does the release of davis-bacon certified payrolls … · does the release of davis-bacon certified...

TRANSCRIPT

Does the Release of Davis-Bacon Certified Payrolls

Cause Competitive Harm to Contractors?

Submitted to Torres Law Group

2239 W. Baseline Road

Tempe, AZ 85283

Kevin Duncan, Ph. D.

Senior Economist,

BCG Economics, LLC

Professor of Economics

Colorado State University-Pueblo

Jeffrey Waddoups, Ph. D.

Senior Economist,

Economic Consulting of Nevada, LLC

Professor of Economics

University of Nevada, Las Vegas

August 31, 2014.

About the Authors

Kevin Duncan, Ph.D. Kevin Duncan is Professor of Economics, Hasan School of Business, Colorado State University-Pueblo

where he specializes in labor and regional economics. He received his

Ph.D. from the University of Utah in 1987 and his B.A. from the University

of California, Riverside in 1981. Duncan is the author of over 60 academic

papers and applied regional projects and is the winner of several honors and

awards including the Provost’s Award for Excellence in Teaching, the

Provost’s Award for Excellence in Scholarship, the Outstanding Faculty

Member Award for the Hasan School of Business, the Enterprise Rent-A-

Car Student Choice Award for Excellence in Teaching, the Dean’s Advisory

Council Award for Outstanding Faculty Member, as well as the Dean’s Award for Excellence in

Teaching. He is a nationally recognized expert on prevailing wage laws. His research on this topic has

appeared in leading national and international journals such as Industrial and Labor Relations Review

(forthcoming), Construction Management and Economics, and Industrial Relations (forthcoming). He

has provided expert testimony to the Colorado, Hawaii, and Vermont state legislatures on policy related

to construction labor markets. His research was referenced by the California Senate President pro Tem

(Darrel Steinberg) in support of SB7 (2013) that extends the payment of prevailing wages on public

works to charter cities. He has also provided data and analysis to the Legislative Auditors Office during

the review of Minnesota’s prevailing wage law. He is also a nationally recognized expert on economic

impact analysis and has authored numerous studies that examine the impact of the California

pharmaceutical industry, America’s Cup Races in San Diego, Colorado State Fair, CSU-Pueblo, project

labor and local hire agreements (in California, Colorado, and Hawaii), the installation and operation of

wind energy towers, the nonprofit sector, Amtrak’s Southwest Chief, as well as the impact of the

proposed Colorado Amendment 61. He has served on the Advisory Board for Economic Impact Analysis

of the Colorado Nonprofit Association. He teaches regional economics where his students learn

economic impact analysis.

Jeff Waddoups, Ph.D. Jeff Waddoups received a B.A. degree in 1984 and a Ph.D. degree in 1989 from the University of Utah

in Economics with specializations in labor economics and industrial relations. In

1989 he joined the Department of Economics at the University of Nevada, Las

Vegas where he has developed and taught courses at the graduate and

undergraduate levels in labor economics, research methods, labor law, statistics,

health economics, the economics of discrimination, and macroeconomics. He

has also held adjunct faculty positions at Penn State’s Human Resource and

Employment Relations masters’ program, at Griffith University’s Department of

Management, and at the Helsinki School of Economics Bachelor of Business

Administration Program. He is the author or co-author of 45 academic articles,

and is an internationally and nationally recognized scholar with publications in

some of the top journals in labor economics and industrial relations including in such journals as

Industrial & Labor Relations Review, Industrial Relations, and the British Journal of Industrial

Relations. Waddoups has developed a number of areas of research expertise over his career. Most

recently he has focused on the impact of responsible contracting policies on construction costs. He has

also examined the extent to which low-wage employers are subsidized through uncompensated health

care at public hospitals, the impact of collective bargaining on wages and other outcomes in the hotel-

casino industry, and the impact of unions and collective bargaining on the incidence of job training both

in Australia and the U.S. He currently directs the graduate program for the Department of Economics at

the University of Nevada, Las Vegas.

1

Table of Contents

Introduction/Executive Summary ................................................................................................... 4

Section 1. Construction Worker Labor Costs as a Percent of Total Construction Costs. ............ 10

Introduction ............................................................................................................................... 10

Labor Costs as a Percent of Total Construction Costs for Specialty Trade Contractors Related

to Certified Payroll Requests made by TCLG. ......................................................................... 15

Labor Cost Estimate for Solana Solar Generation Station, Arizona: Insulation Contractors .. 16

Labor Cost Estimate for Energy Systems Integration Facility Project, Colorado: Plumbing,

Heating and Air Conditioning and Electrical Contractors ........................................................ 19

Labor Cost Estimate for Hanford Tank Waste Treatment and Immobilization Plant,

Washington: Plumbing, Heating and Air Conditioning Contractors ....................................... 21

Conclusion of Labor Cost Section ............................................................................................ 22

Section 2: Certified Payrolls, Competitive Harm, and Trade Secrets.......................................... 23

Introduction ............................................................................................................................... 23

Deriving Labor Costs from Certified Payrolls .......................................................................... 25

Change Orders and Certified Payrolls ....................................................................................... 27

Off-Site Work and Certified Payrolls........................................................................................ 30

Labor Estimating Manuals, Bid Preparation, and Labor Costs ................................................. 31

Labor Costs and Total Construction Costs ................................................................................ 32

Differences in Construction Worker Productivity .................................................................... 33

Project Backlogs, Equipment Rentals, and Other Factors Affecting Bids ................................ 39

Incomplete and Inconsistent Labor Cost Data Reported in Certified Payrolls ......................... 42

Trade Secrets and Crew Mix ..................................................................................................... 45

Calculating Labor Costs Based on Incomplete Certified Payrolls ............................................ 50

Conclusion ................................................................................................................................. 51

Section 3: Uneven Reporting of Certified Payrolls ..................................................................... 52

Comparison of the Level of Redaction in Certified Payroll Releases for Selected Federal

Agencies .................................................................................................................................... 52

Section 4: The Availability of Certified Payrolls through FOIA often Results in Workers being

Paid Back Wages .......................................................................................................................... 54

Case 1: Faith Technologies, Inc. ............................................................................................... 54

Case 2: Faith Technologies, Bergelectric Corp., and International Electric, Inc. ..................... 55

2

Case 3: THECO, a division of Tom Hagen Enterprises ............................................................ 56

Case 4: Wilson Electric Services Corporation .......................................................................... 57

Section 5: Low-Bid Contracting is becoming Increasingly Rare in Construction Procurement .. 57

Section 6: Publicly Available Bid Results from State Departments of Transportation. .............. 59

Section 7: The Davis-Bacon Act, Prevailing Wage Policies, and Construction Costs ................. 64

Introduction ............................................................................................................................... 64

First Generation Studies ............................................................................................................ 65

Second Generation Studies: Cost Estimates using Regression Analysis .................................. 66

Third Generation Studies .......................................................................................................... 71

Economic Benefits of Prevailing Wage Laws........................................................................... 72

Related Research: Cost Effects of Project Labor Agreements and Responsible Bidding Policies

................................................................................................................................................... 74

Conclusion ................................................................................................................................. 75

References ..................................................................................................................................... 76

Appendix A………………………………………………………………………………………81

3

List of Tables

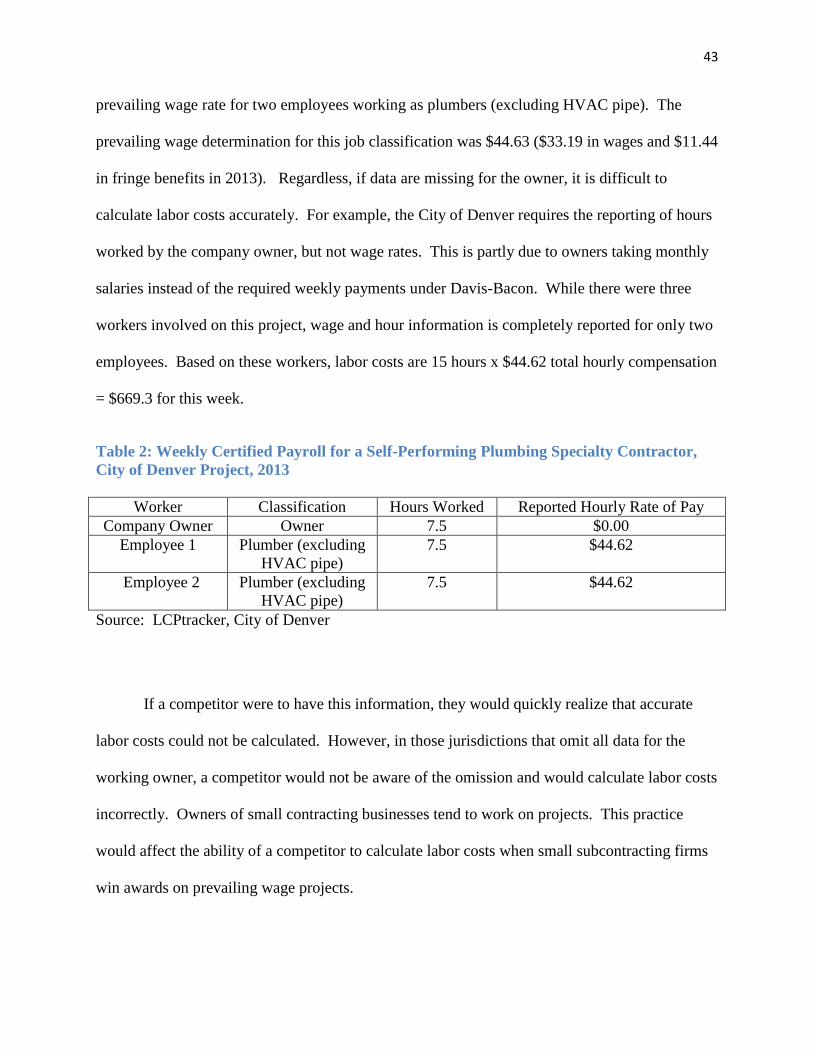

Table 1: Summary of Complete Certified Payroll Data, Electrical Specialty Contractor #1,

Projects for City of Denver, 2008-2009. ....................................................................................... 26

Table 2: Weekly Certified Payroll for a Self-Performing Plumbing Specialty Contractor, City of

Denver Project, 2013 .................................................................................................................... 43

Table 3: Certified Payrolls with Changing Retirement Contributions. Plumbing/HVAC

Specialty Contractor, City of Denver Project, 2013 ..................................................................... 44

Table 4: Percent of Project Labor Hours by Trade. Projects by Mechanical Contractor #2, 2013.

....................................................................................................................................................... 47

Table 5: Order of Applying Workers from Different Trades. Projects by Mechanical Contractor

#2, 2013......................................................................................................................................... 49

Table 6: Certified Payroll Data for Selected Weeks. Project by Mechanical Contractor #2, 2013.

....................................................................................................................................................... 51

Table 7: Publicly Released Bid Results from State Departments of Transportation for Highway

Construction. ................................................................................................................................. 61

Table 8: Information from a CDOT Bid Tabulation, Federal Highway Maintenance Project,

2014............................................................................................................................................... 62

4

Introduction/Executive Summary

The federal Davis-Bacon Act establishes minimum wage and benefit rates for

construction workers employed on federally funded or federally assisted construction projects.

The purpose of the act is to ensure that construction workers will not see their wages and benefits

undercut as a result of government spending practices.1 The infusion of federal dollars into an

area, along with a process that rewards low bids, may depress wages by attracting contractors

from other areas. These contractors may undercut local wage rates by importing lower paid

workers or by offering less pay to local workers. The purpose of the wage floor is to protect

construction workers’ pay and benefits and to establish a level playing field for contractors who

are bidding on federally funded projects. The Department of Labor’s Wage and Hour Division

(WHD) determines local prevailing wage and fringe benefit rates through the conduct of wage

surveys on government contracts covered by the Davis-Bacon Act.2 Data collection for these

surveys is dependent upon the voluntary submission of information from contractors and third

parties that have performed construction work within the geographic scope of the wage survey.

Other federal regulations require all contractors and subcontractors engaged on federally

funded projects to deliver weekly payroll statements to the federal or state agency in charge of

the construction site.3 Payroll records must include the name and address of each laborer and

mechanic, their job classifications, wage and benefit rates, daily and weekly number of hours

worked, deductions, and actual wages paid. These certified payrolls are made available for

1 See The Davis-Bacon Act Protecting Wage Equality Since 1931. Accessed at:

http://www.dol.gov/whd/programs/dbra/Survey/conformancefaq.htm. 2 Davis-Bacon prevailing wage rates are reported at Wage Determinations On-Line.gov. Accessed at:

http://www.wdol.gov/. 3 See Code of Federal Regulations, Title 29, Chapter 1, Secretary of Labor, 29 CFR 3.3 and 3.4. Accessed at:

http://www.dol.gov/dol/cfr/Title_29/Chapter_I.htm.

5

inspection by the federal or state contracting officer and by authorized representatives of the U.S.

Department of Labor.

Other parties may gain access to the certified payrolls by submitting a Freedom of

Information Act (FOIA) request to the appropriate contracting agency.4 Exemption 4 of FOIA

protects against the release of trade secrets and commercial or financial information that is

privileged or confidential. This protection is intended to assure the interests of the submitters of

information and the government by encouraging submitters to furnish accurate and reliable

information. The exemption protects submitters from competitive disadvantages that could

result from the disclosure of the payroll information.

Torres Consulting and Law Group has experienced inconsistent responses to FOIA

requests for certified payrolls from federal contracting agencies. Some agencies routinely redact

requested hours worked and other data based on Exemption 4. Other agencies provide complete

information. Third-party checks of certified payrolls are important for the enforcement of the

Davis-Bacon Act. If Exemption 4 is to be used to prevent the release of certified payroll

information, it is important that the exemption is properly justified.

The present study is a case-specific inquiry into the nature of the construction industry to

determine if the specific claims that have been made by federal agencies, regarding the potential

for competitive disadvantage associated with the release of certified payrolls, are relevant to the

industry. For example, the Department of Energy (DOE) has presented contactor affidavits

indicating that the labor cost data contained in a certified payroll is treated as confidential

information in the construction industry. The primary argument is that disclosing this

4 See the Department of Justice Guide to the Freedom of Information Act. Accessed at:

http://www.justice.gov/oip/doj-guide-freedom-information-act.

6

information would allow competitors to undercut bids on future contracts because labor costs are

a significant element of contractors’ costs and bids.

The claim that labor costs are a significant element of a contractor’s costs is not

supported by numerous peer-reviewed studies and white papers that use data from the Economic

Census of Construction to calculate construction worker labor costs as a percent of total

construction costs. Such studies reveal that labor costs range from 17 to 32 percent of

construction costs, depending on the type of construction. The results of these studies indicate

that construction worker labor costs are one of many factors that make up a bid, that the labor

cost information included in a certified payroll is insufficient to undercut bids, and that releasing

this information would not cause competitive harm to a contractor. A complete evaluation of

this issue is presented in Section 1 of the report.

The contractor affidavits presented by the DOE were considered sufficient evidence to

rule that the payroll information, if released, could be used by competitors to undercut future

bids. This decision was made in the absence of a detailed examination of certified payrolls. This

study conducts such an examination. In Section 2 certified payroll data for projects covered by

the City of Denver prevailing wage policy are examined. These data illustrate how numerous

factors limit the usefulness of the payroll information from one project in estimating the bid-

price of another project. For example, change orders and off-site work cause distortions between

the estimate of labor hours used in bid preparation and the labor hours reported in a certified

payroll. Qualitative and size differences between projects render the labor cost information from

one project of little use in undercutting the bid on another. The hours needed to complete a

project vary with the skills and experience of construction workers, but information on labor

7

productivity is not included in certified payrolls. Changes in contractor bid behavior, project

backlogs, and economic conditions contribute to changing bids from project to project.

Incomplete and selected certified payrolls contribute to inaccurate estimates of project labor

costs. These and other factors discussed in Section 2 illustrate that bids are moving targets from

project to project and that too much uncertainty limits the use of payroll information in bid

undercutting.

Another concern is that the job classification and hours worked data contained in a

certified payroll may reveal confidential information (trade secrets) about how a contractor

employs workers from different trades in particular ratios that allows the company to complete

projects efficiently and at a low cost. Our examination of certified payrolls illustrates how, even

among very similar projects, the ratios in which workers from different trades are employed

vary. Another possible concern is that a contractor applies labor in a particular order over the

course of a project in a unique manner that is efficient and is a trade secret. However, our

examination of certified payrolls indicates that, even on similar projects, the order of labor varies

from week to week and likely responds to factors such as the demands of the project schedule,

working around the schedule of other contractors, and work on other projects, etc. This analysis

demonstrates that information included in a certified payroll does not reveal trade secrets

regarding the order and application of workers.

As indicated above, third-party audits of certified payrolls are an important tool for

enforcing prevailing wage requirements under the Davis-Bacon Act. When information vital to

the enforcement of the law is redacted, verification of compliance by third parties becomes

impossible. Section 3 of the report provides evidence of the uneven compliance. The results

suggest that most federal agencies release the information that is required to adequately

8

determine whether contractors are in compliance with Davis-Bacon prevailing wage

requirements, with the notable exception of the Department of Energy. If construction

contractors were truly fearful of harming their competitive position because of the release of

certified payrolls, one would expect that there would be significantly more redactions among

other agencies as contractors were trying to protect their competitive position, and that there

would not be a concentration of noncompliance found in only one agency.

The inability to enforce Davis-Bacon prevailing wage requirements is not

inconsequential. Violations often leave workers with substantially lower wages and benefits

than they are entitled to. Section 4 details several examples of how the release of certified

payrolls allowed third-party auditors to uncover violations that resulted in penalties and back-pay

for workers.

The release of certified payrolls through a FOIA request becomes more useful to a

possible competitor to the extent that labor costs are an important factor in winning a bid, which

is mostly the case in situations where the lowest bid prevails. If bids are won or lost based on

something other than low bid, however, knowledge of labor costs becomes less important.

Section 5 cites evidence that low bid contracting is less prevalent in the private sector compared

to the public sector, and is becoming less important in the public sector, which is moving toward

best value contracting. The implication is that in much of the construction industry, knowledge

of a competitors labor costs as found in certified payrolls will not be particularly helpful in

gaining competitive advantage for the purpose of winning bids.

In many instances detailed information about construction bids are routinely released to

the public. For example, state departments of transportation provide detailed bid results including

9

the name and bid of the winning contractor. Section 6 shows that many departments of

transportation release to the public detailed bid-price information on specific items included in a

highway project. This information can be used by contractors to determine how much they lost

the bid by, and the specific areas of the bid that require changes to become more competitive.

This information is far more accurate and useful in obtaining information of competitor’s bids

than the labor cost information that is reported in a certified payroll. However, this information

is routinely released without apparent harm to contractors.

Finally, Section 7 contains a review of the literature regarding the effect of federal, state,

and municipal prevailing wage policies on total construction costs, bid competition, and local

economies. The preponderance of the research indicates that prevailing wage requirements are

not associated with increased construction costs. Supplemental information indicates that

projects covered by prevailing wage standards are characterized by increased productivity and

efficiency that is associated with stable costs. Projects covered by prevailing wage laws are not

less competitive than projects that are not covered by the policy. Economic impact studies

indicate increased spending and higher levels of economic activity in those jurisdictions with

prevailing wage policies. Also included in Section 7 is a summary of academic research detailing

the impact of project labor agreements and responsible contracting policies on construction costs.

Overall, the results of this study indicate that the justifications typically employed for the

use of FOIA Exemption 4 are not appropriate for the construction industry.

10

Section 1. Construction Worker Labor Costs as a Percent of Total

Construction Costs.

Introduction

In Torres Consulting and Law Group (TCLG) v. Department of Energy (DOE) 2013,

subcontractors involved in the Energy Systems Integration Facility (ESIF) construction project

located in Golden, Colorado submitted affidavits indicating that disclosing the wage and hour

data reported in a certified payroll request would be a competitive disadvantage.5 Multiplying

hourly wage rates by the number of hours worked yields labor costs, or what these

subcontractors refer to as “labor production rates.” The subcontractors assert that “labor

production rates are treated as confidential information in the construction industry and that

disclosing them would allow to (sic) competitors to underbid the contractors when competing for

work because labor production rates are a significant element of a contractor’s price.”6 These

affidavits were considered sufficient evidence for Judge Wake to rule in DOE’s favor.7

The claim that construction worker labor costs are a “significant element” of total

construction costs is at variance with publicly available information that has been reported in

peer-reviewed research and in white papers addressing the effect of prevailing wage laws on

building costs. These studies, which are reviewed below, indicate that labor costs range between

17% and 32% of the total cost of construction. These data reveal that other factors such as the

costs of materials, supplies, fuels, overhead, profit, etc. make up between 83% and 68% of

construction costs. If labor costs are at best a minor element of overall costs, then even knowing

5 See United States District Court for the District of Arizona, Torres Consulting and Law Group, LLC, Plaintiff, v.

Department of Energy, Defendant. No. CV-13-00858-PHX-NVW. Document 24 Filed 11/27/13, p. 7. 6 Ibid.

7 Ibid., p. 8.

11

them perfectly will be of little use to competitors seeking to undercut bids. In his decision, Judge

Wake indicated that “the essence of this dispute is whether the labor production rate is just one

of the many variables that make up a bid, or if the labor production rate is such a significant

piece of a bid that release of the data would essentially reveal the bid price, causing substantial

competitive harm.”8 The studies examining labor costs as a percent of total construction costs

provide consistent and clear evidence that labor costs are just one of the many variables that

make up a bid and that releasing this information will not cause competitive harm.

Azari-Rad, Phillips and Prus (2003) report that, for the overall U.S. construction industry,

construction worker labor costs were 30% of total construction costs in 1982 and 26% in 1992.

While the change over this period may be influenced by that stage of the business cycle, other

data discussed below indicates that labor costs have continued to fall as a percent of construction

costs over time. These authors define labor costs as including construction worker wages,

benefits, and payroll taxes. Total construction costs are defined as material and labor costs and

exclude land purchases and architect fees. The data used in the study by Azari-Rad, Philips, and

Prus was obtained from the Economic Census of Construction.

The U.S. Census Bureau conducts a survey of construction contractors in every state

regarding industry employment, compensation, value of construction, expenditures on materials,

and supplies, etc.9 The survey is conducted every five years.

10 Data from the 2012 survey have

not been released. Information from the 2007 survey is the most recent available. The

Economic Census of Construction (hereinafter, ECC) reports data by geographic area, type of

8 Ibid.

9 See the Construction Geographic Area Series: Detailed Statistics for Establishments: 2007. Accessed at:

http://factfinder2.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ECN_2007_US_23A1&prodTyp

e=table. 10

For an explanation of the sampling methodology used in the Economic Census of Construction see:

http://www.census.gov/econ/census/pdf/2007_meth/meth_23.pdf.

12

construction (residential, commercial, industrial, and highway, etc.), and for specialty trade

contractors (plumbing, and electrical, etc.).11

Therefore, it is possible to determine labor costs as

a percent of total construction costs in a state, a particular sector of the construction industry, and

to track changes over time.

Other studies have also used the ECC to measure labor costs as a percent of total

construction costs. For example, Philips (2014) uses data for Kentucky to measure differences

by sector and over time. Data indicate that construction worker labor costs as a percent of total

construction cost decreased steadily between 1977 and 2007 in the overall construction industry

in this state. Labor costs were approximately 30% of total costs in 1977 and 21% in 2007. In

this study labor costs include construction worker wages, benefits, and payroll taxes.

Construction costs are based on building costs, excluding land acquisition costs, construction

design and oversight services not provided by construction contractors. Philips also observes

that construction worker employment, as a percent of total contractor employment, has decreased

from 87% in 1972 to 73% by 2007. Philips attributes the trends in labor costs and employment

to technological change in the industry, increased construction worker productivity, and the

greater use of white-collar labor as construction contractors have expanded the array of services

they provide. These are national trends in the construction industry with effects that are not

isolated to Kentucky. Philips also reports labor costs for different sectors of the Kentucky

construction industry in 2007. For example, labor costs are 17% of total costs in for highway,

11

The classification of establishments covered in the 2007 Economic Census of Construction uses the industry

definitions in the North American Industry Classification System (NAICS). In the NAICS system, an industry is

generally defined as a group of establishments that use similar processes. The numeric coding system provides

progressively narrower definitions of establishments with similar processes through successive additions of

numerical digits. For example, the NAICS code of 23 identifies and covers all construction establishments and six-

digit codes identify specific types of establishments involved in highway, street, and bridge construction or in

particular specialty trades.

13

street, and bridge construction and 20% for other civil engineering construction. For all projects

funded by state, county, and municipal governments, labor costs are 20% of total construction

cost.

Philips also points out several reasons why some contractors may assert that their labor

costs are higher than the information obtained from the ECC. First, contractors may not

distinguish between blue-collar construction worker labor costs and the labor costs of all

employees (including white-collar workers). Second, if the contractor is a subcontractor, they

may not be responsible for, or aware of the costs of materials, fuels, and other supplies used on

the project. Third, the contractor may present data from an addition/renovation project that

involved primarily construction labor (and did not involve significant material or white-collar

labor costs). Finally, Philips points out that when contractors consider their labor costs they do

not typically consider their profit as part of total construction costs. While profits are a return on

the contractor’s investment, this income is part of the cost paid by the project owner. For these

four reasons, Philips concludes that data from the U.S. Economic Census of Construction are

more reliable than the testimony of individual contractors regarding construction worker labor

costs as a percent of total building costs. We agree with Professor Philips that the ECC is the

most reliable data available to obtain measures of labor and total costs. The data reported by the

ECC is based on information obtained from a large number of contractors, is publicly available,

and is collected by an agency that is objective with respect to the issues involved in legal matters

related to certified payroll requests.

Other researchers have used the ECC for different states and industries and have provided

labor cost estimates that are comparable to those reported by Philips. For example, Duncan

(forthcoming) reports that labor costs were approximately 21% of total costs for highway, street,

14

and bridge construction in Colorado in 2007. The ECC does not report labor costs as a percent

of total costs. This ratio must be calculated based on other ECC data. In the study by Duncan,

labor cost as a percent of total construction cost is derived by dividing total construction worker

payroll, plus proportionally allocated total fringe benefits, by the net value of construction

work.12

The net value of construction is based on the value of work completed by a contractor,

less the value of work subcontracted to other contractors.13

This measure of the value of

construction work is used as a measure of total construction costs because it is the price the

project owners paid for the work completed. Price can be thought of as the ‘cost’ incurred by the

project owner. The net value of construction is a broader measure of total costs than contractor

bid prices since this measure of the value of construction includes the costs associated with add-

on charges and follow-up maintenance. In the current study we use Duncan’s method to

determine labor costs as a percent of total construction costs as it is the most accurate way to

compare total construction worker payroll with contractor building costs (minus any work

subcontracted out).14

12

The ECC defines construction worker payroll as the gross earnings paid in the reporting year to all construction

workers on the payroll of construction establishments. It includes all forms of compensation such as salaries, wages,

commissions, dismissal pay, bonuses, and vacation and sick leave pay, prior to deductions such as employees' Social

security contributions, withholding taxes, group insurance, union dues, and savings bonds. See Construction:

Geographic Area Series: Detailed Statistics for Establishments: 2007. Accessed at:

http://factfinder2.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ECN_2007_US_23A1&prodTyp

e=table. 13

The ECC defines the net value of construction as the receipts, billings, or sales for construction work done by

contractors, less the value of construction work subcontracted to others. The net value of construction does not

include contractor business receipts from retail and wholesale trade, rental of equipment without operator,

manufacturing, transportation, legal services, insurance, finance, rental of property and other real estate operations,

and other nonconstruction activities. Receipts for separately definable architectural and engineering work for others

are also excluded. Nonoperating income such as interest, dividends, the sale of fixed assets, and receipts from other

business operations in foreign countries are also excluded. See Construction: Geographic Area Series: Detailed

Statistics for Establishments: 2007. Accessed at:

http://factfinder2.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ECN_2007_US_23A1&prodTyp

e=table. 14

Some may argue that the value of construction work added should be used as the measure of construction costs.

In the ECC, this measure of construction activity is equal to value of business done, less costs for construction work

15

Labor Costs as a Percent of Total Construction Costs for Specialty Trade

Contractors Related to Certified Payroll Requests made by TCLG.

In 2012 and 2013, TCLG made several requests for certified payroll data for DOE

projects in Arizona, Colorado, and Washington. These requests were made for work completed

by electrical, insulation, and plumbing/HVAC specialty trade contractors. In this section of the

study, we report construction worker labor costs as a percent of total construction costs for these

specialty trade contractors in the relevant states. The data, obtained from the ECC and reported

below, indicate that construction worker labor costs range between 26% and 32% of total

construction costs for applicable specialty trade contractors and states. This information is

compared to the DOE’s rationale for not releasing wage and hour data. The DOE claims that

the release of hours worked information would result in financial harm to the DOE and

competitive harm to participating contractors if competing contractors used the wage and hour

information to undercut the business of contractors participating on DOE projects.15

The threat

of this damage may discourage participation in future DOE bid offerings. The reduction in bid

competition would result in higher project costs for DOE. The range in labor costs described

above indicates that it is improbable that a competing contractor, with access to the certified

payroll information, could derive sufficient information to undercut the bids of participating

contractors. Because labor costs are such a low percent of total construction costs for the types

of specialty trade contractors involved in TCLG requests for certified payroll information, it is

unlikely that the release of this information would alter bid competition for DOE projects in a

way that would affect costs.

subcontracted out to others, and costs for materials, components, supplies, and fuels. This is a measure of the value

created by construction workers, but is not a measure of costs since materials, supplies, etc., are omitted. 15

See correspondence between Torres Consulting and Law Group and U.S. Department of Energy accessed at:

http://s3.documentcloud.org/documents/686508/az-2-2013cv00744-complaint-attachment-1.txt.

16

Labor Cost Estimate for Solana Solar Generation Station, Arizona: Insulation

Contractors

In June of 2012, Torres Consulting and Law Group requested certified payroll

information regarding the Solana Solar Generation Station located in Gila Bend, Arizona. The

request was made on behalf of the Heat and Frost Insulators Local 7. The requested materials

included three weeks of the most recent certified payroll for Petrochem Insulation Inc. and Brand

Energy Solution Infrastructure (A.K.A Brand Energy Services).16

The DOE response to the certified payroll request states that the information withheld

“includes payroll information such as individual employee's hours worked, net and gross wages,

which could be used to determine total labor costs. Release of this type of information could

cause substantial financial and competitive harm to this project, as competing sub-contractors

could utilize this information to respond to the bid request which would result in a less

competitive process now and in the future and result in a substantial increase in the cost of the

project. Similarly, the release of such information could result in substantial harm to the

competitiveness of the contractor in bidding future projects.”17

Data from the ECC can be used to derive a measure of labor costs as a percent of total

construction costs for insulation specialty trade contractors, like those involved in the Solana

Solar project in Arizona.18

Based on the definitions of labor and total construction cost described

16

Ibid. 17

Ibid., p. 6. 18

The type of workers and contractors involved in this project are best described by NAICS code 238310 for

drywall and insulation specialty contractors.

17

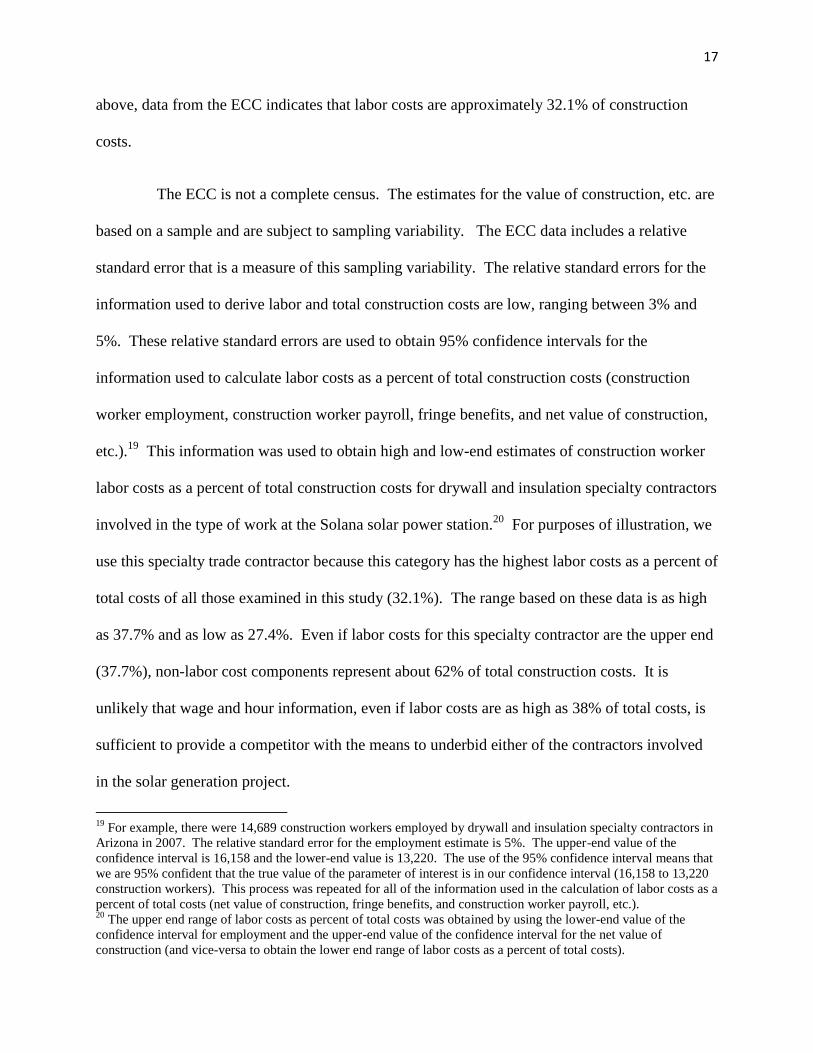

above, data from the ECC indicates that labor costs are approximately 32.1% of construction

costs.

The ECC is not a complete census. The estimates for the value of construction, etc. are

based on a sample and are subject to sampling variability. The ECC data includes a relative

standard error that is a measure of this sampling variability. The relative standard errors for the

information used to derive labor and total construction costs are low, ranging between 3% and

5%. These relative standard errors are used to obtain 95% confidence intervals for the

information used to calculate labor costs as a percent of total construction costs (construction

worker employment, construction worker payroll, fringe benefits, and net value of construction,

etc.).19

This information was used to obtain high and low-end estimates of construction worker

labor costs as a percent of total construction costs for drywall and insulation specialty contractors

involved in the type of work at the Solana solar power station.20

For purposes of illustration, we

use this specialty trade contractor because this category has the highest labor costs as a percent of

total costs of all those examined in this study (32.1%). The range based on these data is as high

as 37.7% and as low as 27.4%. Even if labor costs for this specialty contractor are the upper end

(37.7%), non-labor cost components represent about 62% of total construction costs. It is

unlikely that wage and hour information, even if labor costs are as high as 38% of total costs, is

sufficient to provide a competitor with the means to underbid either of the contractors involved

in the solar generation project.

19

For example, there were 14,689 construction workers employed by drywall and insulation specialty contractors in

Arizona in 2007. The relative standard error for the employment estimate is 5%. The upper-end value of the

confidence interval is 16,158 and the lower-end value is 13,220. The use of the 95% confidence interval means that

we are 95% confident that the true value of the parameter of interest is in our confidence interval (16,158 to 13,220

construction workers). This process was repeated for all of the information used in the calculation of labor costs as a

percent of total costs (net value of construction, fringe benefits, and construction worker payroll, etc.). 20

The upper end range of labor costs as percent of total costs was obtained by using the lower-end value of the

confidence interval for employment and the upper-end value of the confidence interval for the net value of

construction (and vice-versa to obtain the lower end range of labor costs as a percent of total costs).

18

There may be instances where labor costs as a percent of total construction costs for a

specialty trade contractor may deviate from the average. These instances may occur when

specialty contractors are, and are not responsible for the equipment, materials, and supplies, etc.,

that are used on a project. For example, if a project (Project A) involves the installation of

expensive equipment that requires very little labor to install, and if the equipment cost is

included in the specialty contractor’s bid, labor costs may be a relatively low percent of total

project costs. On the other hand, consider Project B where the cost of equipment is included in

the general contractor’s bid and the specialty subcontractor is only responsible for the installation

of the equipment. In this case, labor costs may be a high percent of the project cost for the

specialty contractor. Because of differences in the composition of the bids for projects A and B,

the labor cost estimate of one of these projects would not be useful in estimating the bid-price of

the other, even though these projects may be very similar with respect to the installation of

equipment. 21

The labor costs of Project A would be useful in estimating the labor costs of a

project that is very similar to A. But, characteristics differ from project to project and it is

unlikely that a future project will involve the installation of the same equipment with the same

price. In the next section of this report, we illustrate the various ways projects differ and how

these differences limit the usefulness of the labor costs information in certified payrolls in

undercutting bids.

21

The low relative standard error for the net value of construction for specialty contractors (for example, 4% for

drywall and insulation contractors in Arizona, versus 1% for all Arizona construction) suggests that extreme cases

like projects A and B are rare. The higher relative standard error for specialty trade contractors suggests a greater

dispersion around the estimate of the net value of construction. This suggests a wider range in the net value of

construction, perhaps due to project differences in equipment costs described above. However, if these cases were

common, the relative standard error for specialty contractors would be much larger.

19

Labor Cost Estimate for Energy Systems Integration Facility Project, Colorado:

Plumbing, Heating and Air Conditioning and Electrical Contractors

In July of 2012, TCLG filed a FOIA request with the DOE regarding the Energy Systems

Integration Facility construction project located in Golden, Colorado.22

Specifically, the payroll

request was made for project subcontractors M Tech Mechanical Technologies Group and

Diamond Fire Protection. TCLG received redacted payroll information based on DOE’s

rationale that “trade secrets and commercial or financial information obtained from a person are

privileged or confidential.”23

Services offered by Diamond Fire Protection and M Tech Mechanical Technologies

Group include plumbing, heating, ventilation, and air conditioning. Data from the ECC for

Colorado indicates that labor costs for this specialty trade are approximately 25.8% of total

construction costs.24

Certified payroll requests were also submitted for two electrical specialty

trade contractors (Encore Electrical and Weifield Group Contractors) that also worked on the

ESIF project.25

TCLG also received redacted payroll information regarding these requests.26

ECC data indicate that labor costs are approximately 27.8% of total construction costs for this

type of specialty trade contractor in Colorado.

The DOE response to the certified payroll request by TCLG stated that “Encore Electric

has substantial commercial interests in protecting the release of this information, since the public

release of this information could be used by competitors to undercut the bid prices of Encore

22

See United States District Court for the District of Arizona, Torres Consulting and Law Group, LLC, Plaintiff, v.

Department of Energy, Defendant. No. CV-13-00858-PHX-NVW. Document 24 Filed 11/27/13, p. 2. 23

Ibid. 24

The NAICS code for plumbing, heating, and air conditioning contractors is 238220. 25

The NAICS code for electrical contractors is 238210. 26

Based on information provided by TCLG personnel.

20

Electric in the future resulting in substantial harm to the competitive position of Encore

Electric.”27

Since labor costs are a low percent of total construction costs for electrical specialty

trade contractors in Colorado, it is very unlikely that releasing payroll information would be

associated with a competitive disadvantage for these electrical contractors.

In TCLG v. DOE 2013, the DOE submitted affidavits from Diamond Fire Protection and

M Tech Mechanical Technologies Group stating that “labor production costs could be calculated

by multiplying the government’s labor rate by the hours worked. They attest that labor

production rates are treated as confidential information in the construction industry and that

disclosing them would allow competitors to underbid the contractors when competing for work

because labor production rates are a significant element of a contractor’s price.”28

In his

decision, Judge Wake agreed with these conclusions, stating that “substantial competitive harm

occurs when disclosure would allow competitors to estimate and undercut a contractor’s bid”

and: “a likelihood of substantial competitive harm is often found when the disclosed information

would give a competitor conclusive insight into how it could modify its business to undercut

another’s.”29

Data from the ECC indicate that labor costs for plumbing, heating, and air

conditioning specialty contractors in Colorado are approximately 26% and do not represent a

“significant element of a contractor’s price.” Since labor costs are a relatively low percent of a

contractor’s costs, the information contained in a certified payroll request is insufficient to

provide competitors with sufficient information to undercut a contractor’s bids.

27

Correspondence between Torres Consulting and Law Group and U.S. Department of Energy, August 7, 2012. 28

See United States District Court for the District of Arizona, Torres Consulting and Law Group, LLC, Plaintiff, v.

Department of Energy, Defendant. No. CV-13-00858-PHX-NVW. Document 24 Filed 11/27/13, p. 9. 29

Ibid., p. 6.

21

In his decision, Judge Wake also indicated that “substantial competitive harm is less

likely to be found when the information redacted provides insight into only one of several

variables a competitor needs to gain an advantage.”30

The data for the types of specialty trade

contractors involved in the ESIF facility indicate that labor costs are indeed, “one of several

variables a competitor needs to gain an advantage.” Consequently, it is unlikely that substantial

competitive harm would have occurred with the release of the certified payroll information.

Labor Cost Estimate for Hanford Tank Waste Treatment and Immobilization

Plant, Washington: Plumbing, Heating and Air Conditioning Contractors

In August of 2013, TCLG submitted a FIOA request regarding certified payroll records

for the Hanford Tank Waste Treatment and Immobilization Plant located in Hanford,

Washington.31

The request was made on behalf of the United Association Local Union No. 598.

The payroll information was not provided. The DOE responded that the requested information

was the property of the contractors.32

Data from the ECC for Washington state indicate that

labor cost as a percent of total construction costs for plumbing, heating, and air conditioning

specialty contractors was 26.4% in 2007.

30

Ibid., p. 7. 31

See correspondence between TCLG and the U.S. Department of Energy. Accessed at:

http://www.hanford.gov/files.cfm/FOI%202013-01446.Response%20Letter.pdf. 32

Information provided by TCLG personnel.

22

Conclusion of Labor Cost Section

Various studies that use data from the Economic Census of Construction indicate that

construction worker labor costs are a low percent of total construction costs. This is the case for

labor costs in the aggregate construction industry, individual states, or particular types of

construction. Additional evidence indicates that labor costs as a percent of total construction

costs have decreased over time. Data specific to specialty trade contractors in states with recent

DOE projects uniformly indicate that labor costs are also a low percent of construction costs,

ranging between 26% and 32% in these cases. These estimates are based on data from 2007.

Given the long-term trend of decreasing labor costs in the construction industry, it is likely that

these costs have decreased further since 2007.

This evidence casts doubt on claims that if certified payroll information is released,

competitors would be able to estimate and undercut a contractor’s bid, bid competition on DOE

projects would be reduced, and costs of DOE projects would increase. Our empirical

examination of the specialty trades involved in recent DOE projects indicates that labor costs do

not represent a significant element of a contractor’s price, but should be considered one of many

variables that make up a contractor’s bid. Our empirically-based, case-specific inquiry into the

nature of the construction industry indicates that the rationale used to prevent the release of

certified payroll information is unfounded.

23

Section 2: Certified Payrolls, Competitive Harm, and Trade Secrets

Introduction

In this section of the report we present summary data from complete certified payrolls to

examine the implications regarding the release of this information and competitive harm. In

Torres Consulting and Law Group (TCLG) v. Department of Energy (DOE) 2013, the DOE

presented affidavits by contractors regarding the sensitivity of certified payroll information.

These affidavits were considered sufficient evidence to rule that the payroll information, if

released, could be used by competitors to undercut future bids. This decision was made in the

absence of a detailed examination of certified payrolls. This section of the report conducts such

an examination. The advantage of this analysis is that we are able to gain insight into the

possible effects of releasing the information through an examination of certified payrolls from

the beginning to the end of a project, payroll data for different projects for the same contractor,

as well as payroll data when different job classifications are involved in a project.

Payroll information was collected from LCPtracker archives for the City of Denver.

Public construction funded by the City and County of Denver is governed by a prevailing wage

standard.33

This policy closely follows the Davis-Bacon Act with respect to project value

threshold and apprenticeship programs, etc. Denver prevailing wage and benefit rates are based

on Davis-Bacon wage determinations. Union wage and benefit rates prevail for all of the job

classifications examined below.34

33

See Ordinance Section 20-76 at: http://www.denvergov.org/Portals/741/documents/PW_General/20-76.pdf. 34

See http://www.denvergov.org/auditor/DenverAuditor/PrevailingWage/tabid/443008/Default.aspx.

24

LCPtracker is labor compliance software used for prevailing wage reporting.35

Certified

payroll reports, based on federal, state, and municipal prevailing wage standards, are created for

public works construction. The certified payroll reporting for City of Denver projects contains

the same information included in form WH-347 that is used for federal projects covered by the

Davis-Bacon Act. The information contained in LCPtracker certified payroll reports includes

employee and contractor identification, job classification, hours worked each day of the reporting

week, wage rate, fringe benefits for the project, and payroll information for other work

completed during the reporting week. The City of Denver uses the LCPtracker software for city

and federal prevailing wage reporting within its jurisdiction. Contractors use the software to

submit weekly payroll reports and certification documents. In the analysis that follows,

information that identifies individual employees and contractors, specific projects, and specific

project dates are omitted. The analysis is restricted to certified payrolls for nonunion contractors.

There are thousands of certified payrolls within the LCPtracker archives for Denver

public works projects. Our analysis is not a comprehensive examination of all project types.

Instead, our analysis is based on the same types of specialty trade contractors included in the

section of the report on labor costs (electrical and plumbing/HVAC). This focus allows the

information on percent labor costs to be integrated into the discussion of how releasing payroll

data may be associated with competitive harm. We also limit the analysis to an examination of

building construction (omitting heavy and highway projects). In the subsections that follow, we

illustrate the implications regarding the use of payroll information by a competitor to undercut

the future bids of a participating contractor. We also discuss the implications of the use of the

job classification and hours worked data to reveal trade secrets. These data may be used to

35

See http://www.lcptracker.com/.

25

determine how workers from different classifications are employed in ratios that may reveal a

contractor’s unique ‘recipe’ for construction.

Deriving Labor Costs from Certified Payrolls

In this section we present summary data from four complete certified payrolls for an

electrical specialty contractor who completed these projects for the City of Denver between 2008

and 2009. These data are reported in Table 1. Projects 1, 2, and 3 are relatively small and were

completed in approximately the same number of hours (ranging from 60 to 63.5 hours). Projects

1 and 2 are both electrical repair projects. Project #1 involved work on an existing electrical

system in a historic building.36

Project 2 required repairs to mechanical equipment. Project 3

involved the installation of mechanical equipment. Project 4 was a large demolition project that

required approximately 590 labor hours to complete.

36

The LCPtracker records for Denver do not contain detailed job descriptions. These are available from the city,

but require a Colorado Open Records Act request to obtain them. Time limits for this study do not allow for this

process. The descriptions included in the records are sufficient to provide information on general differences

between the projects.

26

Table 1: Summary of Complete Certified Payroll Data, Electrical Specialty Contractor #1,

Projects for City of Denver, 2008-2009.

Project Total

Project

Hours

Prevailing

Wage &

Fringe

Hours at

Prevailing

Wage

Hours and Wages Above

Prevailing Wage

Hours and Wages/

Apprentices

Project 1

(repair work)

60.0 $30.00

($10.82)

60.0 – –

Project 2

(repair work)

63.5 $30.00

($10.82)

54.5 4 hours at $40.82 ($10.82)

5 hours at $33.32 ($10.82)

–

Project 3

(non-repair

project)

63.0 $30.00

($10.82)

57.0 – 6 hours at $11.63

($2.63)

Project 4

(demolition

project)

588.5 $28.91

($10.33)

385.5 – 203 hours at rates

ranging between

$12.00 and $14.65

($2.53 and $4.64)

Source: LCPtracker, City of Denver.

The first three projects (projects 1, 2, and 3 in Table 1) were started in early summer of

2009 and ended by early fall of the same year. The fourth and larger project (Project 4) was

started and completed before the other three jobs (with a start date in the fall of 2008, finishing at

year’s end). The contractor reported the payment of applicable prevailing wage rates for the

corresponding job classifications. Building electricians and electrician apprentices were the only

workers employed on all of these projects. The prevailing wage and benefit rate for electricians

engaged on projects 1-3 was $30.00 hourly wage, plus $10.82 in fringes in late 2009.37

Total

hourly prevailing compensation was $40.82 in this period ($30.00 plus $10.82). In 2008, when

Project 4 was conducted, the prevailing wage for electricians was $28.91 ($10.33 in fringes).

Consequently, total compensation was $39.24 an hour ($28.91 plus $10.33). The hourly

compensation for apprentices ranged between $11.63 and $14.65 (with $2.53 to $4.64 in fringe

benefits) over the period.

37

See http://www.denvergov.org/auditor/DenverAuditor/PrevailingWage/tabid/443008/Default.aspx.

27

Calculating labor costs for Project 1 from the information reported in the certified payroll

is straight forward. This project involved 60 hours of labor time. All workers earned the same

hourly compensation rate and only one job classification was employed. Consequently, labor

cost equals $2,449.20 ($40.82 x 60 hours). The argument used by the DOE is that if a

competitor were to gain access to this information, it could be used to undercut future bids by

this contractor. This could be the case if a future project is similar to Project 1 in terms of repair

work on an existing electrical system in a building with constraints imposed by historic structure

status and if construction worker skills, experience, and productivity are constant for this and the

competing contractor. But, information presented below indicates that change orders and

differences in off-site work cause distortions between the labor hour estimates included in bids

and the labor hours reported in a certified payroll that are needed to complete a project. Also,

projects differ in terms of size and technical requirements. The quantity and quality of

construction labor also varies from project to project. Construction worker skills and experience

vary within a contracting firm and between firms. These and other factors illustrate the difficulty

in using labor costs from one project to undercut a bid on another project.

Change Orders and Certified Payrolls

One fundamental problem with using labor costs from one project to undercut bids on

future projects has to do with differences in the labor hour estimates used in preparing a bid for a

project and the hours needed to complete the project. For example, if a competitor’s bid on

Project 1 was based on an expected 70 hours of labor, and Contractor #1 (that was awarded the

project) finished the job in 60 hours; this implies that the competitor needs to reduce labor hours

28

on a future bid by more than 10 hours (14.3%) to undercut Contractor #1 on a comparable future

project.38

The problem with this approach is that differences exist between the labor hour

estimates used in calculating the bid for the project and the hours actually expended to complete

the work, particularly on repairs to an existing electrical system in a historic structure where

uncertainty exists regarding the extent of the work. For example, Contractor #1 may have based

its winning bid on an expected 50, 60, 70, or 80 labor hours, but finished in 60 hours. If the

labor hours required to complete a project differ from the labor hours used in the preparation of

the bid, the hours reported in a certified payroll are of little use in bid undercutting. One source

of the difference between the labor hours estimate used in the preparation of the bid and the

hours needed to complete the project is change orders.

Change orders involve adding or deleting work that was originally specified in the

contract. These are common in the construction industry with the typical commercial project

involving 56 change orders.39

Philips, Mangum, Waitzman, and Yeagle’s (1995) examination of

highway construction projects in Utah indicates that, on average, change orders added two

percent to the winning bids of projects covered by the state’s prevailing wage policy.40

On the

other hand, change orders were more than three times higher on highway projects that were not

covered by Utah’s prevailing wage standard. In an examination of new school construction in

Massachusetts, Bellman, et al. (2010) report that change orders and other costs increase winning

bids by an average of 6.2%.

38

This ignores the role of material and supply costs in bid costs. This issue is pursued below. 39

See Kent Lang, “The Trouble with Change Orders.” Accessed at: http://www.lang-

baker.com/publications/constructionadvisor/changeorders.htm. See also “Common Causes of Change Orders” by

Juan Rodriguez, accessed at: http://construction.about.com/od/Claims-Management/a/Common-Causes-For-A-

Change-Order.htm. 40

The Utah state-level prevailing wage law was repealed in 1981. See Dollar Threshold Amount for Contract

Coverage, U. S. Department of Labor. Accessed at: http://www.dol.gov/whd/state/dollar2011.htm#1.

29

The changes in labor hours associated with change orders will be reflected in certified

payrolls. For example, if change orders add hours of work to a project, the labor costs reported

in a certified payroll will also increase. The final cost of the project will also increase and rise

above the level of the initial bid. While information on the bids of all participating contractors is

often available after the completion of a project, the costs associated with change orders are

rarely reported and are very difficult to obtain.41

When change orders add to the final cost of a

project, it is very difficult to accurately use the labor cost data in a certified payroll to estimate

the winning contractor’s bid. A competitor with a complete payroll record may be able to

calculate the labor costs required to complete the project, but the competitor will not be able to

determine how much change orders caused the final costs to exceed the winning bid. Also, a

competitor will not be able to distinguish between the hours reported in the certified payroll that

were accounted for in the original bid and the hours dedicated to change orders. In other words,

if change orders add to project costs and to hours of work, and if a competitor used the certified

payroll to attempt to undercut on a future bid, the competitor’s bid would be too high. This is

due to basing the bid undercut on the hours required to complete the project, not the hours

estimated to win the bid. The opposite is the case for change orders that are associated with

fewer hours of work. In this case the reduction in hours needed to finish the job would be lower

than the labor hours included in the bid. Due to the prevalence of change orders in the

construction industry, certified payrolls are very unreliable for the purpose of undercutting bids.

41

See Duncan (forthcoming).

30

Off-Site Work and Certified Payrolls

The labor cost information reported in a certified payroll will also vary depending on how

the off-site work for a project is conducted.42

For example, the wages of workers employed by a

contractor at an off-site fabrication facility are not covered by Davis-Bacon prevailing wages if

the location and operation of the fabrication plant are not dedicated exclusively to the federal

project. In these cases, the wages and benefits of these off-site workers would not be included in

the certified payrolls required under Davis-Bacon. However, the wages of these off-site workers

are part of the contractor’s expenses since they are producing components to be used on the

federal project. Only the wages and benefits for those working on-site or at a fabrication facility

exclusively dedicated to the project are covered by Davis-Bacon and reported in the certified

payrolls. If a contractor utilizes an off-site facility that is exclusively dedicated to the federal

project, the certified payrolls will reflect these labor costs. However, if an off-site facility that is

not exclusively dedicated to the project is used, the certified payrolls will not reflect all of the

labor costs of the project. Uncertainty regarding the use of off-site facilities limits the reliability

of the information reported in a certified payroll in estimating another contractor’s labor costs

and future bids.

42

See requirements for off-site work in DBA/DBRA Compliance Principles, US Department of Labor, Prevailing

Wage Resource Book. Accessed at: http://www.dol.gov/whd/recovery/pwrb/Tab9.pdf.

31

Labor Estimating Manuals, Bid Preparation, and Labor Costs

Labor estimating manuals are widely used in the construction industry during the

preparation of bids.43

These manuals provide estimates of the labor hours needed to complete a

project and are highly specialized. For example, members of the Mechanical Contractors

Association of America have access to WebLEM, a web-based labor estimating manual that

provides detailed labor units for typical HVAC, plumbing, and pipefitting tasks.44

Contractors

typically use labor estimating manuals to obtain initial labor cost estimates. These figures are

adjusted for any risk factors such as the height at which work will be performed and other project

features that increase construction time. The labor cost estimate is also marked up for overhead

costs and profit. If all contractors bidding on a project are using the same or similar labor

estimating software and all have access to the project description, their initial labor hour

estimates will be similar. If all contractors pay the required Davis-Bacon rate for a federal

project, their initial labor costs will also be similar. What differs between contractors is how

much the initial labor hours and cost estimates are adjusted for risk factors, profit, and overhead.

Contractors with higher (lower) risk factors and profit markups will submit bids based on higher

(lower) labor costs. These markups may influence whether a contractor wins the bid. In this bid

preparation setting, initial labor hour and cost estimates tend to be uniform. If a competitor is

seeking to undercut another contractor’s bid using labor costs data, they need information on the

43

See RS Means for a description. Accessed at: http://www.rsmeans.com/links/estimates.asp. 44

See MCAA “Labor Estimating Manual” for the mechanical trades. Accessed at: https: //www.weblem.org/.

Other examples include estimating software by RS Means that, in addition to labor hour estimates, calculates crew

sizing and allows for verification of subcontractor quotes. Accessed at: http://www.rsmeansonline.com/. The

National Electrical Contractors Association (NECA) offers the NECA Manual of Labor Units to members.

Accessed at: http://www.necanet.org/neca-store/publications.

32

rival’s risk, overhead, and profit markups. However, information on markups is not contained in

certified payrolls.

Labor Costs and Total Construction Costs

A contractor may have won the bid by a wider margin than the implied difference in

labor costs between the two companies. Contractor #1 may have won based on the non-labor

cost components. Data presented in the section of the report on construction worker labor costs

as a percent of total construction costs indicates that labor costs for electrical specialty

contractors in Colorado are, on average, approximately 28% of total costs. This suggests that

non-labor components make up about 70% of total project costs (on average). Contractor #1

may have won the project with a lower bid on non-labor components that constitute the majority

of a project. Since labor costs are a low percent of total construction costs, using this

information is not a reliable method to undercut the bids of other contractors.

Unless the bids of participating subcontractors are released by the general contractor

(which is unlikely), or if federal agencies release general contractor bid information after the

project has been awarded, a competing contractor will not know the winning bid. Under these

conditions, attempting to undercut future bids based on the labor cost component that constitutes

approximately 28% of project costs is very difficult. If contractors receive bid information from

a federal agency after the completion of a project, all losing firms can quickly calculate

33

differences between their bids and the winning bid without relying on labor cost estimates of the

winner.45

Differences in Construction Worker Productivity

The argument that knowing the labor costs on one project can be used to undercut the

bids on future projects assumes that the past and future projects are similar. Data reported in

Table 1 indicate that Contractor #1 was also engaged in repair-oriented Project 2 that required

similar labor hours to complete (60 hours for Project 1 and 63.5 hours for Project 2). While

projects 1 and 2 are both repair jobs with similar labor hours, there are qualitative differences

between these jobs. Project 1 required repair work on an existing electrical system in a historic

building. Work on these types of structures may require modern code compliance and system

upgrades (see Swanke Hayden Connell Architects, 2000). The types of tasks electricians would

perform on this project likely differ from the diagnostic work required of repairs to the

mechanical equipment involved in Project 2. Because of the qualitative differences between

projects 1 and 2, similarity in quantity of hours worked is of little use to a competitor who wishes

to use labor cost information from Project 1 to undercut the bid on Project 2.

In addition to qualitative differences, projects can also differ in terms of size. Contractor

#1 completed several projects for the City of Denver. We have selected three that had similar

labor hours, but hours ranged significantly between all projects completed by this contractor.

Project 4 is an example. It is clear that the labor cost data from a small project, Project #1 with

45

The availability of bid information is discussed in a following section.

34

60 hours, would be of little use in estimating the labor costs of a much larger project like Project

4 with approximately 590 hours.

Another problem with undercutting bids based on labor costs is that if the competitor

reduced its labor hours, by more than 14% in the example described above, the competitor would

have to produce at that rate, if it won the contract. Given the productivity of the existing

workforce, overhead, and current method of construction, this may not be a profitable practice.

Reducing labor costs involves changes to the existing workforce (additional training, or finding

and hiring more productive workers). In this situation it is likely easier for a competitor to find

ways to reduce bids based on non-labor cost components (such as purchasing cheaper supplies,

materials, etc.) to gain a competitive advantage.46

While Project 2 is also a repair job that required a similar number of hours to complete as

Project 1, the electricians used in Project 2 were not all paid the same wage rate (according to

data reported in the certified payrolls for Project 2). For example, of the total 63.5 total hours

reported, 54.5 hours were completed by employees who were paid the prevailing wage rate

($40.82 total hourly compensation). Two other employees were paid $40.82, plus $10.82 in

fringes (total hourly compensation of $51.64) and $33.32, plus a fringe of $10.82 per hour (for a

total hourly equal to $44.14). These two employees worked four and five hours on this project,

respectively. Labor cost for this project can be calculated by taking these differences into

account. Here, labor cost equals $2,651.95 ([54.5 hours x $40.82] + [4 hours x $51.64] + [5

hours x $44.14]). The labor hours for projects 1 and 2 are roughly similar ($2,449.20 versus

$2,651.95) with the difference due slightly more required time and to the workers receiving

46

Materials and supplies on government projects are typically standardized to achieve safety and quality standards.

See Duncan (forthcoming). In these situations, cost savings may be achieved by lower material prices rather than

the use of lower material quality.

35

higher pay in Project 2. The problem with comparing labor costs between these two projects is

that the quantitative measure of cost does not capture qualitative difference in the workers

completing these projects.

Construction worker compensation depends, in part, on skills and experience. The two

employees who received compensation in excess of the prevailing wage rate minimum for

Project 2 are likely more skilled and experienced than those employees receiving the prevailing

wage rate. Contractor #1 may have needed these skilled workers to address the diagnostic

requirements of Project 2 that involved repairs to mechanical equipment. Regardless, the