1

CHAPTER 12Substantive

Audit Testing: Expenditure

Cycle

2

What are the What are the primaryprimary audit audit objectives with regard to objectives with regard to inventoryinventory??

- existence

3

What are the What are the primaryprimary audit audit objectives with regard to objectives with regard to inventoryinventory??

- existence- rights

ABC Electronics Co.

Sales Invoice

4

What are the What are the primaryprimary audit audit objectives with regard to objectives with regard to inventoryinventory??

- existence- rights- accuracy

5

What are the What are the primaryprimary audit audit objectives with regard to objectives with regard to inventoryinventory??

- existence- rights- accuracy- realizable value

6

What is the What is the primaryprimary audit audit procedureprocedure with regard to with regard to inventoryinventory??

Observe the client’s inventory-taking

procedures.

7

What is the What is the primaryprimary audit audit procedureprocedure with regard to with regard to inventoryinventory??

Observe the client’s inventory-taking

procedures.

required by AU 331

8

WhenWhen do client inventory- do client inventory-taking procedures occur?taking procedures occur?

If the client has aperiodic inventory system, the physical inventory count determinesthe balance in inventory accounts and will probablyoccur on the balance sheet date.

December

9

WhenWhen do client inventory- do client inventory-taking procedures occur?taking procedures occur?

If the client has aperpetual inventory system, the physical inventory count may occurany time during the accounting period.Whenever the count occurs, the auditoris required to observe.

June

10

Some clients use Some clients use statistical sampling statistical sampling in their in their

inventory methods.inventory methods.

why?

11

Some clients use Some clients use statistical sampling statistical sampling in their in their

inventory methods.inventory methods.

reduces the need to count

every inventory item (sample results can be statistically extended

to the population)

12

Some clients use Some clients use statistical sampling statistical sampling in their in their

inventory methods.inventory methods.

What are the auditor’s

concerns?

13

Some clients use Some clients use statistical sampling statistical sampling in their in their

inventory methods.inventory methods.

The auditor is concerned thatthe statistical inventory plan:- has statistical validity- is properly applied- achieves reasonable results

14

Should the auditor test Should the auditor test beginningbeginning inventory balances? inventory balances?

how?

When the auditing firm has not auditedbeginning balances, the auditors mustsatisfy themselves as to the appropri-ateness of beginning balances, if theyare satisfied as to the current balances.

15

how?analytical

procedures

review of priorinventory

count records

tests of inventorytransactions and

documents

When the auditing firm has not auditedbeginning balances, the auditors mustsatisfy themselves as to the appropri-ateness of beginning balances, if theyare satisfied as to the current balances.

16

How should the auditor test How should the auditor test inventory held at a public inventory held at a public

warehouse?warehouse?

client head-quarters &auditor’s

officepublicwarehouse

17

How should the auditor test inventory How should the auditor test inventory held at a public warehouse?held at a public warehouse?

- direct written confirmation with the public warehouse

Confirmation, alone, will not be sufficient if inventory quantities

held at the warehouse are significant.

18

How should the auditor test inventory How should the auditor test inventory held at a public warehouse?held at a public warehouse?

- direct written confirmation with the public warehouse- if inventory held at the public ware- house is significant: ~ review client’s procedures for investigating and evaluating the warehouse

19

How should the auditor test inventory How should the auditor test inventory held at a public warehouse?held at a public warehouse?

- direct written confirmation with the public warehouse- if inventory held at the public ware- house is significant: ~ review client’s procedures for investigating and evaluating the warehouse ~ obtain report from warehouse’s auditor regarding internal controls

20

How should the auditor test inventory How should the auditor test inventory held at a public warehouse?held at a public warehouse?

- direct written confirmation with the public warehouse- if inventory held at the public ware- house is significant: ~ review client’s procedures for investigating and evaluating the warehouse ~ obtain report from warehouse’s auditor regarding internal controls ~ observe warehouse’s physical counts (if practical)

21

Some large merchandisers use Some large merchandisers use outside outside inventory-taking companiesinventory-taking companies that that specialize in counting inventory.specialize in counting inventory.

What are theauditing

implications?

22

Some large merchandisers use Some large merchandisers use outside outside inventory-taking companiesinventory-taking companies that that specialize in counting inventory.specialize in counting inventory.

- since the inventory-taking company is a third party, their work has greater reliability than the client’s

23

Some large merchandisers use Some large merchandisers use outside outside inventory-taking companiesinventory-taking companies that that specialize in counting inventory.specialize in counting inventory.

- since the inventory-taking company is a third party, their work has greater reliability than the client’s- the auditor still should observe the physical inventory count

24

Some large merchandisers use Some large merchandisers use outside outside inventory-taking companiesinventory-taking companies that that specialize in counting inventory.specialize in counting inventory.

- since the inventory-taking company is a third party, their work has greater reliability than the client’s- the auditor still should observe the physical inventory count- the auditor must test the effectiveness of the inventory-taking company’s procedures

25

inventory audit proceduresinventory audit procedures

perform analytical

proceduresto test inventoryreasonableness

26

inventory audit proceduresinventory audit proceduresregarding the client physical inventory count:

Review the client’s plan for counting the physical inventory. Attendclient count planningmeetings.

27

inventory audit proceduresinventory audit procedures

Observe the physical inventory count.Determine whether client counting methodsare effective.

regarding the client physical inventory count:

28

inventory audit proceduresinventory audit procedures

Observe the quality and condition of theinventory. Consider obsolescence.

regarding the client physical inventory count:

29

inventory audit proceduresinventory audit procedures

On a random basis:- select a sample of inventory items from the warehouse floor, count them, trace the quantity to client count records

regarding the client physical inventory count:

30

inventory audit proceduresinventory audit procedures

On a random basis:- select a sample of inventory items from the client count records, find them in the warehouse, count them

regarding the client physical inventory count:

31

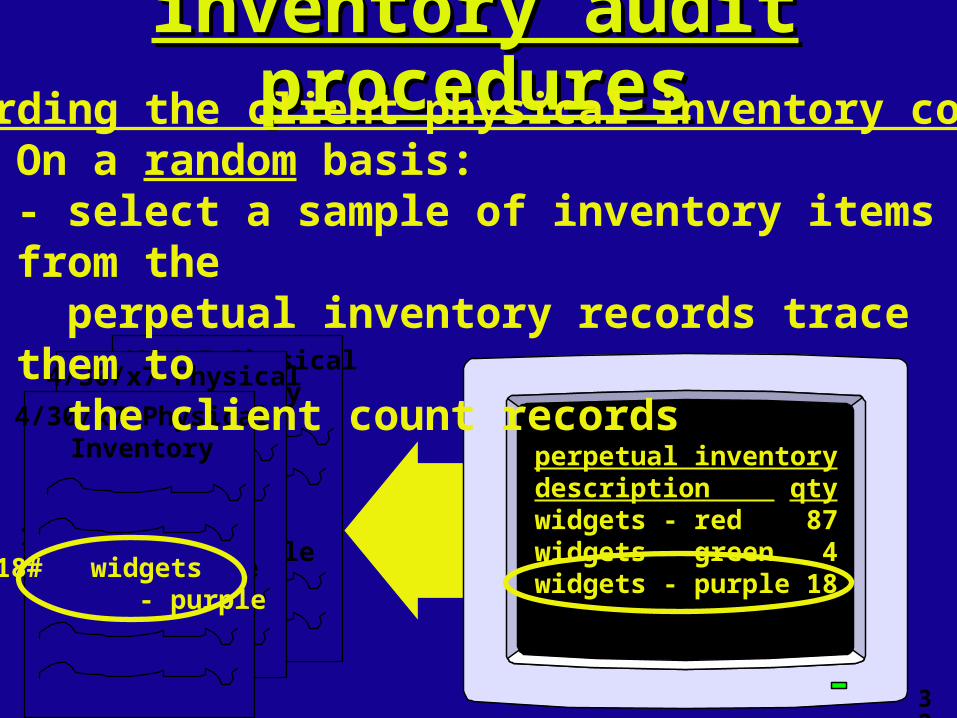

inventory audit proceduresinventory audit procedures

On a random basis:- select a sample of inventory items from the client count records, trace them to the perpetual inventory records

4/30/x7 PhysicalInventory

18# widgets - purple

4/30/x7 PhysicalInventory

18# widgets - purple

4/30/x7 PhysicalInventory

18# widgets - purple

perpetual inventorydescription qtywidgets - red 87widgets - green 4widgets - purple 18

regarding the client physical inventory count:

32

inventory audit proceduresinventory audit procedures

4/30/x7 PhysicalInventory

18# widgets - purple

4/30/x7 PhysicalInventory

18# widgets - purple

4/30/x7 PhysicalInventory

18# widgets - purple

perpetual inventorydescription qtywidgets - red 87widgets - green 4widgets - purple 18

regarding the client physical inventory count:On a random basis:- select a sample of inventory items from the perpetual inventory records trace them to the client count records

33

inventory audit proceduresinventory audit procedures

determine whether any inventory has been pledged as

collateral (disclosure)

34

inventory audit proceduresinventory audit proceduresInquire of client management

regarding the existence of consigned inventories.

consignments “R” us

ACE

35

inventory audit proceduresinventory audit procedures

Inquire of client management regarding the existence of

consigned inventories:- if a consignee holds a portion of the client’s inventory, confirm that amount with the consignee

36

inventory audit proceduresinventory audit proceduresInquire of client management

regarding the existence of consigned inventories:

- if a consignee holds a portion of the client’s inventory, confirm that amount with the consignee- if a client consignee holds a portion of a consignor’s inventory, confirm that amount with the consignor

37

inventory audit proceduresinventory audit procedures

Consider the effects of sales and purchases cutoff tests on

inventories.

38

inventory audit proceduresinventory audit proceduresTest the client’s

application of their inventory valuation method (FIFO, LIFO)

and the lower-of-cost-or-market rule.

39

inventory audit proceduresinventory audit procedures

For manufactured inventories:

test the cost accumulation process as it affects valuation of ending

inventories and COGS

40

Auditing Plant AssetsAuditing Plant Assets

- perform analytical procedures- verify current-year acquisitions- verify current-year disposals- verify ending asset balances- verify depreciation expense- verify ending accumulated de- preciation balances

41

- perform analytical procedures examples: depreciation expense / equipment manufacturing costs / production

Auditing Plant AssetsAuditing Plant Assets

42

Auditing Plant AssetsAuditing Plant Assets- verify current-year acquisitions

~Select a sample of entries in the acqui- sitions journal and trace to fixed asset master file.~Select a sample of entries in the acqui- sitions journal and trace to vendor in- voices and receiving reports.~Select a sample of entries in the acqui- sitions journal and physically examine the related assets.

43

Auditing Plant AssetsAuditing Plant Assets- verify current-year disposals ~ analyze gains on the disposal of as- sets and miscellaneous income for receipts from asset disposals ~ review plant modifications and changes in product line, taxes, or in- surance coverage for indications of deletions of equipment ~ make inquiries of management and production personnel about disposals

44

Auditing Plant AssetsAuditing Plant Assets

- verify ending asset balances

EXAMPLE PROCEDURE: Trace totalsfrom fixed asset master file to the general ledger.

45

Auditing Plant AssetsAuditing Plant Assets

- verify depreciation expense

- recalculate depreciation expense- determine whether the client’s depreciation policy is consistent

46

Auditing Plant AssetsAuditing Plant AssetsWhat audit procedures addressthe auditor’s concern regarding accu-racy of accumulated depreciation?

Trace totals from fixed assetmaster file to the generalledger.

Recalculateaccumulateddepreciation