Ben Is Back:Lessons and Ideas from Benjamin Graham

Jason Zweig

Money Magazine

Equity Research & Valuation Conference

AIMR, Philadelphia, Dec. 3, 2003

Did Ben Ever Go Away?

• “You have to throw out all of the matrices and formulas and texts that existed before the Web…. If we used any of what Graham and Dodd teach us, we wouldn’t have a dime under management.”– James J. Cramer, thestreet.com, Feb. 29, 2000

• “[My books] have probably been read and disregarded by more people than any book on finance that I know of.” – Benjamin Graham, in The New York Times, May 5, 1974

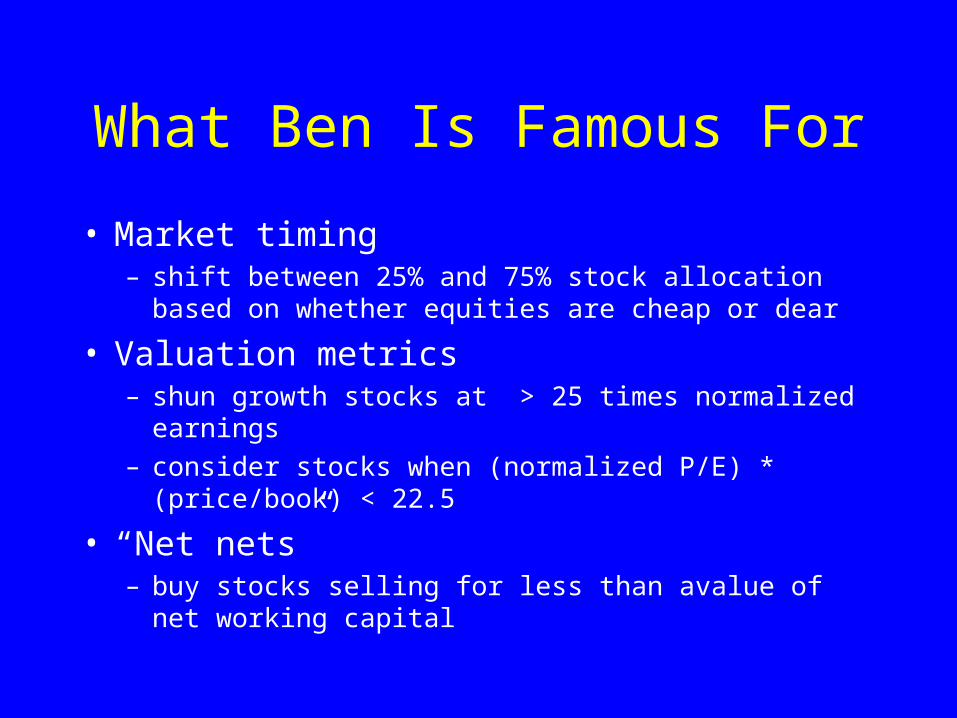

What Ben Is Famous For

• Market timing – shift between 25% and 75% stock allocation based on

whether equities are cheap or dear

• Valuation metrics– shun growth stocks at > 25 times normalized earnings

– consider stocks when (normalized P/E) * (price/book) < 22.5

• “Net nets”– buy stocks selling for less than avalue of net working capital

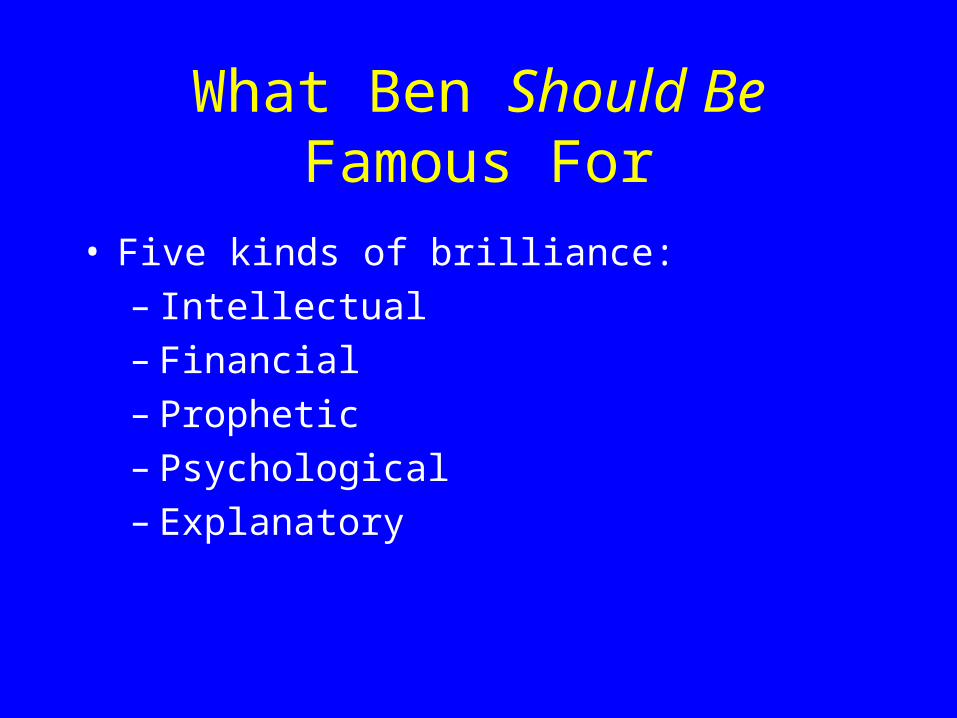

What Ben Should Be Famous For

• Five kinds of brilliance:– Intellectual– Financial– Prophetic– Psychological– Explanatory

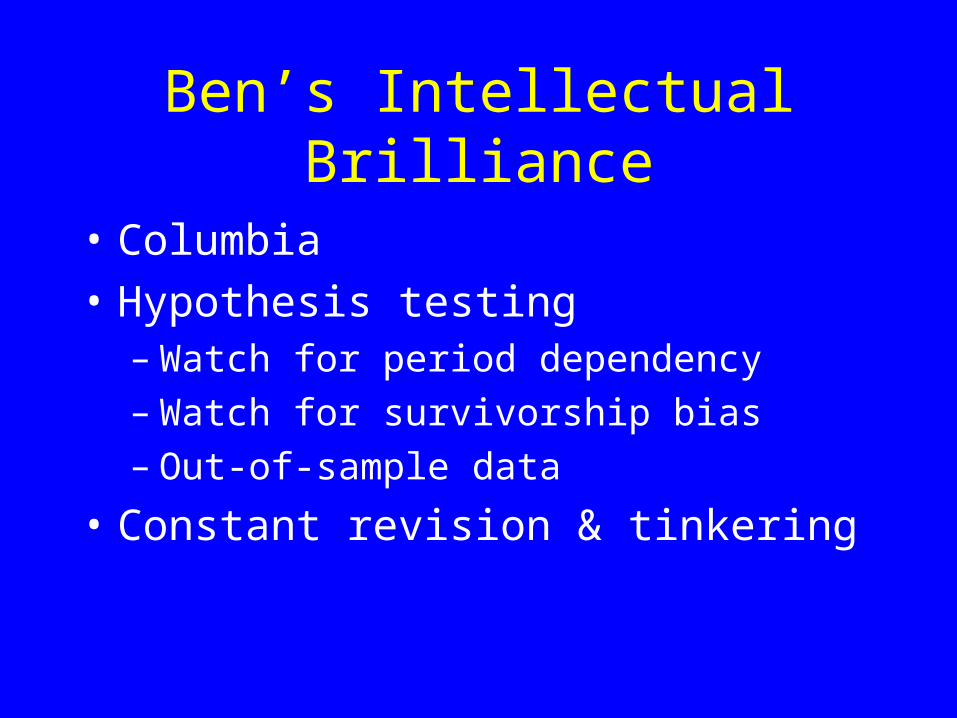

Ben’s Intellectual Brilliance

• Columbia

• Hypothesis testing– Watch for period dependency– Watch for survivorship bias– Out-of-sample data

• Constant revision & tinkering

Ben’s Investment Brilliance

• 1936-1956

• Graham-Newman Corp.: 14.7%

• S&P 500: 12.2%

Ben’s Prophetic Brilliance

• The “new era” autopsy– Graham & Dodd, 1934

• “Can such heedlessness go unpunished? We think the investor must be prepared for difficult times ahead -- perhaps in the form of a fairly quick replay of the 1969-1970 decline, or perhaps in the form of another bull market fling, to be followed by another catastrophic collapse.”– Benjamin Graham, 1972

Ben’s Psychological Brilliance• “The investor’s chief problem -- and even his worst enemy -- is

likely to be himself.” (Introduction) • The best investing advice is not theoretically ideal, but

psychologically practical.• “The chief advantage, perhaps, is that such a formula will give

him something to do.” (Chapter 8)• Mad money (Chapter 1)• The margin of safety (Chapter 20)• “The speculative public is incorrigible. In financial terms it

cannot count beyond 3. It will buy anything, at any price, if there seems to be some ‘action’ in progress.” (Chapter 17)

Neuroscience and Ben Graham

…

Stimulus Onset Asynchrony: 2000 ms

Stimulus Duration: 250 ms

a

b

Repeating Pattern

Alternating Patterns

…

Courtesy Prof. Scott A. Huettel, Duke University

Neuroscience and Benjamin Graham

Random-order sequence with fixed probability p (G) = 0.8 p (R) = 0.2 Subjects explicitly informed that order of series is

random & unpredictable Subjects allowed to try predicting the next outcome

anyway

The Prediction Addiction What’s the optimal strategy?

p (G) = 0.8p (R) = 0.2

If you never guess R, you’ll be right 80% of the time If you guess R 20% of the time, your accuracy rate will be 68% (0.2

* 0.2 + 0.8 * 0.8) Rewarded with grain or fruit, rats and pigeons soon learn to choose

G all the time Humans will persist in guessing G or R for hundreds if not

thousands of trials. [ > data = higher confidence!] “Nearly everyone interested in common stocks wants to be told by

someone else what he thinks the market is going to do. The demand being there, it must be supplied.” (Chapter 10)

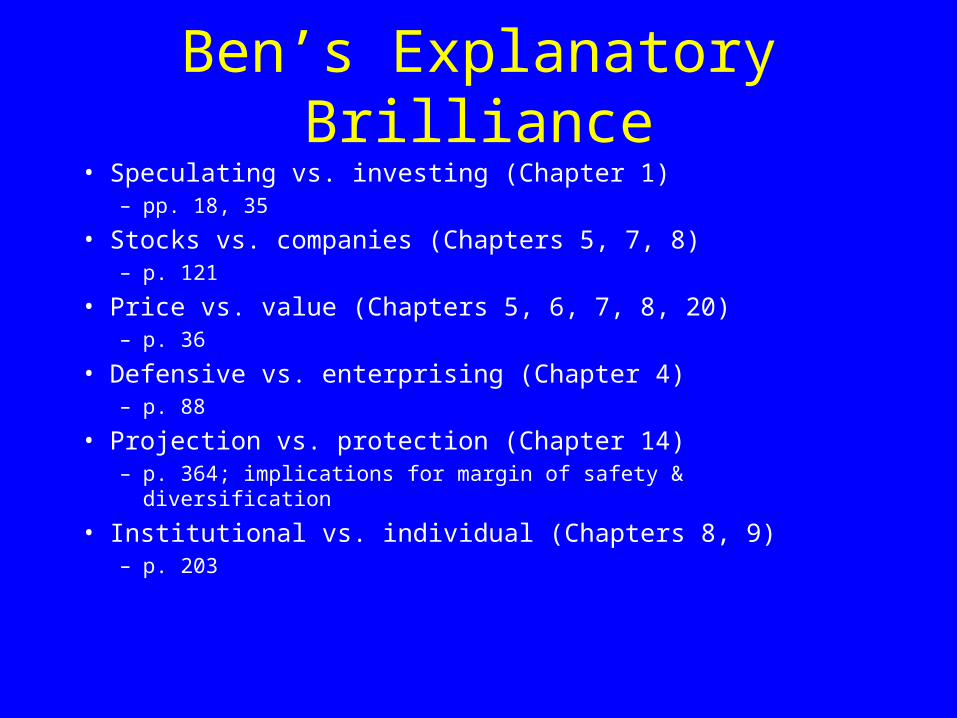

Ben’s Explanatory Brilliance• Speculating vs. investing (Chapter 1)

– pp. 18, 35

• Stocks vs. companies (Chapters 5, 7, 8)– p. 121

• Price vs. value (Chapters 5, 6, 7, 8, 20)– p. 36

• Defensive vs. enterprising (Chapter 4)– p. 88

• Projection vs. protection (Chapter 14)– p. 364; implications for margin of safety & diversification

• Institutional vs. individual (Chapters 8, 9)– p. 203

What Is an “Intelligent” Investor?• Nothing to do with IQ or SAT (or GMAT) scores• MBA, Ph.D, CFP, CPA (even CFA!) not required• “The word ‘intelligent’ in our title will be used throughout the book in its common and

dictionary sense as meaning ‘endowed with the capacity for knowledge and understanding.’ It will not be taken to mean ‘smart’ or ‘shrewd,’ or gifted with unusual foresight or insight. Actually the intelligence here presupposed is a trait more of the character than the brain.”– Benjamin Graham, 1949 (first ed.)

• Patience• Independent thinking (p. 524)• Discipline• Eagerness to learn• Self-control (ability to harness your emotions)• Self-knowledge (in Graham’s terms); knowledge of your clients

What Is an Intelligent Owner?• The “lost Ben Graham” (Chapter 19)• Where did it go?• Northern Pipe Line, Unexcelled Manufacturing, etc. etc.• “Nothing in finance is more fatuous and harmful, in our opinion, than the firmly

established attitude of common stock investors and their Wall Street advisers regarding questions of corporate management. That attitude is summed up in the phrase: “If you

don't like the management, sell the stock.’ ” --Benjamin Graham, 1949

• “Certainly there is just as much reason to exercise care and judgment in being as in becoming a stockholder.” (p. 499)

• The “two basic questions” (p. 499)• The trouble with cash (p. 503)• Who cares about dividends? (pp. 502-511)• If it’s broke, how can you fix it? (pp. 499, 502)

Did Ben Ever Go Away?

“I read the first edition of this book early in 1950, when I was nineteen. I thought then

that it was by far the best book about investing ever written. I still think it is.”

– Warren Buffett

![A Passion for the Elements - AIMR, Tohoku Univ. · 019 ]AIMR Action Log[April 2015 - March 2016 Contents It is our great pleasure to publish Volume 8 of AIMR Magazine. Fiscal year](https://cdn.vdocuments.mx/doc/165x107/5f32efe6caee3e246a54f6b7/a-passion-for-the-elements-aimr-tohoku-univ-019-aimr-action-logapril-2015.jpg)