donor information resource centre helping to improve donor effectiveness in microfinance ...

TRANSCRIPT

DONOR INFORMATION RESOURCE CENTRE

Helping to Improve Donor Effectiveness in Microfinance

www.microfinancegateway.org

Microinsurance: Microinsurance: A Risk Management StrategyA Risk Management Strategy

PRESENTATION INSTRUCTIONSPRESENTATION INSTRUCTIONS

• This is a DIRECT presentation designed for microfinance donors. These slides may be used or changed without permission. Attribution to CGAP/DIRECT is appreciated.

• Slides are accompanied by notes.• To view notes, select from the PowerPoint menu: View/

Notes Page. Scroll to advance to next page.• To print notes, select File/ Print/ Print what: Notes Pages. • To print handouts of just slides (no notes), select File/

Print/ Print what: Handouts. Then enter the number of slides to print per page.

• For optimal printing on a black-and-white printer, select from the menu: File/ Print/ Pure Black and White.

April 22, 2004

OverviewOverview

What risks do poor people face and how do they protect themselves?

What is microinsurance?

What are the difficulties in providing insurance to poor people?

What are some microinsurance delivery models?

What are some dos and don’ts for donors?

What Risks Do Poor People Face?What Risks Do Poor People Face?

Key Risks

Death

Illness or injury

Loss of property (theft, fire)

Natural disaster (earthquake, drought) “Life is one long risk”

Microfinance client in the Philippines “Life is one long risk”

Microfinance client in the Philippines

How Do Poor PeopleHow Do Poor PeopleProtect Themselves from Risk?Protect Themselves from Risk?

PreparationPreparation

CopingCoping

Prevention and AvoidancePrevention and Avoidance

• Careful sanitation• Identifying business opportunities• Careful sanitation• Identifying business opportunities

• Saving• Accumulating assets (i.e., livestock)• Buying insurance• Educating children

• Saving• Accumulating assets (i.e., livestock)• Buying insurance• Educating children

• Taking emergency loans • Depleting savings• Selling productive assets• Defaulting on loans• Reducing spending

• Taking emergency loans • Depleting savings• Selling productive assets• Defaulting on loans• Reducing spending

Alternative Coping

Strategies

Alternative Coping

Strategies

Social Conditions

Social Conditions

Education, Biases,

Risk Tolerance

Education, Biases,

Risk Tolerance

Cash FlowCash Flow

Planning PropensityPlanning

Propensity

Understanding the Demand for Risk-Managing Understanding the Demand for Risk-Managing Financial ServicesFinancial Services

The demand forThe demand for

Liquid savings Emergency loansMicroinsurance

depends on

The demand forThe demand for

Liquid savings Emergency loansMicroinsurance

depends on

Poverty Level

Poverty Level

Type of Risk

Type of Risk

Very Large

Small

Certain Highly Uncertain

Degree of Uncertainty

Relative Loss / Cost

Life Cycle Events

Death

Disability

He

alth

Pro

perty

Mass, Co-

variant

Different Financial Services for Different RisksDifferent Financial Services for Different Risks

Source: Warren Brown and Craig F. Churchill, Insurance Provision in Low-Income Communities, Part I.Source: Warren Brown and Craig F. Churchill, Insurance Provision in Low-Income Communities, Part I.

Flexible Savings and

Credit

Flexible Savings and

Credit

InsuranceInsurance

Flexible Savings

Partial protection

Flexible Savings

Partial protection

What Is Microinsurance?What Is Microinsurance?

Protection of low-income people against specific perils in exchange for regular monetary payments (premiums) proportionate to the likelihood and cost of the risk involved.

Protection of low-income people against specific perils in exchange for regular monetary payments (premiums) proportionate to the likelihood and cost of the risk involved.

To serve poor people, microinsurance must be:

Responsive to their priority needs for risk protection

Easy to understand

Affordable

To serve poor people, microinsurance must be:

Responsive to their priority needs for risk protection

Easy to understand

Affordable

ONE

STRATEGY

ONE

STRATEGY

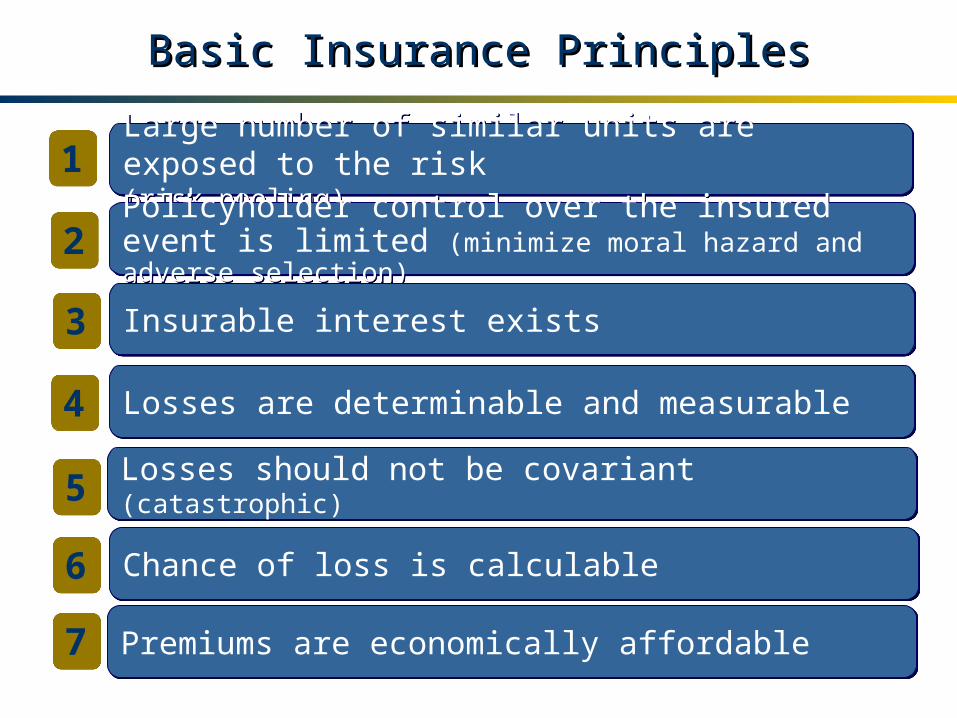

Basic Insurance PrinciplesBasic Insurance Principles

Large number of similar units are exposed to the risk(risk pooling)Large number of similar units are exposed to the risk(risk pooling)

Policyholder control over the insured event is limited (minimize moral hazard and adverse selection)Policyholder control over the insured event is limited (minimize moral hazard and adverse selection)

Insurable interest existsInsurable interest exists

Losses are determinable and measurableLosses are determinable and measurable

Losses should not be covariant (catastrophic)Losses should not be covariant (catastrophic)

Chance of loss is calculableChance of loss is calculable

Premiums are economically affordablePremiums are economically affordable

11

22

33

44

55

66

77

What Are Some of the Difficulties in Providing What Are Some of the Difficulties in Providing Insurance to Poor People?Insurance to Poor People?

Technical Specialization

Technical Specialization

Requires specialized actuarial capacity, which is complicated by the lack of reliable data characteristic of low-income, informal markets

Most poor people do not understand insurance or may be biased against it

Requires a distribution system that can handle small financial transactions efficiently in convenient locations, and engender trust

Marketing and Sales

Marketing and Sales

Distribution Channels

Distribution Channels

Relative Complexity of Insurance ProductsRelative Complexity of Insurance Products

Crop insurance

Health and disability insurance

Annuities and endowment

(retirement provision)

Property insurance

Term life insurance(payment to beneficiaries on death)

HIGHLY COMPLEXHIGHLY COMPLEX

SIMPLERSIMPLER

Degree of Risk in Providing InsuranceDegree of Risk in Providing Insurance

Moral HazardMoral Hazard

FraudFraud

Adverse SelectionAdverse Selection

OverusageOverusage

Limited RiskLimited Risk

Moderate RiskModerate Risk

Substantial RiskSubstantial Risk

Health Insurance

Property Insurance

Life Insurance

The The DismalDismal History of Crop Insurance History of Crop Insurance

Unspecific Coverage By guaranteeing a minimum crop yield, programs insured against all possible causes of poor crop yield, an endless list of risks

Covariant Losses Many programs were bankrupted when a natural calamity affected most insured members at once

Moral Hazard Farmers were less likely to follow sound husbandry practices because all severe yield losses were protected, leading to increase in claims

Balance of Risks Coverage was focused in specific regions and provided only for poor farmers, covering only the highest risks

Trying to provide insurance in uninsurable conditions:Trying to provide insurance in uninsurable conditions:

Activities Involved in Offering InsuranceActivities Involved in Offering Insurance

Product Sales

Marketing, education,

signature of

policies

Product Sales

Marketing, education,

signature of

policies Product

Manufacturing

Design issues such as pricing,

claims procedures, level of coverage

Product Manufacturing

Design issues such as pricing,

claims procedures, level of coverage Product

Servicing

Premium collection, payment of

claims

Product Servicing

Premium collection, payment of

claims

Policy HoldersPolicy

Holders

Some Microfinance Delivery ModelsSome Microfinance Delivery Models

Partnerships between MFIs (or other intermediaries) and insurers

Full service provision where regulated insurers provide specific products to the low-income market

Health care service providers offer a health care financing package and absorb the insurance risk

MFI-based insurance where MFIs take on the risk offering insurance to their clients

Community-based programs where communities pool funds and manage a relationship with a health care provider

Examples of Microinsurance DeliveryExamples of Microinsurance Delivery

Partner-Agent Model• Insurers utilize MFIs’ delivery

mechanism to provide sales and basic services to clients

• There is no risk and limited administrative burden for MFIs

• Example: FINCA Uganda partners with American International Group

Community-Based Model• The policyholders own and manage

the insurance program, and negotiate with external health care providers

• Example: UMASIDA in Tanzania

Provider Model• The service provider and the

insurer are the same, i.e., hospitals or doctors offer policies to individuals or groups

• Example: Gonoshatsasthya Kendra in Bangladesh

Full-Service Model• The provider is responsible for all

aspects of product manufacturing, sales, servicing, and claims assessment

• The insurers are responsible for all insurance-related costs and losses and they retain all profits

• Example: SEWA in India

Example: AIG and FINCA UgandaExample: AIG and FINCA Uganda

Product Sales

Product Sales

PolicyHolders

PolicyHolders

Product Manufacturing

Product Manufacturing

Product ServicingProduct

Servicing

PartnerPartner AgentAgent

FINCA UgandaFINCA

UgandaAIGAIG

Potential Market• Are clients interested in

insurance protection? • Is this the most effective

risk management solution?

Linkage identified?

Pre-requisites for Donor Intervention in MicroinsurancePre-requisites for Donor Intervention in Microinsurance

Consider alternativ

e risk- managing financial services

Consider alternativ

e risk- managing financial services

Broker partnership,

monitor performance

YESYES

NO

Donor Skillsand Knowledge

• Does donor have experience develop-ing markets for low income people?

• Does donor have basic insurance technical expertise?

• Does donor have access to local market knowledge?

NO YESYES

YESYESNO

Preliminary Guidance for Donors Preliminary Guidance for Donors

Consider client demand

Invest in technical expertise

Monitor performance

Move cautiously and facilitate linkages

11

22

33

44

Work with strong institutions

55

1. Consider Client Demand1. Consider Client Demand

DO Consider client demand to

understand what risk-managing financial service is most appropriate

Invest in educating poor people on the benefits of insurance

DO NOT

Push institutions to offer microinsurance

The demand for risk protection should come from clients, not donors

2. Move Cautiously and Facilitate Linkages2. Move Cautiously and Facilitate Linkages

DO

Encourage commercial insurers to serve the

poor by brokering relationships with MFIs

DO NOT

Try to influence government policies before there is more

experience with microinsurance

Coordinate microinsurance efforts with other donors, insurers, governments

3. Work with Strong Institutions3. Work with Strong Institutions

DO

Take a patient approach, but define a clear, time-bound exit

strategy

DO NOT

Fund new microinsurance

providers without sufficient technical

capacity

Work with strong institutions and conduct a careful analysis of their capacity to manage microinsurance products

4. Invest in Technical Expertise4. Invest in Technical Expertise

DO

Provide access to technical assistance for

specific technical problems

DO NOT

Provide grant funding to cover claims costs

Be careful about supporting unregulated insurance schemes that lack expertise, access to reinsurance, or consumer protection oversight

For MFIs Volumes of policyholders (% of

women)

Premium and claim values

Loss ratios

Renewal rates

Average time for claim settlement, premium rate charged to clients

Administrative costs ratio

For Insurers Annual reviews of premiums

written

Loss and expense ratios

Claims reserves ratio

Other reserves

Investment returns

Premium rate charged to the MFI

Net income, capital, and surplus

Key Microinsurance Performance IndicatorsKey Microinsurance Performance Indicators

5. Monitor Performance of Microinsurance 5. Monitor Performance of Microinsurance PartnersPartners

SummarySummary

Microinsurance is one of many financial services that helps manage risk

To serve poor people, microinsurance must respond to their priority needs for risk protection, be easy to understand, and be affordable

Insurance is a complex matter requiring technical expertise that most MFIs and donors do not possess

At present, the ability of donors to facilitate linkages and share knowledge on microinsurance is more important than providing funds for specific programs

Where to Get More InformationWhere to Get More Information

Contact: Nataša Goronja1818 H Street, NW Washington, DC 20433

Tel: 202-473-9594 Fax: 202-522-3744E-mail: [email protected]

Web: www.cgap.org

• CGAP Working Group on Microinsurance, “Donor Guidelines for Funding Microinsurance,” (paper prepared for CGAP, Washington, DC, October 2003).

• Microinsurance: Improving Risk Management for the Poor, Nos. 1 and 2 (Luxembourg: ADA, August and November 2003).

• W. Brown, C. Green, and G. Lindquist, A Cautionary Note for Microfinance Institutions and Donors Considering Developing Microinsurance Products (Bethesda, Md., USA: DAI, 2000).

• C. Churchill, D. Liber, M.J. McCord, and J. Roth, Making Microinsurance Work for Microfinance Institutions: A Technical Guide to Developing and Delivering Microinsurance (Geneva: ILO, 2003).

• W. Brown and C. Churchill, Insurance Provision to Low-Income Households: Part I (Toronto:Calmeadow, 1999), and Part 2 (Bethesda, Md., USA: DAI, 2000).