Download - Bus ethics csr 13 2013 1-2

Corporate Social ResponsibilityWhat is CSR?• “Is the overall relationship of the corporation with all of its stakeholders.

• Elements of social responsibility include investment in community outreach, employee relations, creation and maintenance of employment, environmental stewardship, and financial performance.”

• A corporation should act in a way that enhances society and its inhabitants and be held accountable for any of its actions that affect people, their communities, and their environment

– ‘Is the continuing commitment by business to behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well as of the local community and society at large’. – World Business Council For Sustainable Development

• “CSR is generally understood to be the way a company achieves a balance or integration of economic, environmental and social imperatives while at the same time addressing shareholder and stakeholder expectations.” (Canadian Govt)

Terminologies of CSR

The term [CSR] is often used interchangeably with others, including

• Corporate responsibility• Corporate citizenship• Social enterprise • Corporate conscience • Sustainability • Sustainable development • Sustainable responsible business/ responsible Business • Social performance • Triple-bottom line • Corporate ethics• and in some cases corporate governance.

• Though these terms are different, they all point in the same direction:

• Throughout the industrialised world and in many developing countries there has been a sharp escalation in the social roles corporations are expected to play.

Ethics and CSR

Why growing Interest and Awareness of Ethics and CSR?

• High-profile scandals and unethical behaviour

• Demand for ethical behaviour

• Globalisation and instant communications

• Public awareness and consumer behaviour

• Reputational risk

• Used as a ‘competitive advantage’

• Offensive and defensive marketing

Drivers of CSR

• Values - a value shift has taken place within businesses where they not only feel responsibility for wealth creation but also for social and environmental goods.

• Strategy - being more socially and environmentally responsible is important for the strategic development of a company.

• Public Pressure - pressure groups, consumers, media, the state and other public bodies are pressing companies to become more socially responsible.

Theories of Social Responsibility

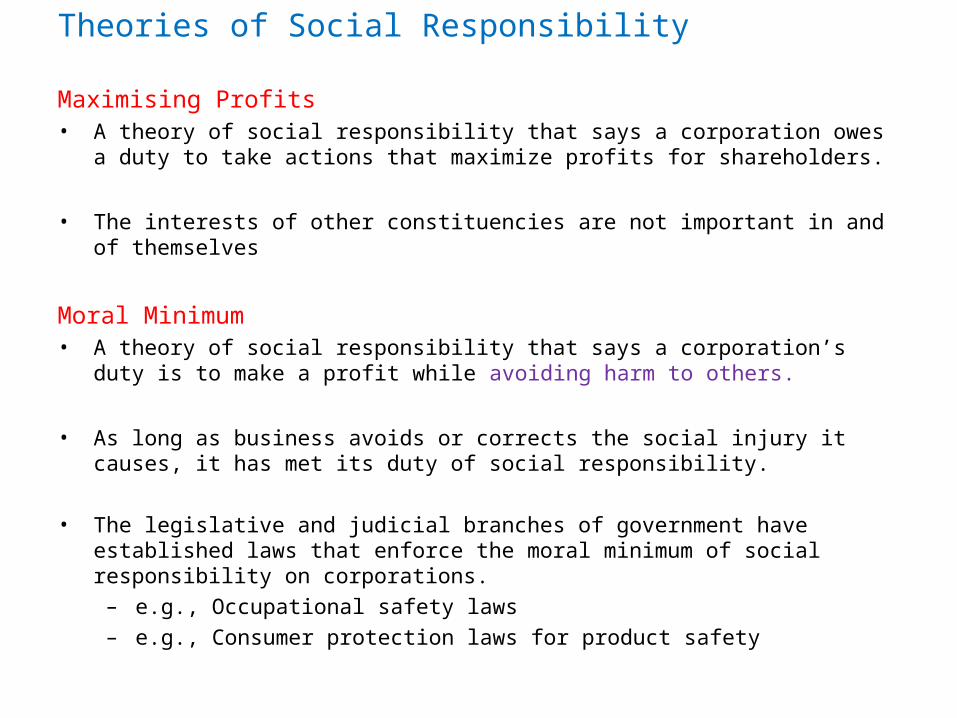

Maximising Profits

Moral Minimum

Stakeholder Interest

Corporate Citizenship

Theories of Social Responsibility

Maximising Profits• A theory of social responsibility that says a corporation owes a duty to take

actions that maximize profits for shareholders.

• The interests of other constituencies are not important in and of themselves

Moral Minimum• A theory of social responsibility that says a corporation’s duty is to make a

profit while avoiding harm to others.

• As long as business avoids or corrects the social injury it causes, it has met its duty of social responsibility.

• The legislative and judicial branches of government have established laws that enforce the moral minimum of social responsibility on corporations.

– e.g., Occupational safety laws– e.g., Consumer protection laws for product safety

Theories of Social Responsibility

Stakeholder Interest• A theory of social responsibility that says a corporation must consider the effects its

actions have on persons other than its stockholders.

• This theory is criticised because it is difficult to harmonise the conflicting interests of stakeholders.

Corporate Citizenship• A theory of responsibility that says a business has a responsibility to do good.

• Business is responsible for helping to solve social problems.

• Corporations owe a duty to promote the same social goals as do individual members of society.

• This theory argues that corporations owe a debt to society to make it a better place.

– This duty arises because of the social power bestowed on corporations.

• A major criticism of this theory is that the duty of a corporation to “do good” cannot be expanded beyond certain limits.

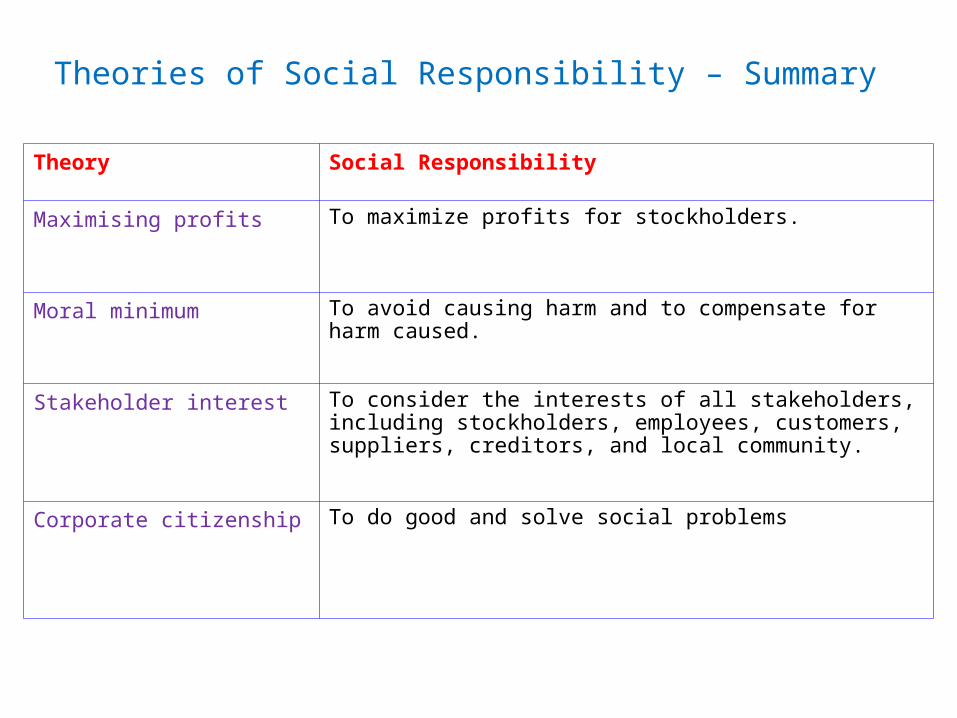

Theories of Social Responsibility – Summary

Theory Social Responsibility

Maximising profits To maximize profits for stockholders.

Moral minimum To avoid causing harm and to compensate for harm caused.

Stakeholder interest To consider the interests of all stakeholders, including stockholders, employees, customers, suppliers, creditors, and local community.

Corporate citizenship To do good and solve social problems

The Corporate Social Audit• A social audit is an attempt to measure a company’s actual social

performance against its social objectives.

• The social audit may be used for more than simply monitoring and evaluating firm social performance.

• Corporate audits should be extended to include the moral health of the corporation.

• Corporations that conduct social audits will be more apt to prevent unethical and illegal conduct by managers, employees, and agents.

• The audit would examine how well:– Employees have adhered to the company’s code of ethics; and– The corporation has met its duty of social responsibility.

• Such audits would focus on the corporation’s efforts to:– Promote employment opportunities for members of protected classes– Worker safety– Environmental protection– Consumer protection

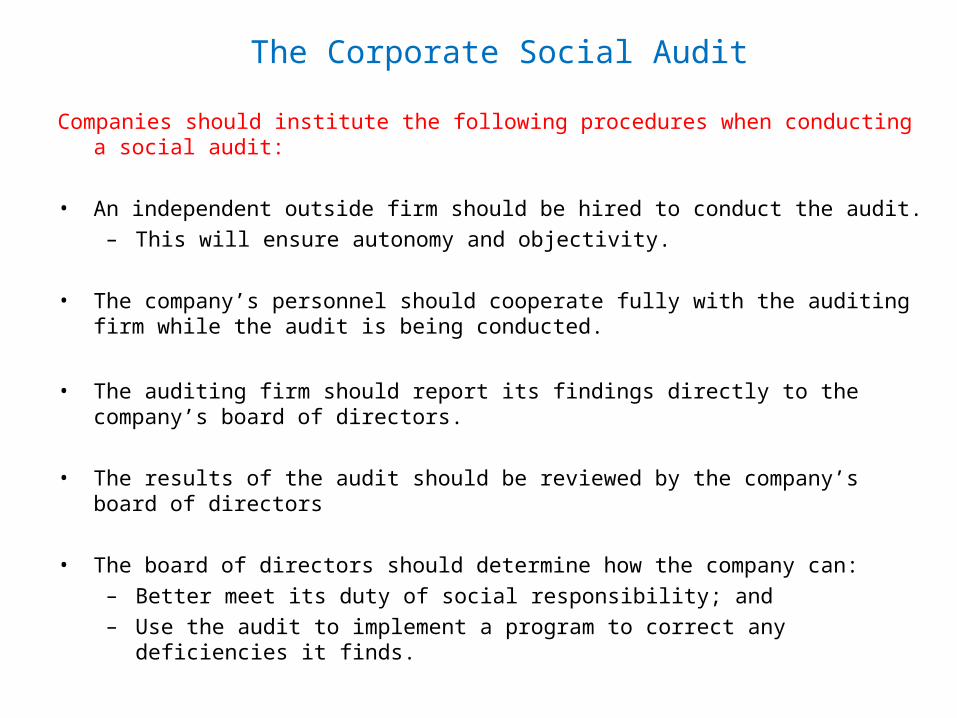

The Corporate Social Audit Companies should institute the following procedures when conducting a social

audit:

• An independent outside firm should be hired to conduct the audit.– This will ensure autonomy and objectivity.

• The company’s personnel should cooperate fully with the auditing firm while the audit is being conducted.

• The auditing firm should report its findings directly to the company’s board of directors.

• The results of the audit should be reviewed by the company’s board of directors

• The board of directors should determine how the company can:– Better meet its duty of social responsibility; and– Use the audit to implement a program to correct any deficiencies it finds.

The Clarkson Principles

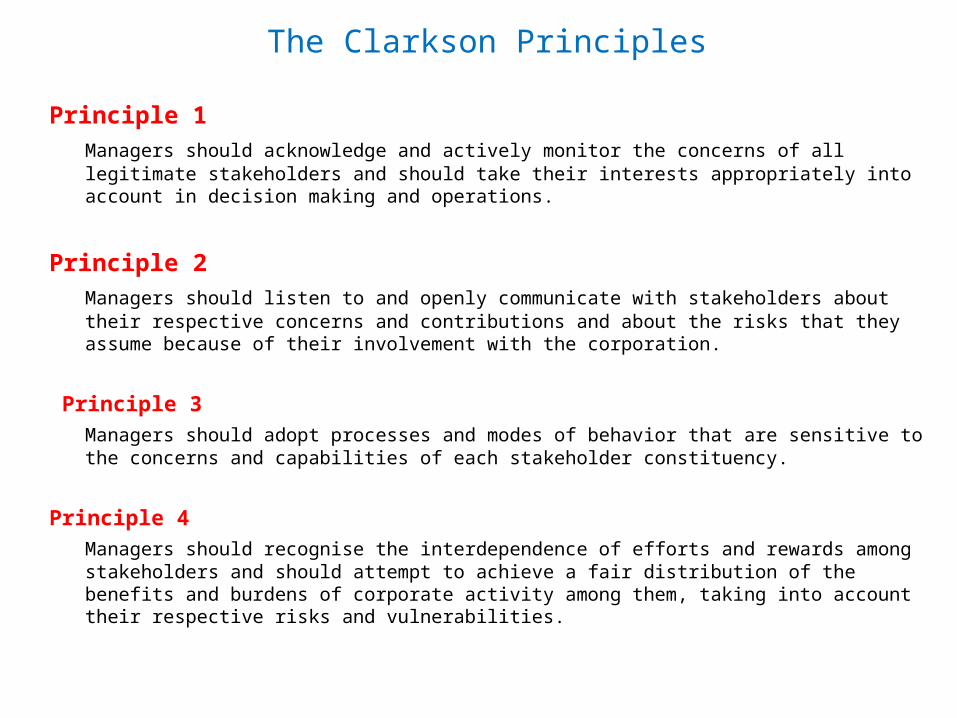

Principle 1Managers should acknowledge and actively monitor the concerns of all legitimate stakeholders and should take their interests appropriately into account in decision making and operations.

Principle 2Managers should listen to and openly communicate with stakeholders about their respective concerns and contributions and about the risks that they assume because of their involvement with the corporation.

Principle 3Managers should adopt processes and modes of behavior that are sensitive to the concerns and capabilities of each stakeholder constituency.

Principle 4Managers should recognise the interdependence of efforts and rewards among stakeholders and should attempt to achieve a fair distribution of the benefits and burdens of corporate activity among them, taking into account their respective risks and vulnerabilities.

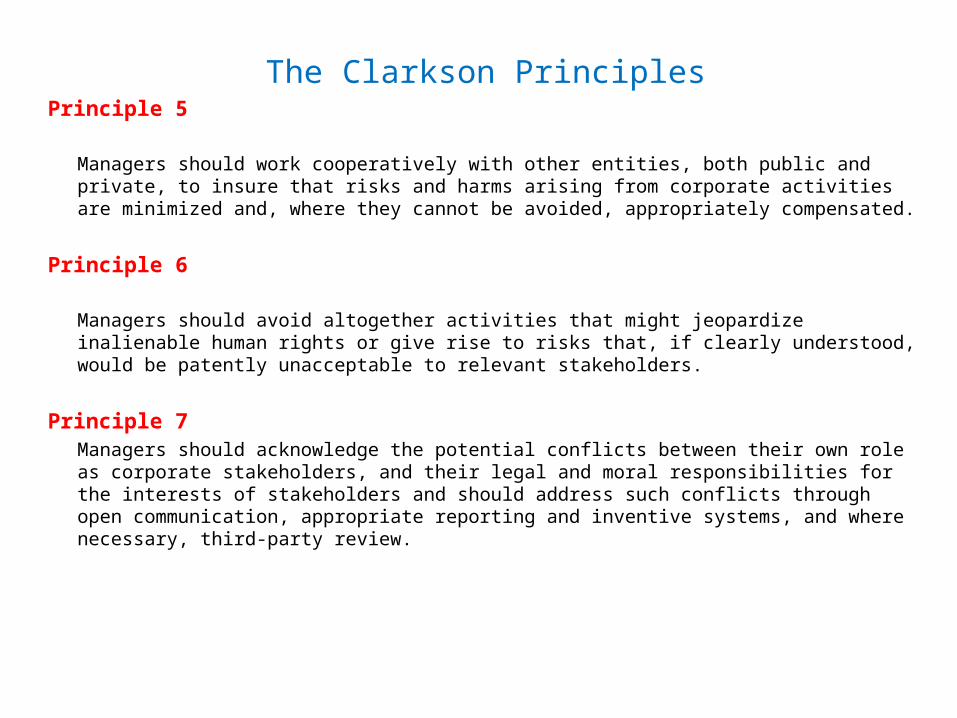

The Clarkson PrinciplesPrinciple 5

Managers should work cooperatively with other entities, both public and private, to insure that risks and harms arising from corporate activities are minimized and, where they cannot be avoided, appropriately compensated.

Principle 6

Managers should avoid altogether activities that might jeopardize inalienable human rights or give rise to risks that, if clearly understood, would be patently unacceptable to relevant stakeholders.

Principle 7Managers should acknowledge the potential conflicts between their own role as corporate stakeholders, and their legal and moral responsibilities for the interests of stakeholders and should address such conflicts through open communication, appropriate reporting and inventive systems, and where necessary, third-party review.

Social Responsibility Strategies

• Reactive Strategy– Denying responsibility while striving to maintain the status quo by

resisting change

• Defensive Strategy– Resisting additional social responsibilities with legal and public

relations tactics

• Accommodation Strategy– Assuming social responsibility only in response to pressure from

interest groups or the government

• Proactive Strategy– Taking the initiative in formulating and putting in place new programs

that serve as role models for industry

Social Responsibility Strategies

Key Components of CSR Best Practices

Key Components of CSR Best PracticesStrategic Partnerships

•Partnership = new development approach favoured by the multilateral and bilateral donor community, industry, public and private sector organizations.

• Advantages include pooling resources, building respect and understanding between potential adversaries, and transferring knowledge.

• Tri-sector partnerships requires business, government and civil society to pull together complementary resources.

Key Components of CSR Best Practices

Stakeholder Engagement

•Stakeholders are individuals or groups who have a vested interest in a company’s operations, who interact with a company in one or more of its activities and whose co-operation or active involvement a company needs for its ‘license to operate’.

• Engagement methods include consultation papers, perception surveys, stakeholder workshops, public and private meetings, liaison groups and academic roundtables.

• The overall success of the engagement process will depend to a large extent on corporate communication.

Key Components of CSR Best Practices

Public Sector Support

a) Mandating - define minimum standards for business performance. b) Facilitating - provide incentives for companies to engage with the CSR agenda.

c) Partnering - act as participants, convenors or facilitators.

d) Endorsing - direct recognition of the efforts of individual enterprises through award schemes or ‘honourable mentions’ in speeches by top government officials.

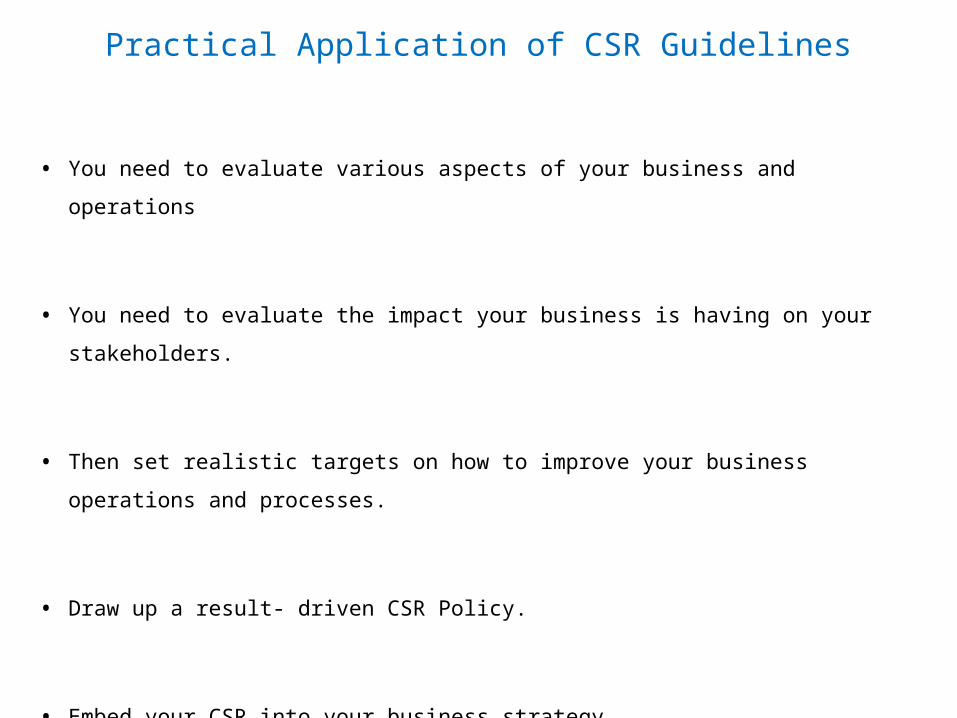

Practical Application of CSR Guidelines

• You need to evaluate various aspects of your business and operations

• You need to evaluate the impact your business is having on your stakeholders.

• Then set realistic targets on how to improve your business operations and processes.

• Draw up a result- driven CSR Policy.

• Embed your CSR into your business strategy.

Practical Application of CSR Guidelines

• Appoint a driver for your CSR initiative

• Communicate your CSR efforts to all your stakeholders clearly and boldly.

• Make your CSR initiative part of your business culture

• Set up CSR measuring indicators to monitor progress and possible deviations.

• Be enthusiastic about your CSR initiative; be committed to it.

• Report on your initiatives and measure progress/ impact made.

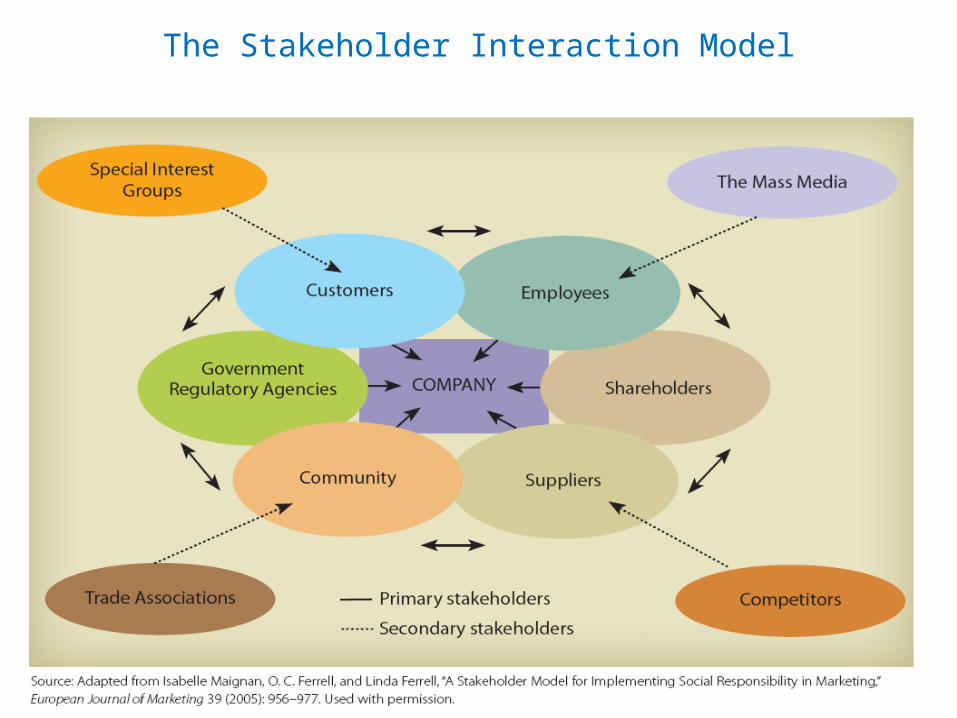

Business Organisations’ Stakeholders

A stakeholder is as any group or individual who is ‘either harmed by or benefits from the organisation; or whose rights can be violated or have to be respected, by the corporation’ Evan and Freeman (1993)

Primary vs. Secondary Stakeholders

• Primary stakeholders: those whose continued association is necessary for a firm’s survival

– Employees, customers, investors, governments and communities

• Secondary stakeholders: are not essential to a company’s survival– Media, trade associations, and special interest groups

The Stakeholder Interaction Model

Business Organisations’ Stakeholders

Government Taxation, Legislation

Customer Value, Quality, safety

Creditor Credit score, new contracts, Liquidity

Shareholder Profit, Performance, Direction

Trade Union Working conditions, Minimum wage

Local Community Jobs, Involvement, Environmental issues

Stakeholder Examples of interests

Business Organisations’ Stakeholders

environment pollution control, protection of environment

Non-Managerial staff Job security, Living salary

Suppliers Trade credit obligations

Senior Management staff Performance, Targets

Stakeholder Examples of interests

Media dissemination to the public

Senior Management staff Performance, Targets

Trade Unions

Special Interest Groups

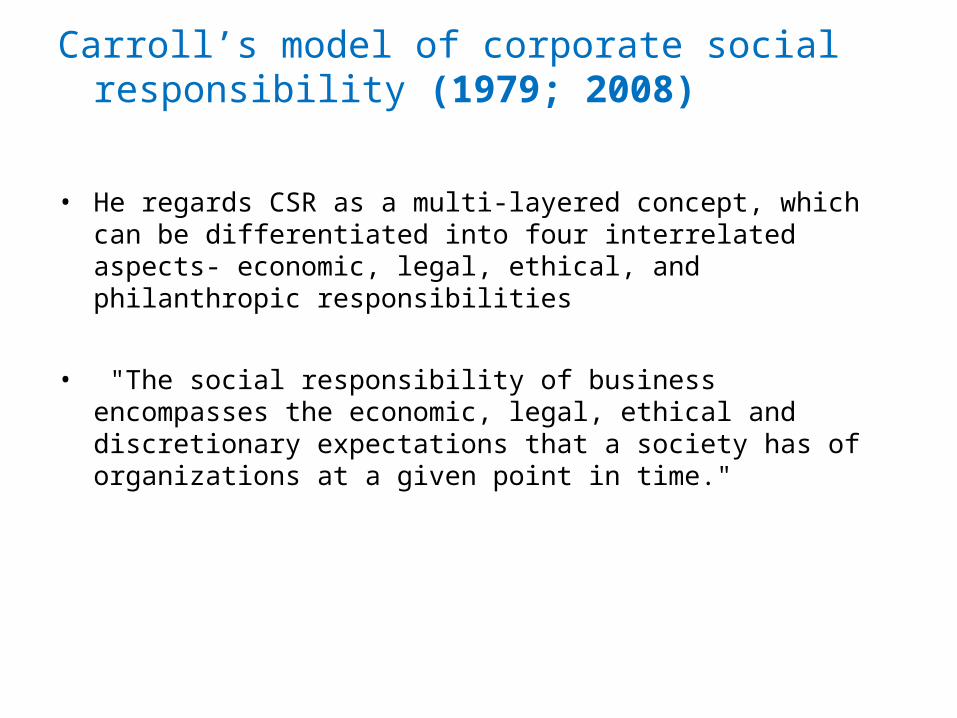

Carroll’s model of corporate social responsibility (1979; 2008)

• He regards CSR as a multi-layered concept, which can be differentiated into four interrelated aspects- economic, legal, ethical, and philanthropic responsibilities

• "The social responsibility of business encompasses the economic, legal, ethical and discretionary expectations that a society has of organizations at a given point in time."

Carroll’s Model of Corporate Social Responsibility

The Pyramid of Social Responsibility

Carroll’s model of corporate social responsibility

a) Economic: Companies have shareholders who demand a reasonable return on their

investments, they have employees who want safe and fairly paid jobs, they have customers who demand good-quality products at a fair price.

b) Legal : The legal responsibility of corporation demands that business abide by the law

and play by the rules of the game. Laws are the codification of society’s moral views.

The satisfaction of legal responsibilities is required of all corporations seeking to be socially responsible.

Carroll’s model of corporate social responsibility

C) Ethical : These responsibilities oblige corporations to do what is right, just, and fair even

when they are not compelled to do so by the legal framework.

Carroll argues ethical responsibilities consist of what is generally expected by society over and above economic and legal requirements.

d) Philanthropic: It means literally ‘the love of the fellow human’ The model includes all those issues that are within the corporation’s discretion to

improve the quality of life of employees, local communities and ultimately society in general.

Benefits of CSRLegislative Framework

Benefits of CSR

Winning new businesses

Enhancing your influence in the

industry

Attracting, Retaining and

Maintaining a happy workforce

Increase in customer retention

Differentiating yourself from the

competitor

Saving money on energy and operating cost

Access to funding opportunities

Media interestand goodreputation

Bene

fits

Bene

fits

Enhanced Relationship with

stakeholders

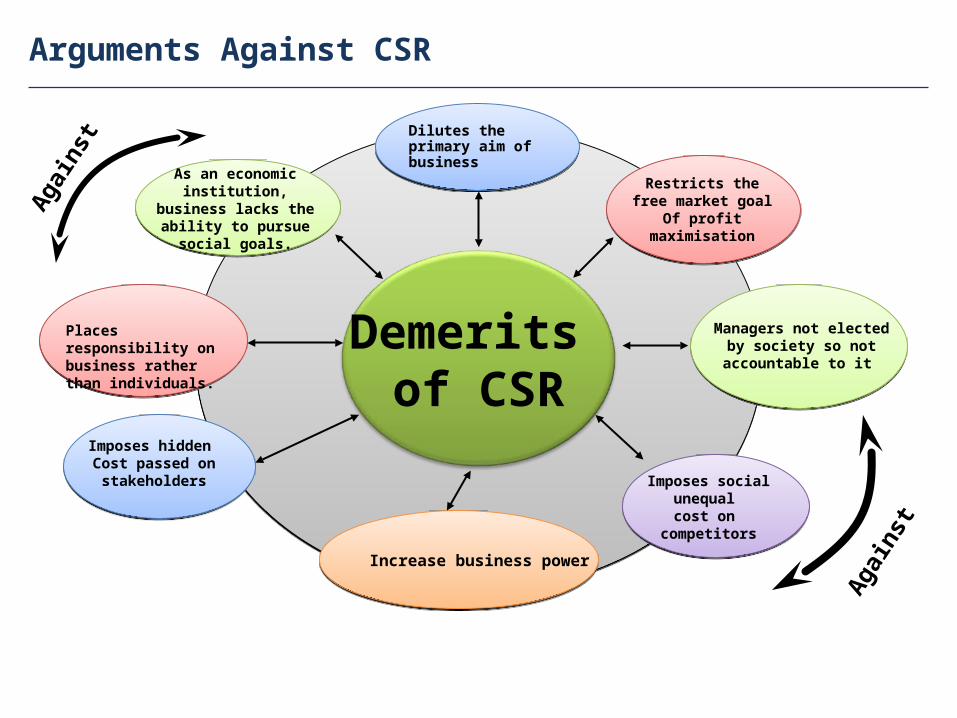

Arguments Against CSRLegislative Framework

Demerits of CSR

Dilutes the primary aim of business

Increase business power

Managers not elected by society so not

accountable to it

As an economic institution, business lacks the ability to

pursue social goals.

Imposes hidden Cost passed on

stakeholders

Places responsibility on business rather than individuals.

Imposes social unequal cost on

competitors

Again

st

Again

st

Restricts the free market goal

Of profit maximisation

Corporate Benefits of CSR

• Building a strong corporate reputation, image and clout as well as strengthen brand positioning

• Attracting and retaining a motivated workforce

• Reducing risks and operating costs

• Reducing regulatory oversight by working closely with regulatory agencies to meet or exceed guidelines

• Increased appeal to investors and financial analysts.

• Building strong community relationships with organisations and agencies that can provide technical expertise.

The Social Contract

32

The OrganisationThomas Hobbes,

John Locke &Jean-Jacques Rousseau

(1600s & 1700s)

Individuals

Other Organisations

Government

Society

The Social Contract Theory Social Contract

--set of written and unwritten rules and assumptions about acceptable interrelationships among various elements of society - hiring minorities

Organisational Stakeholder --individual or group whose interests are affected by organisational activities

Obligations to Other Organisations --managers must be concerned with relationships with other organisations, both like their own (such as competitors) and very different ones

Obligations to Government --expect to work with government agencies

Obligations to Individuals

--certain obligations to organisation’s employees- Voting and Jury Duty