Community Webinarswww.insurancecommunitycenter.com

Sales Opportunities in Life & Annuities - An Introduction to Quick Life

Presented by:George Fraser

Director of Annuities Quick Life

www.InsuranceCommunityUniversity.com

Insurance Community Center

Presents Monthly Webinars Free to Community Members

Community webinars are archived on the Community homepage under the right hand tab titled: Webinar Archive

Community University provides webinars that qualify for CE in several states.

www.InsuranceCommunityUniversity.com

Introducing QuicklifeA strategic partner of Insurance Community Center

+

www.InsuranceCommunityUniversity.com

About George Fraser

George Fraser has over 40 years of Life and Annuity sales experience. In that time, he has acted as an agent, General Agent and Vice President of Retail Sales for leading Insurance providers.

George has served as National President of GAMA International, Chairman of the Board for AMTC as well as committee work for LIMRA. He also serves as a Director for Rainmaker Advisory LLC a leading consulting firm within the retail insurance broking sector.

www.InsuranceCommunityUniversity.com

What this course will cover:

Sales Opportunities in Life InsuranceSales Opportunities in AnnuitiesHow to Sell and Increase your Profits in 2012How you can be in the Life Insurance business

without having to set up a support structure

www.InsuranceCommunityUniversity.com

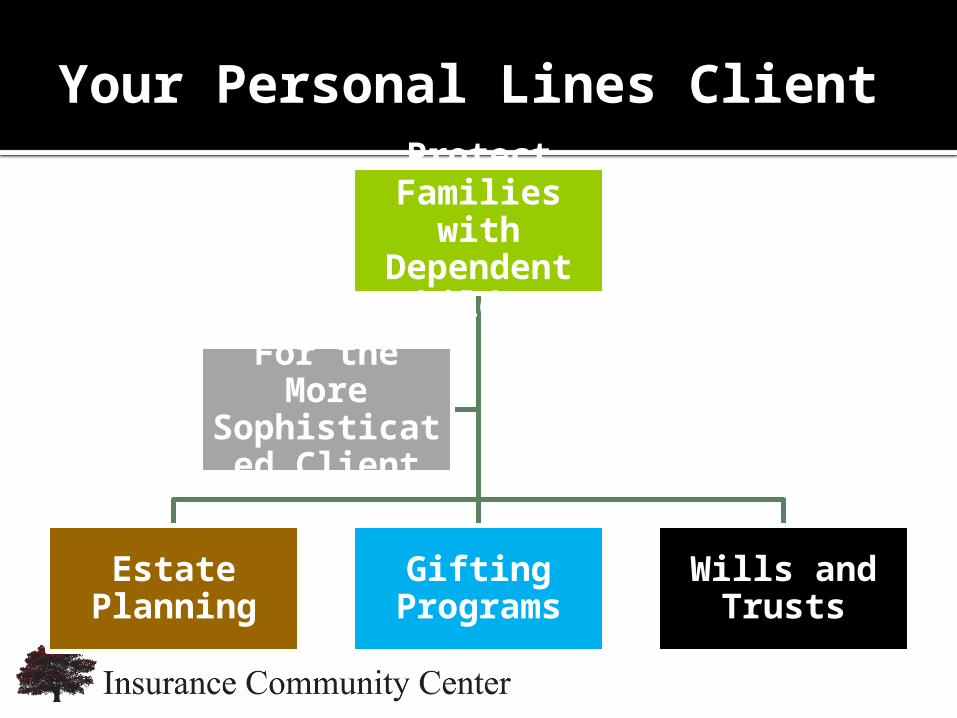

Your Personal Lines ClientProtect Families

with Dependent

Children

Estate Planning

Gifting Programs

Wills and Trusts

For the More

Sophisticated Client

www.InsuranceCommunityUniversity.com

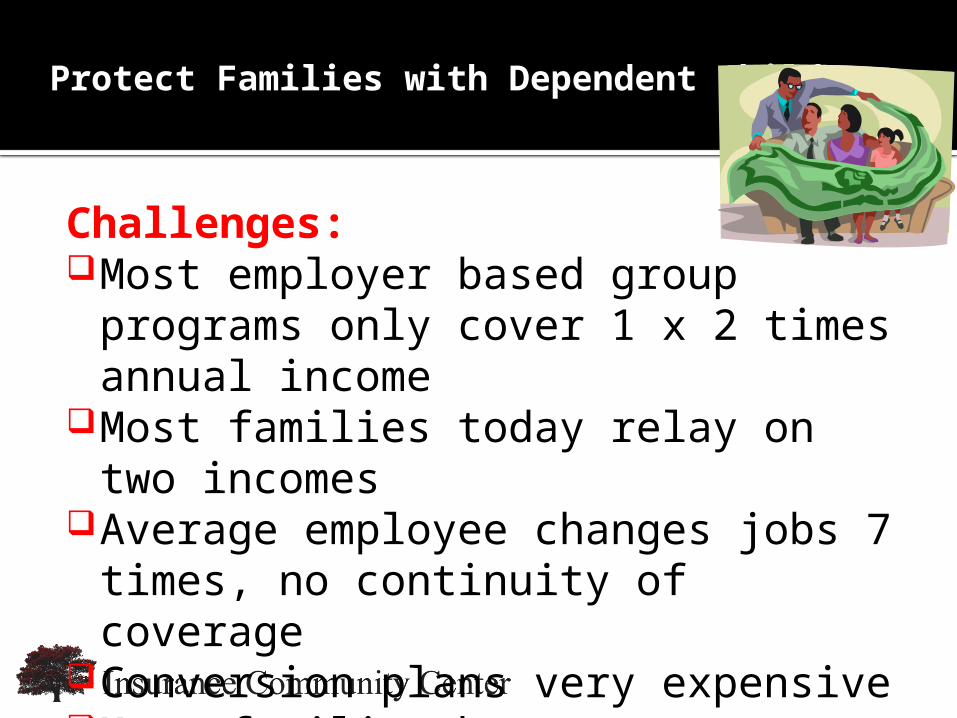

Protect Families with Dependent Children

Challenges:Most employer based group programs only

cover 1 x 2 times annual incomeMost families today relay on two incomesAverage employee changes jobs 7 times, no

continuity of coverageConversion plans very expensiveMost families have no emergency savings

www.InsuranceCommunityUniversity.com

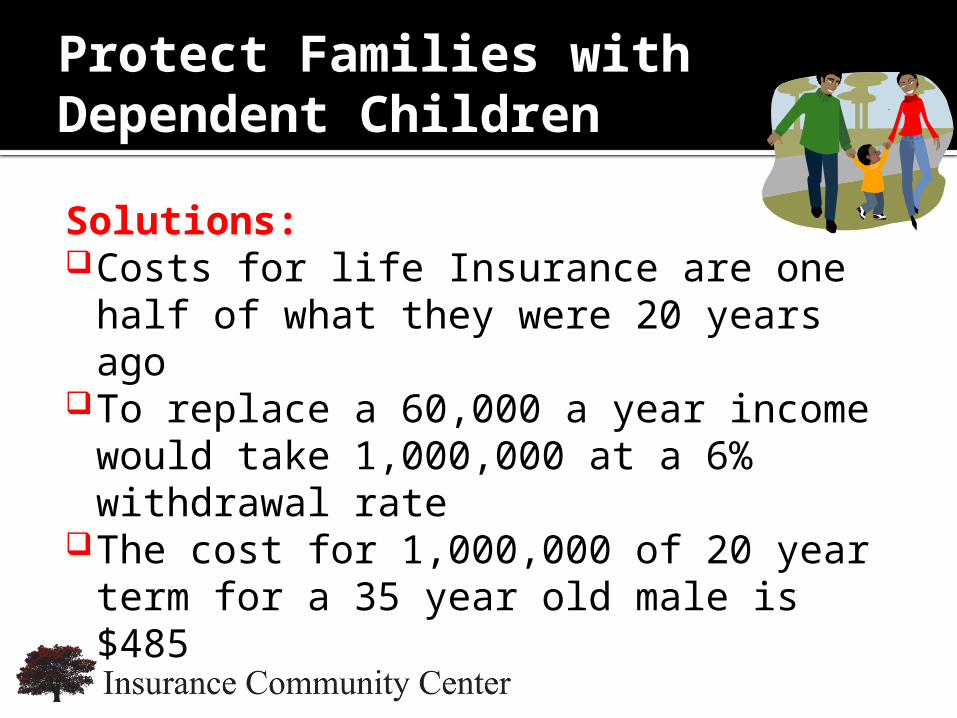

Protect Families with Dependent Children

Solutions: Costs for life Insurance are one half of what

they were 20 years agoTo replace a 60,000 a year income would take

1,000,000 at a 6% withdrawal rateThe cost for 1,000,000 of 20 year term for a

35 year old male is $485

www.InsuranceCommunityUniversity.com

Protect Families with Dependent Children

Individual coverages are not employer dependent

Two income families require coverage on both spouses

Automatically include low cost term coverage as part of the renewal process

www.InsuranceCommunityUniversity.com

General Uses of Life Insurance in Estate Planning

1. To provide liquidity to pay potential federal and state tax obligations

Starting in January of 2013 under current law tax rate will be 55% on estates In excess of 1,000,000

Many estates have assets tied up in real estate, business interests and fixed investments that are not liquid and would incur investment loss under forced liquidation

www.InsuranceCommunityUniversity.com

General Uses of Life Insurance in Estate Planning

2. To provide estate equalization Allows families to divide estate assets equally

without having to liquidate the asset Allows families to target specific family members

without endangering a business3. To provide income to a family while estate is

being settled 4. To pay off estate liabilities outside of taxes

www.InsuranceCommunityUniversity.com

Gifting Programs

Allows families to make specific gifts to endowments or charities

Allows families to make gifts to grandchildren or other relatives

Allows a family to set up a foundation to direct money to charities helping to reduce estate tax liability

www.InsuranceCommunityUniversity.com

Wills and Trusts

Helps eliminate double taxation of estate assets

Allows purchase of Life Insurance to be kept out of gross estate

Can provide ongoing income for successor generations

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Two types of funding agreements Cross Purchase and Entity Plans

1. Cross purchase agreements are typically used for partnerships that do not exceed three partners or in situations where the business may be sold at a later date and cost basis becomes important

2. Entity Plans are used with multiple ownership beyond three or In situations where the estate is going to redeem stock to pay estate settlement costs

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Cross Purchase Plans

Each partner agrees to purchase the other partners interest at death or retirement

Purchase price can be agreed on at time of agreement or a evaluation method can be established

The agreement can be funded or unfunded

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Cross Purchase Plans

1. Unfunded agreements are paid out of current earnings at the time of death and are a taxable event

2. Unfunded agreements can cause a strain on cash flow

3. Funded agreements with life insurance provide tax free funds to execute the agreement

4. Funded agreements can provide an accumulation to retire a partner

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Entity PlansCorporation purchases the decedents interest

at time of death or retirement and retires the stock leaving the remaining partners as holders of all outstanding shares

Commonly used when you have multiple partners

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Under section 303 has some estate tax advantages to estate of deceased partner

Remaining shareholders do not get a “stepped up” basis on the decedents share

www.InsuranceCommunityUniversity.com

Purchase Agreement Funding Mechanisms - Buy & Sell Plans

Entity PlansCan be funded or unfunded1. Funds may not be available for the future

purchase if unfunded2. If unfunded money for purchase is after tax

funds3. Funded agreements with life insurance

provide tax free money for purchase

www.InsuranceCommunityUniversity.com

Key Person Insurance

This is coverage written to indemnify a company against the loss of a key employee. There are several reasons for this type of coverage Loss of the employee would incur a loss of revenue A bank may require this in return for certain types

of lending to the company Used to provide funds for replacement of a key

employee

www.InsuranceCommunityUniversity.com

Key Person Insurance

A key employee is part of an long term succession plan and their loss would undermine the plan

A life Insurance policy is used to provide tax free funds to the company

www.InsuranceCommunityUniversity.com

Supplemental Retirement Programs

Deferred Compensation plans are an agreement between an employer and employee to pay out funds at a future date

Deferred compensation plans are typically used in C corporations

Deferred compensation plans do not offer current deductibility to company, but employee money is tax deferred

Company can be discriminatory on who it covers in the plan and how much they contribute

www.InsuranceCommunityUniversity.com

Supplemental Retirement Programs

Plans do not require 5500 annual filings or ERISA filings although an initial letter of notification is required

Plan must have substantial rights of forfeitureWhen paid out funds are deductible to the

employer and reported as income to the employee

Deferred compensation plans have substantial balance sheet advantages to an employer

Can be funded or unfunded

www.InsuranceCommunityUniversity.com

Bonus Plans

A Section 162 Bonus Plans is a non-qualified plan in which an employer gives a bonus to an employee as a supplement for their retirement. The bonus is tax deductible to the corporation and reported as current income to the employee. The employer can also bonus the tax amount due.

Almost always funded with Life Insurance Funds accumulate tax deferred Can be taken out tax deferred at retirement Can be discriminatory No ERISA filings No 5500 annual filings

www.InsuranceCommunityUniversity.com

Annuities

An annuity is a contract between an Insurance company and an annuitant to accumulate funds which are paid out at a later date either in a lump sum or in periodic payments The money accumulates on a tax deferred basis. No current

income tax is paid on the earnings When the money is taken out the first distributions are

considered gain If annuitized the annuitant can receive a lifetime income even

if the initial funds are depleted Modern riders allow for withdrawals with the potential of

protecting principal

www.InsuranceCommunityUniversity.com

Fixed Index Annuity

A fixed annuity where the annual crediting rate is pegged to a stock index Does not require securities licensing The value can go up, but never down Some products pay a bonus to the annuitant up

front. These bonuses range from 5-10% depending on the carrier. The bonus is immediately credited to the cash value of the annuity

www.InsuranceCommunityUniversity.com

Fixed Index Annuity

This product is particularly attractive to individuals approaching retirement who want a hedge in their portfolio

Individuals who have accumulated money in an IRA who are concerned about conserving principal with a return that could keep pace with inflation

People who do not have large sums of retirement funds and because of age or other factors want to avoid market risk

www.InsuranceCommunityUniversity.com

Why does the P & C Agent NOT sell Life Insurance

The Reasons are Many!Everyone recognizes the value of cross selling

to increase top line revenue from their existing book of business, yet in most agencies this does not happen.

How do you get company appointments. Who are the competitive carriers? How do I create a back office to assist me in

quoting and underwriting these products.

www.InsuranceCommunityUniversity.com

Why does the P & C Agent NOT sell Life Insurance

What are some common problems that individuals and business owners face that these new products would provide solutions.

How am I going to find the time to sell and service these new products.

www.InsuranceCommunityUniversity.com

Quick Life Solution

The Quick Life platform creates an instant back office for a producer with no cost Quick Life will help facilitate all company appointments

needed to sell the top carriers products The Quick Life quoting platform illustrates and compares

all of the competitive term products in the state a producer does business in

If a producer has knowledge ahead of time that a prospective client has a particular health issue it will only quote those carriers who have competitive underwriting for those conditions and the possible rates they will charge

www.InsuranceCommunityUniversity.com

Quick Life Solution

The Quick Life platform eliminates underwriting time and producer involvement in the application and underwriting process Part one of application can be taken over the phone and

downloaded to the Quick Life website Quick Life arranges the medical exam and orders all attending

physician statements Quick Life secures all client signature requirements through the

paramedical examiner If underwriting issues arise Quick Life will shop the coverage to

other carriers When a policy is issued Quick Life will send the policy directly to the

client or to the producer

www.InsuranceCommunityUniversity.com

Quick Life Solution

This user friendly platform lends itself to cross selling programs that do not involve large time commitment on the part of the P&C producer Eliminates time on the part of the producer to travel

to client to sell and secure applications The platform could be operated by a CSR in a

producers office eliminating need to find an outside producer to sell and service business

Could become an automatic part of the agencies renewal process

www.InsuranceCommunityUniversity.com

Quick Life Solution

Through Quick Life concierge program clients could be driven to a website that requires no producer involvement, but will still receive a commission

Quick Life director available to work with agency to customize a marketing program for them

www.InsuranceCommunityUniversity.com

Disclaimer

Insurance forms and endorsements vary based on insurance company; changes in edition dates; regulations; court decisions;

and state jurisdiction. This instructional materials provided by Insight is intended as a general guideline and any

interpretations provided by Insight do not modify or revise insurance policy language. The authors of these materials are

Quick Life and Insurance Community Center. In providing these materials neither Quick Life nor, Insurance Community Center

assumes any liability or responsibility to any person or business with respect to any loss that is alleged to be caused directly or

indirectly as a result of the instructional materials provided. Copyright 2010 – 2012 All Rights Reserved

www.insurancecommunitycenter.com

www.InsuranceCommunityUniversity.com

Join Today

Community: www.insurancecommunitycenter.com

University www.insurancecommunitycenter.com and click

“learn more” about the University

www.InsuranceCommunityUniversity.com36

Upcoming CE Classes

FREE Community Class

10/18 Homeowners Insurance

10/22 Integrated Disability

11/6 Insight on Ethics and the Insurance Industry

10/23 Business Income Claims in a Bad Economy

11/15 Preparing for 2013 & an Overview of AnnuitiesJoin the Community TODAY at:

www.insurancecommunitycenter.com