Currency crises and exchange rate policy

Chapter 9

Learning objectives

• Defining currency crisis• First, second, and third generation

models of currency crises• Role of speculation, expectations, and

international contagion • Coordination, efficiency, frequency, and

measurement of currency crises• Policy trilemma and its role in current

exchange rate problems

International capital mobility is often viewed as the main determinant of financial fragility and financial crises

What is a currency crisis? Speculative attack on the currency (usually when the value of the

currency is expected to change significantly). Investors start selling their investments (denominated in that currency). Currency crises tend to affect fixed exchange rate regimes rather than flexible (floating) regimes.

Initially the authorities may try to resist the devaluation of the currency by raising interest rates and/or selling foreign reserves.

Eventually, the authorities have to let the value of the currency fall.

The speculative attacks on the currency can be largely self-fulfilling.

Note that (i) even in the case where the attacks are not successful there is still a

currency crisis if, for example, the authorities had to raise interest rates significantly or to deplete their foreign exchange reserves.

(ii) A currency crisis may originate from perceived weaknesses of the local economy.

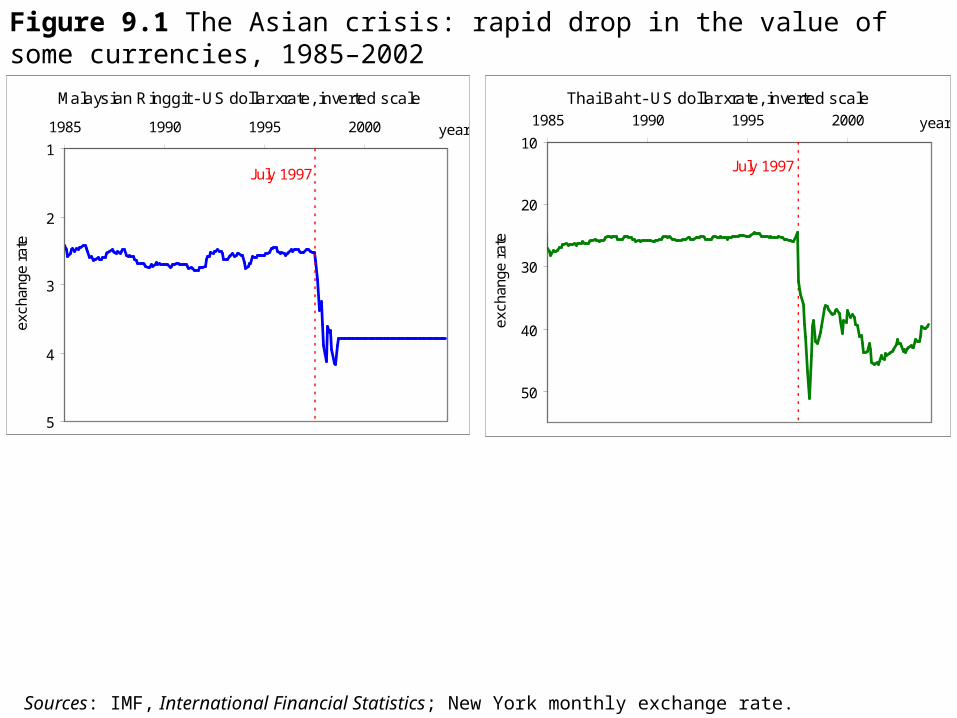

Example: The currency crisis in Southeast Asia in 1997 (Fig. 9.1)

Figure 9.1 The Asian crisis: rapid drop in the value of some currencies, 1985–2002

Malaysian Ringgit - US dollar xrate, inverted scale

1

2

3

4

5

1985 1990 1995 2000 year

exch

ange

rat

e

July 1997

Thai Baht - US dollar xrate, inverted scale

10

20

30

40

50

1985 1990 1995 2000 year

exch

ange

rat

e

July 1997

Sources: IMF, International Financial Statistics; New York monthly exchange rate.

18000

10

20

30

40

1830 1860 1890 1920 1950 1980 2010

perc

ent

Napoleonic wars Great Depression

Asian crisis

Figure 9.2 Currency crashes since 1800

Source: based on Reinhart and Rogoff (2009); share of countries with an annual depreciation greater than 15 per cent, five year moving average.

Frequency and measurement

Empirical studies (e.g., Bordo et al., 2001) find that the frequency of currency crises has increased over time (Fig. 9.2).

Bordo et al. conclude that the increased frequency is largely due to currency crises in emerging markets and the increase in international capital mobility.

Characteristics of currency crises

Reversal of capital flowsA current account surplus has to develop as

the net capital outflow increases (Fig. 9.3)Devaluation of domestic currency implies

higher real value of debt for domestic firms and banks.

Currency crises can have a significant negative impact on real GDP growth (Table 9.1) and per capita income (Fig. 9.4).

Figure 9.3 The Asian crisis: current account balance, 1990–2009, per cent of GDP

Current account balance (% of GDP)

-15

-10

-5

0

5

10

15

20

1990 1995 2000 2005 2010

Thailand

Malaysia

Indonesia

Source: World Development Indicators online

Beugelsdijk, Brakman, Garretsen, and van Marrewijk International Economics and Business© Cambridge University Press, 2013 Chapter 9 – Currency crises and exchange rate policyTable 9.1 Real income growth from before to after the crisis

Real GDP growth

Country Crisis year Previous year Crisis year Following year

Argentina 1995 5.8 −2.8 5.5

Brazil 1999 0.2 0.8 4.2

Indonesia 1998 4.5 −13.1 0.8

Korea 1998 5.0 −6.7 10.9

Mexico 1995 4.4 −6.2 5.2

Philippines 1998 5.2 −0.6 3.3

Thailand 1998 −1.4 −10.8 4.2

Turkey 1994 7.7 −4.7 8.1

Euro area 2008 3.0 0.4 -4.3

Greece 2008 3.0 -0.1 -3.3

Spain 2008 3.5 0.9 -3.7 Source: IMF (2002a, 2012; World Economic Outlook, April 2012).

Figure 9.4 The Asian crisis: developments of GDP per capita, 1990–2009

GDP per capita (PPP, constant 2005 international $)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990 1995 2000 2005 2010

Malaysia

Thailand

Indonesia

1997 2002 2005

2003

Source: World Development Indicators online

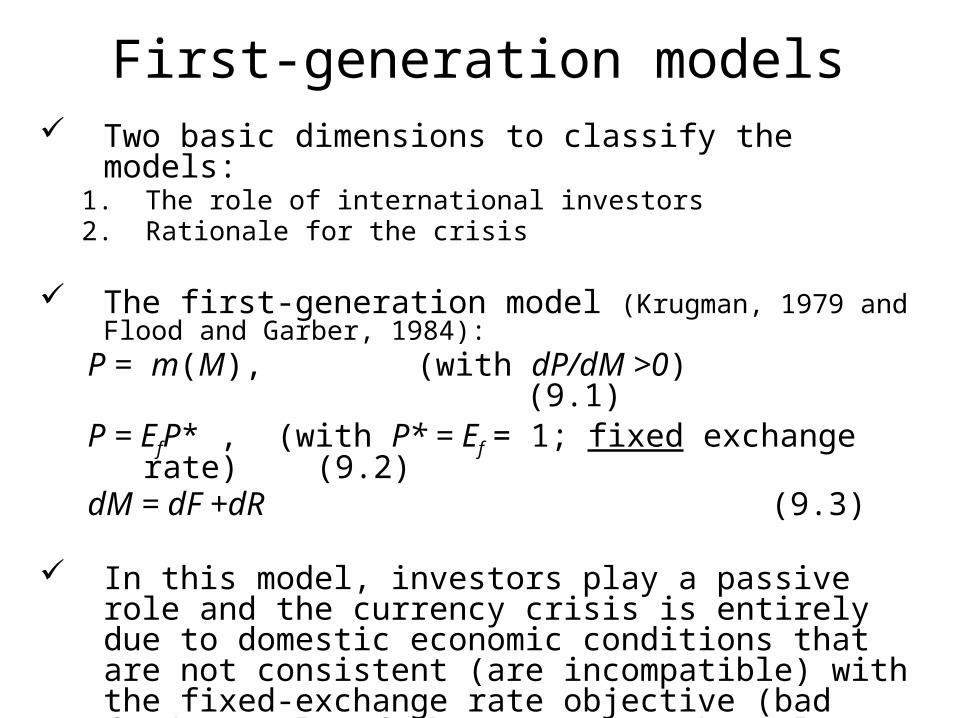

First-generation models Two basic dimensions to classify the models:

1. The role of international investors2. Rationale for the crisis

The first-generation model (Krugman, 1979 and Flood and Garber, 1984):

P = m(M), (with dP/dM >0) (9.1)P = EfP* , (with P* = Ef = 1; fixed exchange rate) (9.2) dM = dF +dR (9.3)

In this model, investors play a passive role and the currency crisis is entirely due to domestic economic conditions that are not consistent (are incompatible) with the fixed-exchange rate objective (bad fundamentals of the economy). The only possible outcome is devaluation of the local currency.

• Is the first-generation model useful? Yes.1. Most economists think that currency

crises are on average the result of bad fundamentals (at least to some degree).

2. The model explains why a currency crisis can happen quite suddenly during a time when the authorities appear to still be able to maintain the fixed-exchange rate.

Box 9.1: Speculative coordination

Coordination of investors’ decision is required for a currency crisis to occur.

Beugelsdijk, Brakman, Garretsen, and van Marrewijk International Economics and Business© Cambridge University Press, 2013 Chapter 9 – Currency crises and exchange rate policy

Table 9.2 Coordination of a speculative attack

Pay-off matrix (investor 2, investor 1)

Investor 1

Sell Hold

Investor 2 Sell (3/2, 3/2) (−1, 0)

Hold (0, −1) (0, 0)

Box 9.1

Second-generation models

The first generation model assumes that both investors and monetary authorities behave passively; their behavior is mechanical.

We need a model that can link currency crises and the loss of confidence in the fixed exchange rate to the workings of the financial sector at large.

In second-generation models, currency crises do not depend only on a given set of fundamentals but also on the behavior of investors.

Second-generation models show multiple equilibria: the occurrence and absence of a speculative currency attack can both be an equilibrium outcome.

The second generation models (Krugman, 1996) are based on three assumptions.

1. Policymakers have a reason to abandon the fixed exchange rate.

2. Policymakers also have a reason to maintain the fixed exchange rate.

3. The cost to maintain the fixed exchange rate rises if investors expect a devaluation of the currency. Investors will demand higher interest rates (Fig. 9.5).

Assumptions (1) and (2) imply that there is a trade-off; there are costs and benefits to maintaining or not maintaining the fixed exchange rate. From assumption (3) we can see that investors determine the policymakers’ position on this trade-off.

Expectations are crucial in these models and the devaluation may or may not take place. It all depends on the interaction between investors and policymakers.

The empirical evidence on the causes of currency crises largely points to the incompatibility between economic fundamentals and the fixed exchange rate.

Kaminsky and Reinhart (1999): countries that are hit by a currency crisis have on average excessive money and credit growth rates, a high current account deficit (high capital inflow), overvalued (in real terms) currency, and lower GDP growth rates.

However, self-fulfilling expectations can also play a role. The evidence on this may be derived from studies examining contagion in currency crises.

Kaminsky and Reinhart (2000, p. 147): “Contagion is a case where knowing that there is a crisis elsewhere increases the probability of a crisis at home.”

(Table 9.3) Fundamentals-based contagion (when a country hit by

the crisis is linked to other countries through international trade or finance) versus pure contagion (self-fulfilling crisis).

Figure 9.5 Interest rates for selected Euro area countries, 1993–2012

Interest rates; selected countries, 1993-2012

0

5

10

15

20

25

30

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Germany Spain Greece Italy Netherlands

Greece

Greece

Germany

Italy

Spain

NL

Source: ECB, monthly interest rates statistics; long term interest rates- 10 year maturity (www.ECB.org).

Beugelsdijk, Brakman, Garretsen, and van Marrewijk International Economics and Business© Cambridge University Press, 2013 Chapter 9 – Currency crises and exchange rate policyTable 9.3 The incidence of global contagion, 1970–1998

Probabilities (%)

Other countries with crises (share, %) Unconditional (A) Conditional (B)

Difference: (B) – (A)

0–25 29.0 20.0 −9.0

25–50 29.0 33.0 4.0

50 and above 29.0 54.7 25.7 Source: Kaminsky and Reinhart (2000).

Expectations and contagion

Market efficiency The first- and second-generation models make a strong

assumption about market efficiency. They assume that currency crises never catch investors by surprise and investor expectations about the incompatibility between the fixed exchange rate and the economic fundamentals turn out to be correct. Thus, currency crises can be of entirely self-fulfilling nature (based on any information).

Empirical evidence shows that self-fulfilling crises, although they can still occur, are not the rule.

Exchange rate and policy trilemma

Three policy objectives:

1. Fixed exchange rate

2. Monetary policy independence

3. Capital mobility

Problem: Only two of these objectives can be achieved at any one point in time!

(Fig. 9.6)

Figure 9.6 The policy trilemma

fixed exchange rate

fixed exchange rate

fixed exchange rate

capital mobility

capital mobility

capital mobility

policy independence

policy independence

policy independence

fixed exchange rate

fixed exchange rate

fixed exchange rate

capital mobility

capital mobility

capital mobility

policy independence

policy independence

policy independence

Beugelsdijk, Brakman, Garretsen, and van Marrewijk International Economics and Business© Cambridge University Press, 2013 Chapter 9 – Currency crises and exchange rate policyTable 9.4 Looking for the trilemma: estimates of β

Policy regime All observations Fixed exchange rate regimes only

Gold standard 0.42 (0.03)a 0.52 (0.04)

Bretton Woods −0.11 (0.14) −.05 (0.12)

Post-Bretton Woods 0.36 (0.05) 0.46 (0.04) Source: Obstfeld, Shambaugh and Taylor (2003). Notes: a Standard errors in brackets.