Paul Craven

Head of EMEA Institutional Business, GSAM

Behavioural Finance: from biases to

bubbles

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

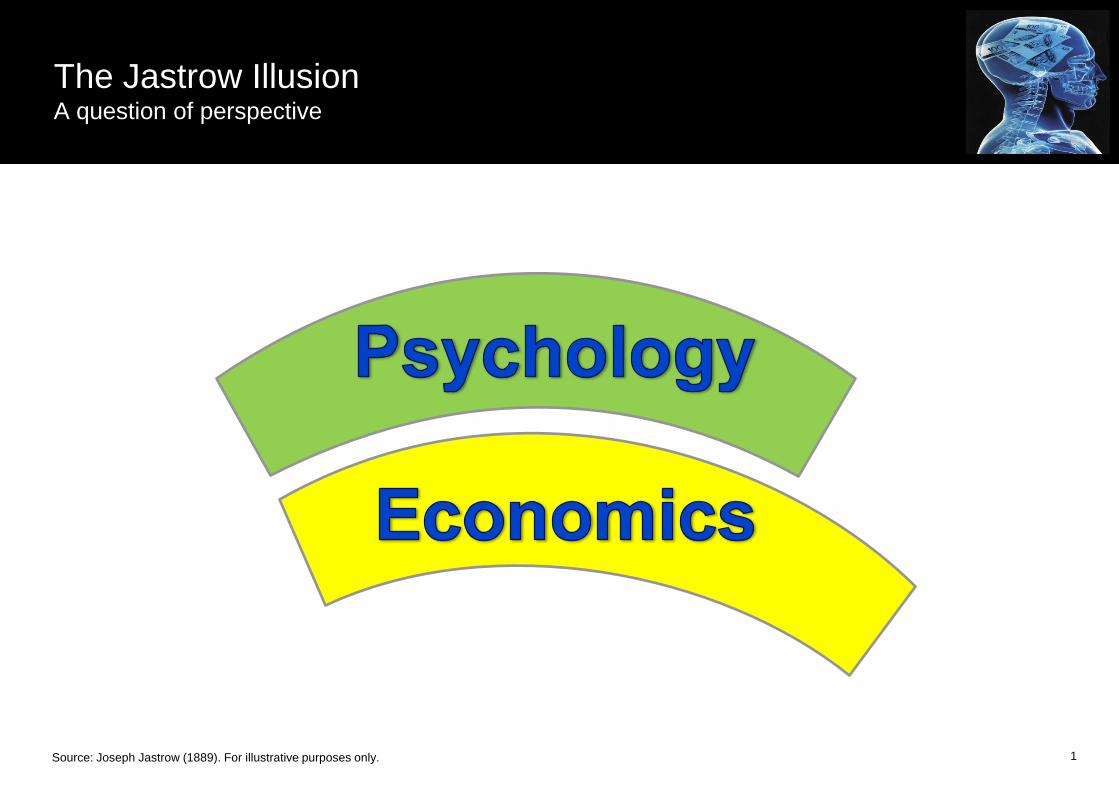

The Jastrow Illusion A question of perspective

Source: Joseph Jastrow (1889). For illustrative purposes only. 1

Today’s talk

A. How Behavioural Finance can help

System 1 vs. System 2 Thinking

Cognitive Biases - The Herd Instinct, Base Rate Neglect and Anchoring

Bubbles - Historical Examples

B. What can we do about our biases?

The Loser’s Game

Market Cap. Indices

The Wisdom of Crowds, Randomness & ‘Nudge’

2

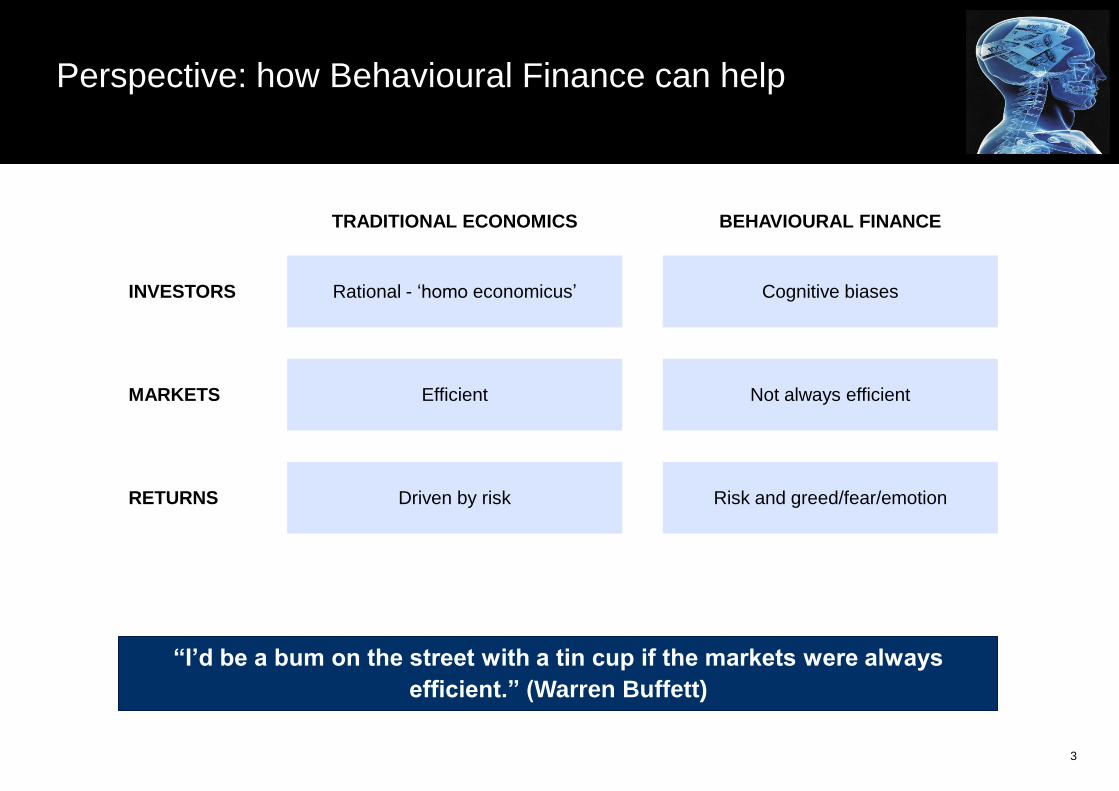

Perspective: how Behavioural Finance can help

3

“I’d be a bum on the street with a tin cup if the markets were always

efficient.” (Warren Buffett)

TRADITIONAL ECONOMICS BEHAVIOURAL FINANCE

INVESTORS

MARKETS

RETURNS

Rational - ‘homo economicus’ Cognitive biases

Efficient Not always efficient

Driven by risk Risk and greed/fear/emotion

System 1 vs. System 2 ‘Dual process’ model of the brain

4

“System 1 can never be switched off…” (Daniel Kahneman)

SYSTEM 2 – THINKING SLOW

Evolutionarily recent, rational, analytical

Source: Individual Differences in Reasoning, Keith Stanovitch and Richard West (2000), Thinking Fast and Slow, Daniel Kahneman (2011).

Hard wired, instinctive, based on intuition

SYSTEM 1 - THINKING FAST

Conscious reasoning, requires effort, slow process Unconscious reasoning, effortless, quick process

Influenced by evidence, facts and logic Influenced by emotions and memories

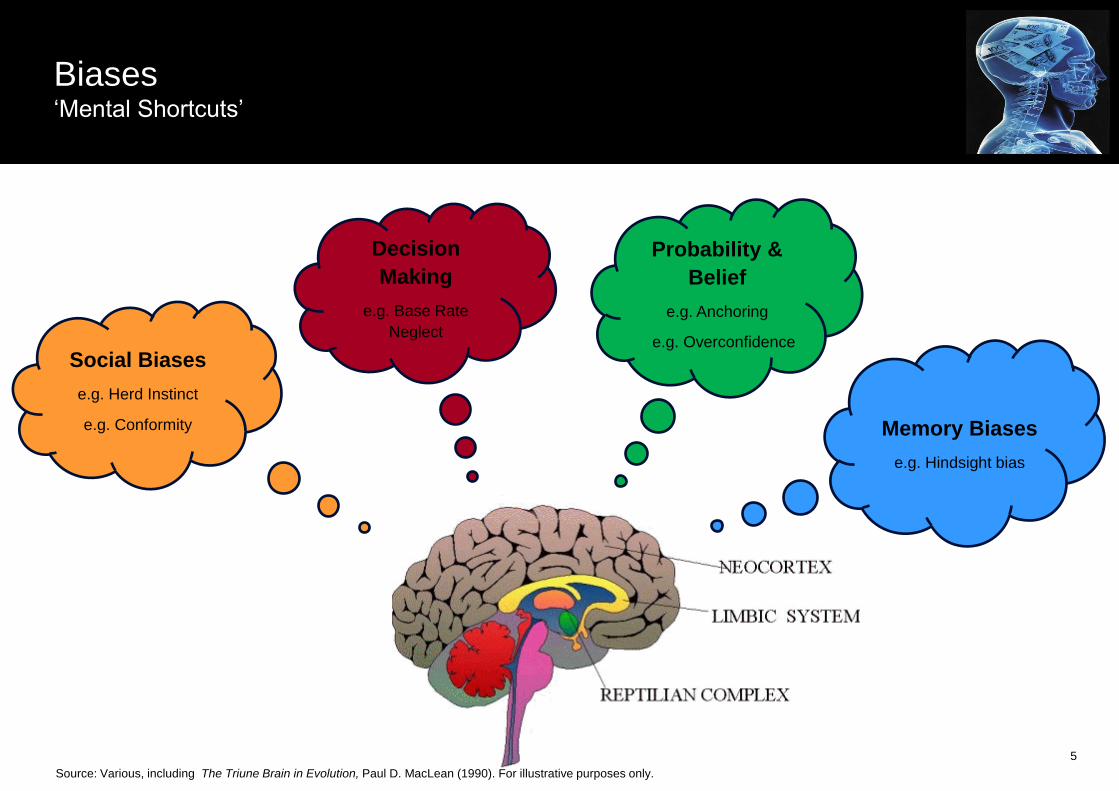

Biases ‘Mental Shortcuts’

5

Probability &

Belief

e.g. Anchoring

e.g. Overconfidence

Decision

Making

e.g. Base Rate

Neglect

Social Biases

e.g. Herd Instinct

e.g. Conformity

Memory Biases

e.g. Hindsight bias

Source: Various, including The Triune Brain in Evolution, Paul D. MacLean (1990). For illustrative purposes only.

Bias Awareness 1. The Herd Instinct

You observe other’s actions before you make your own decision.

An ‘information cascade’ arises if it becomes optimal to ignore your own information

in favour of the (inferred) information of others.

The herd instinct…

6 For illustrative purposes only.

In financial markets, the herd instinct can lead to bubbles

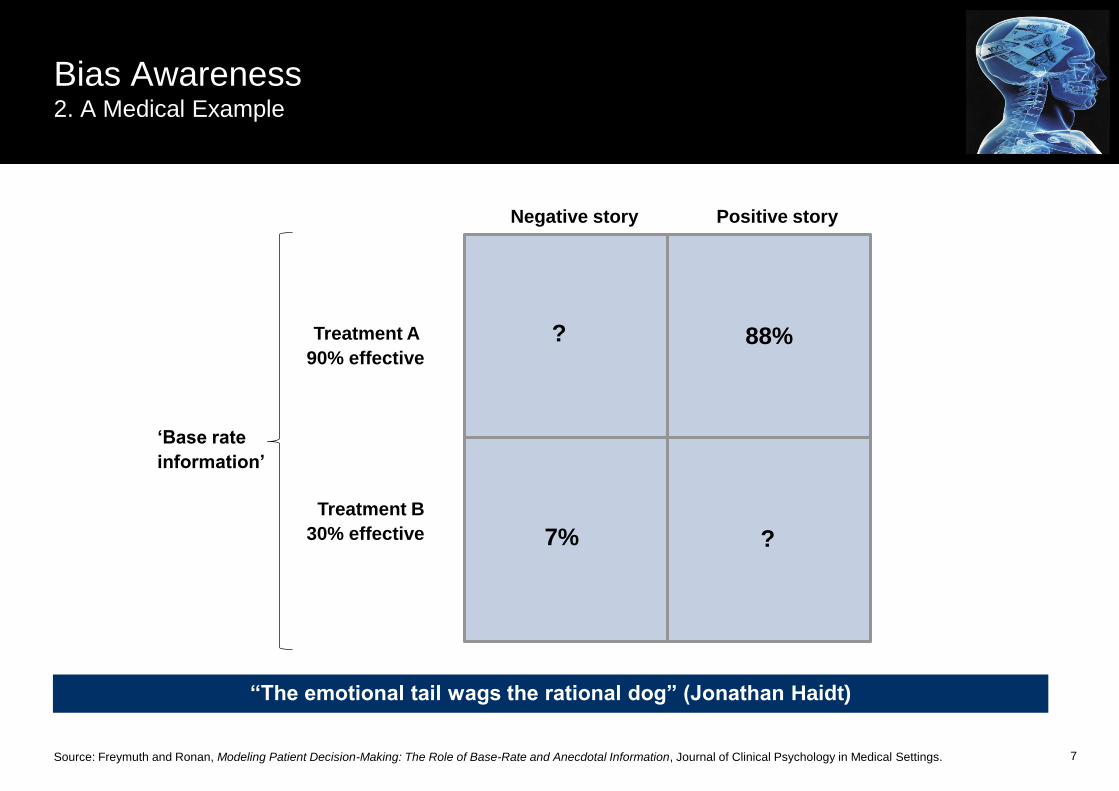

Source: Freymuth and Ronan, Modeling Patient Decision-Making: The Role of Base-Rate and Anecdotal Information, Journal of Clinical Psychology in Medical Settings. 7

“The emotional tail wags the rational dog” (Jonathan Haidt)

Negative story Positive story

88% Treatment A

90% effective

Treatment B

30% effective ? 7%

‘Base rate

information’

Bias Awareness 2. A Medical Example

?

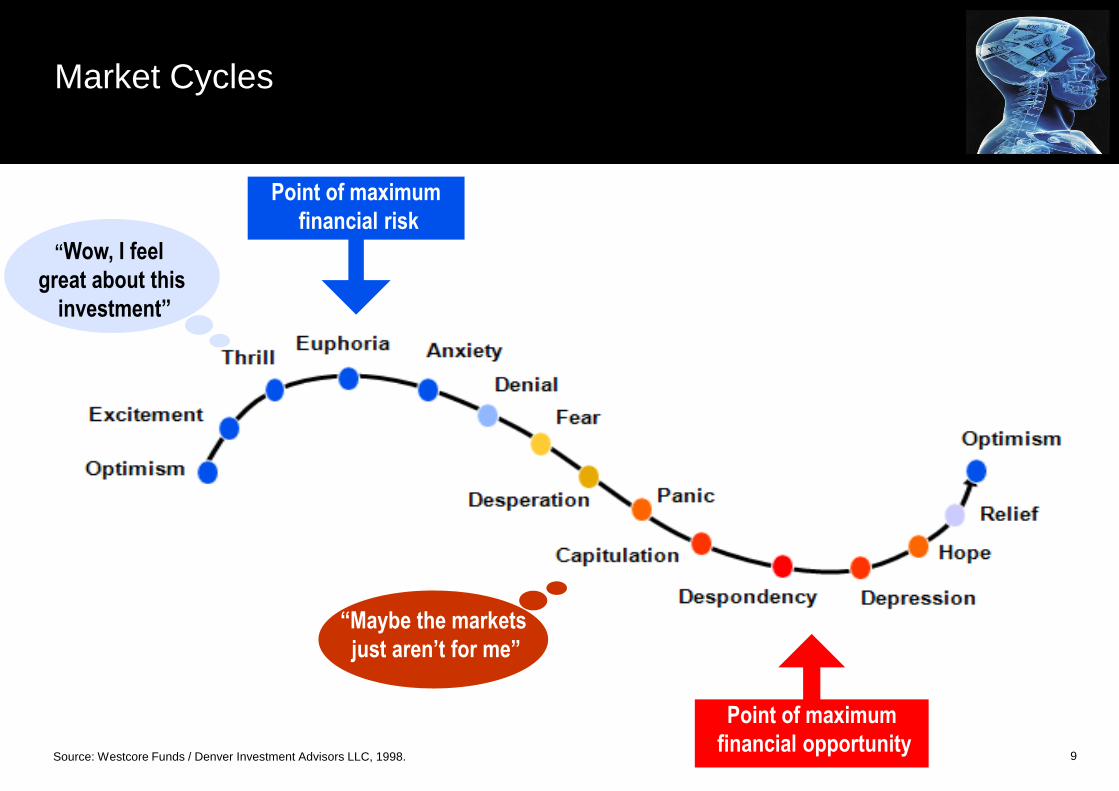

Bias Awareness 3. Anchoring

8

A cognitive bias whereby we rely too heavily on a particular piece of information

Sometimes we unconsciously or illogically anchor on irrelevant information

Important consequences for assessing probabilities

“Wow, I feel

great about this

investment”

Point of maximum

financial risk

“Maybe the markets

just aren’t for me”

Source: Westcore Funds / Denver Investment Advisors LLC, 1998.

Market Cycles

Point of maximum

financial opportunity 9

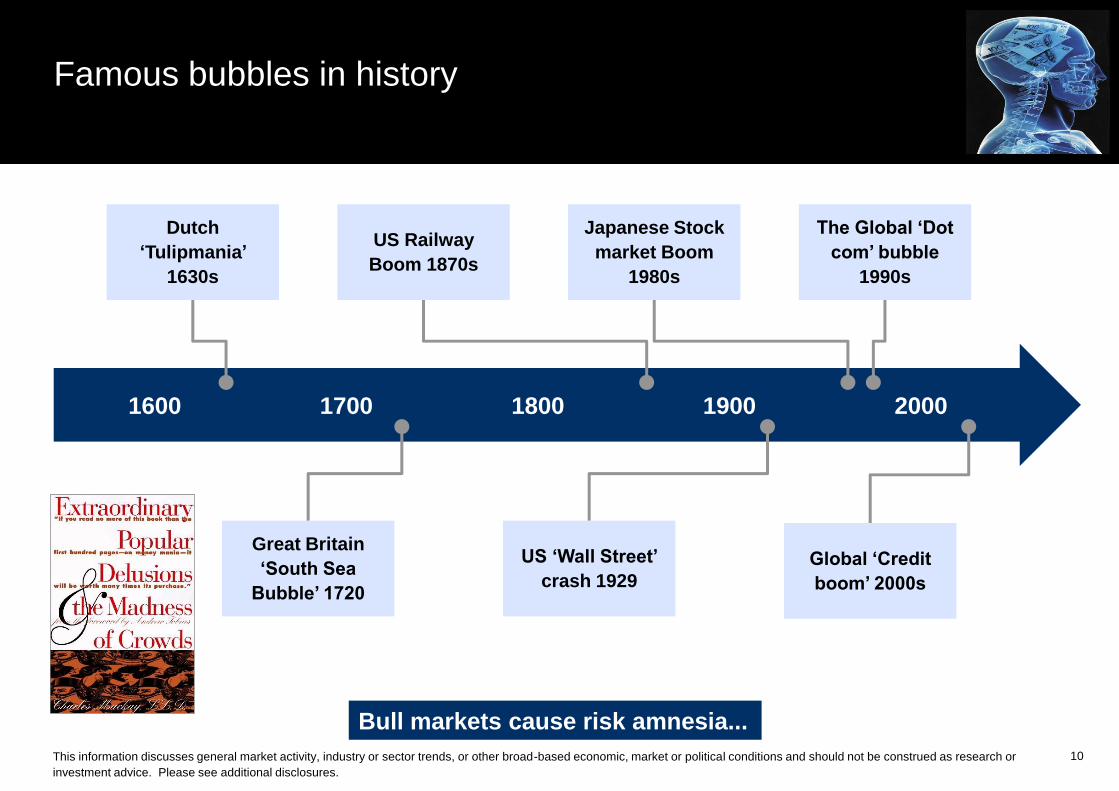

Famous bubbles in history

10

1600 1700 1800 1900 2000

Dutch

‘Tulipmania’

1630s

US Railway

Boom 1870s

Japanese Stock

market Boom

1980s

The Global ‘Dot

com’ bubble

1990s

Great Britain

‘South Sea

Bubble’ 1720

US ‘Wall Street’

crash 1929

Global ‘Credit

boom’ 2000s

Bull markets cause risk amnesia...

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. Please see additional disclosures.

Recent Bubbles An emotional rollercoaster

11

"History does not repeat itself, but it does rhyme” (Mark Twain)

Source: Dr Jean-Paul Rodrigue, Hofstra University. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political

conditions and should not be construed as research or investment advice. Please see additional disclosures.

Beware the Lazy Consensus

Source: GMO. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed

as research or investment advice. For illustrative purposes only.

12

12

10

8

6

4

2

0

-2

-4

-6

-8

Ja

n-8

6

Ja

n-8

7

Ja

n-8

8

Ja

n-8

9

Ja

n-9

0

Ja

n-9

1

Ja

n-9

2

Ja

n-9

3

Jan-9

4

Ja

n-9

5

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Jan-0

3

US

$ d

evia

tio

n f

rom

tre

nd

Earnings

Forecasts

The consensus reflects the herd instinct, base rate neglect and anchoring

B. What can we do about our biases?

The Loser’s Game

Market Cap. Indices

The Wisdom of Crowds, Randomness & ‘Nudge’

13

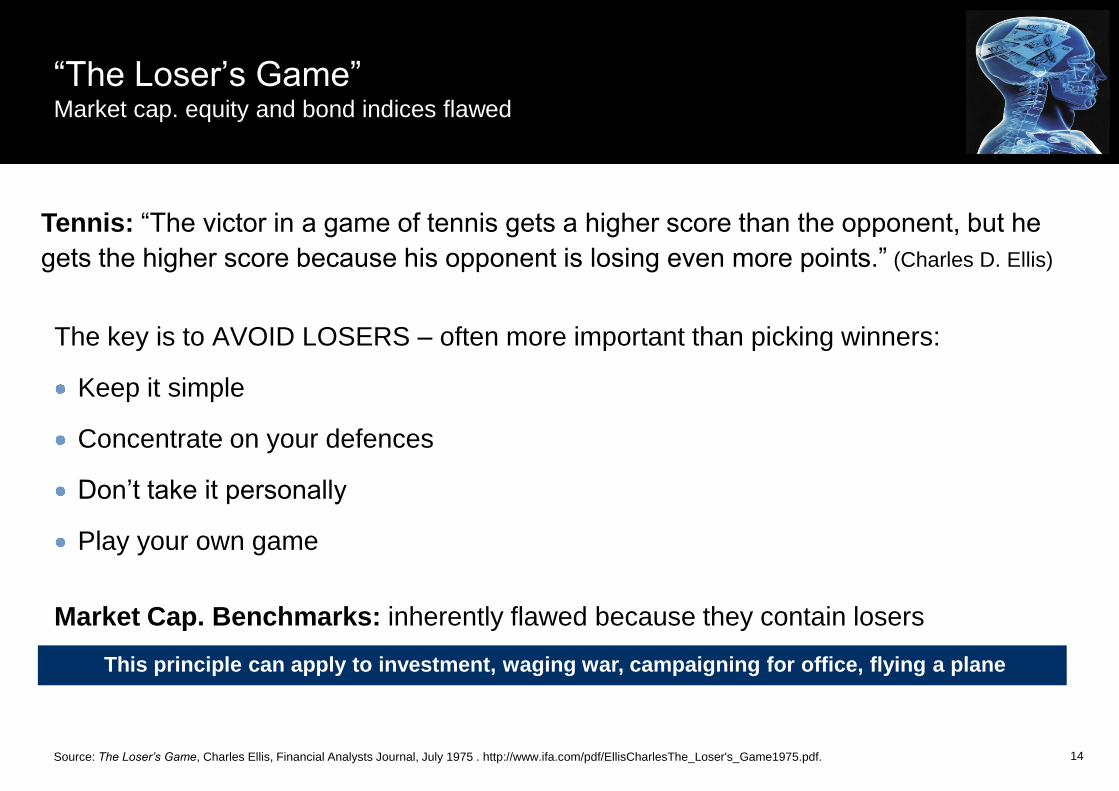

Tennis: “The victor in a game of tennis gets a higher score than the opponent, but he

gets the higher score because his opponent is losing even more points.” (Charles D. Ellis)

“The Loser’s Game” Market cap. equity and bond indices flawed

The key is to AVOID LOSERS – often more important than picking winners:

Keep it simple

Concentrate on your defences

Don’t take it personally

Play your own game

Source: The Loser’s Game, Charles Ellis, Financial Analysts Journal, July 1975 . http://www.ifa.com/pdf/EllisCharlesThe_Loser's_Game1975.pdf.

This principle can apply to investment, waging war, campaigning for office, flying a plane

Market Cap. Benchmarks: inherently flawed because they contain losers

14

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

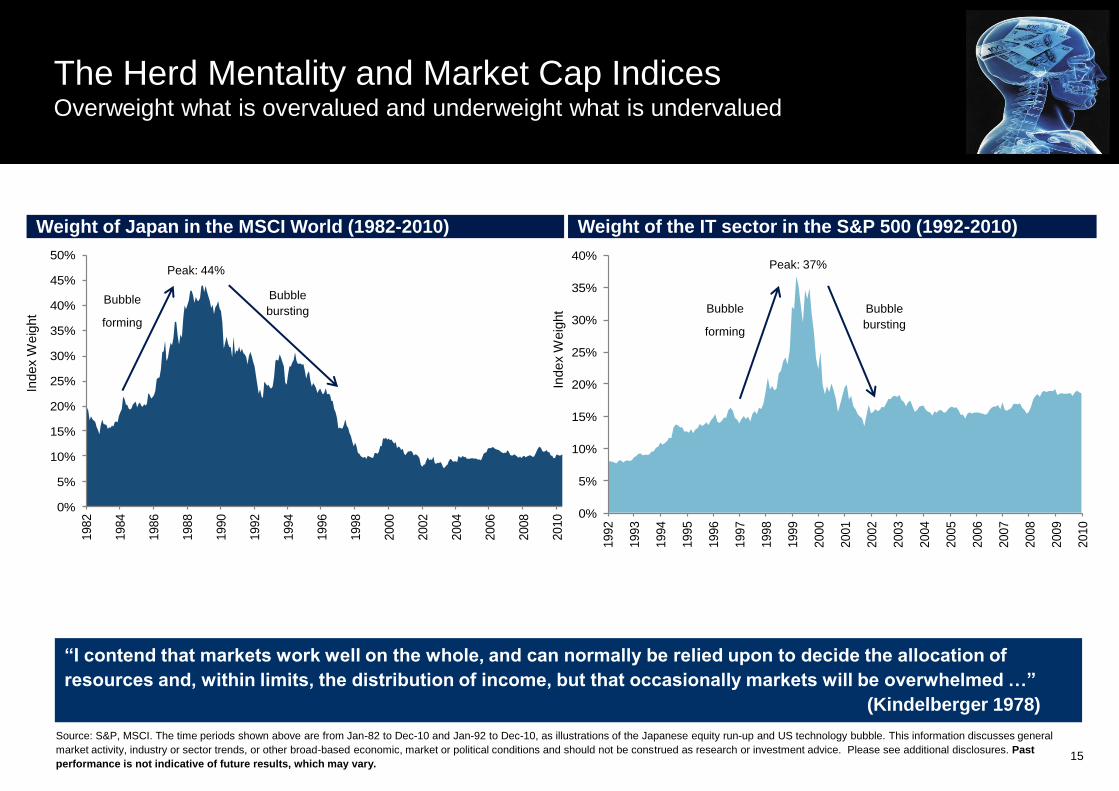

The Herd Mentality and Market Cap Indices Overweight what is overvalued and underweight what is undervalued

Source: S&P, MSCI. The time periods shown above are from Jan-82 to Dec-10 and Jan-92 to Dec-10, as illustrations of the Japanese equity run-up and US technology bubble. This information discusses general

market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Please see additional disclosures. Past

performance is not indicative of future results, which may vary.

0%

5%

10%

15%

20%

25%

30%

35%

40%

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Index W

eig

ht

Index W

eig

ht

Weight of Japan in the MSCI World (1982-2010) Weight of the IT sector in the S&P 500 (1992-2010)

Bubble

forming

Bubble

bursting Bubble

forming

Bubble

bursting

Peak: 44% Peak: 37%

“I contend that markets work well on the whole, and can normally be relied upon to decide the allocation of

resources and, within limits, the distribution of income, but that occasionally markets will be overwhelmed …”

(Kindelberger 1978)

15

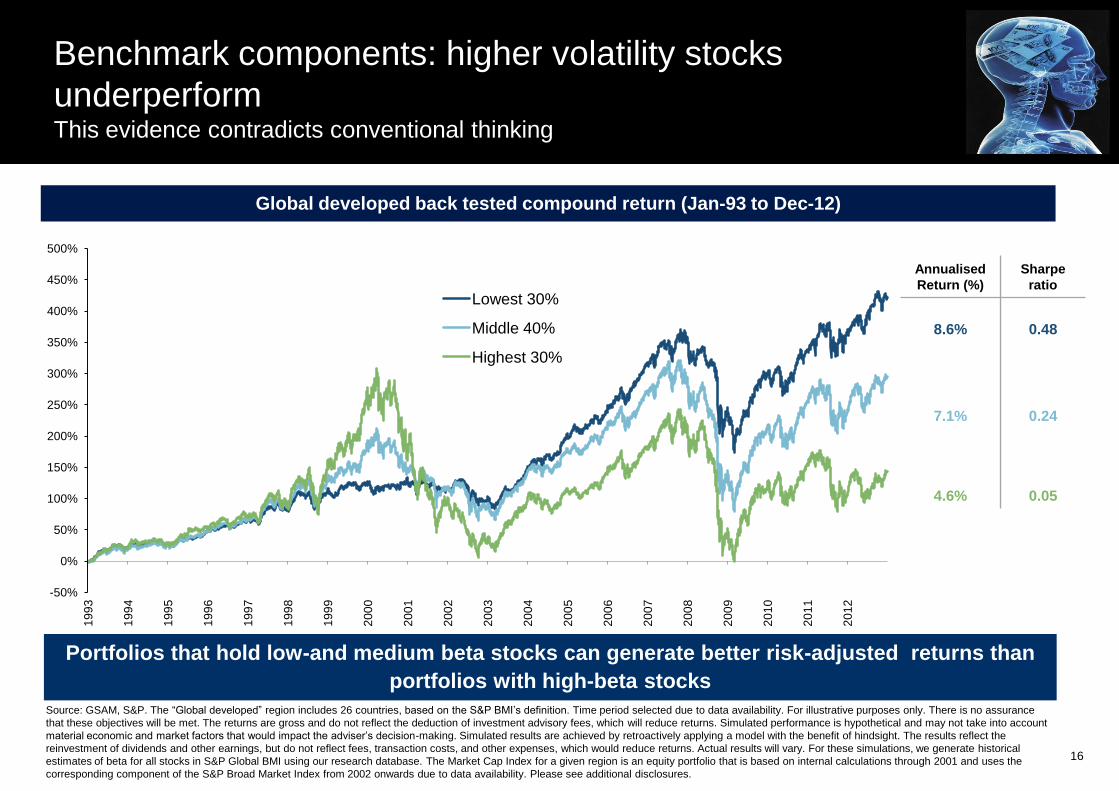

Benchmark components: higher volatility stocks

underperform This evidence contradicts conventional thinking

16

Global developed back tested compound return (Jan-93 to Dec-12)

Portfolios that hold low-and medium beta stocks can generate better risk-adjusted returns than

portfolios with high-beta stocks

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Lowest 30%

Middle 40%

Highest 30%

Source: GSAM, S&P. The “Global developed” region includes 26 countries, based on the S&P BMI’s definition. Time period selected due to data availability. For illustrative purposes only. There is no assurance

that these objectives will be met. The returns are gross and do not reflect the deduction of investment advisory fees, which will reduce returns. Simulated performance is hypothetical and may not take into account

material economic and market factors that would impact the adviser’s decision-making. Simulated results are achieved by retroactively applying a model with the benefit of hindsight. The results reflect the

reinvestment of dividends and other earnings, but do not reflect fees, transaction costs, and other expenses, which would reduce returns. Actual results will vary. For these simulations, we generate historical

estimates of beta for all stocks in S&P Global BMI using our research database. The Market Cap Index for a given region is an equity portfolio that is based on internal calculations through 2001 and uses the

corresponding component of the S&P Broad Market Index from 2002 onwards due to data availability. Please see additional disclosures.

Annualised

Return (%)

Sharpe

ratio

8.6%

0.48

7.1%

0.24

4.6%

0.05

The Wisdom of Crowds, Randomness & ‘Nudge’

17

Conclusion 1: there are four features of most good decision making bodies

Conclusion 2: human beings overestimate causality

Conclusion 3: people’s decision making can respond well to appropriate ‘nudges’

Source: Google Images. For illustrative purposes only.

Diversity of Opinion Ensure there are a diversity of backgrounds, roles, interests and personality types

Independence Due diligence based on independent facts and assign homework

Being part of a Wise Crowd Decision making

Decentralisation Specialist or local knowledge and encourage all members to speak up (incl. devil’s

advocates)

Aggregation Collective decisions: agenda, goals, voting systems etc.

These appear necessary for any effective team…

… including decision making groups and trustee boards

Source: James Surowiecki, The Wisdom of Crowds, 2004. 18

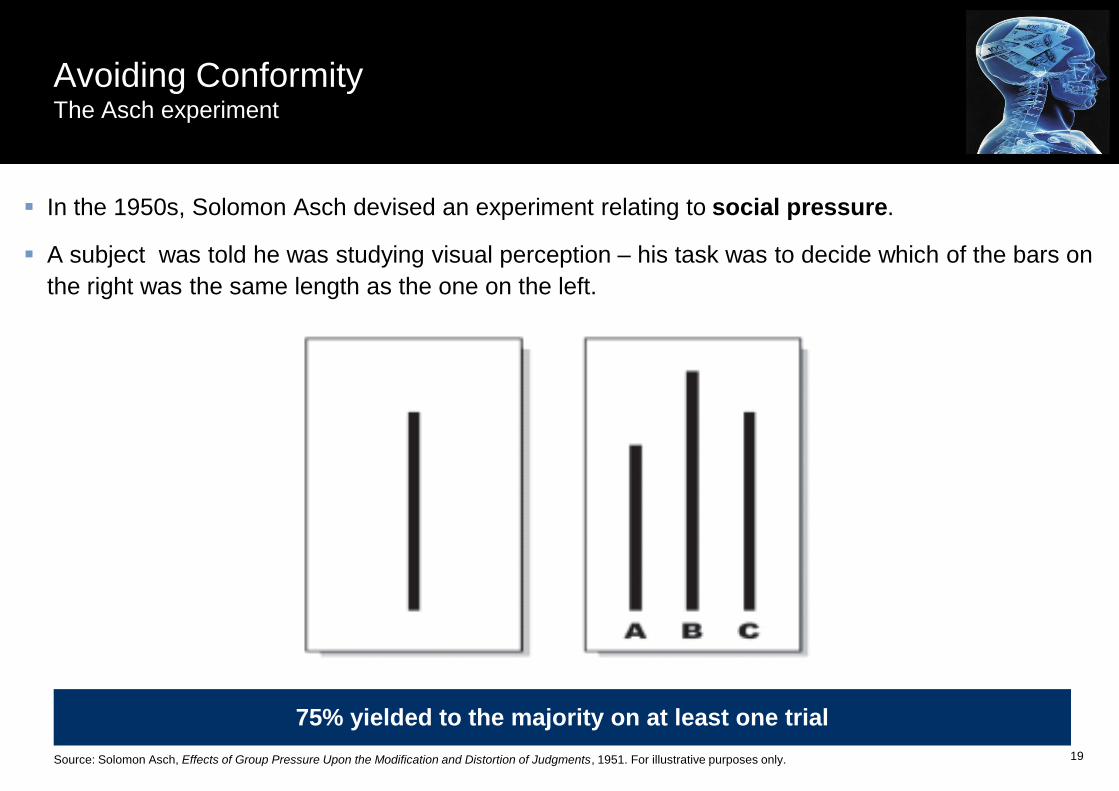

Avoiding Conformity The Asch experiment

In the 1950s, Solomon Asch devised an experiment relating to social pressure.

A subject was told he was studying visual perception – his task was to decide which of the bars on

the right was the same length as the one on the left.

Source: Solomon Asch, Effects of Group Pressure Upon the Modification and Distortion of Judgments, 1951. For illustrative purposes only. 19

75% yielded to the majority on at least one trial

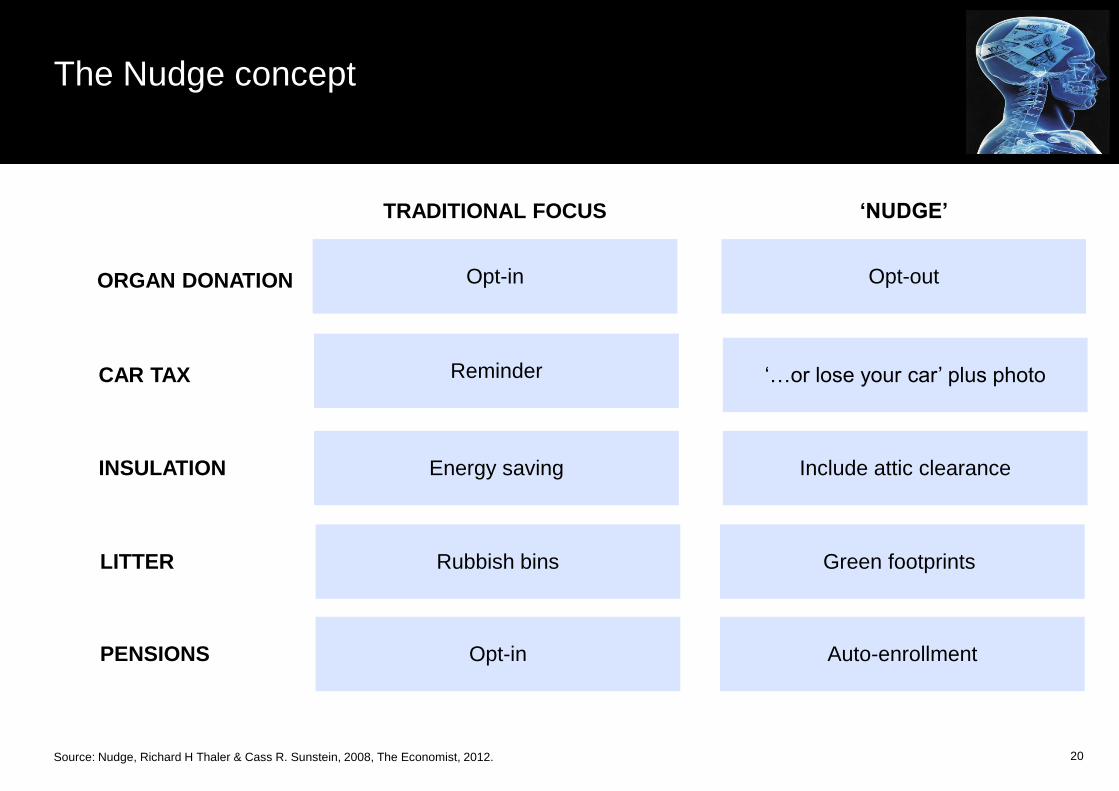

Opt-in Opt-out

Reminder ‘…or lose your car’ plus photo

Energy saving Include attic clearance

Rubbish bins Green footprints

Opt-in Auto-enrollment

The Nudge concept

20 Source: Nudge, Richard H Thaler & Cass R. Sunstein, 2008, The Economist, 2012.

TRADITIONAL FOCUS ‘NUDGE’

ORGAN DONATION

CAR TAX

INSULATION

LITTER

PENSIONS

Lessons from Behavioural Finance Conclusions

21

1. Traditional economic models assume that people are rational decision makers who analyse

data and act logically before they reach conscious decisions…

3. Behavioural Finance - the study of the psychology behind the real life thought

processes of individuals or groups – offers exciting insights for superior decision-making.

2. In real life, however, we are all subject to a variety of biases, often subconscious, that

affect our judgment. This can lead to ‘Groupthink’ in decision making bodies.

Being aware of our cognitive biases:

(i) reduces potential downside consequences and (ii) offers opportunities for upside in all areas of our lives…

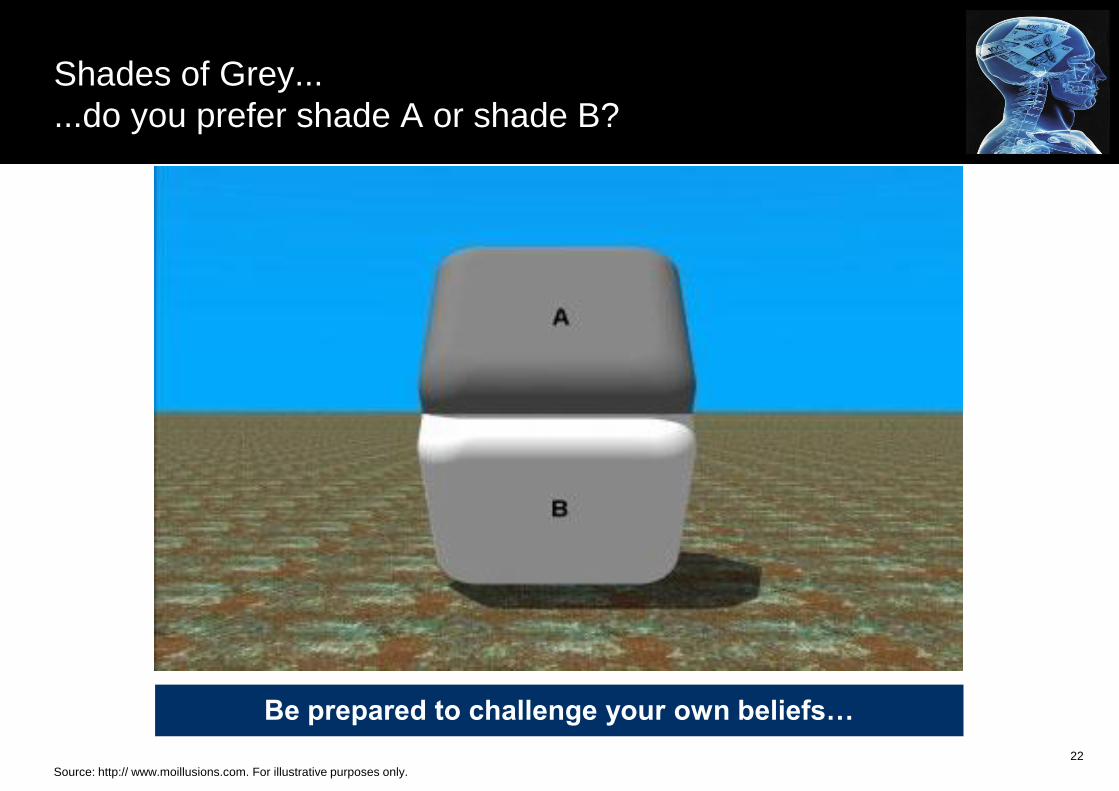

Shades of Grey...

...do you prefer shade A or shade B?

22

Source: http:// www.moillusions.com. For illustrative purposes only.

Be prepared to challenge your own beliefs…

Appendix

Biography

Paul Craven Head of EMEA Institutional Business,

Goldman Sachs Asset Management

Paul is head of EMEA Institutional Business. He joined Goldman Sachs Asset

Management in 2007 as a managing director. Prior to joining the firm, Paul worked

at PIMCO Europe Ltd for four years, where he was head of UK Business

Development. Previously, he spent seventeen years at Schroders as a portfolio

manager and latterly as head of UK Institutional Sales.

He is a Trustee of the Goldman Sachs Pension Plan and is a regular guest

speaker on the topic of behavioural finance at the Cass and London Business

Schools. Paul has an MA (Hons) in History from St. John’s College, Cambridge

University, is a Freeman of the City of London, and is a member of the CFA Institute

and the Magic Circle.

Additional notes

This material is provided at your request solely for your use. This material is provided for educational purposes only and should not be construed as investment advice or an offer

or solicitation to buy or sell securities.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are

current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

These examples are for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go

down as well as up. A loss of principal may occur.

Economic and market forecasts presented herein reflect our judgment as of the date of this presentation and are subject to change without notice. These forecasts do not take into

account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These

forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of

possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions

change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and

assumed without independent verification, the accuracy and completeness of all information available from public sources.

Backtested performance results do not represent the results of actual trading using client assets. They do not reflect the reinvestment of dividends, the deduction of any fees,

commissions or any other expenses a client would have to pay. If GSAM had managed your account during the period, it is highly improbable that your account would have been

managed in a similar fashion due to differences in economic and market conditions.

This material has been prepared by GSAM and is not a product of Goldman Sachs Global Investment Research. The views and opinions expressed may differ from those of

Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors

before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the

United Kingdom by the Financial Conduct Authority.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not

an employee, officer, director, or authorized agent of the recipient.

© 2013 Goldman Sachs. All rights reserved. 88884.OTHER.TMPL/1/2013 . 110185.OTHER.MED.OTU. 25