12nd quarter 2012

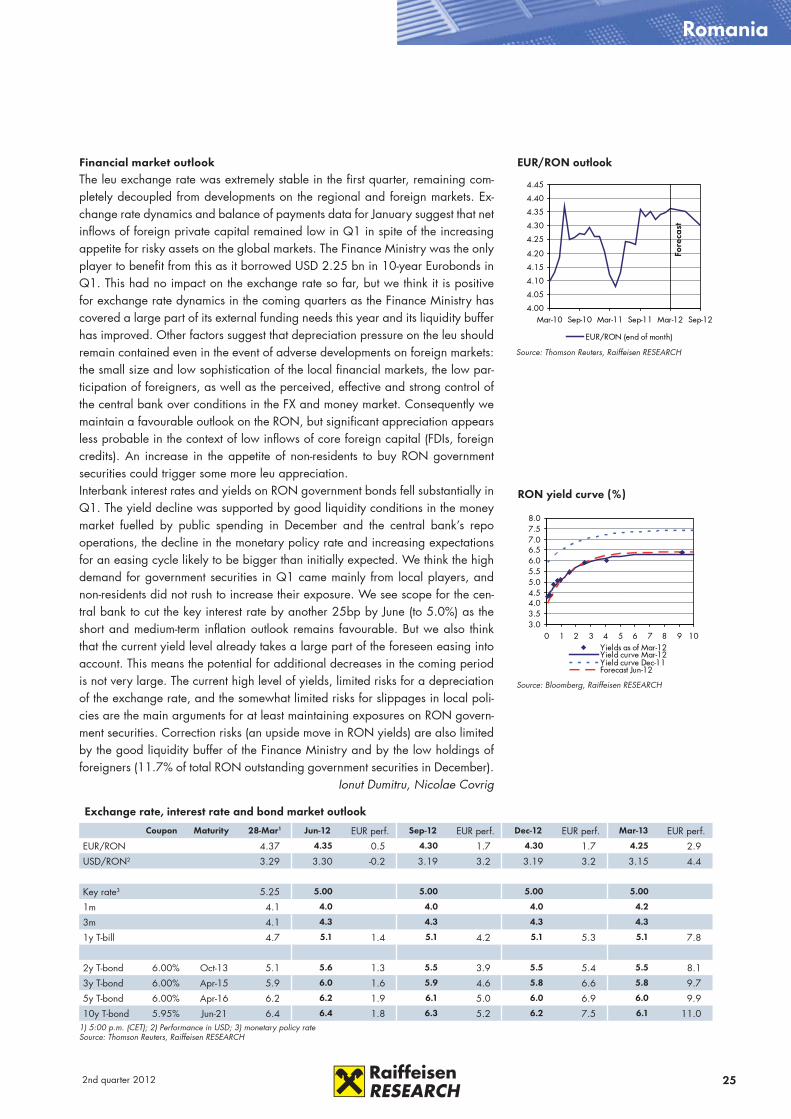

www.raiffeisenresearch.at

Central & Eastern European StrategyCentral & Eastern European Strategy2nd quarter 2012

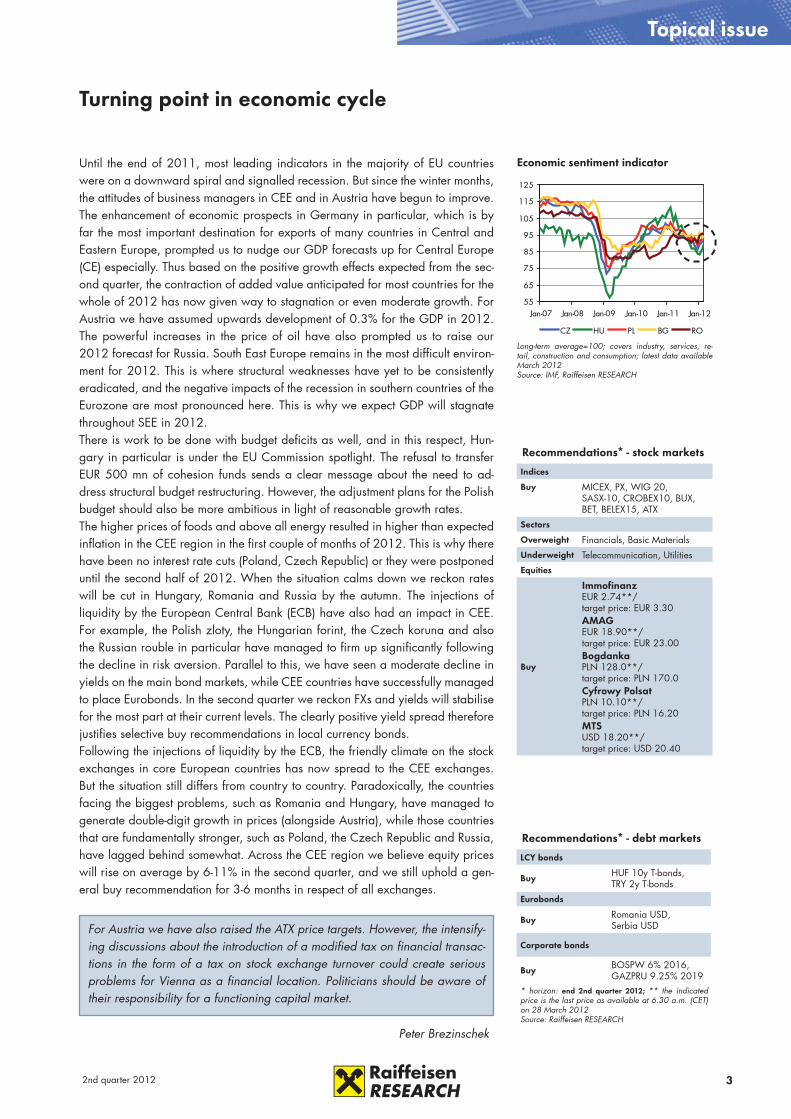

Turning point in economic cycle

Economic outlook improving on Eurozone revision

Limited potential for further FX appreciation

Buy recommendation on equities

Overweight risky assets in CEE

2 2nd quarter 2012

Content

Topical issue: Turning point in economic cycle 3

Forecasts CEE incl. Austria 4

Asset allocation CEE incl. Austria 6

Special: CEE growth revision – where is growth coming from? 10

Austria 12

CE: Poland 14

Hungary 16

Czech Republic 18

Slovakia 20

Slovenia 21

SEE: Croatia 22

Romania 24

Bulgaria 26

Serbia 27

Bosnia and Herzegovina 28

Albania 29

CIS: Russia 30

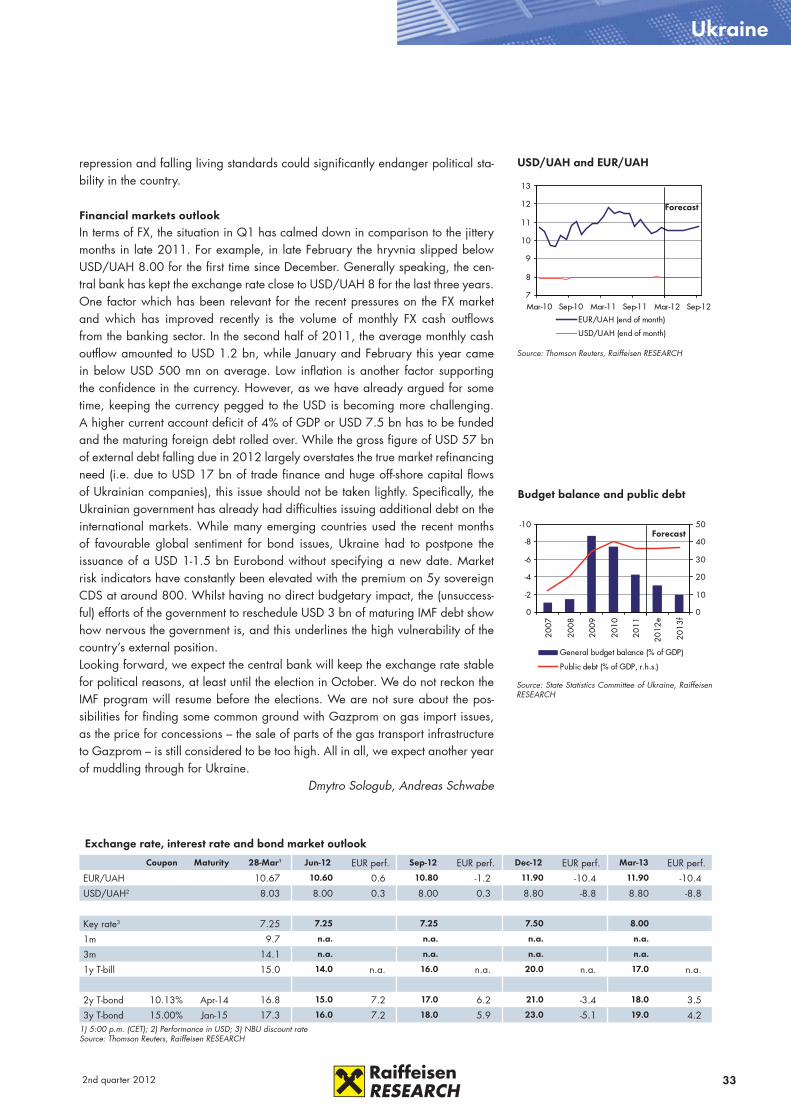

Ukraine 32

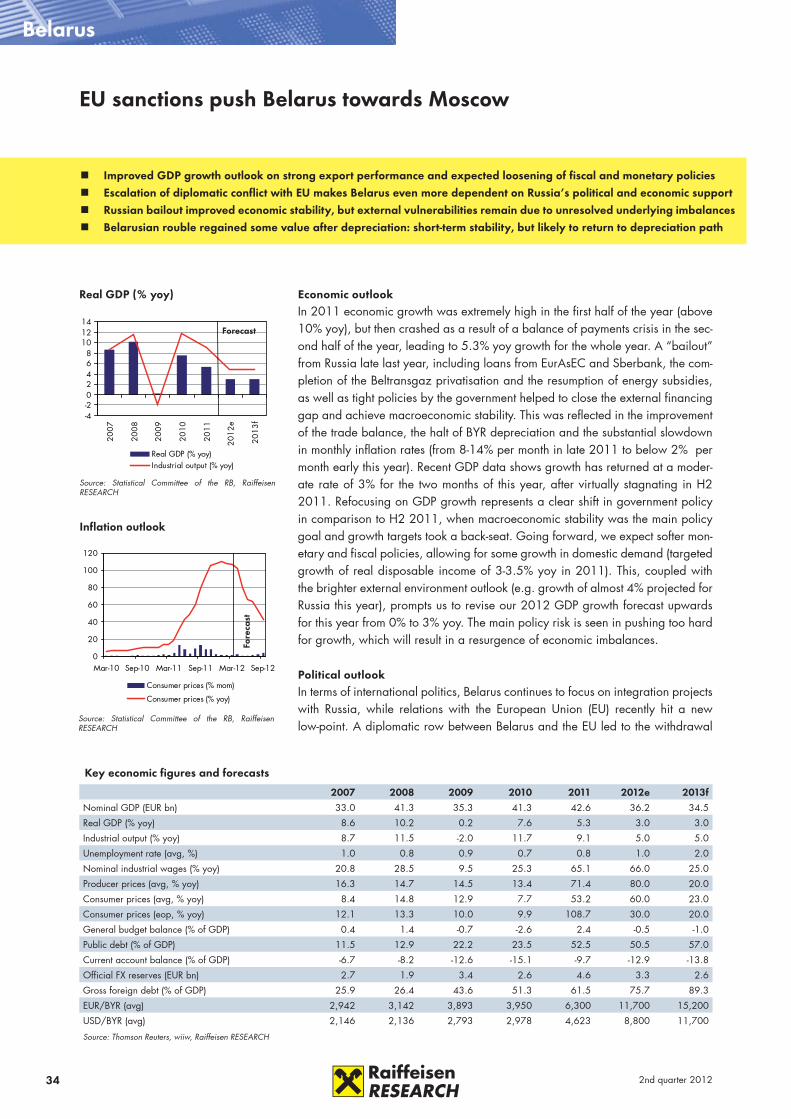

Belarus 34

Turkey 36

Sovereign Eurobonds 38

Corporate Eurobonds 40

Equity markets 42

Sectors 48

Equities - top picks 54

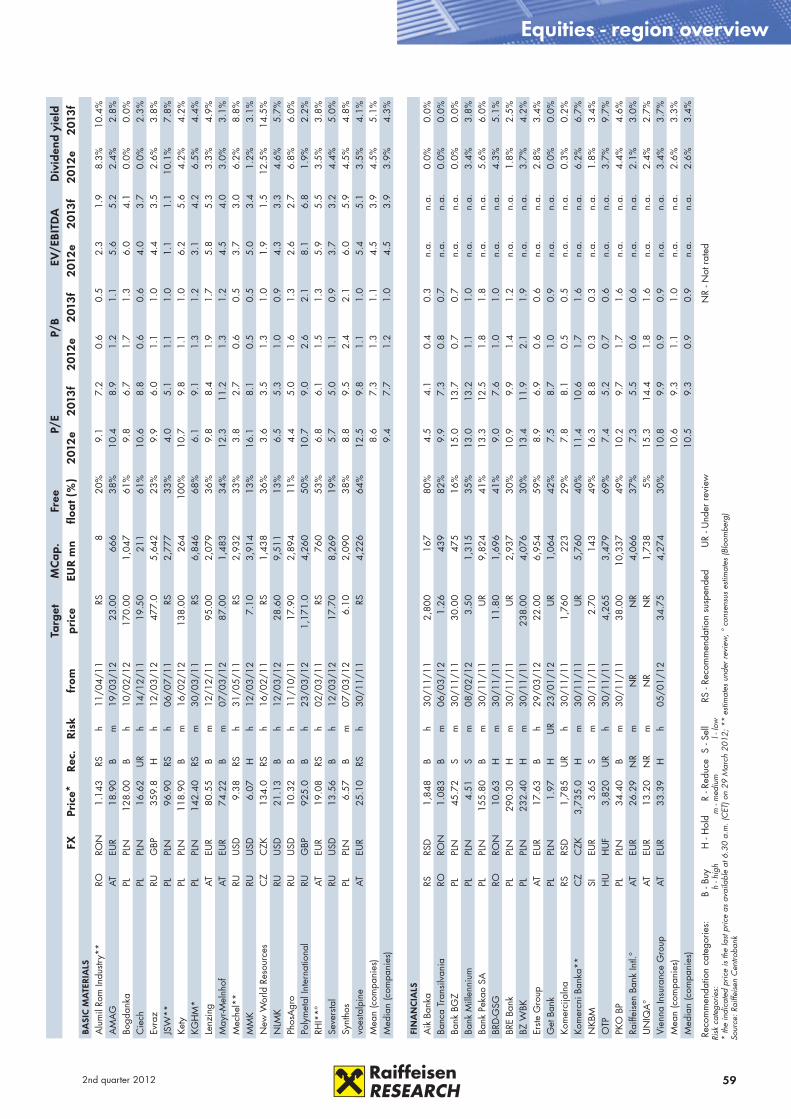

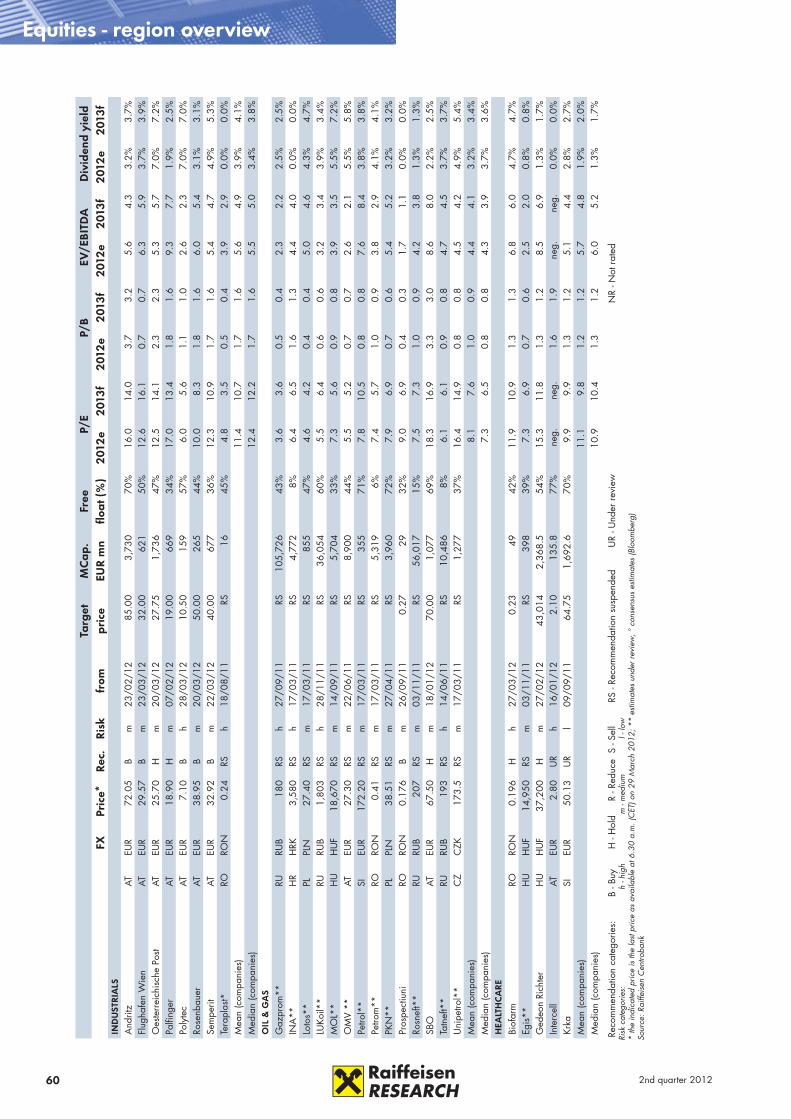

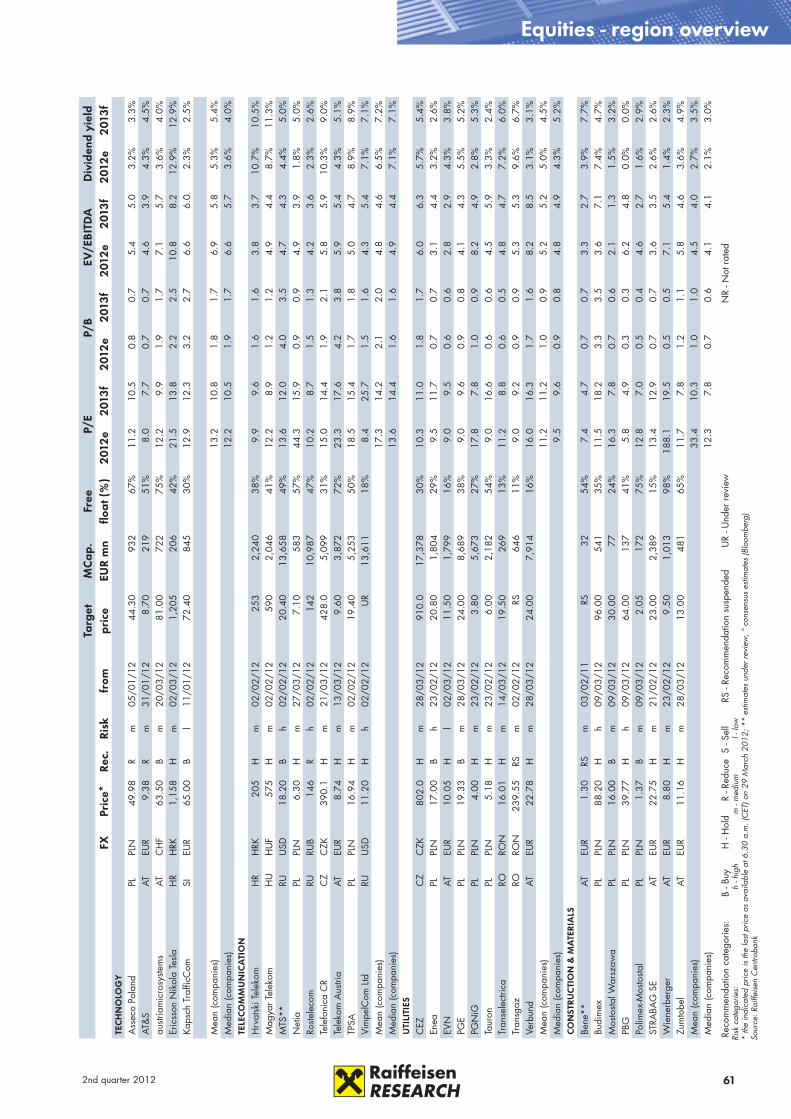

Equities - region overview 59

Sector weightings in comparison 63

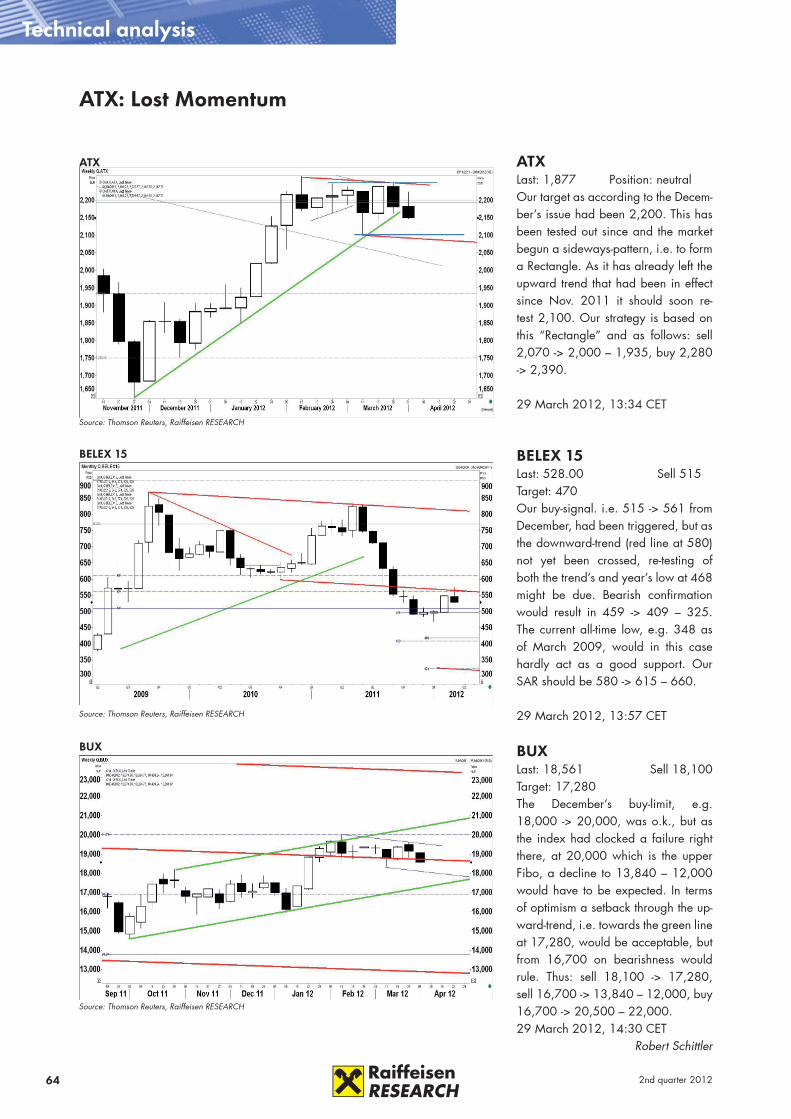

Technical analysis 64

Quantitative analysis 66

Acknowledgements & abbreviations 67

Explanation:e ... estimatef ... forecastp ... preliminary figures Eurozone ... Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, Netherlands, Portugal, Slovenia, Slovakia, SpainCE ... Central European countries - Poland, Hungary, Czech Republic, Slovakia, SloveniaSEE ... South East European countries - Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Romania, SerbiaCIS ... European CIS (Commonwealth of Independent States) countries - Russia, Ukraine, BelarusCEE ... Central and Eastern Europe (CE + SEE + CIS)

Central & Eastern European Strategy

32nd quarter 2012

Topical issue

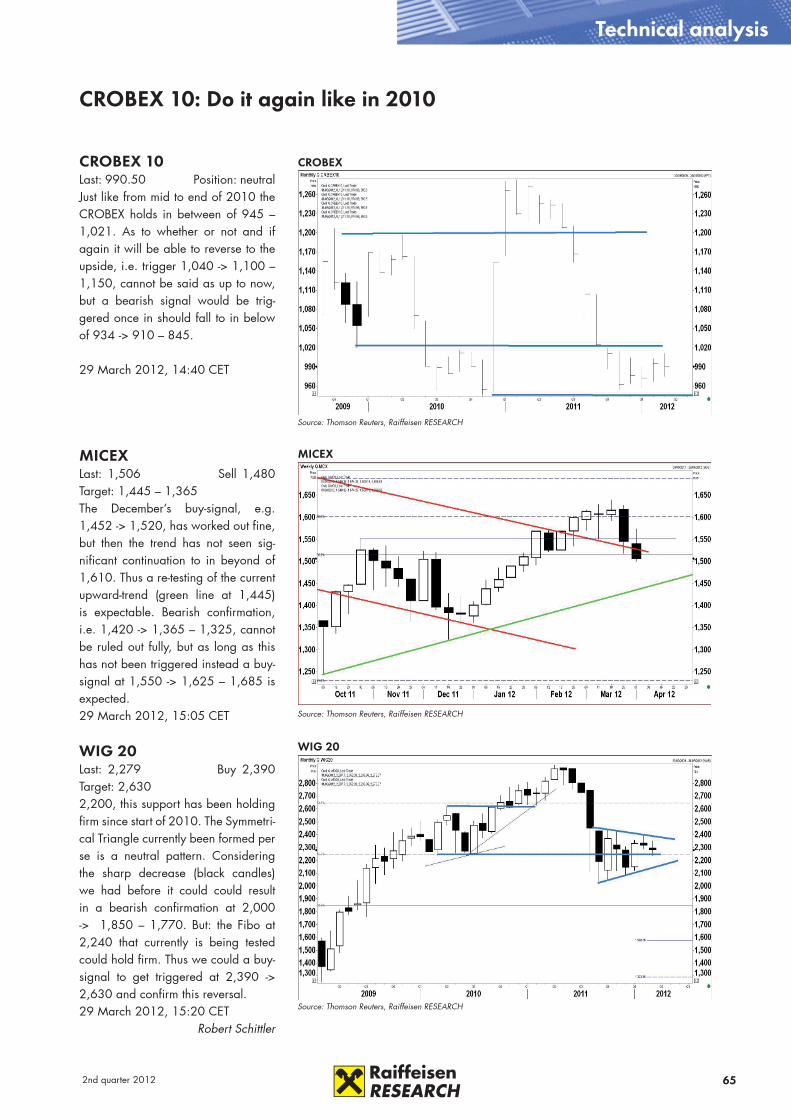

Until the end of 2011, most leading indicators in the majority of EU countries were on a downward spiral and signalled recession. But since the winter months, the attitudes of business managers in CEE and in Austria have begun to improve. The enhancement of economic prospects in Germany in particular, which is by far the most important destination for exports of many countries in Central and Eastern Europe, prompted us to nudge our GDP forecasts up for Central Europe (CE) especially. Thus based on the positive growth effects expected from the sec-ond quarter, the contraction of added value anticipated for most countries for the whole of 2012 has now given way to stagnation or even moderate growth. For Austria we have assumed upwards development of 0.3% for the GDP in 2012. The powerful increases in the price of oil have also prompted us to raise our 2012 forecast for Russia. South East Europe remains in the most difficult environ-ment for 2012. This is where structural weaknesses have yet to be consistently eradicated, and the negative impacts of the recession in southern countries of the Eurozone are most pronounced here. This is why we expect GDP will stagnate throughout SEE in 2012. There is work to be done with budget deficits as well, and in this respect, Hun-gary in particular is under the EU Commission spotlight. The refusal to transfer EUR 500 mn of cohesion funds sends a clear message about the need to ad-dress structural budget restructuring. However, the adjustment plans for the Polish budget should also be more ambitious in light of reasonable growth rates.The higher prices of foods and above all energy resulted in higher than expected inflation in the CEE region in the first couple of months of 2012. This is why there have been no interest rate cuts (Poland, Czech Republic) or they were postponed until the second half of 2012. When the situation calms down we reckon rates will be cut in Hungary, Romania and Russia by the autumn. The injections of liquidity by the European Central Bank (ECB) have also had an impact in CEE. For example, the Polish zloty, the Hungarian forint, the Czech koruna and also the Russian rouble in particular have managed to firm up significantly following the decline in risk aversion. Parallel to this, we have seen a moderate decline in yields on the main bond markets, while CEE countries have successfully managed to place Eurobonds. In the second quarter we reckon FXs and yields will stabilise for the most part at their current levels. The clearly positive yield spread therefore justifies selective buy recommendations in local currency bonds.Following the injections of liquidity by the ECB, the friendly climate on the stock exchanges in core European countries has now spread to the CEE exchanges. But the situation still differs from country to country. Paradoxically, the countries facing the biggest problems, such as Romania and Hungary, have managed to generate double-digit growth in prices (alongside Austria), while those countries that are fundamentally stronger, such as Poland, the Czech Republic and Russia, have lagged behind somewhat. Across the CEE region we believe equity prices will rise on average by 6-11% in the second quarter, and we still uphold a gen-eral buy recommendation for 3-6 months in respect of all exchanges.

Turning point in economic cycle

Recommendations* - debt markets

LCY bonds

Buy HUF 10y T-bonds, TRY 2y T-bonds

Eurobonds

Buy Romania USD, Serbia USD

Corporate bonds

Buy BOSPW 6% 2016,GAZPRU 9.25% 2019

* horizon: end 2nd quarter 2012; ** the indicated price is the last price as available at 6.30 a.m. (CET) on 28 March 2012Source: Raiffeisen RESEARCH

Recommendations* - stock markets

Indices

Buy MICEX, PX, WIG 20, SASX-10, CROBEX10, BUX, BET, BELEX15, ATX

Sectors

Overweight Financials, Basic MaterialsUnderweight Telecommunication, UtilitiesEquities

Buy

ImmofinanzEUR 2.74**/ target price: EUR 3.30AMAGEUR 18.90**/ target price: EUR 23.00BogdankaPLN 128.0**/ target price: PLN 170.0Cyfrowy PolsatPLN 10.10**/ target price: PLN 16.20MTSUSD 18.20**/ target price: USD 20.40

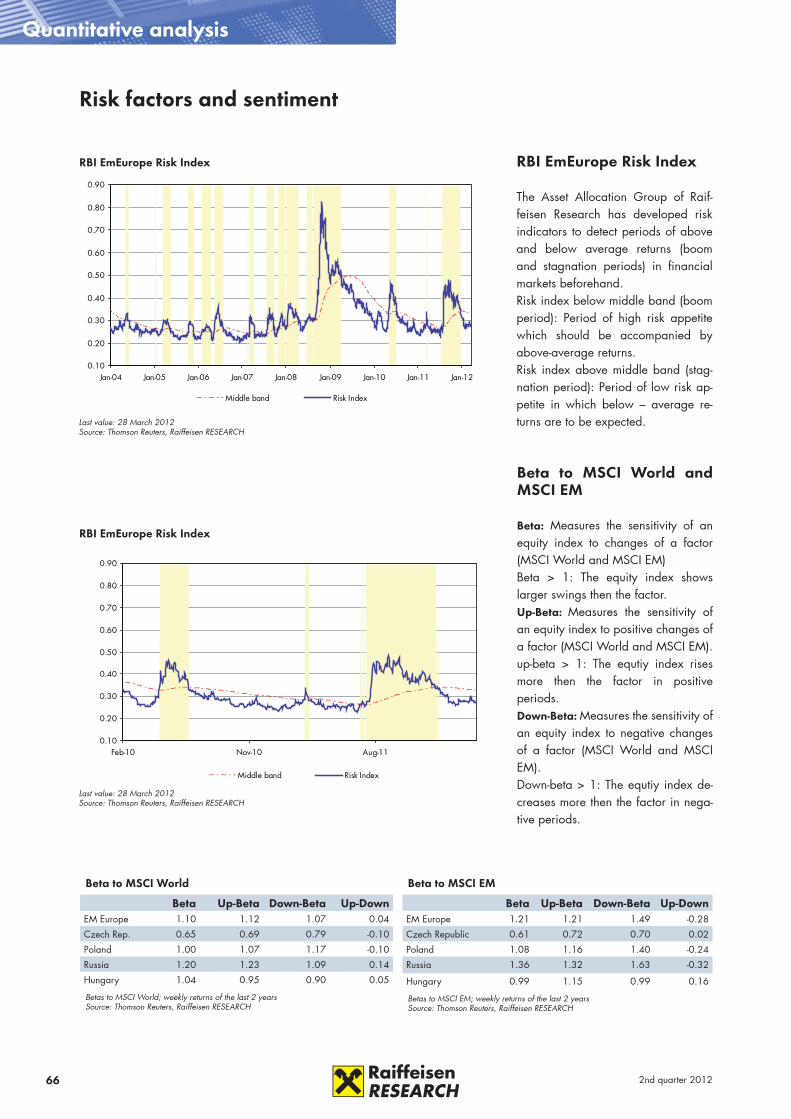

Economic sentiment indicator

Long-term average=100; covers industry, services, re-tail, construction and consumption; latest data available March 2012Source: IMF, Raiffeisen RESEARCH

55

65

75

85

95

105

115

125

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

CZ HU PL BG RO

Peter Brezinschek

For Austria we have also raised the ATX price targets. However, the intensify-ing discussions about the introduction of a modified tax on financial transac-tions in the form of a tax on stock exchange turnover could create serious problems for Vienna as a financial location. Politicians should be aware of their responsibility for a functioning capital market.

4 2nd quarter 2012

Real GDP (% yoy)

Countries 2010 2011 2012e 2013fPoland 3.9 4.3 2.8 3.7Hungary 1.3 1.7 -0.5 1.5Czech Rep. 2.7 1.7 -0.2 1.4Slovakia 4.0 3.3 0.8 2.5Slovenia 1.4 -0.2 0.0 1.5CE 3.2 3.1 1.4 2.7Croatia -1.2 0.2 -1.0 1.0Bulgaria 0.4 1.7 1.0 2.5Romania -1.6 2.5 0.5 2.5Serbia 1.0 2.0 0.0 1.0Bosnia a. H. 0.7 1.9 0.0 2.0Albania 3.9 2.0 2.5 3.5SEE -0.7 1.9 0.3 2.1Russia 4.3 4.3 3.7 4.0Ukraine 4.2 5.2 3.5 4.0Belarus 7.6 5.3 3.0 3.0CIS 4.4 4.4 3.7 4.0CEE 3.5 3.7 2.6 3.4Turkey 8.9 8.2 2.5 4.0Austria 2.3 3.1 0.3 1.3Eurozone 1.8 1.5 -0.5 1.1USA 3.0 1.7 2.0 1.0Source: Thomson Reuters, Raiffeisen RESEARCH

Private consumption (% yoy)

Countries 2010 2011 2012e 2013fPoland 3.2 3.4 2.3 3.0Hungary -2.3 0.0 0.0 0.5Czech Rep. 0.6 -0.5 -1.0 0.8Slovakia -0.8 -0.4 0.0 1.2Slovenia -0.6 -0.2 0.0 1.0CE 1.3 1.6 1.0 1.9Croatia -0.9 0.2 -0.8 1.0Bulgaria 0.6 -0.2 0.2 3.5Romania -0.4 1.4 0.6 2.0Serbia n.a. n.a. n.a. n.a.Bosnia a. H. -1.3 2.5 -0.5 2.5Albania n.a. n.a. n.a. n.a.SEE -0.3 0.8 0.2 1.8Russia 5.1 6.4 5.5 6.0Ukraine 6.7 12.2 7.0 4.9Belarus 10.2 n.a. n.a. n.a.CIS 5.4 6.7 5.5 5.7CEE 3.6 4.5 3.6 4.2Turkey 6.7 7.7 3.7 4.0Austria 2.2 0.6 0.9 1.3Eurozone 0.8 0.2 -0.3 0.8USA 2.0 2.2 1.8 1.2Source: Thomson Reuters, Raiffeisen RESEARCH

Consumer prices (avg, % yoy)

Countries 2010 2011 2012e 2013fPoland 2.6 4.3 3.9 2.5Hungary 4.9 3.9 5.5 3.5Czech Rep. 1.5 1.9 3.0 2.2Slovakia 1.0 3.9 3.0 2.5Slovenia 1.8 1.8 2.2 2.0CE 2.5 3.6 3.8 2.5Croatia 1.1 2.3 2.5 3.0Bulgaria 2.4 4.2 2.7 3.1Romania 6.1 5.8 3.0 3.6Serbia 6.5 11.0 6.5 6.0Bosnia a. H. 2.1 3.7 2.2 2.0Albania 4.0 3.5 3.0 3.5SEE 4.5 5.4 3.2 3.6Russia 6.9 8.5 6.0 6.9Ukraine 9.4 8.0 4.2 8.5Belarus 7.7 53.2 60.0 23.0CIS 7.1 9.7 7.4 7.5CEE 5.5 7.4 5.9 5.6Turkey 8.6 6.5 9.5 6.5Austria 1.7 3.6 2.3 2.0Eurozone 1.6 2.7 2.2 1.8USA 1.6 3.2 2.1 1.5Source: Thomson Reuters, Raiffeisen RESEARCH

Current account balance (% of GDP)

Countries 2010 2011 2012e 2013fPoland -4.1 -3.9 -3.8 -3.1Hungary 1.1 1.6 1.8 1.0Czech Rep. -3.9 -2.9 -2.2 -2.3Slovakia -2.5 0.2 1.4 2.0Slovenia -0.8 -0.5 -0.6 -1.1CE -3.0 -2.4 -2.1 -1.8Croatia -1.2 0.3 0.3 0.9Bulgaria -1.3 1.9 1.6 0.9Romania -4.4 -4.2 -4.0 -4.2Serbia -7.4 -8.9 -7.4 -7.3Bosnia a. H. -5.3 -8.1 -6.6 -8.1Albania -10.3 -11.5 -10.6 -9.6SEE -4.0 -3.6 -3.3 -3.4Russia 6.1 5.5 2.8 0.9Ukraine -2.2 -5.5 -4.1 -4.1Belarus -15.1 -9.7 -12.9 -13.8CIS 4.7 4.2 1.9 0.2CEE 1.3 1.4 0.2 -0.7Turkey -6.6 -10.2 -8.4 -7.8Austria 3.0 1.9 2.6 2.6Eurozone -0.5 -0.3 -0.2 -0.4USA -3.2 -3.1 -2.9 -2.8Source: Thomson Reuters, Raiffeisen RESEARCH

Forecasts

General budget balance (% of GDP)

Countries 2010 2011 2012e 2013fPoland -7.9 -5.4 -4.9 -3.4Hungary -4.2 0.0 -3.4 -3.4Czech Rep. -4.8 -4.4 -3.7 -3.4Slovakia -7.9 -5.0 -4.6 -2.8Slovenia -5.8 -6.5 -4.5 -4.0CE -6.6 -4.5 -4.4 -3.4Croatia -4.9 -5.5 -4.3 -3.5Bulgaria -4.0 -2.1 -2.2 -1.8Romania -6.8 -4.6 -3.0 -3.0Serbia -4.8 -4.5 -5.2 -4.6Bosnia a. H. -2.2 -3.0 -3.0 -2.0Albania -5.7 -3.5 -4.0 -4.0SEE -5.6 -4.3 -3.4 -3.1Russia -4.1 0.8 -1.3 -1.0Ukraine -7.5 -4.3 -3.0 -2.0Belarus -2.6 2.4 -0.5 -1.0CIS -4.3 0.4 -1.4 -1.1CEE -5.1 -1.5 -2.5 -2.0Turkey -3.7 -1.5 -3.0 -2.5Austria -4.5 -2.6 -3.1 -2.2Eurozone -6.2 -4.1 -3.4 -3.0USA -8.9 -8.7 -7.6 -3.8Source: Thomson Reuters, Raiffeisen RESEARCH

Public debt (% of GDP)

Countries 2010 2011 2012e 2013fPoland 53.4 55.9 54.2 51.9Hungary 81.3 82.7 80.7 79.9Czech Rep. 37.6 41.1 43.6 45.2Slovakia 41.0 44.4 48.2 48.8Slovenia 38.8 47.5 50.0 51.0CE 52.0 55.0 54.8 54.0Croatia 41.2 45.1 52.2 53.7Bulgaria 16.7 17.0 19.9 19.1Romania 30.5 33.4 34.3 35.0Serbia 43.2 45.8 48.0 45.0Bosnia a. H. 38.4 37.4 39.7 40.1Albania 59.5 59.6 59.6 59.4SEE 33.3 35.6 38.0 38.2Russia 9.4 10.2 12.0 13.0Ukraine 40.0 36.0 36.0 37.0Belarus 23.5 52.5 50.5 57.0CIS 12.2 13.5 15.0 16.2CEE 26.2 28.1 29.2 29.7Turkey 42.2 39.1 36.2 35.0Austria 71.9 72.2 74.8 75.2Eurozone 85.4 88.0 90.4 90.9USA 93.1 98.7 103.7 106.2Source: Thomson Reuters, Raiffeisen RESEARCH

Gross foreign debt (% of GDP)

Countries 2010 2011 2012e 2013fPoland 66.4 70.1 58.9 60.3Hungary 139.4 132.9 133.9 125.1Czech Rep. 47.9 48.9 47.4 47.9Slovakia 74.5 79.0 81.3 86.0Slovenia 114.9 116.3 116.7 115.8CE 75.8 77.4 71.3 71.2Croatia 101.3 100.7 103.6 100.7Bulgaria 102.7 92.7 88.0 79.7Romania 74.5 72.2 72.5 71.0Serbia 84.5 74.5 75.7 70.3Bosnia a. H. 58.3 58.9 61.0 60.6Albania 23.5 24.0 25.4 25.1SEE 81.7 77.8 77.9 74.8Russia 32.8 29.1 28.0 27.9Ukraine 84.9 82.2 70.4 72.9Belarus 51.3 61.5 75.7 89.3CIS 37.2 34.3 32.6 32.8CEE 54.5 51.7 48.0 47.8Turkey 39.7 46.0 42.7 41.2Austria n.a. n.a. n.a. n.a.Eurozone n.a. n.a. n.a. n.a.USA n.a. n.a. n.a. n.a.Source: Thomson Reuters, Raiffeisen RESEARCH

Exchange rate EUR/LCY (avg)

Countries 2010 2011 2012e 2013fPoland 3.99 4.11 4.14 3.94Hungary 275.5 279.3 290.5 285.0Czech Rep. 25.3 24.6 24.5 23.5Slovakia euro euro euro euroSlovenia euro euro euro euro

Croatia 7.29 7.43 7.56 7.55Bulgaria 1.96 1.96 1.96 1.96Romania 4.21 4.24 4.34 4.24Serbia 103.0 102.0 109.0 106.9Bosnia a. H. 1.96 1.96 1.96 1.96Albania 137.8 140.3 140.2 138.5

Russia 40.3 40.9 39.7 41.2Ukraine 10.54 10.92 10.89 11.57Belarus 3950 6300 11700 15200

Turkey 2.00 2.30 2.36 2.28Austria euro euro euro euro

USA 1.33 1.37 1.33 1.30Source: Thomson Reuters, Raiffeisen RESEARCH

Ratings*

Countries S&P Moody's FitchPoland A- A2 A-Hungary BB+ Ba1 BB+Czech Rep. AA- A1 A+Slovakia A A2 A+Slovenia A+ A2 A

Croatia BBB- Baa3 BBB-Bulgaria BBB Baa2 BBB-Romania BB+ Baa3 BBB-Serbia BB n.r.1 BB-Bosnia a. H. B B2 n.r.1

Albania B+ B1 n.r.1

Russia BBB Baa1 BBBUkraine B+ B2 BBelarus B- B3 n.r.1

Turkey BB Ba2 BB+Austria AA+ Aaa AAA

USA AA+ Aaa AAA* for FCY, long-term debt; 1 not ratedSource: Bloomberg, Raiffeisen RESEARCH

52nd quarter 2012

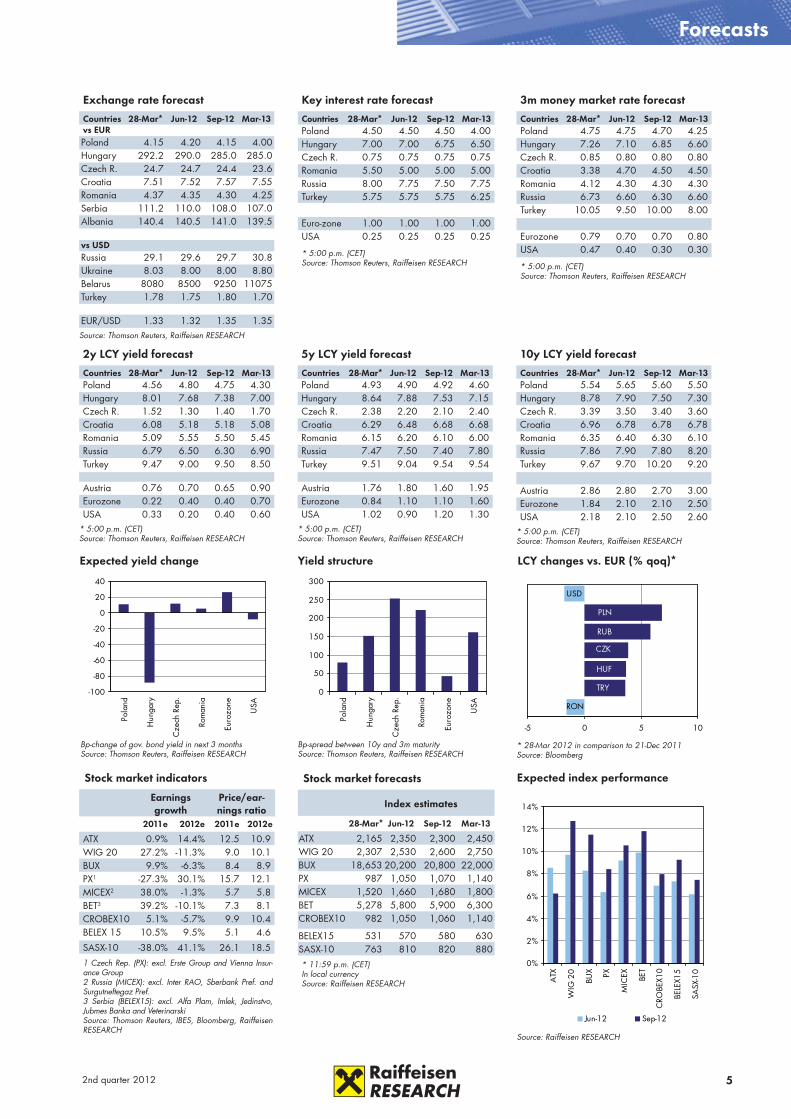

Exchange rate forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13vs EURPoland 4.15 4.20 4.15 4.00Hungary 292.2 290.0 285.0 285.0Czech R. 24.7 24.7 24.4 23.6Croatia 7.51 7.52 7.57 7.55Romania 4.37 4.35 4.30 4.25Serbia 111.2 110.0 108.0 107.0Albania 140.4 140.5 141.0 139.5

vs USDRussia 29.1 29.6 29.7 30.8Ukraine 8.03 8.00 8.00 8.80Belarus 8080 8500 9250 11075Turkey 1.78 1.75 1.80 1.70

EUR/USD 1.33 1.32 1.35 1.35Source: Thomson Reuters, Raiffeisen RESEARCH

2y LCY yield forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13Poland 4.56 4.80 4.75 4.30Hungary 8.01 7.68 7.38 7.00Czech R. 1.52 1.30 1.40 1.70Croatia 6.08 5.18 5.18 5.08Romania 5.09 5.55 5.50 5.45Russia 6.79 6.50 6.30 6.90Turkey 9.47 9.00 9.50 8.50

Austria 0.76 0.70 0.65 0.90Eurozone 0.22 0.40 0.40 0.70USA 0.33 0.20 0.40 0.60

* 5:00 p.m. (CET)Source: Thomson Reuters, Raiffeisen RESEARCH

Key interest rate forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13Poland 4.50 4.50 4.50 4.00Hungary 7.00 7.00 6.75 6.50Czech R. 0.75 0.75 0.75 0.75Romania 5.50 5.00 5.00 5.00Russia 8.00 7.75 7.50 7.75Turkey 5.75 5.75 5.75 6.25

Euro-zone 1.00 1.00 1.00 1.00USA 0.25 0.25 0.25 0.25

* 5:00 p.m. (CET)Source: Thomson Reuters, Raiffeisen RESEARCH

Forecasts

3m money market rate forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13Poland 4.75 4.75 4.70 4.25Hungary 7.26 7.10 6.85 6.60Czech R. 0.85 0.80 0.80 0.80Croatia 3.38 4.70 4.50 4.50Romania 4.12 4.30 4.30 4.30Russia 6.73 6.60 6.30 6.60Turkey 10.05 9.50 10.00 8.00

Eurozone 0.79 0.70 0.70 0.80USA 0.47 0.40 0.30 0.30

* 5:00 p.m. (CET)Source: Thomson Reuters, Raiffeisen RESEARCH

5y LCY yield forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13Poland 4.93 4.90 4.92 4.60Hungary 8.64 7.88 7.53 7.15Czech R. 2.38 2.20 2.10 2.40Croatia 6.29 6.48 6.68 6.68Romania 6.15 6.20 6.10 6.00Russia 7.47 7.50 7.40 7.80Turkey 9.51 9.04 9.54 9.54

Austria 1.76 1.80 1.60 1.95Eurozone 0.84 1.10 1.10 1.60USA 1.02 0.90 1.20 1.30

* 5:00 p.m. (CET)Source: Thomson Reuters, Raiffeisen RESEARCH

10y LCY yield forecast

Countries 28-Mar* Jun-12 Sep-12 Mar-13Poland 5.54 5.65 5.60 5.50Hungary 8.78 7.90 7.50 7.30Czech R. 3.39 3.50 3.40 3.60Croatia 6.96 6.78 6.78 6.78Romania 6.35 6.40 6.30 6.10Russia 7.86 7.90 7.80 8.20Turkey 9.67 9.70 10.20 9.20

Austria 2.86 2.80 2.70 3.00Eurozone 1.84 2.10 2.10 2.50USA 2.18 2.10 2.50 2.60

* 5:00 p.m. (CET)Source: Thomson Reuters, Raiffeisen RESEARCH

Yield structure

Bp-spread between 10y and 3m maturitySource: Thomson Reuters, Raiffeisen RESEARCH

0

50

100

150

200

250

300

Pola

nd

Hun

gary

Cze

ch R

ep.

Rom

ania

Euro

zone

USA

LCY changes vs. EUR (% qoq)*

* 28-Mar 2012 in comparison to 21-Dec 2011Source: Bloomberg

RON

TRY

HUF

CZK

RUB

PLN

USD

-5 0 5 10

Expected yield change

Bp-change of gov. bond yield in next 3 monthsSource: Thomson Reuters, Raiffeisen RESEARCH

-100

-80

-60

-40

-20

0

20

40

Pola

nd

Hun

gary

Cze

ch R

ep.

Rom

ania

Euro

zone

USA

Expected index performance

Source: Raiffeisen RESEARCH

0%

2%

4%

6%

8%

10%

12%

14%

ATX

WIG

20

BUX PX

MIC

EX BET

CRO

BEX1

0

BELE

X15

SASX

-10

Jun-12 Sep-12

Stock market indicators

Earnings growth

Price/ear-nings ratio

2011e 2012e 2011e 2012e

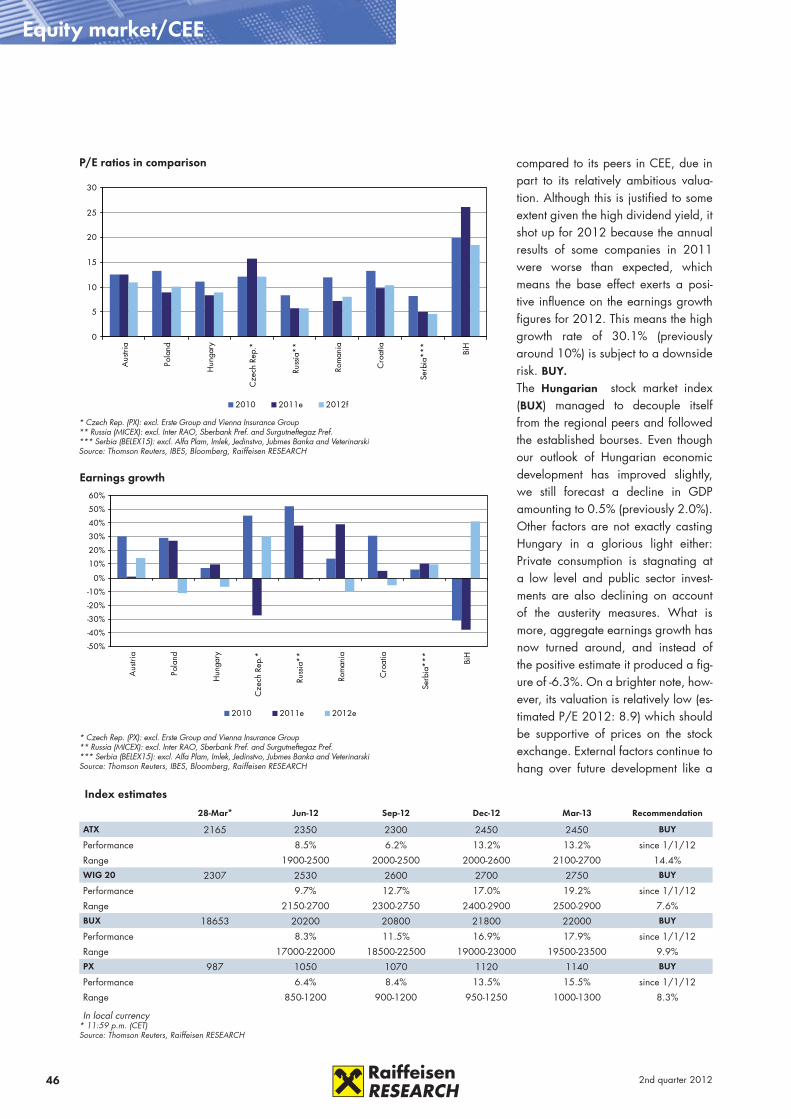

ATX 0.9% 14.4% 12.5 10.9 WIG 20 27.2% -11.3% 9.0 10.1 BUX 9.9% -6.3% 8.4 8.9 PX1 -27.3% 30.1% 15.7 12.1 MICEX2 38.0% -1.3% 5.7 5.8 BET3 39.2% -10.1% 7.3 8.1 CROBEX10 5.1% -5.7% 9.9 10.4 BELEX 15 10.5% 9.5% 5.1 4.6

SASX-10 -38.0% 41.1% 26.1 18.5 1 Czech Rep. (PX): excl. Erste Group and Vienna Insur-ance Group2 Russia (MICEX): excl. Inter RAO, Sberbank Pref. and Surgutneftegaz Pref.3 Serbia (BELEX15): excl. Alfa Plam, Imlek, Jedinstvo, Jubmes Banka and VeterinarskiSource: Thomson Reuters, IBES, Bloomberg, Raiffeisen RESEARCH

Stock market forecasts

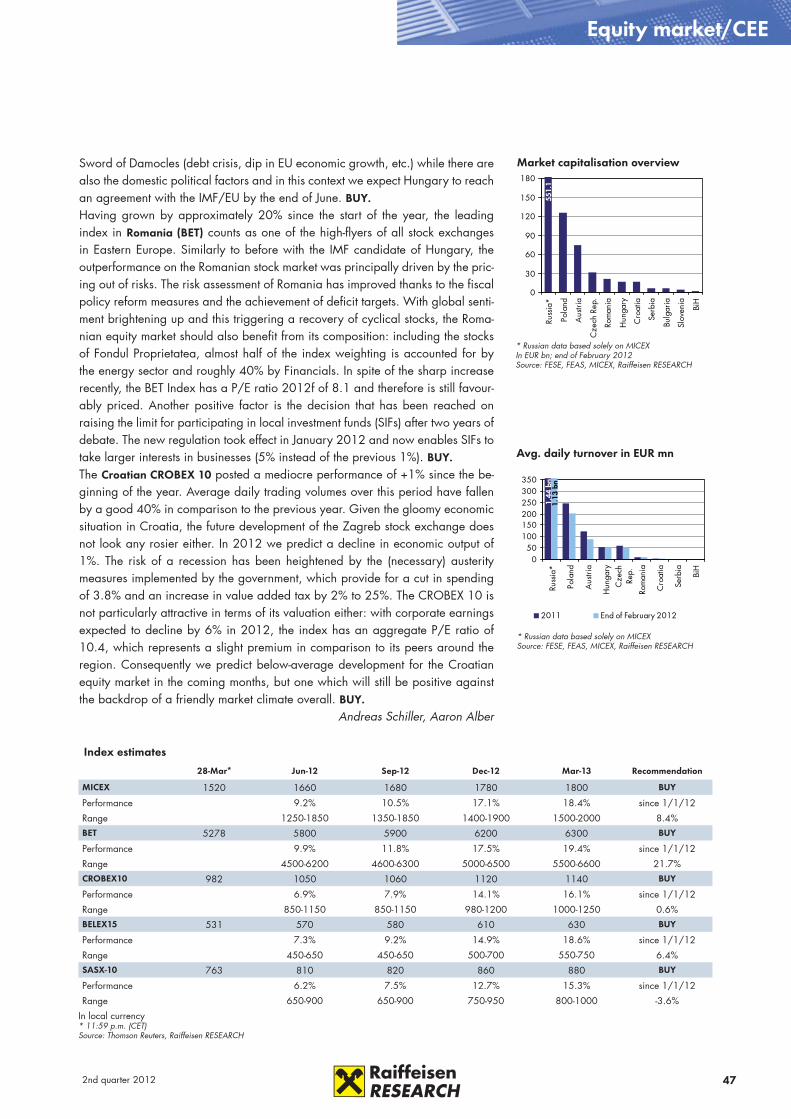

Index estimates

28-Mar* Jun-12 Sep-12 Mar-13

ATX 2,165 2,350 2,300 2,450WIG 20 2,307 2,530 2,600 2,750BUX 18,653 20,200 20,800 22,000PX 987 1,050 1,070 1,140MICEX 1,520 1,660 1,680 1,800BET 5,278 5,800 5,900 6,300CROBEX10 982 1,050 1,060 1,140

BELEX15 531 570 580 630SASX-10 763 810 820 880* 11:59 p.m. (CET)In local currencySource: Raiffeisen RESEARCH

6 2nd quarter 2012

Forecasts

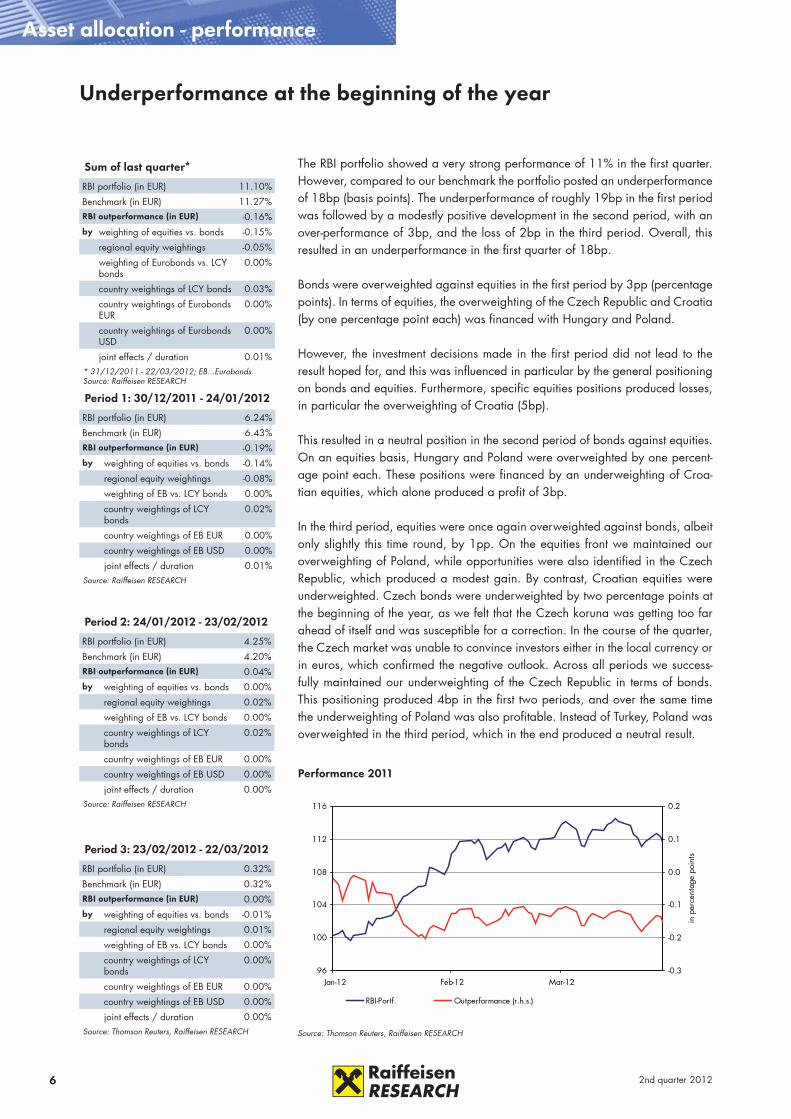

Sum of last quarter*

RBI portfolio (in EUR) 11.10%

Benchmark (in EUR) 11.27%RBI outperformance (in EUR) -0.16%by weighting of equities vs. bonds -0.15%

regional equity weightings -0.05%

weighting of Eurobonds vs. LCY bonds

0.00%

country weightings of LCY bonds 0.03%

country weightings of Eurobonds EUR

0.00%

country weightings of Eurobonds USD

0.00%

joint effects / duration 0.01%* 31/12/2011 - 22/03/2012; EB...EurobondsSource: Raiffeisen RESEARCH

The RBI portfolio showed a very strong performance of 11% in the first quarter. However, compared to our benchmark the portfolio posted an underperformance of 18bp (basis points). The underperformance of roughly 19bp in the first period was followed by a modestly positive development in the second period, with an over-performance of 3bp, and the loss of 2bp in the third period. Overall, this resulted in an underperformance in the first quarter of 18bp.

Bonds were overweighted against equities in the first period by 3pp (percentage points). In terms of equities, the overweighting of the Czech Republic and Croatia (by one percentage point each) was financed with Hungary and Poland.

However, the investment decisions made in the first period did not lead to the result hoped for, and this was influenced in particular by the general positioning on bonds and equities. Furthermore, specific equities positions produced losses, in particular the overweighting of Croatia (5bp).

This resulted in a neutral position in the second period of bonds against equities. On an equities basis, Hungary and Poland were overweighted by one percent-age point each. These positions were financed by an underweighting of Croa-tian equities, which alone produced a profit of 3bp.

In the third period, equities were once again overweighted against bonds, albeit only slightly this time round, by 1pp. On the equities front we maintained our overweighting of Poland, while opportunities were also identified in the Czech Republic, which produced a modest gain. By contrast, Croatian equities were underweighted. Czech bonds were underweighted by two percentage points at the beginning of the year, as we felt that the Czech koruna was getting too far ahead of itself and was susceptible for a correction. In the course of the quarter, the Czech market was unable to convince investors either in the local currency or in euros, which confirmed the negative outlook. Across all periods we success-fully maintained our underweighting of the Czech Republic in terms of bonds. This positioning produced 4bp in the first two periods, and over the same time the underweighting of Poland was also profitable. Instead of Turkey, Poland was overweighted in the third period, which in the end produced a neutral result.

Underperformance at the beginning of the year

Period 1: 30/12/2011 - 24/01/2012

RBI portfolio (in EUR) 6.24%

Benchmark (in EUR) 6.43%RBI outperformance (in EUR) -0.19%by weighting of equities vs. bonds -0.14%

regional equity weightings -0.08%

weighting of EB vs. LCY bonds 0.00%

country weightings of LCY bonds

0.02%

country weightings of EB EUR 0.00%

country weightings of EB USD 0.00%

joint effects / duration 0.01%Source: Raiffeisen RESEARCH

Period 2: 24/01/2012 - 23/02/2012

RBI portfolio (in EUR) 4.25%

Benchmark (in EUR) 4.20%RBI outperformance (in EUR) 0.04%by weighting of equities vs. bonds 0.00%

regional equity weightings 0.02%

weighting of EB vs. LCY bonds 0.00%

country weightings of LCY bonds

0.02%

country weightings of EB EUR 0.00%

country weightings of EB USD 0.00%

joint effects / duration 0.00%Source: Raiffeisen RESEARCH

Period 3: 23/02/2012 - 22/03/2012

RBI portfolio (in EUR) 0.32%

Benchmark (in EUR) 0.32%RBI outperformance (in EUR) 0.00%by weighting of equities vs. bonds -0.01%

regional equity weightings 0.01%

weighting of EB vs. LCY bonds 0.00%

country weightings of LCY bonds

0.00%

country weightings of EB EUR 0.00%

country weightings of EB USD 0.00%

joint effects / duration 0.00%Source: Thomson Reuters, Raiffeisen RESEARCH

96

100

104

108

112

116

Jan-12 Feb-12 Mar-12-0.3

-0.2

-0.1

0.0

0.1

0.2

in p

erce

ntag

e po

ints

RBI-Portf. Outperformance (r.h.s.)

Performance 2011

Source: Thomson Reuters, Raiffeisen RESEARCH

Asset allocation - performance

72nd quarter 2012

xxAsset allocation - total portfolio

It does not seem as if the European sovereign debt crisis will pass through to core countries in Eastern Europe for now. The intervention by the European Central Bank offering the European banking system better access to liquidity seems to have borne fruit. The yield spreads of (almost) all countries at risk on the Euro-pean periphery to German Bunds have fallen drastically during the last quarter. European banks have presumably used part of the extra liquidity provided under favourable conditions to buy (euro) government bonds. This also means that one of the main risk factors has been averted – namely a collapse of the European banking system followed by a massive deleveraging process and the resultant tur-moil in the economies of CEE. This scenario was rated extremely likely by many investors, and penalised by massive sales of equities and government bonds from the CEE region. Many Eastern European currencies were also badly affected by this veritable sell-off.

Since the end of January though, CEE has experienced a significant recovery. Some of the main contributors to performance for euro investors were the stronger currencies in particular. For the coming quarter we assume that the upbeat eco-nomic activity will continue in broad parts of the CEE region, and we have identi-fied additional potential particularly on the equities markets, which are still trad-ing at a discount by international comparison. Most of the currencies in Eastern Europe, which in the past have been responsible for significant volatility in the CEE portfolio, should also stabilise (or even appreciate) in the course of the year. These factors have prompted us to overweight equities over bonds in our CEE portfolio by three percentage points.

Mario Annau

Improved outlook in CEE

Historical volatility & performance (in %)

Equities* BondsVolatility Performance Volatility Performance

Countries EUR LCY EUR LCY EUR LCY EUR LCY

Czech Republic 21.1% 18.8% 7.8% 4.3% 8.1% 4.0% 5.5% 2.1%

Hungary 30.9% 23.1% 20.6% 12.1% 18.2% 8.0% 12.6% 4.7%

Poland 20.2% 13.9% 15.2% 7.7% 10.1% 2.0% 9.7% 2.5%

Romania 19.0% 18.7% 19.7% 21.0% 2.9% 1.5% -0.4% 0.7%

Russia 21.6% 19.4% 16.2% 10.2% 7.6% 2.0% 11.2% 4.1%

Turkey - - - - 9.8% 3.1% 7.9% 4.3%

Croatia 5.3% 5.3% -11.6% -11.8% 3.0% 3.0% 6.0% 6.0%

CEE 18.1% - 0.0% - 7.2% - 8.9% -* MSCI indicesVolatility in EUR; 3 months volatility annualised; ytd performance in EURLCY…local currencySource: Thomson Reuters, Raiffeisen RESEARCH

CEE portfolio weightings Q2 2012

LCY…local currencySource: Raiffeisen RESEARCH

Risk-return (in %)

In local currencySource: Thomson Reuters, Raiffeisen RESEARCH

European sovereign debt crisis (seems to be) averted for now Further potential for recovery Equities overweighted versus bonds

Equities: 53% [3 pp]

LCY-bonds: 37.6% [-2.4 pp]

EB EUR: 4,7% [-0,3 pp]

EB USD: 4,7% [-0,3 pp]

DJ Euro-stoxx

CEE

Poland

Czech Republic

Russia

HungaryDow Jones

Romania

0

5

10

15

20

25

15 20 25 30 35

Historic 1y volatility in %

Hist

oric

ytd

per

form

ance

in %

8 2nd quarter 2012

Forecasts

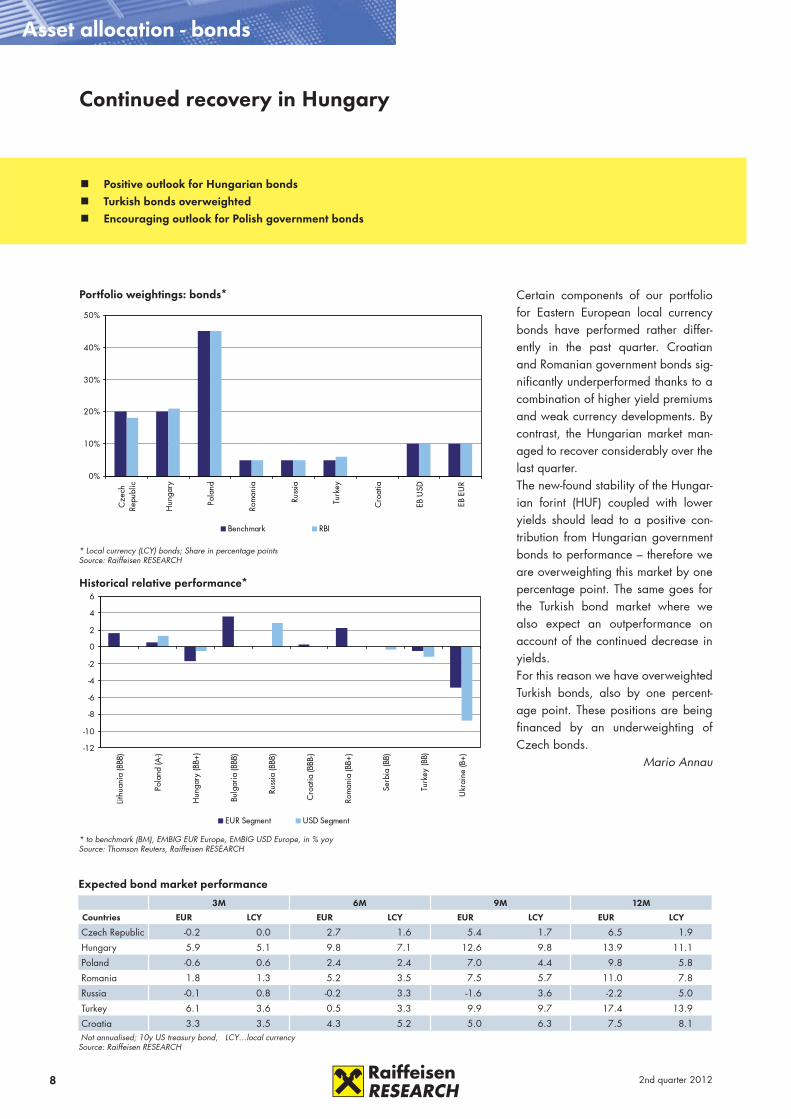

Certain components of our portfolio for Eastern European local currency bonds have performed rather differ-ently in the past quarter. Croatian and Romanian government bonds sig-nificantly underperformed thanks to a combination of higher yield premiums and weak currency developments. By contrast, the Hungarian market man-aged to recover considerably over the last quarter.The new-found stability of the Hungar-ian forint (HUF) coupled with lower yields should lead to a positive con-tribution from Hungarian government bonds to performance – therefore we are overweighting this market by one percentage point. The same goes for the Turkish bond market where we also expect an outperformance on account of the continued decrease in yields. For this reason we have overweighted Turkish bonds, also by one percent-age point. These positions are being financed by an underweighting of Czech bonds.

Mario Annau

Continued recovery in Hungary

Asset allocation - bonds

Expected bond market performance

3M 6M 9M 12M

Countries EUR LCY EUR LCY EUR LCY EUR LCY

Czech Republic -0.2 0.0 2.7 1.6 5.4 1.7 6.5 1.9

Hungary 5.9 5.1 9.8 7.1 12.6 9.8 13.9 11.1

Poland -0.6 0.6 2.4 2.4 7.0 4.4 9.8 5.8

Romania 1.8 1.3 5.2 3.5 7.5 5.7 11.0 7.8

Russia -0.1 0.8 -0.2 3.3 -1.6 3.6 -2.2 5.0

Turkey 6.1 3.6 0.5 3.3 9.9 9.7 17.4 13.9

Croatia 3.3 3.5 4.3 5.2 5.0 6.3 7.5 8.1 Not annualised; 10y US treasury bond, LCY…local currencySource: Raiffeisen RESEARCH

-12

-10

-8

-6

-4

-2

0

2

4

6

Lithu

ania

(BBB

)

Pola

nd (A

-)

Hun

gary

(BB+

)

Bulg

aria

(BBB

)

Russ

ia (B

BB)

Cro

atia

(BBB

-)

Rom

ania

(BB+

)

Serb

ia (B

B)

Turk

ey (B

B)

Ukr

aine

(B+)

EUR Segment USD Segment

Historical relative performance*

* to benchmark (BM), EMBIG EUR Europe, EMBIG USD Europe, in % yoySource: Thomson Reuters, Raiffeisen RESEARCH

0%

10%

20%

30%

40%

50%

Cze

chRe

publ

ic

Hun

gary

Pola

nd

Rom

ania

Russ

ia

Turk

ey

Cro

atia

EB U

SD

EB E

UR

Benchmark RBI

Portfolio weightings: bonds*

* Local currency (LCY) bonds; Share in percentage pointsSource: Raiffeisen RESEARCH

Positive outlook for Hungarian bonds Turkish bonds overweighted Encouraging outlook for Polish government bonds

92nd quarter 2012

xxAsset allocation - equities

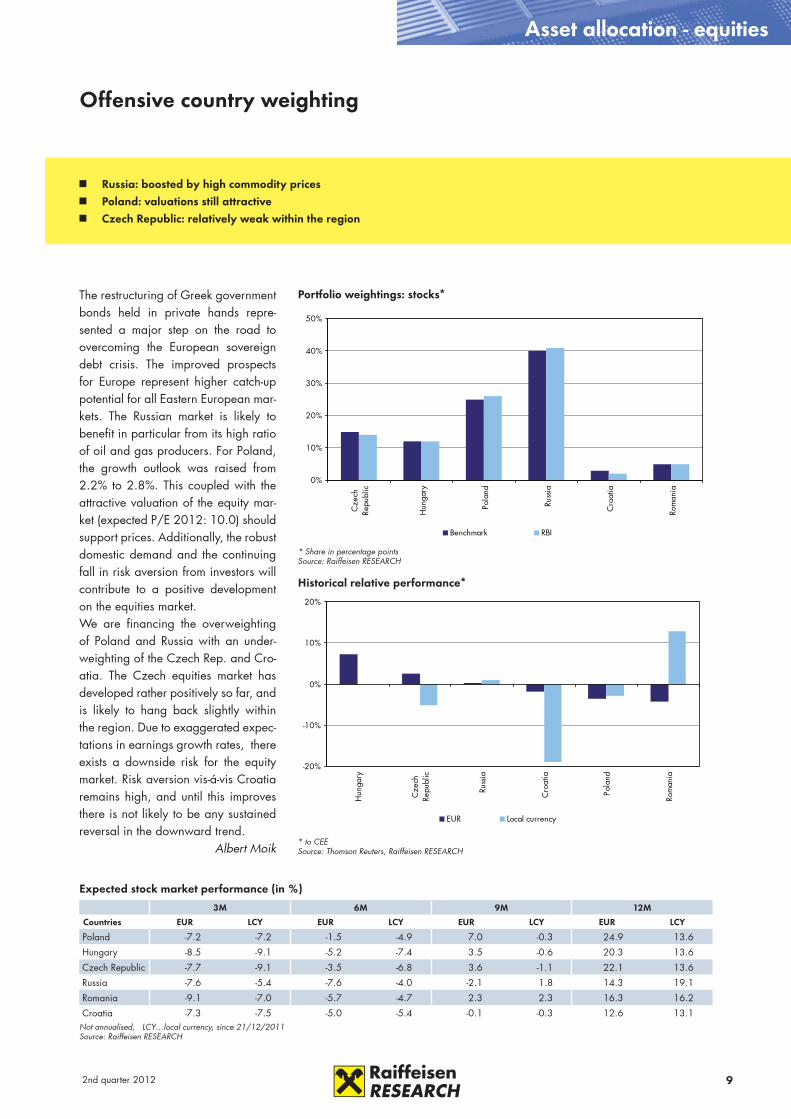

Offensive country weighting

Russia: boosted by high commodity prices Poland: valuations still attractive Czech Republic: relatively weak within the region

Expected stock market performance (in %)

3M 6M 9M 12M

Countries EUR LCY EUR LCY EUR LCY EUR LCY

Poland -7.2 -7.2 -1.5 -4.9 7.0 -0.3 24.9 13.6

Hungary -8.5 -9.1 -5.2 -7.4 3.5 -0.6 20.3 13.6

Czech Republic -7.7 -9.1 -3.5 -6.8 3.6 -1.1 22.1 13.6

Russia -7.6 -5.4 -7.6 -4.0 -2.1 1.8 14.3 19.1

Romania -9.1 -7.0 -5.7 -4.7 2.3 2.3 16.3 16.2

Croatia -7.3 -7.5 -5.0 -5.4 -0.1 -0.3 12.6 13.1Not annualised, LCY…local currency, since 21/12/2011Source: Raiffeisen RESEARCH

-20%

-10%

0%

10%

20%

Hun

gary

Cze

chRe

publ

ic

Russ

ia

Cro

atia

Pola

nd

Rom

ania

EUR Local currency

Historical relative performance*

* to CEESource: Thomson Reuters, Raiffeisen RESEARCH

0%

10%

20%

30%

40%

50%

Cze

chRe

publ

ic

Hun

gary

Pola

nd

Russ

ia

Cro

atia

Rom

ania

Benchmark RBI

Portfolio weightings: stocks*

* Share in percentage pointsSource: Raiffeisen RESEARCH

The restructuring of Greek government bonds held in private hands repre-sented a major step on the road to overcoming the European sovereign debt crisis. The improved prospects for Europe represent higher catch-up potential for all Eastern European mar-kets. The Russian market is likely to benefit in particular from its high ratio of oil and gas producers. For Poland, the growth outlook was raised from 2.2% to 2.8%. This coupled with the attractive valuation of the equity mar-ket (expected P/E 2012: 10.0) should support prices. Additionally, the robust domestic demand and the continuing fall in risk aversion from investors will contribute to a positive development on the equities market. We are financing the overweighting of Poland and Russia with an under-weighting of the Czech Rep. and Cro-atia. The Czech equities market has developed rather positively so far, and is likely to hang back slightly within the region. Due to exaggerated expec-tations in earnings growth rates, there exists a downside risk for the equity market. Risk aversion vis-á-vis Croatia remains high, and until this improves there is not likely to be any sustained reversal in the downward trend.

Albert Moik

10 2nd quarter 2012

Forecasts

The most recent economic indicators confirm our expectations of an economic slowdown, but at the same time the data indicates that our initial expectations of the extent of this downturn where a touch too negative. Even though we continue to expect slower growth into 2012, the recession should be a lighter one. In the following special we want to shed some light on why we have revised our eco-nomic expectations for CEE and especially for the CE region upwards. Why we expect the SEE region to remain rather subdued compared to CEE, and last but not least, we want to give a brief outlook of what to expect from the whole region in 2012.

Looking at high frequency indicators such as PMI manufacturing or economic sen-timent it seems that the negative expectations bottomed out at the end of 2011. There are clear signs of an improvement and thus we decided to increase our growth expectations for the Eurozone in 2012 from -1.0% to -0.5%. The increase in the economic growth outlook for Germany was crucially important (where we now expect stagnation rather than a recession) as it is the main trading partner for the CE countries. Germany accounts for 20-30% of total exports in the small open economies of the CE region and is by far the biggest export market. With the export sector currently the only source of growth, this importance cannot be stressed enough. This is one of our main arguments underpinning the improve-ment, especially in the CE GDP outlook.

CELooking at our growth expectations for the CE region it might seem as if the entire region will grow solidly in 2012, but we need to differentiate strongly between the different countries in the region. While Poland can rely on relatively strong do-mestic demand, solid investment growth besides the export sector, and it has less severe cuts in government spending to cope with, the story looks very different for the remaining CE countries. Rising unemployment rates are dampening domestic demand with Hungary and Slovenia probably suffering the most in 2012, while the Czech Republic and Slovakia are not likely to witness any stronger domestic demand recovery either. Looking at gross fixed capital formation (GFCF) the story is similar: Poland fell the least and recovered well from early 2010, as did Slova-kia to some extent. Hungary and Slovenia, however, are not showing comparable improvements in the same time-frame, and are unlikely to do so in 2012. That said, the growth projections in 2012 for Poland are solid, with Slovakia also likely to gain some momentum, especially in H2. The Czech Republic, however, should only see flat economic development due to the weak domestic demand and restric-tive fiscal policy. The downside potential seems to be the highest in Hungary and Slovenia, where only the export sector should prevent a deeper recession.

CEE growth revision – where is growth coming from?

Special - External debt in CEE

Household consumption (% yoy)

3-month moving averageSource: Central banks

Gross fixed capital formation (% yoy)

Government consumption (% yoy)

3-month moving averageSource: Central banks

3-month moving averageSource: Central banks

-8-6-4-202468

1012

Q3

2002

Q3

2003

Q3

2004

Q3

2005

Q3

2006

Q3

2007

Q3

2008

Q3

2009

Q3

2010

Q3

2011

Slovakia Poland HungaryCzech Rep. Slovenia

-30-25-20-15-10

-505

10152025

Q3

2002

Q3

2003

Q3

2004

Q3

2005

Q3

2006

Q3

2007

Q3

2008

Q3

2009

Q3

2010

Q3

2011

Slovakia Poland HungarySlovenia Czech Rep.

-8-6-4-202468

101214

Q3

2002

Q3

2003

Q3

2004

Q3

2005

Q3

2006

Q3

2007

Q3

2008

Q3

2009

Q3

2010

Q3

2011

Slovakia Poland HungaryCzech Rep. Slovenia

CE economy will remain export driven and profit most from the upward revision of the Eurozone SEE economies to show stagnation as domestic demand will remain subdued and main export partners are the troubled

southern Eurozone countries CIS to continue strongest economic performance, driven by high oil and commodity prices

112nd quarter 2012

xxSpecial - External debt in CEE

Household consumption (% yoy)

3-month moving averageSource: Central banks

Government consumption (% yoy)

Gross fixed capital formation (% yoy)

3-month moving averageSource: Central banks

3-month moving averageSource: Central banks

SEEWhile we have revised the GDP forecast for the CE region up considerably on the back of the improved outlook in the Eurozone, the SEE region remains more or less flat compared to our earlier expectations from Q1 2012. SEE has far fewer export ties to the stronger performing northern Eurozone countries (such as Ger-many) which have been revised upwards, but far more export links to troubled Eurozone countries in the south, such as Italy. Therefore, the region will continue to have to deal with the full blow of the Eurozone debt crisis via the export sector. Do-mestic demand has seen a comparable decline to most countries of the CE region after the financial crisis, household consumption as a pillar for economic growth has deteriorated considerably, and is not likely to improve in 2012 given the high unemployment and ongoing austerity. Government consumption will also remain hamstrung given the need of further austerity measures to reduce the budget defi-cits. GFCF did show some improvement according to the latest data, but the rate of improvement should remain low in 2012. Adding all this up the SEE region is profiting less from the upward revision of GDP in the northern Eurozone member states, and instead will have to deal with the pessimistic outlooks in the southern Eurozone member states. Therefore, we only expect stagnation in economic de-velopment in 2012.

CISCIS remains one of the best performing regions, where we expect the stronger development to last in 2012. While we were already rather optimistic on CIS before our last GDP revision, the latest economic indicators along with rising oil and commodity prices via the global economic recovery indicate that the region will grow even more strongly in 2012. Therefore, we have increased our GDP estimates from 3.1% to 3.7%. A vast portfolio of export partners as well as their commodity-driven economies have a positive impact on the region. The high oil price is currently supported by global growth, and hence Russia should continue to withstand the troubles surrounding the Eurozone. The Ukrainian as well as Be-larusian economies have closer ties to the Russian economy than to the Eurozone, shielding these economies to some extent from the slowing economic growth in the Eurozone.

All told, the economic indicators are stabilising in CEE, even though we predict the recession will get worse in H1 2012 before we see some improvement in the second half of 2012. However, a lot of these expectations depend on the export sector as the main source of growth in 2012 and therefore on the ability of the Eu-rozone to regain its growth momentum. Domestic as well as government demand will remain weak throughout almost the entire CEE region, with a few exceptions. Attracting investments into CEE will be the main objective to support the export-driven growth, but the success of this task will most likely be as varied across the different countries as their current economic situations.

Wolfgang Ernst

-20-15-10

-505

10152025

Q3

2005

Q2

2006

Q1

2007

Q4

2007

Q3

2008

Q2

2009

Q1

2010

Q4

2010

Q3

2011

Romania Croatia BulgariaRussia Ukraine

F t

-20-15-10

-505

10152025

Q3

2005

Q2

2006

Q1

2007

Q4

2007

Q3

2008

Q2

2009

Q1

2010

Q4

2010

Q3

2011

Croatia Bulgaria RomaniaRussia Ukraine

-70-60-50-40-30-20-10

010203040

Q3

2005

Q2

2006

Q1

2007

Q4

2007

Q3

2008

Q2

2009

Q1

2010

Q4

2010

Q3

2011

Romania Bulgaria CroatiaRussia Ukraine

12 2nd quarter 2012

Forecasts

The dark storm clouds that gathered over the Austrian economy in the autumn held nothing more than a brief rain shower. Although real gross domestic product contracted in the fourth quarter of 2011 compared to the previous quarter (-0.1% qoq), the feared sharp decline is now not likely to come.

The looming slowdown in international economic activity became apparent rela-tively early. Crucial leading indicators for example (purchasing manager index for manufacturing and the economic sentiment index of the European Commission) reached their cyclical highs in early 2011 before starting to head sharply down-wards. However, the situation stabilised again in the autumn. This gloomier pic-ture was also reflected in hard economic data, with real GDP growth in the third quarter of 2011 amounting to just 0.2% qoq (Q1: +0.9% qoq, Q2: +0.5% qoq). This means the impressive annual growth rate of 3.1% yoy in 2011 is largely attributable to the positive developments in the first two quarters. Exports were strong in this respect, along with investment activity to a slightly lesser extent. The latter proved to be comparatively robust in Q3 and Q4 2011, whereas exports contracted in both of these three-month periods.

The Austrian economy is set to weaken in the first quarter of this year as well, but then the worst part should be over. This is because the remaining quarters should post positive, although not stunning rates of growth, resulting in an expected growth rate of real GDP in 2012 of +0.3% yoy. For the following year (2013) we expect real GDP growth of +1.3% yoy.

Investments and external trade should be a drag on economic activity in the first quarter, though investments are likely to contract to a lesser extent. This is because confidence in industry has already moved far away from its cyclical low recorded in November. What is more, capacity utilisation has stabilised slightly below its

long-term average. While private con-sumption did not weaken in the sec-ond half of the year, it was not overly dynamic either. Retail sales have been rather unsatisfactory of late, while consumer confidence is currently also at a low level. But if we manage to avoid any unexpected inflation hikes – resulting from a higher than expected oil price for example –, private con-sumption should gain some momentum in the course of the year. This view is supported not least by the low unem-ployment rate and the encouraging employment trends.

Slowdown, but no setback

Austria

Inflation has already peaked

Source: Thomson Reuters, Statistics Austria, Raiffeisen RESEARCH

Industrial sector bottomed out

Source: Thomson Reuters, Raiffeisen RESEARCH

Key economic figures and forecasts

2010 2011 2012e 2013fReal GDP (% yoy) 2.3 3.1 0.3 1.3

Private consumption (% yoy) 2.2 0.6 0.9 1.3

Gross fixed capital formation (% yoy) 0.1 5.7 1.1 2.2

Nominal exports (% yoy) 10.1 10.5 1.8 5.7

Nominal imports (% yoy) 9.8 10.8 2.1 5.6

Trade balance (EUR bn) 12.3 9.0 8.7 9.3

Current account balance (EUR bn) 8.5 5.9 8.0 8.3

General budget balance (EUR bn)* -12.9 -7.8 -9.6 -7.0

General budget balance (% of GDP)* -4.5 -2.6 -3.1 -2.2

Unemployment rate (avg, %, EU definition) 4.4 4.2 4.3 4.2

Consumer prices (avg, % yoy) 1.7 3.6 2.3 2.0

Real wages (% yoy) -1.2 -1.0 0.9 0.8

Unit labour costs (% yoy) 0.0 1.3 3.4 2.3* state, provinces, municipalities and social security authoritiesSource: Statistics Austria, Thomson Reuters, Raiffeisen RESEARCH

Feared downturn in economic activity will not materialise Weak first quarter should be low point, external trade and investments to blame Inflation has already peaked, further declines likely The government’s austerity package is a first step, nothing more

-8

-6

-4

-2

0

2

4

6

8

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12

Inflation (HICP, % yoy)Inflation perception (goods of weekly use, % yoy)

-50

-40

-30

-20

-10

0

10

20

30

2001 2003 2005 2007 2009 201175

77

79

81

83

85

87

89

91

Industrial production (% yoy)Industrial confidenceCapacity utilisation (%, r.h.s.)

132nd quarter 2012

The dynamic inflation trend recorded last year has already peaked (HICP in September: +3.9% yoy). This devel-opment was driven first and foremost by transport, housing as well as res-taurants and hotels. Pressure on prices has faded noticeably since the start of the year, which is in no small part owed to the much lower contribution of transport to inflation. Consumer prices (HICP) in February, for example, in-creased by only 2.6% yoy. In spite of the elevated oil price, inflation is set to fall in the coming months as the base effects, which led to a sharp increase in the HICP in the early months of last year, expire (inflation forecast 2012: 2.3% yoy).

The recently announced measures to consolidate the budget mean that sov-ereign debt should fall from 72.2% of GDP (2011) to 70.0% of GDP (2016). Having said that, the measures total-ling EUR 27.9 bn by 2016 are subject to a high degree of uncertainty. For ex-ample, the envisaged tax agreement with Switzerland and the planned rev-enues from a financial transaction tax yet to be introduced are anything but certain. Moreover, the reform package is missing genuine structural reforms – first and foremost in the areas of pen-sions and healthcare. Such reforms are necessary, however, in order to ensure the long-term sustainability of public finances.

Matthias Reith

xxAustria

GDP: expenditure composition

Change (% yoy, in real terms) 2010 2011 2012e 2013f

Private consumption 2.2 0.6 0.9 1.3

Public consumption -0.2 2.7 0.6 0.1

Gross fixed capital formation 0.1 5.7 1.1 2.2

Equipment 4.3 8.6 2.3 4.2

Construction -2.9 2.7 0.0 0.5

Exports (broad definition) 8.3 6.7 -0.5 3.7

Imports (broad definition) 8.0 7.0 -0.2 3.5

Gross domestic product 2.3 3.1 0.3 1.3Source: Statistics Austria, Raiffeisen RESEARCH

GDP: value added by sector

Change (% yoy, in real terms) 2010 2011 2012e 2013f

Agriculture & forestry -5.5 4.1 0.0 0.0

Prod. of goods/mining 7.2 9.9 0.5 4.0

Energy/water supply 3.8 10.3 3.0 1.5

Construction -3.0 2.7 0.0 0.5

Wholesale and retail trade 3.1 0.1 1.2 1.5

Transportation -1.1 2.9 -3.0 1.0

Accom. & restaurant trade 1.8 -0.5 0.0 1.5

Information and communication -3.7 -1.5 -1.0 2.0

Credit and insurance 6.9 6.0 1.5 2.0

Property & business services -0.6 -0.1 1.5 1.5

Other economic services 5.0 2.8 1.0 1.5

Public sector 0.0 0.0 -0.1 -0.1

Healthcare, social services 0.6 1.7 0.0 0.7

Other services 1.7 0.5 0.0 0.5

Gross domestic product 2.3 3.1 0.3 1.3Source: Statistics Austria, Raiffeisen RESEARCH

Budget consolidation: Even 2016 gross debt not below 70%!

*For 2011 no breakdown into structural and cyclical budget balance available yetSource: European Commission, Ministry of Finance, Raiffeisen RESEARCH

70.0

74.4

-5

-4

-3

-2

-1

0

1

22000 2002 2004 2006 2008 2010 2012f 2014f 2016f

50

55

60

65

70

75

80

85

Structural budget balance (% GDP) Cyclical budget balance (% GDP)Gross debt (% GDP)

Governmentforecast

*

14 2nd quarter 2012

0

1

2

3

4

5

6

7

2007

2008

2009

2010

2011

2012

e

2013

f -5

-3

0

3

5

8

10

Real GDP (% yoy)Industrial output (% yoy, r.h.s.)

Real GDP (% yoy)

Source: Thomson Reuters, Raiffeisen RESEARCH

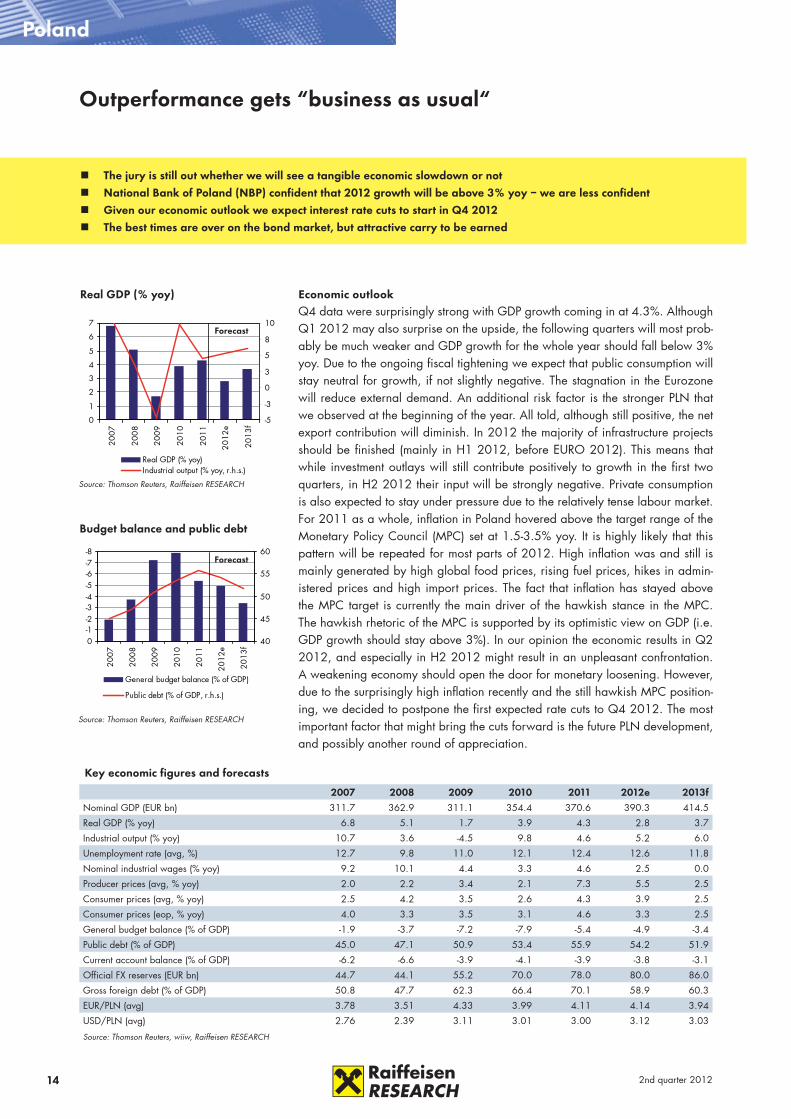

Poland

Outperformance gets “business as usual“

-8-7-6-5-4-3-2-10

2007

2008

2009

2010

2011

2012

e

2013

f 40

45

50

55

60

General budget balance (% of GDP)

Public debt (% of GDP, r.h.s.)

Budget balance and public debt

Source: Thomson Reuters, Raiffeisen RESEARCH

Forecast

Key economic figures and forecasts

2007 2008 2009 2010 2011 2012e 2013fNominal GDP (EUR bn) 311.7 362.9 311.1 354.4 370.6 390.3 414.5

Real GDP (% yoy) 6.8 5.1 1.7 3.9 4.3 2.8 3.7

Industrial output (% yoy) 10.7 3.6 -4.5 9.8 4.6 5.2 6.0

Unemployment rate (avg, %) 12.7 9.8 11.0 12.1 12.4 12.6 11.8

Nominal industrial wages (% yoy) 9.2 10.1 4.4 3.3 4.6 2.5 0.0

Producer prices (avg, % yoy) 2.0 2.2 3.4 2.1 7.3 5.5 2.5

Consumer prices (avg, % yoy) 2.5 4.2 3.5 2.6 4.3 3.9 2.5

Consumer prices (eop, % yoy) 4.0 3.3 3.5 3.1 4.6 3.3 2.5

General budget balance (% of GDP) -1.9 -3.7 -7.2 -7.9 -5.4 -4.9 -3.4

Public debt (% of GDP) 45.0 47.1 50.9 53.4 55.9 54.2 51.9

Current account balance (% of GDP) -6.2 -6.6 -3.9 -4.1 -3.9 -3.8 -3.1

Official FX reserves (EUR bn) 44.7 44.1 55.2 70.0 78.0 80.0 86.0

Gross foreign debt (% of GDP) 50.8 47.7 62.3 66.4 70.1 58.9 60.3

EUR/PLN (avg) 3.78 3.51 4.33 3.99 4.11 4.14 3.94

USD/PLN (avg) 2.76 2.39 3.11 3.01 3.00 3.12 3.03

Source: Thomson Reuters, wiiw, Raiffeisen RESEARCH

Forecast

Economic outlookQ4 data were surprisingly strong with GDP growth coming in at 4.3%. Although Q1 2012 may also surprise on the upside, the following quarters will most prob-ably be much weaker and GDP growth for the whole year should fall below 3% yoy. Due to the ongoing fiscal tightening we expect that public consumption will stay neutral for growth, if not slightly negative. The stagnation in the Eurozone will reduce external demand. An additional risk factor is the stronger PLN that we observed at the beginning of the year. All told, although still positive, the net export contribution will diminish. In 2012 the majority of infrastructure projects should be finished (mainly in H1 2012, before EURO 2012). This means that while investment outlays will still contribute positively to growth in the first two quarters, in H2 2012 their input will be strongly negative. Private consumption is also expected to stay under pressure due to the relatively tense labour market. For 2011 as a whole, inflation in Poland hovered above the target range of the Monetary Policy Council (MPC) set at 1.5-3.5% yoy. It is highly likely that this pattern will be repeated for most parts of 2012. High inflation was and still is mainly generated by high global food prices, rising fuel prices, hikes in admin-istered prices and high import prices. The fact that inflation has stayed above the MPC target is currently the main driver of the hawkish stance in the MPC. The hawkish rhetoric of the MPC is supported by its optimistic view on GDP (i.e. GDP growth should stay above 3%). In our opinion the economic results in Q2 2012, and especially in H2 2012 might result in an unpleasant confrontation. A weakening economy should open the door for monetary loosening. However, due to the surprisingly high inflation recently and the still hawkish MPC position-ing, we decided to postpone the first expected rate cuts to Q4 2012. The most important factor that might bring the cuts forward is the future PLN development, and possibly another round of appreciation.

The jury is still out whether we will see a tangible economic slowdown or not National Bank of Poland (NBP) confident that 2012 growth will be above 3% yoy – we are less confident Given our economic outlook we expect interest rate cuts to start in Q4 2012 The best times are over on the bond market, but attractive carry to be earned

152nd quarter 2012

4.5

4.8

5.0

5.3

5.5

5.8

6.0

0 1 2 3 4 5 6 7 8 9 10

Yields as of Mar-12Yield curve Mar-12Yield curve Dec-11Forecast Jun-12

3.8

3.9

4.0

4.1

4.2

4.3

4.4

4.5

Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12

EUR/PLN (end of month)

Poland

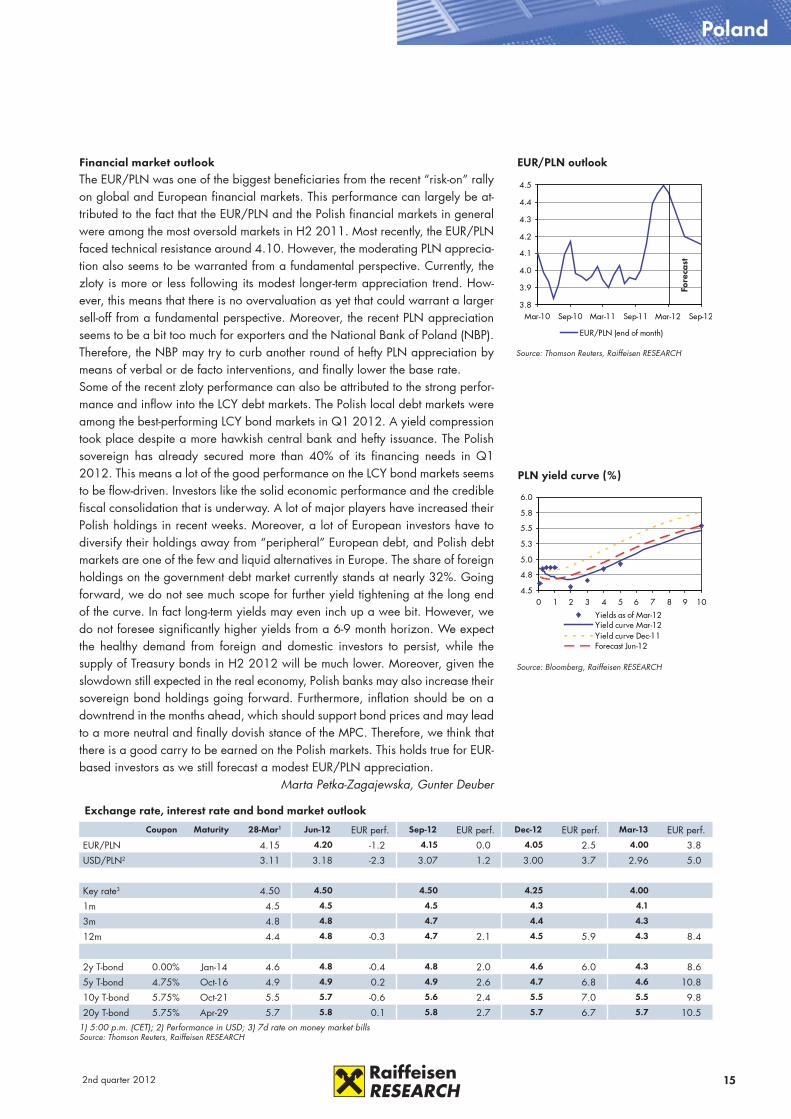

EUR/PLN outlook

Source: Thomson Reuters, Raiffeisen RESEARCH

PLN yield curve (%)

Source: Bloomberg, Raiffeisen RESEARCH

Exchange rate, interest rate and bond market outlook

Coupon Maturity 28-Mar1 Jun-12 EUR perf. Sep-12 EUR perf. Dec-12 EUR perf. Mar-13 EUR perf.

EUR/PLN 4.15 4.20 -1.2 4.15 0.0 4.05 2.5 4.00 3.8

USD/PLN2 3.11 3.18 -2.3 3.07 1.2 3.00 3.7 2.96 5.0

Key rate3 4.50 4.50 4.50 4.25 4.00

1m 4.5 4.5 4.5 4.3 4.1

3m 4.8 4.8 4.7 4.4 4.3

12m 4.4 4.8 -0.3 4.7 2.1 4.5 5.9 4.3 8.4

2y T-bond 0.00% Jan-14 4.6 4.8 -0.4 4.8 2.0 4.6 6.0 4.3 8.6

5y T-bond 4.75% Oct-16 4.9 4.9 0.2 4.9 2.6 4.7 6.8 4.6 10.8

10y T-bond 5.75% Oct-21 5.5 5.7 -0.6 5.6 2.4 5.5 7.0 5.5 9.8

20y T-bond 5.75% Apr-29 5.7 5.8 0.1 5.8 2.7 5.7 6.7 5.7 10.51) 5:00 p.m. (CET); 2) Performance in USD; 3) 7d rate on money market billsSource: Thomson Reuters, Raiffeisen RESEARCH

Fore

cast

Financial market outlookThe EUR/PLN was one of the biggest beneficiaries from the recent “risk-on” rally on global and European financial markets. This performance can largely be at-tributed to the fact that the EUR/PLN and the Polish financial markets in general were among the most oversold markets in H2 2011. Most recently, the EUR/PLN faced technical resistance around 4.10. However, the moderating PLN apprecia-tion also seems to be warranted from a fundamental perspective. Currently, the zloty is more or less following its modest longer-term appreciation trend. How-ever, this means that there is no overvaluation as yet that could warrant a larger sell-off from a fundamental perspective. Moreover, the recent PLN appreciation seems to be a bit too much for exporters and the National Bank of Poland (NBP). Therefore, the NBP may try to curb another round of hefty PLN appreciation by means of verbal or de facto interventions, and finally lower the base rate.Some of the recent zloty performance can also be attributed to the strong perfor-mance and inflow into the LCY debt markets. The Polish local debt markets were among the best-performing LCY bond markets in Q1 2012. A yield compression took place despite a more hawkish central bank and hefty issuance. The Polish sovereign has already secured more than 40% of its financing needs in Q1 2012. This means a lot of the good performance on the LCY bond markets seems to be flow-driven. Investors like the solid economic performance and the credible fiscal consolidation that is underway. A lot of major players have increased their Polish holdings in recent weeks. Moreover, a lot of European investors have to diversify their holdings away from “peripheral” European debt, and Polish debt markets are one of the few and liquid alternatives in Europe. The share of foreign holdings on the government debt market currently stands at nearly 32%. Going forward, we do not see much scope for further yield tightening at the long end of the curve. In fact long-term yields may even inch up a wee bit. However, we do not foresee significantly higher yields from a 6-9 month horizon. We expect the healthy demand from foreign and domestic investors to persist, while the supply of Treasury bonds in H2 2012 will be much lower. Moreover, given the slowdown still expected in the real economy, Polish banks may also increase their sovereign bond holdings going forward. Furthermore, inflation should be on a downtrend in the months ahead, which should support bond prices and may lead to a more neutral and finally dovish stance of the MPC. Therefore, we think that there is a good carry to be earned on the Polish markets. This holds true for EUR-based investors as we still forecast a modest EUR/PLN appreciation.

Marta Petka-Zagajewska, Gunter Deuber

16 2nd quarter 2012

-8

-6

-4

-2

0

2

4

2007

2008

2009

2010

2011

2012

e

2013

f -24

-18

-12

-6

0

6

12

Real GDP (% yoy)Industrial output (% yoy, r.h.s.)

-8

-6

-4

-2

0

2

4

2007

2008

2009

2010

2011

2012

e

2013

f -4

-2

0

2

4

6

8

Current account (% of GDP)

Net FDI (% of GDP, r.h.s.)

Real GDP (% yoy)

Source: Thomson Reuters, Raiffeisen RESEARCH

Hungary

Light recession ahead

Current account and FDI inflows

Source: Thomson Reuters, Raiffeisen RESEARCH

Forecast

Forecast

Key economic figures and forecasts

2007 2008 2009 2010 2011 2012e 2013fNominal GDP (EUR bn) 99.4 105.5 91.5 97.2 100.8 99.3 105.5

Real GDP (% yoy) 0.1 0.9 -6.8 1.3 1.7 -0.5 1.5

Industrial output (% yoy) 7.9 0.0 -17.8 10.6 5.4 2.0 3.0

Unemployment rate (avg, %) 7.5 7.8 9.8 11.1 11.0 11.4 11.0

Nominal industrial wages (% yoy) 8.4 6.5 3.8 5.5 6.2 9.3 4.3

Producer prices (avg, % yoy) 0.1 5.1 4.9 4.5 4.3 6.4 2.6

Consumer prices (avg, % yoy) 8.0 6.1 4.2 4.9 3.9 5.5 3.5

Consumer prices (eop, % yoy) 7.4 3.5 5.6 4.7 4.1 5.0 3.4

General budget balance (% of GDP) -5.1 -3.7 -4.6 -4.2 0.0 -3.4 -3.4

Public debt (% of GDP) 67.0 72.9 79.7 81.3 82.7 80.7 79.9

Current account balance (% of GDP) -6.6 -7.1 0.3 1.1 1.6 1.8 1.0

Official FX reserves (EUR bn) 16.0 24.0 30.0 33.7 37.8 39.6 40.7

Gross foreign debt (% of GDP) 103.2 116.1 146.6 139.4 132.9 133.9 125.1

EUR/HUF (avg) 251.3 250.8 280.1 275.5 279.3 290.5 285.0

USD/HUF (avg) 183.3 170.5 200.9 207.7 203.9 218.8 219.2

Source: Thomson Reuters, wiiw, Raiffeisen RESEARCH

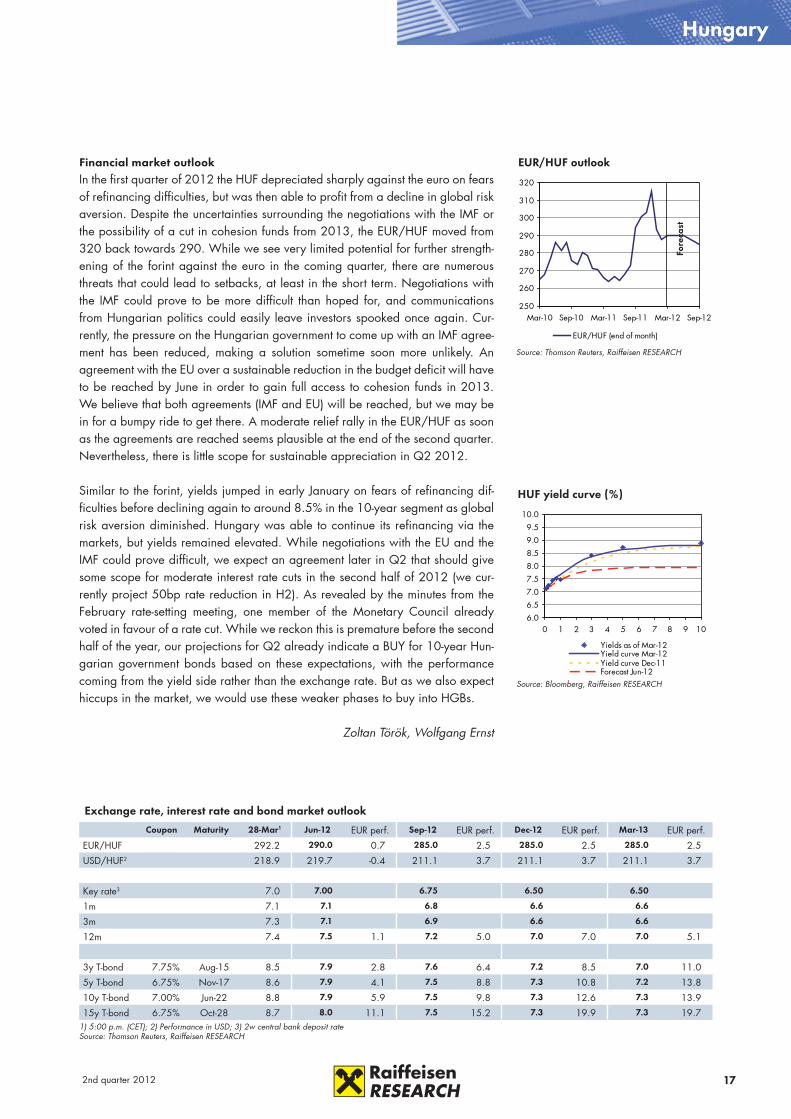

Economic outlook2011 GDP growth (1.7%) was driven by the above-average output of agriculture and strong manufacturing exports facilitated by the benign external environment. Expansionary fiscal policy was unable to ignite local demand.In 2012 we expect no growth in the export markets and a massively restrictive fiscal stance. After last year’s performance, any plus from agriculture would be a nice surprise. Apart from the booming car industry (new plants of Mercedes, Audi and GM/Opel) we still cannot identify any growth. Still, the car industry is helping manufacturing and exports remain in the black. Real household income is unlikely to increase, and the labour market is expected to stagnate – at best. Therefore, we do not expect any household consumption growth. Public services will be cut, and private services are likely to be in the red too (especially financial services). No recovery is yet due in the construction industry, and we expect a recession in 2012 (GDP -0.5%). Fiscal austerity is quite tangible in 2012. The government is proceeding with structural reforms and there is a wide range of tax hikes (VAT hike; excise duty hike; abolition of the system of personal income tax deduction, etc.). Current fis-cal austerity aims to improve the budget balance by over 3% of GDP. Still, it is likely that additional measures will be needed to reach the budget deficit target of below 3%. The big issue, however, is the 2013 budget: how to fill the budget gap caused by the diminishing crisis and banking tax receipts (approximately 1% of GDP)? If the government is able to give a proper (i.e. orthodox) answer to this, then Hungary may exit the EDP procedure and sign the new IMF loan agreement with relative ease. The bad news is that there are no painless solu-tions. Further fiscal measures would certainly weigh down on Hungary’s growth prospects for 2013 (and potentially damage the popularity of the governing party). Short-term and long-term views conflict with each other, while economics conflicts with politics.

2012 should bring no economic growth and a massively restrictive fiscal stance Government is proceeding with structural reforms and a wide range of tax hikes IMF and EU agreement would mean an end to unorthodox measures in the medium term Forint and yields showed strong volatility, more stability expected after an IMF/EU agreement

172nd quarter 2012

Hungary

250

260

270

280

290

300

310

320

Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12

EUR/HUF (end of month)

EUR/HUF outlook

Source: Thomson Reuters, Raiffeisen RESEARCH

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

0 1 2 3 4 5 6 7 8 9 10

Yields as of Mar-12Yield curve Mar-12Yield curve Dec-11Forecast Jun-12

HUF yield curve (%)

Source: Bloomberg, Raiffeisen RESEARCH

Financial market outlookIn the first quarter of 2012 the HUF depreciated sharply against the euro on fears of refinancing difficulties, but was then able to profit from a decline in global risk aversion. Despite the uncertainties surrounding the negotiations with the IMF or the possibility of a cut in cohesion funds from 2013, the EUR/HUF moved from 320 back towards 290. While we see very limited potential for further strength-ening of the forint against the euro in the coming quarter, there are numerous threats that could lead to setbacks, at least in the short term. Negotiations with the IMF could prove to be more difficult than hoped for, and communications from Hungarian politics could easily leave investors spooked once again. Cur-rently, the pressure on the Hungarian government to come up with an IMF agree-ment has been reduced, making a solution sometime soon more unlikely. An agreement with the EU over a sustainable reduction in the budget deficit will have to be reached by June in order to gain full access to cohesion funds in 2013. We believe that both agreements (IMF and EU) will be reached, but we may be in for a bumpy ride to get there. A moderate relief rally in the EUR/HUF as soon as the agreements are reached seems plausible at the end of the second quarter. Nevertheless, there is little scope for sustainable appreciation in Q2 2012.

Similar to the forint, yields jumped in early January on fears of refinancing dif-ficulties before declining again to around 8.5% in the 10-year segment as global risk aversion diminished. Hungary was able to continue its refinancing via the markets, but yields remained elevated. While negotiations with the EU and the IMF could prove difficult, we expect an agreement later in Q2 that should give some scope for moderate interest rate cuts in the second half of 2012 (we cur-rently project 50bp rate reduction in H2). As revealed by the minutes from the February rate-setting meeting, one member of the Monetary Council already voted in favour of a rate cut. While we reckon this is premature before the second half of the year, our projections for Q2 already indicate a BUY for 10-year Hun-garian government bonds based on these expectations, with the performance coming from the yield side rather than the exchange rate. But as we also expect hiccups in the market, we would use these weaker phases to buy into HGBs.

Zoltan Török, Wolfgang Ernst

Exchange rate, interest rate and bond market outlook

Coupon Maturity 28-Mar1 Jun-12 EUR perf. Sep-12 EUR perf. Dec-12 EUR perf. Mar-13 EUR perf.

EUR/HUF 292.2 290.0 0.7 285.0 2.5 285.0 2.5 285.0 2.5

USD/HUF2 218.9 219.7 -0.4 211.1 3.7 211.1 3.7 211.1 3.7

Key rate3 7.0 7.00 6.75 6.50 6.50

1m 7.1 7.1 6.8 6.6 6.6

3m 7.3 7.1 6.9 6.6 6.6

12m 7.4 7.5 1.1 7.2 5.0 7.0 7.0 7.0 5.1

3y T-bond 7.75% Aug-15 8.5 7.9 2.8 7.6 6.4 7.2 8.5 7.0 11.0

5y T-bond 6.75% Nov-17 8.6 7.9 4.1 7.5 8.8 7.3 10.8 7.2 13.8

10y T-bond 7.00% Jun-22 8.8 7.9 5.9 7.5 9.8 7.3 12.6 7.3 13.9

15y T-bond 6.75% Oct-28 8.7 8.0 11.1 7.5 15.2 7.3 19.9 7.3 19.71) 5:00 p.m. (CET); 2) Performance in USD; 3) 2w central bank deposit rateSource: Thomson Reuters, Raiffeisen RESEARCH

Fore

cast

18 2nd quarter 2012

-6

-4

-2

0

2

4

6

8

2007

2008

2009

2010

2011

2012

e

2013

f -15

-10

-5

0

5

10

15

20

Real GDP (% yoy)Industrial output (% yoy, r.h.s.)

Czech Republic

-7

-6-5

-4

-3

-2-1

0

2007

2008

2009

2010

2011

2012

e

2013

f 0

1020

30

40

5060

70

General budget balance (% of GDP)

Public debt (% of GDP, r.h.s.)

Real GDP (% yoy)

Source: Thomson Reuters, Raiffeisen RESEARCH

Economic outlookThe Czech economy slipped into a mild recession in H2 2012 as it contracted by 0.1% qoq in Q3 and Q4. The annual growth of GDP reached 1.7% in 2011. The decline in Q4 was driven by falling investment (mainly inventories) and government consumption. Household consumption remained flat. The VAT hike from January came as a one-off boost to retail sales and construction in Q4. The only positive driver of GDP was net exports. In other words, the weak domestic demand was the cause of the recession. We expect the recession to deepen in Q1 because these one-time factors will mainly reduce household consumption. The way we see it, GDP should decline by 0.4% qoq in Q1. The situation should stabilise at the end of H1 or at the beginning of H2, mainly thanks to an improve-ment in external demand. A recovery is now visible in new industrial orders. As a result we forecast an annual decline of the Czech economy by 0.2% in 2012.Due to the VAT hike, CPI inflation rose to 3.5% yoy in January. However, funds obtained from the VAT hike are apparently insufficient to achieve the 2012 fiscal target (deficit of 3.2% of GDP) and further expenditure cuts will be necessary throughout the year. To achieve the fiscal targets after 2012 the Czech gov-ernment is considering implementing other VAT hikes in 2013. The most likely strategy, at this moment, is to raise both rates by one percentage point to 21% and 15% respectively. This would nudge inflation again, and thus inflation would remain above the inflation target of 2% even in 2013. Another measure consid-ered is freezing pensions, which would reduce the weak domestic demand even further.The new president will be elected by a ballot at the beginning of 2013. In the autumn of 2012 the leftist opposition has a good chance of remaining in power in some regions due to the general dissatisfaction with austerity measures of the central government.

Economic weakness in the first half of 2012

Budget balance and public debt

Source: Thomson Reuters, Raiffeisen RESEARCH

Forecast

Forecast

Key economic figures and forecasts

2007 2008 2009 2010 2011 2012e 2013fNominal GDP (EUR bn) 132.2 154.2 141.5 149.2 154.9 156.9 169.7

Real GDP (% yoy) 5.7 3.1 -4.7 2.7 1.7 -0.2 1.4

Industrial output (% yoy) 9.0 0.4 -13.4 10.1 6.9 -0.9 1.9

Unemployment rate (avg, %) 6.6 5.4 8.1 9.0 8.5 8.9 9.1

Nominal industrial wages (% yoy) 7.2 8.1 3.5 3.7 4.4 3.0 3.8

Producer prices (avg, % yoy) 4.1 4.5 -3.1 1.2 5.6 2.7 2.2

Consumer prices (avg, % yoy) 2.8 6.3 1.0 1.5 1.9 3.0 2.2

Consumer prices (eop, % yoy) 5.4 3.6 1.0 2.3 2.4 2.5 2.0

General budget balance (% of GDP) -0.7 -2.2 -5.8 -4.8 -4.4 -3.7 -3.4

Public debt (% of GDP) 29.0 28.7 34.4 37.6 41.1 43.6 45.2

Current account balance (% of GDP) -4.3 -2.1 -2.4 -3.9 -2.9 -2.2 -2.3

Official FX reserves (EUR bn) 23.7 26.6 28.9 31.8 31.1 32.0 34.0

Gross foreign debt (% of GDP) 39.1 38.7 43.7 47.9 48.9 47.4 47.9

EUR/CZK (avg) 27.7 24.9 26.4 25.3 24.6 24.5 23.5

USD/CZK (avg) 20.2 17.0 19.0 19.1 17.9 18.5 18.1

Source: Thomson Reuters, wiiw, Raiffeisen RESEARCH

Czech economy in technical recession, recovery expected in H2 More VAT hikes possible in 2013 Czech crown showing strong appreciation in Q1 2012, sideways movement expected in Q2 No change in interest rates expected over the next 12 months

192nd quarter 2012

Czech Republic

23.0

23.5

24.0

24.5

25.0

25.5

26.0

Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12

EUR/CZK (end of month)

EUR/CZK outlook

Source: Thomson Reuters, Raiffeisen RESEARCH

0.00.51.01.52.02.53.03.54.04.5

0 1 2 3 4 5 6 7 8 9 10

Yields as of Mar-12Yield curve Mar-12Yield curve Dec-11Forecast Jun-12

CZK yield curve (%)

Source: Bloomberg, Raiffeisen RESEARCH

Financial market outlookIn the first quarter of 2012 the Czech crown more than met our expectations. Against the euro the Czech koruna appreciated to 24.40 from almost 26.0 at the beginning of 2012. The faster than expected appreciation can mostly be explained by the fall in risk aversion after the adoption of the LTROs by the ECB. Our baseline view on the Czech currency, however, remains unchanged. Funda-mentally, the CZK-EUR convergence story still has some way to go. Nevertheless, in the short-term the sudden rises and falls of risk aversion might significantly influence the path of the EUR/CZK.As the outlook on the economy improved this year and inflation started a bit higher in 2012, the chances of an interest rate cut have diminished. On the other hand, some board members have started to talk about a possible need to increase interest rates in the foreseeable future. As mentioned, we expect the CZK will appreciate more in H2. We assume that the ECB will leave interest rates unchanged over the next 12 months. The Czech economy will be driven by ex-ports and just a gradual rise of investments. Domestic demand will probably be subdued throughout 2012-2013 as fiscal policy will be restrictive. All in all we do not expect any change in the CNB key interest rate over the next 12 months.In Q1 2012, Czech government bond yields moved sideways, justifying our neutral recommendation on Czech government bonds. The Ministry of Finance essentially has no problems placing domestic bonds. In February the Ministry successfully sold EUR 2.0 bn. The net borrowing requirement decreased to about CZK142 bn in 2011 and for 2012 the Ministry expects CZK 107.2 bn. The central government budget deficit is expected to reach CZK105 bn this year. The gross borrowing requirement is likely to reach CZK 243.4 bn which is slightly lower than in 2011. Assuming the debt crisis in the Eurozone does not escalate anew, the Ministry should not have any problems securing all its requirements for 2012. In our baseline scenario we expect a gradual decrease in the spread between Czech government bonds and the German benchmark. For the second quarter of 2012 our recommendation remains hold.

Pavel Mertlik, Michal Brozka

Exchange rate, interest rate and bond market outlook

Coupon Maturity 28-Mar1 Jun-12 EUR perf. Sep-12 EUR perf. Dec-12 EUR perf. Mar-13 EUR perf.

EUR/CZK 24.7 24.7 -0.2 24.4 1.1 23.8 3.6 23.6 4.5

USD/CZK2 18.5 18.7 -0.9 18.1 2.6 17.6 5.2 17.5 6.1

Key rate3 0.8 0.75 0.75 0.75 0.75

1m 0.6 0.7 0.7 0.7 0.7

3m 0.9 0.8 0.8 0.8 0.8

12m 1.1 1.4 0.1 1.4 1.7 1.4 4.6 1.4 5.9

2y T-bond 2.75% Mar-14 1.5 1.3 0.6 1.4 2.0 1.5 4.9 1.7 3.5

5y T-bond 4.00% Apr-17 2.4 2.2 1.2 2.1 3.4 2.2 6.6 2.4 7.7

10y T-bond 3.85% Sep-21 3.4 3.5 -0.2 3.4 2.7 3.5 5.4 3.6 6.5

15y T-bond 5.70% May-24 3.7 3.7 0.7 3.7 2.9 3.8 5.6 3.9 6.61) 5:00 p.m. (CET); 2) Performance in USD, 3) 2w repo rateSource: Thomson Reuters, Raiffeisen RESEARCH

Fore

cast

20 2nd quarter 2012

Slovakia

-9-8-7-6-5-4-3-2-10

2007

2008

2009

2010

2011

2012

e

2013

f 20253035404550556065

General budget balance (% of GDP)

Public debt (% of GDP, r.h.s.)

Source: Thomson Reuters, Raiffeisen RESEARCH

Budget balance and public debt

Source: Thomson Reuters, Raiffeisen RESEARCH

Forecast

-6-4-202468

1012

2007

2008

2009

2010

2011

2012

e

2013

f -20-15-10

-50510

1520

Real GDP (% yoy)Industrial output (% yoy, r.h.s.)

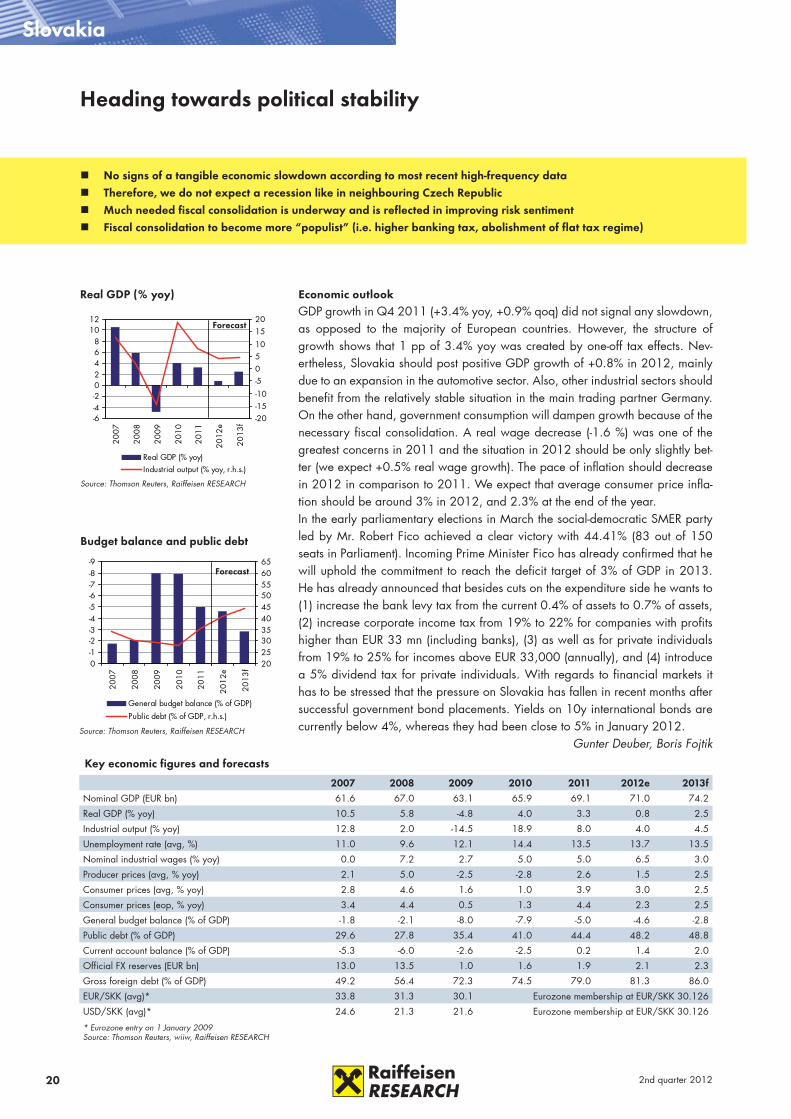

Heading towards political stability

Key economic figures and forecasts

2007 2008 2009 2010 2011 2012e 2013fNominal GDP (EUR bn) 61.6 67.0 63.1 65.9 69.1 71.0 74.2

Real GDP (% yoy) 10.5 5.8 -4.8 4.0 3.3 0.8 2.5

Industrial output (% yoy) 12.8 2.0 -14.5 18.9 8.0 4.0 4.5

Unemployment rate (avg, %) 11.0 9.6 12.1 14.4 13.5 13.7 13.5

Nominal industrial wages (% yoy) 0.0 7.2 2.7 5.0 5.0 6.5 3.0

Producer prices (avg, % yoy) 2.1 5.0 -2.5 -2.8 2.6 1.5 2.5

Consumer prices (avg, % yoy) 2.8 4.6 1.6 1.0 3.9 3.0 2.5

Consumer prices (eop, % yoy) 3.4 4.4 0.5 1.3 4.4 2.3 2.5

General budget balance (% of GDP) -1.8 -2.1 -8.0 -7.9 -5.0 -4.6 -2.8

Public debt (% of GDP) 29.6 27.8 35.4 41.0 44.4 48.2 48.8

Current account balance (% of GDP) -5.3 -6.0 -2.6 -2.5 0.2 1.4 2.0

Official FX reserves (EUR bn) 13.0 13.5 1.0 1.6 1.9 2.1 2.3

Gross foreign debt (% of GDP) 49.2 56.4 72.3 74.5 79.0 81.3 86.0

EUR/SKK (avg)* 33.8 31.3 30.1 Eurozone membership at EUR/SKK 30.126

USD/SKK (avg)* 24.6 21.3 21.6 Eurozone membership at EUR/SKK 30.126

* Eurozone entry on 1 January 2009Source: Thomson Reuters, wiiw, Raiffeisen RESEARCH

Forecast

Real GDP (% yoy) Economic outlookGDP growth in Q4 2011 (+3.4% yoy, +0.9% qoq) did not signal any slowdown, as opposed to the majority of European countries. However, the structure of growth shows that 1 pp of 3.4% yoy was created by one-off tax effects. Nev-ertheless, Slovakia should post positive GDP growth of +0.8% in 2012, mainly due to an expansion in the automotive sector. Also, other industrial sectors should benefit from the relatively stable situation in the main trading partner Germany. On the other hand, government consumption will dampen growth because of the necessary fiscal consolidation. A real wage decrease (-1.6 %) was one of the greatest concerns in 2011 and the situation in 2012 should be only slightly bet-ter (we expect +0.5% real wage growth). The pace of inflation should decrease in 2012 in comparison to 2011. We expect that average consumer price infla-tion should be around 3% in 2012, and 2.3% at the end of the year.In the early parliamentary elections in March the social-democratic SMER party led by Mr. Robert Fico achieved a clear victory with 44.41% (83 out of 150 seats in Parliament). Incoming Prime Minister Fico has already confirmed that he will uphold the commitment to reach the deficit target of 3% of GDP in 2013. He has already announced that besides cuts on the expenditure side he wants to (1) increase the bank levy tax from the current 0.4% of assets to 0.7% of assets, (2) increase corporate income tax from 19% to 22% for companies with profits higher than EUR 33 mn (including banks), (3) as well as for private individuals from 19% to 25% for incomes above EUR 33,000 (annually), and (4) introduce a 5% dividend tax for private individuals. With regards to financial markets it has to be stressed that the pressure on Slovakia has fallen in recent months after successful government bond placements. Yields on 10y international bonds are currently below 4%, whereas they had been close to 5% in January 2012.

Gunter Deuber, Boris Fojtik

No signs of a tangible economic slowdown according to most recent high-frequency data Therefore, we do not expect a recession like in neighbouring Czech Republic Much needed fiscal consolidation is underway and is reflected in improving risk sentiment Fiscal consolidation to become more “populist” (i.e. higher banking tax, abolishment of flat tax regime)

212nd quarter 2012

-10-8-6-4-202468

10

2007

2008

2009

2010

2011

2012

e

2013

f -20-16-12-8-4048121620

Real GDP (% yoy)Industrial output (% yoy, r.h.s.)

Slovenia

-7

-6

-5

-4

-3

-2

-1

0

2007

2008

2009

2010

2011

2012

e

2013

f 0

10

20

30

40

50

60

70

General budget balance (% of GDP)

Public debt (% of GDP, r.h.s.)

Real GDP (% yoy)

Source: Thomson Reuters, Raiffeisen RESEARCH

Budget balance and public debt

Source: Thomson Reuters, Raiffeisen RESEARCH

Forecast

Forecast

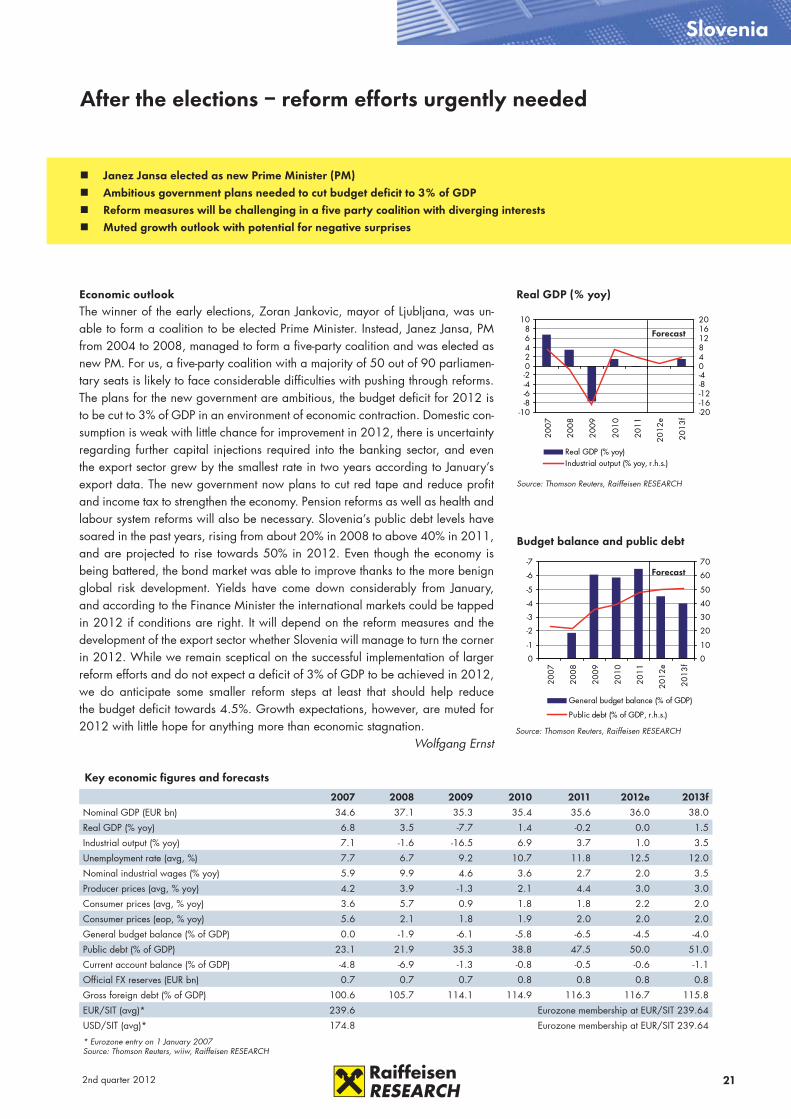

After the elections – reform efforts urgently needed

Key economic figures and forecasts

2007 2008 2009 2010 2011 2012e 2013fNominal GDP (EUR bn) 34.6 37.1 35.3 35.4 35.6 36.0 38.0

Real GDP (% yoy) 6.8 3.5 -7.7 1.4 -0.2 0.0 1.5

Industrial output (% yoy) 7.1 -1.6 -16.5 6.9 3.7 1.0 3.5

Unemployment rate (avg, %) 7.7 6.7 9.2 10.7 11.8 12.5 12.0

Nominal industrial wages (% yoy) 5.9 9.9 4.6 3.6 2.7 2.0 3.5

Producer prices (avg, % yoy) 4.2 3.9 -1.3 2.1 4.4 3.0 3.0

Consumer prices (avg, % yoy) 3.6 5.7 0.9 1.8 1.8 2.2 2.0

Consumer prices (eop, % yoy) 5.6 2.1 1.8 1.9 2.0 2.0 2.0

General budget balance (% of GDP) 0.0 -1.9 -6.1 -5.8 -6.5 -4.5 -4.0

Public debt (% of GDP) 23.1 21.9 35.3 38.8 47.5 50.0 51.0

Current account balance (% of GDP) -4.8 -6.9 -1.3 -0.8 -0.5 -0.6 -1.1

Official FX reserves (EUR bn) 0.7 0.7 0.7 0.8 0.8 0.8 0.8

Gross foreign debt (% of GDP) 100.6 105.7 114.1 114.9 116.3 116.7 115.8

EUR/SIT (avg)* 239.6 Eurozone membership at EUR/SIT 239.64

USD/SIT (avg)* 174.8 Eurozone membership at EUR/SIT 239.64

* Eurozone entry on 1 January 2007Source: Thomson Reuters, wiiw, Raiffeisen RESEARCH

Janez Jansa elected as new Prime Minister (PM) Ambitious government plans needed to cut budget deficit to 3% of GDP Reform measures will be challenging in a five party coalition with diverging interests Muted growth outlook with potential for negative surprises

Economic outlookThe winner of the early elections, Zoran Jankovic, mayor of Ljubljana, was un-able to form a coalition to be elected Prime Minister. Instead, Janez Jansa, PM from 2004 to 2008, managed to form a five-party coalition and was elected as new PM. For us, a five-party coalition with a majority of 50 out of 90 parliamen-tary seats is likely to face considerable difficulties with pushing through reforms. The plans for the new government are ambitious, the budget deficit for 2012 is to be cut to 3% of GDP in an environment of economic contraction. Domestic con-sumption is weak with little chance for improvement in 2012, there is uncertainty regarding further capital injections required into the banking sector, and even the export sector grew by the smallest rate in two years according to January’s export data. The new government now plans to cut red tape and reduce profit and income tax to strengthen the economy. Pension reforms as well as health and labour system reforms will also be necessary. Slovenia’s public debt levels have soared in the past years, rising from about 20% in 2008 to above 40% in 2011, and are projected to rise towards 50% in 2012. Even though the economy is being battered, the bond market was able to improve thanks to the more benign global risk development. Yields have come down considerably from January, and according to the Finance Minister the international markets could be tapped in 2012 if conditions are right. It will depend on the reform measures and the development of the export sector whether Slovenia will manage to turn the corner in 2012. While we remain sceptical on the successful implementation of larger reform efforts and do not expect a deficit of 3% of GDP to be achieved in 2012, we do anticipate some smaller reform steps at least that should help reduce the budget deficit towards 4.5%. Growth expectations, however, are muted for 2012 with little hope for anything more than economic stagnation.

Wolfgang Ernst

22 2nd quarter 2012

-10-8-6-4-20246

2007

2008

2009

2010

2011

2012

e

2013

f

Real GDP (% yoy)Industrial output (% yoy)

Croatia

-6

-5

-4

-3

-2

-1

0

2007

2008

2009

2010

2011

2012

e

2013