Accounting “Oopsies” Accounting Topics That Can Trip You Up & Cause You To Go “Oops!”

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC

Jennifer Goodman, CPA, CGMA Shareholder, Elliott Davis Decosimo May 12, 2015

1

This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation is for informational purposes and does not contain or convey specific advice. It should not be used or relied upon in regard to any particular situation or circumstances without first consulting the appropriate advisor. No part of the presentation may be circulated, quoted, or reproduced for distribution without prior written approval from Elliott Davis Decosimo.

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC

Accounting “Oopsies”

2

Accounting “Oopsies”

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 3

Accounting “Oopsie” aka uhoh, whoops, mistake, #$&!

___________________

• Oopsie topics not overly technical, but have an unusual element that can sometimes trip us up

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 4

• Accruals • Capitalization Minimums • Legal Fees • Compensated Absences • FOB Destination vs Shipping • Stock Compensation

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 5

Accruals

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 6

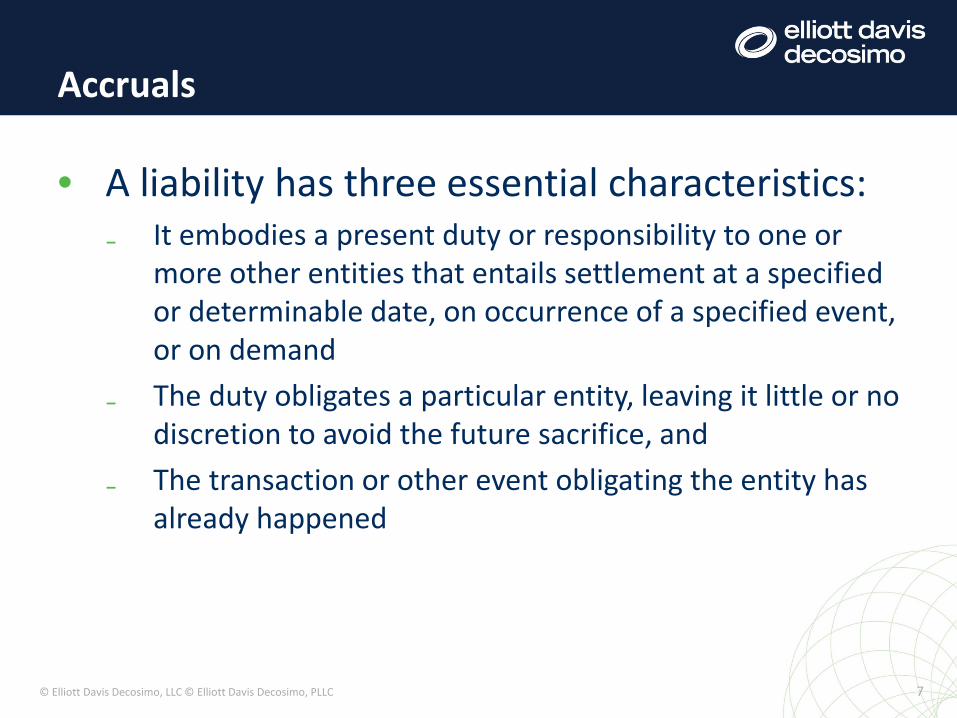

• A liability has three essential characteristics: ₋ It embodies a present duty or responsibility to one or

more other entities that entails settlement at a specified or determinable date, on occurrence of a specified event, or on demand

₋ The duty obligates a particular entity, leaving it little or no discretion to avoid the future sacrifice, and

₋ The transaction or other event obligating the entity has already happened

Accruals

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 7

• A public accounting firm has been engaged to audit your financial statements for the year ended 12/31/2014 ₋ You sign the engagement letter which commits your

company and the firm to the terms of the engagement letter on 10/1/2014

₋ Your bank requires an audit so there is no uncertainty that the cost will be incurred

• Is it proper to accrue the entire audit fee as an expense in 2014?

Accruals – Example #1

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 8

• Your boss wants F/S by January 10th. You use a PO system for inventory purchases but not other expenses. The auditors always seem to find one or two invoices that slip through the cracks and don’t get accrued

• To avoid an audit adjustment this year, you decide to accrue a $50k “general accrual” for possible un-accrued invoices and for the spring in-house retreat which the board has approved and budgeted $25k for the event

• If you were auditing this entity, how would you conclude on the $50k general accrual?

Accruals – Example #2

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 9

• On Sept 1, the board has approved management’s plan to shut down Building 4 production and production ceased

November 1 • Half of the equipment will be relocated to another facility

within the company next year and half of the equipment is currently up for sale for $250k, it’s fair market value

• The lessor was notified of the building lease termination before year end but you have 1 more year obligation on the lease agreement

Accruals – Example #3

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 10

• It’s December 31 and you have identified the following costs associated with the shut down:

NBV of equipment $ 1,000,000 One-time termination benefits paid in January $ 50,000 Remaining bldg. lease payments due – do not plan to sublease forgoing $40,000 in lease income $ 100,000 Estimated equipment relocation/set-up cost to be incurred in February $ 200,000 Estimated general cost for shut down (ex. building repairs, employee relocation, clean up) $ 75,000

Accruals – Example #3

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 11

• What losses/impairments and accruals should be reflected at December 31?

Half of property held for sale $ 250,000 Half of property held and used evaluate One-time termination benefits paid in January Employees identified, completion date set and employees informed $ 50,000 Lease (100,000 less sublease value 40,000) $ 60,000 • Cannot accrue for relocation costs or “general accruals” • Commitment to an exit or disposal plan by management

does not, by itself, result in the incurrence of a liability

Accruals – Example #3

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 12

Capitalization Minimums

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 13

• Capitalization Policies ₋ For expediency, many entities adopt policies specifying

the minimum cost that a property unit must have before it is capitalized

₋ These policies are acceptable for US GAAP as long as the minimum is reasonable

₋ There is not an automatic assumption the new $5k IRS De Minimis rule is acceptable for GAAP purposes

Capitalization Minimums

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 14

• New IRS rules for capitalization and depreciation: ₋ IRS released regulations on capitalization of tangible

property costs that provide a “de minimis safe harbor election”

₋ Allows eligible businesses to expense certain property that would otherwise have to be capitalized

₋ To qualify, you must have book capitalization policies in place for expensing amounts costing less than a specified amount or have a useful life of 12 months or less

Capitalization Minimums

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 15

• Entity has annual sales of $2.5M • Net income is $250k • Total PPE NBV is $3M

₋ The CFO wants to put a new capitalization policy in place which states that tangible property with a useful life over 1 year is capitalized if purchase price is over $5k

Is this policy reasonable?

Capitalization Minimums - Example

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 16

Legal fees Capitalize, Accrue or Expense???

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 17

• Acquisition related costs 805-10-25 (finder’s fees, advisory, legal, accounting, valuation, and other professional or consulting fees) ₋ General rule - expense acquisition fees ₋ Exception – registering and issuing debt securities

• Capitalize and amortize ₋ Exception – registering and issuing equity securities

• Paid in capital

Legal Fees – Business Combinations

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 18

Legal Fees – Example Business Combinations Footnote

Consideration $1,949,000

Identifiable Assets Acquired:

Inventories $ 170,000

Machinery and equipment $1,109,000

Other intangibles $595,000

Total identifiable assets $1,874,000

Goodwill $75,000

$1,949,000

Legal fees expensed in operations $ 157,000

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 19

• You pick your policy! ₋ Select an accounting policy that provides for either the

inclusion or exclusion of estimated legal fees • Consistently apply such a policy

₋ If policy is to include legal fees as part of loss contingency accrual – • Costs should be accrued even when the related loss is not accrued

• Another tricky area is when there is a range of losses for estimating loss contingencies ₋ Sometimes choosing the low end range is correct

Legal Fees – Loss Contingencies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 20

Step 1: Has liability derecognition threshold been met? Yes – Apply extinguishment accounting Step 2: Is borrower experiencing financial difficulties and lender is granting concessions? Yes – Apply troubled debt restructuring accounting Step 3: Is new or changed loan “substantially different” from old loan? Yes – Apply Extinguishment Accounting No – Apply Modification Accounting

Legal Fees – Debt Modifications and Restructuring

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 21

Debt treatment

Fees between

borrower/lender

Cost incurred with third parties

i.e. Legal Counsel

Unamortized deferred cost of old

loan

Extinguishment Accounting

Expensed Capitalized and amortize to

expense over new loan term

Written off

Modification Accounting

Reflected in debt premium or

discount

Expensed Leave on books and continue to

amortize

Legal Fees – Debt Modification or Extinguishment

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 22

• ABC Bank hires Lewis law firm in connection with

your loan modification. ABC Bank tells Lewis to bill you directly for legal services provided to ABC Bank in relation to the loan. You agree to pay Lewis directly

• Lewis bills you $100,000 and ABC Bank bills you $400,000 for fees associated with the modification

• How do you account for these fees?

Legal Fees – Example Debt Modification

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 23

Compensated Absences

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 24

• ASC 710 Compensation – a liability should be accrued for compensation if all of the following: Obligation attributable to services already rendered

• Rights vest or accumulate ₋ Vest – obligation to pay even if employee terminated ₋ Accumulate – rights may be carried forward ₋ Modification rule for sick pay where accrual not

required but permitted if rights accumulate but do not vest

• Payment is probable, and • Amount can be estimated

Compensated Absences

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 25

• Suzanne has earned but not used 5 days of vacation and 5 days of sick pay at 12/31/2014

Your Company Policy: Vacation and sick days accumulate but will not be paid if employment is terminated. An employee can only use sick days due to illness.

₋ Should vacation and sick pay be accrued at 12/31/14? ₋ What if new employees have to wait until second year of

employment to take vacation? ₋ Accrue at current salary rates or salary rates expected at

time vacation is actually paid?

Compensated Absences - Example

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 26

FOB shipping point vs destination

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 27

• FOB terms are an important consideration in product sales, because they determine the point at which title to the product, and thus the risks and rewards of ownership, has legally passed to the buyer ₋ FOB destination indicates that title to the product passes

upon delivery to the customer • Revenue recorded when it reaches customer

₋ FOB shipping point indicates that title to the product passes at the time of shipment • Revenue recorded when it ships

FOB shipping point vs destination

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 28

• Your product is sold FOB shipping point as indicated

on the invoice. However, for one important customer you have agreed to be responsible for hiring and paying the shipping agent and insuring the goods in transit.

Can you recognize the sale upon shipment?

FOB Shipping Point - Example

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 29

• A third party shipping agent rather than your

company has assumed the risk of physical loss on the products during transit

Can you go ahead and recognize the sale since you no longer have the risk of loss during transit?

FOB Destination - Example

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 30

• A company has a implied (not written) policy of

replacing lost or damaged goods. The contractual terms specifically state that product is FOB shipping point. Can the Company recognize revenue at the time of shipment?

The phrase “synthetic FOB destination” is used when a vendor offers FOB shipping point terms, but also has a standard business practice of replacing goods that are lost or damaged while in transit to the customer.

FOB Shipping Point - Example

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 31

Stock Compensation

Accounting Oopsies

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 32

• ASC 718 Compensation – Stock Compensation ₋ Applies to both public and non-public companies ₋ Some examples

• Stock issued to employee • Stock options • Incurring liabilities based on price of company’s stock • Restricted stock units (RSU)

BIGGEST TRIP UP – ASSUMING AWARD HAS NO FIANCIAL IMPACT

Employee Stock Based Compensation

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 33

• ASC 718’s measurement objective – ₋ Determine the fair value of stock-based compensation at

the grant date assuming that employees fulfill the award’s vesting conditions and will retain the award

• The fair value of an award – ₋ Reflect the estimated value that the company would be

obligated to provide when an employee is entitled to the award and is no longer required to provide service to the employer

Employee Stock Based Compensation

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 34

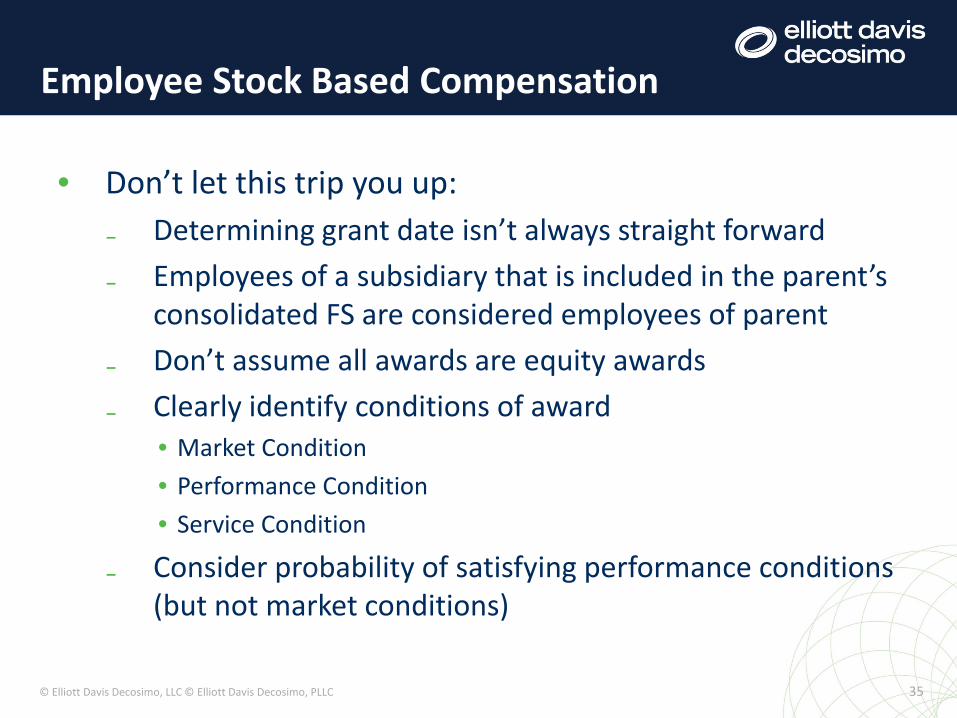

• Don’t let this trip you up: ₋ Determining grant date isn’t always straight forward ₋ Employees of a subsidiary that is included in the parent’s

consolidated FS are considered employees of parent ₋ Don’t assume all awards are equity awards ₋ Clearly identify conditions of award

• Market Condition • Performance Condition • Service Condition

₋ Consider probability of satisfying performance conditions (but not market conditions)

Employee Stock Based Compensation

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 35

Questions?

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC © Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 36

Providing Additional Resources to Meet Your Needs

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC

Subscribe at www.elliottdavis.com/subscribe

37

Jennifer Goodman Email: [email protected] Phone: 423.266.2308 Website: www.elliottdavis.com

Elliott Davis Decosimo ranks among the top 30 CPA firms in the U.S. With sixteen offices across seven states, the firm provides clients across a wide range of industries with smart, customized solutions. Elliott Davis Decosimo is an independent firm associated with Moore Stephens International Limited, one of the world's largest CPA firm associations with resources in every major market around the globe. For more information, please visit elliottdavis.com.

© Elliott Davis Decosimo, LLC © Elliott Davis Decosimo, PLLC 38