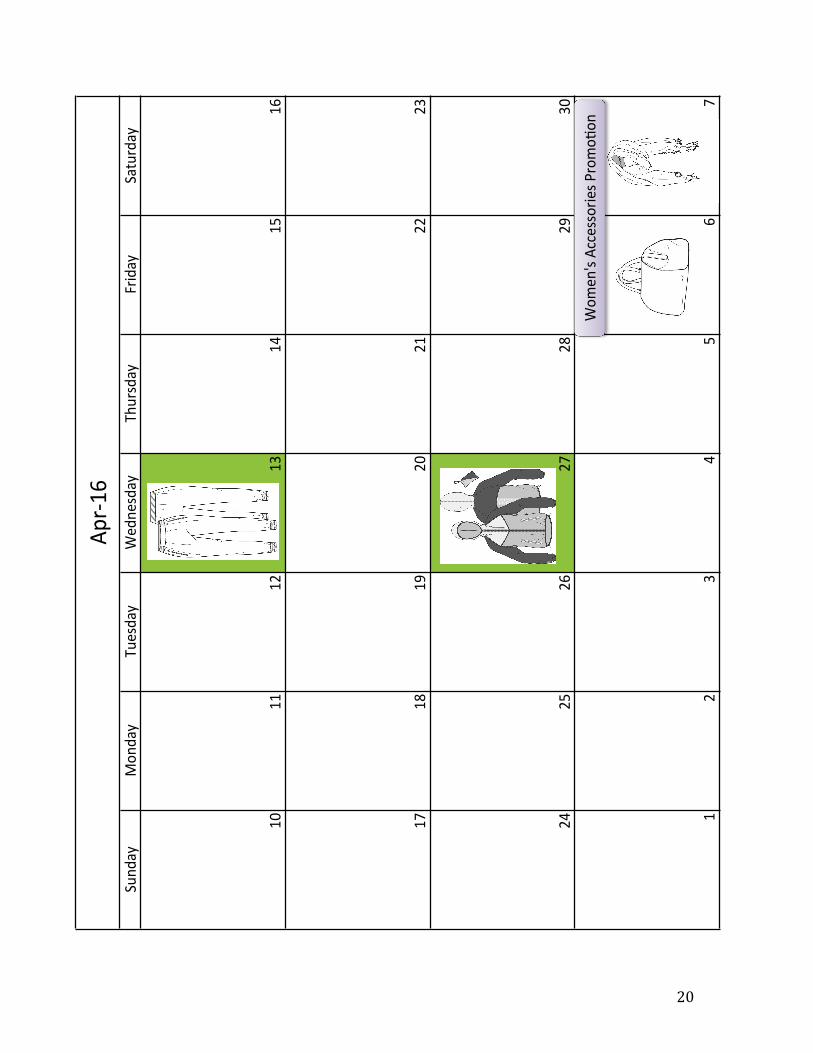

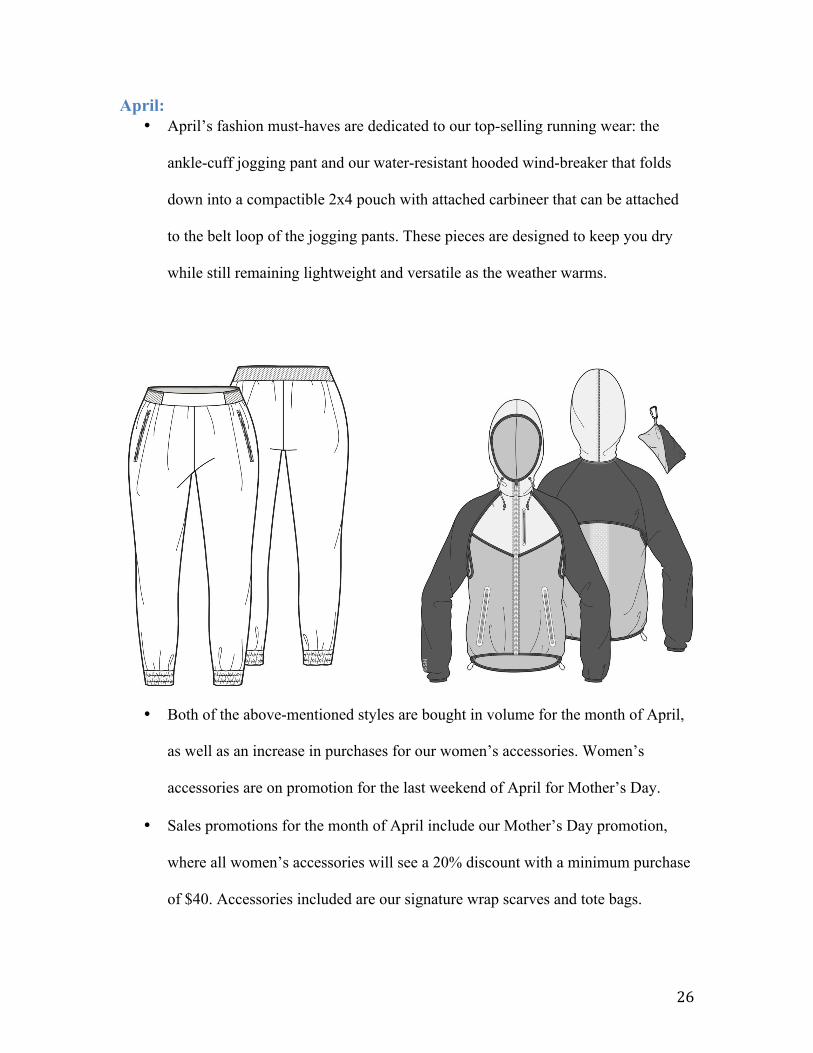

April: • April’s fashion must-haves are dedicated to our top-selling running wear: the

ankle-cuff jogging pant and our water-resistant hooded wind-breaker that folds

down into a compactible 2x4 pouch with attached carbineer that can be attached

to the belt loop of the jogging pants. These pieces are designed to keep you dry

while still remaining lightweight and versatile as the weather warms.

• Both of the above-mentioned styles are bought in volume for the month of April,

as well as an increase in purchases for our women’s accessories. Women’s

accessories are on promotion for the last weekend of April for Mother’s Day.

• Sales promotions for the month of April include our Mother’s Day promotion,

where all women’s accessories will see a 20% discount with a minimum purchase

of $40. Accessories included are our signature wrap scarves and tote bags.

27

May: • Fashion must-haves in May are all about functional layers: our sleeveless puffy

vest to add just the right amount of warmth on your morning jog, as well as our

hooded racer-back sweater which is the perfect layer over any of our sports-bras

while at the gym or practicing yoga outdoors.

• Layering merchandise shown above will be bought in volume and featured

according to the promotional calendar.

• There will be no sales promotions for the month of May.

28

June: • June is our highest sales month of the season, as it includes three features during

the month on all of our top-selling summer merchandise, as well as our Father’s

Day promotion and our Semi-Annual Sale. Fashion must-haves for June include

our customer favourite backless yoga tank, our classic sport short, and a brand

new style for this season, our loose and airy blouson maxi-romper. All of these

pieces are perfect for the warm weather.

29

• Volume buys for the month of June include all of the aforementioned

merchandise, as well as an increase in purchases on our men’s yoga pants to

support our Father’s Day promotion. We will also see leader-priced goods during

our semi-annual sale in the fourth week of June. These goods will not remain at a

permanent markdown and will return to their regular price at the end of the week.

Feature will be taken on these goods during this week, shortening the feature life

of our sport short.

• Sales promotions are in full effect in June as we near the end of our

Spring/Summer 2016 season. Items included in our semi-annual sale are: our

classic high-rise and low-rise leggings, ladies zip-up and hoodies, ladies

intimates, select top styles, and remaining coats and jackets from earlier in the

season. We will also see a promotion earlier in the month from the men’s

department on yoga pants for Father’s Day. The promotion will run for the

weekend and will see 30% off with minimum purchase of $50.

July: • The end of the season sees fashion must-haves that are necessities year-round,

such as our cropped layering hoodie that can be worn on it’s own in the summer

months, or over a long sleeve knit as the weather starts to cool again. We also see

a feature on our women’s intimates, as these remain one of our top-selling items

regardless of season.

30

• The above merchandise will be purchased in volume for the month of July and

will be featured according to the monthly promotional calendar.

• There will be no sales promotions for the month of July, save for regularly

scheduled markdowns on slow moving summer merchandise.

31

Merchandise Plan

32

%$

%$

BOS

54.5%

93,708

///////////

54.5%

84,993

//////////

Purchases

54.5%

424,908

/////////

54.5%

401,420

////////

EOS

54.5%

518,616

/////////

54.5%

486,413

////////

25%

151,250

/////////

30%

165,000

2.5%

15,125

///////////

2.5%

13,750

//////////

1%6,050

//////////////

1%5,500

////////////

40.99%

247,990

/////////

38.71%

212,905

////////

3.1

3.1

/////////////////

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Last/Year

77,000

94,600

83,600

94,600

136,400

63,800

550,000

Plan

84,700

//////////

104,060

////////

91,960

/////////

104,060

/////////

150,040

////////

70,180

//////////

605,000

//////////////

10.00%

T/D/L/Year

77,000

171,600

255,200

349,800

486,200

550,000

T/D/Plan

84,700

//////////

188,760

////////

280,720

///////

384,780

/////////

534,820

////////

605,000

////////

August

Avg./Stock

Last/Year

155,950

172,000

////////

167,000

186,500

205,500

176,000

177,500

177,207

////////

Plan

171,941

////////

189,389

////////

183,920

///////

204,998

/////////

226,560

////////

193,697

////////

195,339

195,121

////////

Last/Year

19,310

21,200

16,000

18,970

59,320

30,200

165,000

30%

Plan

17,696

//////////

19,436

//////////

14,671

/////////

17,394

///////////

54,374

//////////

27,679

//////////

151,250

//////////////

25%

T/D/L/Year

19,310

40,510

56,510

75,480

134,800

165,000

T/D/Plan

17,696

//////////

37,132

//////////

51,803

/////////

69,197

///////////

123,571

////////

151,250

////////

Last/Year

112,360

////////

110,800

////////

119,100

///////

132,570

/////////

166,220

////////

95,500

//////////

736,550

//////////////

Plan

119,844

////////

118,026

////////

127,709

///////

143,016

/////////

171,551

////////

99,501

//////////

779,648

//////////////

5.85%

T/D/L/Year

112,360

////////

223,160

////////

342,260

///////

474,830

/////////

641,050

////////

736,550

////////

T/D/Plan

119,844

////////

237,871

////////

365,580

///////

508,596

/////////

680,147

////////

779,648

////////

Last/Year/%

54.5%

54.5%

54.5%

54.5%

54.5%

54.5%

54.5%

Last/Year/$

61,236

//////////

60,386

//////////

64,910

/////////

72,251

///////////

90,590

//////////

52,048

//////////

401,420

//////////////

Plan/%

54.5%

54.5%

54.5%

54.5%

54.5%

54.5%

54.5%

Plan/$

61,236

//////////

64,324

//////////

69,602

/////////

77,944

///////////

93,495

//////////

54,228

//////////

424,908

//////////////

SixRMon

th/

Merchandisin

g/Plan

Departmen

t:/Lululemon

/Wom

en's/Wear

Results/fo

r/Season

Plan/This/Y

ear

Buyer:/Kati/Woo

d

Actual/La

st/Year

Remarks

Sales/+

10%////////////////

Markdow

ns/R5

%/of/Sales/

Purchases/+

5.85%////////////

Markup/remains/th

e/same/on

/pu

rchases/////////////////////////////

Gross/P

rofit/+2.28%

Sprin

g/Summer/Season

Markup Markdow

nsStock/Shortage

Workroo

mGross/P

rofit

Turnover

Initial/

Markup

Season

/Total

%/Change

Fall/Winter

Sprin

g/Summer

Sales

Retail/Stock/

(BOM)

Markdow

ns

Retail/

Purchases

33

%$

%$

BOS

0.545

=C20*E

50.5

45=G

5*C19

Purcha

ses0.5

45=I2

6*E6

0.545

=I25*G

6EO

S0.5

45=F5

+F60.5

45=H

5+H6

0.25

=I22

0.3=I2

10.0

25=I1

6*E9

0.025

=I15*G

90.0

1=E1

0*I16

0.01

=G10*

I15=I3

1@(((J2

2+E9)*

(1@I31

))+E10

)=0.409

9*I16

=I29@(

((J21+G

9)*(1@

I29)+G

10))=0.387

1*I15

=I16/J

20=I1

5/J19

Aug

Sept

OctNo

vDe

cJan

FebMa

rAp

rMa

yJun

JulLas

tUYear

77000

94600

83600

94600

136400

63800

=C15+D

15+E15

+F15+G

15+H1

5Pla

n=0.

14*I16

=0.172

*I16

=0.152

*I16

=0.172

*I16

=0.248

*I16

=0.116

*I16

=(J16*

I15)+I1

50.1

T/DUL/Y

ear=C1

5=C1

5+D15

=D17+

E15=E1

7+F15

=F17+G

15=G

17+H1

5T/D

UPlan

=C16

=C18+D

16=D

18+E16

=E18+F

16=F1

8+G16

=G18+

H16

Augus

tAvg

.UStock

LastUYe

ar155

950172

000167

000186

500205

500176

000177

500=(C

19+D1

9+E19+

F19+G

19+H1

9+I19)

/7Pla

n=2.

03*C16

=1.82*

D16

=2*E16

=1.97*

F16=1.

51*G1

6=2.

76*H1

6195

339=(C

20+D2

0+E20+

F20+G

20+H2

0+I20)

/7Las

tUYear

19310

21200

16000

18970

59320

30200

=C21+D

21+E21

+F21+G

21+H2

10.3Pla

n=0.

117*I2

2=0.

1285*I

22=0.

097*I2

2=0.

115*I2

2=I2

2*0.35

95=I2

2*0.18

3=I1

6*J22

0.25

T/DUL/Y

ear=C2

1=C2

3+D21

=D23+

E21=E2

3+F21

=F23+G

21=G

23+H2

1T/D

UPlan

=C22

=C24+D

22=D

24+E22

=E24+F

22=F2

4+G22

=G24+

H22

LastUYe

ar=C1

5+D19+

C21@C1

9=D

15+E19

+D21@

D19

=E15+F

19+E21

@E19

=F15+G

19+F21

@F19

=G15+

H19+G

21@G1

9=H

15+I19

+H21@

H19

=SUM(

C25:H2

5)Pla

n=C1

8+D20+

C22@C2

0=D

16+E20

+D22@

D20

=E16+F

20+E22

@E20

=F16+G

20+F22

@F20

=G16+

H20+G

22@G2

0=H

16+I20

+H22@

H20

=SUM(

C26:H2

6)=(I2

6@I25)/

I25T/D

UL/Year

=C25

=C27+D

25=D

27+E25

=E27+F

25=F2

7+G25

=G27+

H25

T/DUPla

n=C2

6=C2

8+D26

=D28+

E26=E2

8+F26

=F28+G

26=G

28+H2

6Las

tUYearU%

0.545

0.545

0.545

0.545

0.545

0.545

0.545

LastUYe

arU$=C2

9*C25

=D29*

D25

=E29*E

25=F2

9*F25

=G29*

G25

=H29*

H25

=I29*I

25Pla

nU%0.5

450.5

450.5

450.5

450.5

450.5

450.5

45Pla

nU$=C3

1*C27

=D31*

D26

=E31*E

26=F3

1*F26

=G31*

G26

=H31*

H26

=I31*I

26

RetailU

Purcha

ses

InitialU

Marku

p

Season

UTotal

%UChan

geSpr

ing/Su

mmer

Sales

RetailU

StockU

(BOM)

Markd

owns

Markd

owns

StockU

Shorta

geWo

rkroom

GrossUP

rofit

Turnov

erFal

l/Winte

r

Six@M

onthUM

erchan

dising

UPlan

Depar

tment

:ULulule

monUW

omen'

sUWear

Buyer:

UKatiUW

ood

Results

UforUSe

ason

PlanUT

hisUYe

arAct

ualULa

stUYear

Remark

sSal

esU+10

%UUUUUUU

UUUUUUUUUM

arkdow

nsU@5%

UofUSal

esUPur

chases

U+5.85

%UUUUUUU

UUUUUMa

rkupUre

mains

UtheUsam

eUonU

purcha

sesUUUUU

UUUUUUUUUU

UUUUUUUUUU

UUUUGros

sUProf

itU+2.2

8%

Spring

/Summ

erUSeas

on

Marku

p

34

Merchandise Plan Justifications:

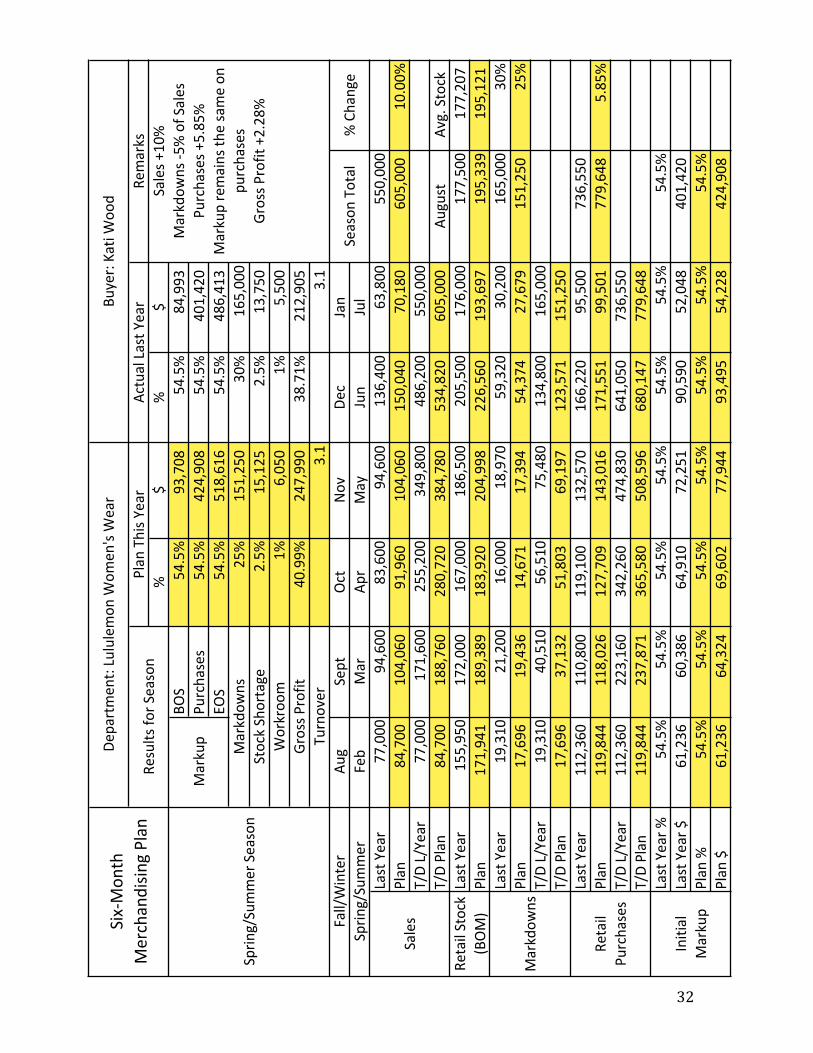

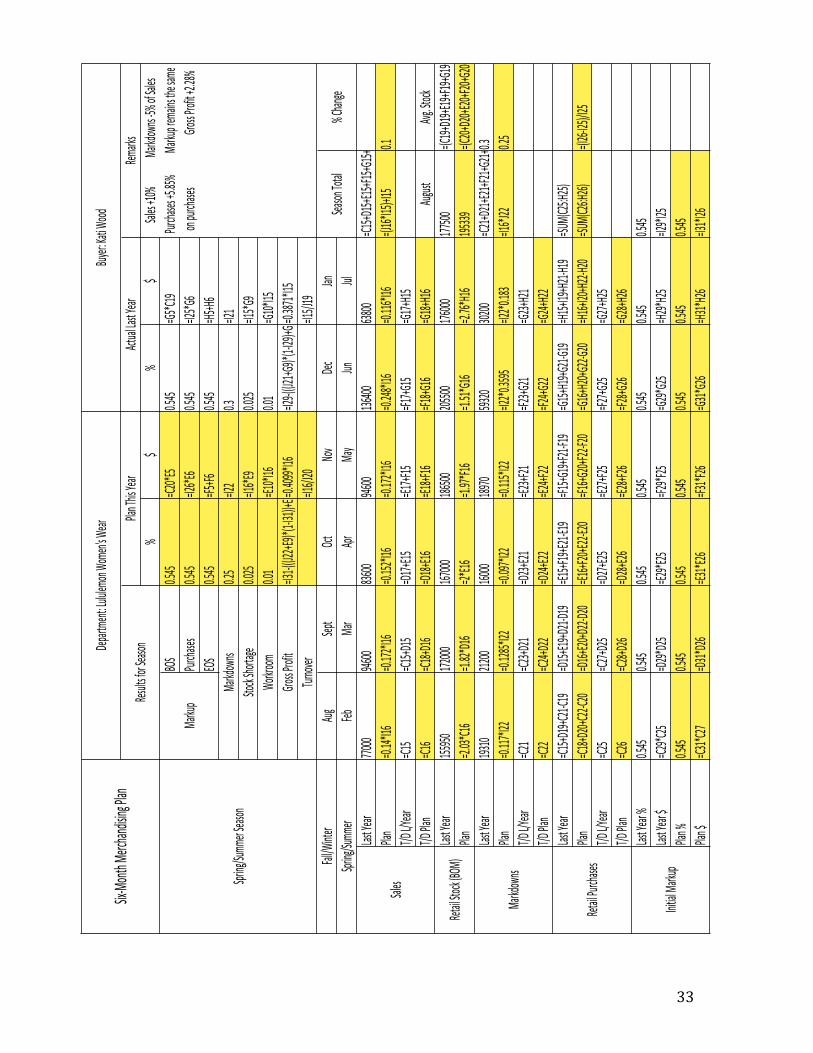

Sales: • Though the actual percentage of growth has been dropping incrementally over the

last three years, we are still seeing between a 12-16% growth in sales annually

from 2013-15. This historical data helps to justify the 10% increase in sales we

are forecasting for this Spring/Summer season (Annual Report, p.18)

• Canadian retail sales in general are up for the second quarter of 2015, with growth

of 25% over the first quarter of 2015 according to Stats Canada (“StatsCan”)

• Instead of maintaining our 12% growth increase from last year, we chose to

temper this and decrease our growth to only 10%, which was largely decided

based on the current rise in Canadian unemployment rates and the inevitable

effect this has on consumer spending (Younglai)

• The consumer trend towards researching goods via online sources will play a role

in our sales as well this season. We have invested heavily in e-commerce as one

of our strategic moves, which market research shows consumers are depending on

more and more prior to making a buying decision in-store (Thangavelu)

• Our success in building relationships with fitness professionals will continue to

drive our sales, especially during these summer months when our running

programs are at their peak and consumers are looking to get back into shape (“Our

Ambassadors”)

• Introduction of the new Ivivva line for the younger generation will bring a

secondary target consumer into our already existing locations, improving the

likelihood of cross-selling and thus increasing our sales overall (Shaw B.2)

35

• Net revenue increase for the last two years was driven by sales from new stores

and the growth of our direct to consumer segment, as well as increased sales at

locations in comparable stores. Knowing this, our prediction that this trend will

continue is well founded (Annual Report, p.24)

• Internally, we recognize that our ability to properly anticipate and respond

effectively to our customer preferences for technical athletic apparel is one of our

biggest attributing factors to our consistent sales growth annually (Annual Report,

p.28)

• Gross profit increased for fiscal 2014 by 9%, allowing for more cash flows and

increased buying potential. This will allow us to increase our purchases, which

directly correlates with an increase in sales (Annual Report, p. 20)

• Lululemon athletica inc. has always maintained a strong brand identity within the

yoga community, however with the growth in the activewear market we are now

seeing top-of-mind recognition from our secondary market as well, such as

lifestyle consumers and other athletic enthusiasts, which will increase our market

reach and thus our sales

• Fiscal 2014 saw a focus on our product assortment, guest experiences, and our

“go-to-market process” for our products. This improved our product assortment

and helped to enhance our guest experience, contributing to improved total

comparative sales performance. With plans in motion for these initiatives to

continue, it follows that our sales growth can be predicted as well (Annual Report,

p. 19)

• Monthly sales distribution will remain the same, with our highest sales percentage

36

falling in June, consistent with our semi-annual sale

Markdowns: • Markdowns will see a 5% decrease, from 30% of sales in 2015, to 25% of sales in

the 2016 Spring/Summer season. This decrease is attributed to a number of

factors both internally, and externally, such as the increase in retail spending by

Canadians. Given the surge in retail spending in the second quarter of 2015, we

know that Canadians buying power is up, allowing for a decreased necessity of

markdowns to combat low consumer spending (“StatsCan”)

• Internally, we were affected last year by distribution issues with our top-selling

women’s bottoms. The bottoms were recalled due to quality issues, resulting in a

need for quick reproduction and reintroduction to market, however they missed

their prime selling season and resulted in higher markdowns for the season (Lutz)

• Though we are forecasting an increase in sales of 10%, we are only raising our

purchases budget incrementally by 5.85% over the season. This will ensure that

we are not over-buying, which is the number one reason for increased markdowns

(Carter)

• Monthly distribution of markdown dollars will remain the same, with the highest

percentage allocated to June at 35.95% to accommodate our semi-annual sale

Markup: • We will be keeping our markup percentage the same at 54.5%. We will not be

affected this year by an increase in the cost of our goods, so our retail prices will

be able to remain the same

• We must remain competitive in this growing athleisure market, ensuring our

37

competitive position remains high. If we raise our prices without demonstrating a

new added value, our customer will seek new alternatives

• Increasing markup percent can have a negative effect on resulting markdown

dollars, as customers will not be willing to pay the higher price. Similarly, if we

were to decrease our initial markup, customers may become suspicious that our

value would be decreasing, which may lead them to turn to our competitors

• The most effective way for us to continue to achieve this markup percentage is by

ensuring our customer always sees the added value in purchasing our

merchandise. This will consist of quality control in all areas of our business to

ensure customer perception of high-quality goods, as well as maintaining the

social community that our brand has created that drives our sales exponentially

each season. It will also mean that we will need to manage our markdowns

carefully, while ensuring that we keep our operating expenses to a minimum

38

Classification List/Investment Summary

39

40

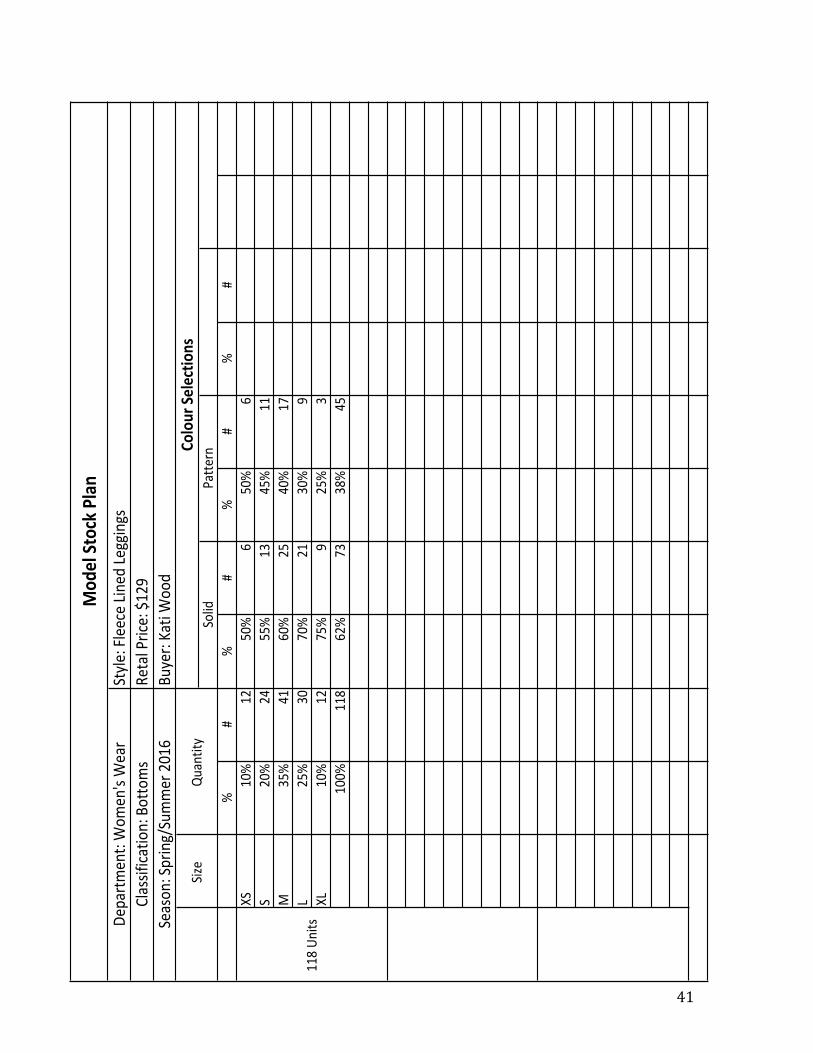

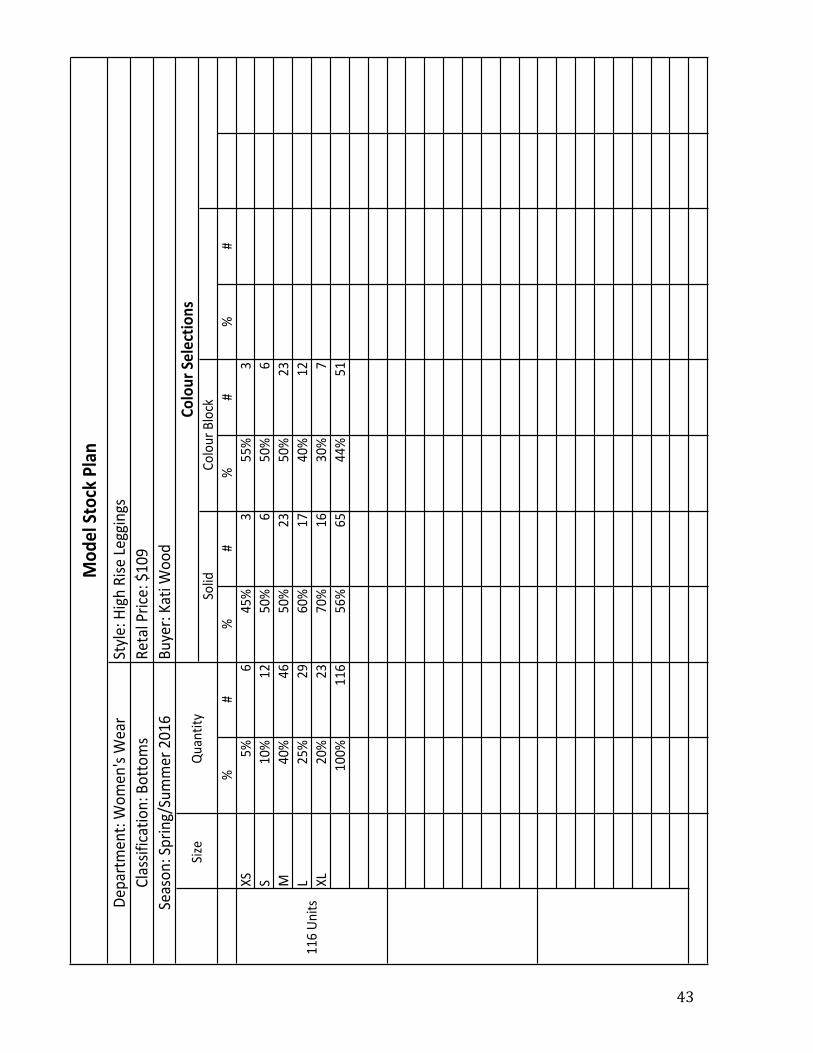

Model Stock Plans

41

%#

%#

%#

%#

XS10%

1250%

650%

6S

20%

2455%

1345%

11M

35%

4160%

2540%

17L

25%

3070%

2130%

9XL

10%

1275%

925%

3100%

118

62%

7338%

45

Colour&Se

lections

Solid

Patte

rnSiz

e<Qu

antity<

118<Un

its<

Mod

el&St

ock&P

lan

Departm

ent:<Wom

en's<Wear

Style

:<Fleece<Lin

ed<Le

ggings

Retal<Price:<$129

Buyer:<Kati<Woo

dClassifica

tion:<Bottoms

Season

:<Spring/Summer<2016

42

%#

%#

%#

%#

XS15%

1940%

835%

725%

5S

20%

2640%

1030%

830%

8M

30%

3845%

1725%

1030%

12L

25%

3250%

1625%

825%

8XL

10%

1360%

815%

225%

3100%

128

46%

5927%

3428%

35

1281Un

its1

Size1

Quantity1

Colour&Se

lections

Solid

Patte

rnCo

lour1Block

Season

:1Spring/Summer12016

Buyer:1Kati1Woo

d

Mod

el&St

ock&P

lan

Departm

ent:1Wom

en's1Wear

Style

:1Yoga1C

rop

Classifica

tion:1Bottoms

Retal1Price:1$99

43

%#

%#

%#

%#

XS5%

645%

355%

3S

10%

1250%

650%

6M

40%

4650%

2350%

23L

25%

2960%

1740%

12XL

20%

2370%

1630%

7100%

116

56%

6544%

51

1160Units0

Size0

Quantity

0Co

lour&Selectio

nsSolid

Colour0Block

Season

:0Spring/Summer02016

Buyer:0Kati0W

ood

Mod

el&Stock&Plan

Dep

artm

ent:0W

omen

's0W

ear

Style:0High0Rise0Leggings

Classification:0Bottoms

Retal0Price:0$109

44

%#

%#

%#

%#

XS20%

1945%

855%

10S

40%

3750%

1950%

19M

25%

2355%

1345%

10L

10%

965%

635%

3XL

5%5

75%

325%

1100%

9353%

4947%

44

931Units

Size1

Quantity1

Colour&Se

lections

Solid

Patte

rn

Season

:1Spring/Summer12016

Buyer:1Kati1Woo

d

Mod

el&St

ock&P

lan

Departm

ent:1Wom

en's1Wear

Style

:1Low

1Rise

1Leggings

Classifica

tion:1Bottoms

Retal1Price:1$129

45

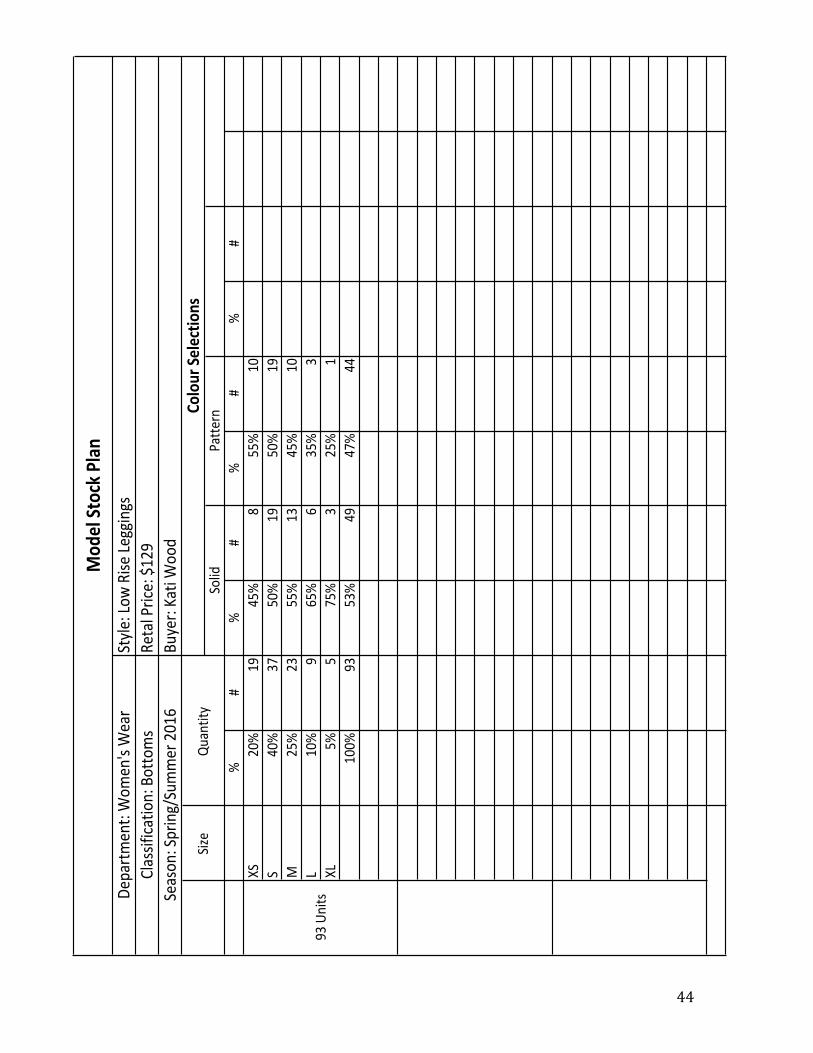

Model Stock Plan Explanation: The four styles that were chosen to be purchased for the month of February are

our two classic lifestyle styles, the high-rise and low-rise leggings, our most popular yoga

style, the yoga crop, and our top-selling cold-weather style, the full-fleece legging. The

classic high- and low-rise leggings remain our top-selling bottom, as they are the most

versatile in our collection. They can be worn in everyday life, and then transition

seamlessly to any type of exercise you choose to do. They are also available in two

different rises, the high or low, to accommodate a wide range of body types and comfort

preferences. The yoga crop was purchased in the February budget, as it is our top-selling

yoga-specific pant. The cropped length allows for freedom of movement in all yoga

positions, and ensures the wearer will not overheat if she chooses to practice hot yoga or

higher intensity classes. Finally, our seasonal full-fleece legging, which is modeled after

our original high-rise legging, is stocked in February to allow the lululemon woman to

wear her favourite legging style while still combatting the elements in the colder months

of the year. We recognize that her busy lifestyle keeps her on the go, necessitating a style

that can take her through her whole day with ease.

46

Works Cited Athleta. “Athleta.” Athleta. Athleta, 2015. Web. 15 Oct. 2015.

“Annual Report.” Investor Relations. lululemon athletica, inc., 2014. Web. 18 Nov. 2015.

Bagnall, James. "Economy in Recovery, Conference Board Says; Group Foresees Growth

of 1.6% this Year, 2.1% Next Year and 2.2% in 2017." The Ottawa CitizenSep 24

2015. ProQuest. Web. 15 Oct. 2015.

Brooke, Eliza. “What’s Next for Lululemon.” Fashionista. n.p., 31 January 2014. Web.

15 Oct. 2015.

Caplinger, Dan. “Why Lululemon Athletica has Crashed 30% in 2013.” Fool.com. n.p., 4

October 2014. Web. 19 Oct. 2015.

Carter, Linda. “Retail Markdowns.” Smyth Retail. n.p., 16 July 2013. Web. 18 Nov. 2015.

Donnelly, Christopher. “Who Are the Millennials?” Accenture. n.p., n.d. Web. 15 Oct.

2015.

“Ecommerce Has Room to Grow.” FirstData. n.p., 20 April 2015. Web. 12 Oct. 2015.

"Good Signs for Economy Despite Ongoing Weakness in Energy Sector, Says RBC."

Telegraph-JournalSep 23 2015. ProQuest. Web. 21 Oct. 2015.

Kopun, Francine. "Millennials Turning Away from Big Brands." Toronto Star. Aug 14

2015. ProQuest. Web. 21 Oct. 2015.

Lululemon athletica, inc. “About Us.” lululemon athletica, inc. lululemon athletica, inc.,

2015. Web. 15 Oct. 2015.

Lululemon athletica, inc. “lululemon athletica, inc.” lululemon athletica, inc. lululemon

athletica, inc., 2015. Web. 15 Oct. 2015.

47

Lululemon athletica, inc. “Our Ambassadors.” lululemon athletica, inc. lululemon

athletica, inc., 2015. Web. 15 Oct. 2015.

Lululemon athletica, inc. “Our Quality Promise.” lululemon athletica, inc. lululemon

athletica, inc., 2015. Web. 15 Oct. 2015.

Lululemon athletica, inc. “Textiles.” lululemon athletica, inc. lululemon athletica, inc.,

2015. Web. 15 Oct. 2015.

Lutz, Ashley. “Hot Brands Vying to be the Next Lululemon.” Business Insider. n.p., 20

March 2013. Web. 19 Oct. 2015.

McKnight, Zoe. "A Look Inside the Cult of Lululemon; Clothing Maker Urges

Employees to 'Work on Self First'." The GazetteAug 20 2013. ProQuest. Web. 21

Oct. 2015.

Nike. “Nike.” Nike. Nike, 2015. Web. 15 Oct. 2015.

Nordstrom. “Zella.” Nordstrom. Zella, 2015. Web. 12 Oct. 2015.

Olive, David. "It's Time to Upgrade our 'Mediocre' Economy." Toronto StarOct 14 2015.

ProQuest. Web. 21 Oct. 2015.

Peterson, Elizabeth. “8 Outrageous Remarks by Lululemon’s Founder.” Business Insider.

n.p., 10 December 2013. Web. 19 Oct. 2015.

Peterson, Elizabeth. “Lululemon’s Pants Not Worth That Much More than

Competition’s.” Business Insider. n.p., 24 September 2014. Web. 19 Oct. 2015.

Shaw, Hollie. "Lululemon Puts PR Disasters Behind it; Shares Jump as Q3 Results Beat

Estimates." National PostDec 12 2014. ProQuest. Web. 21 Oct. 2015.

48

Shaw, Hollie. "Wooing Young Shoppers Pays Off for Lululemon; Yogawear Company's

Stock Jumps 14% After Expectations Topped." Edmonton JournalSep 12 2014.

ProQuest. Web. 21 Oct. 2015.

Soni, Phalguni. “Why Valuations are Jumping for Lululemon Athletica.” Market Realist.

n.p., 13 April 2015. Web. 15 Oct. 2015.

Soybu. “Soybu.” Soybu. Soybu, 2015. Web. 14 Oct. 2015.

"StatsCan Says Spending Up Despite Slump in Oil." Leader PostOct 15 2015. ProQuest.

Web. 21 Oct. 2015.

Statistics Canada. “Canada’s Changing Retail Market.” Government of Canada, 2 August

2013. Web. 19 Oct. 2015.

Statistics Canada. “Retail Sales by Industry: Monthly.” Government of Canada, 23

September 2015. Web. 19 Oct. 2015.

Suddath, Claire. “What Lululemon’s Yoga Pant Recall Reveals.” Business Week. n.p., 28

March 2013. Web. 19 Oct. 2015.

Thangavelu, Poonkulali. “Understanding Lululemon’s Business Model.” Investopedia.

n.p., 28 May 2015. Web. 13 Oct. 2015.

Younglai, Rachelle. "Jobless Rate Highest since February of Last Year." The Globe and

Mail. 10 October 2015. ProQuest. Web. 21 Oct. 2015.

All Images Sourced from WGSN:

WGSN. “Women’s Active.” WGSN. n.p, November 2015. Web. 18 Nov. 2015.

49

Appendix