Dec 2012

The research leading to these results has received funding from the

European Union´s 7th Framework Programme (FP7/2007-2013) for

the Fuel Cells and Hydrogen Joint Undertaking Technology Initiative

under Grant Agreement Number 303462.

European-wide deployment of residential fuel cell micro-CHP Fuel Cells for Stationary

Power Applications

Fuel Cells Network Webinar, 12 February 2016

Agenda

1. Introduction to the ene.field project

2. Lessons learned to-date

3. Preliminary findings

1. Technical monitoring

2. Forthcoming research and analysis

2

Commercialisation: joint JU FCH /private sector

• 88 million euro in demo-type projects for energy applications

• Energy projects still strongly R&D oriented

• 28 demo projects

– 12 field demonstrations

– 16 proof-of-concept, components, diagnostics and control

• Currently distributed in 3 different application areas:

– Hydrogen Production and Storage

– Stationary applications and CHP

– Early markets (Back-up power and off-grid systems)

• Almost 50% of the budget committed to ENERGY oriented projects

3

v

Introduction to ene.field

• ene.field is the largest European demonstration of the latest smart energy solution for private homes, fuel cell micro-CHP.

• It will deploy up to 1,000 Fuel Cell heating systems in 8 key European member states.

• Project duration of 5 years. Systems will be demonstrated for 2 to 3 years.

• Outputs of the project include: Detailed performance data, lifecycle cost and environmental assessments, market analysis, commercialisation strategy.

Countries where units are currently expected to be installed

4

The consortium brings together 26 partners including:

• the leading European FC micro-CHP developers,

• leading European utilities,

• leading research institutes,

• partners in charge of dissemination and coordination of the project.

ene.field is a European platform for FC mCHP

The Fuel Cells and Hydrogen Joint Undertaking (FCH JU) is

committing c. €26 million to ene.field under the EU's 7th

Framework Programme for funding research and

development.

5

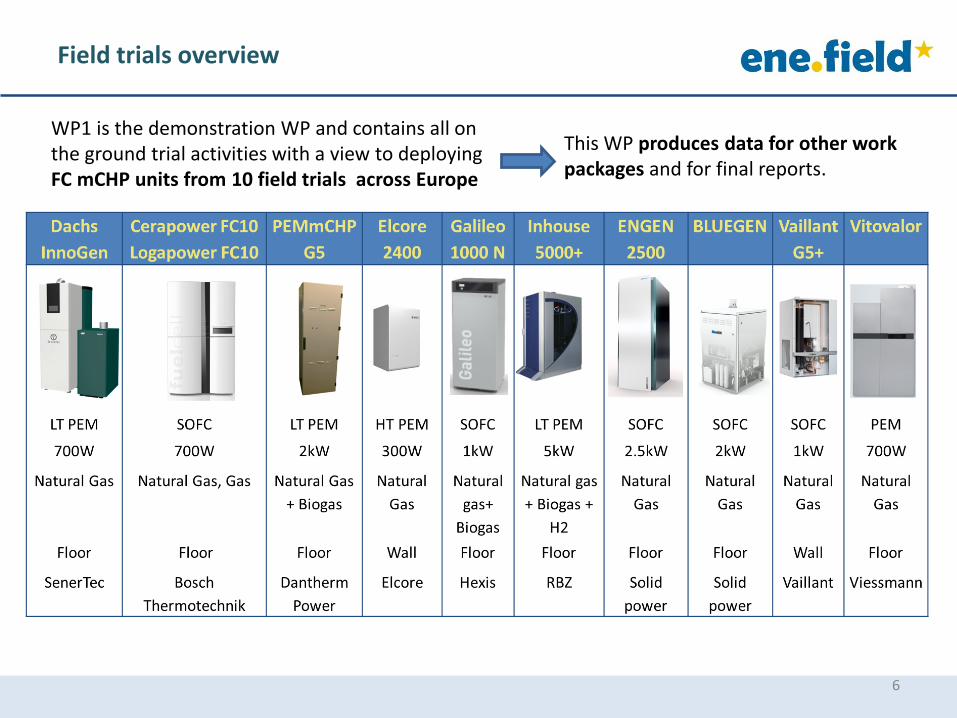

Field trials overview

6

WP1 is the demonstration WP and contains all on the ground trial activities with a view to deploying FC mCHP units from 10 field trials across Europe

This WP produces data for other work packages and for final reports.

Agenda

1. Introduction to the ene.field project

2. Lessons learned to-date

3. Preliminary findings

4. Technical monitoring

5. Forthcoming research and analysis

7

• ene.field has successfully installed approx. 400 FC mCHP in a range of house types across 8 European markets – performance data is being collected and will be analysed in the forthcoming phase of the project

• Germany is the strongest early market, this is due to regional funding opportunities, tolerance of higher cost heating systems and a more developed manufacturer and installer base, among other factors

• Route to market via utilities has proven very difficult; less finance available for demonstration projects – interest in only small numbers of units and limited co-financing

• System capital costs are the major challenge for growth of the market (running costs are competitive with incumbents).

• Increased manufacturing volumes is expected to be the biggest driver of capital cost reductions, which will require continued public funding support

Lessons learned - field trials

8Source: ene.field project

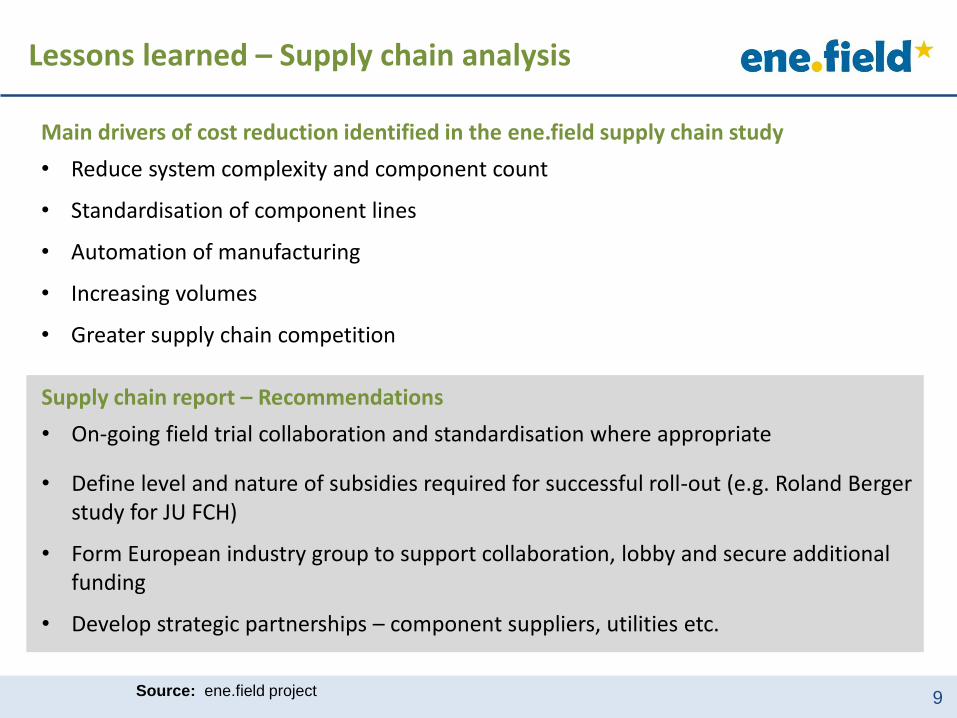

Lessons learned – Supply chain analysis

Main drivers of cost reduction identified in the ene.field supply chain study

• Reduce system complexity and component count

• Standardisation of component lines

• Automation of manufacturing

• Increasing volumes

• Greater supply chain competition

Supply chain report – Recommendations

• On-going field trial collaboration and standardisation where appropriate

• Define level and nature of subsidies required for successful roll-out (e.g. Roland Berger study for JU FCH)

• Form European industry group to support collaboration, lobby and secure additional funding

• Develop strategic partnerships – component suppliers, utilities etc.

9Source: ene.field project

Agenda

1. Introduction to the ene.field project

2. Lessons learned to-date

1. Preliminary findings

2. Technical monitoring

3. Forthcoming research and analysis

10

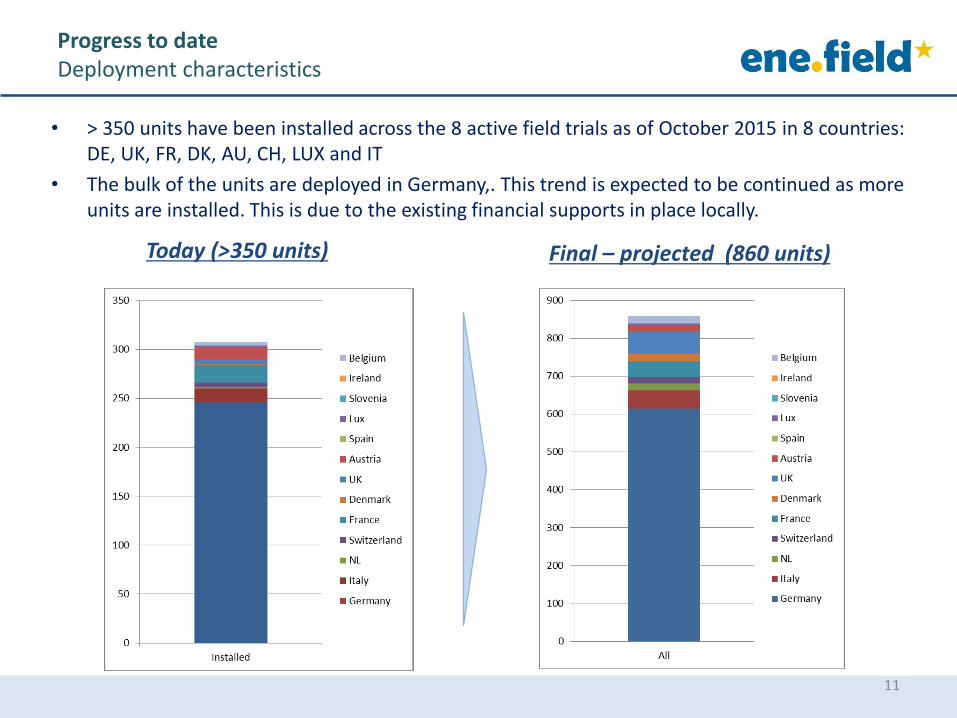

• > 350 units have been installed across the 8 active field trials as of October 2015 in 8 countries: DE, UK, FR, DK, AU, CH, LUX and IT

• The bulk of the units are deployed in Germany,. This trend is expected to be continued as more units are installed. This is due to the existing financial supports in place locally.

11

Today (>350 units)

Progress to date Deployment characteristics

Final – projected (860 units)

• Age of buidlings :preliminary

• Desired temperature

Type of accomodation : preliminary

0

5

10

15

20

25

4

15

21

1310

3 2

0

5

10

15

20

25

19 20 21 22 23 24 25+

Fre

qu

en

cy

fd

19%

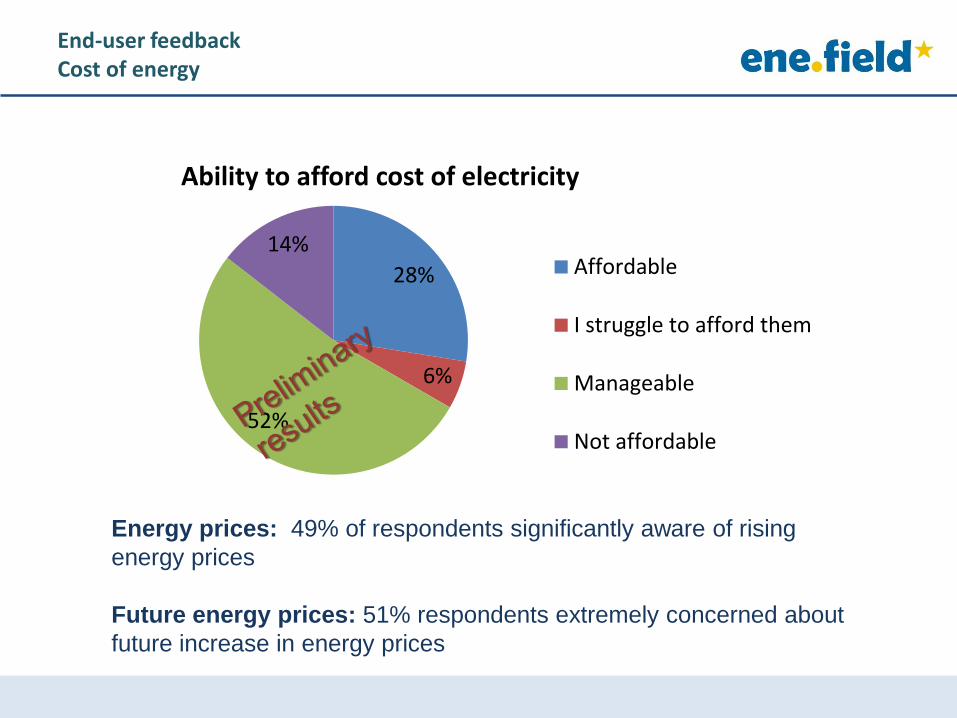

End-user feedbackCost of energy

28%

6%

52%

14%

Ability to afford cost of electricity

Affordable

I struggle to afford them

Manageable

Not affordable

Energy prices: 49% of respondents significantly aware of rising

energy prices

Future energy prices: 51% respondents extremely concerned about

future increase in energy prices

Agenda

1. Introduction to the ene.field project

2. Lessons learned to-date

3. Preliminary findings

4. Technical monitoring

5. Forthcoming research and analysis

14

Progress to dateSnapshot data collection

• 100% of units installed are monitored – including 10% of all units with detailed monitoring

15

No. installations

Monitoring status (detailed and standards)

ACOS700 - the “Callux-box” from IDS GmbH

(source: IDS)

Communication gateway/data logger for collecting

and archiving in database servers. It includes:

• 2 Ethernet ports (ETH 0 and ETH1),

• a wireless communication port (M-Bus),

• internal communication networks (S1 and S2),

• a mini-USB service port for direct connection,

• a plug in electrical power connection (PWR).

Agenda

1. Introduction to the ene.field project

2. Lessons learned to-date

3. Preliminary findings

1. Technical monitoring

2. Forthcoming research and analysis

16

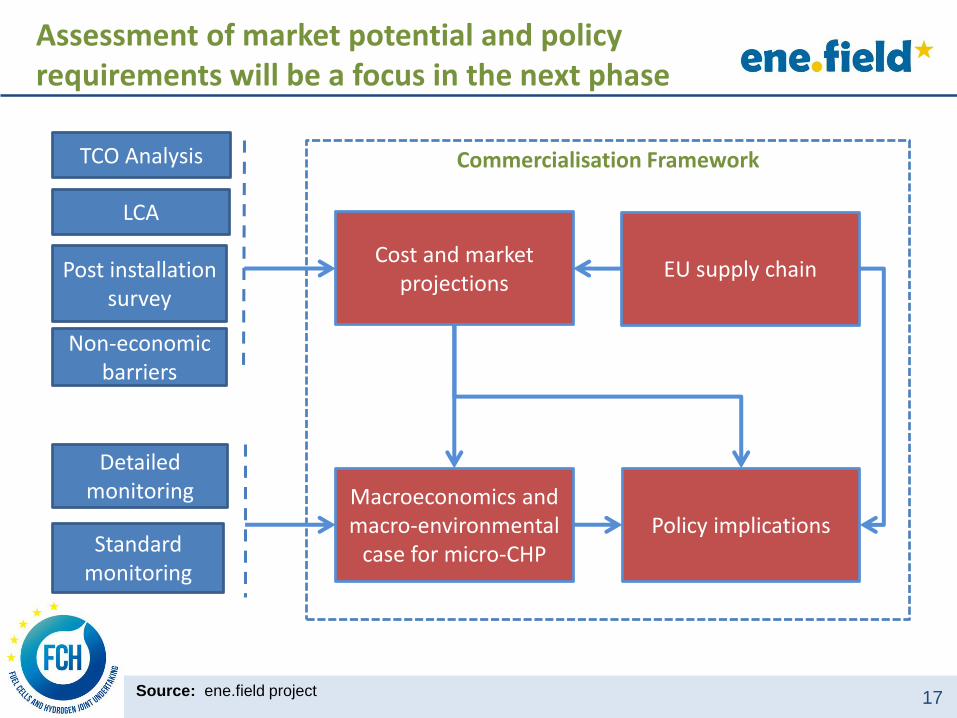

Assessment of market potential and policy requirements will be a focus in the next phase

Policy implicationsMacroeconomics and macro-environmental

case for micro-CHP

Cost and market projections

EU supply chain

TCO Analysis Commercialisation Framework

LCA

Post installation survey

Detailed monitoring

Standard monitoring

17Source: ene.field project

Non-economic barriers

Detailed modelling of the impact of FCmCHP on Europe’s electricity system will be performed

0

200

400

600

800

1000

1200

1400

1600

1800

2020 2030withoutmicroCHP

2030with

microCHP

Inst

alle

d c

apac

ity

(GW

)

OCGT

Storage

Hydro reservoir

Hydro ROR

Geothermal

CHP

micro CHP

CSP

PV

Wind

Oil

Nuclear

Gas CCS

Coal CCS

Gas Conventional

Coal conventional

0.95 km

0

1

2

3

4

5

0 4 8 12 16 20 24

Po

we

r (M

We

)

Time (h)

Base Base+HP Base+CHP

18

Changing grid electricity mix Representative models of electricity transmission and distribution networks

Impact of FCmCHP deployment on network loads

Next steps

• Continuation and acceleration of deployment of units across the field trials

• Technical performance monitoring across all field trials, including 10% of units with detailed monitoring. First monitoring data to pass through the clean room and made available to analysis partners and the FCH JU

• Further analysis of customer perception through pre- and post-installation surveys

• Lifecycle analysis (LCA) and lifecycle cost analysis (LCC)

• Market growth projections and detailed modelling of FC mCHP impacts on European electricity systems

• Development of policy recommendations reflecting the lessons learned from the project and the requirements for commercialisation of FC mCHP across Europe

• Implementing the project dissemination plan, including external communication via tools such as the project website, information packs for householders, press releases and key stakeholder engagement activities

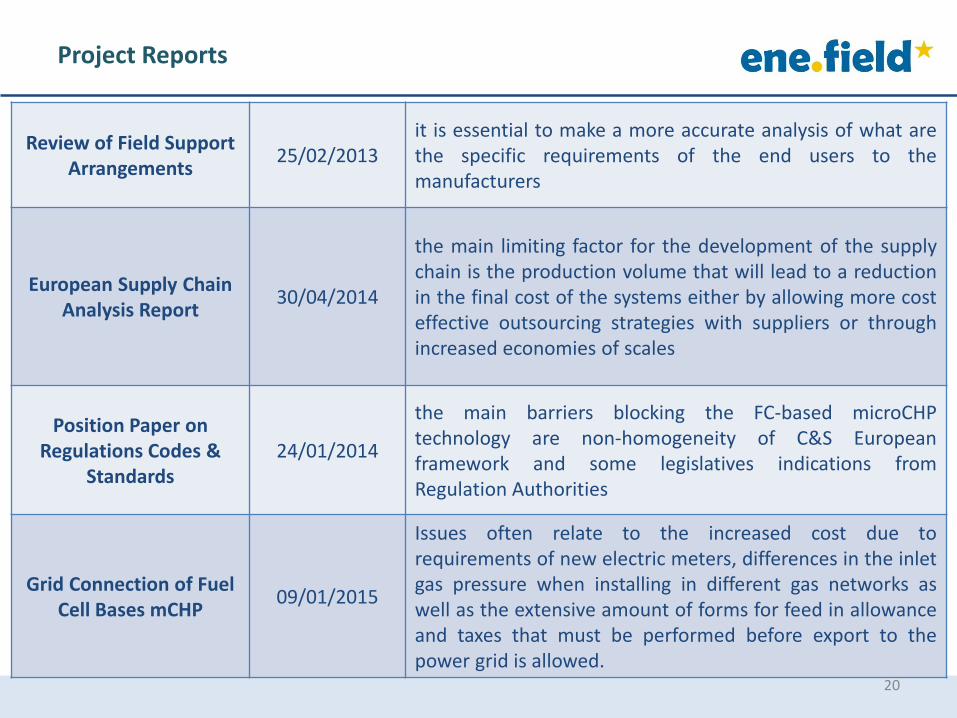

Project Reports

Review of Field Support Arrangements

25/02/2013it is essential to make a more accurate analysis of what arethe specific requirements of the end users to themanufacturers

European Supply Chain Analysis Report

30/04/2014

the main limiting factor for the development of the supplychain is the production volume that will lead to a reductionin the final cost of the systems either by allowing more costeffective outsourcing strategies with suppliers or throughincreased economies of scales

Position Paper onRegulations Codes &

Standards24/01/2014

the main barriers blocking the FC-based microCHPtechnology are non-homogeneity of C&S Europeanframework and some legislatives indications fromRegulation Authorities

Grid Connection of Fuel Cell Bases mCHP

09/01/2015

Issues often relate to the increased cost due torequirements of new electric meters, differences in the inletgas pressure when installing in different gas networks aswell as the extensive amount of forms for feed in allowanceand taxes that must be performed before export to thepower grid is allowed.

20

Dec 2012

The research leading to these results has received funding from the

European Union´s 7th Framework Programme (FP7/2007-2013) for

the Fuel Cells and Hydrogen Joint Undertaking Technology Initiative

under Grant Agreement Number 303462.

THANK YOU

www.enefield.eu

21