CHILE'S SALMONCULTURE. FOUR YEARS LATER.

A TRIANGULAR PROCESS

FOR REBOOTING SALMON 2.0

C.R. Hernandez Salas

THREE FACTORS EXPLAIN THE CRISIS AND RAPID RECOVERY IN CHILE

We must be focused on how the regime works.

A regime geared towards growth.

Sanitary aspects were separated from the

environmental management. (First buffer)

A regime geared for expansion, spreading the risk geographically.

Trends for expansion were working before the

“crisis”. (Second buffer)

A regime expanding the financial risk.

Shifting the risks from the banks to the stock

market (Third buffer).

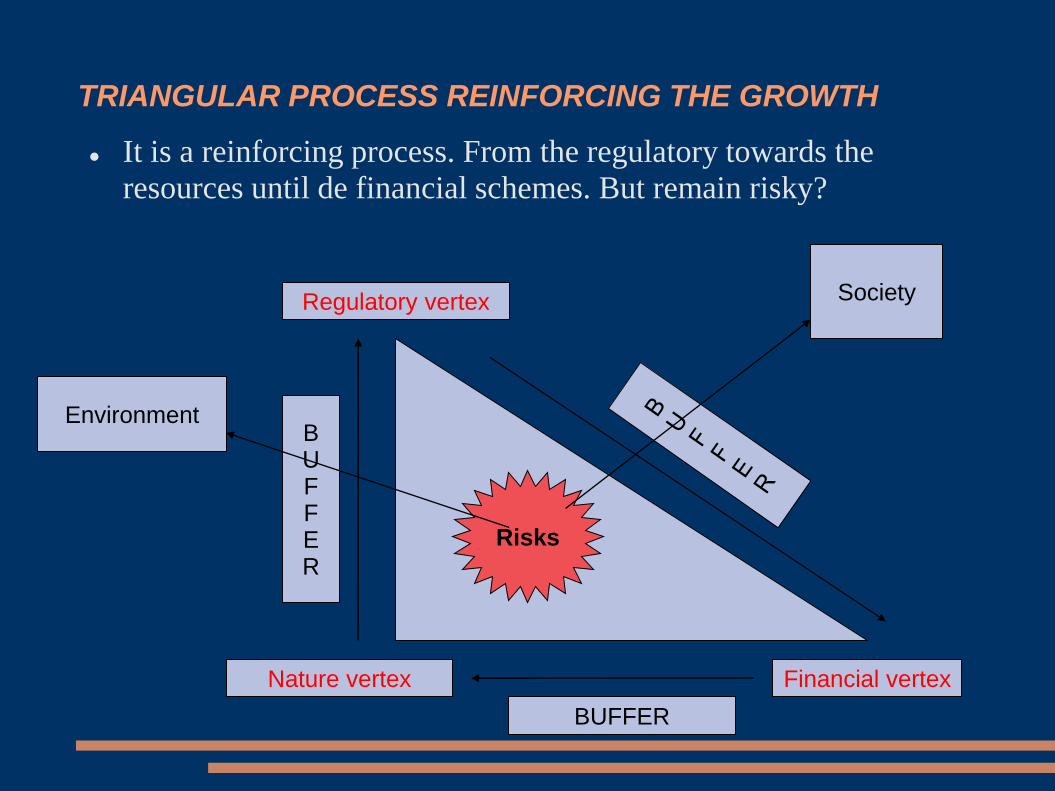

TRIANGULAR PROCESS REINFORCING THE GROWTH

It is a reinforcing process. From the regulatory towards the

resources until de financial schemes. But remain risky?

Regulatory vertex

Financial vertex Nature vertex

Risks

B U F F E R

BUFFER

Environment

Society

Outline of presentation

The working of the barrios

The economic situation of the Chilean

companies

The environmental situation

The sanitary situation

The monitoring and enforcement capacity

(SERNAPESCA)

Moving further south ? (to Magallanes)

58 barrios in Region X, XI and XII

The system of barrios a good idea, but it is a problem

of implementation especially in Region X

The idea of one company, one barrio has been

difficult to implement.

You only need one bad neighbour to get disease

problems. ''A healthy enterprise in an insane

neighborhood''

Better performance in Region XI

Probably even better in Region XII where you can

plan nearly from scratch

GROWTH & ENVIRONMENT. CURRENT TRENDS

Consequences:

Public response remains reactive while the system

gains in complexity.

About 400 new concessions for the

next years.

The public sector is essentialy the

same as before the crisis.

Nevertheless, there is a better response to sanitary

emergencies, and better practices in the industry.

But, key issues like the distance between centres

and between barrios have not been dealt with.

The economic situation of the Chilean companies

Bank debts have to be paid in 2012.

Several companies need to renegotiate their debts.

Difficult situation when the prices are falling.

The banks decide of the future structure of the

industry.

Lately several companies have successfully gone

on the stock exchange – shifting the risks to

private investors.

EXPORTS OF SALMO SALAR PERIOD JANUARY SEPTEMBER. TONS

2008: 173.738 Tons US$ 6,5 kg. FOB

2009: 149.994 Tons US$ 5,8 kg. FOB

2010: 63,700 Tons US$ 8,1 kg. FOB

2011: 96.373 Tons US$ 9,2 kg. FOB

November 2011:

+- 50% less

(USA remains the main market)

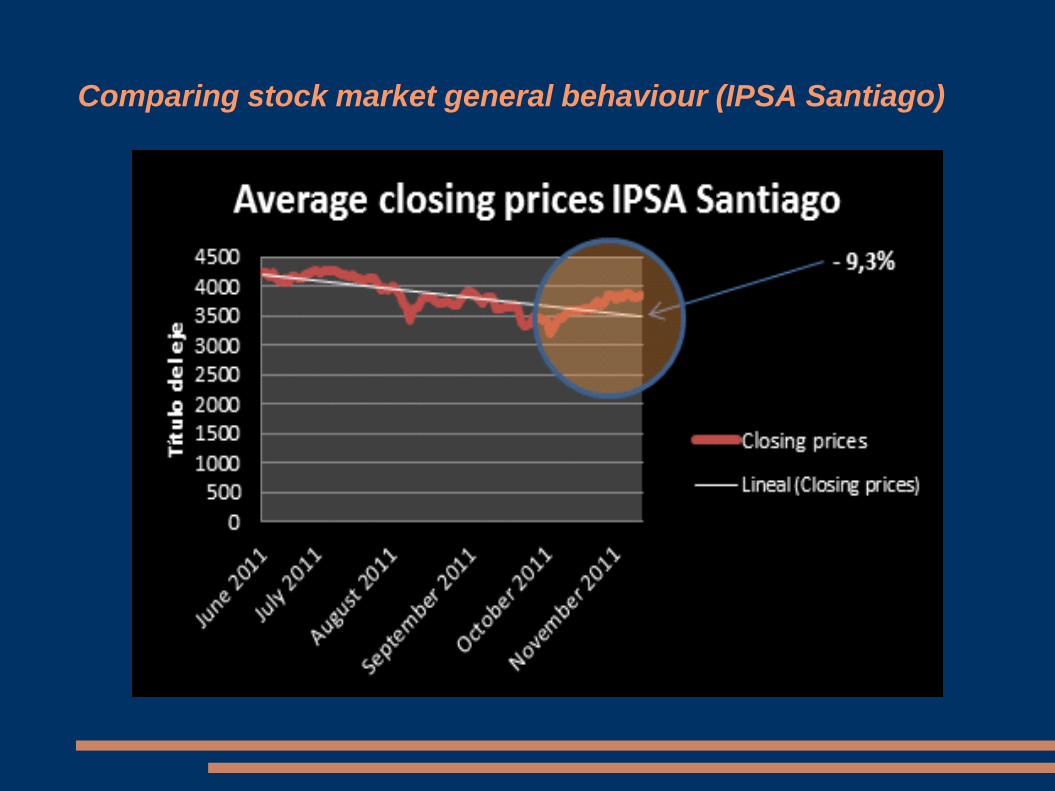

Comparing stock market general behaviour (IPSA Santiago)

Salmon Stock Market. Close prize, Salmon Index (Santiago)

Growth & environment: Barrios are not enough.

New regulations still have some gaps:

A major focus on the processes (less on institutions).

New regulations are based on improving

processes, based on private skills. But

institutions remain unchanged in substance.

More controls and biosecurity measures in the

production chain. But, with weak

implementation.

Liability gaps. New rules are focused on the monitoring

capacity but less on the objective liability of farmers.

Problems of administrative capacity (SERNAPESCA)

SERNAPESCA has improved, but

Is not able to follow the present growth

Increasing number of regulations

Increasing complexity of regulations

Public regulations still based on private processes

and skills

Unclear relations between SERNAPESCA and the

Undersecretary of Fisheries under the Ministry of

Economics.

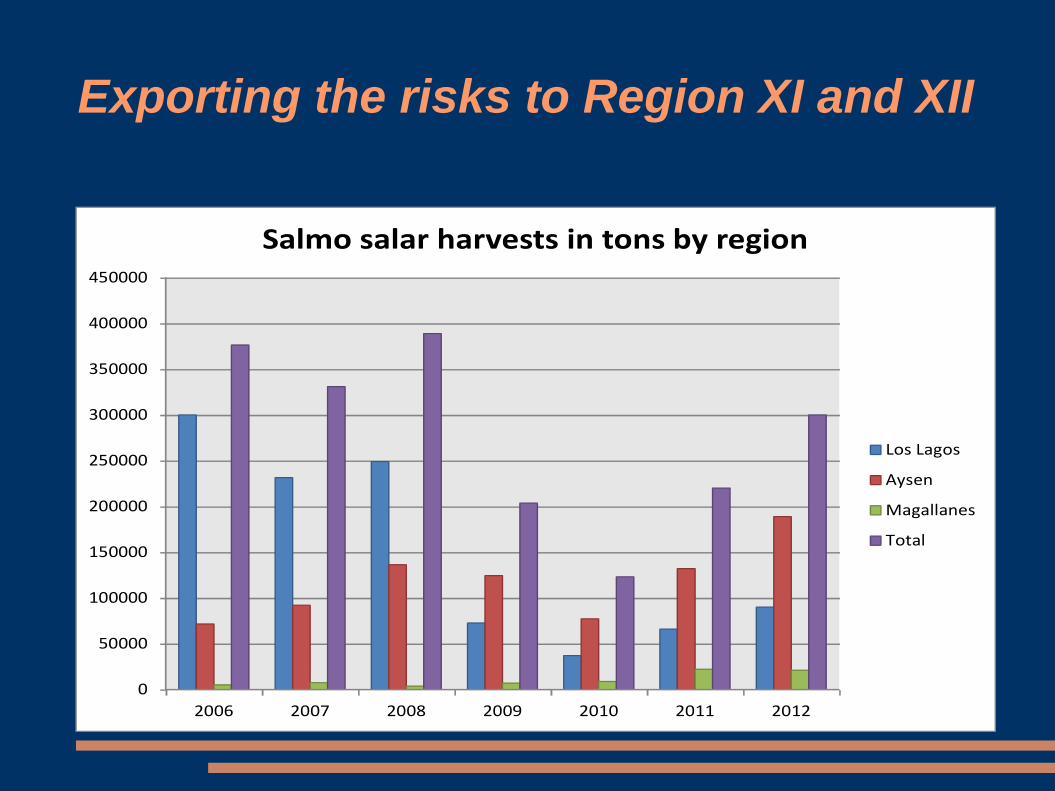

Exporting the risks to Region XI and XII

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

2006 2007 2008 2009 2010 2011 2012

Salmo salar harvests in tons by region

Los Lagos

Aysen

Magallanes

Total

Risks are blurred in the geography

Why was the recovery so fast?

New spaces for aquaculture: Aysen, Magallanes

In fact, Aysen harvests have increased their share in the annual

harvesting.

2006: 19% (71,402 tons)

2010: 63% (77,233 tons)

Projections maintain or increase these trend.

Projections of the industry are optimistics:

2011: 215,000 tons.

2012: 300,000 – 320,000 tons.

Calculated on a rate of 30% - 50% of concessions effectively

working and entry of 800,000 – 900,000 smolts per concession

annually.

Double dip: social expectations

The future of salmonculture

remains uncertain.

Aysen's economy is

becoming highly dependent

on salmonculture (the last

quarter Aysen was the

economy that grew more in

the country, driven by the

salmonculture). NGOs and artisanal fishers are weak today, and have their own

problems and agendas.

Politicians are worried for the future of the industry. A sign of new

collapse would be an argument againts the industry as a whole.

A double dip? The uncertain future and the Virgin

There are worring signs:

Why has the most remote area

become infected?

Cupquelan fjord is the most

unlikely area for finding ISA.

But the “virgin” is infected.

Gaps in the management of

wellboats?

CONCLUSIONS

The future of the industry remains highly uncertain.

Key factors of the sanitary and environmental management of the

new regulations remain unimplemented.

The new regime is still based on private processes and skills. The

claim for more state intervention by the beginning of the crisis was

forgotten.

The main actor in the near future will be the banks. Mergers and

sales will be pushed probably by them, based on their guarantees.

There are worrying signs of bad sanitary conditions. Nevertheles,

cases of sanitary emergencies have been well managed.

CONCLUSIONS

The regime is under stress. Its propensity to growth is

clashing with:

The capacity of the monitoring and enforcement

regime of sanitary management;

The present price level makes the negotiations

with the banks difficult;

Liquidity. The march southward is only for larger

companies. Wider space, fewer companies.

Any sign of a new sanitary crisis will be politically

untenable.

NGOs. artisanal fishers and workers are in a

weak position, being involved in their own

problems and agendas. This could change!