doing business with india

TRANSCRIPT

Doing Business with India

1-846730-22-8_FM_i_12/29/2006

1-846730-22-8_FM_ii_12/29/2006

GLOBAL MARKET BRIEFINGS

Doing Business withIndia

Second Edition

Consultant Editor:Roderick Millar

Forewords from:Kamal Nath, Minister for Commerce and Industry

andR Seshasayee, President, Confederation of Indian Industry

GMB

1-846730-22-8_FM_iii_12/29/2006

Publishers’ note

Every possible effort has been made to ensure that the information contained in this pub-lication is accurate at the time of going to press and neither the publishers nor any of theauthors, editors, contributors or sponsors can accept responsibility for any errors or omis-sions, however caused. No responsibility for loss or damage occasioned to any person acting,or refraining from action, as a result of the material in this publication can be accepted bythe editors, authors, the publisher or any of the contributors or sponsors.

This second edition first published 2007 by GMB Publishing Ltd.

Users and readers of this publication may copy or download portions of the material hereinfor personal use, and may include portions of this material in internal reports and/o

rreports to customers, and on an occasional and infrequent basis individual articles fromthe material, provided that such articles (or portions of articles) are attributed to this pub-lication by name, the individual contributor of the portion used and GMB Publishing Ltd.

Users and readers of this publication shall not reproduce, distribute, display, sell, publish,broadcast, repurpose, or circulate the material to any third party, or create new collectiveworks for resale or for redistribution to servers or lists, or reuse any copyrighted componentof this work in other works, without the prior written permission of GMB Publishing Ltd.

GMB Publishing Ltd.120 Pentonville Road 525 South 4th Street, #241London N1 9JN Philadelphia, PA 19147United Kingdom United States of Americawww.globalmarketbriefings.com

© GMB Publishing Ltd. and contributors

Hardcopy ISBN 1-84673-022-8 E-book ISBN 1-84673-023-6

British Library Cataloguing in Publication Data

A CIP record for this book is available from the British Library

Library of Congress Cataloguing-in Publication Data

Typeset by Digital Publishing SolutionsPrinted and bound in Great Britain

ContentsForewordShri Kamal Nath, Minister for Commerce and Industry

ForewordMr R Seshasayee, the President of the Confederation of Indian Industry

About the Contributors

vii

ix

xiii

Acronyms

Map

Part One – Overviews

1.1 India at a Glance1.2 Political Background and Overview1.3 An Economic Overview of India

Part Two – Mechanics of Business Engagement

2.1 Labour, Skills and Training2.2 Real Estate2.3 An Opportunity to SE(i)Z(e)2.4 Inward Investment2.5 ITES-BPO2.6 Distribution2.7 Partner Selection2.8 Analyzing the Indian Market

Part Three – Finance, Tax and Accounting

3.1 Audit Requirements3.2 Accounting Requirements and Tax Issues

Part Four – Legal Issues

4.1 Available Legal Structures4.2 Investment Facilities for NRIs/PIOs and Other Foreign Investors4.3 Mergers and Acquisitions4.4 Employment Issues

xxiii

xxv

37

17

2733374147576371

8185

109115125133

1-846730-22-8_FM_v_12/29/2006

Contentsvi

4.5 Export and Import Issues4.6 Intellectual Property4.7 Company Dissolution and Liquidation4.8 Dispute Resolution4.9 Contract Issues, Consumer Protection and Property Issues4.10 Legal Impediments

Part Five – Business Culture

5.1 People5.2 Language and Communication5.3 Management and Leadership Style5.4 Business Interaction

Part Six – Industry Sector Reports

6.1 Trends in the Indian Pharmaceutical Market6.2 The India Opportunity in the Energy Sector

Part Seven – Appendices

1. Sector Specific Guidelines for FDI

2. Clearances and Approvals Information

3. Addresses for Filing Applications

4. Inward Investment from Japan Liaison Office

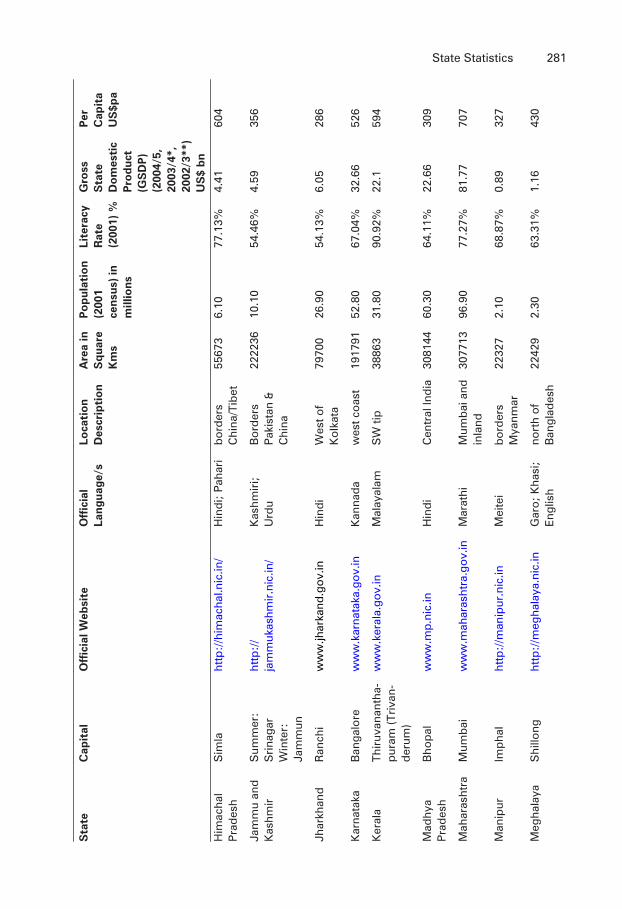

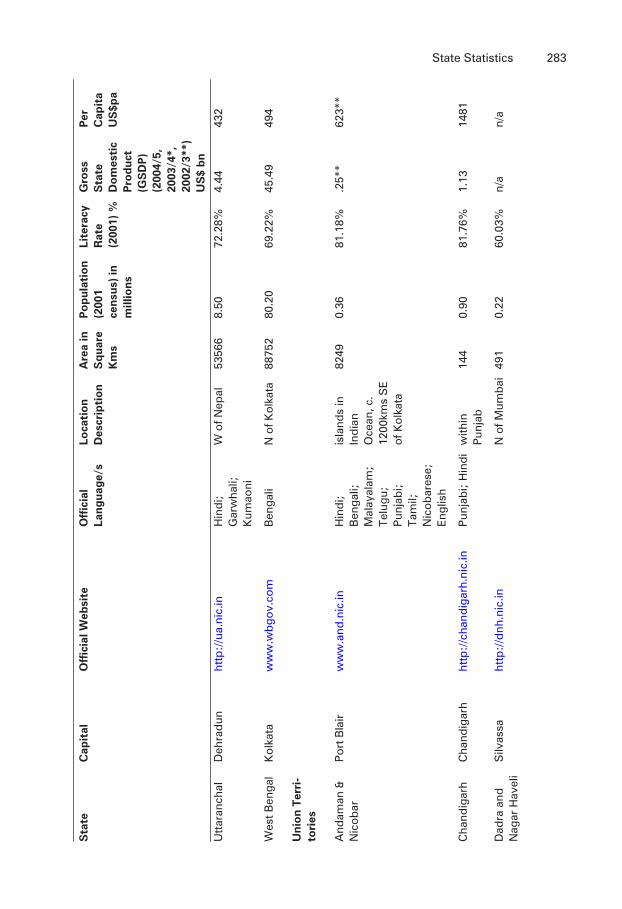

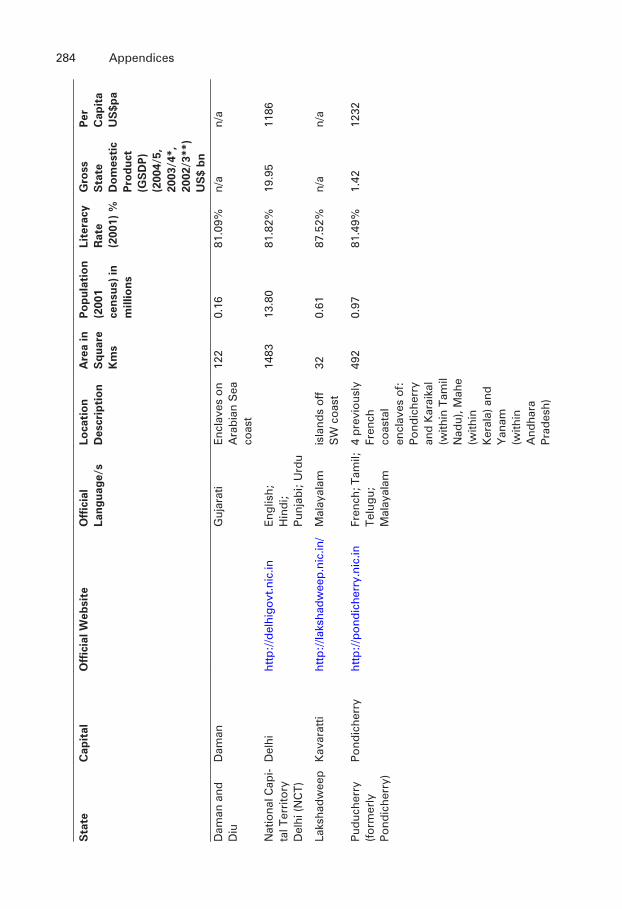

5. State Statistics

6. Joint Venture Service Providers in India

7. Indian Numbering System

8. Useful Websites

139145153161167175

185191197203

211231

267

273

275

277

279

287

291

293

1-846730-22-8_FM_vi_12/29/2006

ForewordIndia’s economy is expected to grow at over eight percent in 2007. This is aremarkable statistic for any economy, it is an extraordinary one for an econ-omy the size of India’s. The fact that it will be the fourth year in a row withover eight percent GDP growth means that it is little surprise that India hasbecome such an attractive and exciting place to do business.

The most recent ATKearney FDI Confidence Index puts India’s FDI attrac-tiveness at an all-time high above all other countries save China, and notes“India appears to be on the cusp of an FDI take-off”. With the continuedemphasis of the Indian Government on moving the Indian economy on frombeing a major provider of IT and service sector related exports to also being adestination for manufacturing investment dollars the country is truly now“open for business”.

As such this new edition of Doing Business with India is well timed. Indiais a complex and sophisticated country and the prospect of entering such anenormous market can be daunting. This book is a welcome guide to gettingstarted with that process, giving the prospective business person a detailedintroduction to the structures and processes that exist and indicating some ofthe best practices in establishing a business presence in India.

The Indian government welcomes the increasing involvement of foreignbusinesses in the growth of the Indian economy as Indian businesses, in turn,are increasingly being seen as major players in the international economy. Ihope that this guide will encourage even more businesses to come to India anddiscover the wealth of opportunities that awaits them here.

Mr Kamal NathMinister for Commerce and Industry

1-846730-22-8_FM_vii_12/29/2006

1-846730-22-8_FM_viii_12/29/2006

ForewordVarious studies done across the globe and different views from economistshave been of the opinion that India along with China will rule the world inthe 21st century. By 2025 the Indian economy is projected to be about 60 percent the size of the US economy. The transformation into a tri-polar economywill be complete by 2035, with the Indian economy only a little smaller thanthe US economy but larger than that of Western Europe. By 2035, India islikely to be a larger growth driver than the six largest countries in the EU,though its impact will be a little over half that of the US.

Since independence, the Indian economy has flourished improving its paceof development. India has set up joint ventures in a number of countries andundertaken successfully several projects and contracts independently of andin co-operation with developed economies. Not only that even the infrastruc-ture within the cities of India have had enormous upgradation.

The Indian Economy is now in a state of rapid growth and developmenthaving a strong industrial backbone. It is now regarded as a major player inthe global economic horizon, driven by a commitment to achieve a world-classstandard in future years to come.

Industrial growth is driven by robust performances from manufacturingand construction sectors. Within industry, while manufacturing growth hasaccelerated steadily from 7.1 per cent in 2003-04 to 9.4 per cent in 2005-06,construction growth has been in double digits in each of the last three years.Substantive commercial bank credit flows to the housing and real estate andretail sectors continue to provide support to the boom in construction andconsumer durables. Looking at all this one can concur that India is the perfectrecipe for growth.

Even if we look at the food sector, India is the world’s second largest pro-ducer of food next to China, and has the potential of being the biggest in theworld. Food processing is a key industrial sector for India, it accounts for agross output of more than US$ 69.4 billion, out of which value-added foodproducts comprise US$ 22.2 billion. Size of the semi-processed and ready toeat packaged food industry is over US$ 1 billion, and it is growing at over20 per cent a year. The total processed food production in India is likely todouble in the next ten years.

In the year 2005-2006 itself, The GDP grew by 7.4 per cent in the firstquarter and 6.6 per cent in the second quarter of the current year, comparedwith 5.3 per cent and 8.6 per cent in the corresponding quarters of the previ-ous year. The Economic Survey 2005-06 estimates that the GDP will grow at8.1 per cent. Growth of Gross Domestic Product (GDP) at constant prices in

1-846730-22-8_FM_ix_12/29/2006

excess of 8.0 per cent has been achieved by the economy in only five years ofrecorded history, and two out of these five are in the last three years.

In its initiative to consolidate this growth CII has as its theme for the year(2006-07) ‘Competitiveness for Sustainable and Inclusive Growth’. In conclu-sion, it may be appropriate to mention that the growth of Industry andEconomy are necessary prerequisites for sustained development to comeabout, but for it to be sufficient, we need to make this growth sustainable andinclusive.

Mr R SeshasayeePresident, Confederation of Indian Industry

Forewordx

1-846730-22-8_FM_x_12/29/2006

1-846730-22-8_FM_xi_12/29/2006

1-846730-22-8_FM_xii_12/29/2006

About the Contributors

CII Institute of Logistics. The Confederation of Indian Industry has estab-lished a specialized Institute of Logistics - to be built as a centre of excellencein logistics and supply chain management. The principal objectives of the CIIInstitute of Logistics are to enhance the competitiveness of the Indian Indus-try and all the key sectors of the economy, which impacts India’s growththrough integrated initiatives in supply chain management and logisticsdomain area; and meet the latent need of the industry for specialized servicesin Logistics and Supply Chain Management, ranging from education toresearch to consultancy, information services etc. Ramya Kannan is a seniorexecutive within the CII.

Mr Vivek Dahiya is an associate director of DTZ India, with over sevenyears’ experience in real estate. He is a town planner and an MBNA (finance).DTZ is one of the world’s leading property advisory groups with a strong pres-ence in Europe, the Middle East and Africa, the Asia-Pacific region and is inpartnership with the Staubach Company in the Americas.

Roderick Millar has an MBA from the University of Houston, USA and anMA in Economic and Social History from St Andrews University, Scotland.He has written several financial and business books and has been consultanteditor for eight GMB titles. He also is managing editor of IEDP.info, a businessthat monitors the executive education and management development indus-try. In the 1990’s he created and ran a new concept food retail business inLondon. He is a fellow of the Royal Society for the Arts Manufactures andCommerce and the SMWS. He now lives in Spain and Scotland.

C Jayanthi. Jayanthi has been working as a print journalist for over 17 yearsin leading English-language dailies in India and also with Gulf News, Dubai.He launched the Education Times supplement for the leading English dailyin India, The Times of India, in 1998 and was its editor, until 2005. Since thenhe has worked with The Financial Express as deputy features editor, corporatenews features. He has written a couple of novels, English JournalisticQuiche, and A Reporter’s Journey, published by the Writers Workshop, India.

KPMG India. KPMG is the global network of professional services firms ofKPMG International. KPMG member firms provide audit, tax and advisoryservices through industry focussed, talented professionals who deliver valuefor the benefit of their clients and communities.

1-846730-22-8_FM_xiii_12/29/2006

The member firms of KPMG International in India were established inSeptember 1993. As members of the cohesive business unit that serves theMiddle East and South Asia (KPMG’s MESA business unit), they respond toa client service environment by leveraging the resources of a globally alignedorganisation and providing detailed knowledge of local laws, regulations,markets and competition.

KPMG has offices in India in Mumbai, Delhi, Bangalore, Chennai, Hyderabad,Kolkata and Pune and services over 2,000 international and national clients.The firms in India have access to more than 1500 Indian and expatriate pro-fessionals, many of whom are internationally trained.

Dr Amit Kapoor is a Ph.D. in Industrial Economics and Business Strategy.He has lead several well-respected consultancy projects with the Governmentof India, Bharti Televentures, Spice Telecom and NAFED amongst others. Heis an affiliate faculty of the Institute of Strategy and Competitiveness,Harvard Business School. He also jointly offers the course with ProfessorMichael Porter at Management Development Institute, India. Amit is also theChairman of Institute for Competitiveness in India. Under this initiative heis looking at completing the India Competitiveness Report by December 2006.He is also a member of the Sub Committee on Manufacturing Competitivenessof CII.

Dr. A. Sahay, Professor of Strategic Management, a hard core business exec-utive turned academician has been successful in both the corporate andacademic world. He was Chairman and Managing Director of Scooters IndiaLimited, a company which had been declared a “mortuary case” until histurnaround of it. In recognition of this, he was made the founder President ofthe Strategic Management Forum of India. He has been invited to serve onmany Corporate Boards as well as those of the technical and managementinstitutions. He represents Govt. of India on task forces in companies likeNuclear Power Corporation Of India, Power Grid Corporation of India,National Thermal Power Corporation and National Hydro Power Corporation.A mechanical engineer by training he also studied management at Univer-sity of Madras and the Advanced Management Course at Henley College ofManagement (U.K). He is ferocious reader and writer and presently con-tributes in the fields of Business Strategy, Innovation & Technology andEntrepreneurship.

Rajdeep Sahrawat is a Vice President and part of the leadership team atNASSCOM and he is responsible for accelerating the growth of the domesticIT market and increasing innovation & R&D within the IT industry. Hestarted his career in 1990 with Tata Consultancy Services (TCS) and workedwith TCS for 15 years in various roles. Rajdeep has a Masters degree in Busi-ness Administration (Finance) from the Faculty of Management Studies,University of Delhi (1990).

About the Contributorsxiv

1-846730-22-8_FM_xiv_12/29/2006

Purvi Sheth, Vice President, Shilputsi Consultants, Inda and USA. Purvihas a first class BA from St Xavier’s College, Bombay University and hascompleted the Leadership & Strategy Program at Wharton Business School.In addition to her work at Shilputsi she is an advisor to the EntrepreneurshipCells at the Indian Institute of Technology, Mumbai and the Jamnalal BajInstitute of Management, Mumbai. She has been a member of the jury panelto judge “India’s Under 40 Hot Executives” for three years.

Shilputsi Consultants is a leading Indian consulting firm specialising inStrategic Human resource Development solutions. Shilputsi provides Strate-gic HR advisory, executive development and search and selection services.

Shilputsi has a global presence and reach with a wide range of multinationaland Indian clients. They work in a variety of industries to offer valuable guid-ance fro strategic business, HR and leadership issues.

Karthik Ramamurthy heads the business consulting operations of Synovatein Mumbai and Amit Naikare is a Manager in the same office. SynovateBusiness Consulting is the market strategy consulting arm of Synovate, aleading market research firm. Synovate India is headquartered in Mumbaiwith a pan-India presence. Synovate is a group company of global media com-munications specialist Aegis Group plc.

Titus & Co (10 biogs - to have a whole page for themselves)

Diljeet Titus is Managing Partner of law firm Titus & Co. He holds aBA from St. Stephens’ College, University of Delhi and an LLB from theUniversity of Jabalpur, Madhya Pradesh. He is member of the SupremeCourt Bar Association and the Bar Council of Delhi. His main practice areasinclude project finance, mergers and acquisitions, capital markets and debtrestructuring.

Suhail Dutt is Senior Member with law firm Titus & Co. and heads the Dis-pute Resolution Group. He holds a BA from St. Stephens’ College, Universityof Delhi and an LLB from the University of Delhi. He is member ofthe Supreme Court Bar Association and the Bar Council of Delhi. His mainpractice areas include civil and criminal litigation and alternate disputeresolution.

Rai S. Mittal is Senior Member with law firm Titus & Co. He holds a B.Comand an LLB from the University of Meerut, Uttar Pradesh. He is a memberof the Bar Council of Uttar Pradesh. His main practice areas include corporateand commercial transactions, mergers and acquisitions, joint ventures,inbound investments, capital markets, intellectual property, litigation andarbitration.

Clinton Johnston is a Of Counsel with law firm Titus & Co. He holds J.D.,Harvard Law School and M.A. in Latin American Studies, New York Univer-sity Graduate School of Arts & Sciences. He is member of New York State Bar

About the Contributors xv

1-846730-22-8_FM_xv_12/29/2006

Association. His main practice areas include mergers and acquisitions, projectfinance, capital markets, venture capital finance and debt restructuring.

Baljit Singh Kalha is a Senior Member with law firm Titus & Co. He holdsBA (History Hons.) from St. Stephens’ College, University of Delhi, LLB fromUniversity of Delhi and LLM from the Georgetown University, USA. He ismember of the Bar Council of Delhi. His main practice areas include cross-border mergers and acquisitions, infrastructure projects, power, telecommu-nications, internet and software/information technology.

Payal Pohani is a Senior Associate with law firm Titus & Co. She holds BA(Sociology Hons.) from Lady Shriram College for Women, University of Delhiand an LLB from the University of Delhi. She is a member of the Bar Councilof Delhi. Her main practice areas include corporate transactions, mergers andacquisitions, capital markets, joint ventures and foreign investments.

Abhixit Singh is a Senior Associate with law firm Titus & Co. He holds BA.(History Hons.) and LLB from University of Delhi. He is member of the BarCouncil of Delhi. His main practice areas include project finance, joint ven-tures, inbound investments, civil and criminal litigation, alternate disputeresolution, corporate investment structuring and restructuring.

Chandra Shekhar is a Senior Member with law firm Titus & Co. He holdsMA in English Literature from Lucknow University and LLB from Universityof Delhi. With over 20 years of journalistic experience, he is currently workingas Chief of Research Bureau with the leading financial daily, The FinancialExpress, where he writes on the federal government’s fiscal and monetarypolicies, oil, trade and telecom.

Sushmita Ganguly is a Company Secretary with law firm Titus & Co. Sheholds B.Com from Allahabad University, Uttar Pradesh and is a member ofthe Institute of Company Secretaries of India. Her main practice areasinclude regulatory compliances for corporate transactions, mergers and acqui-sitions, capital markets, venture capital funds, joint ventures and foreigninvestments.

Sanjeev Jain is an Associate Advocate with law firm Titus & Co. He holdsBA and LLB from the University of Delhi. He is member of the Bar Councilof Delhi. He has co-authored articles on various legal subjects. His main prac-tice areas include mergers and acquisitions, joint ventures, civil and criminallitigation and arbitration.

Mr Deepak Mahtani, BA, MIMC, FRSA has a business degree from SophiaUniversity in Tokyo, Japan and the American College, Switzerland. Deepakis of Indian origin, lived in the Far East for 14 years and Switzerland for14 years, and speaks English, French, Spanish, Japanese, and two Indianlanguages. He is married and has two sons.

About the Contributorsxvi

1-846730-22-8_FM_xvi_12/29/2006

He is currently a management training consultant, specializing in under-standing and working with different cultures, especially in India, Japan, andChina.

He has coached and trained hundreds of senior managers who are involved inoffshore developments and outsourcing to Indian companies, and in remoteteam management around the globe. Most of his clients are FTSE100 orFortune 500 companies.

About the Contributors xvii

1-846730-22-8_FM_xvii_12/29/2006

1-846730-22-8_FM_xviii_12/29/2006

Contributor Contact Details

CII Institute of Logistics - Ramya KannanExecutiveConfederation of Indian Industry – Institute of Logistics98/1 Velachery main roadGuindyChennai 600 032.IndiaTel : +91 44 42 44 4555 xtn 566Fax: +91 44 42 44 4510

DTZ Debenham Tie Leung - Vivek Dahiya

DTZ Debenham Tie Leung2A Paharpur Software Technology Park21 Nehru Place GreensNew Delhi 110 019IndiaTel: +91 11 2620 7108-114Fax: +91 11 2620 7575Mobile: +91 98715 07801

Global Market Briefings – Roderick MillarEditor120 Pentonville RoadLondonN1 9JNUnited KingdomTel: +44 (0)207 278 0433Fax: +44 (0)207 843 1965

1-846730-22-8_FM_xix_12/29/2006

Email: [email protected]

Associate Director

Website: www.ciilogistics.com

Email: [email protected]: http://www.dtz.com

Email : [email protected] : www.globalmarketbriefings.com

C Jayanthi (Education article)46, Shivalik Apartments,Alaknanda, Pocket-A,New Delhi-110019,IndiaPhone 00 91 9810672403Office: The Financial Express,B 14A, Qutab Institutional Area,New Delhi-110016IndiaTel: +91 11 26030883

KPMG – Subir MoitraMarketing & CommunicationsBlock no 4BDLF Corporate Park, DLF CityPhase IIIGurgaonHaryana 122002IndiaPhone: +91 0124 3074000 / 2549191Fax: +91 0124 2549101 / 2549102

MDI - Dr. Amit Kapoor

Professor of Strategy & Industrial EconomicsManagement Development InstituteMehrauli Road ,Gurgaon - 122 001,HaryanaIndia.Tel: +91 124 2341053Fax: +91 124 2341189

Contributor Contact Detailsxx

1-846730-22-8_FM_xx_12/29/2006

Email: [email protected]

Website: www.in.kpmg.com

Mobile: +91 98104 02639Email: [email protected]

Honorary Chairman, Institute for Competitiveness

Website : www.mdi.ac.in

Contributor Contact Details xxi

MDI - Arun SahayProfessor, Strategic Management & Chairman, Center for EnterpreneurshipManagement Development InstituteMehrauli Road,Gurgaon - 122001HaryanaIndiaTel +91-124-5013050-56, 2346162(direct)Fax: +91-124-2341189

NASSCOM - Rajdeep SahrawatVice PresidentNASSCOM (National Association of Software and Service Companies)International Youth CentreTeen Murti MargChanakyapuriNew Delhi – 110021IndiaTel: +91 11 23010199Fax: +91 11 23015452

Shilputsi Consultants - Ms Purvi ShethVice PresidentShilputsi ConsultantsMumbaiIndiaTel: +91 22 243 79611Fax: +91 22 243 62909

Synovate - Karthik RamamurthyHead, Synovate Business Consulting,2ndfloor, AML Centre I

Off Mahakali Caves RoadAndheri (East)Mumbai 400 093IndiaTel: +91 22 4091 8000Mob: +91 98676 97194

1-846730-22-8_FM_xxi_12/29/2006

Email: [email protected]: www.mdi.ac.in

Email – [email protected]/[email protected]: www.nasscom.in

8 Mahal Industrial Estate

Email: [email protected]: www.shilputsi.com

Email: [email protected]

Contributor Contact Detailsxxii

Amit NaikareManager, Synovate Business Consulting, MumbaiMob: +91 98202 30365

Titus & Co - Diljeet TitusManaging PartnerTitus & Co, AdvocatesTitus HouseR-4, Greater Kailash-I,New Delhi-110048,India.Tel: 91-11-26280100, 26470700, 26475800Fax: 91-11-2648-0300, 2648-9950.

Winning Communications - Deepak MahtaniManaging Director of Winning Communications Partnership Ltd

Surrey

United KingdomTel: +44 (0)208 770 9717Fax: +44 (0)208 770 9747

1-846730-22-8_FM_xxii_12/29/2006

Email: [email protected]

E-mail: [email protected]; [email protected]

PO Box 43Sutton

SM2 5WL

Email: [email protected]: www.winningcommunications.com

AcronymsADR Alternate Dispute ResolutionAEZ Agri Export ZoneAoA Articles of AssociationASEAN Association of South East Asian NationsBTP Bio-Technology ParkCA2002 Competition Act 2002CA56 Companies Act 1956CLB Company Law BoardDEPB Duty Entitlement PassbookDGFT Director General of Foreign TradeDTA Domestic Tariff AreaEEFC Exchange Earners Foreign CurrencyEHTP Electronic Hardware Technology ParkEOU Export Oriented UnitEPCG Export Promotion Capital GoodsEPFMP Employees’ Provident Fund and Miscellaneous Provisions ActER Equal Remuneration Act (1976)ESI Act Employees’ State Insurance Act (1948)EU European UnionEXIM Export-importFA Factories Act (1948)FCNR Foreign Currency Non-Resident Account SchemeFDI Foreign Direct InvestmentFEMA Foreign Exchange Management ActFIPB Foreign Investment Promotion BoardFMCG fast moving consumer goodsFTP Foreign Trade PolicyGDP Gross Domestic ProductGoI Government of IndiaIDA Industrial Disputes Act (1947)IESO Industrial Employment Standing Orders Act (1946)IP Intellectual PropertyIRDA Insurance and Regulatory Development AuthorityITA Income Tax Act (1961)JV joint ventureJVC joint venture companyM&A mergers & acquisitionsMCI Ministry of Commerce and IndustryMBA Maternity Benefit Act (1961)

1-846730-22-8_FM_xxiii_12/29/2006

MW Minimum Wages Act (1948)NCLT National Company Law TribunalNHDP National Highway Development ProjectNIC National Industrial Classification CodeNRE Non-Resident External Rupee Account SchemeNRI Non-Resident IndiansNRO Non-Resident Ordinary Rupee Account SchemeNTT National Tax TribunalOCB Overseas Corporate BodyPB Payment of Bonus Act (1965)PCT Patent Cooperation TreatyPIS Portfolio Investment SchemePPP public-private partnershipRBI Reserve Bank of IndiaRoC Registrar of CompaniesSEA Shops and Establishments ActSEBI Securities and Exchange Board of IndiaSEZ Special Economic ZoneSIA Secretariat for Industrial AssistanceSME small and medium-sized enterprisesSSI Small Scale IndustrySTP Software Technology ParkTM99 Trade Marks Act 1999TM Agreement Trade Mark Licensing AgreementTRIPS Trade Related Aspects of Intellectual Property RightsTU Act Trade Unions Act (1926)UNCITRAL United Nations Commission on International Trade LawWCA Workmen’s Compensation Act (1923)WOS wholly owned subsidiary

Acronymsxxiv

1-846730-22-8_FM_xxiv_12/29/2006

1-846730-22-8_FM_xxvi_12/29/2006

Part One

Overviews

1-846730-22-8_P01_1_12/29/2006

1-846730-22-8_P01_2_12/29/2006

1.1

India at a Glance

Government: Democratic Federal Republic, gained independence in 1947

Political Structure: Head of State: President (A.P.J. Abdul Kalam, elected 2002)Head of Government: Prime Minister (Manmohan Singh, since 2004)Bicameral Parliament (Sansad) - Council of States (Rajya Sabha) - People’s Assembly (Lok Sabha)

Current Government: A coalition headed by Congress. Next elections must be before 2009.

Main Parties: there are many regionally significant political parties. Below are the fivelargest parties in the Federal parliament, with their current number ofseats:

India National Congress (known as “Congress”) 145Bharatiya Janata Party (known as “BJP”) 138Communist Party of India (Marxist) (not to be confused with theCommunist Party of India) 43Samajwadi Party (a democratic socialist party based in UttarPradesh) 36Rashtriya Janata Dal (Hindu/Muslim based democratic party based inBihar) 24

Currency: Indian Rupee (Rs or INR) Nov 06 $1 = 45 Rs; €1 = 57 Rs; £1 = 85 Rs1

GDP: $3.611 trillion at PPP; $719 billion at official exchange rate(June 05 est)2

GDP Growth Rate: 8.3% forecast 2006-073

GDP per Capita: £3,400 (2005 est)2

GDP by Sector: AgricultureIndustryServices

18.6% (2005 est)2

27.6%53.8%

Exports 2002 - $44 billion2005 - $76 billion (est)

Imports 2002 - $52 billion2005 - $113 billion (est)

1 OANDA.com2 CIA Factbook3 CRISIL.com

1-846730-22-8_P01_3_12/29/2006

Labourforce: 482 million (1999 est)2

AgricultureIndustryServices

60%17%23%

Inflation Rate: 5.4% (yr to Oct 21, 2006)4

Area: 3.29 million sq km (approx 1/3 the size of the USA)2

Population: 1.095 billion (July 2006)2

Population structure2: 30% under the age of 15 years65% between 15-64 years5% 65 years and over

Literacy (able to read and write atage 15 years and over)2:

MaleFemale

70%50%

Below poverty line: 25% (people living on less than $1 per day)5

Main Holidays: 1st January (New Years Day)26th January (Republic Day)15th August (Independence Day)2nd October (Mahatma Gandhi’s Birthday)25th December (Christmas Day)

Some Religious Holidays/Festivals:

Musharram (Islamic New Year) (20th January, 2007)Holi (Last day of) (3rd March, 2007)Mahavir Jayanthi (8th March, 2007)Sri Rama Navami (Birthday of Sri Rama) (27th March, 2007)Milad-Un-Nabi (Birth of the Prophet) (31st March, 2007)Good Friday (6th April, 2007)Baisakhi, Vishu/Bahag, Mesadi, Maghi (14th April, 2007)Buddha Purnima (2nd May, 2007)Vijaya Dasami (10th Day of Dashain Festival) (20th October,2007)Dussera or Dusshera (Victory of Good over Evil)(21st October, 2007)Eid al-Fitr (End of Ramadan) (11th-13th October, 2007)Diwali (Festival of Lights) (9th November, 2007)Idu’L Zuha/Bakrid/Eid al Akhra) (Feast of the Sacrifice)(20th December, 2007)

These festival holidays change date each year, and are not necessarily observed nationally.

Languages Spoken: English is the principal business language.Hindi is the first language of approx 38% of the populationThere are 16 further principal languages and hundreds ofregional dialects.

4 Reserve Bank of India5 World Bank, Global Monitoring Report 2006.

Overviews4

1-846730-22-8_P01_4_12/29/2006

International Airports: New Delhi – Indira Gandhi International, www.delhiairport.com(unofficial site)Mumbai (Bombay) – Chattrapathi Shivaji International Airport,www.mumbaiairport.com (unofficial site)

Kolkata (Calcutta) – Netaji Subhash Airport (Dum Dum),www.calcuttaairport.com (unofficial site)

Kochi (Cochin); www.cochin-airport.com

Hyderabad; www.hyderabadairport.com (unofficial site)

Note: Both Hyderabad and Bangalore are building new internationalairports scheduled open in 2008.

Major Ports: Kolkata (Calcutta) – www.portofcalcutta.comChennai (Madras) – www.chennaiport.gov.inKandla – Gujarat, www.kandlaport.gov.inKochi (Cochin) – Kerala, www.cochinport.comMormugao – Goa, www.mormugaoport.gov.inMumbai (Bombay) – www.mumbaiporttrust.comNew Mangalore – Karnataka, www.newmangalore-port.comParadip – Orissa, www.paradipport.gov.inTuticorin – Tamil Nadhu, www.tuticorinport.gov.inVishakapatnam – Andhra Pradesh, www.vizagport.com

Climate (average monthly minimum/maximum temperatures and averagemonthly rainfall)

January April July October

Temp Rain Temp Rain Temp Rain Temp Rain

Bangalore 14/27 °C 6 mm 21/34 °C 41 mm 19/27 °C 100 mm 18/28 °C 149 mm

Hyderabad 15/29 °C 11 mm 24/38 °C 19 mm 22/31 °C 160 mm 20/31 °C 72 mm

Kochi 23/30 °C 23 mm 26/37 °C 125 mm 24/28 °C 592 mm 24/29 °C 340 mm

Kolkata 13/26 °C 9 mm 24/36 °C 44 mm 26/32 °C 125 mm 23/32 °C 114 mm

Mumbai 19/28 °C 4 mm 24/32 °C 4 mm 25/30 °C 165 mm 24/32 °C 64 mm

New Delhi 6/21 °C 25 mm 20/36 °C 8 mm 25/30 °C 179 mm 18/34 °C 10 mm

India at a Glance 5

1-846730-22-8_P01_5_12/29/2006

Chennai (Madras); www.chennaiairport.com (unofficial site)

Bangalore; www.bangaloreairport.com (unofficial site)

1-846730-22-8_P01_6_12/29/2006

1.2

Political Background andOverview

India has long been a nation of philosophers with a well-developed and peacefulsociety. One of the oldest scriptures in the world is the four-volume Vedas, whichmany regard as the thought repository of ‘Indic culture’ that projected some ofthe modern scientific discoveries. There have been many major ruling dynasties,for example the Maurayas, Guptas, the Shakas and the Kushans. Chanakya(350 BC–275 BC) is known for his political and economic astuteness and is stillquoted in management institutes whilst teaching strategy or policy. John DBarrow’s book The Book of Nothing credits the Indian astronomer Brhamagupta(628 AD) for defining zero, whilst Aryabhata (476 BC) is credited for inventingzero, without which today’s progress in science and technology would not havebeen possible. Nearly every major religion in the world is represented in India. Itis also the land of Lord Buddha, Lord Mahavira and Guru Nanak Dev, thefounders of Buddhism, Jainism and Sikhism.

Despite formidable barriers in the form of the mighty Himalayas to the Northand oceans to the East, South and West, India has also received a succession offoreigners, many of them carrying swords, guns and dynamite. The Aryans wereamong the first to arrive in India, which was, until then, inhabited by theDravidians. Others who came later included Greeks, Persians, Mughals and lat-terly the British, Portuguese and French. Among them, the British gainedsupremacy and ruled India for centuries.

Out of these waves of immigration, a composite culture has emerged. ThusIndia has become a land of unity in diversity – a land of integration, adoption andlearning, a land of change and continuity.

Mahatma Gandhi, a British-educated lawyer, mobilized the Indians andthrough his Satyagraha, a unique non-violent campaign, India threw off thebondage of British rule on 15 August 1947. Free India’s first Prime Minister,Pandit Jawaharlal Nehru, described the moment as a ‘tryst with destiny’. In lessthan three years of attaining freedom, India had framed a Constitution anddeclared itself a Republic on 26 January 1950. The Constitution was given shape

Dr Arun Sahay,Professor of Strategic Management andChairman, Centre for Enterpreneurship,Management Development Institute

1-846730-22-8_P01_7_12/29/2006

by some of the finest minds of the country, who ensured the trinity of justice,liberty and equality for the citizens of India. The Constitution was made flexibleenough to adjust to the demands of social and economic changes within a demo-cratic framework.

India, a union of states, is a sovereign, secular, democratic Republic with a par-liamentary system of government. The Indian polity is governed in terms of theConstitution, which was adopted by the Constituent Assembly on 26 November1949 and came into force on 26 January 1950. The President is the constitutionalhead of the Executive of the Union. Real executive power vests in a Council ofMinisters with the Prime Minister as head. Article 74(1) of the Constitution pro-vides that there shall be a Council of Ministers headed by the Prime Minister toaid and advise the President who shall, in exercise of his functions, act in accor-dance with such advice. The Council of Ministers is collectively responsible to theLok Sabha – the House of the People.

India’s bicameral parliament consists of the Rajya Sabha (Council of States)and the aforementioned Lok Sabha (House of the People). The legislatures of thestates and union territories elect 233 members to the Rajya Sabha, and the Pres-ident appoints another 12. The elected members of the Rajya Sabha serve six-yearterms, with one-third up for election every two years. The Lok Sabha consists of545 members; 543 are directly elected to five-year terms. The other two areappointed.

It is generally believed that states are represented in the Rajya Sabha and thepeople in the Lok Sabha but with so many regional parties springing up, the rolesof the Rajya Sabha and the Lok Sabha seem to have become inverted. After 1996,due to the pre-eminence of regional parties in the Lok Sabha, for all practicalpurposes, it is the Lower House (Lok Sabha) that represents states’ interests.Thus the importance of the Upper House (Rajya Sabha) has been declining. Giventhe scheme and design of Indian Constitution, the federalism has been weakbecause it flows downwards from the centre, rather than upwards from the states.The political scenario has changed and an era of coalition government at the cen-tre has emerged, due to the following four developments:

1. Emergence of formal regional parties – ‘regional’ meaning confined to onestate (or at best extended to the neighbouring states) – now account foraround half the seats in the Lok Sabha. This proportion is likely to increasein future elections.

2. Even the so-called national parties have now become regional in terms of theinterests they represent. This is partly due to the aggregative definition of‘national’ that is used in the electoral context. A party needs to win only morethan 5 per cent of the total votes polled to become national, regardless of thedistribution of those votes. Hence, the Communist Party of India-Marxist isa ‘national’ party, even though it is concentrated in just two-and-a-half states.

3. Due to criteria used for candidate selection by political parties – caste, moneyand muscle, in that order – there is lesser talent available in the Lok Sabhafor ministerial posts than in the Rajya Sabha. However, partly, it is compen-sated by the generally rising level of education. Nonetheless, the best minis-ters are from the Rajya Sabha, which also provides a way of bringing decent

Overviews8

1-846730-22-8_P01_8_12/29/2006

folk into politics. Thus the quality of parliamentary debate, which shouldform an essential element of governance and legislation, is better in RajyaSabha compared to that in Lok Sabha.

4. The balance between Rajya Sabha and Lok Sabha has been changing. Thebill that should be thoroughly debated in Lok Sabha and should passthrough Rajya Sabha in reality is debated in Rajya Sabha before being sentfor presidential assent.

There are 26 states and 6 Union territories in the country. The system ofgovernance in the states closely resembles that of the Union. In the states, theGovernor, as the representative of the President, is the Head of State, but realexecutive power rests with the Chief Minister, who heads the Council of Ministers.The Council of Ministers of a state is collectively responsible to the elected leg-islative assembly of the state.

The Constitution governs the sharing of legislative power between Parliamentand the State Legislatures, and provides for the vesting of residual powers inParliament. The power to amend the Constitution also vests in Parliament.

Government and its role

According to its constitution, India is a ‘sovereign, socialist, secular, democraticrepublic.’ Like the United States, India has a federal form of government. How-ever, the Central Government in India has greater power in relation to its states,and its Central Government is patterned after the British parliamentarysystem. Subjects like defence, foreign policy and atomic energy are dealt with bythe Central Government, whilst law and order is dealt with by the state govern-ments. Certain subjects like science and technology, education and environmentare concurrent and dealt with by both the governments.

In 1948, immediately after independence, the GoI (Government of India) intro-duced the Industrial Policy Resolution. This outlined the approach to industrialgrowth and development. To meet new challenges, from time to time, it wasmodified – in 1973, 1977 and 1980. The Industrial Policy Statement of 1980focused attention on the need for promoting competition in the domestic market,technological upgrading and modernization. The policy laid the foundation for thechange of attitude from import substitution to export promotion which encouragedforeign investment, especially in high-technology areas. A number of policy andprocedural changes were introduced in 1985 and 1986 under the leadership of thethen Prime Minister Shri Rajiv Gandhi. These policy initiatives aimed at increas-ing productivity, reducing costs and improving quality. The emphasis was onopening the domestic market to increased competition and readying the domesticindustry to stand on its own in the face of international competition. The publicsector was freed from a number of constraints and given a larger measure ofautonomy. The technological and managerial modernization of industry was pur-sued as the key instrument for increasing productivity and improving globalcompetition. The net result of all these changes was that Indian industry grew byan impressive average annual growth rate of 8.5 per cent.

Political Background and Overview 9

1-846730-22-8_P01_9_12/29/2006

However, India’s 1991 debt crisis provided the opportunity for major economicreforms to deregulate the private sector and liberalize trade and investment. Thisled to the drastic cut-back of compulsory licensing of private sector industries andby 1997 applied only to nine industries. Restrictions on foreign companies andforeign financial institutions wishing to enter the Indian market were lifted oreased. A steady process of removing quantitative quotas and reducing tariff rateson imports created a more favourable environment for export-oriented produc-tion. The recovery from the initial shock of structural adjustment, buffered by amassive infusion of IMF (International Monetary Fund) loans, has generally beenconsidered remarkable. Initially, the politicians of the opposition parties resistedthe reforms tooth and nail but when they came to power, they found no alternativebut to proceed with the reform.

When the present UPA (United Progressive Alliance) Government was formed,backed by the support of communist parties, the general expectations was thatthe reforms undertaken by the earlier governments would be made redundantand the economy would not be able to maintain its growth targets. However, todayin India there exists a stable government, privatization, improved education andjob opportunities, reduction in the deficit balance of payments and favourableforeign exchange reserves, despite pressure from the left-leaning parties opposingsuch initiatives.

Indian judiciary

India’s present judicial system came to life under the British. Thus its conceptsand procedures resemble those of Anglo-Saxon countries. The Supreme Courtconsists of a chief justice and 25 other justices, all appointed by the President onthe advice of the Prime Minister. The active role of the Indian judiciary, particu-larly the Supreme Court of India, has been widely appreciated both within as wellas outside India. The Indian judicial system proved its mettle in handling theBhopal gas leak case, which was unique for the whole world. The independenceof the judiciary ensured through the constitutional provisions and subsequentstrengthening by judicial interpretation has definitely contributed to the presentstatus of the Indian judiciary.

Judicial framework

● independent judiciary with minimal interference from the GoI;

● Supreme Court, the apex judicial authority, is vested with powers to enforcefundamental rights and act as a guardian of the Constitution;

● apart from the Supreme Court, the Indian judicial system has High Courts inevery state, and lower courts at town levels;

● in addition, there are alternative dispute resolution mechanisms to helpliquidate pending cases in the various courts, either through arbitration orconciliation.

Overviews10

1-846730-22-8_P01_10_12/29/2006

Change in attitude of Indian polity

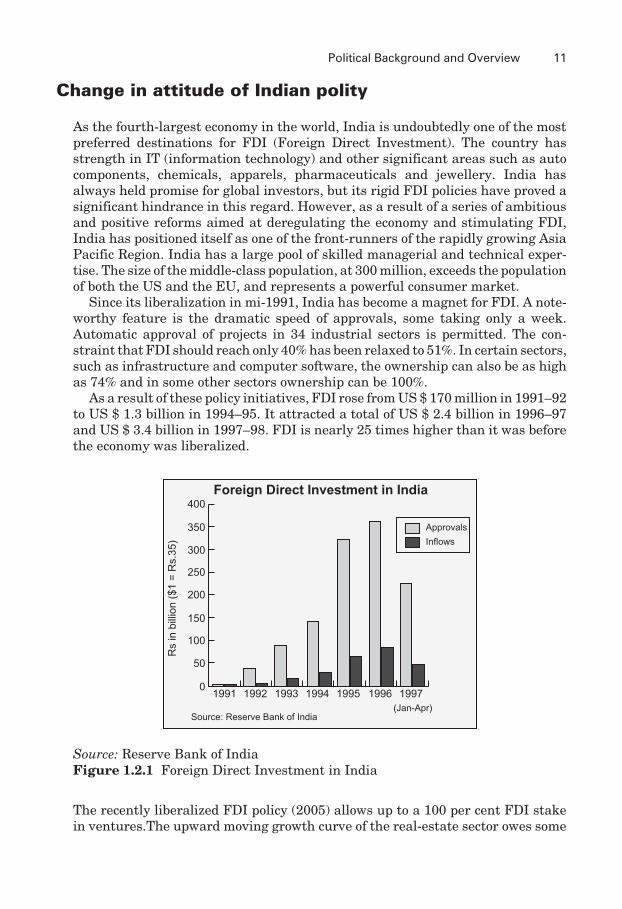

As the fourth-largest economy in the world, India is undoubtedly one of the mostpreferred destinations for FDI (Foreign Direct Investment). The country hasstrength in IT (information technology) and other significant areas such as autocomponents, chemicals, apparels, pharmaceuticals and jewellery. India hasalways held promise for global investors, but its rigid FDI policies have proved asignificant hindrance in this regard. However, as a result of a series of ambitiousand positive reforms aimed at deregulating the economy and stimulating FDI,India has positioned itself as one of the front-runners of the rapidly growing AsiaPacific Region. India has a large pool of skilled managerial and technical exper-tise. The size of the middle-class population, at 300 million, exceeds the populationof both the US and the EU, and represents a powerful consumer market.

Since its liberalization in mi-1991, India has become a magnet for FDI. A note-worthy feature is the dramatic speed of approvals, some taking only a week.Automatic approval of projects in 34 industrial sectors is permitted. The con-straint that FDI should reach only 40% has been relaxed to 51%. In certain sectors,such as infrastructure and computer software, the ownership can also be as highas 74% and in some other sectors ownership can be 100%.

As a result of these policy initiatives, FDI rose from US $ 170 million in 1991–92to US $ 1.3 billion in 1994–95. It attracted a total of US $ 2.4 billion in 1996–97and US $ 3.4 billion in 1997–98. FDI is nearly 25 times higher than it was beforethe economy was liberalized.

400Foreign Direct Investment in India

350

300

250

200

150

Rs

in b

illio

n ($

1 =

Rs.

35)

100

50

Source: Reserve Bank of India

0 1991 1992 1993 1994 1995 1996 1997(Jan-Apr)

ApprovalsInflows

Source: Reserve Bank of IndiaFigure 1.2.1 Foreign Direct Investment in India

The recently liberalized FDI policy (2005) allows up to a 100 per cent FDI stakein ventures.The upward moving growth curve of the real-estate sector owes some

Political Background and Overview 11

1-846730-22-8_P01_11_12/29/2006

credit to a booming economy and liberalized FDI regime. In March 2005, the GoIamended the rules to allow 100 per cent FDI in the construction business. Thisautomatic route has been permitted in townships, housing, built-up infrastruc-ture and construction development projects, including housing, commercialpremises, hotels, resorts, hospitals, educational institutions, recreational facili-ties, and city- and regional-level infrastructure.

entrepreneurship

After independence in 1947, India embarked on a period of centrally plannedindustrialization. The centrepiece of the planning regime was the Industries(Development and Regulation) Act of 1951, which states that ‘it is expedient inthe public interest that the Union should take under its control the industries inFirst Schedule.’ This Act introduced a system of industrial licensing to control thepace and pattern of industrial development across the country, which becameknown as the ‘license raj’. Licensing became the key means of allocating produc-tion targets set out in the five-year plans to firms. Both state and private firms inthe registered manufacturing sector were covered under the licensing regime.State control over industrial development via licensing was intended to accelerateindustrialization and economic growth, and to reduce regional disparities inincome and wealth. However, the policy encouraged the industries to cornerlicense rather than serve consumers.

The bureaucratic nature of the licensing process imposed a substantial admin-istrative burden on firms. There was also considerable uncertainty as to whetherlicence applications would be approved and within what time frame. For example,35 per cent of licence applications in 1959 and 1960 were rejected, with therejected applicants accounting for around 50 per cent of the investment value ofall applications. Recognition of these problems led to various reforms in the 1970s,which attempted to streamline the application process, raise exemption andexpansion limits and exempt specific product lines from the provisionsof the 1951 Industries Act. By this time it had become apparent that industriallicensing had failed to bring about the rapid industrial development that had beenanticipated in the 1950s. The heightened political competition that followed ledto pressure to dismantle government controls, including the industrial licensingsystem. The Congress leader Indira Gandhi responded via the 1980 Statement onIndustrial Policy, which signaled a renewed emphasis on economic growth(GoI, 1980). Large-scale de-licensing, however, did not occur until her son RajivGandhi unexpectedly came to power following his mother’s assassination in 1984.Some 25 broad categories of industry were entirely exempted from industriallicensing in March 1985. In late 1985 and 1986, further relaxations of the indus-trial licensing system followed.

After Gandhi, his successors, in response to external pressures, implementeda large-scale liberalization of the Indian economy. Such reformist tendencies ofthe Narsihma Rao Government were unexpected. Perhaps the then FinanceMinister, Man Mohan Singh, saw the possibilities in reform. In 1991, industriallicensing was abolished, except for a small number of industries where it was

Overviews12

From license raj to the era of innovation and

1-846730-22-8_P01_12_12/29/2006

retained ‘for reasons related to security and strategic concerns, social reasons,problems related to safety and over-riding environmental issues, manufacture ofproducts of hazardous nature and articles of elitist consumption’ (GoI, 1991).Additional industries were removed from the provisions of the 1951 Industries inthe post-1991 period. With the advent of WTO, in which India plays a key role,non-tariff barriers were removed and tariff rates slashed. The stated rationale forthe liberalization of industrial policy was to actively encourage and assist Indianentrepreneurs to exploit and meet the emerging domestic and global opportunitiesand challenges.

Growing youth population

In the 1990s, the population growth rate came down from 2.1 per cent (recordedin the previous decade) to 1.9 per cent. Population control is a legitimate economicagenda but is shunned by political parties due to election pressures and the votinggame. India is the second most populous country in the world, with a higher pop-ulation growth rate than China. India’s population has cssed the billion mark andwill soon exceed that of China. Some 68 per cent of the population still live in ruralareas yet to witness the benefits of the reform process. However, there is a silverlining in this population growth. A total of 550 million Indians are under theage of 25, and 350 million under 15 years (source: IBEF, 2006). By 2013, the netaddition to the productive population (aged 25–44 years) will be 91 million, or33 per cent. The biggest benefit of this demography is the high consumer base.They will also form an educated labour force, trained in technology and aware offorces of globalization.

The youth brings with it newer and more advanced knowledge, technologicalknow-how, and an aggression that was not encouraged by earlier, more sober andrigid social and governmental systems. The manufacturing industry is on a rollonce again, banks have improved their efficiency to cater for demanding cus-tomers, and private entrepreneurship has found a new lease of life from the GoI’spolicies. A new trend of shifting from job seeking to searching for self employmentopportunities is also taking place.

Today’s youth

0100200300400500600

IndiaChina

Indonesia US

Brazil

Japan

Germany 0

102030405060

Absolute population below 25 years (m)Proportion of population below 25 (% RHS)

Source: www.childrendatabank.orgFigure 1.2.2 Today’s youth

Political Background and Overview 13

1-846730-22-8_P01_13_12/29/2006

The new face of the Indian consumers

Indian consumers are increasingly exposed to the latest products and technologiesavailable in different sectors. Exposure occurs not only through internationalmedia, including the Internet and satellite television but also through travel. Withmore and more Indians travelling to foreign countries for business or holidays,purchasing opportunities are also increasing. Around 5.5 million Indians trav-elled abroad in 2004, representing a rise of 25 per cent compared to 2003. Indianshoppers spent US $ 100 million during the Dubai Shopping Festival in 2003, witha large part dedicated to luxury goods such as fragrances, cosmetics, watches and

0

100

200

300

400

500

600

93 94 95 96 97 98 99 0 1 2 3E0

10

20

30

40

50

60GDP Per CapitaPeak Personal Tax Rate

Figure 1.2.3 (this needs some labelling)

Reforms and results during the last 15 years

● 1991 Economic liberalization initiated by Indian Prime MinisterPV Narasimha Rao and his Finance Minister Manmohan Singh in response toa macroeconomic crisis;

● 1998 India’s economy was US $ 1702.7 billion, which accounted for a 5% shareof world income;

● 2005 India’s economy is worth US $ 3319 billion (Purchasing Power Parity)which accounts for a 6% share of world income, the fourth largest in the worldin terms of Purchasing Power Parity.

Overviews14

1-846730-22-8_P01_14_12/29/2006

jewellery (Source: 2006 – www.beauty-on-line.com).

10

8

1951 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

7.6

2.69

6.23

2.533.28

4.67

7.31

4.94

-3.67

-0.33-0.5 -0.09

6

4

2

0

-2

-4

-6

Note: *Constant Prices: Chain seriesSource: Penn World tablesFigure 1.2.4 Growth rate of India’s real GDP per capita, 1950–2006*

Political Background and Overview 15

1-846730-22-8_P01_15_12/29/2006

1-846730-22-8_P01_16_12/29/2006

1.3

An Economic Overview ofIndia

India is a study in contrasts. It is undeniable that India is one of the fastest grow-ing economies in the world but stark issues stare it in the face like, low GDP percapita; a lowly rank on the Human Development Index; abject poverty with 26 percent of its people living under the poverty line; the growing economic disparity,still a large part of the population deriving income from agriculture; 2 per cent ofworld land accommodating nearly 17 per cent of the world population; a dismalstate of healthcare in India; crumbling infrastructure with projects that aredelayed for years; a power situation that is appalling; corruption that is a menace;interfering polity and bureaucracy; Foreign Direct Investment that is smallerthan that received by Hong Kong.

This paints a fairly gloomy picture for India as a country. Then what makes ittick? Why is it that every economist talks about India and each company has anIndia strategy? Lying under this dismal picture is the opportunity that presentsitself, the opportunity to change, contribute and grow. Even though India has alow GDP per capita it has one of the highest saving rates in the world. It is thisbase of GDP per capita that is about to explode and present to the world the largestmiddle class market in the world. At present it is estimated that urban and ruralmiddle class homes in the country total around 40 million. The opportunities thatawait the telecom market with an exploding market that is growing exponentiallyat 30 million connections a year; the opportunities in the healthcare industry; thegrowing tourism industry; the opportunities in infrastructure projects; the grow-ing airline industry; the coming of age of Indian manufacturing; the talentedworkforce that India presents to the world and last but not the least the dynamicIndian IT and ITES industry. India is sitting on the cusp of change, the changethat will transform the very structure and nature of the world economy in thecoming 5 decades.

Amit Kapoor,

Management Development InstituteProfessor of Strategy and Industrial Economics

1-846730-22-8_P01_17_12/29/2006

The Indian Economic History

India has a legacy of long term colonial stagnation and economic backwardness.It was in 1947 that India regained independence and started a journey towardsself-reliance. The aspiration of the leaders during independence was to turn Indiainto a vibrant, self-reliant national economy and do away with the vagaries ofabject poverty. India had negatives, in the form of a limited entrepreneurial classand non-functional capital markets. Looking at this the state, i.e. Government,had to fulfill the role of capital accumulation and acting as an entrepreneur. Thisgave rise to public sector units which ended up becoming the agents for growthand industrialization. The strategy gave results as it accelerated the pace ofgrowth and moved India out of stagnancy of the pre-independence era.

As India continued to pursue these goals, the policies ended up being moreinward looking and protectionist. The huge bureaucracy was put in place to mon-itor and govern the permits designed to stimulate and control the industry whilelimiting foreign trade and investment. The “License Raj” created high barriersthrough tariffs and quantitative restrictions on imports. This disincentiviseddomestic Indian industry from innovating and improving its manufacturing qual-ity. The License Raj administered almost all aspects of business, limiting thecapability of business to expand and improve its productivity. The Governmentinterfered in the proper functioning of the markets by setting prices in manyindustries, regulating transport costs and regulating the labor markets.

Due to these interventionist and isolationist policies the economy started tosuffer. The exports declined from 6.5 per cent of GDP to 3.6 per cent in 1970. Thetrend continued and India ended up facing the worst economic crisis since itsexistence as an independent nation. India faced a severe balance of payment(BOP) crisis in 1991. The crisis was exasperated with the collapse of the SovietUnion in the same year. The collapse of the Soviet Union depicted the final blowto the ideals of a centrally controlled economy, against which India had modeleditself. The collapse crippled India’s most significant export market and put a deathknell on its primary source of economic aid.

This crisis created a condition severe enough for the Government to re-examinethe approach to development that India had since independence. It was in July1991 that the Government embarked on a new approach to economic development.It was clearly recognized that correcting the macroeconomic imbalances, replacingoppressive control of managing entry of firms and competition would help in over-coming the BOP crisis. India started taking serious steps towards making asystematic shift towards a more open economy. The ideas behind the move wereto have a greater reliance on market forces, a larger role for the private sectorwithin the country and the changing role of the government.

The key features in India’s economic reforms were related to fiscal and mone-tary tightening, overhaul of foreign trade and investment regulation, reducedstate control of the industry, financial sector liberalization and elimination ofmicroeconomic regulation.

Overviews18

1-846730-22-8_P01_18_12/29/2006

The Present Economic Situation

The present economic situation in India looks promising with a GDP growth ratearound 8.4%. The economy is propelling upwards with the increase in domesticdemand. The service sector contributes 54% of economic output and is growing ata rate of nearly 10%. The Indian Information Technology and Business ProcessOutsourcing sectors are continuing to grow and perform, driven by internationaldemand and low cost labor that India has in quantity. This sector though has alimited impact on employment generation as at present it employees around onemillion people which is insignificant looking at the base of 1100 million populationof the country.

The Industry or the manufacturing sector accounts for about 26% of GDP andis growing at around 9%. The sectors that contribute to the success are textiles,metals and alloys and transport equipment.

Services54%

Agriculture20%

Composition of Indian Economy

Industry26%

The agriculture sector which has 20% share of GDP is the cause for concern. Eventhough India has had favorable monsoon in the last few years the growth rate forthe sector has been a meager 2.3%. This reflects the difficulties the agriculturesector faces in the country especially in raising productivity. The sector is begin-ning to face an acute water crisis with problems further accentuated throughmismanagement of irrigation and surface water management.

The development that India sees today seems outstanding when compared toits own historical data. If we look at the data in comparison to China the sheenseems to tarnish a little. India grows at 8.4% whereas China at 10%; India con-tributes 6.2% of world GDP as against China’s 14%; 44% of India live as destituteagainst that of 39% in China; China has a literacy rate of 95% to 68% that ofIndia; manufacturing is 16% of India’s GDP to 37% in China; Indian exports are$71 Billion which are just 10% of China’s export of $713 Billion.

Moving further on we notice that China commands 25,000 kilometers of 4 lanehighways against 3,000 kilometers in India; China has 375 million mobile phonesubscribers to that of 100 million in India; 73% of Chinese access the internet tothat of 23% Indians; it takes 71 days to start a business in India to 48 days inChina; 49.5% of per capita income is required to start a business in India tothat of 14% in China; enforcing contracts can be a problem in comparison to

An Economic Overview of India 19

1-846730-22-8_P01_19_12/29/2006

China; India received around $8 billion of Foreign Direct Investment (FDI)against $70 billion to that of China etc.

These statistics may seem to dim the picture for India but also give indicationsas to what India needs to do to have a more resilient model for growth. India needsto invest in infrastructure, focus on manufacturing, improve legal procedures etc.India is also a nascent market which is ready to explode as it would foresee “hockeystick” growth in sectors like telecom, internet, infrastructure. Beyond doubt ifIndia starts looking at infrastructure alone not only will it propel sectors like air-lines etc, the sector has a potential to move India out of dangerous levels ofunemployment which today stands at about 42 million unemployed graduates. IfIndia focuses on improving its governance and its legal frameworks then it hasthe potential of being one of the most attractive FDI destination amongst theemerging economies.

Indian Competitiveness

According to the acclaimed Harvard academic Prof. Michael E. Porter, competi-tiveness is the fundamental underpinning of prosperity. While macroeconomicshifts, political development, resource price swings, and spurs of trade can allmove GDP per capita, but the only reliable basis for true prosperity is the pro-ductive capacity of a nations economy. He further iterates that productivity setsa nations standard of living. Productivity supports high wages, strong currencyand attractive returns to capital and with a high standard of living. Going furtherPorter explains that productivity improves when a country can mobilize its humanresources to generating value within the economy. Porter articulates that it isinnovative capacity of the economy that would be the cornerstone of productivityin the long run. In the context of economic development the innovation referredto a country’s ability to upgrade its business environment. The aspects that reflectthe microeconomic business environment are Factor Conditions, Demand Condi-tions, Related and Supporting Industries and Context for Firm Strategy andRivalry. It is eventually the management of these four determinants that wouldincrease levels of competitiveness of an economy.

Analyzing these aspects of the microeconomic business environment further wecan look at factors that have an impact on growth of the Indian economy andfurther its competitiveness and economic prowess internationally. The aspectsthat are driving India’s growth are basically the factor conditions and the demandconditions.

Factor ConditionsPorter refers to “factor conditions” as the situation in a country regardingproduction factors, like skilled labor, infrastructure, etc., which are rel-evant for competition in particular industries.

India’s factor conditions are mixed with contradictions across cate-gories. India has one of the largest pool of engineers and scientists butwe see an abysmal rate of patenting within the country. It is perceivedthat India has a large English speaking population but according to some

Overviews20

1-846730-22-8_P01_20_12/29/2006

estimates it is around 2% of the population. The infrastructure in thecountry is improving but not at the rate at which it is required to sustainthe growth rates of greater than 8%. India faces huge problems in itstransport infrastructure including rail, road and air. Today the infras-tructure bottlenecks have started hindering the growth of sectors withinthe country.

Demand ConditionsIt is the demographic structure of India that spurts demand today andwould drive the demand for the future. As of today 33% of India’s popu-lation is below the age of 15. In the next 10 – 15 years it is estimated that250 million workers will be added to the labor pool, who when gainfullyemployed will create a consumption class that would be parallel to none.

Furthering the concept of Competitiveness we see that successful economicdevelopment is a process of successive upgrading, in which the nation’s businessenvironment evolves to support increasingly sophisticated and productive waysof competing by firms. The nations evolve through various stages of competitivedevelopment.

Stages of Economic Development

Factor DrivenEconomy

Input Cost

InvestmentDriven Economy

Efficiency

InnovationDriven Economy

Unique Value

Source: Porter (1990)

The growth strategy currently followed by India focuses primarily on exploitingits factor inputs. The boom in IT & BPO is driven by availability of low cost labor.The focus and growth has been lead in work which is not high in value addition.The growth in the software sector is not driven by innovation rather it is theavailability of cheap technical manpower which is driving the industry’s growth.If we look at the productivity of an Indian Information Technology professionalvis-à-vis an Israeli professional we would be surprised to see the results. Low costlabor does not necessarily provide competitive advantage to the nation as it isalways at a precarious position and in danger of being overtaken by another lowcost provider of human capital. In the long run it is not the low cost of factor inputsthat drives the economy rather it is the innovative capacity and capability thatmakes the difference. Innovation in all likelihood increases trade, helps in main-taining market share, improves processes and offers high quality products. Indiaas we see is clearly lagging behind in producing products efficiently. It is the long-term orientation and outlook which would make a difference and not the policyinitiatives that are incomplete and in bursts. India as a country has been drivenby inherited prosperity, i.e., focusing on population, low cost of labor, etc. India

An Economic Overview of India 21

1-846730-22-8_P01_21_12/29/2006

will have to move ahead, wake up and take action. To say the least, India is gainingadvantage because of labor arbitrage. In the future it would have to focus moreon manufacturing and innovation. At this juncture the economic situation Indiahas is full of promises as it has nowhere else to go except upwards.

Regulation

Looking at regulation becomes important as it sets the tone for entry of firms andthe business conducts itself in the country. India has an exhaustive legal frame-work governing all aspects of business. Some of the important ones that haveimplications for a foreign investor are Companies Act, 1956, Governing CorporateBodies; Competition Act, 2002, Ensuring Competitive Spirit in the Market; Con-sumer Protection Act, 1986, Law Protecting Consumers; Factories Act, 1948, LawRegulating Labor in Factories; Foreign Exchange Management Act, 1999, Frame-work regulating foreign exchange transactions; Industries Disputes Act & Work-men Compensation Act, 1951, Laws dealing with labor disputes; IT Act, 1999,Regulation for Internet Commerce Activities; Sales Tax Act, 1948, Governs thelevy of tax on sales.

Various regulatory bodies act as points of contact between the investors andthe Indian Government. Some of the significant regulatory authorities are theForeign Investment Promotion Board (FIPB), Reserve Bank of India (RBI), Reg-istrar of Companies, Securities and Exchange Board of India (SEBI), CentralBoard of Direct Taxes (CBDT) etc.

Since India is moving on the path of economic deregulation there have beensubstantial removal of bureaucratic controls and hurdles on the industry. Licens-ing has been abolished in most of the sectors except atomic energy and railways.Certain industries where licensing is still mandatory are alcohol, cigarettes andtobacco, electronics, aerospace and defense equipment, industrial explosives andhazardous chemicals. With the new Industrial Policy of 1991 the regulatory envi-ronment for foreign investment has been eased consistently which has made thepolicy much more investor friendly. FDI is permitted in most of the sectors exceptatomic energy, lottery and gambling businesses, plantations, retail trading andagriculture (excluding floriculture, horticulture, seed development, animal hus-bandry, pisciculture and cultivation of vegetables and mushrooms).

Challenges that India Faces

No doubt India, with its massive pool of humanity and resources is expected toplay a significant role in world and its own development in coming times. But thisshall necessitate a maturing to its expected role and thereby rising to take upthe challenge. In absence of this inner re-orientation happening the right way,it may collapse inwards, creating problems for rest of the world. The rest ofthe world can duly perceive India to be a vibrant place, filled with investmentopportunities (necessarily with the concomitant risks). Thus more clarity shallaccrue to current policy makers, industry players, potential investors in the

Overviews22

1-846730-22-8_P01_22_12/29/2006

immediate and long run in understanding the lesser known truisms about thephenomena of India following its liberalization-globalization and privatization.William Baumol, professor of economics and entrepreneurship at New YorkUniversity, talks of “the use of imagination, boldness, ingenuity, leadership, per-sistence and determination” as relevant characteristics of those who go forentrepreneurship, a useful inventory of attributes to be applied to assess require-ments of being a successful investor in the current ceaselessly changing India.

In 2006, though huge strides seem to have been made in economic and socialevaluation, the sustenance of momentum is found groping in dark. The initialexuberance is dwindling and policy framers are at mercy of parochial sectarianand regionally obsessed politicians. The disparities have grown. Report afterreport by global agencies rank the country relatively low on positive attributeslike per capita income and shamefully high on negative traits like corruption andease of doing business in India. Resilience to internal disturbances at the handsof terrorists and a successful combating of the Indo-Pakistan border conflict alongthe way is praiseworthy. Sadly, the resilience is more about apathy and ineffec-tiveness of peace ensuring mechanisms than rooting out fundamental drivers ofdisruptive vectors. The population is yet to invoke truly mature democratic routesto ensuring accountability by the ruling elite. If India is to give to its people acountry that commands respect all across the world in the coming years it willcertainly have to answer and tackle the issues it faces. Even though the negativesthat India faces can be burdensome and may disrupt the growth that India hastoday they are greatly outnumbered by the positives.

Finally, let it be said that it is a mistake to analyze India as a monolithic nation:its cultural diversity and economic disparities coupled with its geographical-people-economic size make it an equivalent in complexity to all Europe and Africa.Accordingly, its 29 states need to be studied on case-by-case basis. In fact, if aframework has to be used, we can talk of two India’s, with nearly 20% living inurbanized locations and the major part in rural areas. The sensibilities, mindsetsand priorities are dramatically different across these two India’s. Accordingly, allpolicy making that employs scale neutral techniques and harnesses the tremen-dous manpower resource, also exploiting the diversity shall yield better andlonger-term results.

An Economic Overview of India 23

1-846730-22-8_P01_23_12/29/2006

1-846730-22-8_P01_24_12/29/2006

Part Two

Mechanics of BusinessEngagement

1-846730-22-8_P02_25_12/29/2006

1-846730-22-8_P02_26_12/29/2006

2.1

Labour, Skills and Training

C Jayanthi

As is widely acknowledged, India’s economic growth has been nothing short ofinspiring, and the country’s growth – at 8.4 per cent – is among the highest in theworld. As a result, the country’s education system has been turned upside down.From a population of approximately 300 million at the time of independence, thecountry is now 1 billion people strong. However, a fast growing economy needspeople with skills. The first Prime Minister of the nation, Jawaharlal Nehru, builtexcellent institutions of higher education, such as the IITs (Indian Institutions ofTechnology) and the IIMs (Indian Institutions of Management), which havebenefited the country greatly. Some 80 per cent of India is still rural and primaryeducation has been in a state of neglect. To set right this anomaly, the GoI(Government of India) has attacked the problem with renewed vigour through theEFA (Education for All) or the SSA (Sarva Shiksha Abhiyan) programme.

The SSA, the flagship programme of the UPA Government – that the CentralGovernment launched in partnership with the State Governments, is expected tobe instrumental in attaining the goal of UEE (Universal Elementary Education)in the country. The Prime Minister heads the National Mission for the SSA, whichmonitors the progress made under the scheme. The SSA is expected to providerelevant elementary education for children in the country aged between 6 and14 years old by 2010. The goal of the SSA is consistent with the Constitution (86th)Amendment Act, 2002, which makes elementary education a fundamental rightof every child living in the country.

The performance audit of the SSA, carried out by the CAG (Comptroller andAuditor General) of India (March 2005) mentions specifically the aim of the SSA:“to ensure that all children complete five years of primary schooling by 2007; toensure that all children complete eight years of elementary schooling by 2010;bridge all gender and social category gaps at the primary stage by 2007 and at theelementary educational level by 2010 and achieve universal retention by 2010.”

Covering the period from 2003–04 to 2007, the SSA has received external fund-ing to the tune of US $ 1 billion from the World Bank’s IDA (InternationalDevelopment Association); the Department for International Development, theUK and the European Commission. The SSA is an ambitious programme, meantto cover 19,200,000 children in the country. It evolved from the recommendationsof the state education ministers’ conference held in October 1998 to kick-startUEE. The programme was launched in 2001–02. Since its inception, allocation offunds under the SSA has shown high growth from US $ 77,467,906 in 2000–01 to

1-846730-22-8_P02_27_12/29/2006

US $ 1.6 billion in 2005–06, and to US $ 2.4 billion in 2006–07, representing anincrease of 41 per cent over the previous year (2005–06).

The World Bank Aide-Memoire (January 2006) on the third joint-reviewmission of the SSA mentions that the target of reducing out-of-school children by3 million per year is being exceeded. It mentions that the number of out-of-schoolchildren has fallen from 25 million in 2003 to 13.5 million as on March 2005 andthat “the positive trend will continue in 2006”.

Clearly, a great deal needs to be done. There are 48 districts in the countrywhere more than 50,000 children are out of school, according to the World Bankreport. According to the CAG of India’s report on the SSA (March 2005), nation-ally, there were 71 children out–of school per thousand. Therefore, efforts need tobe speeded up in this direction. Gender parity continues to improve, almost withinreach at the primary level, according to the World Bank report. The girls to boysratio at the primary level has increased from 0.90 in 2003–04 to 0.91 in 2004–05.

Another key component of the flagship programme of the UPA Governmenthas been the midday meal scheme that is seen as key to retaining children atschool. The scheme was launched as a centrally sponsored scheme in August 1995.Central assistance comprised free foodgrain via Food Corporation of India andan admissible transport subsidy. Initially, most states received a dry ration of3 kilogrammes per person. The centre earlier provided a cooking cost of 1 rupeeper day, which has now been increased to 1.50 rupees per day, with 0.50 paisecontributed by the state – the bare minimum by any country’s standards.

Under the scheme, a cooked meal of a minimum of 300 calories is made avail-able to 12 crore children in over 950,000 schools. The allocation for the middaymeal scheme has gone up from US $ 2.7 billion in 2005–06 to US $ 3.7 billion in2006–07, signaling a rise of over 37 per cent, according to a parliamentary stand-ing committee report (2006) on the scheme.

The 2 per cent education cess levied through the Finance Act 2004 yieldedUS $ 1.08 billion in FY (financial year) 2004–05: in FY 2005–06 it rose to toUS $ 1.5 billion and in 2006–07 it amounted to US $ 1.9 billion, according to theMinistry of HRD (Human Resource Development). The cess is used exclusively tofinance the SSA and the midday meal scheme of the GoI. During 2006–07, fundsamounting to US $ 1.6 billion will be required to construct 500,000 much-neededclassrooms, according to the World Bank.