CECL –WHY IT’S A BIG DEAL AND WHAT YOU NEED TO KNOW TO FULFILL YOUR OVERSIGHT ROLE

New Jersey Bankers Association Annual Conference

May 2017

1

TODAY’S PRESENTERS

Faye MillerPartner, National Professional Standards [email protected]

Martin CaineMember of the Firm, Wolf & Company, [email protected]

2

AGENDA

What is CECL?

Why is it a big deal?

What is your oversight role?

3

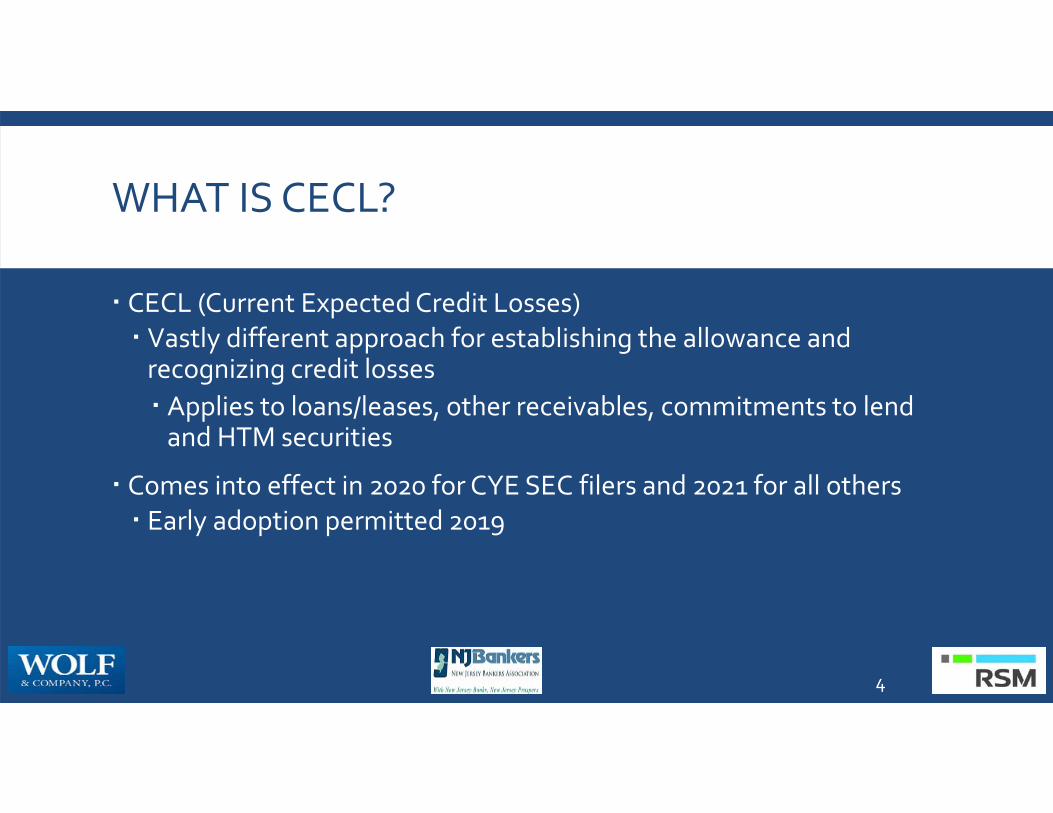

WHAT IS CECL?

CECL (Current Expected Credit Losses) Vastly different approach for establishing the allowance and recognizing credit losses Applies to loans/leases, other receivables, commitments to lend and HTM securities

Comes into effect in 2020 for CYE SEC filers and 2021 for all others Early adoption permitted 2019

4

WHY IS CECL A BIG DEAL?

5

WHY IS CECL A BIG DEAL?

Significant increases to the allowance are likely Provide for expected losses rather than incurred Even if risk of loss is remote Recognize allowance on purchased financial assets Limited circumstances in which you can conclude based solely on the collateral that no allowance is necessary Recognize expected credit losses on HTM securities regardless of impairment status

Ramifications to regulatory capital ratios

6

Management action items

7

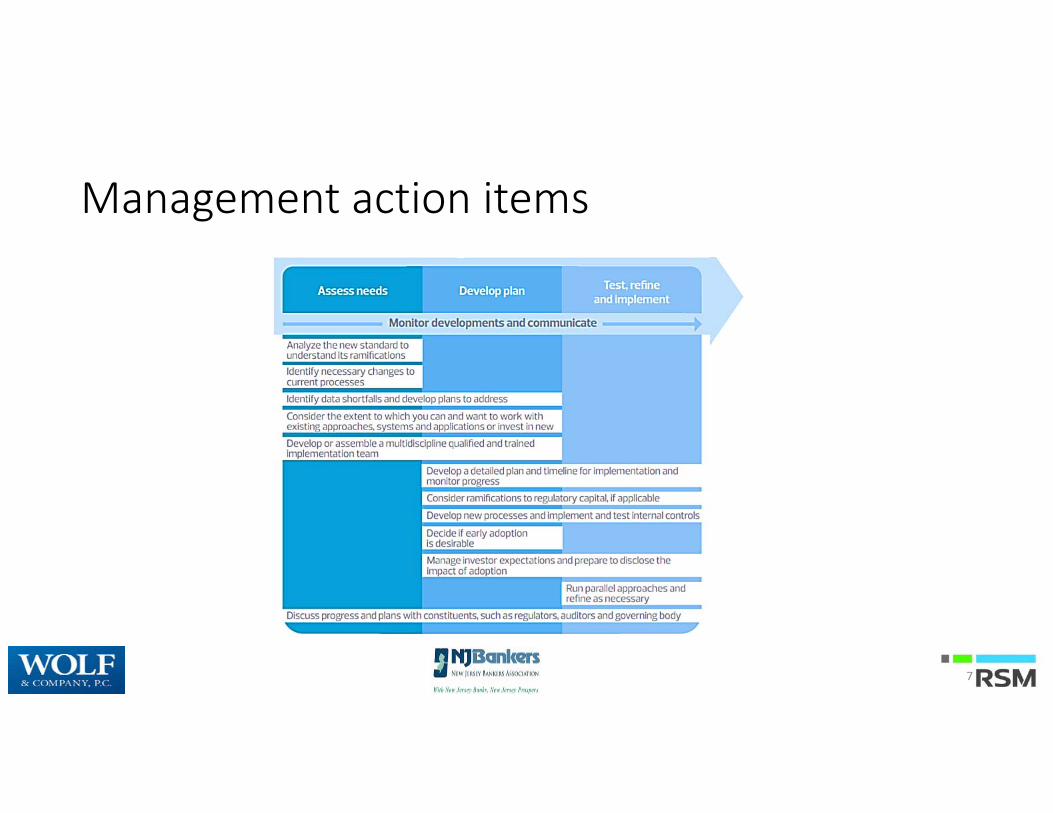

MANAGEMENT ACTION ITEMS

Analyze requirements and assess needs Internal/external expertise Data Systems/applications

Develop plan Implementation timeline/team Methodologies/processes/controls Filling data gaps Modify current systems or invest in new Monitor developments and discuss with constituents

8

MANAGEMENT ACTION ITEMS

Test, refine and implementMonitor progress/adherence to timeline Decide on early adoptionMonitor developments and refine as necessary Regulatory views, TRG interpretations, feedback from auditors Conduct independent assessments/test internal controls Run parallel approach and refine Address ramifications to capital, credit extension, investment philosophy, etc

9

Implementation Considerations

10

Implementation Considerations

11

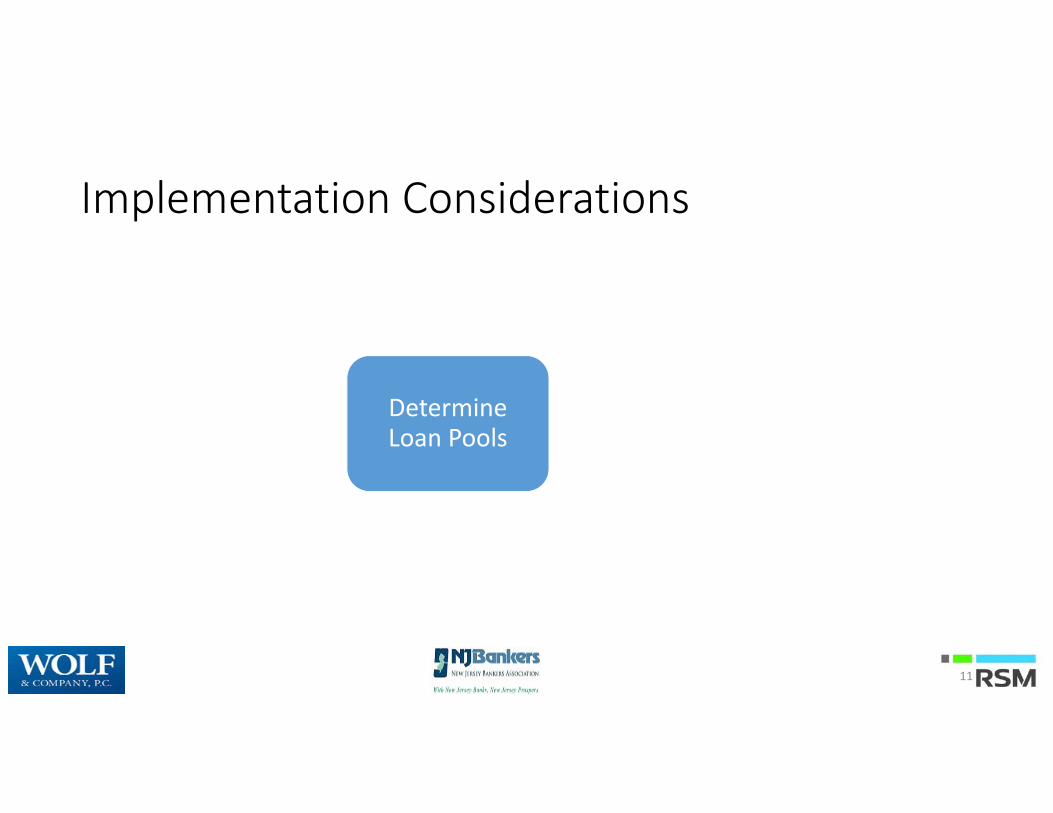

Determine Loan Pools

Implementation Considerations

12

Determine Loan Pools

Identify an appropriate methodology

Implementation Considerations

13

Determine Loan Pools

Identify an appropriate methodology

Obtain sufficient historical loss data

Implementation Considerations

14

Determine Loan Pools

Identify an appropriate methodology

Developreasonable and supportable forecasts

Obtain sufficient historical loss

data

LOAN POOLS

Loan pooling is a critical decision point; impacting all subsequent actions.

The concept of “impaired” loans is eliminated – an estimated credit loss should only be measured individually if there are no similar risk characteristics with other loans.

15

PURCHASED CREDIT DETERIORATED ASSETS (PCD)

Will be able to gross up the allowance for expected credit losses for purchased assets with a more than insignificant deterioration in credit quality.

This will be applied more broadly to purchased loans than the current accounting for purchased credit impaired loans, which generally only applies to impaired assets.

16

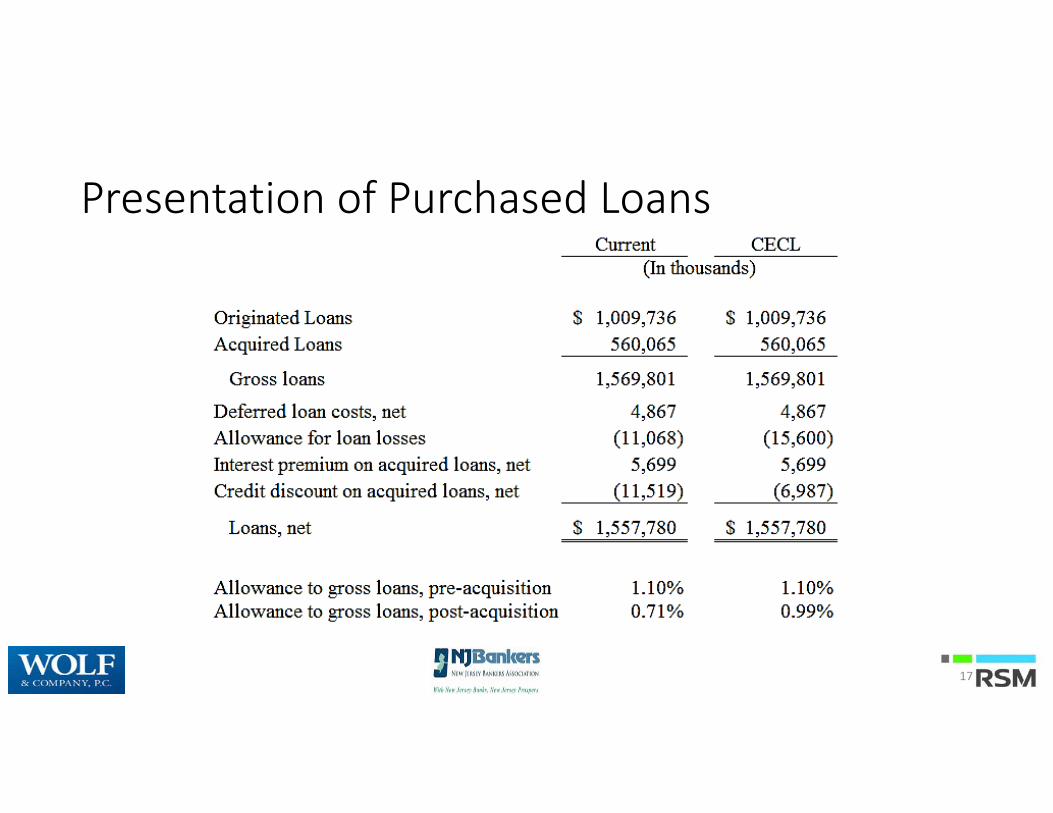

Presentation of Purchased Loans

17

Presentation of Purchased Loans

18

APPROPRIATE METHODOLOGY

The standard is explicitly scalable and allows preparers to develop estimation methods that are appropriate and practical for their circumstances. FASB concluded that different outcomes for expected credit losses are acceptable, given different levels of complexity and sophistication. One model but many methods Methodology by loan segment should be determined early; relevant data (i.e. historical losses, risk characteristics such as geography, LTV, vintage, etc.) and software needs may vary. Industry standards and best practices will emerge.

19

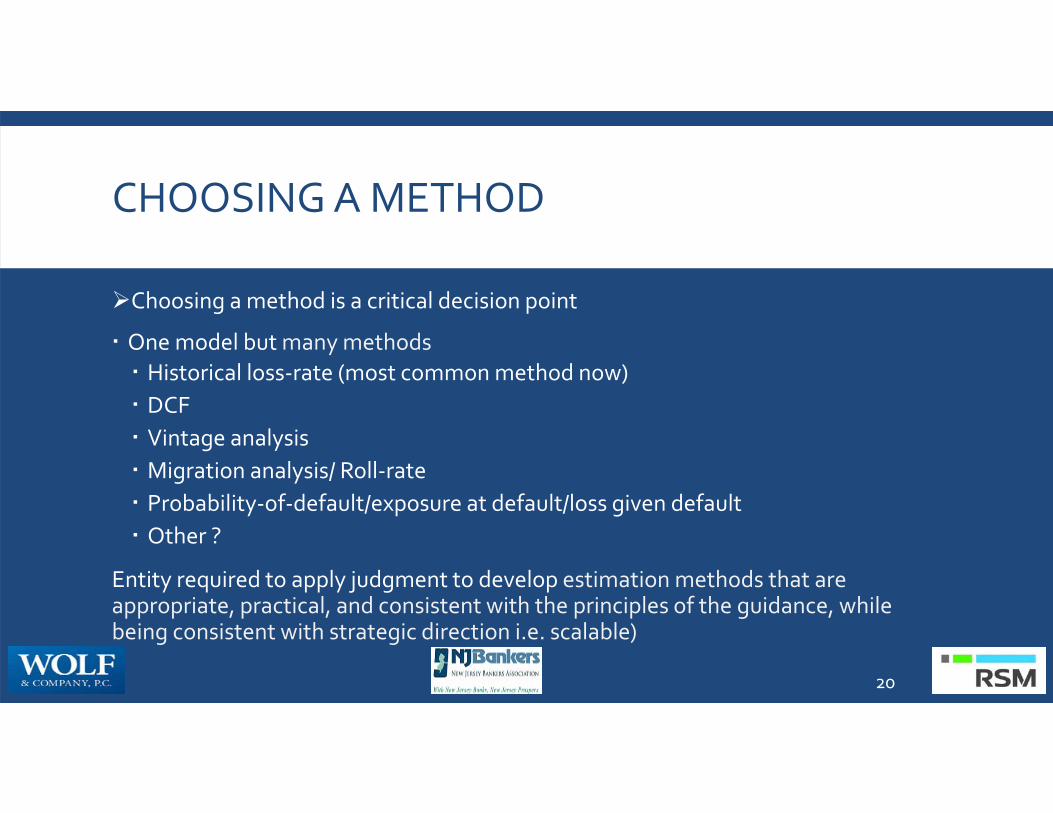

CHOOSING A METHOD

Choosing a method is a critical decision point

One model but many methods Historical loss‐rate (most common method now) DCF Vintage analysis Migration analysis/ Roll‐rate Probability‐of‐default/exposure at default/loss given default Other ?

Entity required to apply judgment to develop estimation methods that are appropriate, practical, and consistent with the principles of the guidance, while being consistent with strategic direction i.e. scalable)

20

HISTORICAL LOSS DATA

An entity’s loss history loss remains as the starting point and generally provides a basis for expected credit losses.GAAP does not specify a particular methodology for determining historical credit loss experience. “That methodology may vary depending on the size of the entity, the range of the entity’s activities, the nature of the entity’s financial assets, and other factors.” [ASU 326‐20‐55‐2] The loan segment and the chosen method will determine the data needs. Consider the impact of loans that will be assessed individually (removed from the pool)

21

REASONABLE AND SUPPORTABLE FORECASTS

The adjustments for current conditions and reasonable and supportable forecasts may continue to be qualitative, similar to the approach applied by many institutions today.

More robust quantitative models and/or greater segmentation may result in a smaller qualitative component, depending on the circumstances. Q‐Factor adjustments may be more significant because of the life‐of‐loan measurement period. Qualitative analysis may not always be directionally consistent with current trends/events.For example, an increase in delinquency rates may have been previously considered/anticipated when estimating expected credit losses.

22

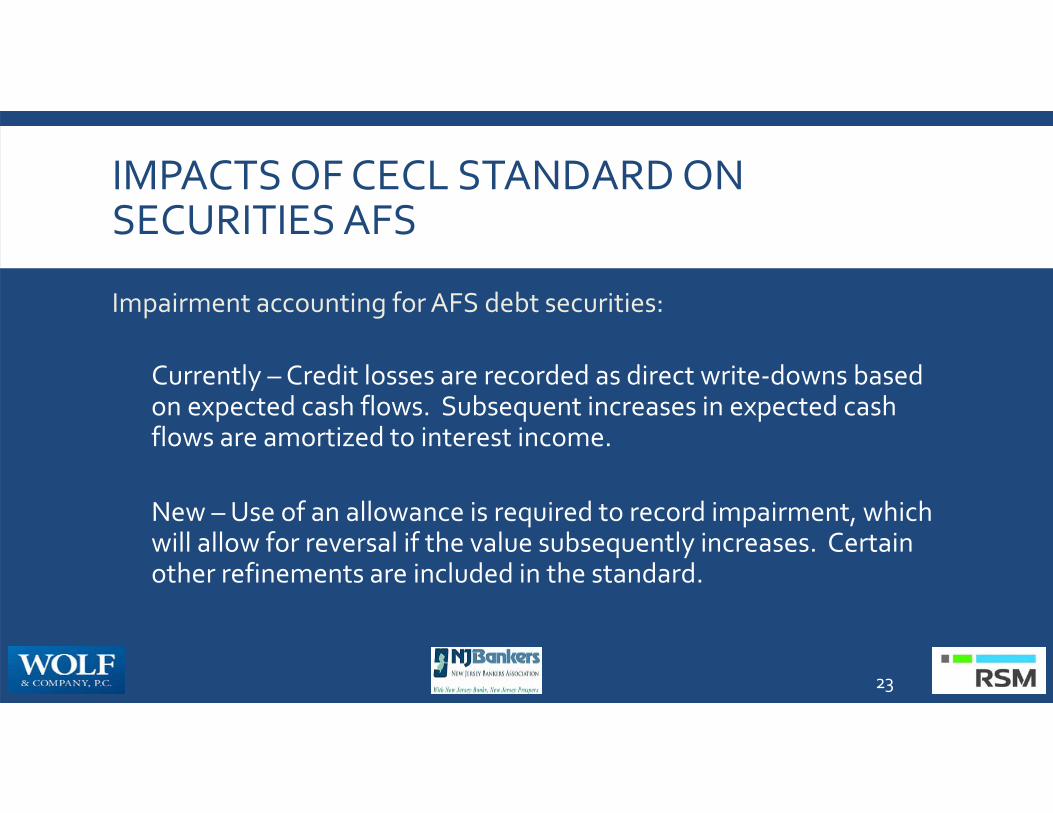

IMPACTS OF CECL STANDARD ON SECURITIES AFS

Impairment accounting for AFS debt securities:

Currently – Credit losses are recorded as direct write‐downs based on expected cash flows. Subsequent increases in expected cash flows are amortized to interest income.

New –Use of an allowance is required to record impairment, which will allow for reversal if the value subsequently increases. Certain other refinements are included in the standard.

23

WHAT IS YOUR OVERSIGHT ROLE

24

Governing Body Considerations

25

GOVERNING BODY QUESTIONS TO ASK

Is tone at the top appropriate?

Are internal/external resources sufficient and qualified?

Is there a detailed plan with key milestones completed as planned?

Are appropriate policies, procedures and controls in place?

What independent assessments will be performed?

What information will be made available to governing body?

26

Questions?

27

SUPPLEMENTARY SECTION ‐ EXAMPLES

The FASB material is copyrighted by the Financial Accounting Foundation, 401 Merritt 7, Norwalk, CT 06856, and is reproduced with permission.

28

Example – Loss Rate Approach

29

Example – Estimating losses by vintage year (ASC 326‐20‐55‐30)

30

EXAMPLE – PROBABILITY OF DEFAULT METHOD

Expected loss = Probability of default x Loss given default x Exposure at default

Bank has a pool of loans with an outstanding balance of $30 million. Management estimates the probability of these loans going in to default to be 5% and the loss given default to be 20%.

5% x 20% x $30 million=$300,000 expected losses

31

RSM Thought Leadership – CECL Resource Center

32

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. Wolf & Company, RSM US LLP, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person.

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International. RSM® and the RSM logo are registered trademarks of RSM International Association. The power of being understood® is a registered trademark of RSM US LLP.

©2016 RSM US LLP. All Rights Reserved.

33