1

David Kloeden

June 2014

Presentation Overview

• RA-FIT Project

• RA-FIT Questionnaire

• Preliminary Results of the 1st Iteration

• Launching the 2nd Iteration

• Lessons Learned

The RA-FIT Project

RA-FIT is an IMF initiative to:

• Gather and analyze revenue administration data (quantitative and qualitative)

• Establish baseline measures by appropriate grouping (e.g. regions/income level)

• Raise the importance of revenue administration performance measurement

• Make data/analysis available to member countries for improving cross-country comparisons and benchmarking (seek to provide data, not rank administrations)

• Improve the quality and effectiveness of IMF’s Technical Assistance

The RA-FIT Project

• Our goal: Help strengthen Tax and Customs Administrations’ management and operational performance.

• Our principle: “If you can’t measure it, you can’t manage it.”

• Yet, the first RA-FIT exercise (2012) shows that revenue administration performance measurement has a long way to go, especially in developing countries.

RA-FIT Questionnaire

Questionnaire Structure (1st Iteration)

• A 62-question survey organized along the following themes: Revenue Data Tax and Customs Administrations’ Institutional Arrangements

(type of entity, autonomy, office network, staffing, cost) Tax Administration Operations (registration, filing, audit,

arrears enforcement, dispute resolution) Customs Administration Operations (selectivity channels and

clearance times, post-clearance audits)

• Targeted 120 countries (mainly developing countries supported by our Regional Technical Assistance Centers).

Survey Response Summary

Received returns from 85 of the 120 countries surveyed(70 percent response rate)

9

Composition of Survey Respondents

LIC

LMIC

UMIC

HIC

0% 5% 10% 15% 20% 25% 30% 35%

The income group composition of the 85 respondents

Response rate

AFR

APD

EUR

MCD

WHD

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

The regional composition of the 85 respondents

Response rate

60% of respondents are from LIC AND LMIC countries; 72% are from AFR and WHD (mainly Caribbean and Central America)

Preliminary Results of the 1st Iteration

Data Issues• Key issues to consider:– Responder bias• Not all countries responded to survey• Some countries unable to provide responses to all

questions• Uncertainty regarding definitions of key concepts

– Structural data issues• Diversity of respondents, will affect summary findings

at “overall” level, vs. income or regional levels• Outliers in the response data

Revenue Data• Analysis combines RA-FIT and WEO data• Key issues to investigate:– What can we say about the relationship between

revenue collection and development level?– Does revenue composition (tax type) differ across

geographic regions/income grouping?– Are there any insights on how different taxes

behaved over the past decade (and during the crisis) across regions?

– How does the VAT behave across countries?

13

Taxes on goods and services Social security Taxes on international trade Personal income tax Corporate income tax0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Africa

Asia and Pacific

Europe

Middle East and Central Asia

Western Hemisphere

Tax

Reve

nue

as a

per

cent

of G

DP

Source: World Economic Outlook.

Tax Composition- 2012

14

RA-FIT VAT Composition- 2010

LOW INCOME COUNTRIES LOWER MIDDLE INCOME COUNTRIES

UPPER MIDDLE INCOME COUNTRIES

HIGH INCOME COUNTRIES GRAND TOTAL0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

44% 32% 35% 32% 35%

49%52% 41% 43%

46%

7%16%

24%18%

Refunds % of Gross - 2010

Import % of Gross - 2010

Domestic % of Gross - 2010

Institutional Arrangements • 60 percent of the RA-FIT respondents have tax

and customs administration conducted by directorates of MoFs; the balance have adopted more autonomous arrangements (semi-autonomous bodies with or without boards).

• Unified semi-autonomous bodies are predominant in Anglophone Africa (85 percent of respondents) while less autonomous arrangements predominate in Asia, Middle East and the Caribbean.

16

Institutional Arrangements

21%

1%

6%

72%

Tax and customs integrated ?

AFR APD EUR WHD No

4%1%

9%

4%

82%

Social security collected by the administration?

AFR APD EUR WHD No

17

Human Resources

AFRICA ASIA PACIFIC EUROPE M/E & C ASIA WESTERN HEM Grand Total0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

56%60%

65%60% 59% 58%

19% 10%

10%14% 18% 16%

16%20%

12% 16% 14% 15%

10% 10% 10%

Debt Collection

Audit, Investigation and Verification

Client Account Management

Corporate Support

66 respondents provided tax staffing information from the 83 countries completing tax operations

18

Cost of Collection-Tax Admin

OECD – CIS HIC SAMPLE (13) 1.16% 88% 12%

68 respondents provided total annual expenditure information from the 83 countries completing tax operations

Total Cost of Collection - 2010 Operating Cost % - 2010 Cap Ex Cost % - 2010

LOW INCOME COUNTRIES 2.41% 95% 5%

LOWER MIDDLE INCOME COUNTRIES 2.15% 94% 6%

UPPER MIDDLE INCOME COUNTRIES 1.86% 91% 9%

HIGH INCOME COUNTRIES 1.16% 97% 3%

LOW INCOME COUNTRIES (17)

LOWER MIDDLE INCOME COUNTRIES (24)

UPPER MIDDLE INCOME COUNTRIES (23)

HIGH INCOME COUNTRIES (17)

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

2.41%2.15%

1.86%

1.16% Total Cost of Collection - 2010

19

Cost of Collection- Customs Admin

48 respondents provided total annual expenditure information from the 63 countries completing customs operations

Total Cost of Collection - 2010 Operating Cost % - 2010 Cap Ex Cost % - 2010

LOW INCOME COUNTRIES 2.60% 95% 5%

LOWER MIDDLE INCOME COUNTRIES 2.79% 95% 5%

UPPER MIDDLE INCOME COUNTRIES 4.08% 83% 17%

HIGH INCOME COUNTRIES 5.53% 83% 17%

LOW INCOME COUNTRIES (12)

LOWER MIDDLE INCOME COUNTRIES (17)

UPPER MIDDLE INCOME COUNTRIES (14)

HIGH INCOME COUNTRIES (5)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2.60%

2.79%

4.08%

5.53%

Total Cost of Collection - 2010

20

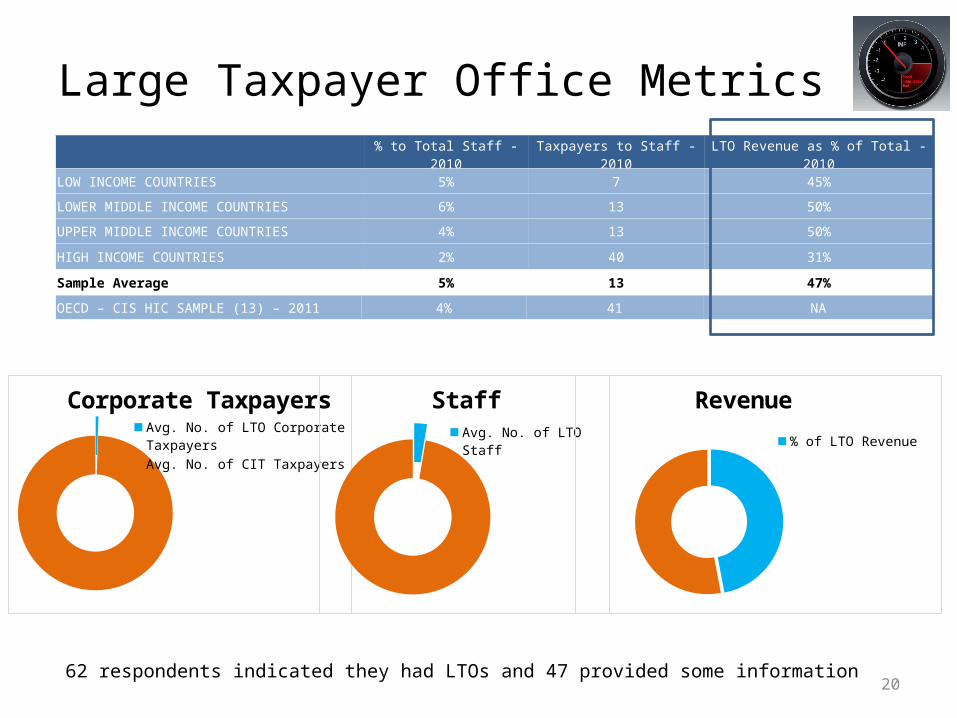

Large Taxpayer Office Metrics

62 respondents indicated they had LTOs and 47 provided some information

% to Total Staff - 2010 Taxpayers to Staff - 2010 LTO Revenue as % of Total - 2010

LOW INCOME COUNTRIES 5% 7 45%

LOWER MIDDLE INCOME COUNTRIES 6% 13 50%

UPPER MIDDLE INCOME COUNTRIES 4% 13 50%

HIGH INCOME COUNTRIES 2% 40 31%

Sample Average 5% 13 47%

OECD – CIS HIC SAMPLE (13) – 2011 4% 41 NA

Corporate Taxpayers

Avg. No. of LTO Corporate Taxpayers

Avg. No. of CIT Taxpayers

StaffAvg. No. of LTO Staff

Avg. No. of Staff

Revenue% of LTO Revenue

% of Non-LTO Revenue

21

On-time Filing Rates

Corporate Income Tax - 2010 Personal Income Tax - 2010 VAT - 2010 0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

46.2%

31.0%

72.3%

47.8%

43.5%

63.2%

53.5%

47.3%

72.2%

49.3%

44.7%

69.1%

LOW INCOME COUNTRIESLOWER MIDDLE INCOME COUNTRIESUPPER MIDDLE INCOME COUNTRIESGrand Total

22

Audit Mix

LOW INCOME COUNTRIES (16)

LOWER MIDDLE INCOME COUNTRIES (20)

UPPER MIDDLE INCOME AND HIGH INCOME

COUNTRIES (19)

Grand Total (55)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

53%

25% 23%33%

28%

50% 52%

44%

19%25% 25% 23%

Desk AuditsIssue Oriented Audits Comprehensive Audits

23

Audit Coverage as a % of Taxpayer Population

40 respondents provided audit coverage information

LIC

LMIC

UMIC/HIC

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Coverage> 5%Coverage 3% - 5%Coverage 1% - 3%Coverage 0% - 1%

24

Audits assessments as a % of collections

AFRICA (20) ASIA PACIFIC (7) EUROPE (7) MIDDLE EAST AND CENTRAL ASIA (3)

WESTERN HEMISPHERE

(17)

Grand Total (54)0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

5.35%

8.76%

6.86%

11.50%

6.14%6.58%

25

Customs: Traffic by Channel

LIC LMIC UMIC HIC Grand Total0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

51.50%

34.39%25.84%

19.99%

34.07%

37.87%

23.57%

51.70%

19.91%

34.78%

10.63%

42.04%

60.09%

31.15%

Green Channel

Yellow Channel Traffic

Red Channel Traffic

26

Customs: Traffic by Channel

AFR APD EUR MCD WHD Grand Total0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

43.22%

31.80%

22.78%

41.00%

27.02%34.07%

39.53%

27.80%40.63%

16.33%

35.23%

34.78%

17.24%

36.59%42.67%

37.75%31.15%

Green Channel

Yellow Channel Traffic

Red Channel Traffic

Launching the 2nd Iteration

2nd Iteration

• New developments for the 2nd round:– Adoption of a web-based platform (rather than an

Excel workbook)– Partnerships with CIAT and WCO– New set of (refined) questions– Development of a dashboard

• Web-based platform to be launched in 2014 Q1

Lessons Learned

Lessons Learned

• Several data problems and challenges (missing data, inconsistencies, sample size)…but, yet, many interesting early conclusions (as we just saw).

• Easy to write strategic plans on paper; much more difficult to apply effective strategic management daily…i.e. measure and follow performance systematically as part of a decision-taking mechanism.

• Performance measurement is an area deserving more international attention and cooperation.

31

THANK YOU!