1111

Consumer and Market Insights: Ice Cream Market in Bulgaria

CS1925MF

April 2015

22214/05/2015 25/14/2015 25/14/2015 25/14/2015 2

This report brings together multiple data sources to provide a comprehensive overview of the Ice Cream sector in

Bulgaria as part of our global coverage of the sector. This report draws on market data, analyzing value and volume

data and category and channel distribution breakdown, also highlighting which categories are witnessing the biggest

growth. Brand and Private Label analysis is also provided. It also contains top line foodservice transaction figures

highlighting where the most opportunistic channels are for industry players in the country. Detailed packaging

analysis is also provided, analyzing category trends and also packaging material and type

Market data coverage – The overall market value and volume included in the report is split on the basis of on-trade

and off-trade volume and value.

Category coverage: This report provides information on three Ice Cream categories including Artisanal Ice

Cream, Impulse Ice Cream - Single Serve and Take-home and Bulk Ice Cream.

More extensive brand coverage: The report provides more extensive brand share coverage. Brand share data is

also validated by inputs from industry experts.

Distribution channel: The Distribution data included in the report covers 11 distribution channels including Cash &

Carries & Warehouse Clubs, “Dollar Stores”, Variety Stores & General Merchandise Retailers, Hypermarkets &

Supermarkets, Convenience Stores

Time period: The report provides overall market value and volume data, including category level data for the period

2009-2019. Distribution channel and brand share data is included for the year 2014.

Report scope

333

Table of Contents

• Country Context

• Market Overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

444

Growing GDP and lower inflation rates provides opportunities in Bulgaria's consumer goods market

The GDP growth rate of Bulgaria showed an upward

trend in 2014 after a huge decline during 2011-2013. It

reached BGN10,925.7 in 2014.

The population matrix of Bulgaria is skewed towards

Older Young Adults and Pre-Mid Lifers.

The consumer prices in Bulgaria grew at a CAGR of

0.6% during 2011-2014, reaching 109.4 basis points in

2014.

The population growth in Bulgaria declined during 2012-

2014. The total Population reached 7.2 million in 2014.

Increase in GDP per capita coupled with rising employment rates have led to a positive growth in consumer goods

market in Bulgaria.

GDP Per Capita Population

Consumer Price Index Age Profile

-4%

0%

4%

8%

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

2009 2010 2011 2012 2013 2014

GD

P P

er

Cap

ita (

BG

N)

Annual g

row

th (

%)

-0.8%

-0.6%

-0.4%

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014

Ann

ual G

row

th (

%)

Pop

ulat

ion

(Mill

ion)

100

104

108

112

2009 2010 2011 2012 2013 2014

Co

nsum

er P

rice

Ind

ex

0 - 9

10 - 19

20 - 29

30 - 39

40 - 49

50 - 59

60 - 69

70 - 79

80+

555

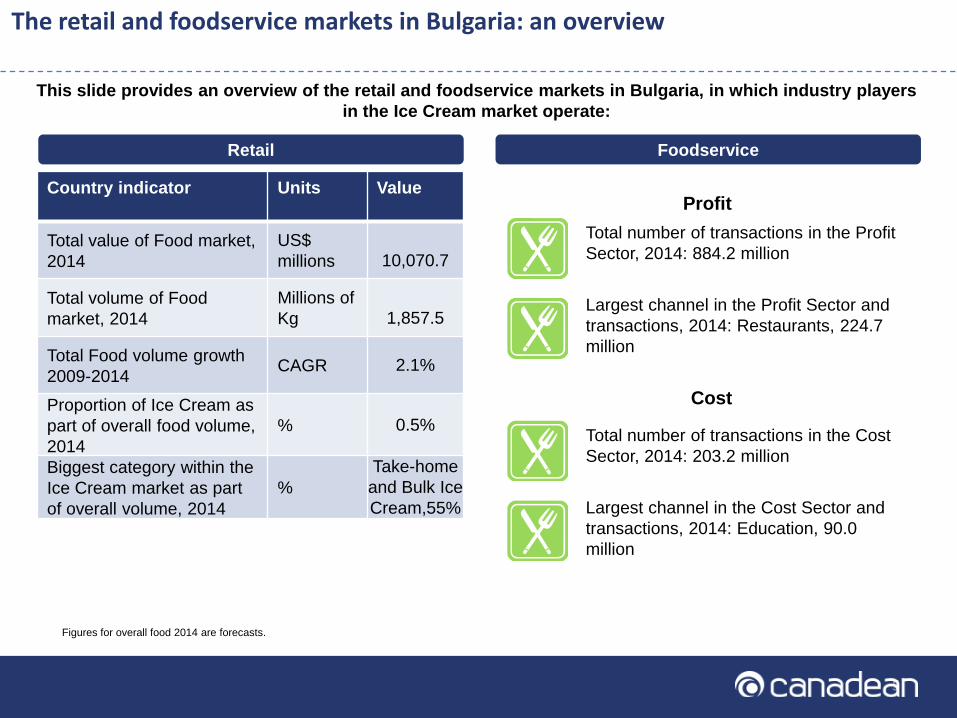

The retail and foodservice markets in Bulgaria: an overview

Foodservice

This slide provides an overview of the retail and foodservice markets in Bulgaria, in which industry players

in the Ice Cream market operate:

Profit

Total number of transactions in the Profit

Sector, 2014: 884.2 million

Largest channel in the Profit Sector and

transactions, 2014: Restaurants, 224.7

million

Cost

Total number of transactions in the Cost

Sector, 2014: 203.2 million

Largest channel in the Cost Sector and

transactions, 2014: Education, 90.0

million

Retail

Country indicator Units Value

Total value of Food market,

2014

US$

millions 10,070.7

Total volume of Food

market, 2014

Millions of

Kg 1,857.5

Total Food volume growth

2009-2014CAGR 2.1%

Proportion of Ice Cream as

part of overall food volume,

2014

% 0.5%

Biggest category within the

Ice Cream market as part

of overall volume, 2014

%

Take-home

and Bulk Ice

Cream,55%

Figures for overall food 2014 are forecasts.

666

Table of Contents

• Country Context

• Market Overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

777

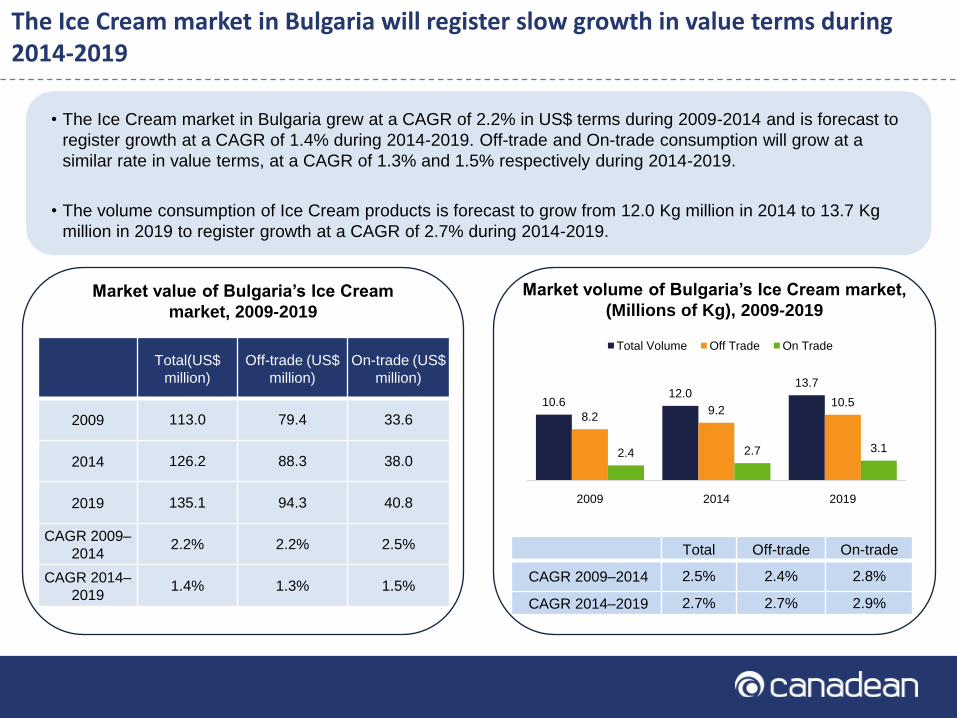

The Ice Cream market in Bulgaria will register slow growth in value terms during 2014-2019

Market value of Bulgaria’s Ice Cream

market, 2009-2019

Market volume of Bulgaria’s Ice Cream market,

(Millions of Kg), 2009-2019

Total Off-trade On-trade

CAGR 2009–2014 2.5% 2.4% 2.8%

CAGR 2014–2019 2.7% 2.7% 2.9%

• The Ice Cream market in Bulgaria grew at a CAGR of 2.2% in US$ terms during 2009-2014 and is forecast to

register growth at a CAGR of 1.4% during 2014-2019. Off-trade and On-trade consumption will grow at a

similar rate in value terms, at a CAGR of 1.3% and 1.5% respectively during 2014-2019.

• The volume consumption of Ice Cream products is forecast to grow from 12.0 Kg million in 2014 to 13.7 Kg

million in 2019 to register growth at a CAGR of 2.7% during 2014-2019.

Total(US$

million)

Off-trade (US$

million)

On-trade (US$

million)

2009 113.0 79.4 33.6

2014 126.2 88.3 38.0

2019 135.1 94.3 40.8

CAGR 2009–

20142.2% 2.2% 2.5%

CAGR 2014–

20191.4% 1.3% 1.5%

10.612.0

13.7

8.29.2

10.5

2.4 2.7 3.1

2009 2014 2019

Total Volume Off Trade On Trade

888

On-trade sales will grow at a faster rate than off-trade sales in Bulgaria’s Ice Cream market

The Ice Cream market in Bulgaria grew at a steady rate during 2009-2019 both in local currency terms and volume

terms. It was worth BGN186.1 million (US$126.2 million) in 2014, and is forecast to register a CAGR of 3.4% in local

currency terms during 2014-2019 to reach BGN219.7 million (US$135.1 million) in 2019. In US$ terms the Ice

Cream market in Bulgaria was impacted due to the fluctuating exchange rates and the growth rate in value terms

declined from a CAGR of 2.2% registered during 2009-2014 to a CAGR of 1.4% during 2014-2019.

On-trade transactions accounted for 30.0% of the Ice Cream market in local currency terms and 22.8% of volume

sales in 2014.

Market value (BGN m and US$ m) and volume growth of

Bulgaria’s Ice Cream market, 2009–2019

Off-trade On-trade

Value

growth

Volume

growth

Value

growth

Volume

growth

2014 3.2% 2.5% 3.4% 2.9%

2015 3.2% 2.5% 3.4% 2.9%

2016 3.3% 2.6% 3.4% 2.9%

2017 3.3% 2.7% 3.5% 2.9%

2018 3.4% 2.7% 3.5% 2.9%

2019 3.4% 2.8% 3.5% 2.9%

Market value (BGN$ m) and volume growth of

Bulgaria’s Ice Cream market, 2014–2019 –

Off-trade/on-trade

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Gro

wth

Rate

(%

)

Value (BGN m) Value (US$ m) Volume Kg m

999

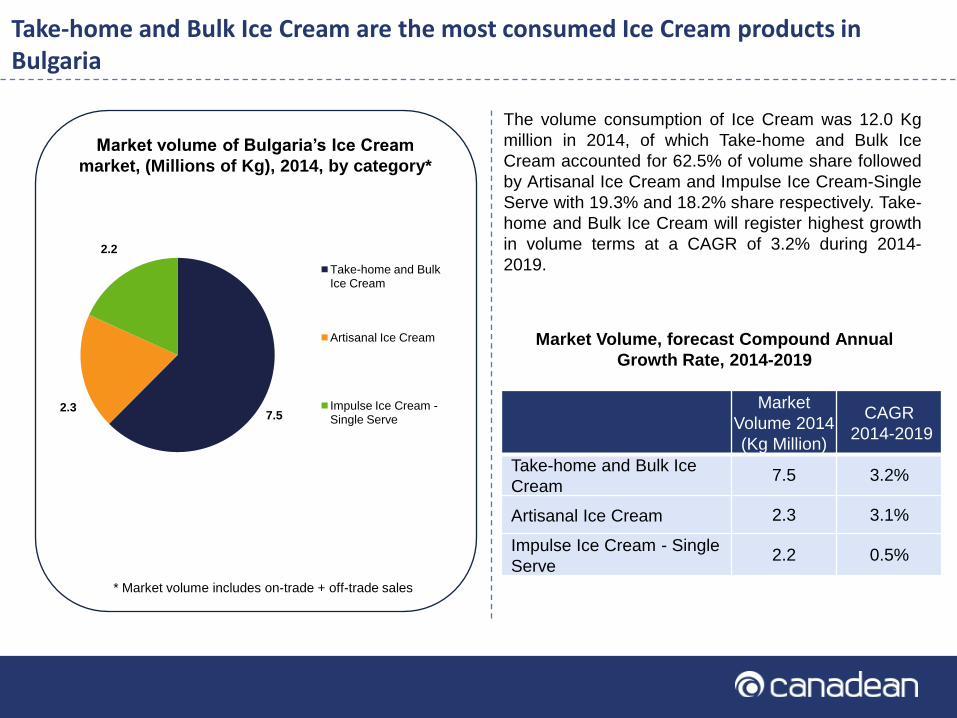

Take-home and Bulk Ice Cream are the most consumed Ice Cream products in Bulgaria

Market volume of Bulgaria’s Ice Cream

market, (Millions of Kg), 2014, by category*

The volume consumption of Ice Cream was 12.0 Kg

million in 2014, of which Take-home and Bulk Ice

Cream accounted for 62.5% of volume share followed

by Artisanal Ice Cream and Impulse Ice Cream-Single

Serve with 19.3% and 18.2% share respectively. Take-

home and Bulk Ice Cream will register highest growth

in volume terms at a CAGR of 3.2% during 2014-

2019.

Market Volume, forecast Compound Annual

Growth Rate, 2014-2019

Market

Volume 2014

(Kg Million)

CAGR

2014-2019

Take-home and Bulk Ice

Cream7.5 3.2%

Artisanal Ice Cream 2.3 3.1%

Impulse Ice Cream - Single

Serve2.2 0.5%

* Market volume includes on-trade + off-trade sales

7.52.3

2.2

Take-home and Bulk Ice Cream

Artisanal Ice Cream

Impulse Ice Cream -Single Serve

101010

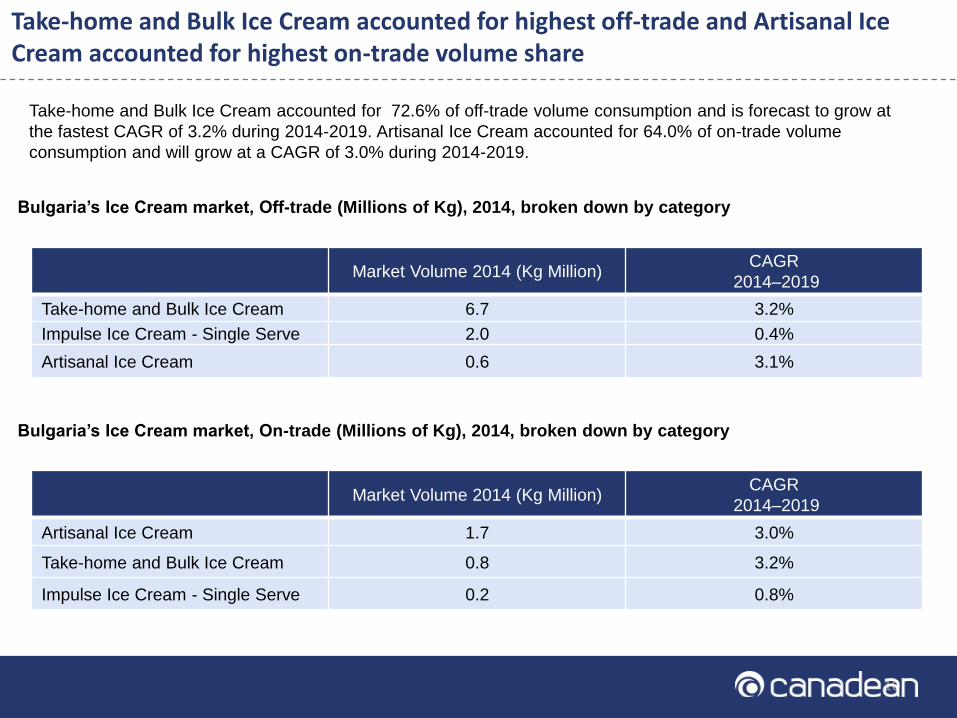

Take-home and Bulk Ice Cream accounted for highest off-trade and Artisanal Ice Cream accounted for highest on-trade volume share

Bulgaria’s Ice Cream market, Off-trade (Millions of Kg), 2014, broken down by category

Take-home and Bulk Ice Cream accounted for 72.6% of off-trade volume consumption and is forecast to grow at

the fastest CAGR of 3.2% during 2014-2019. Artisanal Ice Cream accounted for 64.0% of on-trade volume

consumption and will grow at a CAGR of 3.0% during 2014-2019.

Market Volume 2014 (Kg Million)CAGR

2014–2019

Take-home and Bulk Ice Cream 6.7 3.2%

Impulse Ice Cream - Single Serve 2.0 0.4%

Artisanal Ice Cream 0.6 3.1%

Bulgaria’s Ice Cream market, On-trade (Millions of Kg), 2014, broken down by category

Market Volume 2014 (Kg Million)CAGR

2014–2019

Artisanal Ice Cream 1.7 3.0%

Take-home and Bulk Ice Cream 0.8 3.2%

Impulse Ice Cream - Single Serve 0.2 0.8%

111111

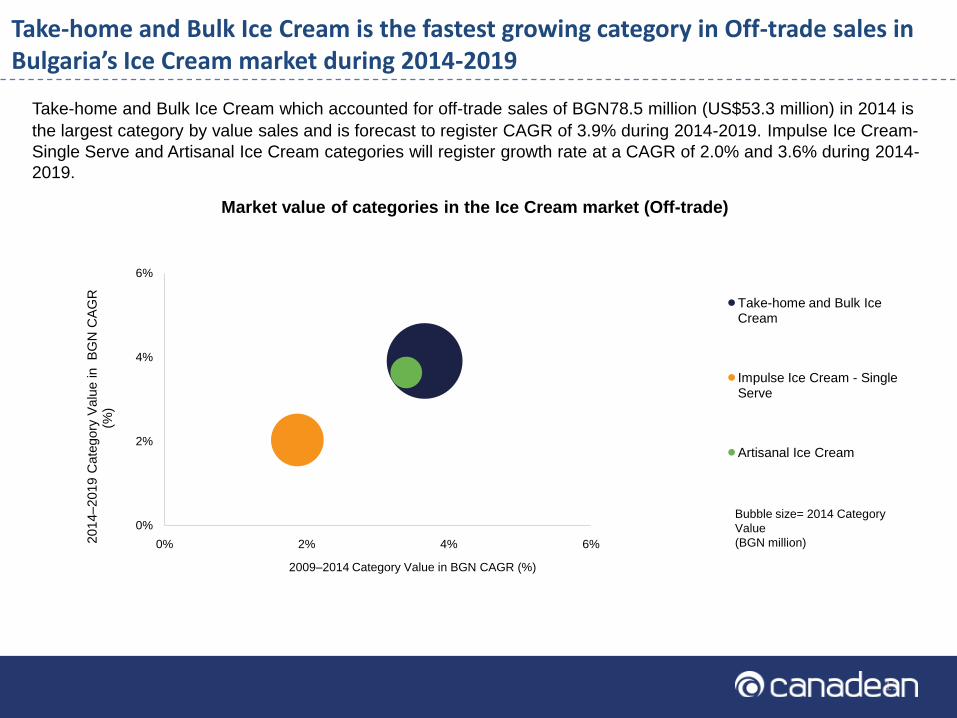

Take-home and Bulk Ice Cream is the fastest growing category in Off-trade sales in Bulgaria’s Ice Cream market during 2014-2019

Market value of categories in the Ice Cream market (Off-trade)

Take-home and Bulk Ice Cream which accounted for off-trade sales of BGN78.5 million (US$53.3 million) in 2014 is

the largest category by value sales and is forecast to register CAGR of 3.9% during 2014-2019. Impulse Ice Cream-

Single Serve and Artisanal Ice Cream categories will register growth rate at a CAGR of 2.0% and 3.6% during 2014-

2019.

0%

2%

4%

6%

0% 2% 4% 6%2014–2019 C

ate

gory

Valu

e in

BG

N C

AG

R

(%)

2009–2014 Category Value in BGN CAGR (%)

Take-home and Bulk Ice Cream

Impulse Ice Cream - Single Serve

Artisanal Ice Cream

Bubble size= 2014 Category

Value

(BGN million)

121212

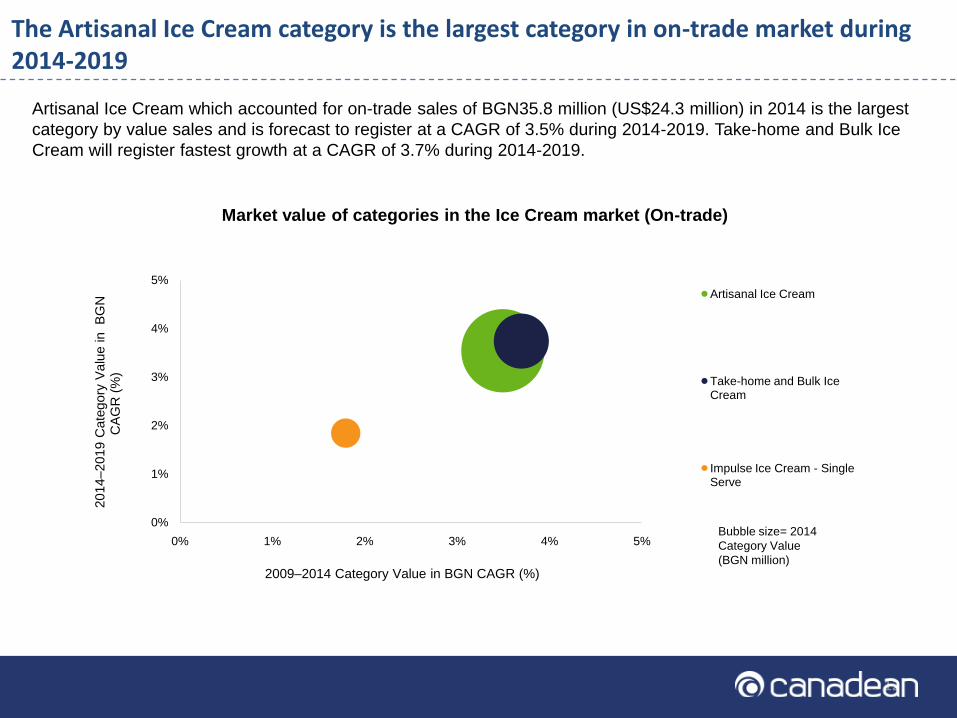

The Artisanal Ice Cream category is the largest category in on-trade market during 2014-2019

Artisanal Ice Cream which accounted for on-trade sales of BGN35.8 million (US$24.3 million) in 2014 is the largest

category by value sales and is forecast to register at a CAGR of 3.5% during 2014-2019. Take-home and Bulk Ice

Cream will register fastest growth at a CAGR of 3.7% during 2014-2019.

Market value of categories in the Ice Cream market (On-trade)

0%

1%

2%

3%

4%

5%

0% 1% 2% 3% 4% 5%

2014–2019 C

ate

gory

Valu

e in

BG

N

CA

GR

(%

)

2009–2014 Category Value in BGN CAGR (%)

Artisanal Ice Cream

Take-home and Bulk Ice Cream

Impulse Ice Cream - Single Serve

Bubble size= 2014

Category Value

(BGN million)

131313

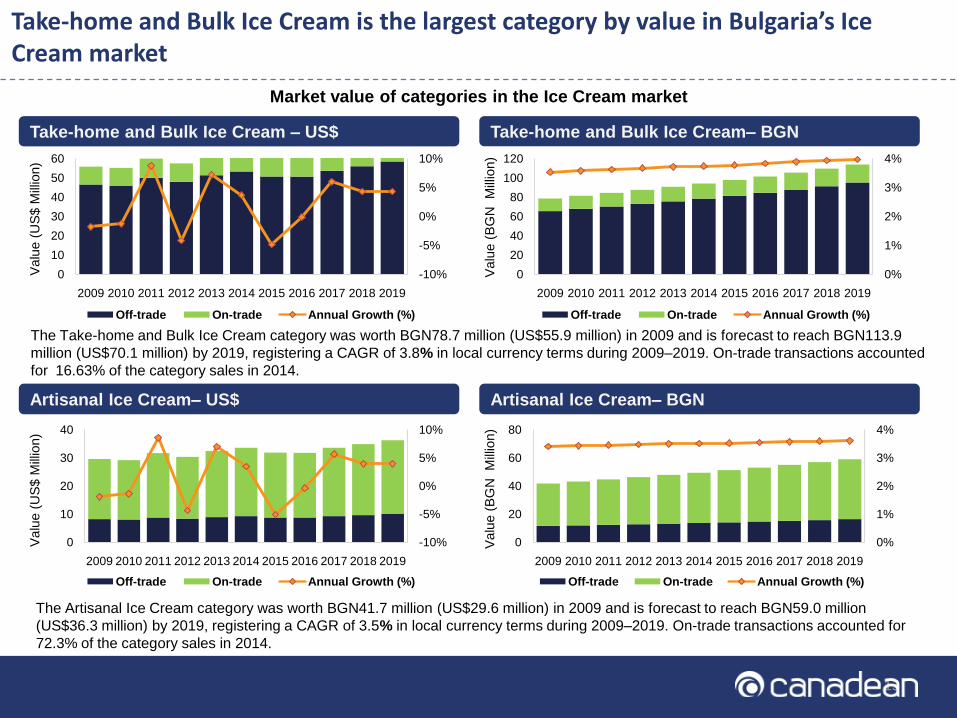

Take-home and Bulk Ice Cream is the largest category by value in Bulgaria’s Ice Cream market

The Take-home and Bulk Ice Cream category was worth BGN78.7 million (US$55.9 million) in 2009 and is forecast to reach BGN113.9

million (US$70.1 million) by 2019, registering a CAGR of 3.8% in local currency terms during 2009–2019. On-trade transactions accounted

for 16.63% of the category sales in 2014.

Take-home and Bulk Ice Cream – US$ Take-home and Bulk Ice Cream– BGN

Market value of categories in the Ice Cream market

Artisanal Ice Cream– US$ Artisanal Ice Cream– BGN

The Artisanal Ice Cream category was worth BGN41.7 million (US$29.6 million) in 2009 and is forecast to reach BGN59.0 million

(US$36.3 million) by 2019, registering a CAGR of 3.5% in local currency terms during 2009–2019. On-trade transactions accounted for

72.3% of the category sales in 2014.

-10%

-5%

0%

5%

10%

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e (

US

$ M

illio

n)

Off-trade On-trade Annual Growth (%)

0%

1%

2%

3%

4%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e (

BG

N

Mill

ion)

Off-trade On-trade Annual Growth (%)

-10%

-5%

0%

5%

10%

0

10

20

30

40

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e (

US

$ M

illio

n)

Off-trade On-trade Annual Growth (%)

0%

1%

2%

3%

4%

0

20

40

60

80

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e (

BG

N

Mill

ion)

Off-trade On-trade Annual Growth (%)

141414

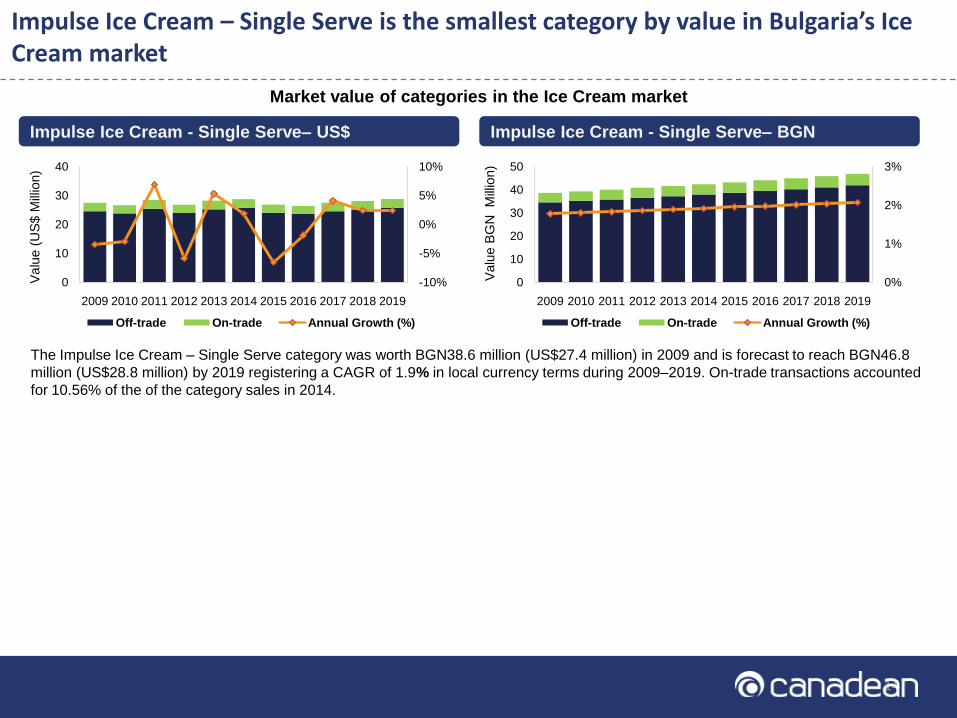

Impulse Ice Cream – Single Serve is the smallest category by value in Bulgaria’s Ice Cream market

The Impulse Ice Cream – Single Serve category was worth BGN38.6 million (US$27.4 million) in 2009 and is forecast to reach BGN46.8

million (US$28.8 million) by 2019 registering a CAGR of 1.9% in local currency terms during 2009–2019. On-trade transactions accounted

for 10.56% of the of the category sales in 2014.

Impulse Ice Cream - Single Serve– US$ Impulse Ice Cream - Single Serve– BGN

Market value of categories in the Ice Cream market

-10%

-5%

0%

5%

10%

0

10

20

30

40

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e (

US

$ M

illio

n)

Off-trade On-trade Annual Growth (%)

0%

1%

2%

3%

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e B

GN

M

illio

n)

Off-trade On-trade Annual Growth (%)

151515

The Take-home and Bulk Ice Cream category will gain maximum market share in value terms during 2014-2019

Winners Losers

Take-home and Bulk Ice

Cream

The Take-home and Bulk Ice Cream category is

forecast to gain market share, growing from 50.6% in

2014 to 51.8% in 2019.

1 1

Change in market

share, 2014–2019Category

Change in market

share, 2014–2019Category

Impulse Ice Cream - Single

Serve

The Impulse Ice Cream - Single Serve category is

forecast to lose market share, declining from 22.8% in

2014 to 21.3% in 2019.

1.2%

Change in market share (in value terms) in the Ice Cream market*

-1.5%

* Change in market share based on on-trade + off-trade values

0.2%Artisanal Ice Cream

The Artisanal Ice Cream category is forecast to gain

market share, growing from 26.6% in 2014 to 26.8% in

2019.

2 0.2%

16161614/05/2015 165/14/2015 165/14/2015 165/14/2015 16

Category level pricing

Average category level prices (BGN) in Bulgaria’s Ice Cream market, 2014

Category Average Price/ Kg (BGN)

2014

Average Price/Kg (USD)

2014

Take-home and Bulk Ice Cream 12.6 8.5

Artisanal Ice Cream 21.4 14.5

Impulse Ice Cream - Single Serve 19.4 13.2

17171714/05/2015 175/14/2015 175/14/2015 175/14/2015 17

Dairy-Based Ice Cream is the largest segment in all the Ice Cream categories

Segment’s share of the overall category by value and change in market share in Bulgaria’s Ice Cream

Market, 2014

Category Off-trade / On-trade Segment Segment‟s Share,

2014Change 2014/2019

Take-home and

Bulk Ice Cream

Off-trade Dairy-Based 74.4% 0.2%

Off-trade On-Trade 16.6% -0.1%

On-trade Water-Based 8.9% -0.1%

Artisanal Ice

Cream

On-trade On-Trade 72.3% -0.1%

Off-trade Artisanal Ice Cream 27.7% 0.1%

Impulse Ice Cream

- Single Serve

Off-trade Dairy-Based 83.6% 0.2%

On-trade On-Trade 10.6% -0.1%

Off-trade Water-Based 5.9% -0.1%

181818

Table of Contents

• Country Context

• Market overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

191919

Profiles of Selected Grocery Retailers

Leading retailers in Bulgaria’s Food market, 2014

Leading retailers, Bulgaria

Company Name Overview

CBA CBA is one of the leading Hungary based Supermarket chain, that

operates with 86 stores across Bulgaria.

BillaBilla, a German-based Rewe Group Supermarket chain, is a leading

retailer with 84 stores operating in Bulgaria.

LidlLidl is a German global discount supermarket chain. It operates 64 stores

across Bulgaria.

Kaufland Kaufland, a German hypermarket chain, operates 48 stores in the country.

T-MarketMaxima Group is a Lithuanian food retail chain that runs 42 stores under

the „T-Market „ brand in the country.

Leading retailers, Bulgaria

Company Name Overview

CBA CBA is one of the leading Hungary based Supermarket chain, that

operates with 86 stores across Bulgaria.

BillaBilla, a German-based Rewe Group Supermarket chain, is a leading

retailer with 84 stores operating in Bulgaria.

LidlLidl is a German global discount supermarket chain. It operates 64 stores

across Bulgaria.

Kaufland Kaufland, a German hypermarket chain, operates 48 stores in the country.

T-MarketMaxima Group is a Lithuanian food retail chain that runs 42 stores under

the „T-Market „ brand in the country.

202020

Leading distribution channels –Overall Food

Ice Cream market as a percentage of overall

Food: Ice Cream accounted for 1.4% of food retail

sales in Bulgaria in 2013.

Convenience Stores are the leading retailers of food

in Bulgaria. They accounted for 40.7% of food retail

sales in the country, followed by Hypermarkets &

Supermarkets with a 34.5% share. Hypermarkets &

Supermarkets registered the highest growth at a

CAGR of 4.3% in local currency terms during 2010-

2013.

Hypermarkets & Supermarkets is the leading distribution channel in Bulgaria’s Ice Cream market in 2014

Leading distribution channels in Bulgaria’s Ice Cream market, 2014

Leading distribution channels – Ice Cream

Hypermarkets & Supermarkets accounted for 34.5%

of the distribution share in Bulgaria‟s Ice Cream

market in 2014. On-trade accounted for 30.1% of the

market share. Food & Drinks specialists accounted for

20.4% and 14.4% of the market share respectively.

Hypermarkets & Supermarkets registered the highest

growth at a CAGR of 3.6% in local currency terms

during 2011-2014.

35%

30%

20%

14%

1%Hypermarkets & Supermarkets

On-trade

Food & Drinks Specialists

Convenience Stores

Others

0

2

4

6

Convenience Stores

Hypermarkets & Supermarkets

Food & Drinks Specialists

Others

Va

lue

(U

S$ b

illio

n)

2010

2013

212121

On-trade transactions account for majority sales in the Artisanal Ice Cream category

Key distribution channels – Take-home and Bulk

Ice Cream

Key distribution channels – Impulse Ice Cream -

Single Serve

Key distribution channels – Artisanal Ice Cream

Leading distribution channels by category in the Ice Cream market, 2014

51%

17%

17%

14% 1% Hypermarkets & Supermarkets

Food & Drinks Specialists

On-trade

Convenience Stores

Others

72%

28%

On-trade

Food & Drinks Specialists

37%

31%

20%

11% 1% Hypermarkets & Supermarkets

Convenience Stores

Food & Drinks Specialists

On-trade

Others

222222

Table of Contents

• Country Context

• Market Overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

232323

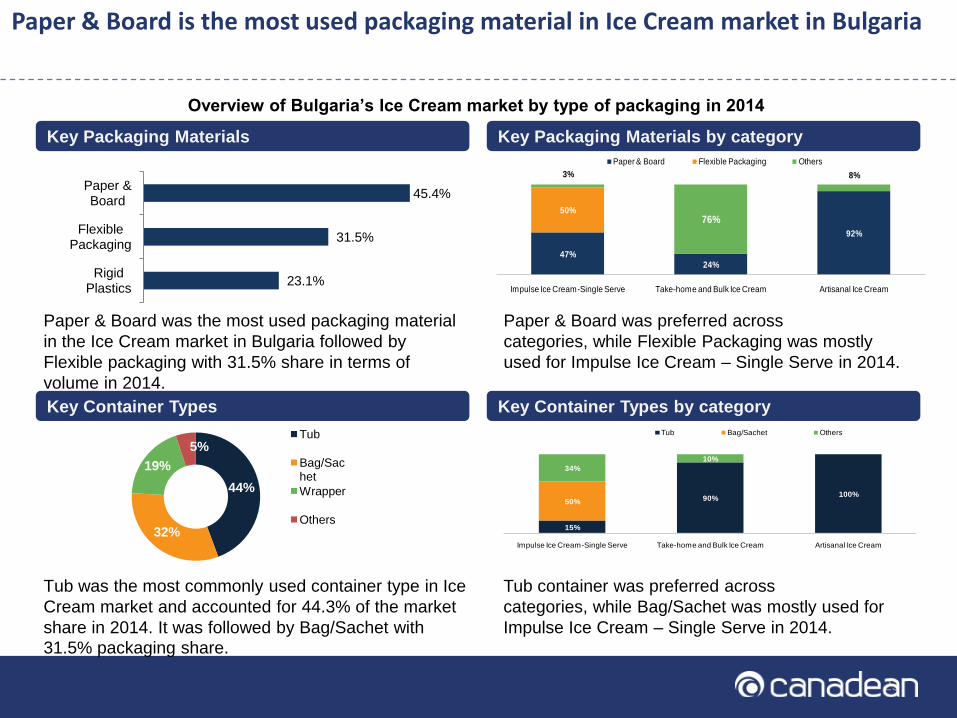

Paper & Board is the most used packaging material in Ice Cream market in Bulgaria

Tub was the most commonly used container type in Ice

Cream market and accounted for 44.3% of the market

share in 2014. It was followed by Bag/Sachet with

31.5% packaging share.

Paper & Board was preferred across

categories, while Flexible Packaging was mostly

used for Impulse Ice Cream – Single Serve in 2014.

Tub container was preferred across

categories, while Bag/Sachet was mostly used for

Impulse Ice Cream – Single Serve in 2014.

Key Packaging Materials Key Packaging Materials by category

Key Container Types Key Container Types by category

Overview of Bulgaria’s Ice Cream market by type of packaging in 2014

Paper & Board was the most used packaging material

in the Ice Cream market in Bulgaria followed by

Flexible packaging with 31.5% share in terms of

volume in 2014.

45.4%

31.5%

23.1%

Paper & Board

Flexible Packaging

Rigid Plastics

44%

32%

19%

5%Tub

Bag/Sachet

Wrapper

Others15%

90%100%

50%

34%

10%

Impulse Ice Cream-Single Serve Take-home and Bulk Ice Cream Artisanal Ice Cream

Tub Bag/Sachet Others

47%24%

92%

50%

3%

76%

8%

Impulse Ice Cream-Single Serve Take-home and Bulk Ice Cream Artisanal Ice Cream

Paper & Board Flexible Packaging Others

242424

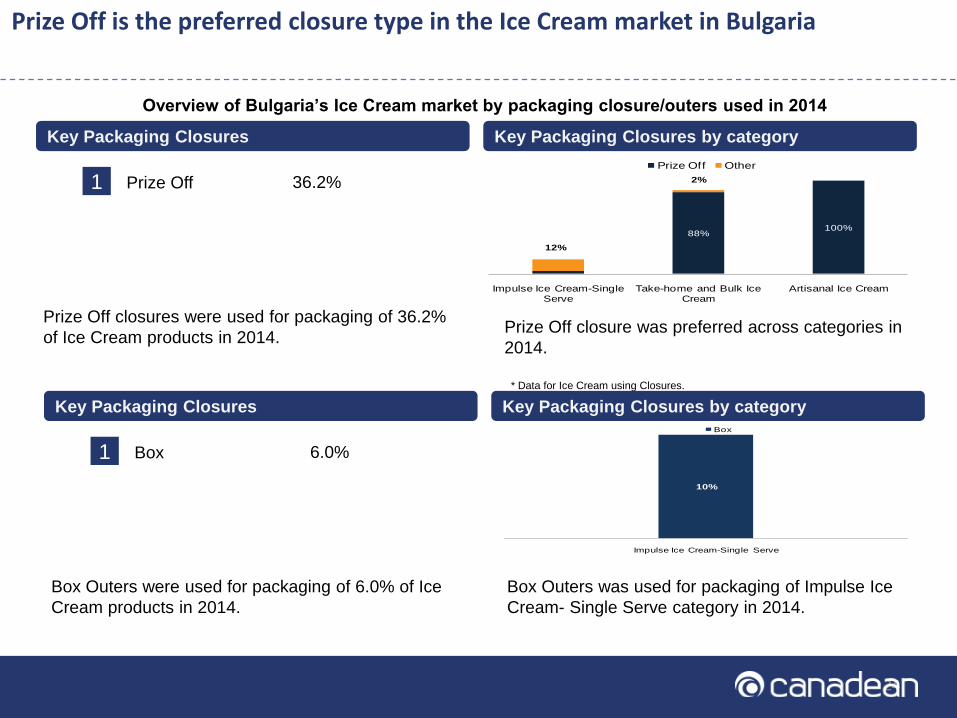

Prize Off is the preferred closure type in the Ice Cream market in Bulgaria

Prize Off closure was preferred across categories in

2014.

Key Packaging Closures Key Packaging Closures by category

Overview of Bulgaria’s Ice Cream market by packaging closure/outers used in 2014

Prize Off closures were used for packaging of 36.2%

of Ice Cream products in 2014.

36.2%1 Prize Off

* Data for Ice Cream using Closures.

Box Outers was used for packaging of Impulse Ice

Cream- Single Serve category in 2014.

Key Packaging Closures Key Packaging Closures by category

Box Outers were used for packaging of 6.0% of Ice

Cream products in 2014.

6.0%1 Box

10%

Impulse Ice Cream-Single Serve

Box

3%

88%100%

12%

2%

Impulse Ice Cream-Single Serve

Take-home and Bulk Ice Cream

Artisanal Ice Cream

Prize Off Other

252525

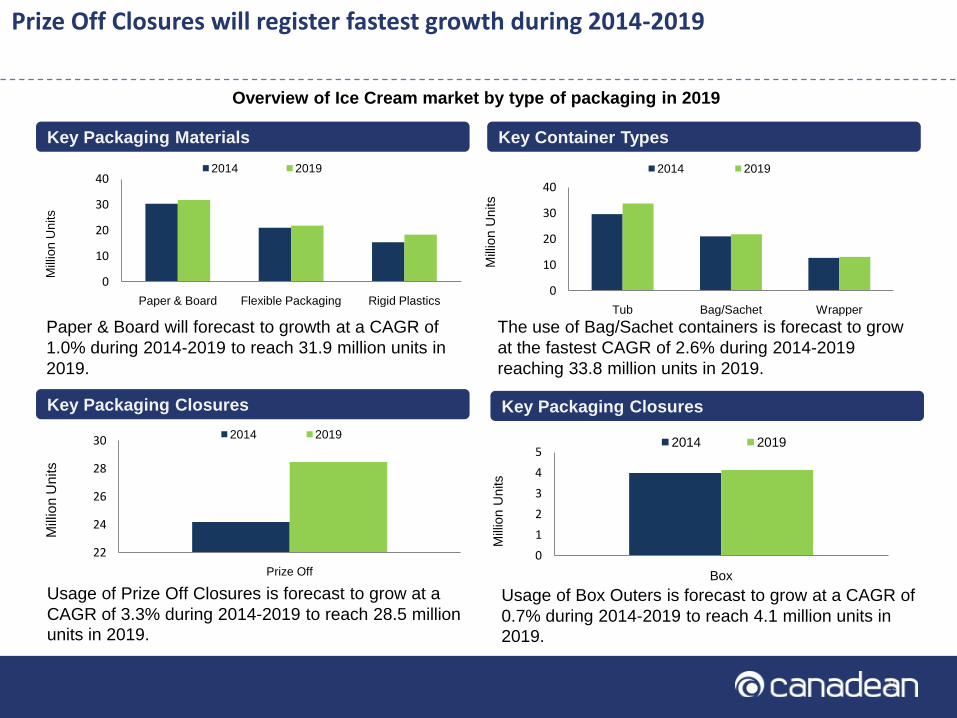

Prize Off Closures will register fastest growth during 2014-2019

Usage of Prize Off Closures is forecast to grow at a

CAGR of 3.3% during 2014-2019 to reach 28.5 million

units in 2019.

The use of Bag/Sachet containers is forecast to grow

at the fastest CAGR of 2.6% during 2014-2019

reaching 33.8 million units in 2019.

Key Packaging Materials Key Container Types

Key Packaging Closures

Paper & Board will forecast to growth at a CAGR of

1.0% during 2014-2019 to reach 31.9 million units in

2019.

Overview of Ice Cream market by type of packaging in 2019

Usage of Box Outers is forecast to grow at a CAGR of

0.7% during 2014-2019 to reach 4.1 million units in

2019.

Key Packaging Closures

0

10

20

30

40

Paper & Board Flexible Packaging Rigid Plastics

Mill

ion U

nits

2014 2019

0

10

20

30

40

Tub Bag/Sachet Wrapper

Mill

ion U

nits

2014 2019

22

24

26

28

30

Prize Off

Mill

ion U

nits

2014 2019

0

1

2

3

4

5

Box

Mill

ion U

nits

2014 2019

262626

Table of Contents

• Country Context

• Market Overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

272727

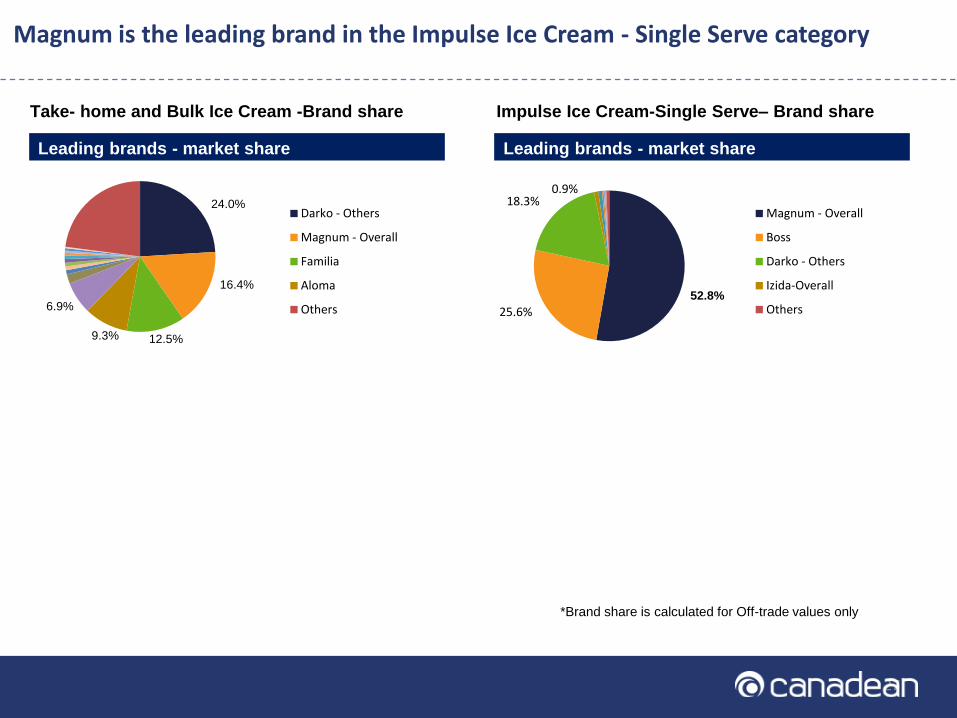

Take- home and Bulk Ice Cream -Brand share

Leading brands - market share

Magnum is the leading brand in the Impulse Ice Cream - Single Serve category

Impulse Ice Cream-Single Serve– Brand share

Leading brands - market share

*Brand share is calculated for Off-trade values only

52.8%

25.6%

18.3%0.9%

Magnum - Overall

Boss

Darko - Others

Izida-Overall

Others

24.0%

16.4%

12.5%9.3%

6.9%

Darko - Others

Magnum - Overall

Familia

Aloma

Others

282828

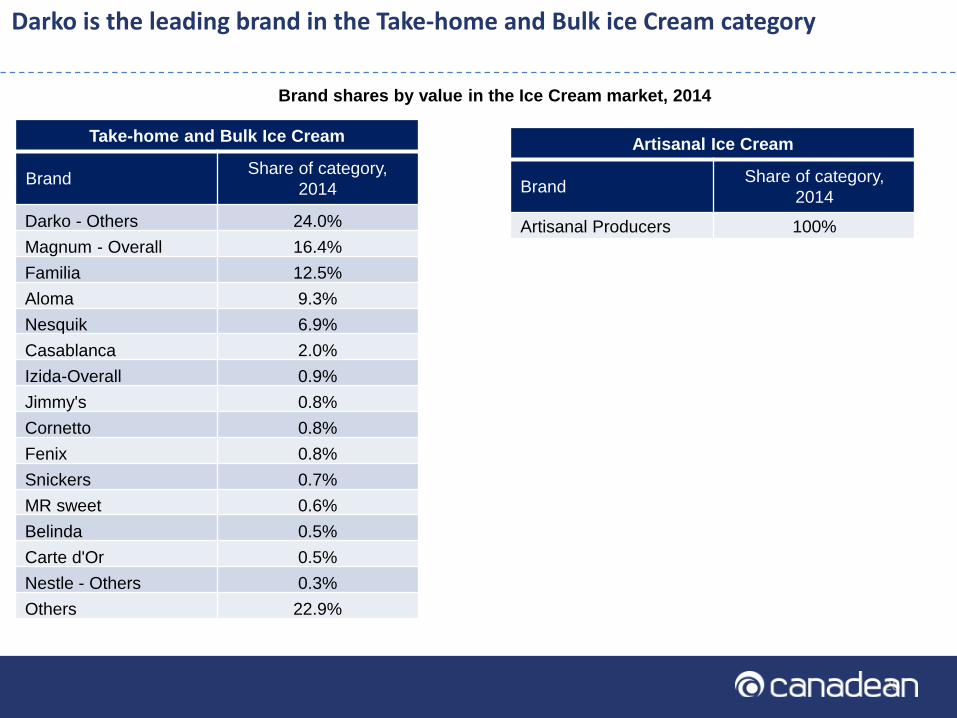

Darko is the leading brand in the Take-home and Bulk ice Cream category

Brand shares by value in the Ice Cream market, 2014

Take-home and Bulk Ice Cream

BrandShare of category,

2014

Darko - Others 24.0%

Magnum - Overall 16.4%

Familia 12.5%

Aloma 9.3%

Nesquik 6.9%

Casablanca 2.0%

Izida-Overall 0.9%

Jimmy's 0.8%

Cornetto 0.8%

Fenix 0.8%

Snickers 0.7%

MR sweet 0.6%

Belinda 0.5%

Carte d'Or 0.5%

Nestle - Others 0.3%

Others 22.9%

Artisanal Ice Cream

BrandShare of category,

2014

Artisanal Producers 100%

292929

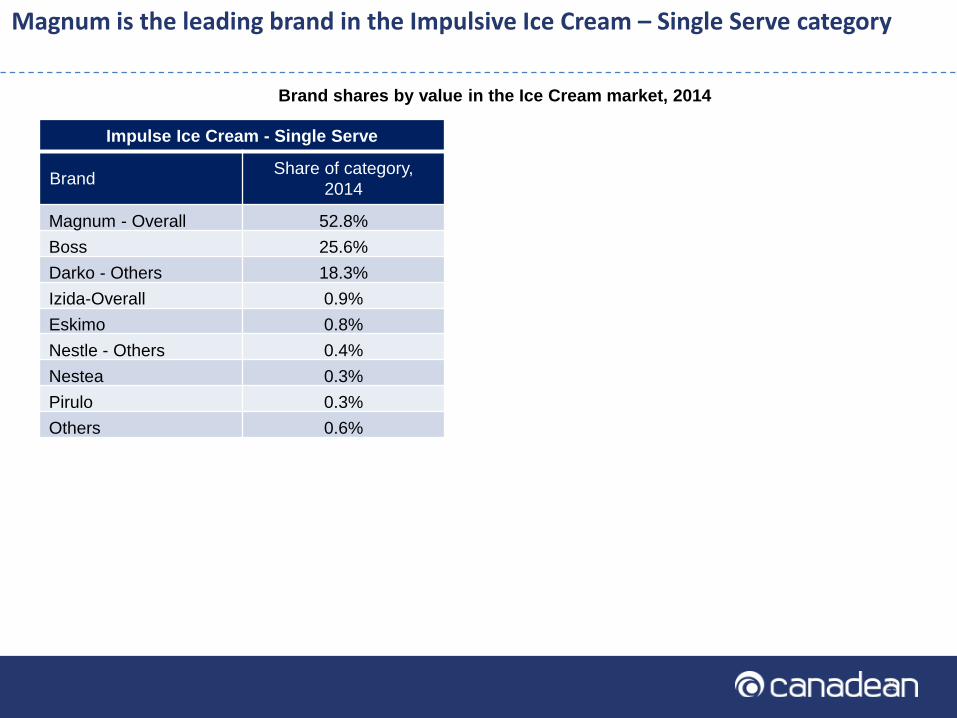

Magnum is the leading brand in the Impulsive Ice Cream – Single Serve category

Brand shares by value in the Ice Cream market, 2014

Impulse Ice Cream - Single Serve

BrandShare of category,

2014

Magnum - Overall 52.8%

Boss 25.6%

Darko - Others 18.3%

Izida-Overall 0.9%

Eskimo 0.8%

Nestle - Others 0.4%

Nestea 0.3%

Pirulo 0.3%

Others 0.6%

303030

Table of Contents

• Country Context

• Market Overview

• Retail Landscape and Key Distribution Channels

• Packaging

• Brand Share

• Appendix

313131

Appendix - Country Context

Year 2009 2010 2011 2012 2013 2014

Total (Millions) 7.4 7.4 7.3 7.3 7.3 7.2

Annual Growth (%) -0.6% -0.7% -0.6% -0.6% -0.6% -0.6%

Year 2009 2010 2011 2012 2013 2014

GDP Per Capita (BGN) 9,177.5 9,534.2 10,248.3 10,688.5 10,752.1 10,925.7

Year 2009 2010 2011 2012 2013 2014

Index 100 102 107 110 111 109

Age Group 0 to 9 10 to 19 20 to 29 30 to 39 40 to 49 50 to 59 60 to 69 70 to 79 80+

Total (Millions) 0.7 0.7 0.9 1.1 1.0 1.0 1.0 0.6 0.3

GDP Per Capita (BGN)

Population

Consumer Price Index

Age Profile (Millions of Persons)

Year 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

BGN-US$ Exchange

Rate (Annual Average)1.4 1.5 1.4 1.5 1.5 1.5 1.6 1.7 1.6 1.6 1.6

Exchange Rates: BGN-US$ , 2009–2019

323232

2010 2013

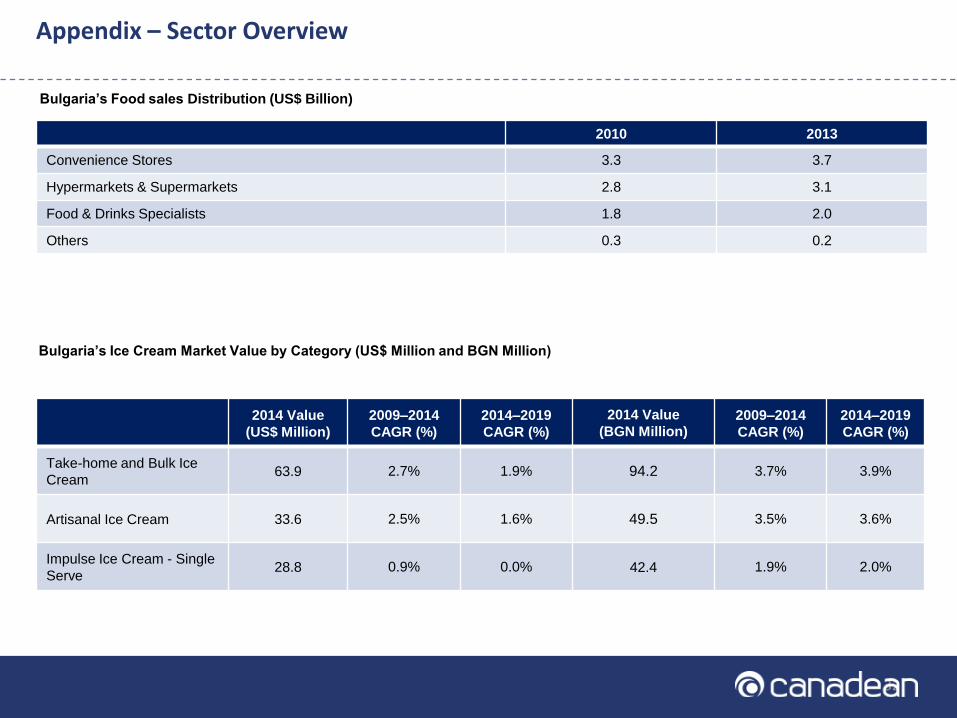

Convenience Stores 3.3 3.7

Hypermarkets & Supermarkets 2.8 3.1

Food & Drinks Specialists 1.8 2.0

Others 0.3 0.2

2014 Value

(US$ Million)

2009–2014

CAGR (%)

2014–2019

CAGR (%)

2014 Value

(BGN Million)2009–2014

CAGR (%)

2014–2019

CAGR (%)

Take-home and Bulk Ice

Cream63.9 2.7% 1.9% 94.2 3.7% 3.9%

Artisanal Ice Cream 33.6 2.5% 1.6% 49.5 3.5% 3.6%

Impulse Ice Cream - Single

Serve28.8 0.9% 0.0% 42.4 1.9% 2.0%

Bulgaria’s Food sales Distribution (US$ Billion)

Bulgaria’s Ice Cream Market Value by Category (US$ Million and BGN Million)

Appendix – Sector Overview

333333

Bulgaria’s Ice Cream sales (US$ Million and BGN Million) – Off-trade

Appendix – Sector Overview

Category2014 Value

(US$ Million)

2009–2014

CAGR (%)

2014–2019

CAGR (%)

2014 Value

BGN Million)

2009–2014

CAGR (%)

2014–2019

CAGR (%)

Take-home and Bulk Ice Cream 53.3 2.7% 1.9% 78.5 3.7% 3.9%

Impulse Ice Cream - Single

Serve25.7 0.9% 0.0% 37.9 1.9% 2.0%

Artisanal Ice Cream 9.3 2.5% 1.6% 13.7 3.4% 3.6%

Bulgaria’s Ice Cream sales (US$ Million and BGN Million) – On-trade

Category2014 Value

(US$ Million)

2009–2014

CAGR (%)

2014–2019

CAGR (%)

2014 Value

BGN Million)

2009–2014

CAGR (%)

2014–2019

CAGR (%)

Artisanal Ice Cream 24.3 2.6% 1.5% 35.8 3.5% 3.5%

Take-home and Bulk Ice Cream 10.6 2.8% 1.7% 4.5 3.7% 3.7%

Impulse Ice Cream - Single

Serve3.0 0.9% -0.1% 15.7 1.8% 1.8%

343434

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Value (US$ Million) 55.9 55.2 60.0 57.5 61.6 63.9 60.8 60.8 64.4 67.2 70.1

Growth (%) -1.8% -1.3% 8.8% -4.2% 7.2% 3.7% -4.8% -0.1% 6.0% 4.3% 4.3%

Value (BGN Million) 78.7 81.5 84.4 87.5 90.8 94.2 97.7 101.5 105.4 109.6 113.9

Growth (%) 3.5% 3.6% 3.6% 3.7% 3.7% 3.7% 3.8% 3.8% 3.9% 3.9% 4.0%

Take-home and Bulk Ice Cream Market Value

Impulse Ice Cream - Single Serve Market Value

Appendix – Category Data

Artisanal Ice Cream Market Value

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Value (US$ Million) 29.6 29.2 31.7 30.4 32.5 33.6 31.9 31.8 33.6 34.9 36.3

Growth (%) -1.9% -1.4% 8.6% -4.4% 6.9% 3.5% -5.1% -0.4% 5.7% 3.9% 4.0%

Value (BGN Million) 41.7 43.2 44.7 46.2 47.8 49.5 51.2 53.1 54.9 56.9 59.0

Growth (%) 3.4% 3.4% 3.4% 3.5% 3.5% 3.5% 3.5% 3.5% 3.6% 3.6% 3.6%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Value (US$ Million) 27.4 26.6 28.5 26.8 28.2 28.8 26.9 26.4 27.5 28.1 28.8

Growth (%) -3.5% -2.9% 6.9% -5.9% 5.3% 1.9% -6.5% -1.9% 4.1% 2.4% 2.4%

Value (BGN Million) 38.6 39.3 40.1 40.8 41.6 42.4 43.2 44.1 44.9 45.9 46.8

Growth (%) 1.8% 1.8% 1.8% 1.9% 1.9% 1.9% 2.0% 2.0% 2.0% 2.0% 2.1%

35353514/05/2015 355/14/2015 355/14/2015 355/14/2015 35

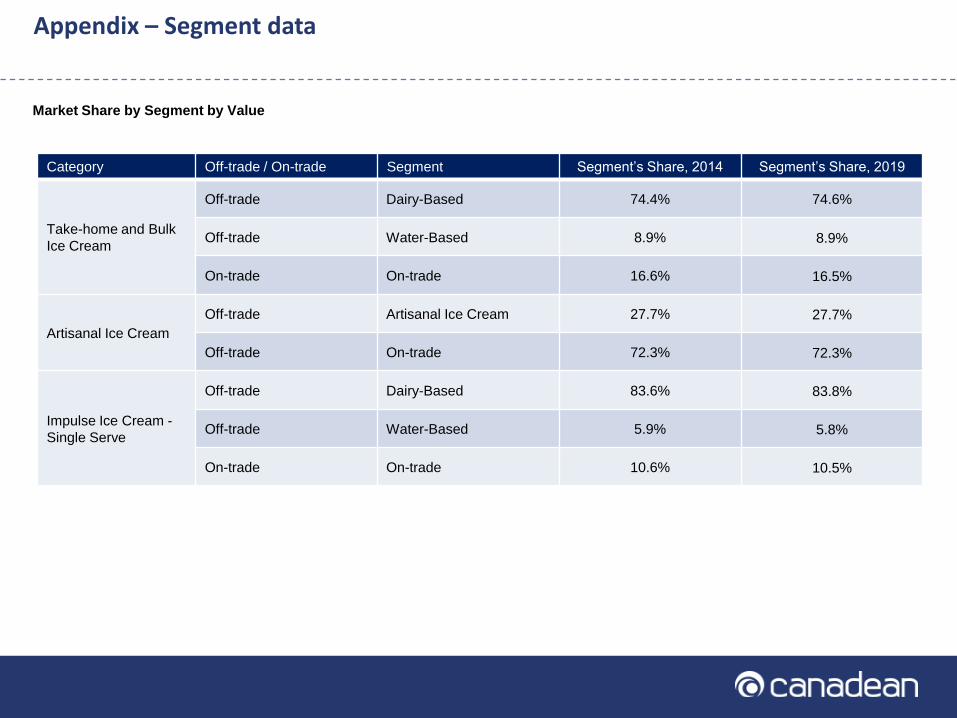

Appendix – Segment data

Category Off-trade / On-trade Segment Segment‟s Share, 2014 Segment‟s Share, 2019

Take-home and Bulk

Ice Cream

Off-trade Dairy-Based 74.4% 74.6%

Off-trade Water-Based 8.9% 8.9%

On-trade On-trade 16.6% 16.5%

Artisanal Ice Cream

Off-trade Artisanal Ice Cream 27.7% 27.7%

Off-trade On-trade 72.3% 72.3%

Impulse Ice Cream -

Single Serve

Off-trade Dairy-Based 83.6% 83.8%

Off-trade Water-Based 5.9% 5.8%

On-trade On-trade 10.6% 10.5%

Market Share by Segment by Value

363636

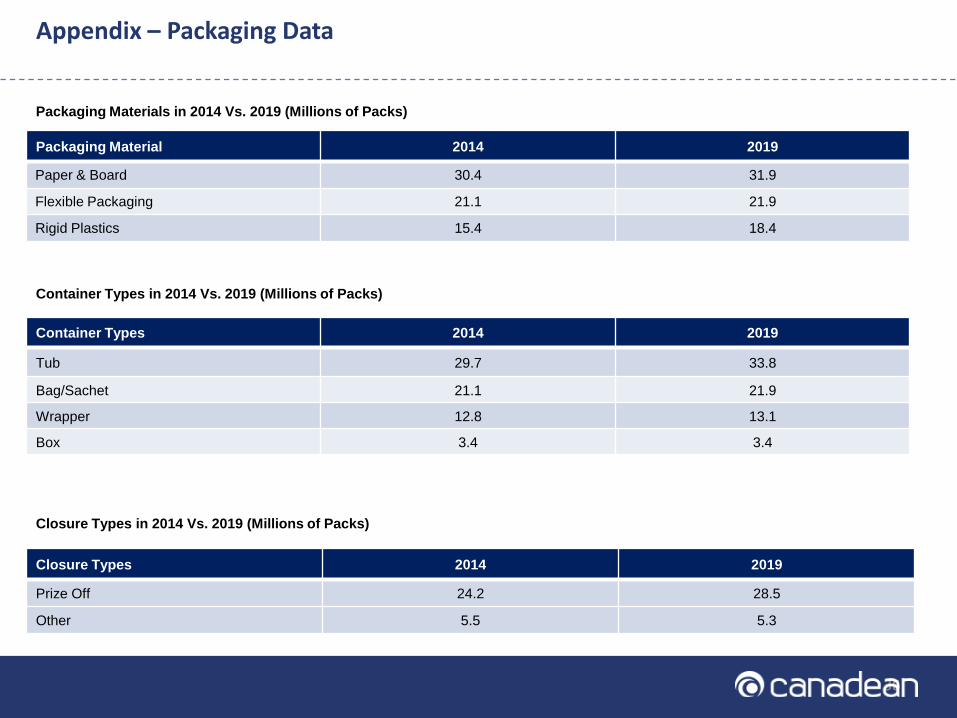

Packaging Material 2014 2019

Paper & Board 30.4 31.9

Flexible Packaging 21.1 21.9

Rigid Plastics 15.4 18.4

Packaging Materials in 2014 Vs. 2019 (Millions of Packs)

Appendix – Packaging Data

Container Types 2014 2019

Tub 29.7 33.8

Bag/Sachet 21.1 21.9

Wrapper 12.8 13.1

Box 3.4 3.4

Container Types in 2014 Vs. 2019 (Millions of Packs)

Closure Types 2014 2019

Prize Off 24.2 28.5

Other 5.5 5.3

Closure Types in 2014 Vs. 2019 (Millions of Packs)

373737

Category definitions

Category Definition

Artisanal Ice CreamArtisanal Ice cream manufactured (both dairy and water-based) by small local producers for sale on the

premises. Also includes branded gourmet ice cream and includes both on and off trade consumption.

Impulse Ice Cream - Single

Serve

Impulse Ice Cream - all dairy- and water-based ice creams. Includes single-serve ice cream tubs,

packaged cones (e.g. Cornetto), ice cream sandwiches, and chocolate-coated ice creams (e.g. Magnum).

Includes low fat dairy, oil-based products (other than frozen yogurt) and ice-lollies. Includes all on-trade

and off-trade consumption.

Take-home and Bulk Ice

Cream

Take-Home Ice Cream - includes all diary and water-based ice cream products sold for take-home and

bulk consumption. Includes multiple-serving ice cream tubs (e.g. Ben & Jerry's, Carte d'Or, Häagen-Dazs)

and, ice-cream cakes (e.g. Vienetta). Includes low-fat dairy- and oil-based products (other than frozen

yogurt). Also includes sorbets. Includes all on trade and off trade consumption.

383838

Category Definition

Artisanal Ice CreamArtisanal Ice

Cream

Artisanal Ice cream manufactured (both dairy and water-based) by small local producers for sale

on the premises. Also includes branded gourmet ice cream and includes both on and off trade

consumption.

Impulse Ice Cream -

Single Serve

Dairy-BasedDairy- or vegetable oil-based ice cream products purchased for immediate consumption. Includes

low fat dairy and oil-based products (other than frozen yogurt).

Water-BasedWater-based frozen desserts purchased for immediate consumption. Includes single serve

sorbet/sherbert tubs and ice lollies e.g. Calippo

Take-home and

Bulk Ice Cream

Dairy-Based

Dairy- or vegetable oil-based ice cream intended for consumption in the home, as opposed to an

impulse purchase for immediate consumption. Includes multiple-serving ice cream tubs and ice-

cream cakes. Includes low-fat dairy- and oil-based products (other than frozen yogurt).

Water-Based

Water-based frozen desserts intended for consumption in the home, as opposed to an impulse

purchase for immediate consumption. Includes multi-serve sorbet/sherbert tubs and ice lollies e.g.

Calippo

Segment definitions

393939

Channel Definition

Hypermarkets &

Supermarkets

Hypermarkets/mass merchandisers include all sales through retailers with floor area over 2,500 sq m that carry full

lines of both grocery and general merchandise (e.g. Wal-Mart). Supermarkets include all sales through retailers with

a floor area of 300 sq. m. -2,500 sq. m. that offer a wide, departmentalized range of groceries, and may carry some

general merchandise lines (e.g. Sainsbury's, Kroger). It also includes hard grocery discounters such as Wal-Mart.

Convenience

Stores

Includes all sales through stores of an area generally less than 300 sq m, that specialize in a limited range of food &

grocery products designed primarily for consumers with top-up shopping needs. Also includes sales in retail outlets

attached to gas stations, where fuel is the main revenue driver, kiosks, and newsstands. This also includes small

independent retailers, particularly those present in countries such as China and India.

Food & Drinks

Specialists

Includes bakers, butchers, delicatessens, drinks specialists, fishmongers, greengrocers, Food & drinks only stores,

and single category stores (e.g. stores selling only cheese, or only olives, or only honey, or only Confectionery

products) Example: Amul Ice Cream shops In India.

On-trade

Sales through consumer foodservice outlets include cafés/bars, FSR (full-service restaurants), fast food, self-service

cafeterias and street stalls/kiosks. Sales to semi captive foodservice outlets are also which include the outlets located

in leisure, travel and retail environments.

Other Retailers

Includes “Dollar Stores”, Variety Stores & General Merchandise Retailers, Cash & Carries & Warehouse Clubs,

Department Stores, Drug stores & Pharmacies, eRetailers, Vending Machines and other generalist retail channels not

included in the categories above (e.g. market traders, charity stores, student union stores, direct sales, and Duty Free

shops).

Channel definitions

404040

This report features data derived from market data.

Market Data

In order to create the data for all reports in this series and ensure their robustness, a comprehensive and empirically robust research

methodology has been adopted. This combines both a large-scale program of industry research with the results of extensive primary

industry interviewing and calling. Furthermore, all definitions are standardized across products and countries to ensure comparability.

The two main research methods, secondary research and primary research (the program of interviewing industry contacts), are brought

together and because both sets of research processes have been designed in conjunction with each other they can be combined and

consolidated into the final, integrated data sets.

The secondary research process involves covering publicly available sources, trade associations, specialist databases, company annual

reports, and industry publications. Primary research involves a major program of interviewing leading industry executives for each category

covered in each country – all with local country experts; typically brand, product and marketing managers for major brands within each

country. These processes help analysts in capturing both qualitative and quantitative information about the market.

The final stage of the process is the triangulation of inputs obtained from all the research methods with the analyst‟s own understanding of

the market in order to finalize the data. Once the data is finalized, it goes through various top level quality checks prior to publishing.

Methodology

414141

About Canadean

Canadean is a full-service business information provider with in-house market research capabilities. We specialize in analysis across

the Consumer Markets Value Chain, covering suppliers, producers, distribution and consumers.

Canadean‟s dedicated research and analysis teams consist of experienced professionals with an industry background in

marketing, market research, consulting and advanced statistical expertise. We offer value-added market research, insight and

strategic analysis and our products help companies to make better, more informed, strategic and tactical sales and marketing

decisions.

Canadean‟s areas of expertise include online research, qualitative and quantitative research, industry analysis, custom

approaches, and actionable insights. In addition Canadean has built a network of consultants and specialist researchers across more

than 60 countries, each with in-depth industry experience and expertise enabling us to conduct unique and insightful research via our

trusted business communities.

Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any

means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher, Canadean.

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the

findings, conclusions and recommendations that Canadean delivers will be based on information gathered in good faith from both

primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such, Canadean can accept no

liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

About Canadean