Download - Ch 01 Bond Pricing - Ready-To-Build

Annual Payments

Inputs

Number of Periods to Maturity (T) 8 8

Face Value (PAR) $1,000 20

Discount Rate / Period (r) 3.25% 6

Coupon Payment (PMT) $35.00 7

Bond Price using a TimelinePeriod 0 1 2 3 4 5 6 7 8

Cash FlowsPresent Value of Cash FlowsBond Price

Bond Price using the FormulaBond Price (P)

Bond Price using the PV FunctionBond Price

BOND PRICING

1 1

1

T

T

PMT r PARP

r r

A B C D E F G H I J

1

234567

8

9

1011

12

13

1415161718192021222324252627282930313233343536

EAR, APR, & Foreign Currencies Currency: US Dollar $1.00

Currency Number 4 Inputs (Select from below)

Rate Convention 2 Annual Percentage Rate 1 = Chinese Yuan

Annual Coupon Rate 4.00% 8 2 = European Euro € 0.6805

Yield to Maturity (Annualized) 1.74% 3 3 = Indian Rupee IDR 39.30

Number of Payments / Year 2 2 4 = US Dollar $1.00

Number of Periods to Maturity (T) 8 8

Face Value (PAR) $1,000 20

OutputsDiscount Rate / Period (r)Coupon Payment (PMT)

Bond Price using a TimelinePeriod 0 1 2 3 4 5 6 7 8Time (Years)Cash FlowsPresent Value of Cash FlowsBond Price

Bond Price using a FormulaBond Price

Bond Price using a FunctionBond Price

Bond Price using the PRICE Function (under APR)Bond Price

Yield to Maturity (Annualized) 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0% 14.0% 15.0% 16.0% 17.0% 18.0% 19.0% 20.0%

Data Table: Sensitivity of Bond Price to Discount Rate / PeriodInput Values for Discount Rate / Period

Output Formula:Bond Price

Bond Pricing By Calendar TimeCalendar Time (Years) 0 0.5 1 1.5 2 2.5 3 3.5 4Time to Maturity (Years) 4 3.5 3 2.5 2 1.5 1 0.5 0Number of Periods to Maturity (T)Bond Price of Coupon BondBond Price of Par Bond

BOND PRICINGExch Rate

$1.00 =

¥7.3790

)8 (Create the bond price Data Table. Select the range B64:V65, click on

Data | Data Tools | What-If Analysis | Data Table , enter B12 in the Row Input Cell ,

and click on OK.

0.00

2.00

4.00

6.00

8.00

10.00

12.00Bond Price By Yield To Maturity

Yield To Maturity

Bond

Pric

e

0 0.5 1 1.5 2 2.5 3 3.5 40.00

2.00

4.00

6.00

8.00

10.00

12.00Bond Pricing by Calendar Time

Calendar Time (Years)

Bo

nd

Pri

ce

E

A B C D E F G H I J K L M N O P Q R S T U V

1

23

4

5

6

7

8

9

10111213141516171819202122232425262728293031323334353637383940414243444546474849505152535455565758596061

62

63646566676869707172737475767778798081828384858687888990

Duration and Convexity

Inputs

Rate Convention 2 Annual Percentage Rate

Annual Coupon Rate 4.00% 8

Yield to Maturity (Annualized) 1.74% 3

Number of Payments / Year 2 2

Number of Periods to Maturity (T) 8 8

Face Value (PAR) $1,000 20

OutputsDiscount Rate / Period (r)Coupon Payment (PMT)

Bond Duration using a TimelinePeriodTime (Years)Cash FlowsPresent Value of Cash FlowsBond Price using a TimelineWeightWeight * TimeDuration using a TimelineModified Duration using a Timeline

Bond Duration using a FormulaDuration (D) using a FormulaModified Duration using a Formula

Bond Duration using a Function (under APR)Duration using a FunctionModified Duration using a Function

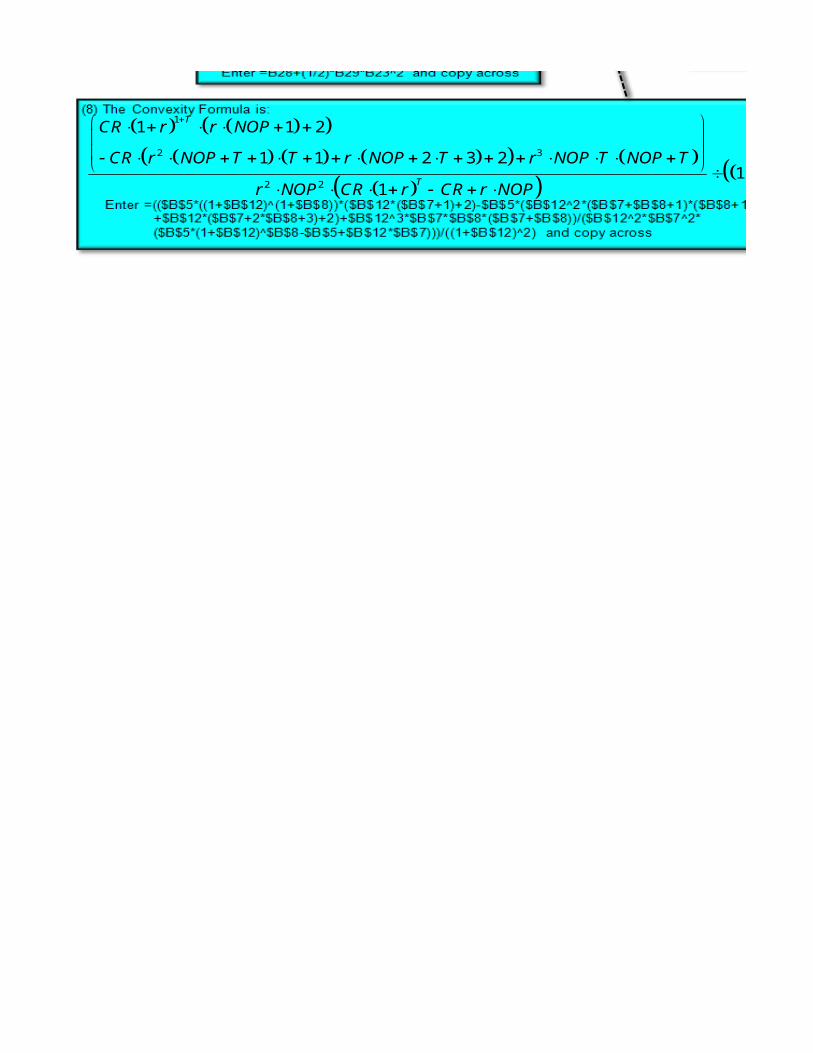

Bond ConvexityWeight * (Time^2+Time)Convexity using a TimelineConvexity using a Formula

BOND PRICING

EAR APR

1 /1

1 1T

r T CR NOP rrD

r NOP CR r r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

Currency: US Dollar $1.00

Currency Number 4 (Select from below)

1 = Chinese Yuan

2 = European Euro € 0.6805

3 = Indian Rupee IDR 39.30

4 = US Dollar $1.00

Exch Rate $1.00 =

¥7.3790

1 /1

1 1T

r T CR NOP rrD

r NOP CR r r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

Price Sensitivity

Inputs Annual Percentage Rate

Rate Convention 2

Annual Coupon Rate (CR) 4.00% 8

Yield to Maturity (Annualized) 1.74% 3

Number of Payments / Year (NOP) 2 2

Number of Periods to Maturity (T) 8 8

Face Value $1,000 20

OutputsDiscount Rate / Period (r) 0.9%Coupon Payment $20

Chart OutputsYield to Maturity (Annualized) 0.50% 1.00% 1.50% 2.00% 2.50%Discount Rate / PeriodChange in Yield to MaturityActual Bond PriceCurrent Bond PriceActual Percent Change in PriceModified DurationDuration ApproximationConvexityDuration and Convexity Approx.

BOND PRICING

0.0% 200.0% 400.0% 600.0% 800.0% 1000.0% 1200.0%

0%

200%

400%

600%

800%

1000%

1200%

Price Sensitivity

Actual Percent Change in Price

Duration Approximation

Duration and Convexity Approx.

Change in Yield To MaturityP

erc

en

t C

ha

ng

e in

Pri

ce

1 /1

* 11 1

T

r T CR NOP rrD r

r NOP CR r r NOP

EAR APR

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

Currency: US Dollar $1.00

Currency Number 4 (Select from below)

1 = Chinese Yuan

2 = European Euro € 0.6805

3 = Indian Rupee IDR 39.30

4 = US Dollar $1.00

3.00% 3.50% 4.00% 4.50% 5.00% 5.50% 6.00% 6.50%

Exch Rate $1.00 =

¥7.3790

0.0% 200.0% 400.0% 600.0% 800.0% 1000.0% 1200.0%

0%

200%

400%

600%

800%

1000%

1200%

Price Sensitivity

Actual Percent Change in Price

Duration Approximation

Duration and Convexity Approx.

Change in Yield To Maturity

Pe

rce

nt

Ch

an

ge

in P

ric

e

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

1

2 32

2 2

1 1 2

1 1 2 3 21

1

T

T

CR r r NOP

CR r NOP T T r NOP T r NOP T NOP Tr

r NOP CR r CR r NOP

7.00% 7.50% 8.00% 8.50% 9.00% 9.50% 10.00%

Immunization

Inputs

Rate Convention 2 Annual Percentage Rate

Yield to Maturity (Annualized) 1.74%

Number of Payments / Year 2

Bond 1 1.50% 4 $1,000 1,783 Bond 2 2.00% 8 $1,000 2,042 Bond 3 0.90% 2 $1,000 0 Bond 4 1.50% 4 $1,000 0 Bond 5 1.90% 6 $1,000 0 Bond 6 2.30% 8 $1,000 0 Bond 7 1.90% 6 $1,000 0 Bond 8 2.30% 8 $1,000 0

OutputsDiscount Rate / Period (r)

Bond Present Value, Duration, and Convexity using a TimelinePeriod 0 1 2 3Time (Years) 0.0 0.5 1.0 1.5Liabilities $0 $0 $0 Present Value of LiabilitiesTotal Present Value of LiabilitiesWeightWeight * TimeDuration of LiabilitiesModified Duration of LiabilitiesWeight * (Time^2+Time)Convexity of Liabilities

Assets Bond 1 $0 $0 $0 Bond 2 $0 $0 $0 Bond 3 $0 $0 $0 Bond 4 $0 $0 $0 Bond 5 $0 $0 $0 Bond 6 $0 $0 $0 Bond 7 $0 $0 $0 Bond 8 $0 $0 $0 Total Assets $0 $0 $0 Present Value of AssetsTotal Present Value of AssetsWeightWeight * TimeDuration of AssetsModified Duration of AssetsWeight * (Time^2+Time)Convexity of Assets

BOND PRICING

Annual Coupon Rate

Number of Periods to

Maturity (T)Face Value

(PAR)Number of

Bonds

EAR APR

DifferencesTotal Assets - LiabilitiesPV of Assets - PV of LiabilitiesDuration of Assets - Duration of LiabConvexity of Assets - Convexity of Liab

To solve the first problem when there is a single liability to immunize

To solve the second problem when there is a series of liabilities to immunize

To solve the third problem when there is a series of liabilities to immunize with cash flow matching

Currency: US Dollar $1.00

4 5 6 7 82.0 2.5 3.0 3.5 4.0$0 $0 $4,000,000 $0 $0

$1,782,856 $0 $0 $0 $0 $0 $0 $0 $0 $2,041,788 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

$1,782,856 $0 $0 $0 $2,041,788

Exch Rate $1.00 =

Coupon Payment (PMT)

Currency Number 4 (Select from below)

1 = Chinese Yuan

2 = European Euro € 0.6805

3 = Indian Rupee IDR 39.30

4 = US Dollar $1.00

¥7.3790

Currency: US Dollar $1.00

Inputs Annual Percentage Rate

Rate Convention 2 Annual Coupon Rate 4.00%Yield to Maturity (Annualized) 1.74%Number of Payments / Year 2 (1) Number of Periods to Maturity (T) 8 (2) Face Value (PAR) $1,000 (3) Discount Rate / Period (r) 0.87%(4) Coupon Payment (PMT) $20.00 (5) Bond Price (P) $1,086.96

(1) Number of Periods to Maturity (T) from the other four variablesNumber of Periods to Maturity using NPER Function

(2) Face Value (PAR) from the other four variablesFace Value using the FV FunctionFace Value using the Formula

(3) Discount Rate / Period (r) from the other four variablesDiscount Rate / Period using the RATE Function

(4) Coupon Payment (PMT) from the other four variablesCoupon Payment using the PMT FunctionCoupon Payment using the Formula

(5) Bond Price (P) from the other four variablesBond Price using the PV FunctionBond Price using the Formula

BOND PRICINGSystem of Five Bond

VariablesExch Rate

$1.00 =

EAR

APR

1 1

1

T

TPMT r

PAR P rr

1

1 1

T

T

P PAR rPMT

r r

1 1

1

T

T

PMT r PARP

r r

A B C D E F G H I J

1

23

4

56789101112131415161718192021222324252627282930313233343536373839404142