1/1/16

ACCT 652 Week 6ACCT652 Week 6 1

ACCT652 Week 6 11

ACCT 652 Accounting

Week 6–Receivables, notes, plant assets, natural resources and

intangible assets

Some slides © Times Mirror Higher Education Division, Inc. Used by permission© Michael D. Kinsman, Ph.D.

ACCT652 Week 6 222

Bad debts• The best of all worlds is when you grant

your customers credit and all of them pay exactly as and when they are supposed to.

• I can tell you from personal experience that doesn’t happen in the real world.

• Trick question: What are the entries Kinsman & Kinsman makes on our books when a client doesn’t pay us?

ACCT652 Week 6 333

Answer to trick question• None. We are a cash basis business, as we

discussed last time, and therefore nothing has been entered on our books for accounts receivable or sales from those receivables to start with. Therefore, we need make no entry.

• We do whimper when this happens to us. If the amount is large enough, we cry.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 2

ACCT652 Week 6 444

Bad Debts: Direct Write-Off Method

• This method is only appropriate in a limited number of cases where the company experiences little or no bad debt losses.

• No effort is made to estimate uncollectible accounts or bad debts expense.

• No adjusting entry is made at year-end.• Bad debts expense is recorded when specific

accounts are written off.

ACCT652 Week 6 555

Direct write-off–example

• Your company has few bad debts, and finally you get a call that John Smith has died with no assets. He owed you $50.

GENERAL JOURNAL Page

D ate D escriptionP ost. R ef. D ebit C redit

M M DD Bad debts expense 50.00 Accounts receivable (Smith) 50.00

Write off bad debt of Smith

ACCT652 Week 6 666

Bad Debts• The reporting of bad debts is normally

governed by the matching principle–bad debts expense should be recognized in the period in which the revenue was produced.

• Managers realize that some portion of credit sales will eventually result in bad debts.

• To match bad debts expense with revenue produced in an accounting period we use the allowance method

PAST DUE

1/1/16

ACCT 652 Week 6ACCT652 Week 6 3

ACCT652 Week 6 777

Allowance Method of Accounting for Bad Debts

• At the end of the accounting period, we estimate total bad debts expected to be realized from sales in the current period.

• Advantages of this method are:– Matches expenses with revenues– Reports accounts receivable at the estimated

cash to be collected.

ACCT652 Week 6 888

Estimating the Amount of Bad Debts Expense

• There are two approaches to estimating the amount of bad debts expense . . .➊ Focus on the income statement relationship

between bad debts expense and sales.➋ Focus on the balance sheet relationship between

accounts receivable and the allowance for doubtful accounts.

ACCT652 Week 6 999

Income Statement Focus

• This approach is based on the notion that a certain percentage of a company’s credit sales will become uncollectible.

• We must determine the percentage relationship between credit sales and bad debts.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 4

ACCT652 Week 6 101010

Income Statement Focus• Based on history, we determine the percentage

of credit sales that result in bad debts.

• Bad debts expense is computed as follows: Current Year Credit Sales

x Bad Debt % Estimated Bad Debt Expense

ACCT652 Week 6 111111

As of 12/31/X1 Melton, Inc. had total sales of $1,000,000 of which $250,000 were cash sales.

Historically, the bad debt percentage based on credit sales has been 0.5%.

Prepare the adjusting journal entry required for Melton, Inc. to record bad debts expense for 20X1.

Income Statement Focus Example

ACCT652 Week 6 121212

Income Statement Approach

GENERAL JOURNAL Page 7

D ate D escrip tionPost. R ef. D eb it C red it

D ec . 31 Bad D eb ts Expense 3,75 0 A llowance fo r D oubtfu l A ccounts 3 ,75 0

S ales revenue 1,000,000$Cash sales (250,000) Credit sales 750,000 Historical bad debts percent 0.50%E stim ated bad debts expense 3,750$

1/1/16

ACCT 652 Week 6ACCT652 Week 6 5

ACCT652 Week 6 131313

Balance Sheet Focus• The assumption is that some portion of the

end-of-period accounts receivable will prove to be uncollectible.

• The goal of the adjusting entry is to state the Allowance for Doubtful Accounts at the estimated uncollectible amount.

ACCT652 Week 6 141414

Aging Accounts Receivable• This balance sheet method produces a more

refined estimate of uncollectible amounts.• It is useful after a company has considerable

experience estimating bad debts.• The assumption we make is that the more past

due an account is, the less likely we are to collect the account.

ACCT652 Week 6 151515

Balance sheet method of Allowance for Doubtful Accounts

On December 31, 20X1, the balance in Allowance for Doubtful Accounts of Eastco is $500 (credit) before the adjustment to recognize bad debts expense. What is the company’s addition to Allowance for Doubtful Accounts?

First, we do an aged account receivables schedule for Eastco.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 6

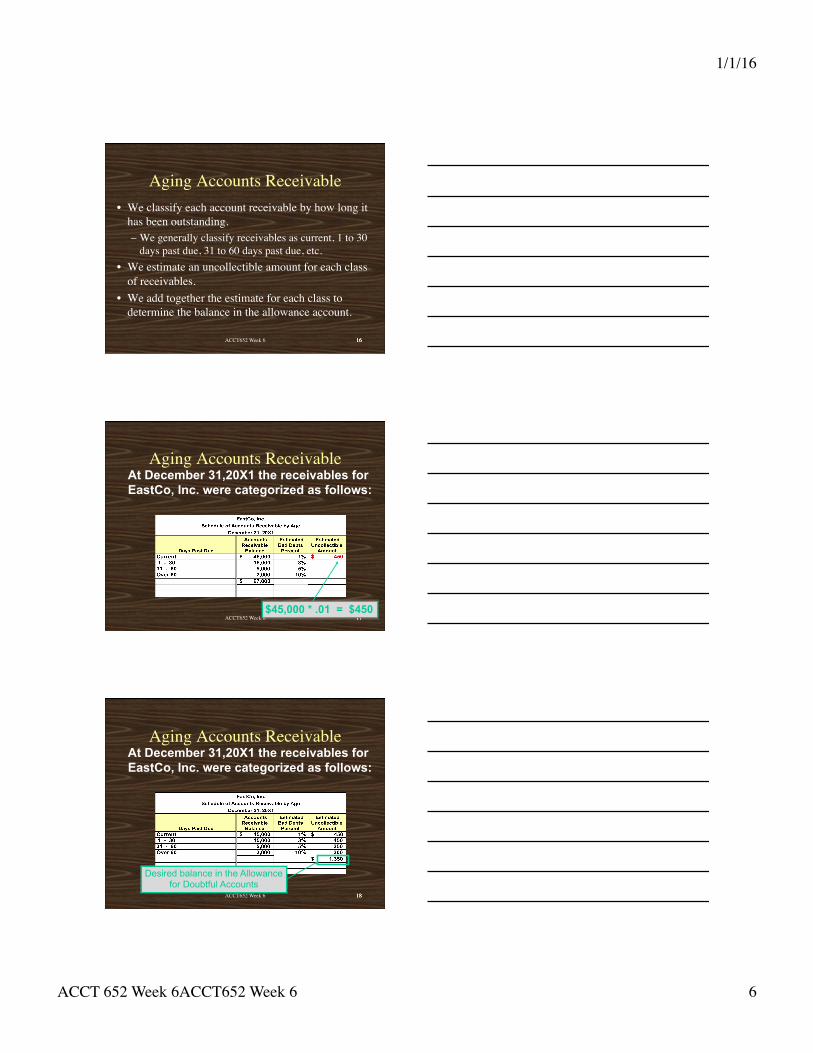

ACCT652 Week 6 161616

Aging Accounts Receivable• We classify each account receivable by how long it

has been outstanding.– We generally classify receivables as current, 1 to 30

days past due, 31 to 60 days past due, etc.• We estimate an uncollectible amount for each class

of receivables.• We add together the estimate for each class to

determine the balance in the allowance account.

ACCT652 Week 6 171717

Aging Accounts ReceivableAt December 31,20X1 the receivables for EastCo, Inc. were categorized as follows:

$45,000 * .01 = $450

ACCT652 Week 6 181818

Aging Accounts ReceivableAt December 31,20X1 the receivables for EastCo, Inc. were categorized as follows:

Desired balance in the Allowance for Doubtful Accounts

1/1/16

ACCT 652 Week 6ACCT652 Week 6 7

ACCT652 Week 6 191919

Allowance for Doubtful Accounts–Balance Sheet method

• What is the journal entry required to enter the bad debts expense and the allowance for doubtful accounts?

ACCT652 Week 6 202020

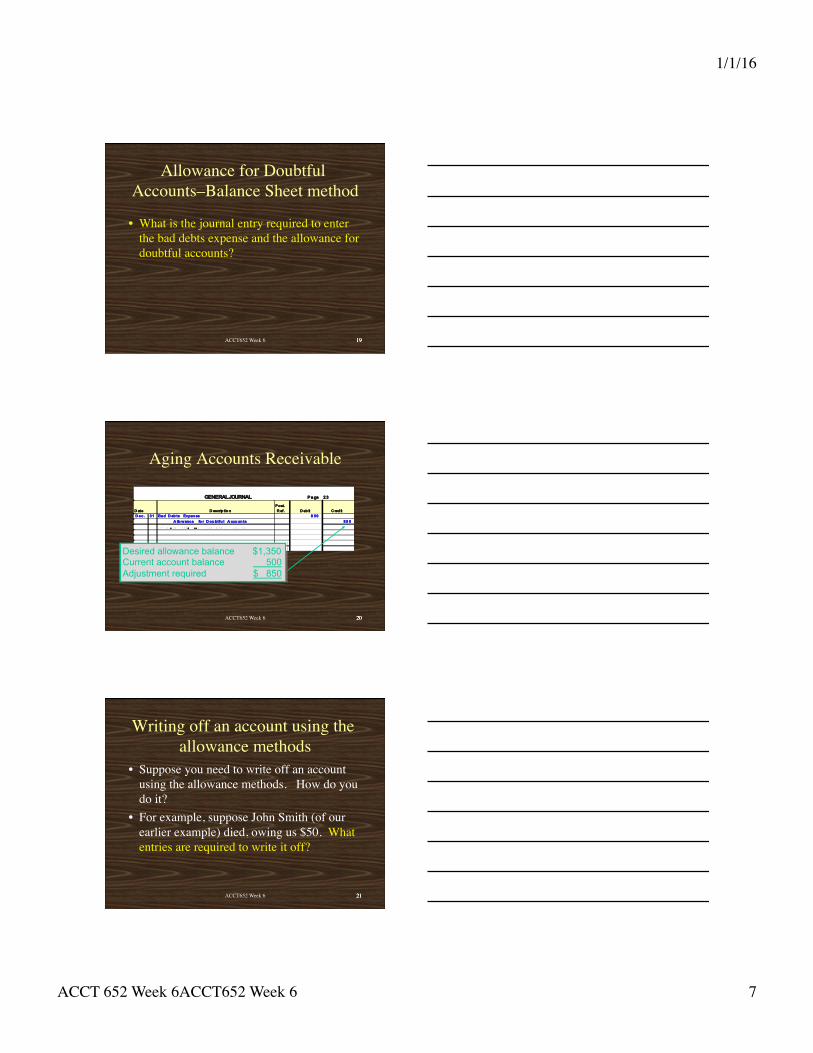

Aging Accounts Receivable

GENERAL JOURNAL Page 23

D ate D escrip tionPost. R ef. D eb it C red it

D ec . 31 Bad D eb ts Expense 8 50 A llowance fo r D oubtfu l A ccounts 85 0

Desired allowance balance $1,350 Current account balance 500 Adjustment required $ 850

ACCT652 Week 6 212121

Writing off an account using the allowance methods

• Suppose you need to write off an account using the allowance methods. How do you do it?

• For example, suppose John Smith (of our earlier example) died, owing us $50. What entries are required to write it off?

1/1/16

ACCT 652 Week 6ACCT652 Week 6 8

ACCT652 Week 6 222222

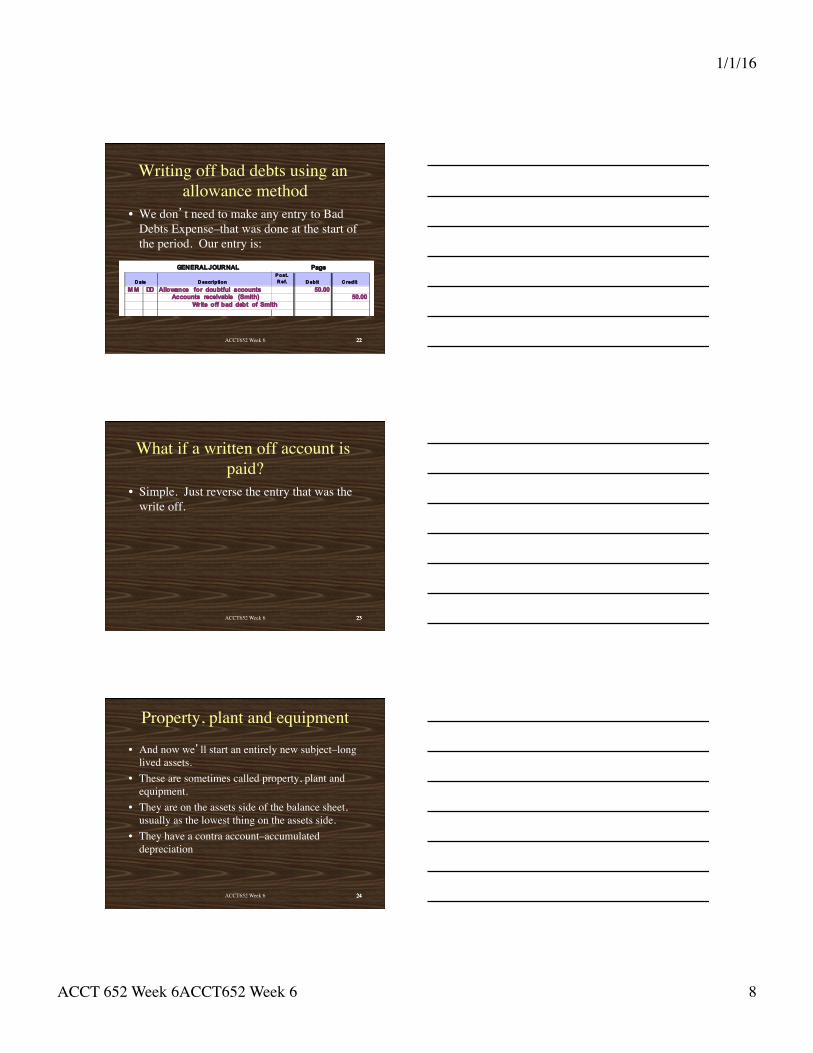

Writing off bad debts using an allowance method

• We don’t need to make any entry to Bad Debts Expense–that was done at the start of the period. Our entry is:

GENERAL JOURNAL Page

D ate D escriptionP ost. R ef. D ebit C redit

M M DD Allowance for doubtful accounts 50.00 Accounts receivable (Smith) 50.00

Write off bad debt of Smith

ACCT652 Week 6 232323

What if a written off account is paid?

• Simple. Just reverse the entry that was the write off.

ACCT652 Week 6 242424

Property, plant and equipment

• And now we’ll start an entirely new subject–long lived assets.

• These are sometimes called property, plant and equipment.

• They are on the assets side of the balance sheet, usually as the lowest thing on the assets side.

• They have a contra account–accumulated depreciation

1/1/16

ACCT 652 Week 6ACCT652 Week 6 9

ACCT652 Week 6 252525

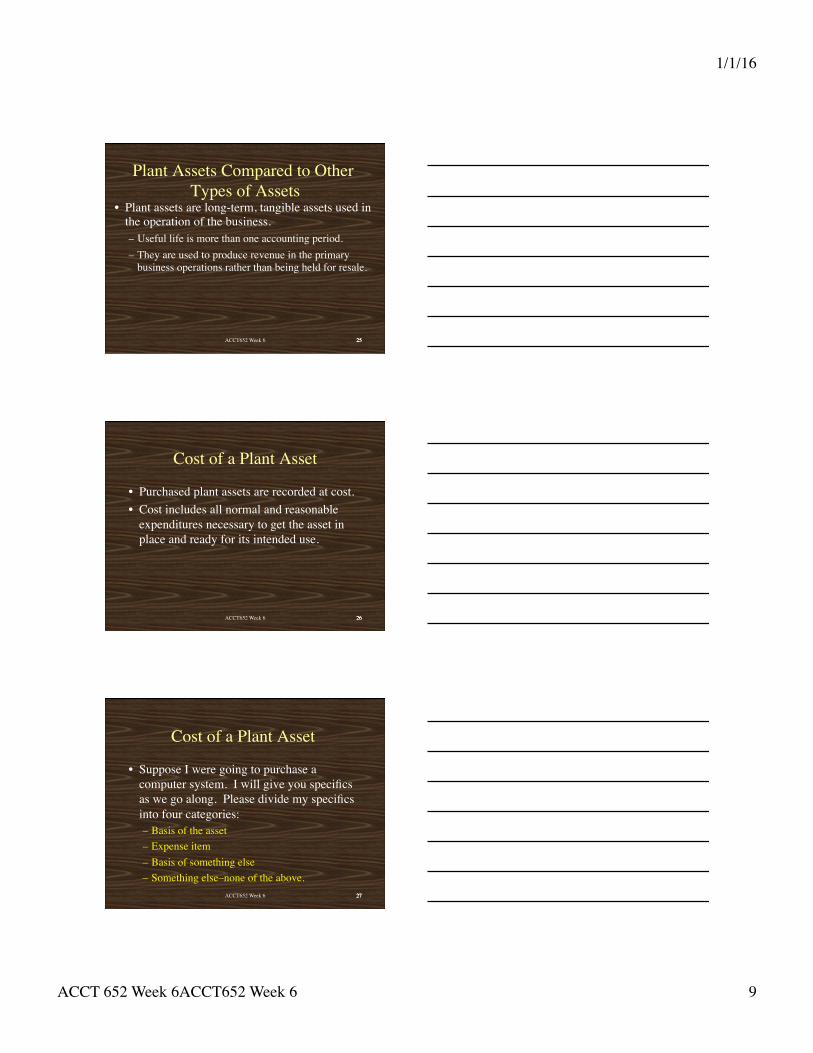

Plant Assets Compared to Other Types of Assets

• Plant assets are long-term, tangible assets used in the operation of the business.– Useful life is more than one accounting period.– They are used to produce revenue in the primary

business operations rather than being held for resale.

ACCT652 Week 6 262626

Cost of a Plant Asset

• Purchased plant assets are recorded at cost.• Cost includes all normal and reasonable

expenditures necessary to get the asset in place and ready for its intended use.

ACCT652 Week 6 272727

Cost of a Plant Asset

• Suppose I were going to purchase a computer system. I will give you specifics as we go along. Please divide my specifics into four categories:– Basis of the asset– Expense item– Basis of something else– Something else–none of the above.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 10

ACCT652 Week 6 282828

Cost of a Plant Asset �Self-Constructed Assets

Cost includes all materials and labor cost directly traceable to the construction as well as a reasonable amount of indirect costs such as utilities and supervision.

ACCT652 Week 6 292929

Cost of a Plant Asset �Land & Buildings

When land and building are purchased together, the land cost and the building cost are placed

in separate ledger accounts. ��

The total cost of the purchase is separated on the basis of relative market values.

ACCT652 Week 6 303030

Nature of Depreciation• The useful life of plant assets, other than land,

is limited, so the usefulness of the asset expires as it is used.

• The expiration of usefulness of the asset is generally described as depreciation.

• Depreciation is the process of allocating a plant asset’s cost to income statements for the years in which it is used.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 11

ACCT652 Week 6 313131

• Depreciation results in matching the cost of acquiring plant assets with the revenues generated by their use.

• Depreciation is recorded with the following adjusting entry:

Nature of Depreciation

ACCT652 Week 6 323232

• Depreciation results in matching the cost of acquiring plant assets with the revenues generated by their use.

• Depreciation is recorded with the following adjusting entry:

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

Depreciation Expense XXXXX

Accumulated Depreciation XXXXX

Nature of Depreciation

ACCT652 Week 6 333333

• Depreciation Expense– Balance in Depreciation

Expense indicates how much depreciation has been recorded in the current year.

– Temporary account, reported on the income statement.

• Accumulated Depreciation– Permanent account, reported

on the balance sheet as a deduction from plant assets.

– Balance in Accumulated Depreciation is a cumulative total of all depreciation recorded on an asset.

Nature of Depreciation

1/1/16

ACCT 652 Week 6ACCT652 Week 6 12

ACCT652 Week 6 343434

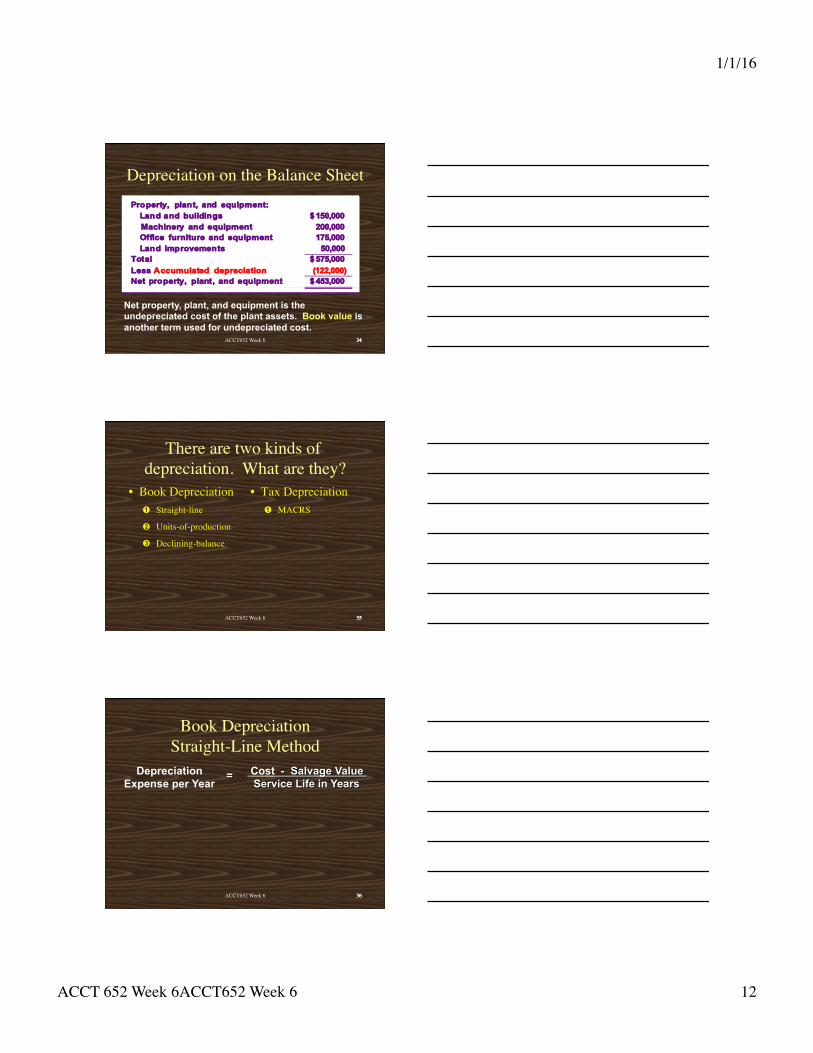

Depreciation on the Balance SheetProperty, plant, and equipment: Land and buildings 150,000$ Machinery and equipment 200,000 Office furniture and equipment 175,000 Land improvements 50,000 Total 575,000$Less Accumulated depreciation (122,000) Net property, plant, and equipment 453,000$

Net property, plant, and equipment is the undepreciated cost of the plant assets. Book value is another term used for undepreciated cost.

ACCT652 Week 6 353535

There are two kinds of depreciation. What are they?

• Book Depreciation➊ Straight-line

➋ Units-of-production

➌ Declining-balance

• Tax Depreciation➊ MACRS

ACCT652 Week 6 363636

Book Depreciation�Straight-Line Method

Depreciation Expense per Year

Cost - Salvage Value Service Life in Years

=

1/1/16

ACCT 652 Week 6ACCT652 Week 6 13

ACCT652 Week 6 373737

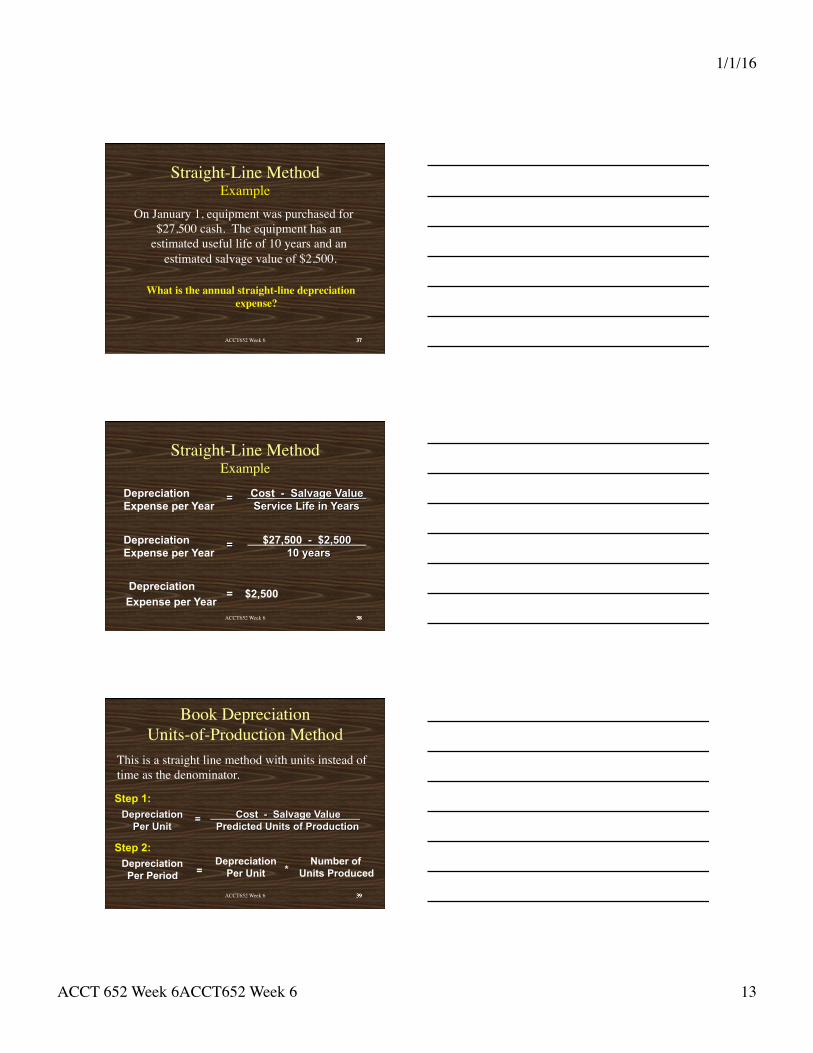

Straight-Line Method�Example

On January 1, equipment was purchased for $27,500 cash. The equipment has an

estimated useful life of 10 years and an estimated salvage value of $2,500.�

What is the annual straight-line depreciation expense?

ACCT652 Week 6 383838

Straight-Line Method�Example

Depreciation Expense per Year

= $2,500

Depreciation Expense per Year

$27,500 - $2,500 10 years

=

Depreciation Expense per Year

Cost - Salvage Value Service Life in Years

=

ACCT652 Week 6 393939

Book Depreciation�Units-of-Production Method

Depreciation Per Unit

= Cost - Salvage Value Predicted Units of Production

Step 1:

Step 2: Depreciation Per Period =

Depreciation Number of Per Unit Units Produced *

This is a straight line method with units instead of time as the denominator.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 14

ACCT652 Week 6 404040

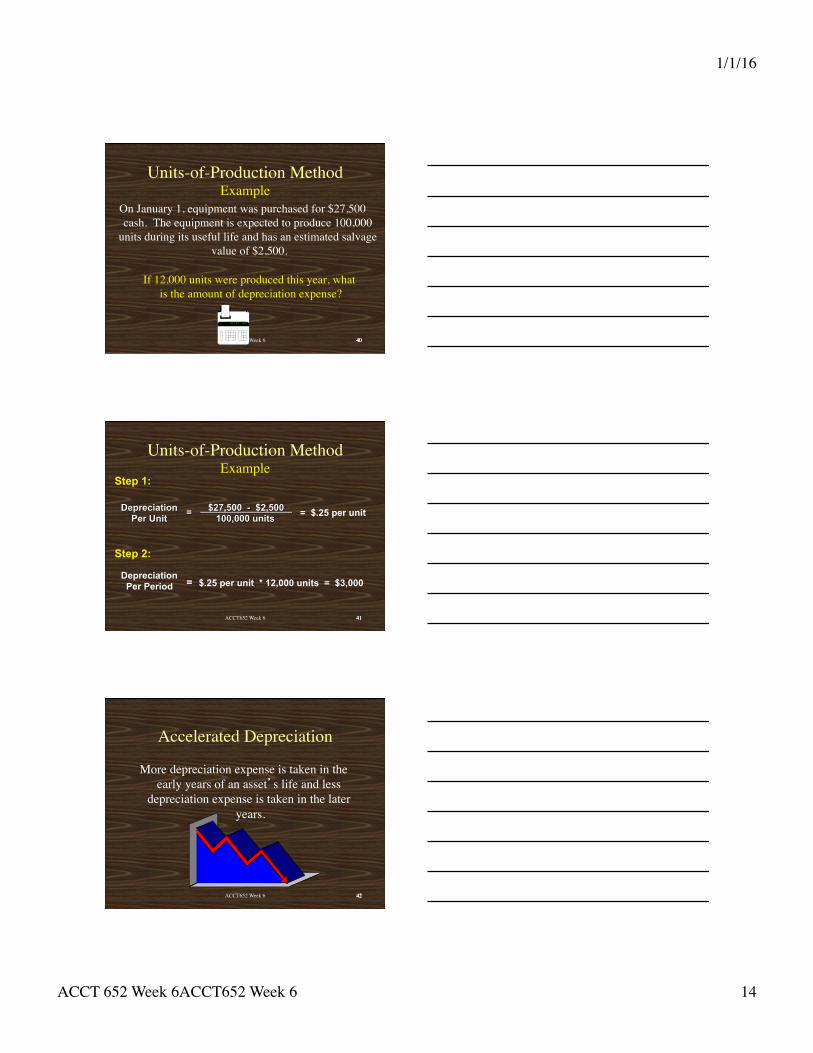

Units-of-Production Method�Example

On January 1, equipment was purchased for $27,500 cash. The equipment is expected to produce 100,000

units during its useful life and has an estimated salvage value of $2,500.�

�If 12,000 units were produced this year, what�

is the amount of depreciation expense?

ACCT652 Week 6 414141

Units-of-Production Method�Example

Depreciation Per Unit = $27,500 - $2,500

100,000 units

Step 1:

= $.25 per unit

Step 2:

Depreciation Per Period = $.25 per unit * 12,000 units = $3,000

ACCT652 Week 6 424242

Accelerated Depreciation

More depreciation expense is taken in the early years of an asset’s life and less

depreciation expense is taken in the later years.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 15

ACCT652 Week 6 434343

Declining Balance methods

• The final financial statement method of depreciation is declining balance. It is actually a family of methods, usually containing three members–125 percent, 150 percent, and 200 percent (also known as double)–declining balance depreciation.

ACCT652 Week 6 444444

Declining-Balance Method

To calculate declining balance depreciation, you first have to calculate the straight line rate:

For example, an asset with a 10-year useful life would have a straight-line rate calculated as follows:

= Straight-Line Rate Useful Life in Years 100%

10 Years 100%

= 10%

ACCT652 Week 6 454545

Declining balance depreciation

• You then need to calculate the annual depreciation:

where X is the chosen rate: 200%, 150%, or 125%.

• Setting up a table helps. One such is shown on the next slide.

Book Value * (X * Straight-Line Rate)

1/1/16

ACCT 652 Week 6ACCT652 Week 6 16

ACCT652 Week 6 464646

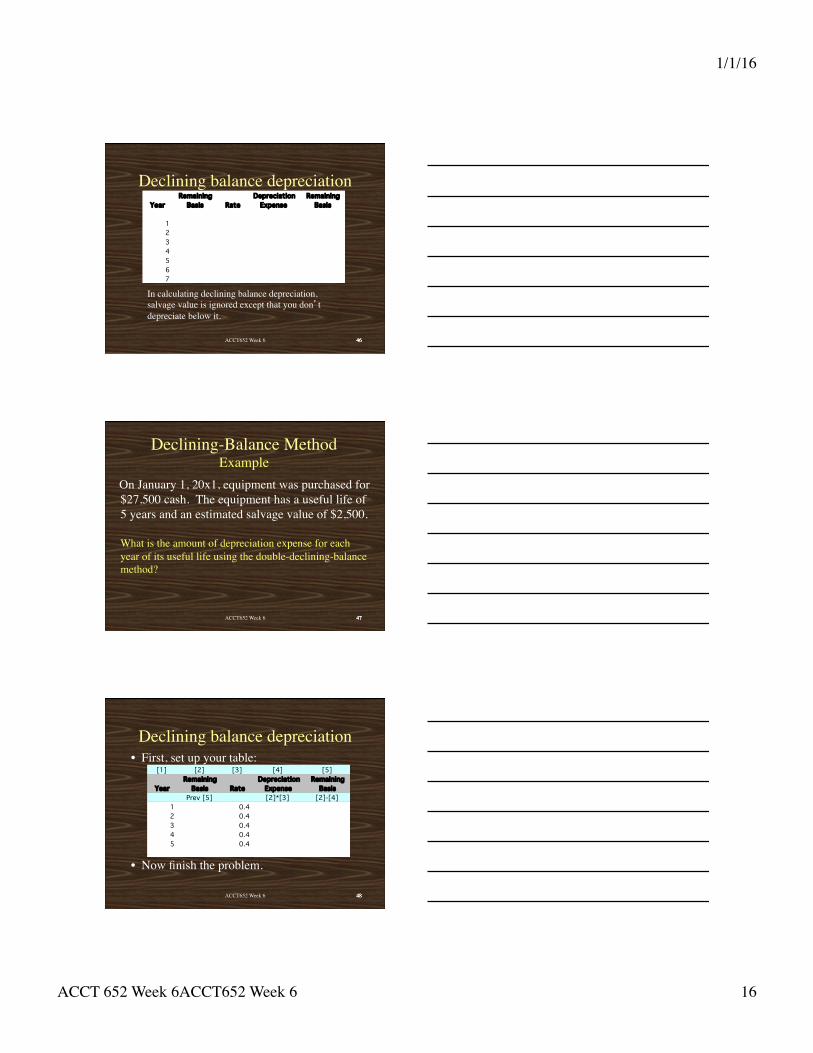

Declining balance depreciation Remaining Depreciation Remaining

Year Basis Rate Expense Basis

1234567

In calculating declining balance depreciation, salvage value is ignored except that you don’t depreciate below it.

ACCT652 Week 6 474747

Declining-Balance Method �Example

On January 1, 20x1, equipment was purchased for $27,500 cash. The equipment has a useful life of 5 years and an estimated salvage value of $2,500.��What is the amount of depreciation expense for each year of its useful life using the double-declining-balance method?

ACCT652 Week 6 484848

Declining balance depreciation• First, set up your table:

• Now finish the problem.

[1] [2] [3] [4] [5] Remaining Depreciation Remaining

Year Basis Rate Expense BasisPrev [5] [2]*[3] [2]-[4]

1 0.42 0.43 0.44 0.45 0.4

1/1/16

ACCT 652 Week 6ACCT652 Week 6 17

ACCT652 Week 6 494949

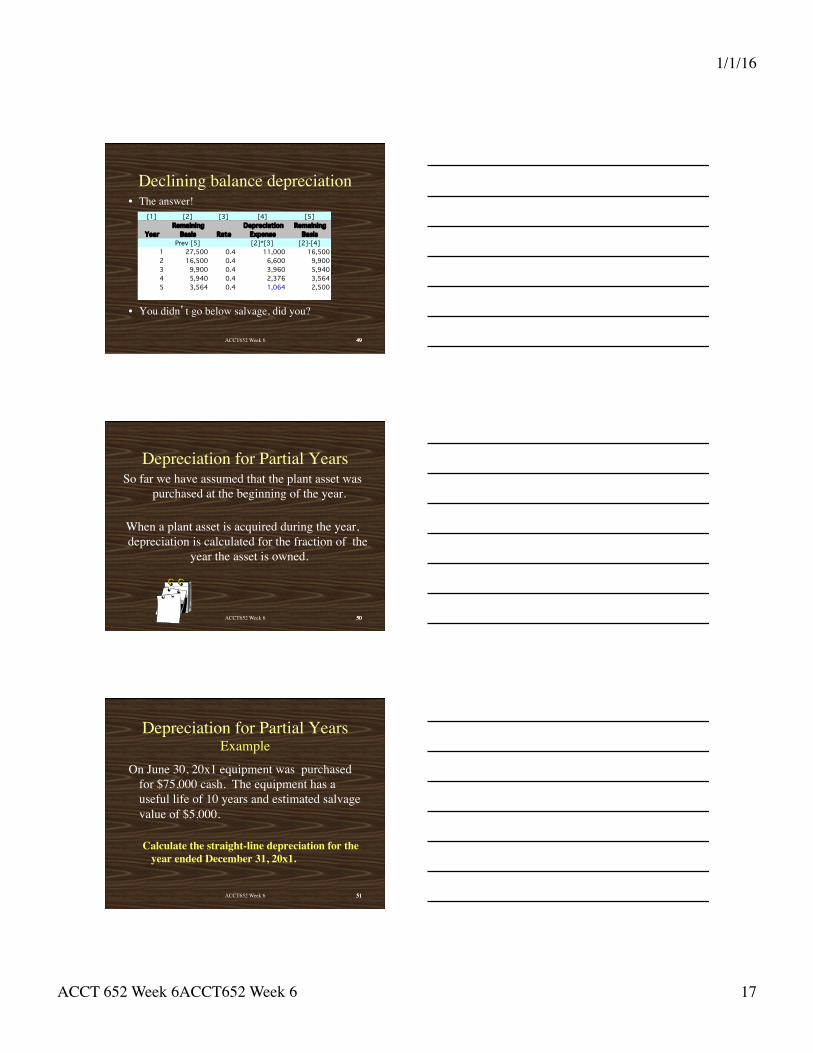

Declining balance depreciation• The answer!

• You didn’t go below salvage, did you?

[1] [2] [3] [4] [5] Remaining Depreciation Remaining

Year Basis Rate Expense BasisPrev [5] [2]*[3] [2]-[4]

1 27,500 0.4 11,000 16,5002 16,500 0.4 6,600 9,9003 9,900 0.4 3,960 5,9404 5,940 0.4 2,376 3,5645 3,564 0.4 1,064 2,500

ACCT652 Week 6 505050

Depreciation for Partial YearsSo far we have assumed that the plant asset was

purchased at the beginning of the year.�

When a plant asset is acquired during the year, depreciation is calculated for the fraction of the

year the asset is owned.

ACCT652 Week 6 515151

On June 30, 20x1 equipment was purchased for $75,000 cash. The equipment has a useful life of 10 years and estimated salvage value of $5,000.�

Calculate the straight-line depreciation for the year ended December 31, 20x1.

Depreciation for Partial Years �Example

1/1/16

ACCT 652 Week 6ACCT652 Week 6 18

ACCT652 Week 6 525252

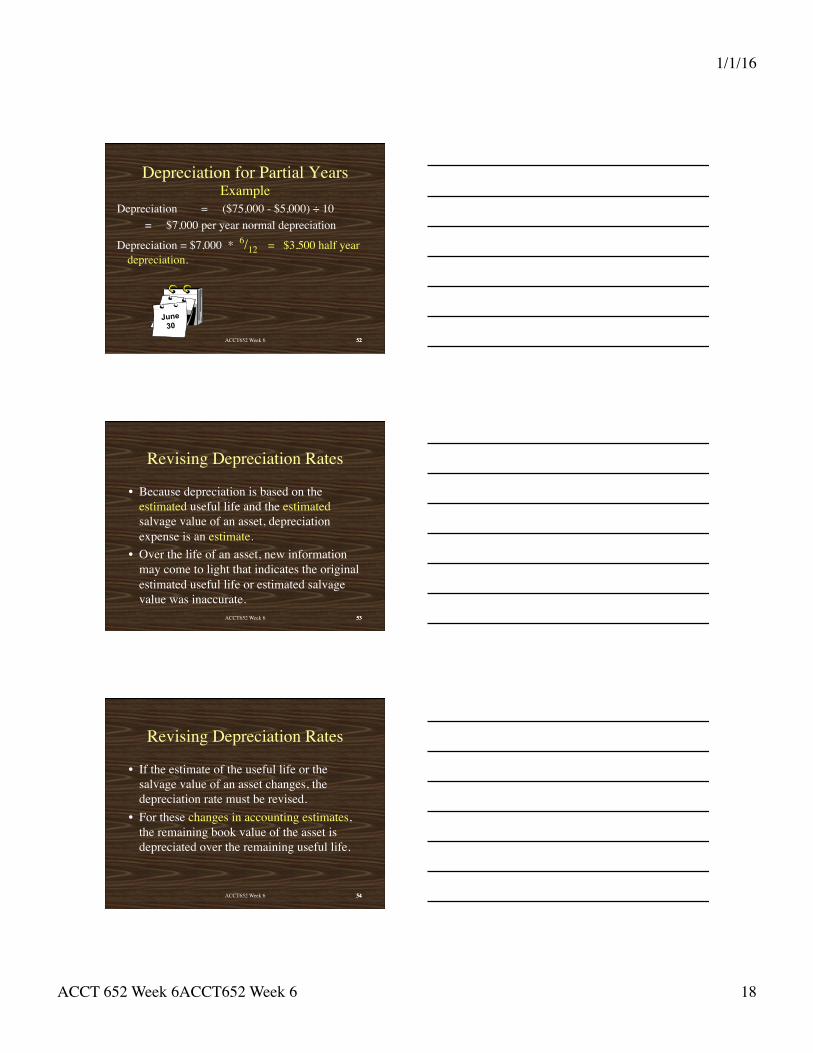

Depreciation = ($75,000 - $5,000) ÷ 10= $7,000 per year normal depreciation

Depreciation = $7,000 * 6/12 = $3,500 half year depreciation.

June 30

Depreciation for Partial Years �Example

ACCT652 Week 6 535353

Revising Depreciation Rates

• Because depreciation is based on the estimated useful life and the estimated salvage value of an asset, depreciation expense is an estimate.

• Over the life of an asset, new information may come to light that indicates the original estimated useful life or estimated salvage value was inaccurate.

ACCT652 Week 6 545454

Revising Depreciation Rates

• If the estimate of the useful life or the salvage value of an asset changes, the depreciation rate must be revised.

• For these changes in accounting estimates, the remaining book value of the asset is depreciated over the remaining useful life.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 19

ACCT652 Week 6 555555

Revising Depreciation Rates

• The easiest way to think about the problem of revising depreciation method, life, or salvage value is to think of “selling” the asset to yourself. You then depreciate the “newly bought” asset over its remaining life with its remaining basis under the appropriate method.

ACCT652 Week 6 565656

Revising Depreciation Rates Example

On January 1, 20x1, equipment was purchased that cost $30,000, has a useful life of 10 years and no salvage value. During 20x4, the useful life was revised to 8 years total (5 years remaining), and a $1,000 salvage value.

�Calculate depreciation expense for the year ended December 31, 20x4 using the straight-line method.

ACCT652 Week 6 575757

Revising Depreciation Rates Example

Asset cost 30,000$ Accumu lated depreciation , 12/31/X3 ($3,000 per year * 3 years) (9,000) New salvage value (1,000)

Remain ing depreciable value 20,000 Divide by remaining life ÷ 5Revised annual depreciation 4,000$

1/1/16

ACCT 652 Week 6ACCT652 Week 6 20

ACCT652 Week 6 585858

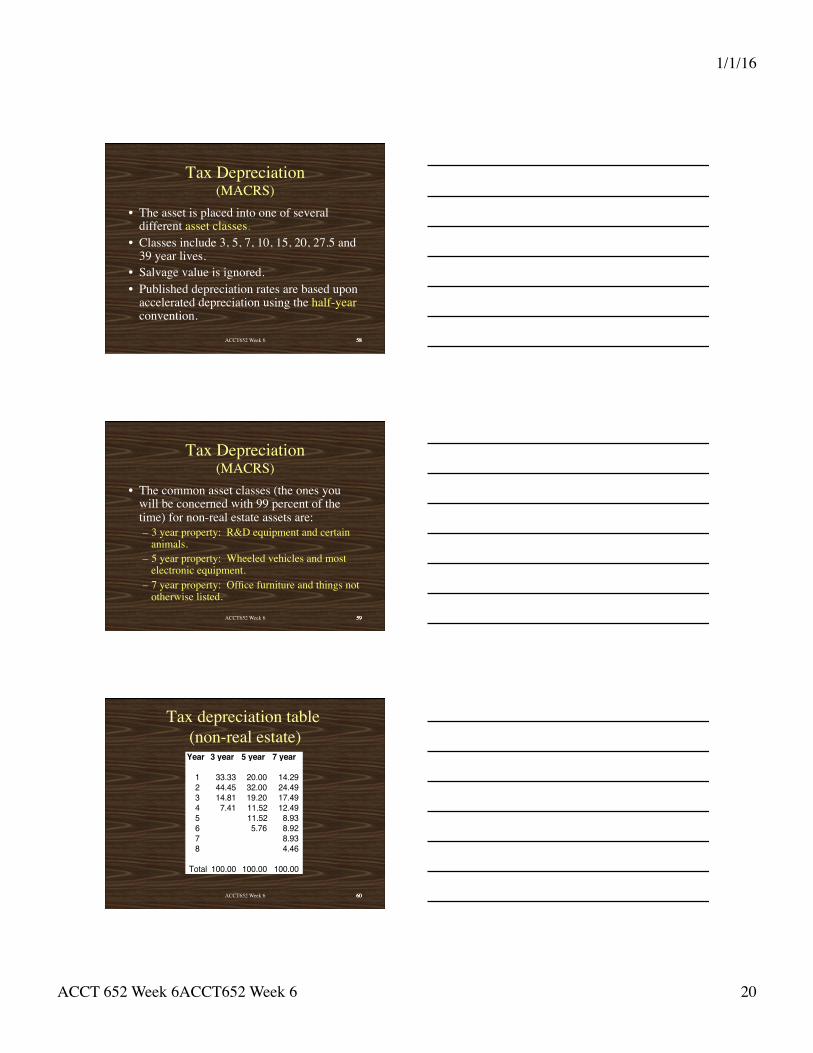

Tax Depreciation�(MACRS)

• The asset is placed into one of several different asset classes.

• Classes include 3, 5, 7, 10, 15, 20, 27.5 and 39 year lives.

• Salvage value is ignored.• Published depreciation rates are based upon

accelerated depreciation using the half-year convention.

ACCT652 Week 6 595959

Tax Depreciation�(MACRS)

• The common asset classes (the ones you will be concerned with 99 percent of the time) for non-real estate assets are:– 3 year property: R&D equipment and certain

animals.– 5 year property: Wheeled vehicles and most

electronic equipment.– 7 year property: Office furniture and things not

otherwise listed.

ACCT652 Week 6 606060

Tax depreciation table �(non-real estate)

Year 3 year 5 year 7 year

1 33.33 20.00 14.29 2 44.45 32.00 24.49 3 14.81 19.20 17.49 4 7.41 11.52 12.49 5 11.52 8.93 6 5.76 8.92 7 8.93 8 4.46

Total 100.00 100.00 100.00

1/1/16

ACCT 652 Week 6ACCT652 Week 6 21

ACCT652 Week 6 616161

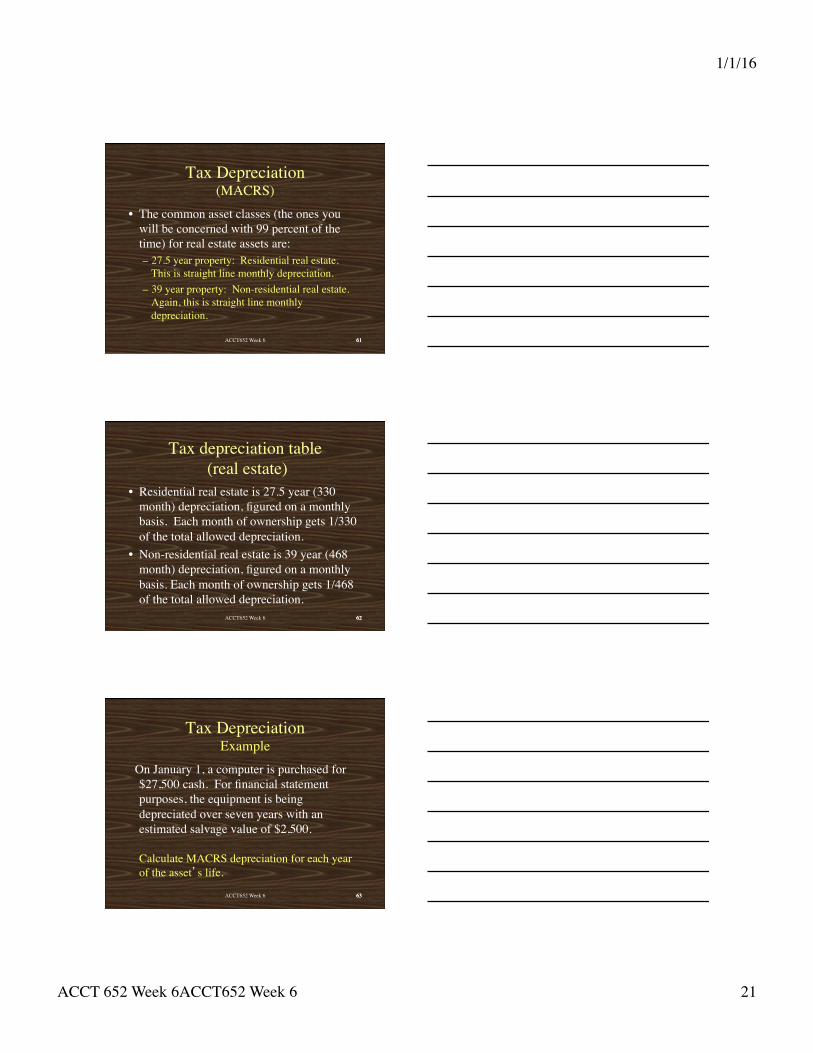

Tax Depreciation�(MACRS)

• The common asset classes (the ones you will be concerned with 99 percent of the time) for real estate assets are:– 27.5 year property: Residential real estate.

This is straight line monthly depreciation.– 39 year property: Non-residential real estate.

Again, this is straight line monthly depreciation.

ACCT652 Week 6 626262

Tax depreciation table� (real estate)

• Residential real estate is 27.5 year (330 month) depreciation, figured on a monthly basis. Each month of ownership gets 1/330 of the total allowed depreciation.

• Non-residential real estate is 39 year (468 month) depreciation, figured on a monthly basis. Each month of ownership gets 1/468 of the total allowed depreciation.

ACCT652 Week 6 636363

Tax Depreciation�Example

On January 1, a computer is purchased for $27,500 cash. For financial statement purposes, the equipment is being depreciated over seven years with an estimated salvage value of $2,500.��Calculate MACRS depreciation for each year of the asset’s life.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 22

ACCT652 Week 6 646464

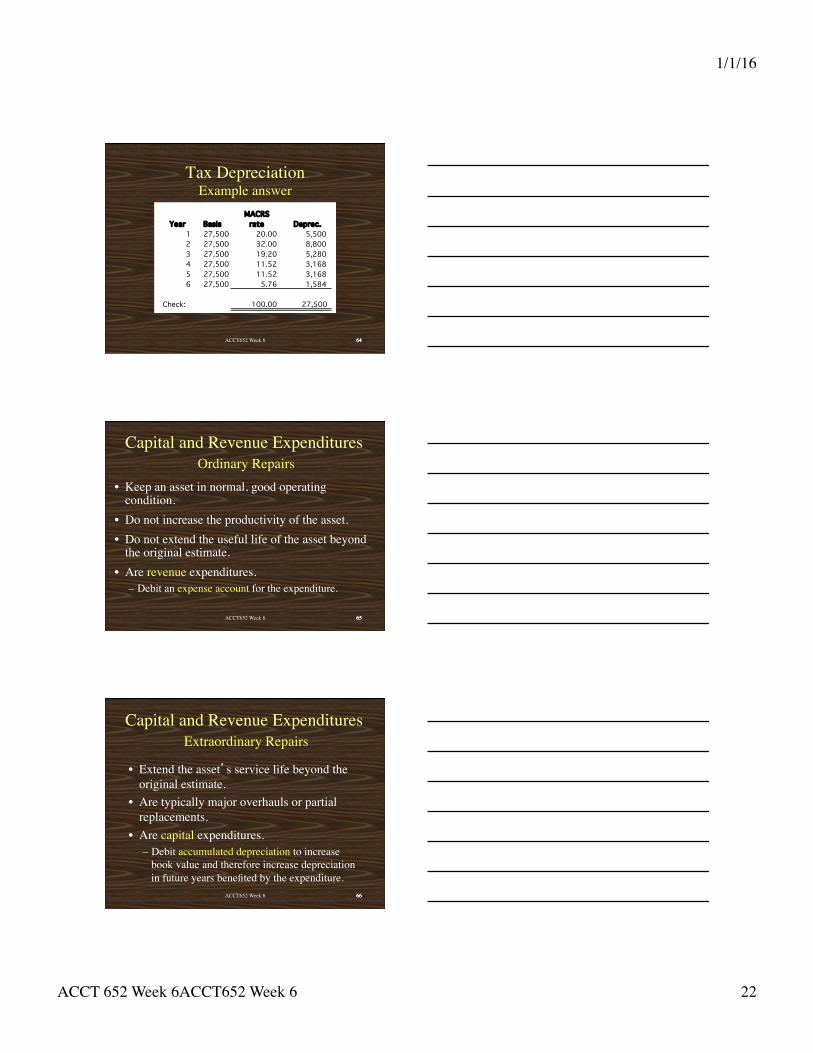

Tax Depreciation�Example answer

MACRSYear Basis rate Deprec.

1 27,500 20.00 5,500 2 27,500 32.00 8,800 3 27,500 19.20 5,280 4 27,500 11.52 3,168 5 27,500 11.52 3,168 6 27,500 5.76 1,584

Check: 100.00 27,500

ACCT652 Week 6 656565

Capital and Revenue Expenditures � Ordinary Repairs

• Keep an asset in normal, good operating condition.

• Do not increase the productivity of the asset.• Do not extend the useful life of the asset beyond

the original estimate.• Are revenue expenditures.

– Debit an expense account for the expenditure.

ACCT652 Week 6 666666

• Extend the asset’s service life beyond the original estimate.

• Are typically major overhauls or partial replacements.

• Are capital expenditures.– Debit accumulated depreciation to increase

book value and therefore increase depreciation in future years benefited by the expenditure.

Capital and Revenue Expenditures � Extraordinary Repairs

1/1/16

ACCT 652 Week 6ACCT652 Week 6 23

ACCT652 Week 6 676767

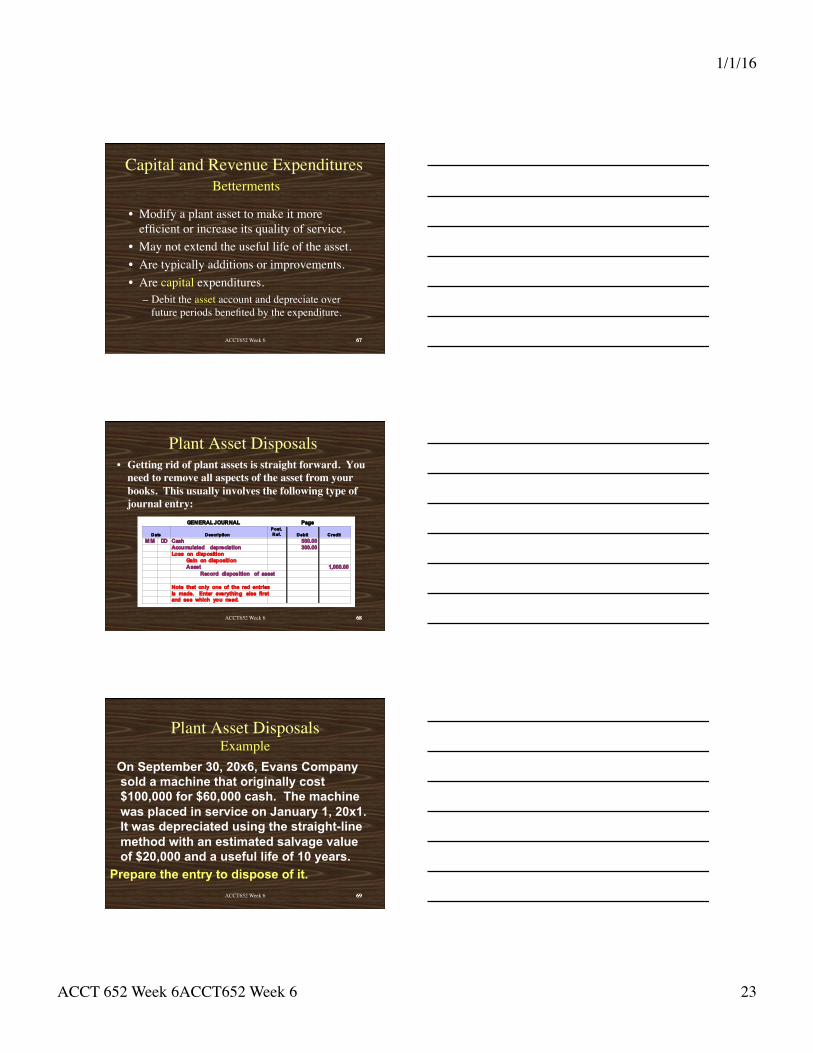

• Modify a plant asset to make it more efficient or increase its quality of service.

• May not extend the useful life of the asset.• Are typically additions or improvements.• Are capital expenditures.

– Debit the asset account and depreciate over future periods benefited by the expenditure.

Capital and Revenue Expenditures � Betterments

ACCT652 Week 6 686868

Plant Asset Disposals • Getting rid of plant assets is straight forward. You

need to remove all aspects of the asset from your books. This usually involves the following type of journal entry:

GENERAL JOURNAL Page

Date DescriptionPost. Ref. Debit Credit

M M DD Cash 500.00Accumulated depreciation 300.00Loss on disposition Gain on disposition Asset 1,000.00

Record disposition of asset

Note that only one of the red entriesis made. Enter everything else firstand see which you need.

ACCT652 Week 6 696969

Plant Asset Disposals �Example

On September 30, 20x6, Evans Company sold a machine that originally cost $100,000 for $60,000 cash. The machine was placed in service on January 1, 20x1. It was depreciated using the straight-line method with an estimated salvage value of $20,000 and a useful life of 10 years.

Prepare the entry to dispose of it.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 24

ACCT652 Week 6 707070

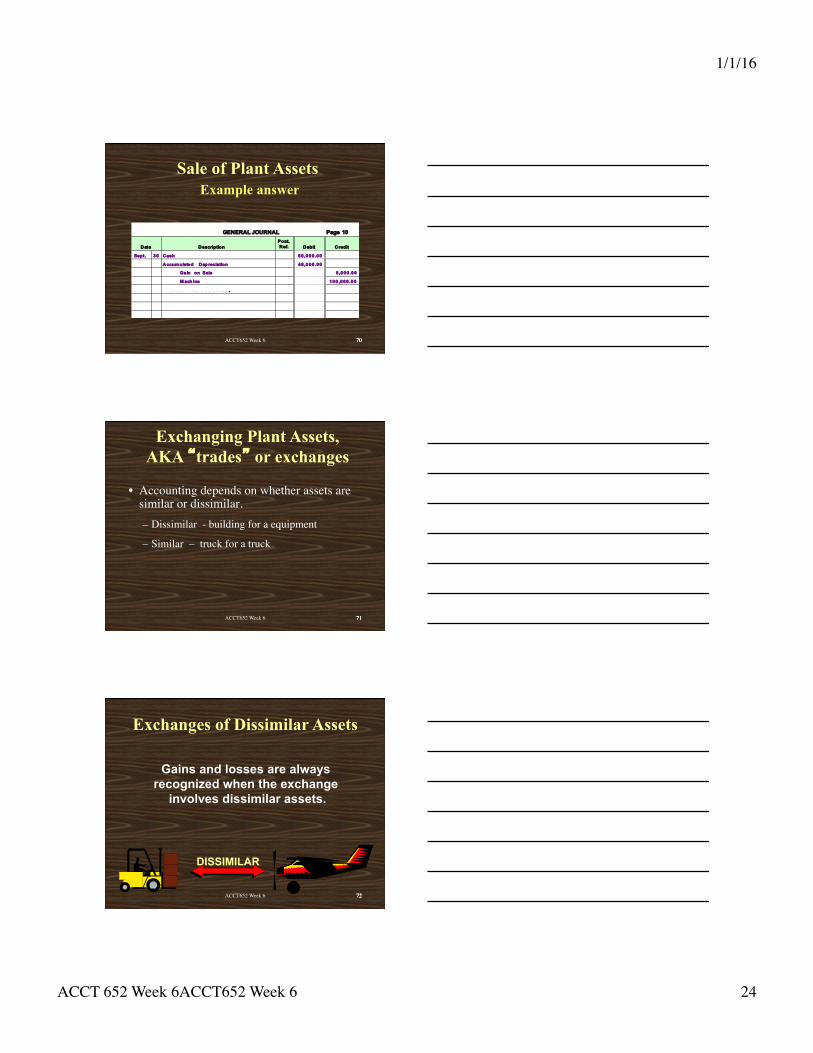

Sale of Plant Assets Example answer

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

Sept. 30 Cash 60,000.00

Accumulated Dep reciation 46,000.00

Gain on Sale 6,000.00

M ach ine 100,000.00

ACCT652 Week 6 717171

• Accounting depends on whether assets are similar or dissimilar.– Dissimilar - building for a equipment

– Similar – truck for a truck

Exchanging Plant Assets, AKA “trades” or exchanges

ACCT652 Week 6 727272

Exchanges of Dissimilar Assets

Gains and losses are always recognized when the exchange

involves dissimilar assets.

DISSIMILAR

1/1/16

ACCT 652 Week 6ACCT652 Week 6 25

ACCT652 Week 6 737373

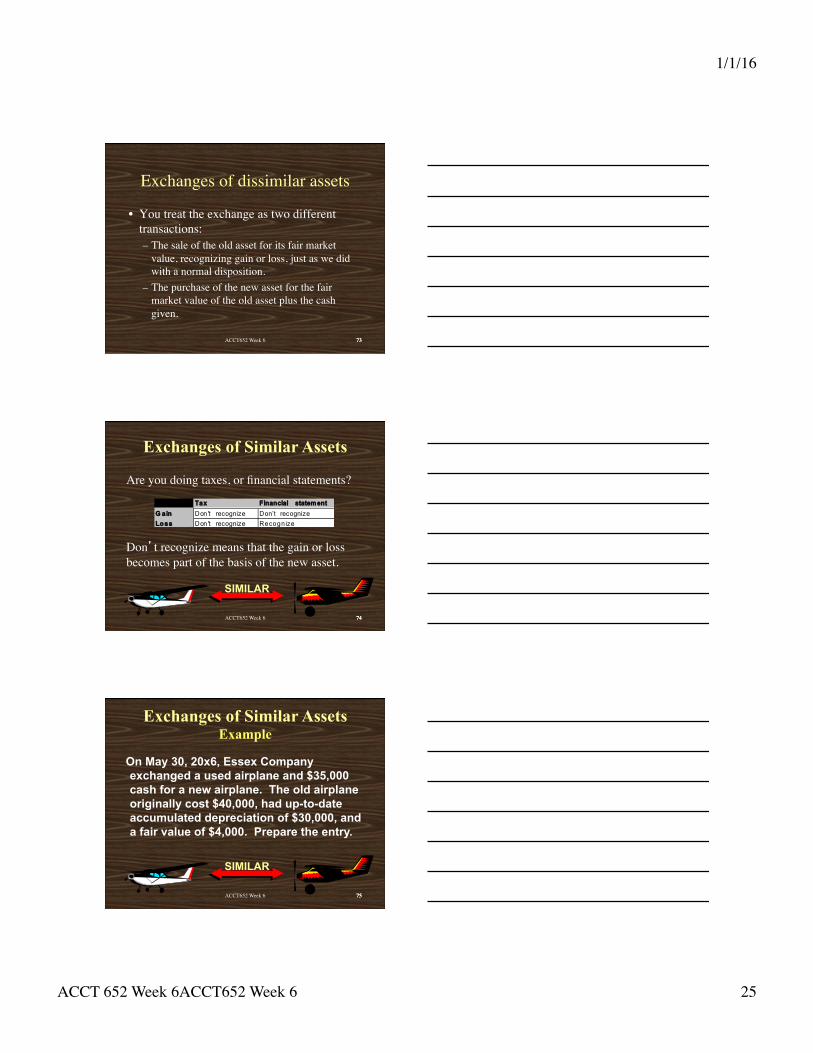

Exchanges of dissimilar assets

• You treat the exchange as two different transactions:– The sale of the old asset for its fair market

value, recognizing gain or loss, just as we did with a normal disposition.

– The purchase of the new asset for the fair market value of the old asset plus the cash given.

ACCT652 Week 6 747474

Are you doing taxes, or financial statements?

Don’t recognize means that the gain or loss becomes part of the basis of the new asset.

SIMILAR

Exchanges of Similar Assets

Tax Financial statement

G ain Don't recognize Don’t recognizeLoss Don't recognize Recognize

ACCT652 Week 6 757575

On May 30, 20x6, Essex Company exchanged a used airplane and $35,000 cash for a new airplane. The old airplane originally cost $40,000, had up-to-date accumulated depreciation of $30,000, and a fair value of $4,000. Prepare the entry.

SIMILAR

Exchanges of Similar Assets Example

1/1/16

ACCT 652 Week 6ACCT652 Week 6 26

ACCT652 Week 6 767676

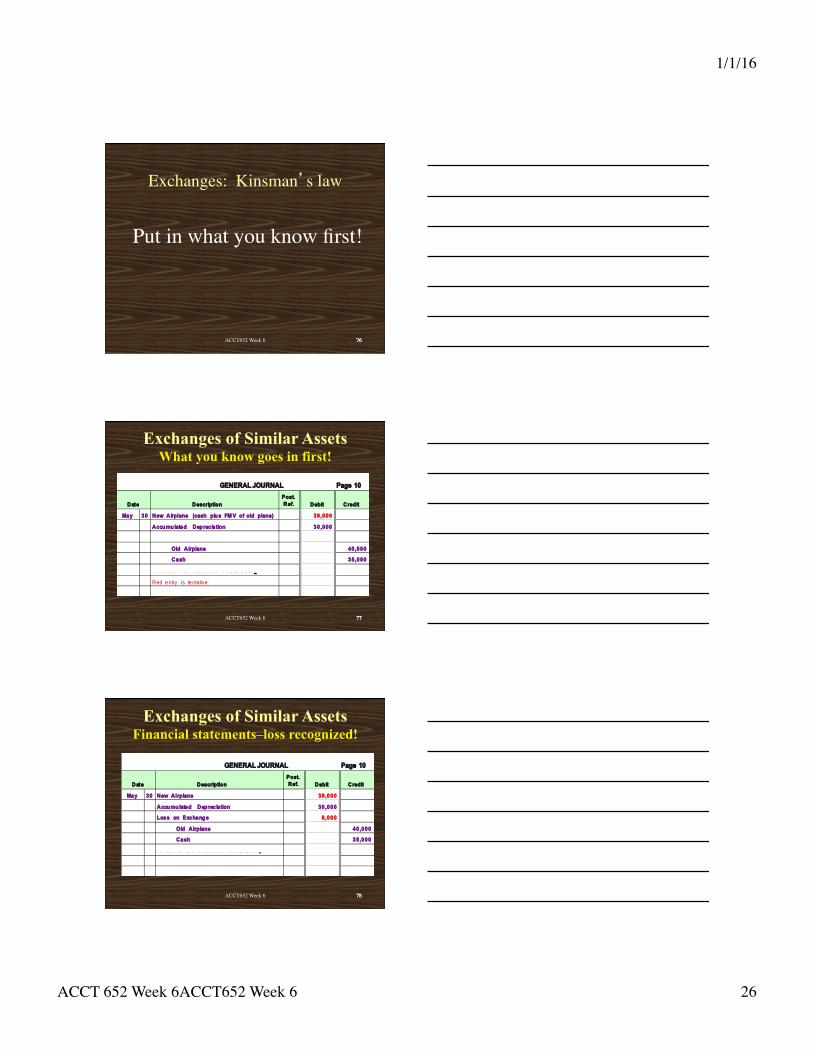

Exchanges: Kinsman’s law

Put in what you know first!

ACCT652 Week 6 777777

Exchanges of Similar Assets What you know goes in first!

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

May 30 New Airplane (cash plu s FM V of old plane) 39,000

Accu mulated Dep reciation 30,000

Old Airplane 40,000

Cash 35,000

Red entry is tentative.

ACCT652 Week 6 787878

Exchanges of Similar Assets Financial statements–loss recognized!

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

May 30 New Airplane 39,000

Accumulated Depreciation 30,000

Loss on Exchang e 6,000

Old Airplane 40,000

Cash 35,000

1/1/16

ACCT 652 Week 6ACCT652 Week 6 27

ACCT652 Week 6 797979

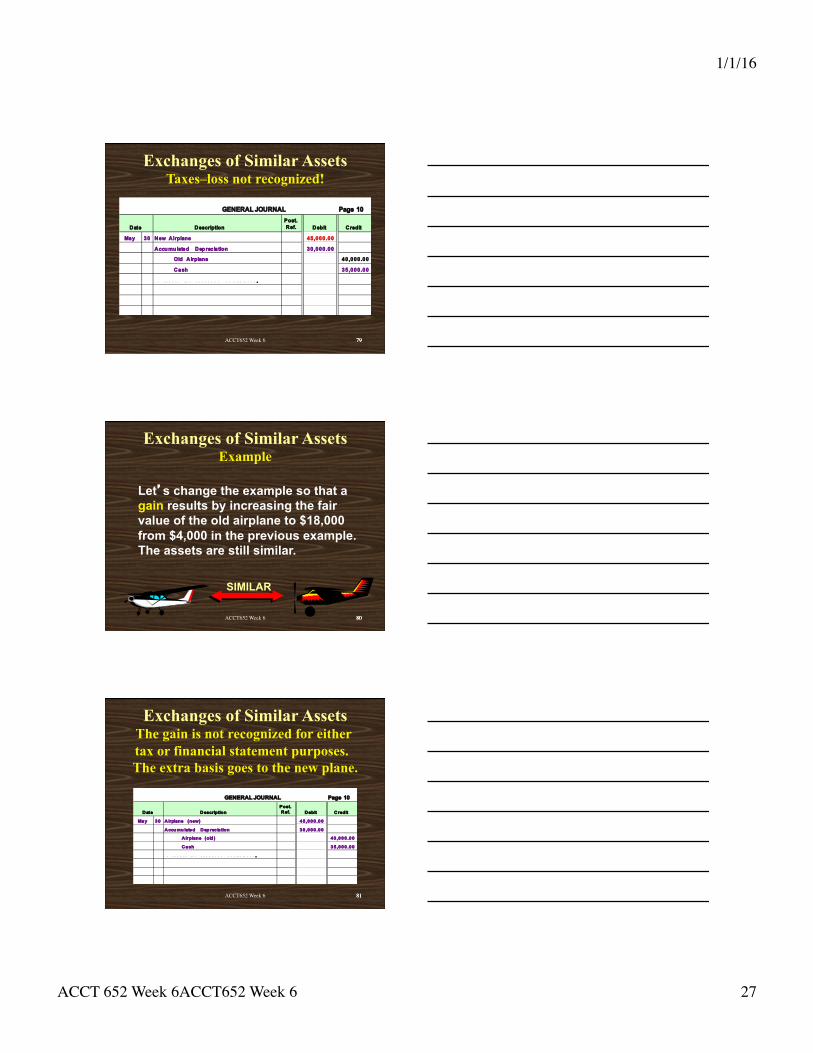

Exchanges of Similar Assets Taxes–loss not recognized!

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

May 30 New Airplane 45,000.00

Accu mulated Dep reciation 30,000.00

Old Airplane 40,000.00

Cash 35,000.00

ACCT652 Week 6 808080

Let’s change the example so that a gain results by increasing the fair value of the old airplane to $18,000 from $4,000 in the previous example. The assets are still similar.

SIMILAR

Exchanges of Similar Assets Example

ACCT652 Week 6 818181

Exchanges of Similar Assets The gain is not recognized for either tax or financial statement purposes. The extra basis goes to the new plane.

GENERAL JOURNAL Page 10

Date DescriptionPost. Ref. Debit Credit

May 30 Airplane (new) 45,000.00

Accumulated Depreciation 30,000.00

Airplane (old ) 40,000.00

Cash 35,000.00

1/1/16

ACCT 652 Week 6ACCT652 Week 6 28

ACCT652 Week 6 8282

Natural Resources• Supplied by nature and extracted from

natural environment.– Examples include standing timber, mineral

deposits and oil reserves.• Because the asset is physically consumed,

they are often called wasting assets.• Presented on balance sheet as non-current

asset at cost less accumulated depletion.The image cannot be displayed. Your computer may not have

ACCT652 Week 6 8383

Natural Resources• Total cost of asset is cost of acquisition,

exploration and development.

• Total cost created by consuming the usefulness of the resource is called depletion.

• Depletion expense is calculated on the units-of-production basis.The image

cannot be displayed. Your computer may not have

ACCT652 Week 6 8484

Intangible Assets• Noncurrent assets without physical existence.

• Often provide exclusive rights or privileges to the owner of the asset.

• Examples: patents, copyrights, leaseholds, leasehold improvements, goodwill, and trademarks.

• When an intangible asset is purchased it is recorded at cost.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 29

ACCT652 Week 6 8585

Intangible Assets

• The recorded cost of an intangible asset is amortized over the shorter of economic or legal life.

• The straight-line method is used to amortize recorded cost.

• If the cost is immaterial, it may be expensed.

ACCT652 Week 6 8686

Patents• Exclusive right granted by federal

government to sell or manufacture an invention.

• The recorded cost includes the purchase price plus any legal cost incurred to defend the patent.

• Amortized over shorter of useful life or 20-year legal life.

ACCT652 Week 6 8787

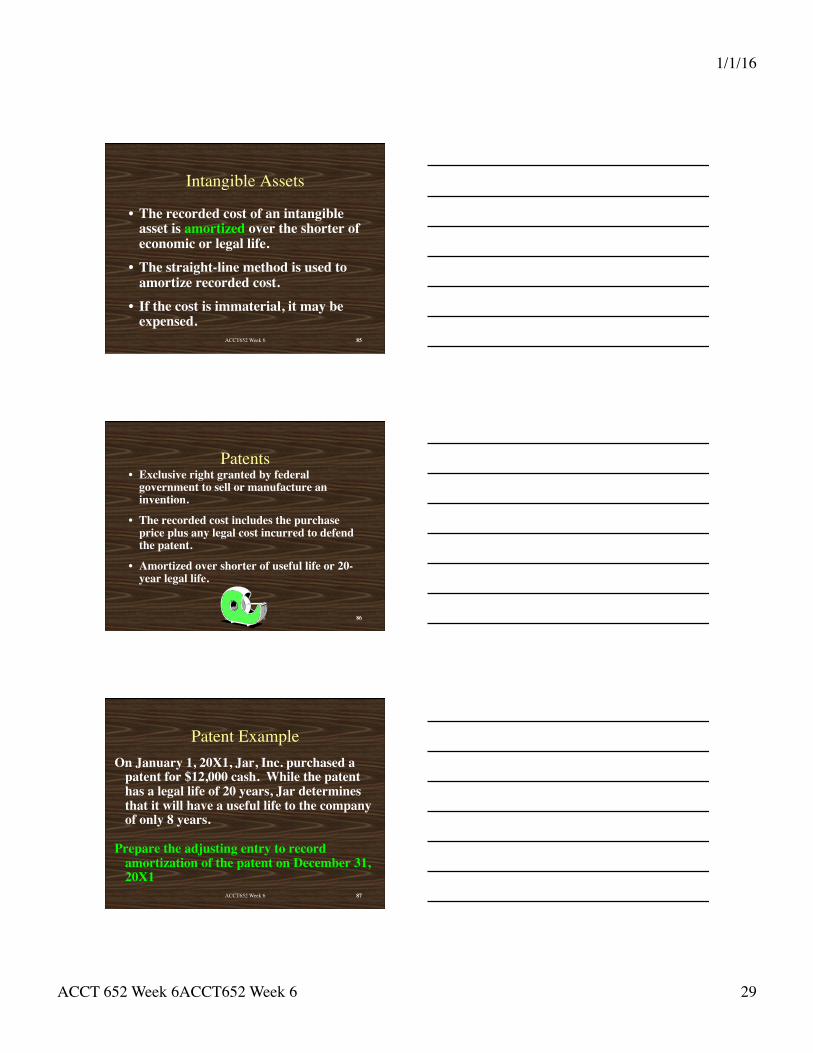

Patent ExampleOn January 1, 20X1, Jar, Inc. purchased a

patent for $12,000 cash. While the patent has a legal life of 20 years, Jar determines that it will have a useful life to the company of only 8 years.�

Prepare the adjusting entry to record amortization of the patent on December 31, 20X1

1/1/16

ACCT 652 Week 6ACCT652 Week 6 30

ACCT652 Week 6 8888

Patent Example GENERAL JOURNAL Page 18

D ate D escrip tionPost. R ef. D eb it C red it

D ec . 31 Am ortization Expense, Patent 1,50 0 Paten ts 1 ,50 0

Cost of patent $12,000 Useful life in years ÷ 8 Annual amortization $ 1,500

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file

ACCT652 Week 6 8989

Copyrights• The federal government grants an exclusive

right to protect artistic or intellectual properties.

• The legal life is the life of creator plus 70 years.

• The actual amortization is over the useful life of the asset.

ACCT652 Week 6 9090

Leaseholds• A lease is a contract to rent property

granted �by lessor to lessee.

• The rights granted by lessor under the lease are calleda leasehold.

• A leasehold is recorded only if an advance payment is involved. Otherwise the periodic payments are recorded as rent expense.

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to delete the image and then insert it again.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 31

ACCT652 Week 6 9191

Leasehold Improvements• Leasehold improvement are long-lived

improvements made to leased property by the lessee.

• Capitalize the costs incurred with a debit to Leasehold Improvements.

• Amortize the improvements over the shorter of useful life of the asset or the life of the lease.

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to delete the image and then insert it again.

ACCT652 Week 6 9292

Goodwill

• Occurs when one company buys another company.

• Goodwill is the amount by which purchase price exceeds the fair market value of net assets acquired.

• Only purchased goodwill is recorded as an intangible asset.

ACCT652 Week 6 9393

Goodwill• Each year, the value of the goodwill

recorded on the balance sheet is analyzed.

• If the value has gone down (this is called “goodwill impairment”), the decrease is recorded as an expense and the value of the goodwill on the balance sheet is reduced.

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to delete the image and then insert it again.

1/1/16

ACCT 652 Week 6ACCT652 Week 6 32

ACCT652 Week 6 9494

Goodwill• In order to determine the decrease in

value, we must analyze the fair market value of the goodwill. Essentially, we do an appraisal of it annually.

• You will talk more in finance about how to do that appraisal–it is essentially the present value of the increased after tax cash flows the purchase brings the firm.

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to delete the image and then insert it again.

ACCT652 Week 6 9595

Goodwill• For taxes, we amortize goodwill over a

straight line amortization period of 15 years. The image cannot be

displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to delete the image and then insert it again.

ACCT652 Week 6 9696

Trademarks and Trade Names• A symbol, design, or logo associated with a

business.

• Purchased trademarks are recorded at cost and amortized over shorter of legal life or economic life. If the use of the trademark will not expire, it is not amortized.

• Amounts spent to maintain or enhance the value of a trademark or trade name are charged to expense.

The image cannot be displayed

1/1/16

ACCT 652 Week 6ACCT652 Week 6 33

ACCT652 Week 6 9797ACCT 652 Week 6 97

Thank you for a good night

• Remember that appeals on your exams, if any, are due back by next week before the start of class.