Business climate for the French business community of the UAE

June 2013

130618-FBC and FBG survey v1DUB

2100208-FBC and FBG survey v1 as presented

Respondents’ profile representative of the French Business Community

0

20

40

60

80

100%

Profile of the respondents

By Council

FBC

Both

FBG

69

By industry

Construction

Telecom and Media

Manufacturing

Retail & Distribution

Business services

Hospitality & food services

Healthcare / Education

Other

Logistics & transport

Utilities

Financial services

68

Source: FBC-FBG survey Apr 2013, N=69

0 20 40 60

Sales/pre-sales

Service delivery 26

Assembly &

Manufacturing

6

Logistics & distribution 5

Local R&D 5

By activity in UAE

58

130618-FBC and FBG survey v1DUB

3100208-FBC and FBG survey v1 as presented

Respondents together employ over 10,000 persons in the UAE, including ~2% Emirati

0

20

40

60

80

100%

50-99

10 to 49

Less than 10

500 or more

250-499

100-249

69

Number of respondents by workforce size

(# employees based in the UAE )

120

Average # employees

10,215

Participant workforce

0

20

40

60

80

100%

1-5%

0%

6-10%

Over 21%

11-20%

69

2%

Average % of Emirati

% of Emirati in the workforce

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

4100208-FBC and FBG survey v1 as presented

Respondents are significant contributor to the UAE economy with AED10B sales including 60% export

0

20

40

60

80

100%

By turnover range

Over 500m

101m-500m

51m-100m

31m-50m

16-30m

1-15m

Less than AED 1m

10BTotal participant turnover (AED )

Turnover of respondents

143mAverage turnover (AED )

0

20

40

60

80

100%

Revenue of the UAE company in the region

(% of company revenue )

% sales

Other

Other MENA

Rest of GCC

UAE

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

5100208-FBC and FBG survey v1 as presented

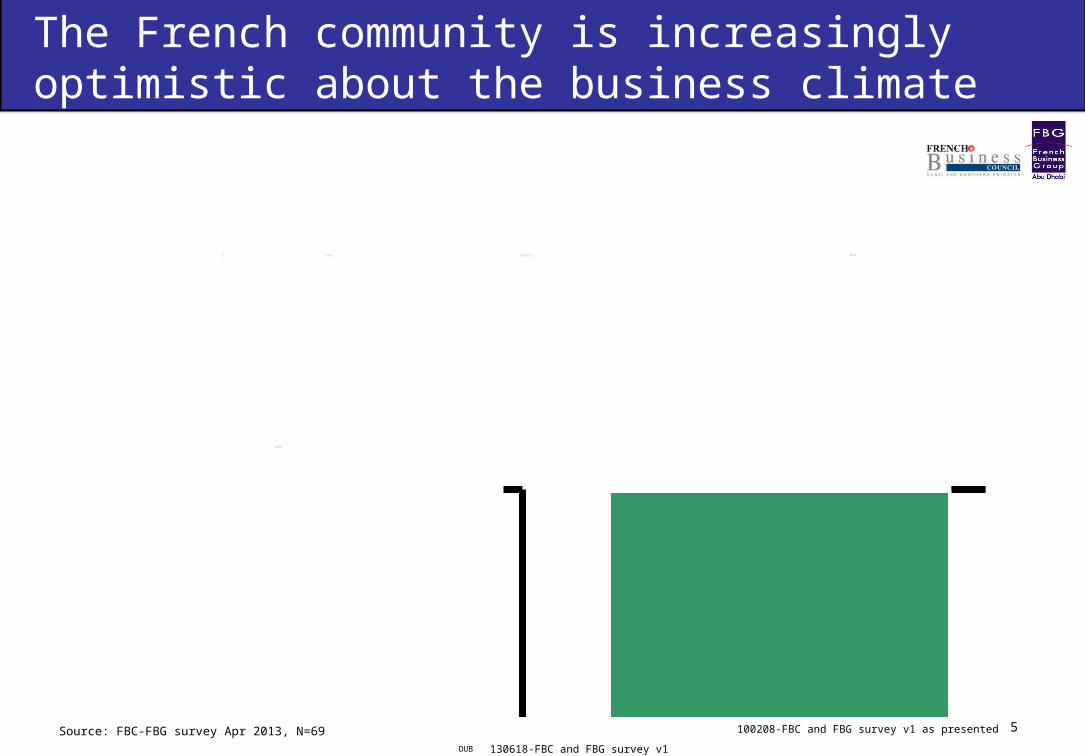

The French community is increasingly optimistic about the business climate

0

20

40

60

80

100%

Q2 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Next 6 month

Growth has

been flat

Growth

has

remained

positive

but lower

than

before

Growth

has been

positive

and

faster

than

before

In your industry what is the market growth in the region?

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

6100208-FBC and FBG survey v1 as presented

The UAE did particularly well in 2012

0

20

40

60

80

100%

UAE

13%

(22% )

13% (13% )

50%

(44% )

23%

(20% )

KSA

24%

(30% )

7% (6% )

38%

(42% )

31%

(22% )

Rest of GCC

28%

(29% )

9% (8% )

23%

(27% )

40%

(35% )

In your industry, how has your sales evolved

during 2012 vs 2011 in each country?2013 results

2012 results

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

7100208-FBC and FBG survey v1 as presented

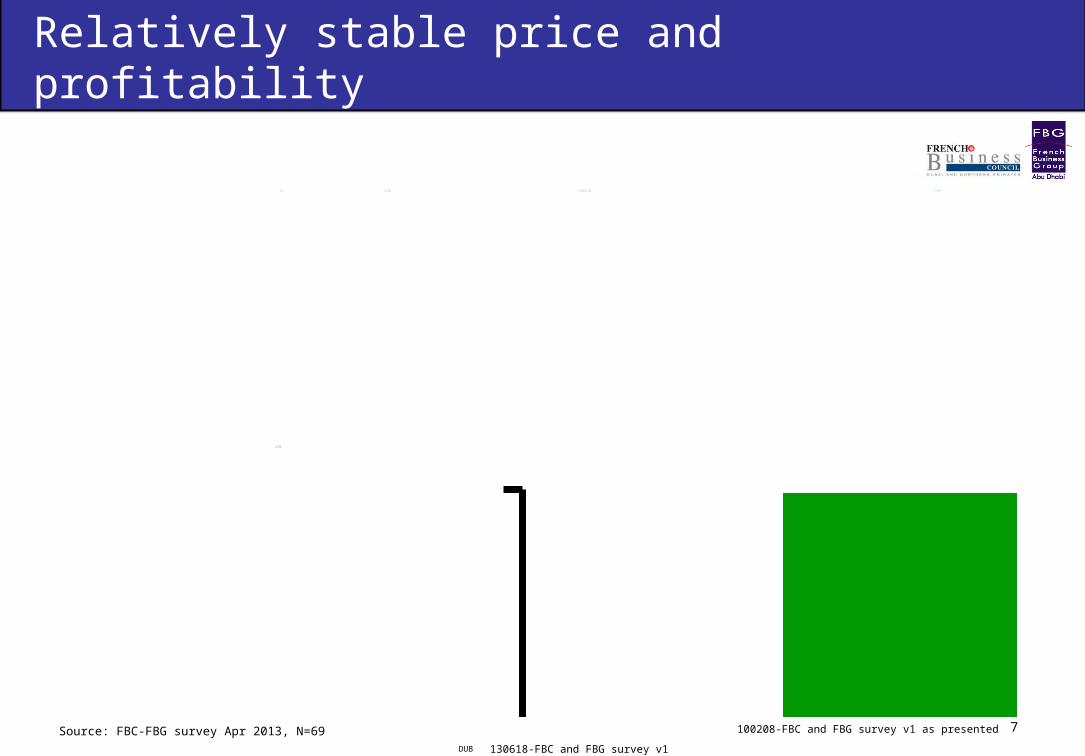

Relatively stable price and profitability

0

20

40

60

80

100%

Profitability

HIgher

Stable

Lower

63

Price

Increased

Stable

Decreased

63

In your industry, how has the following metrics evolved in the last year?

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

8100208-FBC and FBG survey v1 as presented

Continuation of high investment and recruitment trends

0

20

40

60

80

100%

Investment

Stable

Higher

Workforce

Stable

Increase ( recruit )

How do you expect the following metrics to evolve in the region?

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

9100208-FBC and FBG survey v1 as presented

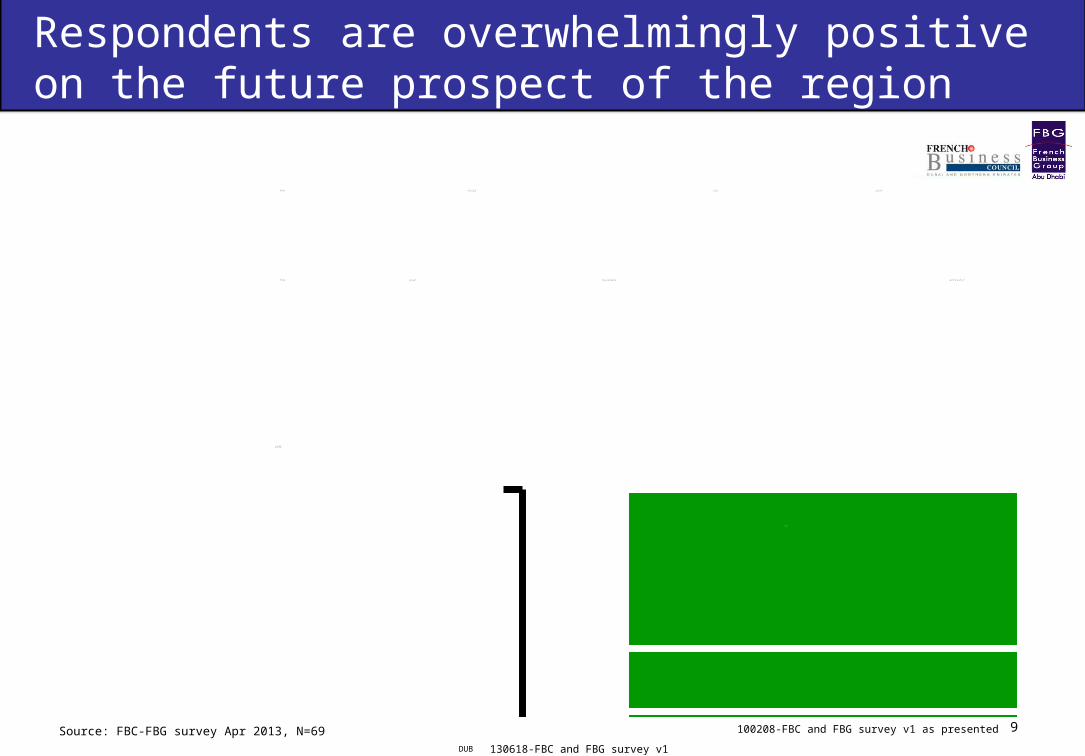

Respondents are overwhelmingly positive on the future prospect of the region

0

20

40

60

80

100%

Q2 2009

10

9

8

7

6

5

4

3

2

2010

10

9

8

7

6

5

4

3

2

1

2011

10

8

7

6

5

2012

10

9

8

7

6

5

2013

9

8

7

6

5

How would you rate the potential of the Middle East in the next three years

for your business activity? (1: no potential, 10: high potential )

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

10100208-FBC and FBG survey v1 as presented

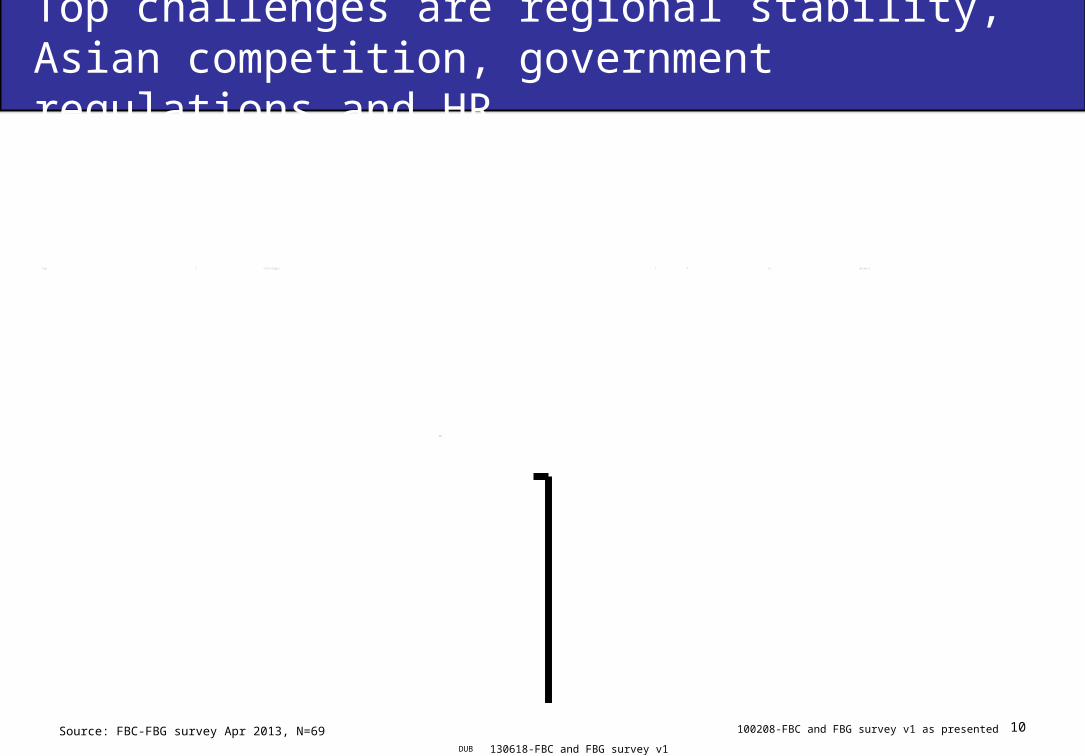

Top challenges are regional stability, Asian competition, government regulations and HR

0

10

20

30

Top 3 challenges ( # of answers )

Regio

n

geopo

litics

21

Asian

com

petit

ion

20

Govern

men

t

regu

latio

ns

14

HR

13

Cost

Infla

tion

10

glob

al

econ

omy

8

public

inve

stm

ent

8

Comm

odity

price

5

Acces

s

to

financ

e

4

Paym

ent

term

s

4

Tour

ism

3

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

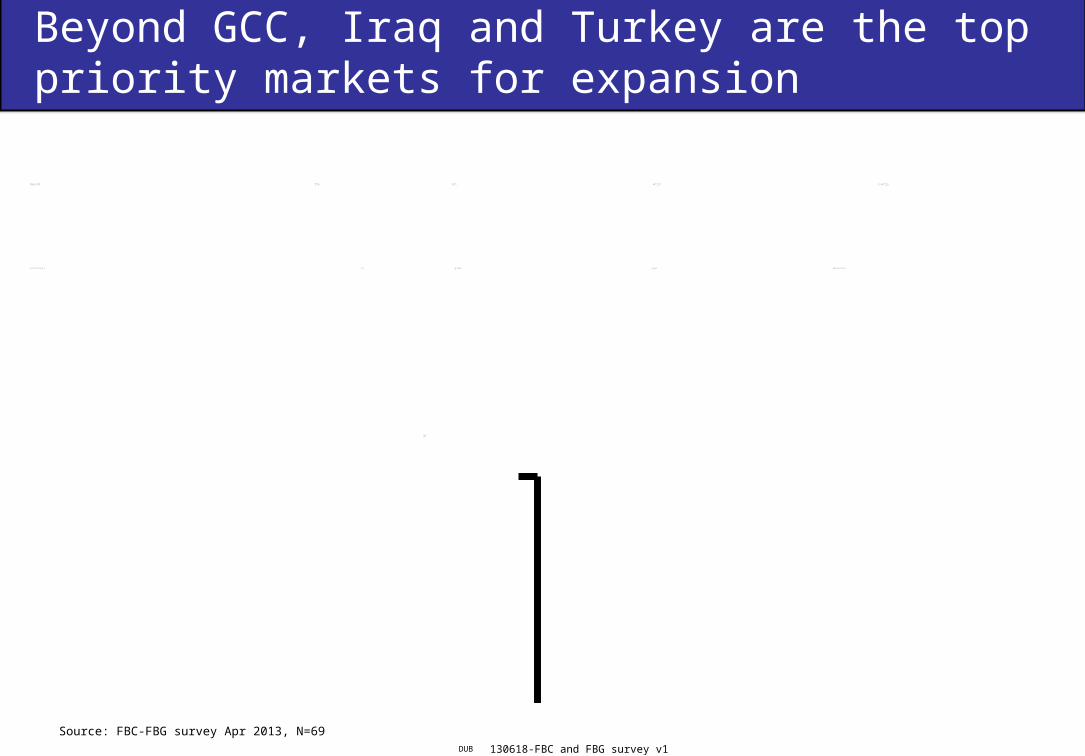

0

10

20

30

Beyond the GCC, which country in the region has the most

potential to grow your business in the coming 5-10 years?

Iraq

21

Turkey

12

Iran

9

Egypt

7

Jordan

3

2

Morocco

1 1

Pakistan

1

Tunisia Libya Syria Yemen

Lebanon

Algeria

Beyond GCC, Iraq and Turkey are the top priority markets for expansion

Source: FBC-FBG survey Apr 2013, N=69

130618-FBC and FBG survey v1DUB

12100208-FBC and FBG survey v1 as presented

BACK UPS FROM PREVIOUS EDITIONS

130618-FBC and FBG survey v1DUB

0 20 40 60 80%

Create supplier development teams in State Owned Enterprises to provide technical assistance to local manufacturer

16

Better market the UAE to potential foreign investors

24

Develop export promotion programs for locally-incorporated companies

28

Split tender requirements into smaller components to allow locally incorporated companies to compete technically

and financially

29

Expand the availability of adequately-serviced industrial land

31

Create an industrial bank that provides easier and cheaper access to finance

39

Improve availability of gas and utilities

40

Improve technical training

44

Introduce some preference for products manufactured in the UAE over imported products, in tenders for

Government and State Owned Enterprises

47

Improve the legal and regulatory environment to best practices

56

Encourage companies to invest locally by creating longer term tender contracts where government or state-owned

buyers commit to buying a minimum quantity over time

56

Foster regional integration and create a single GCC market

63

Allow majority foreign ownership of industrial ventures

Very highHigh 72

Impact on Manufacturing FDI

( % high & very high )

Respondents recommend eight key actions to increase manufacturing FDI in the UAE

The UAE is keen to accelerate the development of manufacturing in the country. Which of the following initiatives would be most effective to achieve this objective in your sector?

Source: Bain & FBC survey of foreign investors in the UAE, Feb 2012, N=87

130618-FBC and FBG survey v1DUB

14100208-FBC and FBG survey v1 as presented

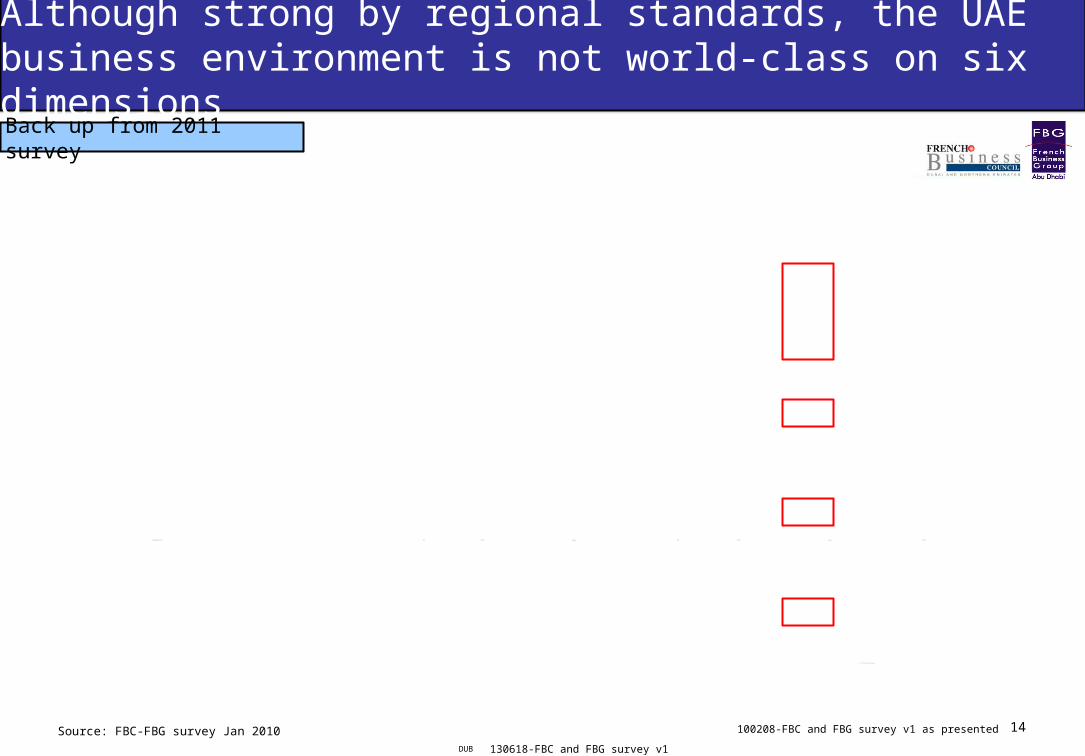

Although strong by regional standards, the UAE business environment is not world-class on six dimensions

0 10 20 30 40 50

Administrative efficiency

13

Quality of the social infrastructure ( education, healthcare,

entertainment )

15

Personal Taxation

17

100% foreign ownership

23

Ability to attract talent

24

Corporate Taxation

26

Business friendly laws

26

Quality of the transport infrastructure ( port, airport,roads... )

28

Cost of doing business

33

Attractiveness of the local market

34

Confidence in the rule of the law and ability to enforce contracts

44

13

6

14

16

19

42

9

40

48

5

2

World

class

29

20

35

48

46

34

28

17

11

41

31

Best of

Region

How important are the following factors when

deciding where to locate your regional

headquarter? (% critical )

Source: FBC-FBG survey Jan 2010

Back up from 2011 survey

130618-FBC and FBG survey v1DUB

15100208-FBC and FBG survey v1 as presented

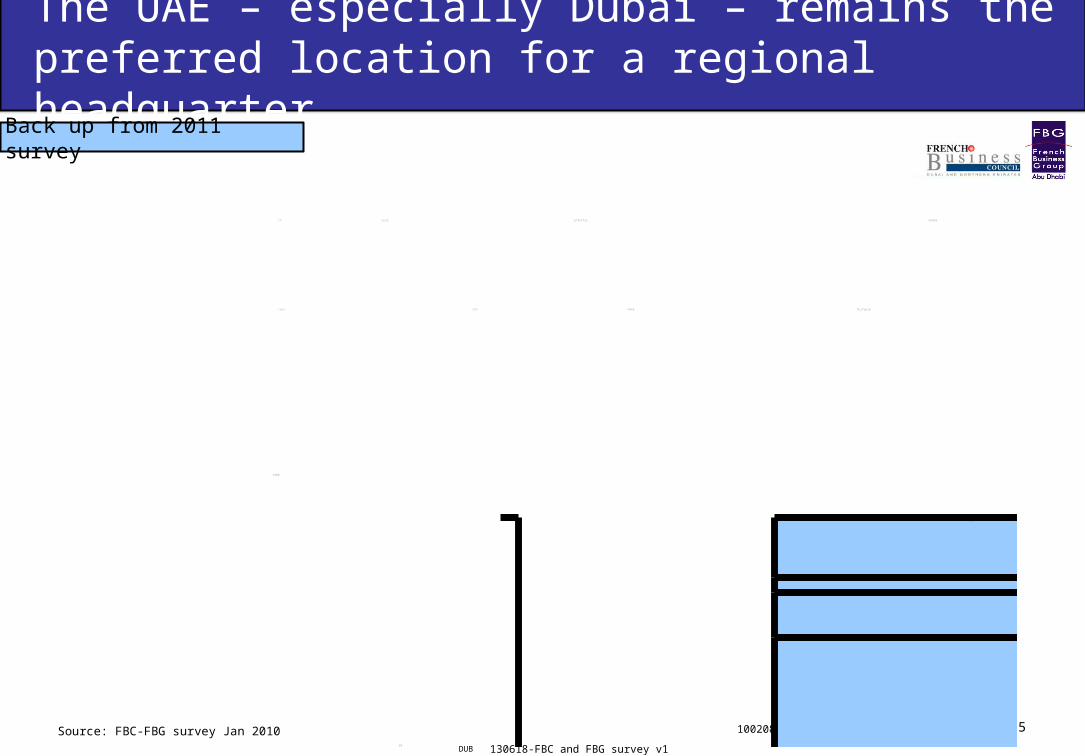

The UAE – especially Dubai – remains the preferred location for a regional headquarter

0

20

40

60

80

100%

Q2 2009

Other Countries of the GCC

Egypt

Levant

Qatar

KSA

UAE – Other cities

UAE – Dubai

UAE – Abu Dhabi

180

H2 2010

Other Countries of the GCC

Egypt

UAE – Other cities

UAE – Dubai

UAE – Abu Dhabi

91

In your industry, where is the best location to setup a headquarter to serve the region?

(you can make multiple choices )

Source: FBC-FBG survey Jan 2010

Back up from 2011 survey