drewry.co.uk

A ‘best-route’ market study for

containerised imports to South

Germany

MARKET STUDY | 1 March 2016

Drewry Supply Chain Advisors | Market Study March 2016

Page 2

© Drewry Shipping Consultants Ltd 2016

Table of Contents

About Drewry Supply Chain Advisors 3

Introducing Best Routes – South Germany 4

Marine connectivity for imports from Shanghai to South Germany 5

Intermodal Connectivity 7

Routing options based on fastest maritime and average inland transit times 8

Tracking relative ocean freight rates by port range 13

Drewry Supply Chain Advisors | Market Study March 2016

Page 3

© Drewry Shipping Consultants Ltd 2016

About Drewry Supply Chain Advisors

We are the market leader in ocean freight market intelligence and cost

benchmarking, providing an elite client base of retailers and manufacturers

with tailored solutions that combine data, tools and advisory services to

improve transport procurement and reduce cost.

Our professionals focus on advising users of international multi-modal transport

services, taking our extensive understanding of the industry and applying it to

all stages of your supply chain. Through our market understanding, industry

knowledge and operational experience, we can help ocean freight

procurement teams reduce costs and more effectively manage their network of

international transport network and supply chain service providers.

Drewry Supply Chain Advisors | Market Study March 2016

Page 4

© Drewry Shipping Consultants Ltd 2016

A best-route market study for

containerised imports to South Germany

MARKET STUDY | 1 March 2016

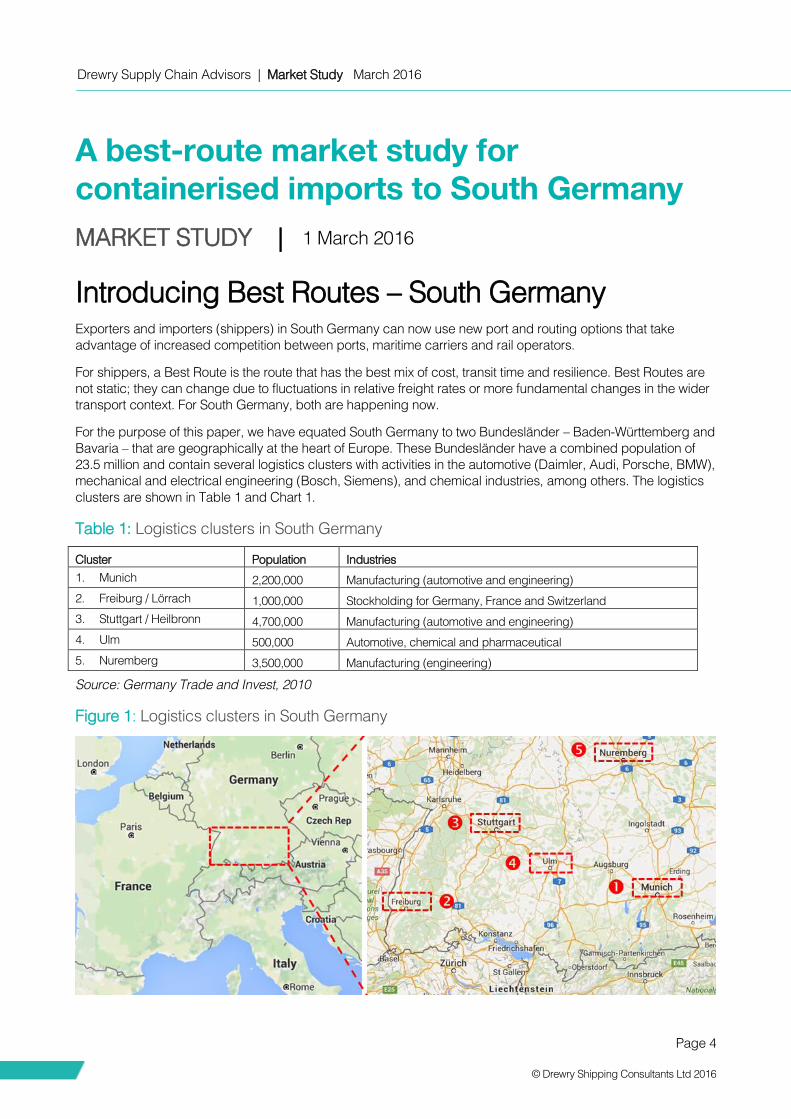

Introducing Best Routes – South Germany Exporters and importers (shippers) in South Germany can now use new port and routing options that take

advantage of increased competition between ports, maritime carriers and rail operators.

For shippers, a Best Route is the route that has the best mix of cost, transit time and resilience. Best Routes are

not static; they can change due to fluctuations in relative freight rates or more fundamental changes in the wider

transport context. For South Germany, both are happening now.

For the purpose of this paper, we have equated South Germany to two Bundesländer – Baden-Württemberg and

Bavaria – that are geographically at the heart of Europe. These Bundesländer have a combined population of

23.5 million and contain several logistics clusters with activities in the automotive (Daimler, Audi, Porsche, BMW),

mechanical and electrical engineering (Bosch, Siemens), and chemical industries, among others. The logistics

clusters are shown in Table 1 and Chart 1.

Table 1: Logistics clusters in South Germany

Cluster Population Industries

1. Munich 2,200,000 Manufacturing (automotive and engineering)

2. Freiburg / Lörrach 1,000,000 Stockholding for Germany, France and Switzerland

3. Stuttgart / Heilbronn 4,700,000 Manufacturing (automotive and engineering)

4. Ulm 500,000 Automotive, chemical and pharmaceutical

5. Nuremberg 3,500,000 Manufacturing (engineering)

Source: Germany Trade and Invest, 2010

Figure 1: Logistics clusters in South Germany

Drewry Supply Chain Advisors | Market Study March 2016

Page 5

© Drewry Shipping Consultants Ltd 2016

Munich, the most populous city (population of 1.4 million), is between 500 km and 850 km from any deep-sea

port:

Hamburg: 790 km

Antwerp: 790 km

Rotterdam: 840 km

Genoa: 650 km

Trieste: 510 km

Koper: 510 km

This “landlocked” location is a curse as well as a blessing. On the one hand, inland transportation costs are high

and shippers are dependent on transport operators for a key element of their product delivery namely timely

dispatch or delivery. On the other hand, because of its central location, South German shippers can choose their

Best Route from the numerous alternatives should an operator fail to deliver on promises.

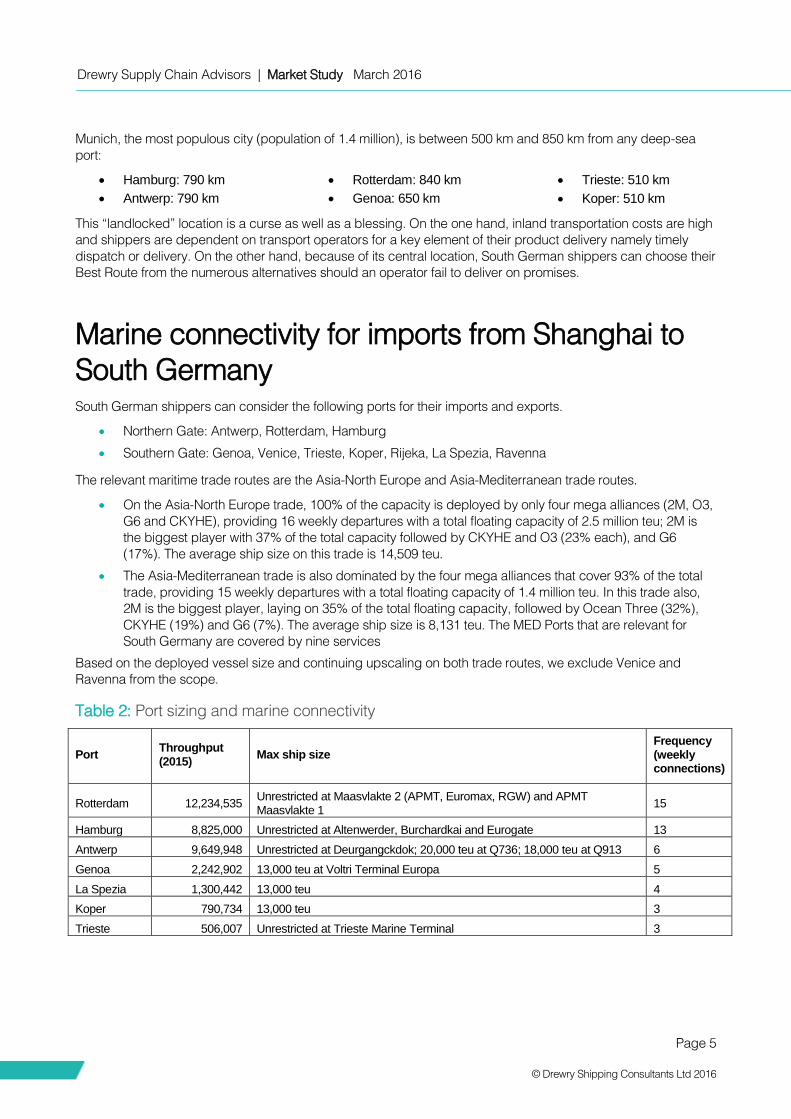

Marine connectivity for imports from Shanghai to

South Germany South German shippers can consider the following ports for their imports and exports.

Northern Gate: Antwerp, Rotterdam, Hamburg

Southern Gate: Genoa, Venice, Trieste, Koper, Rijeka, La Spezia, Ravenna

The relevant maritime trade routes are the Asia-North Europe and Asia-Mediterranean trade routes.

On the Asia-North Europe trade, 100% of the capacity is deployed by only four mega alliances (2M, O3,

G6 and CKYHE), providing 16 weekly departures with a total floating capacity of 2.5 million teu; 2M is

the biggest player with 37% of the total capacity followed by CKYHE and O3 (23% each), and G6

(17%). The average ship size on this trade is 14,509 teu.

The Asia-Mediterranean trade is also dominated by the four mega alliances that cover 93% of the total

trade, providing 15 weekly departures with a total floating capacity of 1.4 million teu. In this trade also,

2M is the biggest player, laying on 35% of the total floating capacity, followed by Ocean Three (32%),

CKYHE (19%) and G6 (7%). The average ship size is 8,131 teu. The MED Ports that are relevant for

South Germany are covered by nine services

Based on the deployed vessel size and continuing upscaling on both trade routes, we exclude Venice and

Ravenna from the scope.

Table 2: Port sizing and marine connectivity

Port Throughput (2015)

Max ship size Frequency (weekly connections)

Rotterdam 12,234,535 Unrestricted at Maasvlakte 2 (APMT, Euromax, RGW) and APMT Maasvlakte 1

15

Hamburg 8,825,000 Unrestricted at Altenwerder, Burchardkai and Eurogate 13

Antwerp 9,649,948 Unrestricted at Deurgangckdok; 20,000 teu at Q736; 18,000 teu at Q913 6

Genoa 2,242,902 13,000 teu at Voltri Terminal Europa 5

La Spezia 1,300,442 13,000 teu 4

Koper 790,734 13,000 teu 3

Trieste 506,007 Unrestricted at Trieste Marine Terminal 3

Drewry Supply Chain Advisors | Market Study March 2016

Page 6

© Drewry Shipping Consultants Ltd 2016

Rotterdam has the best maritime connectivity in the Northern Gate with 15 of the 16 services calling at

the port. The service coverage is also homogeneous, illustrating the commitment of each alliance to

offer their best possible service to Rotterdam by making it an anchor port of their string:

All four alliances have at least one service offering Shanghai-Rotterdam with a transit time of 29

days.

Eight of the 15 services, two for each alliance, have Rotterdam as a first port of call (within the

relevant port set).

Hamburg receives calls from 13 of the 16 services in the Northern Gate. Seven of those have Hamburg

as a first port of call: three for CKYHE, two for 2M and one each for O3 and G6. CKYHE’s commitment to

Hamburg is illustrated by its NE8 service, which offers the best transit time of 29 days, and its NE6

service which, together with 2M’s AE2/Swan service, offers 30 days.

Antwerp has to settle with only six Asia-Europe service calls, or less than half the services calling at

Hamburg. These six services generate eight calls because two services from 2M make a double call to

benefit from the export volumes generated in the Antwerp hinterland. Volumes at Antwerp are boosted

by MSC’s European Hub strategy which links a network of dedicated block trains with its AE2/Swan

service that offers a market leading transit time of 25 days from Shanghai.

Genoa is called by five of the nine Southern Gate services, giving it the best maritime connectivity of all

the Southern Gate ports in this study, but far fewer than Rotterdam and Hamburg in the Northern Gate.

Genoa receives two services from CKYHE and one each from the other three alliances. The best transit

time of 27 days is offered by CKYHE, followed closely by 2M’s AE20/Dragon offering 28 days. The

average transit time is 29 days compared to 33 for the Northern Gate.

La Spezia is called by four of the nine services, with 2M offering two direct calls, and O3 and CKYHE

offering one each. There is no coverage from G6. Each alliance offers a transit time of 27 days to La

Spezia, but the second 2M service offers 30 days.

From the North Adriatic ports, Koper provides the best maritime connectivity with three direct calls, one

each from 2M, O3 and CKYHE. O3’s PHEX/AMC4/AMX8 service makes a double call to load (re-)export

volumes. 2M’s AE12/TP2/Phoenix/Jaguar service offers a 25-day transit time, making it a true competitor

to Genoa as well as the Northern Gate. The same services call at Trieste, but since Trieste is the next

call, the transit times are two to three days longer.

Figure 2: Comparative transit times

Source: Drewry Supply Chain Advisors

24

26

28

30

32

34

36

RTM HAM ANR GEN SPE KOP TRI

Fastest maritime transit time

Average maritime transit time

Drewry Supply Chain Advisors | Market Study March 2016

Page 7

© Drewry Shipping Consultants Ltd 2016

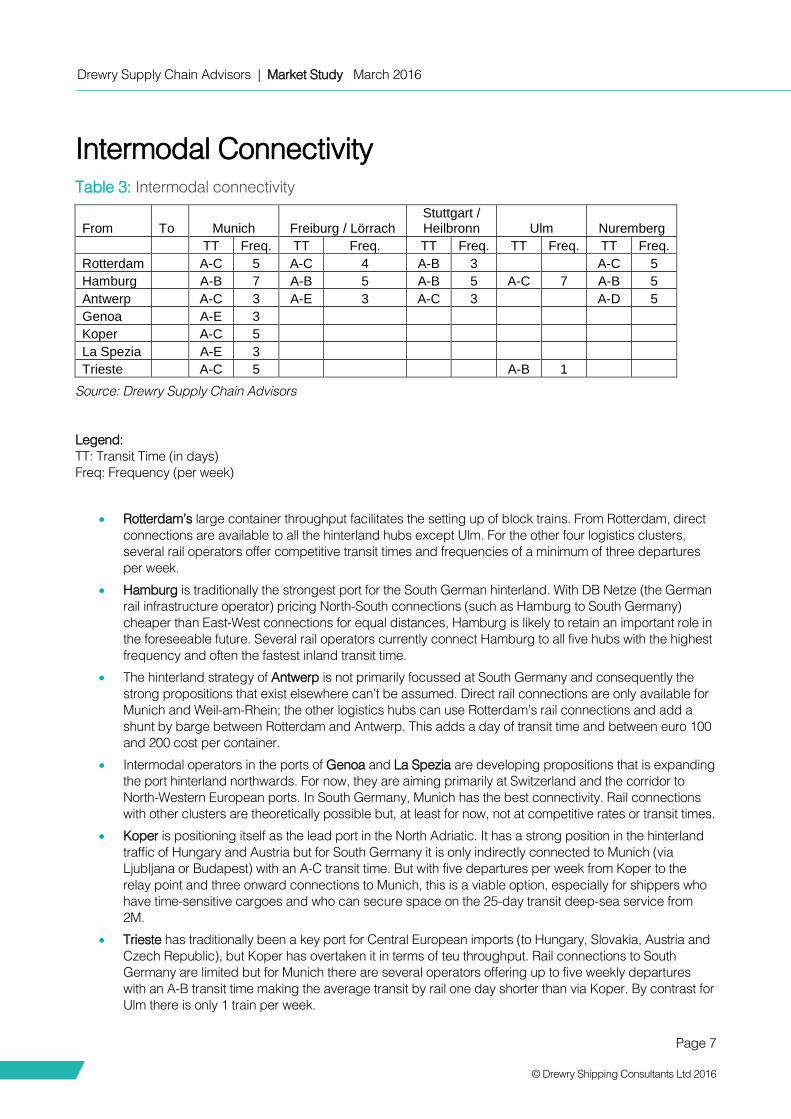

Intermodal Connectivity Table 3: Intermodal connectivity

From To Munich Freiburg / Lörrach Stuttgart / Heilbronn Ulm Nuremberg

TT Freq. TT Freq. TT Freq. TT Freq. TT Freq.

Rotterdam A-C 5 A-C 4 A-B 3 A-C 5

Hamburg A-B 7 A-B 5 A-B 5 A-C 7 A-B 5

Antwerp A-C 3 A-E 3 A-C 3 A-D 5

Genoa A-E 3

Koper A-C 5

La Spezia A-E 3

Trieste A-C 5 A-B 1

Source: Drewry Supply Chain Advisors

Legend:

TT: Transit Time (in days)

Freq: Frequency (per week)

Rotterdam’s large container throughput facilitates the setting up of block trains. From Rotterdam, direct

connections are available to all the hinterland hubs except Ulm. For the other four logistics clusters,

several rail operators offer competitive transit times and frequencies of a minimum of three departures

per week.

Hamburg is traditionally the strongest port for the South German hinterland. With DB Netze (the German

rail infrastructure operator) pricing North-South connections (such as Hamburg to South Germany)

cheaper than East-West connections for equal distances, Hamburg is likely to retain an important role in

the foreseeable future. Several rail operators currently connect Hamburg to all five hubs with the highest

frequency and often the fastest inland transit time.

The hinterland strategy of Antwerp is not primarily focussed at South Germany and consequently the

strong propositions that exist elsewhere can’t be assumed. Direct rail connections are only available for

Munich and Weil-am-Rhein; the other logistics hubs can use Rotterdam’s rail connections and add a

shunt by barge between Rotterdam and Antwerp. This adds a day of transit time and between euro 100

and 200 cost per container.

Intermodal operators in the ports of Genoa and La Spezia are developing propositions that is expanding

the port hinterland northwards. For now, they are aiming primarily at Switzerland and the corridor to

North-Western European ports. In South Germany, Munich has the best connectivity. Rail connections

with other clusters are theoretically possible but, at least for now, not at competitive rates or transit times.

Koper is positioning itself as the lead port in the North Adriatic. It has a strong position in the hinterland

traffic of Hungary and Austria but for South Germany it is only indirectly connected to Munich (via

Ljubljana or Budapest) with an A-C transit time. But with five departures per week from Koper to the

relay point and three onward connections to Munich, this is a viable option, especially for shippers who

have time-sensitive cargoes and who can secure space on the 25-day transit deep-sea service from

2M.

Trieste has traditionally been a key port for Central European imports (to Hungary, Slovakia, Austria and

Czech Republic), but Koper has overtaken it in terms of teu throughput. Rail connections to South

Germany are limited but for Munich there are several operators offering up to five weekly departures

with an A-B transit time making the average transit by rail one day shorter than via Koper. By contrast for

Ulm there is only 1 train per week.

Drewry Supply Chain Advisors | Market Study March 2016

Page 8

© Drewry Shipping Consultants Ltd 2016

Routing options based on fastest maritime and

average inland transit times

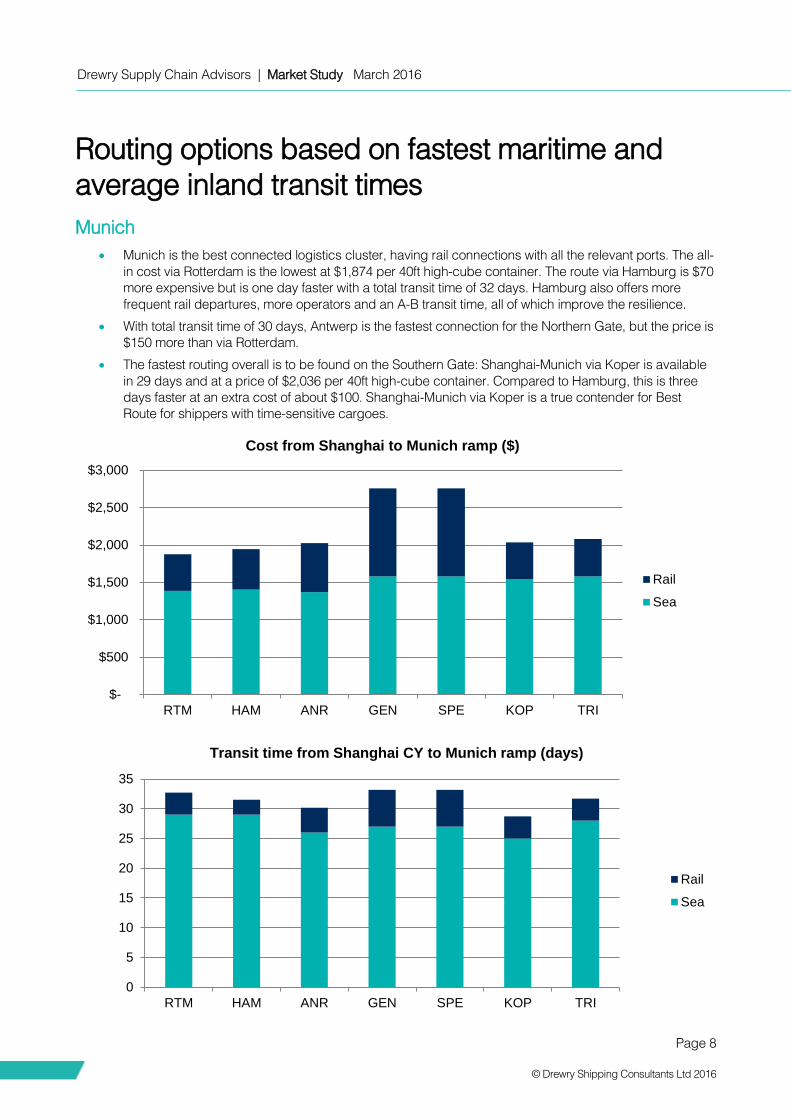

Munich

Munich is the best connected logistics cluster, having rail connections with all the relevant ports. The all-

in cost via Rotterdam is the lowest at $1,874 per 40ft high-cube container. The route via Hamburg is $70

more expensive but is one day faster with a total transit time of 32 days. Hamburg also offers more

frequent rail departures, more operators and an A-B transit time, all of which improve the resilience.

With total transit time of 30 days, Antwerp is the fastest connection for the Northern Gate, but the price is

$150 more than via Rotterdam.

The fastest routing overall is to be found on the Southern Gate: Shanghai-Munich via Koper is available

in 29 days and at a price of $2,036 per 40ft high-cube container. Compared to Hamburg, this is three

days faster at an extra cost of about $100. Shanghai-Munich via Koper is a true contender for Best

Route for shippers with time-sensitive cargoes.

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

RTM HAM ANR GEN SPE KOP TRI

Cost from Shanghai to Munich ramp ($)

Rail

Sea

0

5

10

15

20

25

30

35

RTM HAM ANR GEN SPE KOP TRI

Transit time from Shanghai CY to Munich ramp (days)

Rail

Sea

Drewry Supply Chain Advisors | Market Study March 2016

Page 9

© Drewry Shipping Consultants Ltd 2016

Freiburg / Lörrach

For the Freiburg / Lörrach logistics cluster, only the Northern Gate ports offer competitive connections.

Rail connections from the Southern Gate to Basel exist, but due to the cross border haulage they are

outside the scope of this white paper.

Hamburg is the cheapest routing at $2,082 per 40ft high-cube container, but the cost via Rotterdam is

only $16 higher. The cost via Antwerp at $2,248 is nearly $150 more than via Hamburg.

Thanks to the fast maritime transit on 2M, Antwerp is able to compete with Hamburg on the overall

transit time; however, the rail connection via Antwerp is three times per week on an A-E transit time while

operators in Hamburg are able to offer five departures per week with an A-B transit time. So for an equal

transit time and cheaper price, Hamburg offers much higher resilience than Antwerp.

The routing via Rotterdam scores between Hamburg and Antwerp: with four weekly connections and A-

C transit times, resilience of this route is better than via Antwerp, and an overall transit time of 33 days

puts Rotterdam firmly in the second place to serve this area.

$-

$500

$1,000

$1,500

$2,000

$2,500

RTM HAM ANR GEN SPE KOP TRI

Cost from Shanghai to Freiburg / Lörrach ramp ($)

Rail

Sea

0

5

10

15

20

25

30

35

RTM HAM ANR GEN SPE KOP TRI

Transit time from Shanghai CY to Freiburg / Lörrach ramp (days)

Rail

Sea

Drewry Supply Chain Advisors | Market Study March 2016

Page 10

© Drewry Shipping Consultants Ltd 2016

Stuttgart / Heilbronn

Also for the Stuttgart / Heilbronn region, the Northern Gate is the only competitive option. Rotterdam is

the cheapest routing at $1,924 per 40ft high-cube container and a transit time of 32 days, which is on

par with Hamburg, from where the rate is about $20 more. But on the route via Hamburg there are more

operators offering more frequent departures especially to Kornwestheim. Despite having to barge to

Rotterdam, the route via Antwerp is the fastest with an overall transit time of 30 days. However, at a cost

of $2,071 per 40ft high-cube container, Antwerp is $148 more expensive than Rotterdam and $126

more than Hamburg.

In terms of resilience, Hamburg is again in the lead with operators offering five weekly departures with

an A-B transit time. Rotterdam follows next with three weekly departures of A-B transit. While cargo from

Antwerp connects onto the same trains, it needs one extra day for the barge shunt.

$-

$500

$1,000

$1,500

$2,000

$2,500

RTM HAM ANR GEN SPE KOP TRI

Cost from Shanghai to Stuttgart / Heilbronn ramp ($)

Rail

Sea

0

5

10

15

20

25

30

35

RTM HAM ANR GEN SPE KOP TRI

Transit time from Shanghai CY to Stuttgart/Heilbronn ramp (days)

Rail

Sea

Drewry Supply Chain Advisors | Market Study March 2016

Page 11

© Drewry Shipping Consultants Ltd 2016

Ulm

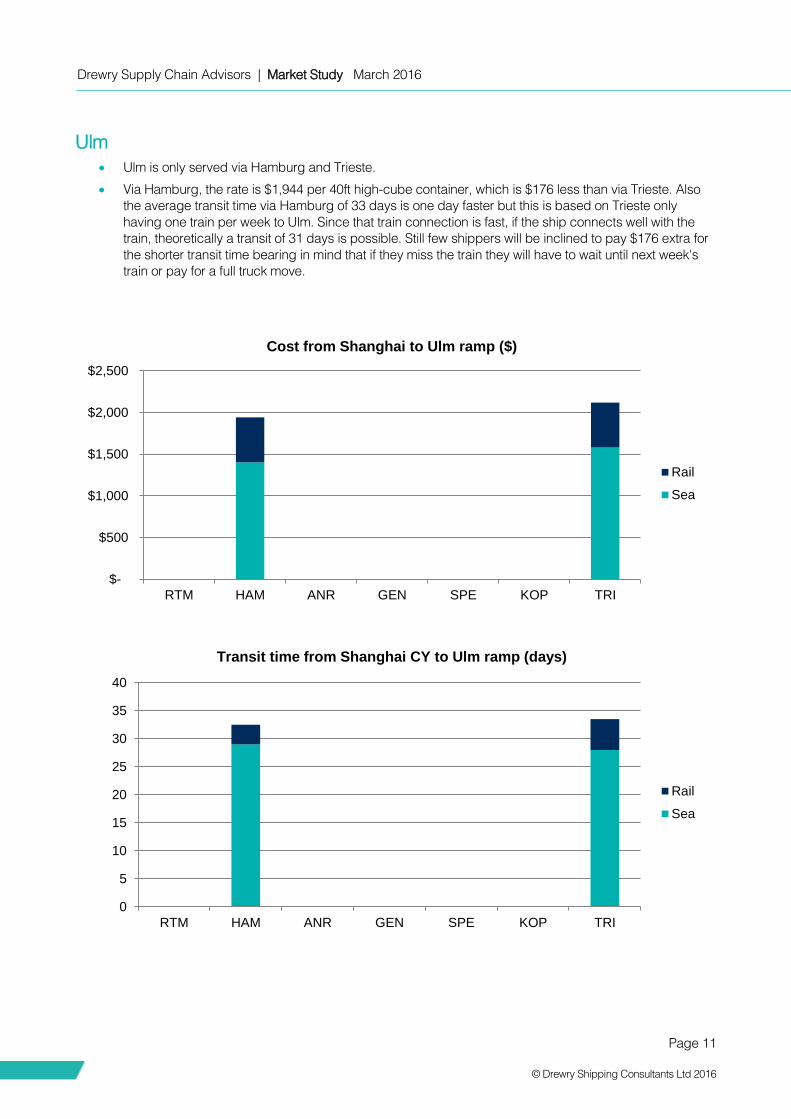

Ulm is only served via Hamburg and Trieste.

Via Hamburg, the rate is $1,944 per 40ft high-cube container, which is $176 less than via Trieste. Also

the average transit time via Hamburg of 33 days is one day faster but this is based on Trieste only

having one train per week to Ulm. Since that train connection is fast, if the ship connects well with the

train, theoretically a transit of 31 days is possible. Still few shippers will be inclined to pay $176 extra for

the shorter transit time bearing in mind that if they miss the train they will have to wait until next week's

train or pay for a full truck move.

$-

$500

$1,000

$1,500

$2,000

$2,500

RTM HAM ANR GEN SPE KOP TRI

Cost from Shanghai to Ulm ramp ($)

Rail

Sea

0

5

10

15

20

25

30

35

40

RTM HAM ANR GEN SPE KOP TRI

Transit time from Shanghai CY to Ulm ramp (days)

Rail

Sea

Drewry Supply Chain Advisors | Market Study March 2016

Page 12

© Drewry Shipping Consultants Ltd 2016

Nuremberg

The Nuremberg logistics cluster is only connected by rail with the Northern Gate ports of Hamburg and

Rotterdam. Cargo via Antwerp will use the barge service to Rotterdam to connect with the rail there.

The routing via Rotterdam is the cheapest, at $1,891 per 40ft high-cube container, while the routing via

Hamburg costs $89 more and via Antwerp $141 more.

The superfast transit on 2M gives Antwerp a transit time advantage of one day over Hamburg and two

days over Rotterdam; however, this comes at the expense of lower resilience: while Hamburg offers five

connections per week with A-B transit time, Rotterdam offers the same frequency with A-C transit time,

and from Antwerp the barge shunt makes it an A-D connection.

$-

$500

$1,000

$1,500

$2,000

$2,500

RTM HAM ANR GEN SPE KOP TRI

Cost from Shanghai to Nuremberg ramp ($)

Rail

Sea

0

5

10

15

20

25

30

35

RTM HAM ANR GEN SPE KOP TRI

Transit time from Shanghai CY to Nuremberg ramp (days)

Rail

Sea

Drewry Supply Chain Advisors | Market Study March 2016

Page 13

© Drewry Shipping Consultants Ltd 2016

Tracking relative ocean freight rates by port range Spot rates volatility reached new heights in 2015. Monthly indices for the Asia-North Europe trade, as tracked in

our Container Freight Rate Insight (CFRI), had a standard deviation of $545 per 40ft. So if you were trying to

predict the next month’s rates based on the one from the current month, you had a 30% chance that the rates

went up or down by more than $545. With such stormy rate developments, some may have missed noticing the

crumbling of a few long-held truths. One of them being that the cheapest route for Asian imports into Europe is

via Northern European ports, when comparing port-to-port rates. What we have seen is that the cheapest route

for Asian imports into Europe has shifted in favour of the Mediterranean ports.

Indices for Asia-North Europe and Asia-Med

Figure 3: Weekly spot rates on Shanghai-Rotterdam

and Shanghai-Genoa

Figure 4: Weekly spot rates on Shanghai-Rotterdam

and Shanghai-Genoa

Source: Drewry’s Container World Index

Figure 3 shows a two-year time series of weekly spot rates on Shanghai-Rotterdam and Shanghai-

Genoa as tracked in our weekly World Container Index (WCI). Rates on both trades are highly

correlated, but rates via Rotterdam (Northern Gate) have historically been lower than those in Southern

Gate, despite the longer sailing distance because of higher volumes and scale economies.

Figure 4 zooms in on the last quarter of 2015 where the Southern Gate was the cheaper option in 10 of

the 14 weeks.

Therefore, clearly the Southern Gate is closing the gap it has historically had with the Northern Gate in

terms of sea freight.

Well-informed shippers closely tracked the spot rate market and selected the cheapest routing every

week, saving 11% of their ocean-spend

Also on the land side, several South European intermodal operators are developing exciting and

competitive concepts. These efforts will be boosted when the Gotthard Base Tunnel (GBT) opens in

June. The GBT will be the world's longest traffic tunnel and will allow rail operators to improve their

efficiency by increasing the length of the trains and reducing the travel time when crossing the Alps.

Once this translates into cheaper rail rates, the area where the Southern Gate can compete will expand

further North.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Shanghai-Rotterdam Shanghai - Genoa

0

500

1000

1500

2000

Oct-15 Nov-15 Dec-15

US

$ p

er

40

ft C

on

tain

er

Shanghai - Genoa Shanghai-Rotterdam

drewry.co.uk

For further information regarding this publication, please contact us at [email protected] The primary source of market insight, analysis and advice trusted by a global audience of maritime and shipping industry stakeholders.

UK 15-17 Christopher Street London EC2A 2BS United Kingdom

India 209 Vipul Square Sushant Lok - 1 Gurgaon 122002 India

Singapore #13-02 Tower Fifteen 15 Hoe Chiang Road Singapore 089316

China Unit D01 Level 10 Shinmay Union Square Tower 2 506 Shang Cheng Road Pudong, Shanghai China, 200120

T +44 20 7538 0191 T +91 124 497 4979 T +65 6220 9890 T +86 (0) 21 5081 0508