Download - Dth business in pakistan

The DTH Business in Pakistan Zulfiqar Qazilbash

Opportunity Overview

www.isbconsult.com

Table of Contents

1. About Islamabad Consulting 2. The Global DTH Market 3. The Landscape in Pakistan 4. Lessons from the Indian DTH Experience 5. Indian DTH Marketing practices 6. The Pakistan Opportunity 7. Analysis of the Market 8. GTM strategy outline 9. Product Packaging 10. Potential Revenues 11. Business Model 12. Sales Management 13. Keys to Success 14. The First 90 days

Zulfiqar Qazilbash www.isbconsult.com

About Islamabad Consulting

Small boutique consultancy firm focusing on: • Market research and go

to market strategy • M&A and new markets

advisory • Project feasibility • Program management • Training and certifications For more information www.isbconsult.com

Zulfiqar Qazilbash

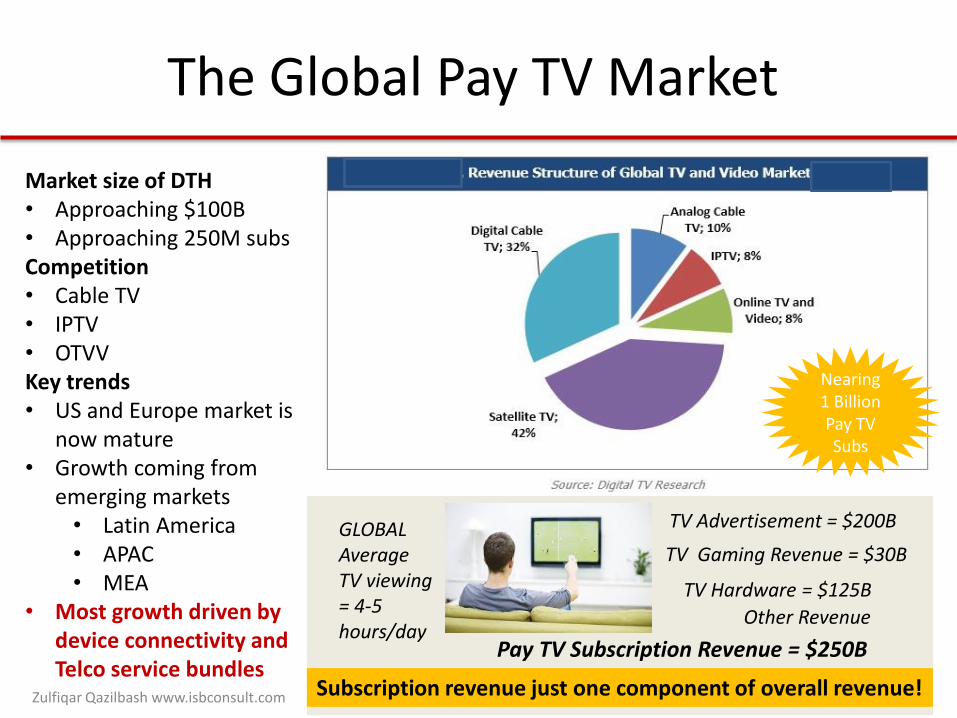

The Global Pay TV Market

Market size of DTH • Approaching $100B • Approaching 250M subs Competition • Cable TV • IPTV • OTVV Key trends • US and Europe market is

now mature • Growth coming from

emerging markets • Latin America • APAC • MEA

• Most growth driven by device connectivity and Telco service bundles

GLOBAL Average TV viewing = 4-5 hours/day

Pay TV Subscription Revenue = $250B

TV Hardware = $125B

TV Gaming Revenue = $30B

Subscription revenue just one component of overall revenue!

TV Advertisement = $200B

Nearing 1 Billion Pay TV Subs

Other Revenue

Zulfiqar Qazilbash www.isbconsult.com

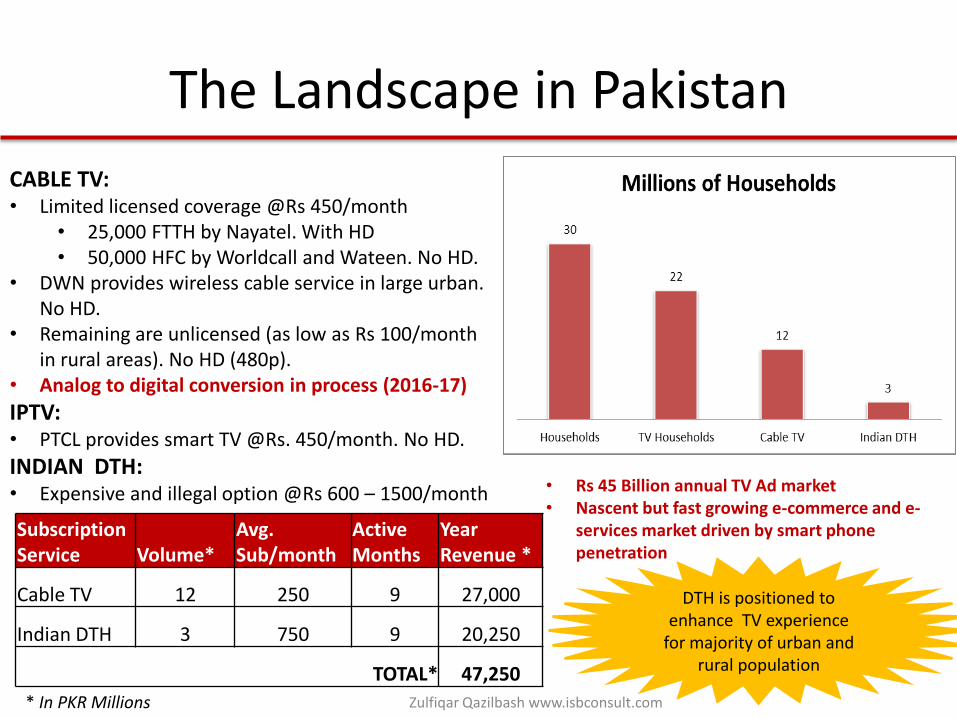

The Landscape in Pakistan

CABLE TV: • Limited licensed coverage @Rs 450/month

• 25,000 FTTH by Nayatel. With HD • 50,000 HFC by Worldcall and Wateen. No HD.

• DWN provides wireless cable service in large urban. No HD.

• Remaining are unlicensed (as low as Rs 100/month in rural areas). No HD (480p).

• Analog to digital conversion in process (2016-17)

IPTV: • PTCL provides smart TV @Rs. 450/month. No HD.

INDIAN DTH: • Expensive and illegal option @Rs 600 – 1500/month

Subscription Service Volume*

Avg. Sub/month

Active Months

Year Revenue *

Cable TV 12 250 9 27,000

Indian DTH 3 750 9 20,250

TOTAL* 47,250

* In PKR Millions

DTH is positioned to enhance TV experience

for majority of urban and rural population

• Rs 45 Billion annual TV Ad market • Nascent but fast growing e-commerce and e-

services market driven by smart phone penetration

Zulfiqar Qazilbash www.isbconsult.com

Lessons from the Indian DTH Experience

Key Learning • South Asian market values price above all – growth is limited

by affordability of target population • Customer acquisition cost keeps operations in red during

growth phase • Ability to raise debt becomes a key driver of growth • Churn is lower compared to Telcos (less than 2%/mo.)

Missed Opportunities • VAR revenue is small and operators still searching for the

Killer App • Operators focused late on developing an advertisement

market

250

125 80

55

Households TV Homes DTH Subs Active Subs

Millions of HouseHolds ARPU 150 INR

Major Costs % of Revenue

Operations <50%

Programming Cost

<45%

Sales & Marketing

<15% (Ad spend 5%)

Taxation 30%

All operators took 7 or more years to break even: • 30% EBITA • 10% PAT

Typical customer stays with

operator 8-10 years

Operators took 12-20 months to first 1M subs Breakeven occurred at around 6M subs

Zulfiqar Qazilbash www.isbconsult.com

Indian DTH Marketing Practices

Operator Brand Association

Dish TV First mover

Sun TV Cost effectiveness

TATA Sky Customer service

Video Con Technology

Airtel Digital clarity

Reliance Big TV

VAS

Survey of India consumer priorities: 1. Price 2. Program choices 3. Reception 4. Tech support 5. Customer service 6. Technology

360 Marketing

Bollywood Actors as

Brand Ambassadors

Mobile DTH fitted vans

for rural areas

TV Set & Telecom

Dealership Alliances

Zulfiqar Qazilbash www.isbconsult.com

The Pakistan Opportunity

Move the role of TV from that of simple entertainment to a major enabling appliance for all major household aspirations and needs

A properly designed

interactive TV can function

as a semi literate

person’s PC

VAS drivers Urban Semi Urban Rural

Aspirations Wants to follow global trends

Wants the urban experience

Enhance quality of life

Package • Latest Technology

• Latest OTT apps

• Edutainment content Urban theme

• Window into the world

• Eliminate travel costs

Brand Personality

New and Trendy

Fashionable and Cosmopolitan

Friendly and Easy to Use

Content Type Example

Fresh global content

Refreshed urban context and themes

Services & Education

Organized content can eliminate the clutter, confusion and frustration associated with unguided internet browsing for less sophisticated users

Zulfiqar Qazilbash www.isbconsult.com

Analysis of the Market

Bargaining power of Suppliers

Bargaining power of Customers

Threat of Substitutes

Threat of new entrants

Competitive Rivalry

• Potential shortage of satellite transponders • High cost of content till sales volumes pick up • Many options for STBs including local manufacture

• Customers are very price sensitive • First mover generally will have some advantage

• Cable TV is inferior • GPON triple play is more expensive • PTCL IPTV is not as yet well regarded • Online TV and Video has yet to take hold in Pakistan

• Capital Intensive business will limit new entrants • However at this early stage, cant be ruled out • Later first mover advantage and loyalty programs can deter

• 3 licenses will have similar offerings due to license conditions • Rivalry in choice urban areas may lead to price war

Zulfiqar Qazilbash www.isbconsult.com

GTM Strategy

Illegal Indian DTH

connections

inferior Cable connections

Free TV and no TV

connections

Accelerate growth by first targeting lower hanging fruit

Create product bundles after detailed market

segmentation and profiling

Build the largest distributor dealer network

Premium Rs 1000-1500

Value Rs 500-Rs 999

Budget Rs 100-Rs 499

• Kids • Students • Professional • Housewife • Retired

• Wholesale/Franchise • Corporate • Consumer • Multi dwelling • Carriage

Urban Semi Urban Rural

• Entertainment • News • Sports • Education • Health • Fashion • Lifestyle

Zulfiqar Qazilbash www.isbconsult.com

Product Packaging

Self Actualization

Esteem/Respect

Love and Belonging

Safety/Security Needs

Physiological Needs Marriage Agriculture Healthcare

Police Education

Legal E-Gov

Chic Flics Disneyland

Religion

Fashion News

Associations

Lifestyle Skill development

Trade

Maslow’s Pyramid of Needs

Premium

Value

Budget

Urban

Semi Urban

Rural

Proper design of the 5 thematic channels and VAS services will become a Competitive differentiator as well as aid in developing the new DTH Adv market

Zulfiqar Qazilbash www.isbconsult.com

Potential Revenues

Year in Operation 1 2 3 4 5 6 7

Cable TAM (millions) 12.0 12.6 13.2 13.9 14.6 15.3 16.1

Growth 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

DTH Penetration 1.0 5.0 7.0 8.5 10.0 11.5 13.0

Growth 400% 40% 21% 18% 15% 13%

DTH Market share 8.3% 39.7% 52.9% 61.2% 68.6% 75.1% 80.8%

Company Share 50% 50% 50% 50% 50% 50% 50%

Subs 0.5 2.5 3.5 4.25 5 5.75 6.5

Growth 400% 40% 21% 18% 15% 13%

ARPU 450 405 365 328 295 266 239

Decline 10% 10% 10% 10% 10% 10%

Sub Revenue 2,700 12,150 15,309 16,731 17,715 18,335 18,654

VAR Contribution 1% 5% 10% 15% 18% 22% 25%

VAR Revenue 27 608 1531 2510 3189 4034 4663

Growth 2150% 152% 64% 27% 27% 16%

Ad Contribution 1% 5% 8% 11% 13% 15%

Ad Revenue 122 765 1338 1949 2384 2798

Growth 530% 75% 46% 22% 17%

Total Revenue 2,727 12,879 17,605 20,579 22,852 24,752 26,115

Growth 372% 37% 17% 11% 8% 6%

in USD 26.0 122.7 167.7 196.0 217.6 235.7 248.7

Zulfiqar Qazilbash www.isbconsult.com

The Business Model

Customer Acquisition

Installation

Recharge

After Sales Support

DTH Licensee

Distributor

Dealer Customer

Call Center

BUILD A COMPETIITIVE ADVANTAGE OR ELSE OUTSOURCE

Zulfiqar Qazilbash www.isbconsult.com

Sales Management

Zonal Regional Area National

National Sales Head

Zonal Director

North

Zonal Director Central

Zonal Director

South

Sales Executive

Regional Sales

Manager Service

Executive

FOS

Mgmt Trainees

Billing system

CRM

Dash boards

Regional Service

Manager

Zulfiqar Qazilbash www.isbconsult.com

Keys to Success

Critical Indicator Need to have Prefer to build

Subscriptions Revenue Growth

VAS Revenue Growth

Advertisement Revenue Growth

1. Build out distributor partnerships and dealer network

2. Raise debt to acquire new customers

3. Optimize operations 4. Build content partnerships

and service bundling Business Complexity

Technology

Regulatory Framework

Customer Service

Content and bundling

Partnerships

Product Packaging

Dealer Distributor Network

Market Research

and Segmentation

Business Analytics

And Dashboards

Zulfiqar Qazilbash www.isbconsult.com

The First 90 days

1. Get debriefing from

stakeholders

Understand what the stake holders want to achieve with the

business

2. Assess institutional

capacity

Benchmark process against selected international references

3. Develop 5 year strategic

plan

Get vision and fund allocations approved by the board

4. Create business plan

Annual Programs,

targets, budget

Provide monthly

milestones

HR development

plan

Define expected ROI

for each program

5. Create Operational

plans

Workflows and process SOP

Monitoring and evaluation

Design KPIs and simplified dashboards)

Schedule staff trainings

Tender for consultancies

Zulfiqar Qazilbash

Q&A?

www.isbconsult.com

Zulfiqar Qazilbash www.isbconsult.com

The Netflix Phenomenon

Zulfiqar Qazilbash www.isbconsult.com

Video Streaming Market Overview

Zulfiqar Qazilbash www.isbconsult.com

Source: internet search

Global Pay TV Market

Zulfiqar Qazilbash

Pay TV Subscriber Growth

Zulfiqar Qazilbash