Offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

Savills International Associate Office. Chartered Surveyors. Regulated by RICS. DMB International W.L.L. Registered in Bahrain CR No. 70236. Registered office: Suite 21, Seef Star Building, Al Seef District, Kingdom of Bahrain.

Eskan Bank 18th August 2016

Valuation Report

Segaya Plaza, Manama Kingdom of Bahrain

savills.bh

Offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

Savills International Associate Office. Chartered Surveyors. Regulated by RICS. DMB International W.L.L. Registered in Bahrain CR No. 70236. Registered office: Suite 21, Seef Star Building, Al Seef District, Kingdom of Bahrain.

18th August 2016

Ref: DMB

Eskan Bank

Seef District, Almoayyed Tower

PO Box 5370 Manama

Kingdom of Bahrain

For the attention of Mr Ahmad Tayara

Dear Sir,

RE: VALUATION REPORT – Segaya Plaza, Manama, Bahrain

We wish to thank you for your instruction to revalue this property following our report of the 15th October 2015.

We are pleased to provide our valuation as of 15th August 2016. If you require the valuation for October please let

us know and we can provide an updated certificate for your records.

We trust the attached report meet your requirements of your instructions and we remain yours faithfully.

Donald M. Bradley FRICS

RICS Registered Valuer CEO DMB International WLL

Donald Bradley FRICS

DL: +973 3961 0600

Suite 21, Seef Star Building

Bahrain

International Associate of Savills

DMB International W.L.L.

savills.bh

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016

Contents

2Executive Summary 1

1. Instructions and Terms of Reference 3

Instructions ................................................................................................................................................................. 4

2. The Property, Statutory & Legal Aspects 7

Location Overview ...................................................................................................................................................... 8

Situation ..................................................................................................................................................................... 8

Description.................................................................................................................................................................. 9

Accommodation ........................................................................................................................................................ 11

Condition .................................................................................................................................................................. 12

Highways and Access .............................................................................................................................................. 12

Access ...................................................................................................................................................................... 12

Services .................................................................................................................................................................... 12

Environmental Considerations .................................................................................................................................. 12

Planning and Approvals ............................................................................................................................................ 13

Town Planning .......................................................................................................................................................... 13

Tenure ...................................................................................................................................................................... 13

Occupational Leases ................................................................................................................................................ 13

Current Rental Income ............................................................................................................................................. 13

Operating Expenditure .............................................................................................................................................. 14

Building Management ............................................................................................................................................... 15

3. Market Commentary 16

Global Macro Economic Factors ............................................................................................................................... 17

Regional Macro Factors ............................................................................................................................................ 17

Bahrain General Factors ........................................................................................................................................... 17

Growth in Office Stock .............................................................................................................................................. 18

Current and Future Supply ....................................................................................................................................... 18

Demand and Supply Dynamics ................................................................................................................................ 19

Rental Growth Over Time ......................................................................................................................................... 20

Current Rental Rates ................................................................................................................................................ 21

Car Parking............................................................................................................................................................... 21

Introduction to Retail Sector ..................................................................................................................................... 22

Market Dynamics ...................................................................................................................................................... 22

Existing Supply ......................................................................................................................................................... 23

Neighbourhood and Community Retail Supply ......................................................................................................... 24

Supply Trends .......................................................................................................................................................... 24

Future Mall Supply .................................................................................................................................................... 25

Rents ........................................................................................................................................................................ 26

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016

4. Valuation Advice 28

Approach to Valuation .............................................................................................................................................. 29

Principal Valuation Consideration ............................................................................................................................. 29

Background to Market Value .................................................................................................................................... 30

Opinion of Market Value ........................................................................................................................................... 30

Market Volatility ........................................................................................................................................................ 30

Confidentiality and Disclosure .................................................................................................................................. 31

Signature .................................................................................................................................................................. 31

5. General Assumptions & Conditions to Valuations 32

General Assumptions and Conditions ...................................................................................................................... 33

Appendixes

Confirmation of instructions………………………………………………………………. .Appendix A

Title Deeds…………………………………………………… ..Appendix B

Service Charge Budgets….…………………………………………………………. Appendix C

Floor Plans.………………………………………………………………………... Appendix D

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016

Executive Summary

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 1

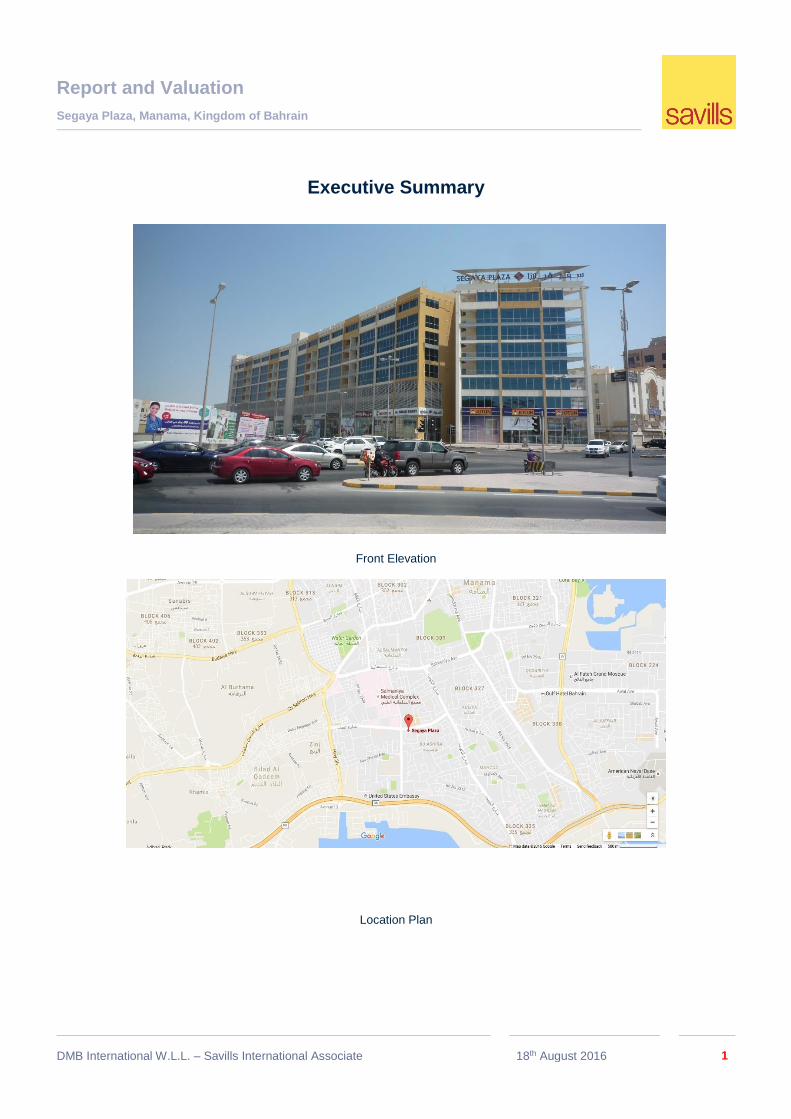

Executive Summary

Front Elevation

Location Plan

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 2

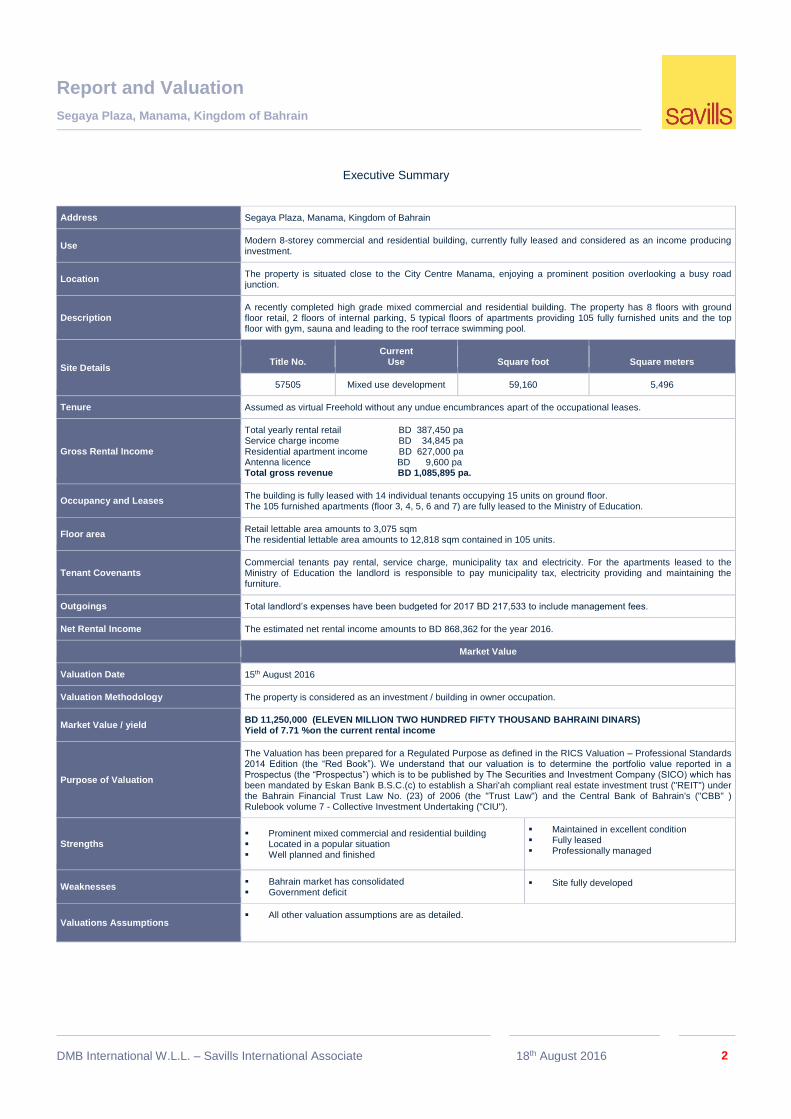

Executive Summary

Address Segaya Plaza, Manama, Kingdom of Bahrain

Use Modern 8-storey commercial and residential building, currently fully leased and considered as an income producing investment.

Location The property is situated close to the City Centre Manama, enjoying a prominent position overlooking a busy road junction.

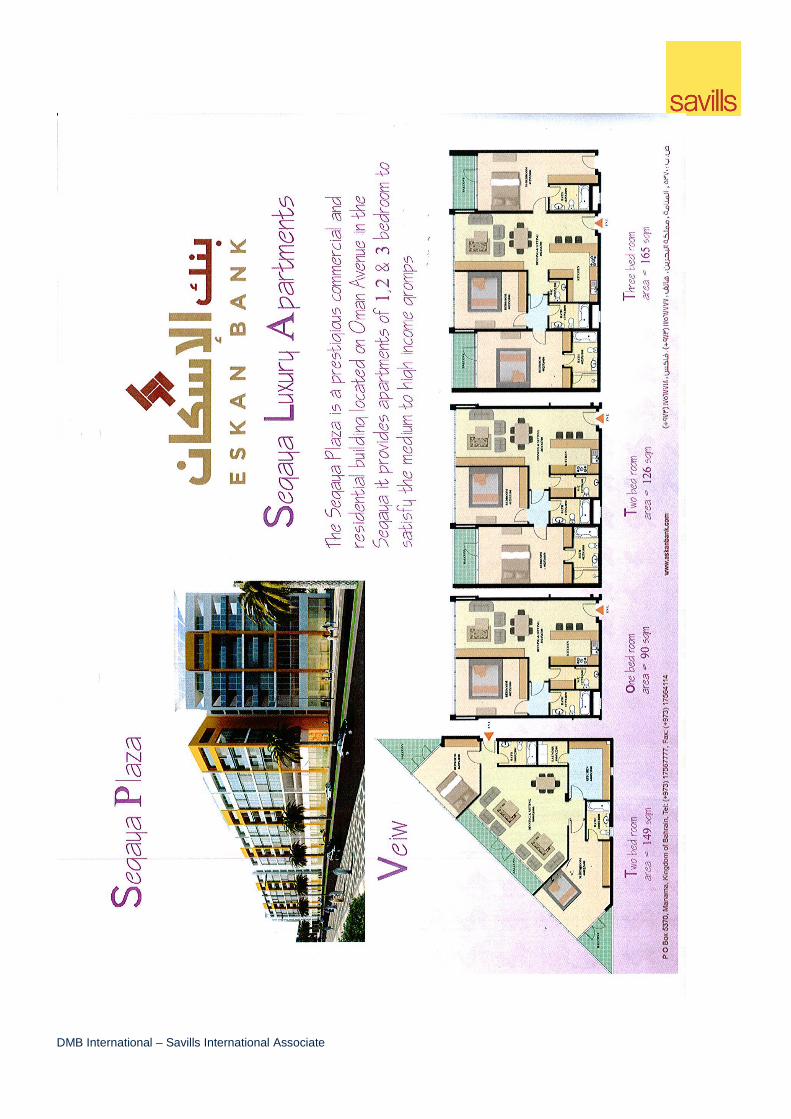

Description A recently completed high grade mixed commercial and residential building. The property has 8 floors with ground floor retail, 2 floors of internal parking, 5 typical floors of apartments providing 105 fully furnished units and the top floor with gym, sauna and leading to the roof terrace swimming pool.

Site Details

Title No.

Current Use

Square foot

Square meters

57505 Mixed use development 59,160 5,496

Tenure Assumed as virtual Freehold without any undue encumbrances apart of the occupational leases.

Gross Rental Income

Total yearly rental retail BD 387,450 pa Service charge income BD 34,845 pa Residential apartment income BD 627,000 pa Antenna licence BD 9,600 pa Total gross revenue BD 1,085,895 pa.

Occupancy and Leases The building is fully leased with 14 individual tenants occupying 15 units on ground floor. The 105 furnished apartments (floor 3, 4, 5, 6 and 7) are fully leased to the Ministry of Education.

Floor area Retail lettable area amounts to 3,075 sqm The residential lettable area amounts to 12,818 sqm contained in 105 units.

Tenant Covenants Commercial tenants pay rental, service charge, municipality tax and electricity. For the apartments leased to the Ministry of Education the landlord is responsible to pay municipality tax, electricity providing and maintaining the furniture.

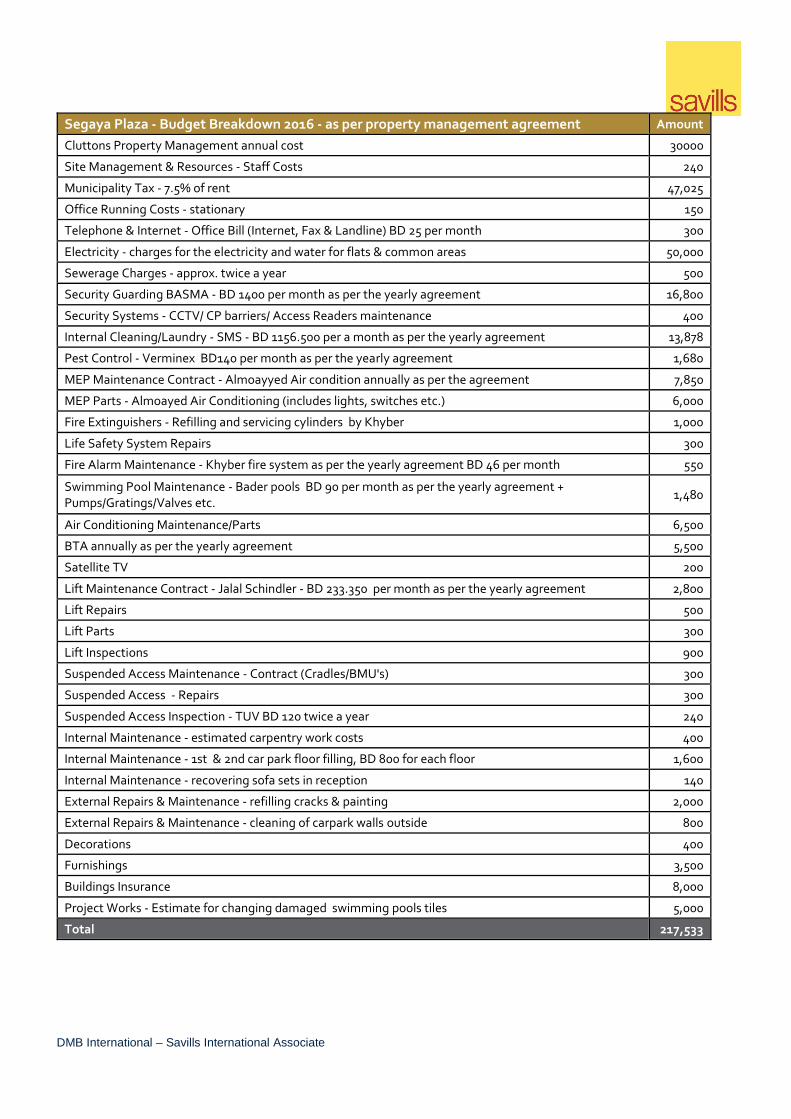

Outgoings Total landlord’s expenses have been budgeted for 2017 BD 217,533 to include management fees.

Net Rental Income The estimated net rental income amounts to BD 868,362 for the year 2016.

Market Value

Valuation Date 15th August 2016

Valuation Methodology The property is considered as an investment / building in owner occupation.

Market Value / yield BD 11,250,000 (ELEVEN MILLION TWO HUNDRED FIFTY THOUSAND BAHRAINI DINARS) Yield of 7.71 %on the current rental income

Purpose of Valuation

The Valuation has been prepared for a Regulated Purpose as defined in the RICS Valuation – Professional Standards 2014 Edition (the “Red Book”). We understand that our valuation is to determine the portfolio value reported in a Prospectus (the “Prospectus”) which is to be published by The Securities and Investment Company (SICO) which has been mandated by Eskan Bank B.S.C.(c) to establish a Shari'ah compliant real estate investment trust ("REIT") under the Bahrain Financial Trust Law No. (23) of 2006 (the "Trust Law") and the Central Bank of Bahrain's ("CBB" ) Rulebook volume 7 - Collective Investment Undertaking ("CIU").

Strengths Prominent mixed commercial and residential building Located in a popular situation Well planned and finished

Maintained in excellent condition Fully leased Professionally managed

Weaknesses Bahrain market has consolidated Government deficit

Site fully developed

Valuations Assumptions All other valuation assumptions are as detailed.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 3

1. Instructions and Terms of Reference

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 4

Instructions

1.1.1. Instructions and Basis of Valuation

You have instructed us to provide our opinions of value on the following bases:

The Valuation will be to Market Value and will be prepared in accordance with RICS (Royal Institution of Chartered

Surveyors) RICS Valuation –Professional Standards January 2014 (the Red Book).

1.1.2. General Assumptions and Conditions

All our valuations have been carried out on the basis of the General Assumptions and Conditions set out in the relevant section

towards the rear of this report.

1.1.3. Date of Valuation

Our opinions of value are as at the 15th August 2016. The importance of the date of valuation must be stressed as property

values can change over a relatively short period.

1.1.4. Definitions of Market Value and Market Rent

In undertaking our valuations, we have adopted the RICS definitions of Market Value and Market Rent, as detailed below:

Valuation Standard VS 4 1.2 of the Red Book defines Market Value (MV) as:

“The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a

willing seller in an arm’s length transaction, after proper marketing and where the parties had each acted knowledgeably,

prudently and without compulsion.”

Valuation Standard VS 4 1.3 of the Red Book defines Market Rent (MR) as:

“The estimated amount for which an interest in real property should be leased on the valuation date between a willing lessor and

a willing lessee on appropriate lease terms in an arm’s length transaction, after proper marketing and where the parties had

each acted knowledgeably, prudently and without compulsion.”

1.1.5. Purpose of Valuations

The Valuation has been prepared for a Regulated Purpose as defined in the RICS Valuation – Professional Standards 2014

Edition (the “Red Book”). We understand that our valuation is to determine the portfolio value reported in a Prospectus (the

“Prospectus”) which is to be published by The Securities and Investment Company (SICO) which has been mandated by Eskan

Bank B.S.c.(c) to establish a Shari'ahcompliant real estate investment trust ("REIT") under the Bahrain Financial Trust Law No.

(23) of 2006 (the "Trust Law") and the Central Bank of Bahrain's ("CBB" ) Rulebook volume 7 - Collective Investment

Undertaking ("CIU")

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 5

1.1.6. Conflicts of Interest

We are not aware of any conflict of interest preventing us from providing you with an independent valuation of the property in

accordance with the RICS Red Book. We are acting as External Valuers, as defined in the Red Book.

1.1.7. Valuer Details and Inspection

The due diligence enquiries referred to below were undertaken by Mr Donald Bradley FRICS. The valuations have also been

reviewed by Michael Lowes MRICS. Both valuers represent DMB International WLL – Savills International Associate.

The property was inspected on the 17th August 2016 by Mr Donald Bradley FRICS. We were able to inspect most areas of the

property and wish to thank the management team for their support. The weather on the date of our inspection was dry and

sunny.

Furthermore, in accordance with PS 3.7, we confirm that the aforementioned individuals have sufficient current local, national

and international knowledge of the particular market and the skills and understanding to undertake the valuation competently.

1.1.8. Extent of Due Diligence Enquiries and Information Sources

The extent of the due diligence enquiries we have undertaken and the sources of the information we have relied upon for the

purpose of our valuation are stated in the relevant sections of our report below.

This valuation has been carried out at the client’s request, based on information supplied to us.

1. Segaya Plaza Tenancy Schedule as provided by Cluttons (undated)

2. Budget breakdowns 2016

3. Copy of July Property Management Report

4. Abstract of Title Deed with site plan

Where reports and other information have been provided, we summarise the relevant details in this report. We do not accept

responsibility for any errors or omissions in the information and documentation provided to us, nor for any consequences that

may flow from such errors and omissions.

1.1.9. Liability Cap

Our confirmation of instructions at Appendix 1 includes details of our liability cap which is set at Bahraini Dinars 100,000.

1.1.10. RICS Compliance

This report has been prepared in accordance with Royal Institution of Chartered Surveyors’ (“RICS”) Valuation – Professional

Standards January 2014 (the “RICS Red Book”) published in November 2013 and effective from 1 January 2014, in particular in

accordance with the requirements of VPS 3 entitled Valuation reports and VPGA 2 Valuations secured lending, as appropriate.

Our report in accordance with those requirements is set out below.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 6

1.1.11. Verification

This report contains many assumptions, some of a general and some of a specific nature. Our valuation is based upon certain

information supplied to us by others. Some information we consider material may not have been provided to us. All of these

matters are referred to in the relevant sections of this report.

We recommend that you satisfy yourself on all these points, either by verification of individual points or by judgement of the

relevance of each particular point in the context of the purpose of our valuation. Our valuation should not be relied upon

pending this verification process.

1.1.12. Confidentiality and Responsibility

Finally, in accordance with the recommendations of the RICS, we would state that this report is provided solely for the purpose

stated above. It is confidential to and for the use only of the party to whom it is addressed only, and no responsibility is

accepted to any third party for the whole or any part of its contents. Any such parties rely upon this report at their own risk.

Neither the whole nor any part of this report or any reference to it may be included now, or at any time in the future, in any

published document, circular or statement, nor published, referred to or used in any way without our written approval of the form

and context in which it may appear.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 7

2. The Property, Statutory & Legal Aspects

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 8

Location Overview

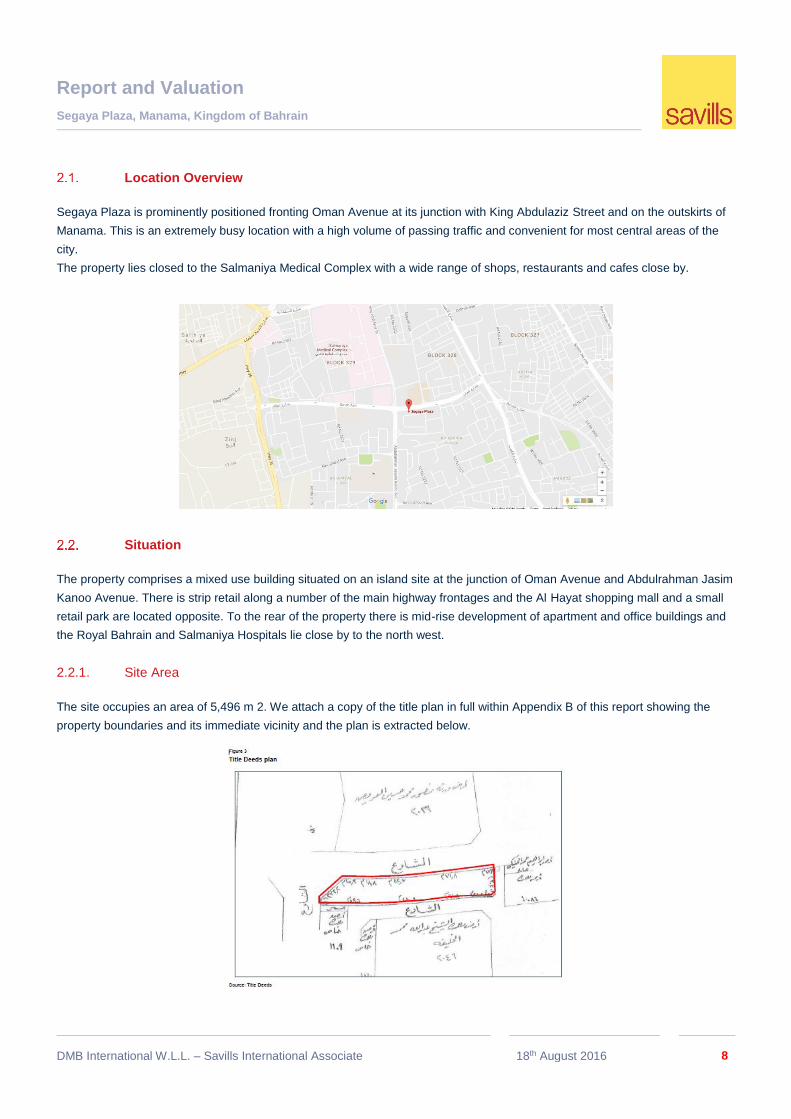

Segaya Plaza is prominently positioned fronting Oman Avenue at its junction with King Abdulaziz Street and on the outskirts of

Manama. This is an extremely busy location with a high volume of passing traffic and convenient for most central areas of the

city.

The property lies closed to the Salmaniya Medical Complex with a wide range of shops, restaurants and cafes close by.

Situation

The property comprises a mixed use building situated on an island site at the junction of Oman Avenue and Abdulrahman Jasim

Kanoo Avenue. There is strip retail along a number of the main highway frontages and the Al Hayat shopping mall and a small

retail park are located opposite. To the rear of the property there is mid-rise development of apartment and office buildings and

the Royal Bahrain and Salmaniya Hospitals lie close by to the north west.

2.2.1. Site Area

The site occupies an area of 5,496 m 2. We attach a copy of the title plan in full within Appendix B of this report showing the

property boundaries and its immediate vicinity and the plan is extracted below.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 9

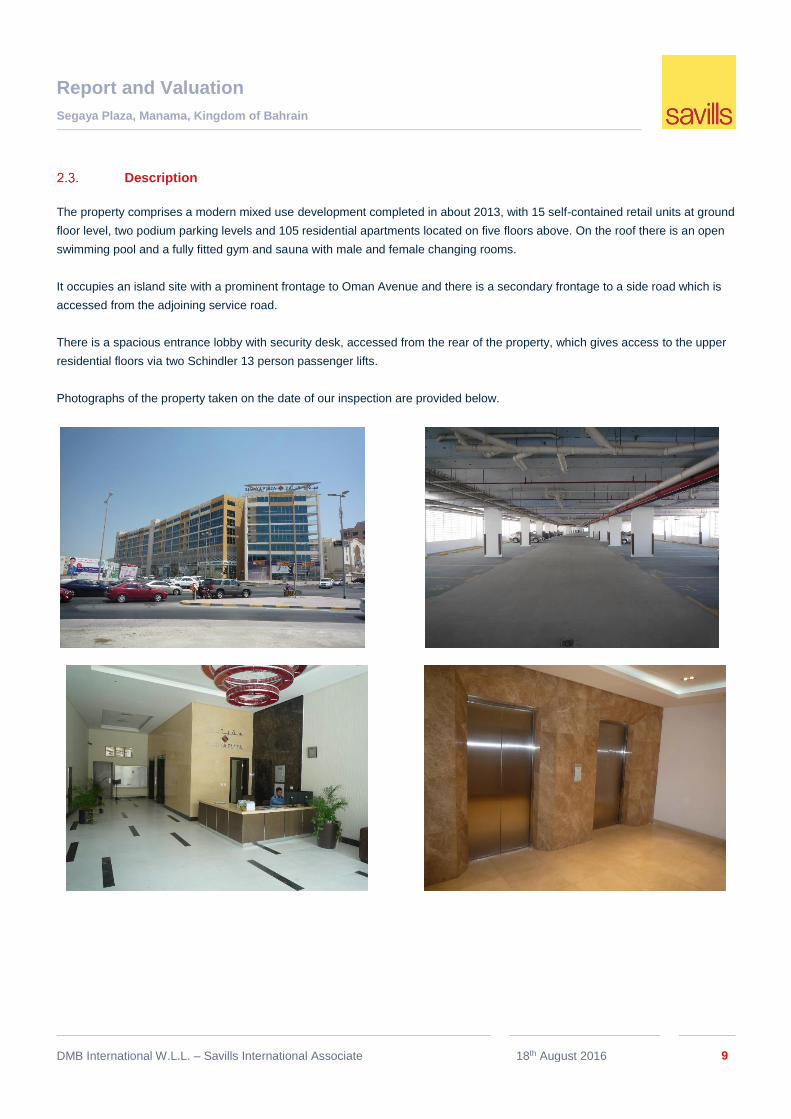

Description

The property comprises a modern mixed use development completed in about 2013, with 15 self-contained retail units at ground

floor level, two podium parking levels and 105 residential apartments located on five floors above. On the roof there is an open

swimming pool and a fully fitted gym and sauna with male and female changing rooms.

It occupies an island site with a prominent frontage to Oman Avenue and there is a secondary frontage to a side road which is

accessed from the adjoining service road.

There is a spacious entrance lobby with security desk, accessed from the rear of the property, which gives access to the upper

residential floors via two Schindler 13 person passenger lifts.

Photographs of the property taken on the date of our inspection are provided below.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 10

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 11

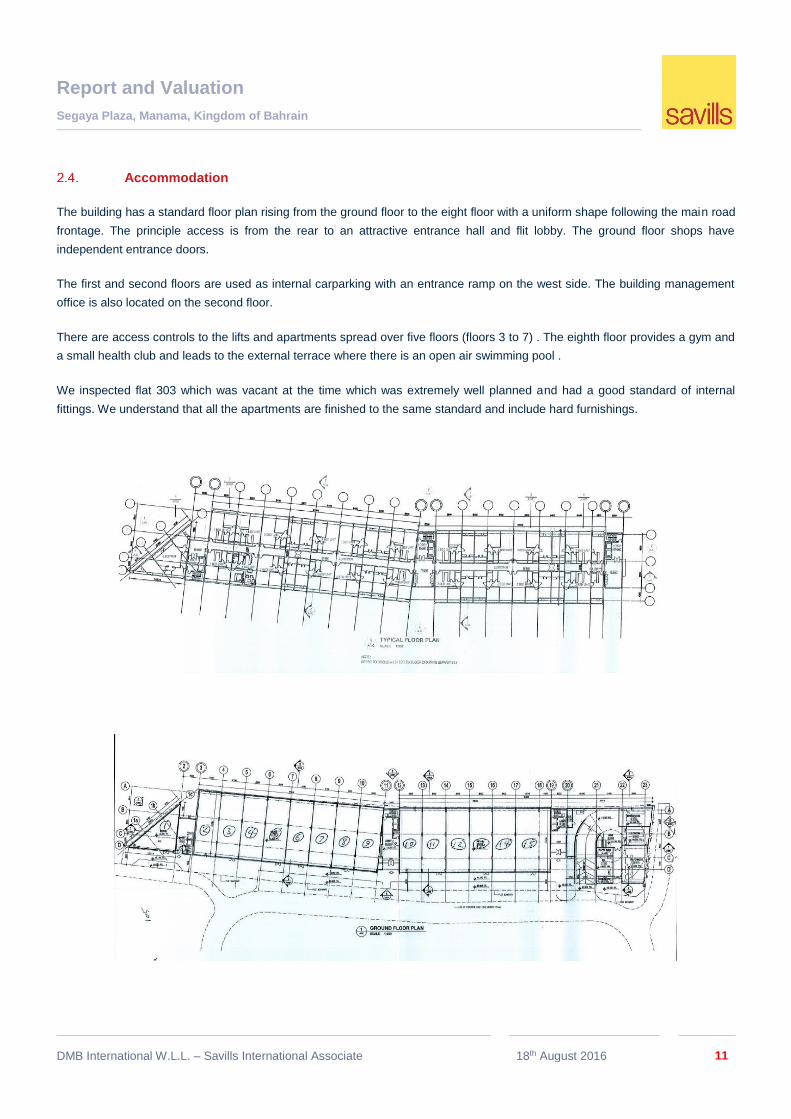

Accommodation

The building has a standard floor plan rising from the ground floor to the eight floor with a uniform shape following the main road

frontage. The principle access is from the rear to an attractive entrance hall and flit lobby. The ground floor shops have

independent entrance doors.

The first and second floors are used as internal carparking with an entrance ramp on the west side. The building management

office is also located on the second floor.

There are access controls to the lifts and apartments spread over five floors (floors 3 to 7) . The eighth floor provides a gym and

a small health club and leads to the external terrace where there is an open air swimming pool .

We inspected flat 303 which was vacant at the time which was extremely well planned and had a good standard of internal

fittings. We understand that all the apartments are finished to the same standard and include hard furnishings.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 12

Condition

As instructed, we have not carried out a site survey. The property is of recent construction and generally well maintained. Some

issues were noted on the roof with slabs broken and lifting and upstands cracked and broken, with some repair being required.

However these items are not considered to be serious.

We noted that the tiling around the eighth floor swimming pool is currently defective and is due to be repaired by the original

contractor.

Highways and Access

The property enjoys access from the adjoining highways, but there is no direct access from Oman Avenue. The main access is

via the service road to Abdulrahman Jasim Kanoo Avenue travelling in a northerly direction, which leads to the service road in

front of the property which provides on- street parking. There is an exit from the service road to Oman Avenue, travelling

eastbound.

The road to the rear of the building is also accessed from the same service road and provides further on-street parking and

access to the podium parking floors via a spiral ramp at the eastern end of the site.

Access

In reporting our opinion of value, we have assumed that there are no third party interests between the boundary of the subject

Property and the adopted highways and that accordingly the site has unfettered vehicular and pedestrian access to and from

the public highways.

Services

As stated in our terms of business, we have not tested the services at the property. We have assumed that adequate mains

services are provide and all are in working order and sufficient for the subject property.

Environmental Considerations

2.9.1. Informal Enquiries

As instructed, we have not carried out a soil test or an environmental audit. We are unaware of the previous development

history of the site, but it would appear unlikely that land contamination exists. This comment is made without liability.

2.9.2. Assumption

As our informal enquiries have suggested that land contamination is unlikely, we have valued the property on the basis that it

has not suffered any land contamination in the past, nor is it likely to become so contaminated in the foreseeable future.

However, should it subsequently be established that contamination exists at the property, or on any neighbouring land, then we

may wish to review our valuation advice.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 13

2.9.3. Flooding

Much of Bahrain is constructed on land reclaimed from the sea which is low lying. It may therefore be susceptible to flooding,

although we are unaware of any specific risk in respect of the subject property

Planning and Approvals

We understand that the property was constructed with the full approval of the master developer and that all consents were

obtained. We have not been informed of any breaches.

Town Planning

We have been provided with an approval BP/51/198049/BA/SB/062013 dated 27 June 2015 for the present building, however

we have not been provided with the accompanying plans. We understand that there are no onerous conditions attached, to this

approval.

Tenure

We have valued the unrestricted freehold interest in the property as outlined in red on the title plan in Appendix B. We have

been advised that the land was initially gifted by the Government on 26 March 1990 to Eskan Bank. From our inspection of the

title deeds it appears that there are no onerous or restrictive covenants affecting the site.

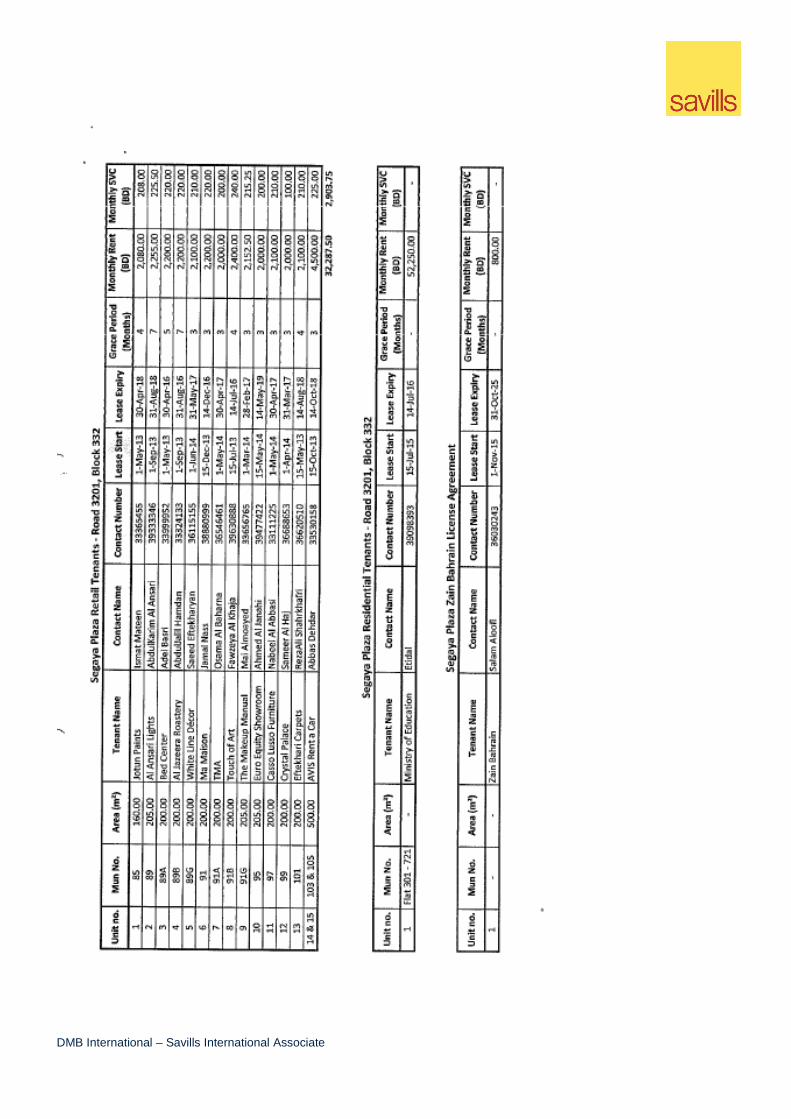

Occupational Leases

In accordance with the schedule provided the property is fully leased. Retail units 1 to 13 are all let to individual tenants and

units 14 and 15 are leased jointly to Avis rental car. Apart for one retail unit the standard rental for the shop units is between

BD 200 to BD 240 per month per bay, which seems reasonable at the current times

All the 105 flats are leased under a single agreement to the Ministry of Education at the current rental of BD 52,250 per month

or BD 627,000 per annum of the year 2016.

There is a licence with Zain Bahrain for the roof antennas at the monthly payment of BD 800 or BD 9,600 per annum.

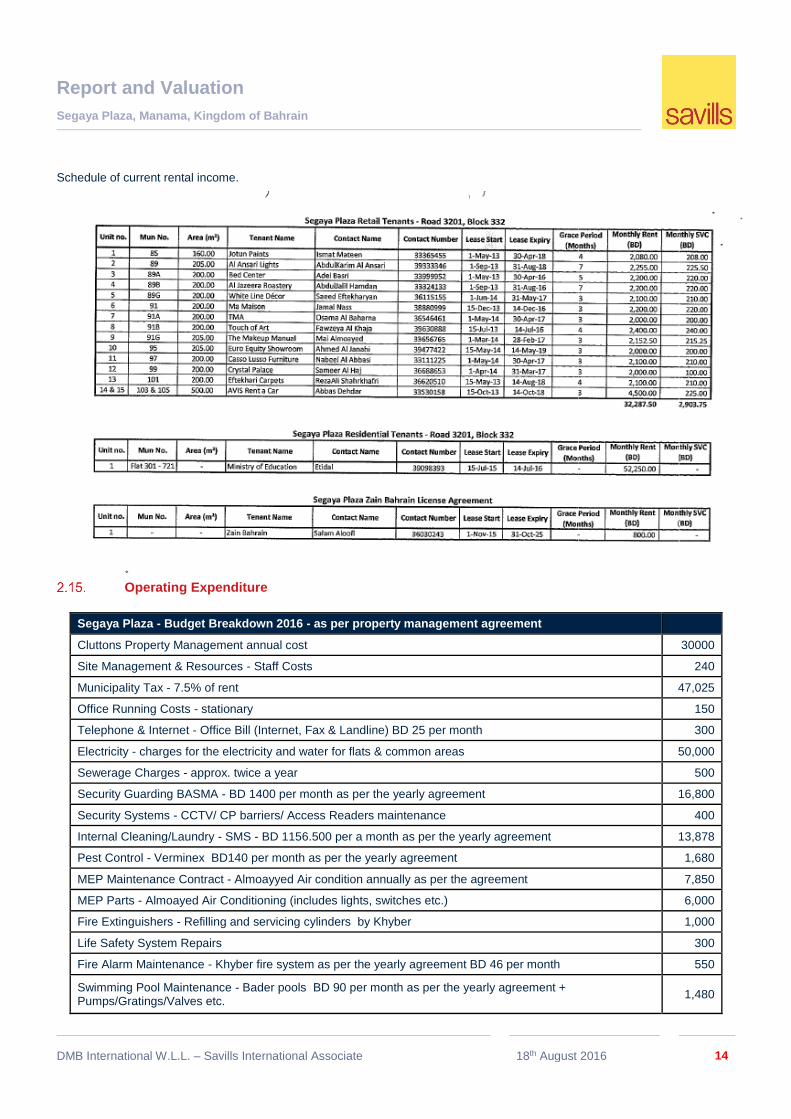

Current Rental Income

Based on the schedule provided during our visit to the management office the following applies

Retail rents BD 387,450 pa

Service charge income on retail rents BD 34,845 pa

Residential apartment income BD 627,000 pa

Antenna licence BD 9,600 pa

Total gross revenue BD 1,085,895 pa

Landlord’s expenditure BD 217,533 pa

Net rental income BD 868,362 pa

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 14

Schedule of current rental income.

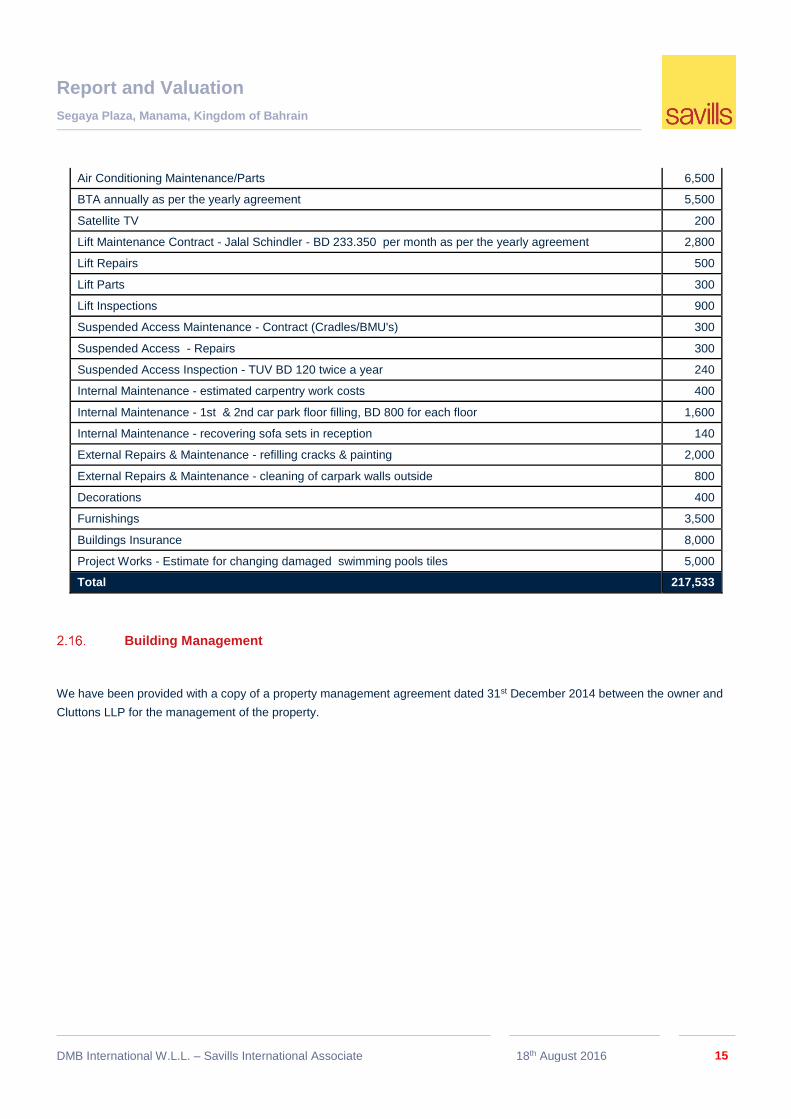

Operating Expenditure

Segaya Plaza - Budget Breakdown 2016 - as per property management agreement Amount

Cluttons Property Management annual cost 30000

Site Management & Resources - Staff Costs 240

Municipality Tax - 7.5% of rent 47,025

Office Running Costs - stationary 150

Telephone & Internet - Office Bill (Internet, Fax & Landline) BD 25 per month 300

Electricity - charges for the electricity and water for flats & common areas 50,000

Sewerage Charges - approx. twice a year 500

Security Guarding BASMA - BD 1400 per month as per the yearly agreement 16,800

Security Systems - CCTV/ CP barriers/ Access Readers maintenance 400

Internal Cleaning/Laundry - SMS - BD 1156.500 per a month as per the yearly agreement 13,878

Pest Control - Verminex BD140 per month as per the yearly agreement 1,680

MEP Maintenance Contract - Almoayyed Air condition annually as per the agreement 7,850

MEP Parts - Almoayed Air Conditioning (includes lights, switches etc.) 6,000

Fire Extinguishers - Refilling and servicing cylinders by Khyber 1,000

Life Safety System Repairs 300

Fire Alarm Maintenance - Khyber fire system as per the yearly agreement BD 46 per month 550

Swimming Pool Maintenance - Bader pools BD 90 per month as per the yearly agreement + Pumps/Gratings/Valves etc.

1,480

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 15

Air Conditioning Maintenance/Parts 6,500

BTA annually as per the yearly agreement 5,500

Satellite TV 200

Lift Maintenance Contract - Jalal Schindler - BD 233.350 per month as per the yearly agreement 2,800

Lift Repairs 500

Lift Parts 300

Lift Inspections 900

Suspended Access Maintenance - Contract (Cradles/BMU's) 300

Suspended Access - Repairs 300

Suspended Access Inspection - TUV BD 120 twice a year 240

Internal Maintenance - estimated carpentry work costs 400

Internal Maintenance - 1st & 2nd car park floor filling, BD 800 for each floor 1,600

Internal Maintenance - recovering sofa sets in reception 140

External Repairs & Maintenance - refilling cracks & painting 2,000

External Repairs & Maintenance - cleaning of carpark walls outside 800

Decorations 400

Furnishings 3,500

Buildings Insurance 8,000

Project Works - Estimate for changing damaged swimming pools tiles 5,000

Total 217,533

Building Management

We have been provided with a copy of a property management agreement dated 31st December 2014 between the owner and

Cluttons LLP for the management of the property.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 16

3. Market Commentary

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 17

Global Macro Economic Factors

While the major economies of the US and UK remain positive in the long term, currently international capital markets are in a

state of some uncertainty as a consequence of Brexit, the decline in the price of oil and commodities and general uncertainties

in the global financial markets. This uncertainty is beginning to reflect the challenges facing other major economies as output

begins to show a downward trend. This uncertainty has caused knock on effects across the globe.

Regional Macro Factors

Until the oil price decline in 2014, regional GCC Governments had been committed to high levels of spending,

particularly on major infrastructure projects. This was particularly true of Saudi Arabia, Kuwait and Abu Dhabi. In

addition, Dubai was commencing a number of expansionary projects to support the 2020 Dubai World Expo and in Qatar

there was continuing spending to meet obligations to host the 2022 FIFA World Cup Qatar.

Since 2014 and the oil price decline, GCC Governments are having to make rapid adjustments to re-align budgets with

the significant drop in available revenues and limit the exposure from drawing from their long held capital reserves,

even where these are significant.

Bahrain General Factors

Even with the Governments expansion of oil production to finance a budget deficit there will now be seen to be a significant

and much greater imbalance. The policies for a diverse market economy with a combination of oil, service industries and

tourism serving the Eastern Province of Saudi had produced an upbeat tone – but not to the point where fundamentals

would not increasingly be exposed.

Nevertheless the provision of a GCC support fund of $10 billion provided over ten years is seen as both an economic and

strategic demonstration of solidarity. Part of this fund will be allocated to recommencing some of the “failed” real estate

projects, which overhang the skyline, such as Villamaar and Marina West. Savills Bahrain office has been appointed by the

judicial authorities on a strategy to deal with these projects and reactivate the market. The necessary tightening of Central

Bank regulations to lending to the real estate development sector are a major constraint on new projects, although domestic

demand has kept reasonable levels of activity for medium and small scale projects, particularly those close to existing urban

areas.

The Government’s long-term strategies outlined in both its 2030 Vision and the 2030 National Land use strategy still

perceive that major real estate projects could be entertained. While the land mass of Bahrain has expanded by over 15%

since 1985 with ambitious large scale reclamation, the prevailing reality is that most of these projects have only attracted

limited international or local investors; apart from parties connected with the Government.

The potential overhang of these projects on the market has increased supply across every sector. The result being that real

estate prices remain close to nominal 20 year norms. Additionally, both institutional and private investment has been

directed to the main global markets where returns are more secure and liquidity higher.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 18

Growth in Office Stock

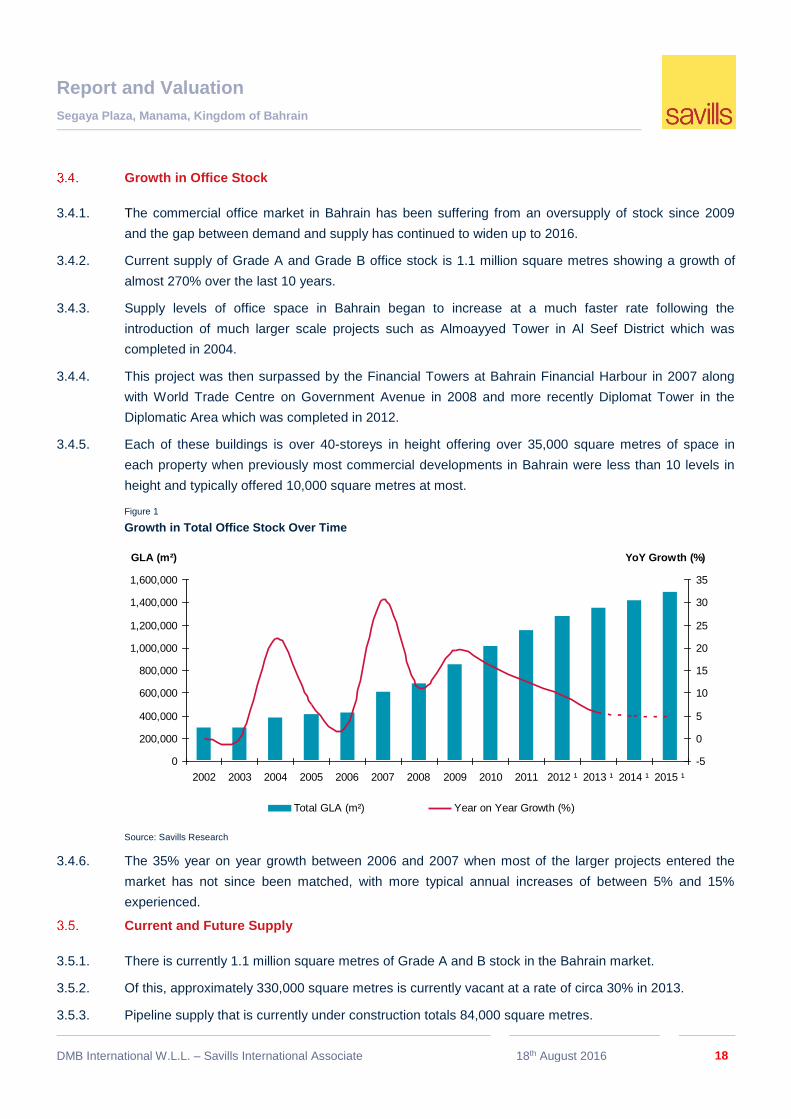

3.4.1. The commercial office market in Bahrain has been suffering from an oversupply of stock since 2009

and the gap between demand and supply has continued to widen up to 2016.

3.4.2. Current supply of Grade A and Grade B office stock is 1.1 million square metres showing a growth of

almost 270% over the last 10 years.

3.4.3. Supply levels of office space in Bahrain began to increase at a much faster rate following the

introduction of much larger scale projects such as Almoayyed Tower in Al Seef District which was

completed in 2004.

3.4.4. This project was then surpassed by the Financial Towers at Bahrain Financial Harbour in 2007 along

with World Trade Centre on Government Avenue in 2008 and more recently Diplomat Tower in the

Diplomatic Area which was completed in 2012.

3.4.5. Each of these buildings is over 40-storeys in height offering over 35,000 square metres of space in

each property when previously most commercial developments in Bahrain were less than 10 levels in

height and typically offered 10,000 square metres at most.

Figure 1

Growth in Total Office Stock Over Time

Source: Savills Research

3.4.6. The 35% year on year growth between 2006 and 2007 when most of the larger projects entered the

market has not since been matched, with more typical annual increases of between 5% and 15%

experienced.

Current and Future Supply

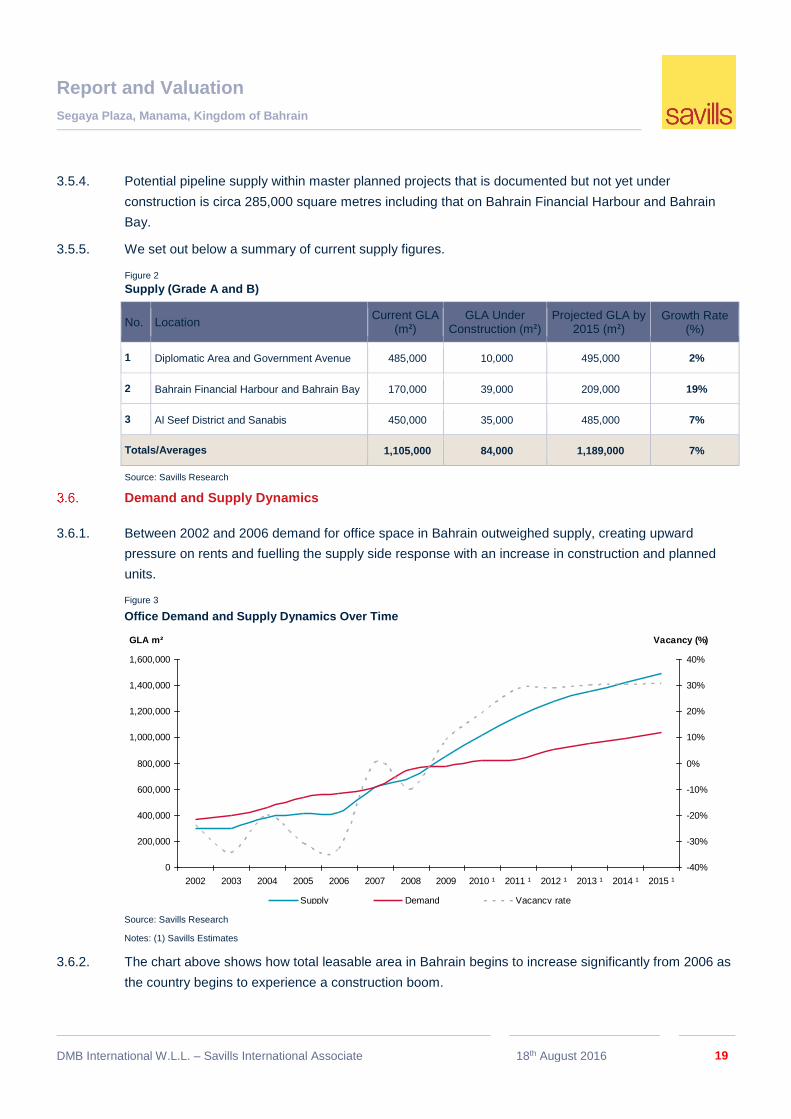

3.5.1. There is currently 1.1 million square metres of Grade A and B stock in the Bahrain market.

3.5.2. Of this, approximately 330,000 square metres is currently vacant at a rate of circa 30% in 2013.

3.5.3. Pipeline supply that is currently under construction totals 84,000 square metres.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 ¹ 2013 ¹ 2014 ¹ 2015 ¹

GLA (m²)

-5

0

5

10

15

20

25

30

35

YoY Growth (%)

Total GLA (m²) Year on Year Growth (%)

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 19

3.5.4. Potential pipeline supply within master planned projects that is documented but not yet under

construction is circa 285,000 square metres including that on Bahrain Financial Harbour and Bahrain

Bay.

3.5.5. We set out below a summary of current supply figures.

Figure 2

Supply (Grade A and B)

No. Location Current GLA

(m²) GLA Under

Construction (m²) Projected GLA by

2015 (m²) Growth Rate

(%)

1 Diplomatic Area and Government Avenue 485,000 10,000 495,000 2%

2 Bahrain Financial Harbour and Bahrain Bay 170,000 39,000 209,000 19%

3 Al Seef District and Sanabis 450,000 35,000 485,000 7%

Totals/Averages 1,105,000 84,000 1,189,000 7%

Source: Savills Research

Demand and Supply Dynamics

3.6.1. Between 2002 and 2006 demand for office space in Bahrain outweighed supply, creating upward

pressure on rents and fuelling the supply side response with an increase in construction and planned

units.

Figure 3

Office Demand and Supply Dynamics Over Time

Source: Savills Research

Notes: (1) Savills Estimates

3.6.2. The chart above shows how total leasable area in Bahrain begins to increase significantly from 2006 as

the country begins to experience a construction boom.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 ¹ 2011 ¹ 2012 ¹ 2013 ¹ 2014 ¹ 2015 ¹

GLA m²

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Vacancy (%)

Supply Demand Vacancy rate

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 20

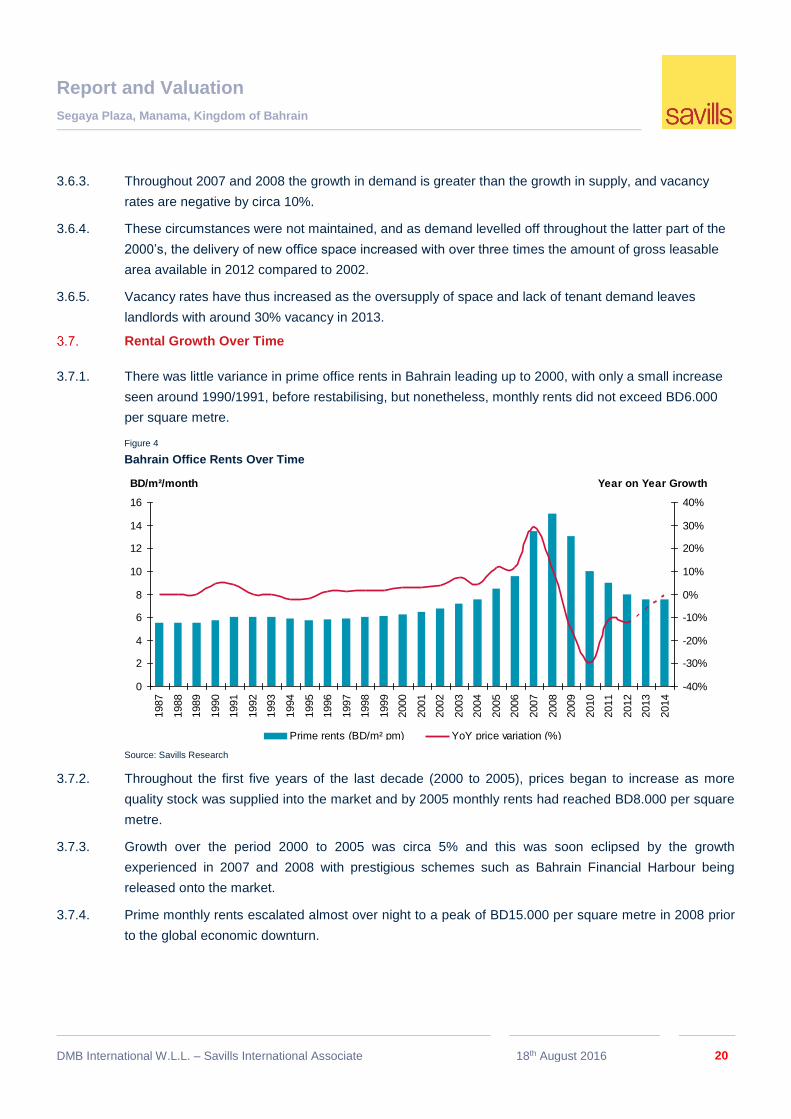

3.6.3. Throughout 2007 and 2008 the growth in demand is greater than the growth in supply, and vacancy

rates are negative by circa 10%.

3.6.4. These circumstances were not maintained, and as demand levelled off throughout the latter part of the

2000’s, the delivery of new office space increased with over three times the amount of gross leasable

area available in 2012 compared to 2002.

3.6.5. Vacancy rates have thus increased as the oversupply of space and lack of tenant demand leaves

landlords with around 30% vacancy in 2013.

Rental Growth Over Time

3.7.1. There was little variance in prime office rents in Bahrain leading up to 2000, with only a small increase

seen around 1990/1991, before restabilising, but nonetheless, monthly rents did not exceed BD6.000

per square metre.

Figure 4

Bahrain Office Rents Over Time

Source: Savills Research

3.7.2. Throughout the first five years of the last decade (2000 to 2005), prices began to increase as more

quality stock was supplied into the market and by 2005 monthly rents had reached BD8.000 per square

metre.

3.7.3. Growth over the period 2000 to 2005 was circa 5% and this was soon eclipsed by the growth

experienced in 2007 and 2008 with prestigious schemes such as Bahrain Financial Harbour being

released onto the market.

3.7.4. Prime monthly rents escalated almost over night to a peak of BD15.000 per square metre in 2008 prior

to the global economic downturn.

0

2

4

6

8

10

12

14

16

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

BD/m²/month

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Year on Year Growth

Prime rents (BD/m² pm) YoY price variation (%)

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 21

Current Rental Rates

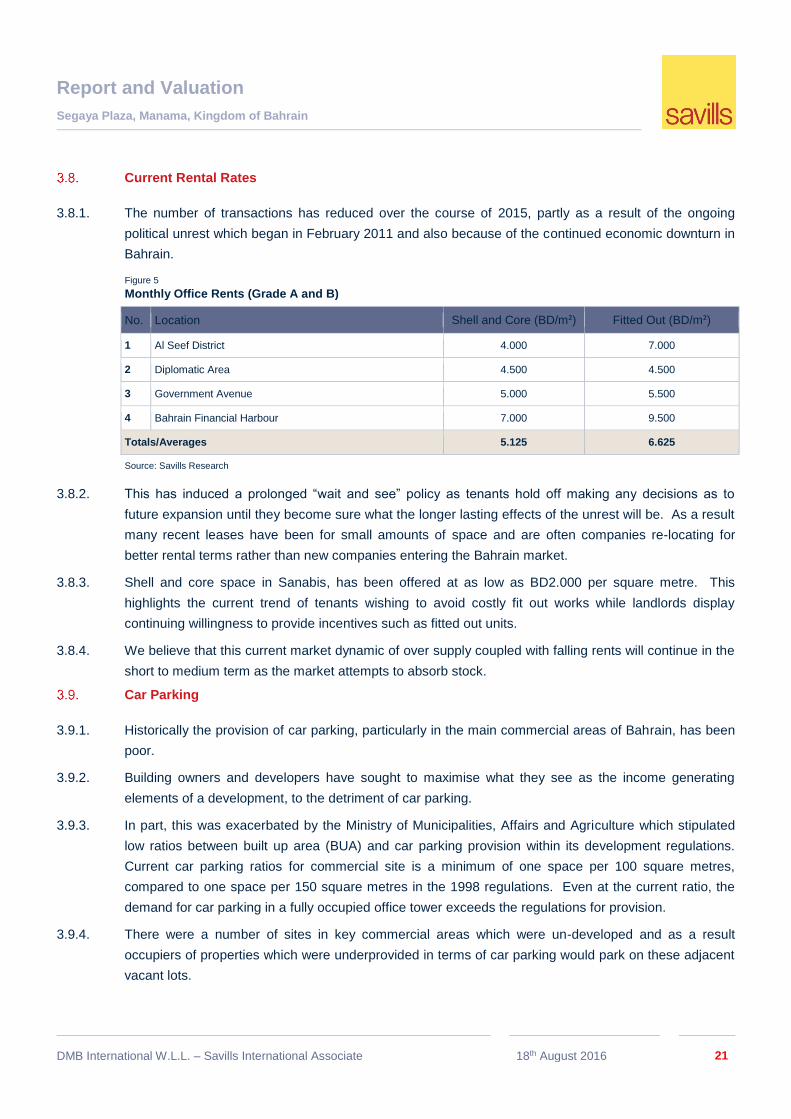

3.8.1. The number of transactions has reduced over the course of 2015, partly as a result of the ongoing

political unrest which began in February 2011 and also because of the continued economic downturn in

Bahrain.

Figure 5

Monthly Office Rents (Grade A and B)

No. Location Shell and Core (BD/m²) Fitted Out (BD/m²)

1 Al Seef District 4.000 7.000

2 Diplomatic Area 4.500 4.500

3 Government Avenue 5.000 5.500

4 Bahrain Financial Harbour 7.000 9.500

Totals/Averages 5.125 6.625

Source: Savills Research

3.8.2. This has induced a prolonged “wait and see” policy as tenants hold off making any decisions as to

future expansion until they become sure what the longer lasting effects of the unrest will be. As a result

many recent leases have been for small amounts of space and are often companies re-locating for

better rental terms rather than new companies entering the Bahrain market.

3.8.3. Shell and core space in Sanabis, has been offered at as low as BD2.000 per square metre. This

highlights the current trend of tenants wishing to avoid costly fit out works while landlords display

continuing willingness to provide incentives such as fitted out units.

3.8.4. We believe that this current market dynamic of over supply coupled with falling rents will continue in the

short to medium term as the market attempts to absorb stock.

Car Parking

3.9.1. Historically the provision of car parking, particularly in the main commercial areas of Bahrain, has been

poor.

3.9.2. Building owners and developers have sought to maximise what they see as the income generating

elements of a development, to the detriment of car parking.

3.9.3. In part, this was exacerbated by the Ministry of Municipalities, Affairs and Agriculture which stipulated

low ratios between built up area (BUA) and car parking provision within its development regulations.

Current car parking ratios for commercial site is a minimum of one space per 100 square metres,

compared to one space per 150 square metres in the 1998 regulations. Even at the current ratio, the

demand for car parking in a fully occupied office tower exceeds the regulations for provision.

3.9.4. There were a number of sites in key commercial areas which were un-developed and as a result

occupiers of properties which were underprovided in terms of car parking would park on these adjacent

vacant lots.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 22

3.9.5. As these lots were developed, the pressure on car parking increased. A number of land owners

developed both grade, surfaced and multi storey car parking and charged licensees to park. Those

unwilling to pay these charges, particularly in the Diplomatic Area, began double parking, on already

narrow roads, leading to the current congestion problems.

3.9.6. Increasing demand for car parking, particularly from banking institutions head quartered in the

Diplomatic Area, led to an increase in the monthly rental rates for car parking spaces.

3.9.7. We are aware of a number of car parks in the Diplomatic Area charging between BD75.000 and

BD100.000, per month while land adjacent to the Diplomat Tower is achieving between BD75.000 and

BD80.000 per space, per month.

3.9.8. We understand that the City Plaza development by Venture Capital Bank is currently achieving

BD80.000 per space, down from BD120.000 per month in the previous years.

3.9.9. As the popularity of the Diplomatic Area as an office location wanes, with occupiers seeking more

recently constructed, better quality stock, with improved car parking ratios and less congestion, in areas

such as Al Seef District and Bahrain Financial Harbour, demand for car parking in the Diplomatic Area

is likely to reduce.

Introduction to Retail Sector

3.10.1. To a large extent the retail market in Bahrain is supported by the spending of foreign nationals, primarily

from the GCC. In particular the retail market in Bahrain relies on the considerable spending power of

Saudi Arabian tourists who visit the Kingdom via the King Fahad Causeway.

3.10.2. Completed retail mall space has increased five fold from approximately 100,000 square metres to

500,000 square metres since 2000.

3.10.3. Of this retail space approximately 80% is located in Al Seef District and Central Manama which has led

to congestion and some developers looking to alternative locations for future schemes.

3.10.4. With approximately 75,000 square metres of additional retail space planned to come on line.Tthe

Bahrain retail market looks set to suffer from a continued supply / demand imbalance.

3.10.5. The above future supply figures do not take account of the large amount of potential pipeline supply

that will be situated in master planned developments such as Amwaj Islands, Reef Island and Bahrain

Bay.

3.10.6. There are also a number of smaller, stand alone schemes in areas such as Riffa, Saar and Budaiya

which have led to a two tiered market comprising neighbourhood retail centres serving their immediate

locality and those retail malls that act as destinations, such as City Centre, which attract clientele from

outside of Bahrain.

Market Dynamics

3.11.1. The retail market in Bahrain is dominated by a small number of large retail malls situated in the Al Seef

District and Northern Manama area which offer destination shopping and provide a wide range of

brands, entertainment and food and beverage outlets.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 23

3.11.2. As mentioned above, supply of retail space has increased dramatically in the past 10 years with Majid

Al Futtaim’s City Centre being the largest single offering.

3.11.3. With the opening of City Centre the supply of retail mall space doubled and overtook Seef Mall as

Bahrain’s premier mall.

3.11.4. Due to the size and extensive range of the retail offering, City Centre changed the dynamics of the retail

market in Bahrain in much the same way that Mall of the Emirates altered the retail sector in Dubai.

3.11.5. For a number of years, the largest and most successful malls have been located in Al Seef District, a

prominent commercial area with high visibility to passing traffic on the Khalifa bin Salman Highway.

Existing Supply

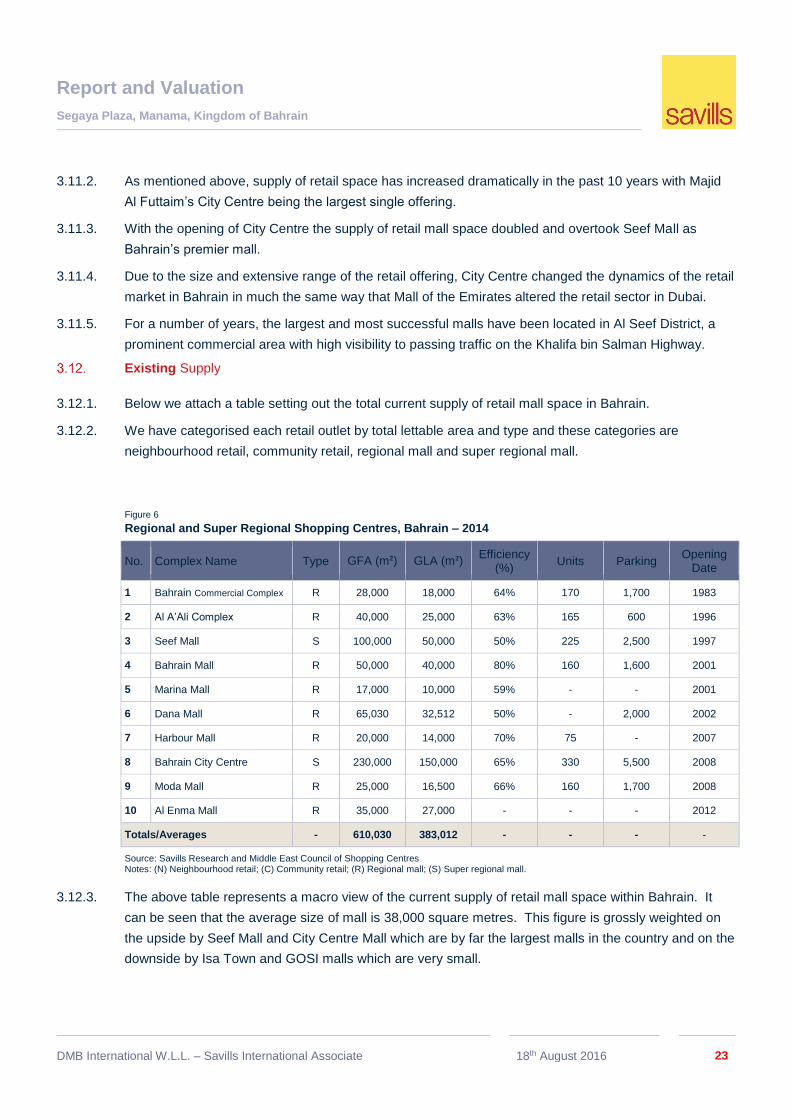

3.12.1. Below we attach a table setting out the total current supply of retail mall space in Bahrain.

3.12.2. We have categorised each retail outlet by total lettable area and type and these categories are

neighbourhood retail, community retail, regional mall and super regional mall.

Figure 6

Regional and Super Regional Shopping Centres, Bahrain – 2014

No. Complex Name Type GFA (m²) GLA (m²) Efficiency

(%) Units Parking

Opening Date

1 Bahrain Commercial Complex R 28,000 18,000 64% 170 1,700 1983

2 Al A’Ali Complex R 40,000 25,000 63% 165 600 1996

3 Seef Mall S 100,000 50,000 50% 225 2,500 1997

4 Bahrain Mall R 50,000 40,000 80% 160 1,600 2001

5 Marina Mall R 17,000 10,000 59% - - 2001

6 Dana Mall R 65,030 32,512 50% - 2,000 2002

7 Harbour Mall R 20,000 14,000 70% 75 - 2007

8 Bahrain City Centre S 230,000 150,000 65% 330 5,500 2008

9 Moda Mall R 25,000 16,500 66% 160 1,700 2008

10 Al Enma Mall R 35,000 27,000 - - - 2012

Totals/Averages - 610,030 383,012 - - - -

Source: Savills Research and Middle East Council of Shopping Centres Notes: (N) Neighbourhood retail; (C) Community retail; (R) Regional mall; (S) Super regional mall.

3.12.3. The above table represents a macro view of the current supply of retail mall space within Bahrain. It

can be seen that the average size of mall is 38,000 square metres. This figure is grossly weighted on

the upside by Seef Mall and City Centre Mall which are by far the largest malls in the country and on the

downside by Isa Town and GOSI malls which are very small.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 24

3.12.4. Adopting the inter quartile range rather than the straight average, the average size of mall falls to

26,000 square metres. This equates to the size of a community mall which clearly shows how Bahrain

is predominantly served by smaller malls when compared to centres such as Dubai.

Neighbourhood and Community Retail Supply

Figure 7

Neighbourhood and Community Retail Centre Supply, Bahrain

No. Complex Name Type Location GFA (m²) GLA (m²) Units Parking Opening

Date

1 Yateem Centre C Manama 20,000 6,000 90 54 1981

2 Al Alawi Complex C Sanad 14,000 9,000 - - 1984

3 Jawad Dome N Budaiya 6,500 5,500 15 230 1988

4 Isa Town Mall C Isa Town 11,710 5,556 114 550 1992

5 GOSI Shopping Complex C Manama 30,000 7,433 160 400 1995

6 Najibi Centre N Budaiya 5,000 3,500 24 100 1995

7 Sitra Mall C Sitra 35,000 24,000 70+ 600+ 2007

8 Country Mall C Budaiya 10,000 7,700 73 370 2007

9 The Lagoon C Muharraq 55,000 34,986 139 1,800 2009

10 Oasis Mall C Muharraq 16,000 12,000 - 250 2009

11 Riffa Lulu C Riffa 25,000 15,000 - - 2009

12 Oasis Centre C Riffa 16,000 12,000 - 250 2009

13 Ramli Mall C A’Ali 72,000 42,000 115 1,400 2011

14 Muharraq Lulu C Muharraq 28,000 20,000 - - 2011

15 Uptown Village N Budaiya 4,500 4,000 16 50 2011

16 Palm Square N Budaiya 3,250 3,000 12 55 2011

17 Al Reem Centre N Riffa 1,800 1,600 20 65 2011

18 St. Christopher’s Centre N Saar 2,100 1,950 30 85 2012

19 The Walk N Riffa 3,600 3,040 17 230 2012

20 Al Hayat Shopping Centre C Segaya 12,000 5,000 24 210 2012

21 Talal Plaza N Segaya TBC TBC - - 2013

22 Saar Mall C Saar 5,600 3,360 52 144 2013

Totals/Averages - - - - -

Source: Savills Research and Middle East Council of Shopping Centres Notes: (N) Neighbourhood retail; (C) Community retail; (R) Regional mall; (S) Super regional mall.

Supply Trends

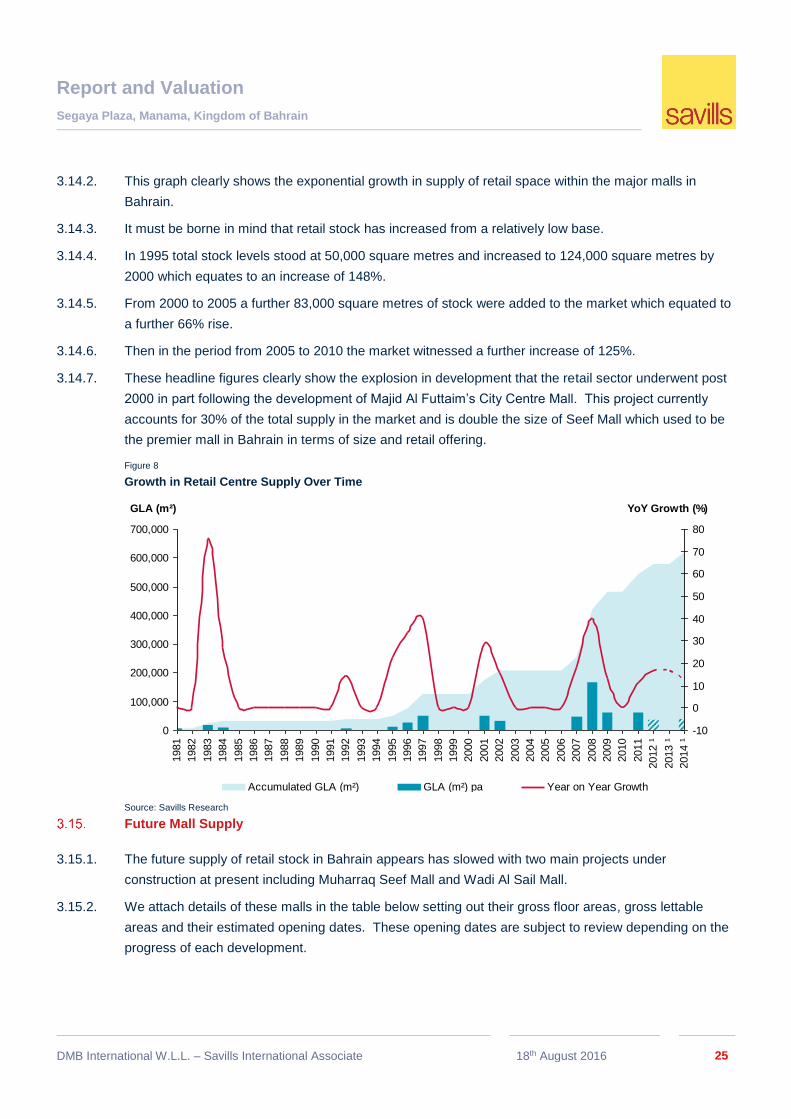

3.14.1. We have tracked the increase in the supply of retail stock coming to the market for over two decades

and the resultant chart is attached below.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 25

3.14.2. This graph clearly shows the exponential growth in supply of retail space within the major malls in

Bahrain.

3.14.3. It must be borne in mind that retail stock has increased from a relatively low base.

3.14.4. In 1995 total stock levels stood at 50,000 square metres and increased to 124,000 square metres by

2000 which equates to an increase of 148%.

3.14.5. From 2000 to 2005 a further 83,000 square metres of stock were added to the market which equated to

a further 66% rise.

3.14.6. Then in the period from 2005 to 2010 the market witnessed a further increase of 125%.

3.14.7. These headline figures clearly show the explosion in development that the retail sector underwent post

2000 in part following the development of Majid Al Futtaim’s City Centre Mall. This project currently

accounts for 30% of the total supply in the market and is double the size of Seef Mall which used to be

the premier mall in Bahrain in terms of size and retail offering.

Figure 8

Growth in Retail Centre Supply Over Time

Source: Savills Research

Future Mall Supply

3.15.1. The future supply of retail stock in Bahrain appears has slowed with two main projects under

construction at present including Muharraq Seef Mall and Wadi Al Sail Mall.

3.15.2. We attach details of these malls in the table below setting out their gross floor areas, gross lettable

areas and their estimated opening dates. These opening dates are subject to review depending on the

progress of each development.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012 ¹

2013 ¹

2014 ¹

GLA (m²)

-10

0

10

20

30

40

50

60

70

80

YoY Growth (%)

Accumulated GLA (m²) GLA (m²) pa Year on Year Growth

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 26

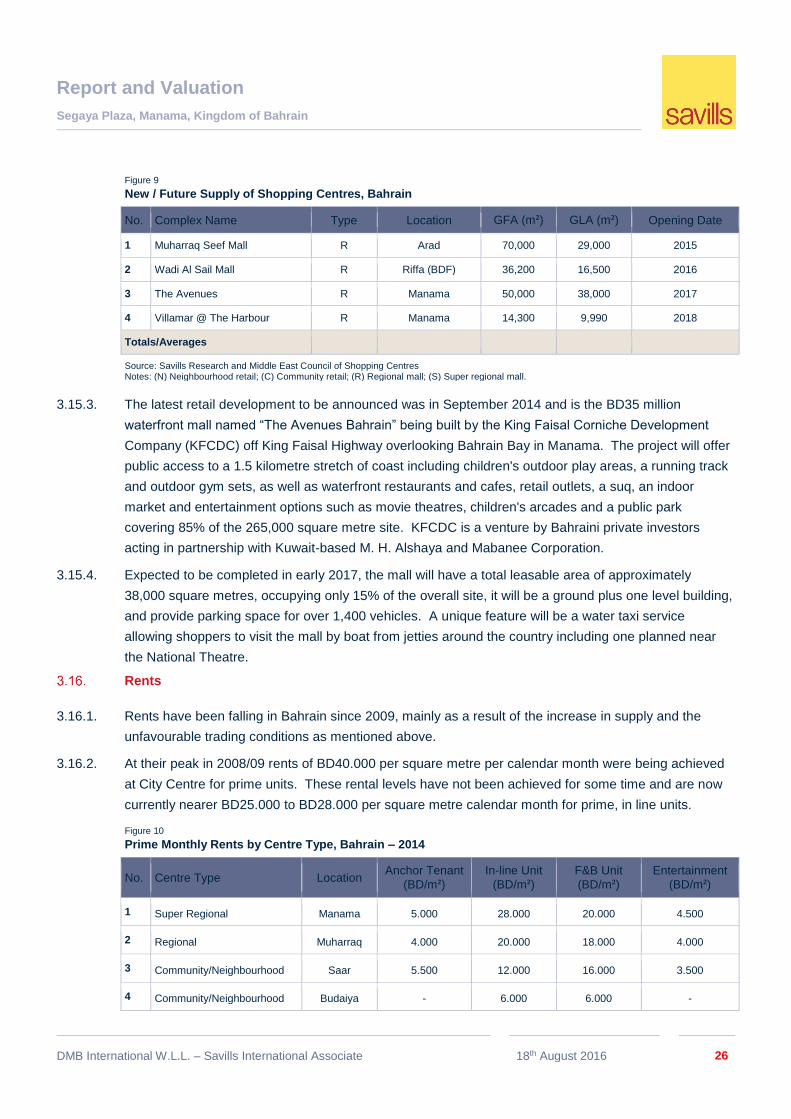

Figure 9

New / Future Supply of Shopping Centres, Bahrain

No. Complex Name Type Location GFA (m²) GLA (m²) Opening Date

1 Muharraq Seef Mall R Arad 70,000 29,000 2015

2 Wadi Al Sail Mall R Riffa (BDF) 36,200 16,500 2016

3 The Avenues R Manama 50,000 38,000 2017

4 Villamar @ The Harbour R Manama 14,300 9,990 2018

Totals/Averages

Source: Savills Research and Middle East Council of Shopping Centres Notes: (N) Neighbourhood retail; (C) Community retail; (R) Regional mall; (S) Super regional mall.

3.15.3. The latest retail development to be announced was in September 2014 and is the BD35 million

waterfront mall named “The Avenues Bahrain” being built by the King Faisal Corniche Development

Company (KFCDC) off King Faisal Highway overlooking Bahrain Bay in Manama. The project will offer

public access to a 1.5 kilometre stretch of coast including children's outdoor play areas, a running track

and outdoor gym sets, as well as waterfront restaurants and cafes, retail outlets, a suq, an indoor

market and entertainment options such as movie theatres, children's arcades and a public park

covering 85% of the 265,000 square metre site. KFCDC is a venture by Bahraini private investors

acting in partnership with Kuwait-based M. H. Alshaya and Mabanee Corporation.

3.15.4. Expected to be completed in early 2017, the mall will have a total leasable area of approximately

38,000 square metres, occupying only 15% of the overall site, it will be a ground plus one level building,

and provide parking space for over 1,400 vehicles. A unique feature will be a water taxi service

allowing shoppers to visit the mall by boat from jetties around the country including one planned near

the National Theatre.

Rents

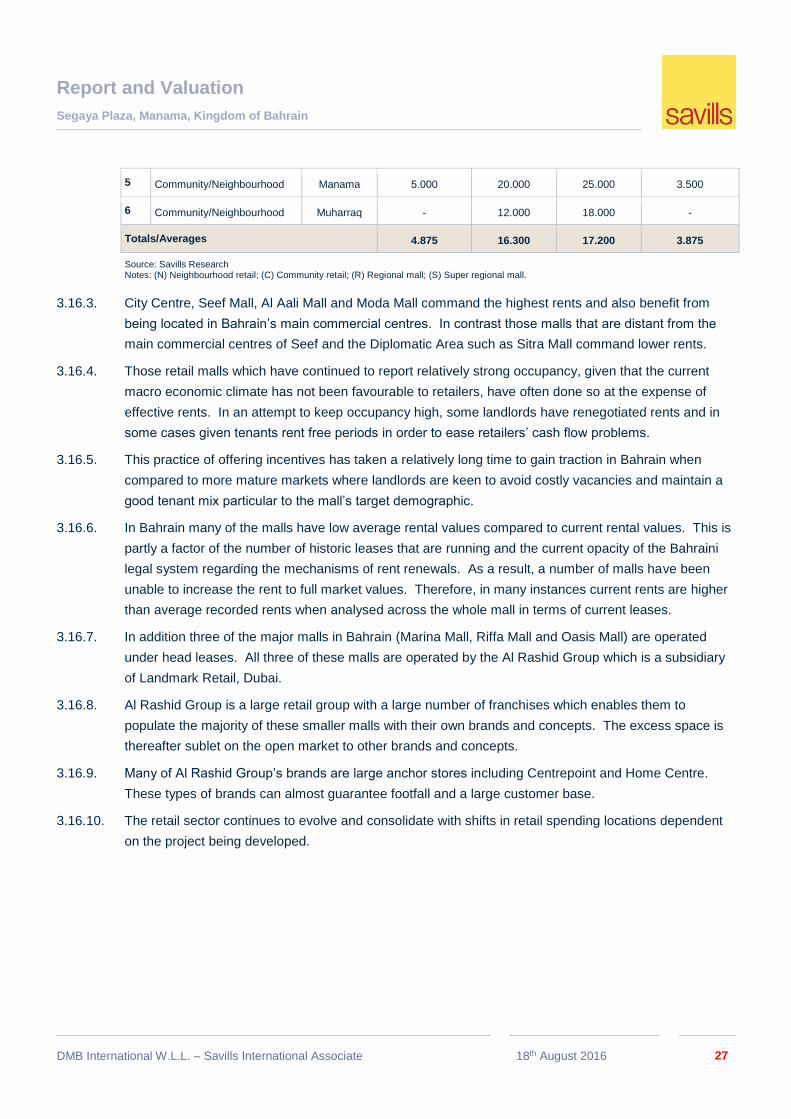

3.16.1. Rents have been falling in Bahrain since 2009, mainly as a result of the increase in supply and the

unfavourable trading conditions as mentioned above.

3.16.2. At their peak in 2008/09 rents of BD40.000 per square metre per calendar month were being achieved

at City Centre for prime units. These rental levels have not been achieved for some time and are now

currently nearer BD25.000 to BD28.000 per square metre calendar month for prime, in line units.

Figure 10

Prime Monthly Rents by Centre Type, Bahrain – 2014

No. Centre Type Location Anchor Tenant

(BD/m²) In-line Unit

(BD/m²) F&B Unit

(BD/m²) Entertainment

(BD/m²)

1 Super Regional Manama 5.000 28.000 20.000 4.500

2 Regional Muharraq 4.000 20.000 18.000 4.000

3 Community/Neighbourhood Saar 5.500 12.000 16.000 3.500

4 Community/Neighbourhood Budaiya - 6.000 6.000 -

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 27

5 Community/Neighbourhood Manama 5.000 20.000 25.000 3.500

6 Community/Neighbourhood Muharraq - 12.000 18.000 -

Totals/Averages 4.875 16.300 17.200 3.875

Source: Savills Research Notes: (N) Neighbourhood retail; (C) Community retail; (R) Regional mall; (S) Super regional mall.

3.16.3. City Centre, Seef Mall, Al Aali Mall and Moda Mall command the highest rents and also benefit from

being located in Bahrain’s main commercial centres. In contrast those malls that are distant from the

main commercial centres of Seef and the Diplomatic Area such as Sitra Mall command lower rents.

3.16.4. Those retail malls which have continued to report relatively strong occupancy, given that the current

macro economic climate has not been favourable to retailers, have often done so at the expense of

effective rents. In an attempt to keep occupancy high, some landlords have renegotiated rents and in

some cases given tenants rent free periods in order to ease retailers’ cash flow problems.

3.16.5. This practice of offering incentives has taken a relatively long time to gain traction in Bahrain when

compared to more mature markets where landlords are keen to avoid costly vacancies and maintain a

good tenant mix particular to the mall’s target demographic.

3.16.6. In Bahrain many of the malls have low average rental values compared to current rental values. This is

partly a factor of the number of historic leases that are running and the current opacity of the Bahraini

legal system regarding the mechanisms of rent renewals. As a result, a number of malls have been

unable to increase the rent to full market values. Therefore, in many instances current rents are higher

than average recorded rents when analysed across the whole mall in terms of current leases.

3.16.7. In addition three of the major malls in Bahrain (Marina Mall, Riffa Mall and Oasis Mall) are operated

under head leases. All three of these malls are operated by the Al Rashid Group which is a subsidiary

of Landmark Retail, Dubai.

3.16.8. Al Rashid Group is a large retail group with a large number of franchises which enables them to

populate the majority of these smaller malls with their own brands and concepts. The excess space is

thereafter sublet on the open market to other brands and concepts.

3.16.9. Many of Al Rashid Group’s brands are large anchor stores including Centrepoint and Home Centre.

These types of brands can almost guarantee footfall and a large customer base.

3.16.10. The retail sector continues to evolve and consolidate with shifts in retail spending locations dependent

on the project being developed.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 28

4. Valuation Advice

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 29

Approach to Valuation

Since our 2015 valuation and commentary a number of new influences are coming to place which would affect the market’s

opinion of this high standard office building.

These factors include:-

The undoubted slowdown in the Bahrain economy caused by a reduction in global oil prices which is resulting in the

Government having a substantial budget deficit;

Similar macro-economic issues are also affecting Saudi Arabia and most of the GCC countries with budget deficits in

almost every country financed by drawing on previous current account surpluses or the bond / sukkuk markets;

Additionally, in Bahrain political issues remain and have an influence on foreign investment into the country;

In recent days global financial markets have been thrown into further turmoil with the UK Brexit decision, extremist

attacks in mainland Europe, the attempted coup in Turkey and the impending US election.

Global investors have focused on liquid assets in the prime core markets and several real estate investment trusts

have been put under pressure to liquidate holdings.

While the US Dollar and GCC currencies have remained firm, they have escalated in comparative terms.

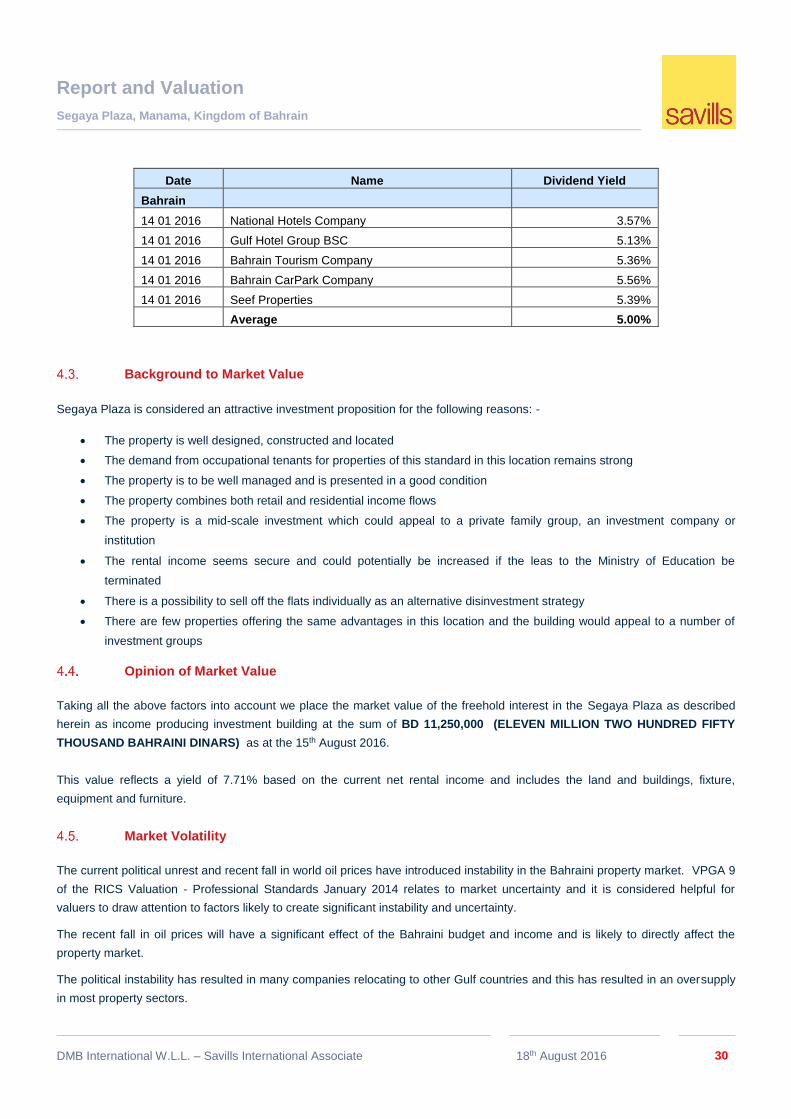

Principal Valuation Consideration

Several property transactions have taken place in the property market over the last few years, which indicates that prime yields

are between 7 to 8%. There has been a compression of real estate yields in the international markets over the last 18 months

with significant activity in the main core capital cities, particularly the UK, Europe and USA.

There are a few actual investment property transaction which taken places in the recent times in Bahrain and indicate a level

of demand, pricing and yield. These include:-

The 2014 sale Addax Bank Head Office in Seef to BMMI reported at BD 8.6 million

The sale of Taib Bank Head office building in the Diplomatic Quarter to ABC Banks reported at US $ 10 million in

2014

The sale / retail investment units between a UAE Investment house and a Bahrain Based Investment Bank, August

2015.

The most recent transaction, which occurred in August 2015, was based on a yield of 8% for leased assets and 9% for

unleased assets. It should be noted that the largest of these transactions was significantly smaller than the subject property

and devaluation led to capital value ranging from only BD 400 to BD 800 per m2 of GLA.

In Bahrain there are four companies listed on the Bahrain bourse which give a dividend yield of between 5 to 6% with long-

term listings and trading patterns. The level of hotel development activity indicates that investors still see strong potential in

the market and are prepared to commit significant capital sums to individual projects. While the general economy has

softened in the last six months, the hospitality sector is being actively promoted as a means of reinvigorating the broader

services sector.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 30

Date Name Dividend Yield

Bahrain

14 01 2016 National Hotels Company 3.57%

14 01 2016 Gulf Hotel Group BSC 5.13%

14 01 2016 Bahrain Tourism Company 5.36%

14 01 2016 Bahrain CarPark Company 5.56%

14 01 2016 Seef Properties 5.39%

Average 5.00%

Background to Market Value

Segaya Plaza is considered an attractive investment proposition for the following reasons: -

The property is well designed, constructed and located

The demand from occupational tenants for properties of this standard in this location remains strong

The property is to be well managed and is presented in a good condition

The property combines both retail and residential income flows

The property is a mid-scale investment which could appeal to a private family group, an investment company or

institution

The rental income seems secure and could potentially be increased if the leas to the Ministry of Education be

terminated

There is a possibility to sell off the flats individually as an alternative disinvestment strategy

There are few properties offering the same advantages in this location and the building would appeal to a number of

investment groups

Opinion of Market Value

Taking all the above factors into account we place the market value of the freehold interest in the Segaya Plaza as described

herein as income producing investment building at the sum of BD 11,250,000 (ELEVEN MILLION TWO HUNDRED FIFTY

THOUSAND BAHRAINI DINARS) as at the 15th August 2016.

This value reflects a yield of 7.71% based on the current net rental income and includes the land and buildings, fixture,

equipment and furniture.

Market Volatility

The current political unrest and recent fall in world oil prices have introduced instability in the Bahraini property market. VPGA 9

of the RICS Valuation - Professional Standards January 2014 relates to market uncertainty and it is considered helpful for

valuers to draw attention to factors likely to create significant instability and uncertainty.

The recent fall in oil prices will have a significant effect of the Bahraini budget and income and is likely to directly affect the

property market.

The political instability has resulted in many companies relocating to other Gulf countries and this has resulted in an oversupply

in most property sectors.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 31

As Bahrain is heavily financially dependent on its oil exports the price instability is likely to have a significant impact on the

property market and certainty is unlikely to return until there is stability in oil prices and the longer term impacts are more fully

known and reflected by buyers and sellers.

Confidentiality and Disclosure

Our valuation is confidential to the addressees for the specific purpose to which our instruction refers and no responsibility is

accepted to any third party for the whole or any part of its contents.

If our opinion of value is disclosed to persons other than the addressees of this report, the basis of valuation should be stated.

Before the report or any part of it is reproduced, or referred to in any document, circular or statement, and before its contents or

contents of any part of it are disclosed verbally to a third party, our written approval as to the form and context of such

publication or disclosure must first be obtained.

Signature

For and on behalf of DMB International WLL

Savills International Associate

Donald Bradley FRICS

RICS Registered Valuer CEO DMB International W.L.L.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 32

5. General Assumptions & Conditions to Valuations

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 33

General Assumptions and Conditions

5.1.1. General Assumptions

1. Unless otherwise stated in this report, our valuation has been carried out on the basis of the following General

Assumptions. If any of them are subsequently found not to be valid, we may wish to review our valuation, as there may

be an impact on it.

2. That the property is not subject to any unusual or especially onerous restrictions, encumbrances or outgoings

contained in the Freehold Title. Should there be any mortgages or charges, we have assumed that the property would

be sold free of them. We have not inspected the Title Deeds.

3. That we have been supplied with all information likely to have an effect on the value of the property, and that the

information supplied to us and summarised in this report is both complete and correct.

4. That the building has been constructed and is used in accordance with all statutory and municipal requirements, and

that there are no breaches of planning control. Likewise, that any future construction or use will be lawful (other than

those points referred to above).

5. That the property is connected, or capable of being connected without undue expense, to the public services of,

electricity, water, telephones and sewerage.

6. That in the construction or alteration of the building no use was made of any deleterious or hazardous materials or

techniques, such as high alumina cement, calcium chloride additives, woodwool slabs used as permanent shuttering

and the like (other than those points referred to above). We have also assumed that any building cladding is

incombustible and fully compliant with UK and US building codes. We have not carried out any investigations into

these matters.

7. That the property does not suffer from any risk of flooding. We have not carried out any investigation into this matter.

8. That the property either complies with all regulations relating to occupation, or if there is any such non-compliance, it is

not of a substantive nature.

9. That the property does not suffer from any ill effects of Radon Gas, high voltage electrical supply apparatus and other

environmental detriment.

10. That there are no adverse site or soil conditions, that the property is not adversely affected by environmental or other

regulations, that the ground does not contain any archaeological remains, nor that there is any other matter that would

cause us to make any allowance for exceptional delay or site or construction costs in our valuation.

5.1.2. General Conditions

Our valuation has been carried out on the basis of the following general conditions:

1. We have made no allowance for any taxation liability that might arise upon a sale of the property.

2. No allowance has been made for any expenses of realisation.

3. Excluded from our valuation is any additional value attributable to goodwill, or to fixtures and fittings which are only of

value in situ to the present occupier.

Additional assumptions and conditions are contained in our Terms of Business attached hereto.

Report and Valuation

Segaya Plaza, Manama, Kingdom of Bahrain

DMB International W.L.L. – Savills International Associate 18th August 2016 34

These General Terms of Business comprise a part of our Terms of Engagement. The following General Terms of Business apply to all professional assignments, valuations and appraisals undertaken by DMB International WLL. unless specifically agreed otherwise in confirming instructions and so stated within the main body of the valuation report.

1. DMB International – Savills International Associate

DMB International WLL. is a Limited Liability Company registered in the Kingdom of Bahrain and the commercial registration no. 70236, ‘(DMB International)’.

2. Jurisdiction

Commercial law shall apply in every respect in relation to our appointment and the agreement with the client which shall be deemed to have been made in the Kingdom of Bahrain. In the event of a dispute arising, unless expressly agreed otherwise in writing by DMB International, the client, and any third party using any of our reports or correspondence of any kind, will submit to the jurisdiction of the Kingdom of Bahrain only. This will apply wherever the property or the client is located or the advice is provided.

3. Limitations on Liability

3.1 Our valuation is confidential to the party to whom it is addressed for the stated purpose and no liability is accepted to any third party for the whole or any part of its contents. Liability will not subsequently be extended to any other party save on the basis of written and agreed instructions; this may incur an additional fee. Maximum liability shall in no event exceed the fee for the professional assignment subject to end absolute maximum of BD100,000.

3.2 The client agrees not to bring any claim arising out of or in connection with this agreement against any Director, employee, ‘partner’ or consultant of DMB International (each called a ‘DMB International Person’). Those individuals will not have a personal duty of care to the client and any such claim for losses must be brought against DMB International...

3. Nothing in these Terms of Business (or in our letter of engagement) shall exclude or limit our liability in respect of fraud or for death or personal injury caused by our negligence or for any other liability to the extent that such liability may not be excluded or limited as a matter of law .

4. Disclosure and Publication

Neither the whole or any part of our reports or correspondence nor any reference thereto may be included in any published document, circular or statement nor published in any way without our prior written approval of the form and context in which it may appear. Our report in entirely confidential to you.

5. Complaints Procedure

If you have any concerns about our service, please raise them in the first instance with the valuer concerned. If this does not result in a satisfactory resolution, please contact the relevant Head of Department. As required by RICS, we will send you a copy of our Complaints Procedure on request.

6. Our Fees

6.1 All fees and expenses are payable to DMB International W.L.L. payments are to be made by the Client within 14 days of fee account submission and failure to remit fees may result in DMB International suspending or terminating the agreement. In such case the payments set out in this agreement above will be payable in full without deduction.

Interest may be charged on unpaid fees 14 days after the date of the invoice, at a rate of 3% per annum above the base rate of Standard Chartered Bank Bahrain from the invoice date of until payment is made.

6.2 If you end this instruction at any stage, we will charge abortive fees on the

basis of reasonable time and expenses incurred.

6.3 Where a valuation is for loan security purposes, and we agree to accept

payment of our fee from the borrower, the fee remains due from yourselves until payment is received by us. Additionally, payment of our fee is not conditional upon the loan being drawn down or any conditions of the loan being met.

7. Assignment

You may not assign this agreement or any of your rights under it without our consent. The Services will be provided solely for the benefit of the Client and not for the benefit of and may not be relied on by any other party or person. Any arrangement for the benefit of any of our services to be passed on to any third party must be agreed with us at the time.

8. Disclosable Interests

We may offer the following services to prospective purchasers and similarly the services may be offered to them by another organisation in circumstances where we may benefit financially: financial services, property letting and management services, building construction, refurbishment and maintenance services and the sale of the prospective purchaser’s property.

9. RICS Valuation Standards - "The Red Book"

Valuations and appraisals will be carried out in accordance with the RICS Valuation – Professional Standards January 2014 ("The Red Book"), by valuers who conform to its requirements and with regard to relevant statutes or regulations. Compliance with The Red Book is mandatory for Chartered Surveyors in the interests of maintaining high standards of service and for the protection of clients.

10. Monitoring

The valuation may be subject to monitoring under the RICS conduct and disciplinary regulations.

11. Valuation Basis

Valuations and appraisals are carried out on a basis appropriate to the purpose for which they are intended and in accordance with the relevant definitions, commentary and assumptions contained in The Red Book. The basis of valuation will be agreed with you in the letter covering the specific terms for the instruction.

12. Portfolios

Where requested to value a portfolio, unless specifically agreed with you otherwise, we will value the individual properties separately, upon the assumption that the properties have been marketed in an orderly manner.

13. Title and Burdens

We do not read documents of title although, where provided, we consider and take account of matters referred to in solicitor’s reports or certificates of title. We would normally assume, unless specifically informed and stated otherwise, that each property has good and marketable title and that all documentation is satisfactorily drawn and that there are no unusual outgoings, planning proposals, onerous restrictions or local authority intentions which affect the property, nor any material litigation pending.

14. Disposal Costs and Liabilities