what explains governance structure in non-profit and for-profit microfinance institutions?

TRANSCRIPT

Electronic copy available at: http://ssrn.com/abstract=1342427

What explains governance structure innon-profit and for-profit microfinance

institutions?

Roy Mersland∗ R. Øystein Strøm †

First version: 0602 2009

Abstract

This paper aims to explain the choice of board and CEO characteristics in mi-crofinance institutions (MFI). Explanations are sought in substitution or comple-mentarity between the characteristics, external governance variables, and financialperformance and outreach performance to the poor. The data are from 290 MFIsin 61 countries, and the logit regressions methodology is employed. The board andCEO characteristics are board size, CEO-chairman duality, international directors,and female CEO. We find relationships among these variables, and also that the ex-ternal governance variables ownership type (shareholder owned) and internationalinitialization induce smaller board, less duality, more international directors, andfewer female CEOs. Except for the female CEO result we argue that these resultsare consistent. The consistency is repeated for outreach performance to poor indi-viduals and small businesses. We believe the study may inform better performancestudies in the future, and also to motivate better governance in MFIs.

Keywords: Micro-finance organization, governance, performance

JEL classification codes: G30, G32, J23

∗Agder University College, Kristiansand, Norway†University College of Østfold, N-1757 Halden, Norway

1

Electronic copy available at: http://ssrn.com/abstract=1342427

1 Introduction

There is no lack of recommendations of how the governance of the microfinance institu-

tion (MFI) should be (Rock et al., 1998), in particular board size and composition, but

little knowledge of what actually determines the MFI’s choice of its internal governance

mechanisms. The MFI pursues the twin objectives of financial sustainability and out-

reach to the poor (Armendariz de Aghion and Morduch, 2005). In this paper, we focus

upon four board and CEO characteristics, that is, board size, CEO-chairman duality, the

presence of international directors, and the presence of a female CEO. We seek explana-

tions of their occurrence from theories of board and CEO determination. Demsetz and

Lehn (1985) argue that interdependencies exist among these characteristics, for instance,

a large board and CEO-chairman duality could be found together in boards. Therefore,

substitutability in boards is important to investigate, as in Agrawal and Knoeber (1996).

External governance mechanisms such as the MFI’s competitive position determine the

board’s size and its composition (Schmidt, 1997). For instance, Mayers and Smith (2005)

find that ownership type is a strong predictor in the US insurance industry. The MFI’s

financial performance is taken to determine the board’s monitoring effort in Hermalin

and Weisbach (1998). Raheja (2005) and Harris and Raviv (2008) can be used to under-

stand how various forms of outreach may induce a better combination of board size and

composition.

The Hermalin and Weisbach (1998) model of endogenous determination of board size

and composition represents a “Copernican revolution” in board studies in particular and

governance in particular. The new idea is that one should study the process by which

the board is put together, and not assume that the board is exogenously given. Raheja

(2005) modifies this explanation since her model implies that board size and composition

are determined by the outside information complexity in the firm’s markets. This leads to

a search for outside, exogenous explanations for board and CEO characteristics. Studies

of this type are often tailored to the particular situation that the firm is engaged in.

The data for the explanations of board and CEO characteristics are income statement and

balance sheet data on 290 MFIs from 61 countries throughout the world collected by third

party rating agencies. We employ logit regression methodology for the purpose.

To our knowledge, no investigation into determinants of MFI governance has been un-

dertaken. The Mayers and Smith (2005) study shows the importance of ownership type

(shareholder or mutual) in understanding the choice of board size and composition. Barth

et al. (2007) find that external governance mechanisms matter for performance (ROA) in

a comparison of banks from 152 countries drawn from a World Bank survey. They include

1

Electronic copy available at: http://ssrn.com/abstract=1342427

measures for accounting standards, external audits, financial statement transparency and

external ratings in their study. Although these measures are different from ours, the in-

vestigation clearly shows the importance of external mechanisms for performance. Our

concern is whether these mechanisms determine the choice of the internal governance

mechanisms of board and CEO characteristics. Also, their sample is not limited to MFIs,

but include banks in general.

A puzzling main result in Mersland and Strøm (2009) is that few governance mecha-

nisms are significant in explaining financial and outreach performance in MFIs. For

instance, the type of MFI ownership turn out to have no influence on either performance

measure. In this paper we concentrate upon the interconnections among governance

mechanisms. These may in turn give better informed models of performance in MFIs at

a later stage.

We do find substitution and complementarity effects among board and CEO character-

istics. The presence of an international director and a female CEO is associated with a

larger board, however, duality decreases with international director. Among the external

governance mechanisms the fact that the MFI is a shareholder owned firm is associated

with a smaller board, more international directors, and no female director, while being

internationally initiated helps the MFI to reduce board size and duality, and increase

the presence of international directors. We note the consistency in these relationships.

A smaller board and no duality are generally considered beneficial in the board litera-

ture, while international directors has turned out to be advantageous in studies. The

same consistent pattern is repeated for outreach performance, where individual loan, the

MFI’s gender bias towards loans to women, and its number of loan products are impor-

tant. Thus, we do not find one theory to explain the occurrences of board and CEO

characteristics. An empirical researcher needs to be eclectic, but also needs to look closer

at the interactions among various governance mechanisms as well as their relations to

outside market conditions when setting up performance models.

The paper proceeds as follows. The next section 2 gives an overview of the hypotheses

we test. Section 3 gives an overview of the data from 61 countries together with descrip-

tive statistics on the variables we use. In the following section 4 the logistic regression

approach is discussed. Section 5 tests hypotheses first by simply comparing means on the

individual variables, and then performing the partial logit regressions with each of the four

board and CEO characteristics as dependent variable. Finally, section 6 concludes.

2

2 MFI governance

The central question in this paper is why an MFI chooses the set of governance mecha-

nisms it does. Before answering, we need to be explicit as to what governance mechanisms

we choose to focus on. Mersland and Strøm (2009) differentiate between internal and

external governance mechanisms. The internal mechanisms are board and CEO charac-

teristics and include variables such as board size, CEO-chairman duality, international

director, internal board auditor, and female CEO. To this list, the MFI’s incorporation,

or its ownership type, is included as well. The external mechanisms are competition and

bank regulation. In this paper, we focus upon the explanation of the internal governance

mechanisms apart from the ownership type. The reason for this is that the MFI’s incor-

poration as well as its regulation and competitive exposure are exogenous to the choice

of internal governance mechanisms. For instance, the ownership type is seldom changed,

and once changed, the MFI is likely to maintain its new incorporation for a long time.

In contrast, board size may well change from one year to the next. Thus, ownership type

and external governance mechanisms can be important predictors for board and CEO

characteristics, but hardly the other way around.

To sum up we will focus upon the board and CEO characteristics board size, CEO-

chairman duality, international director, and female CEO. In one way or another, these

variables turn out to be significantly related to MFI financial performance or outreach in

Mersland and Strøm (2009), and most are suggested in former studies. Yermack (1996)

and Eisenberg et al. (1998) find that a smaller board is associated with higher financial

performance, a result that later studies routinely confirm; Brickley et al. (1997) find

no performance difference between firms with CEO-chairman duality compared to firms

with split roles; and Oxelheim and Randøy (2003) report that higher performance follows

in firms having international directors. We include the female CEO variable since Allen

and Gale (2000) caution about the effectiveness of monitoring; they note that the board’s

monitoring is often ineffective due to the firm’s financing out of retained earnings. Owners

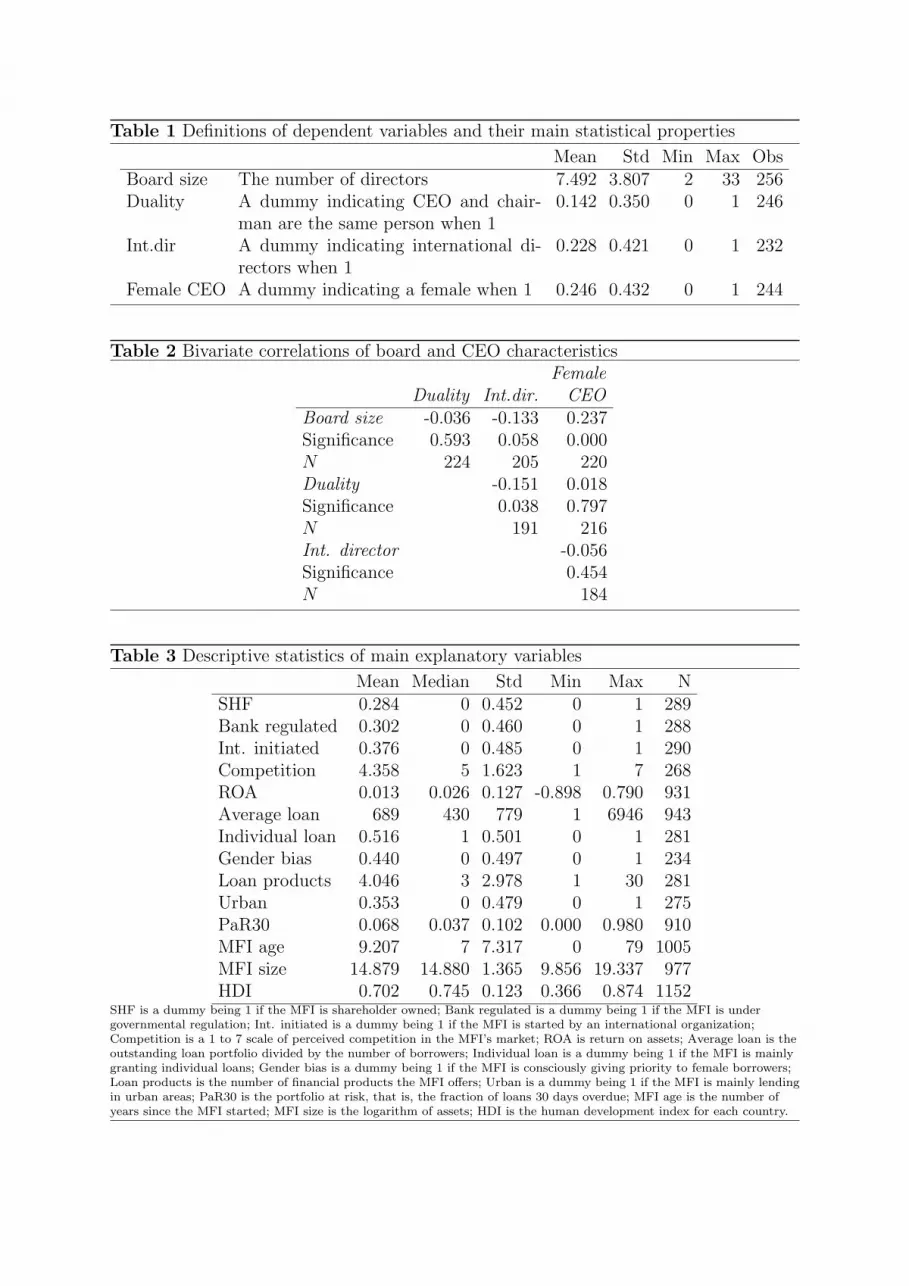

may find it advantageous to yield control to the CEO. Table 1 gives definitions and main

statistics for the dependent variables.

Table 1

Thus, the average number of board members is 7.5 and 24.6 per cent of CEOs are fe-

male.

Are board and CEO characteristics substitutes? The next table shows the correlations

of the four board and CEO characteristics that enter the analysis in this paper.

3

Table 2

We see some significant correlations, especially between board size on the one hand and

the female CEO and international directors on the other. Likewise, the relation between

the CEO-chairman duality and international directors is significant. However, we cannot

conclude from this that the CEO and board characteristics are substitutes (with negative

sign) or complements (with positive signs). The correlations are very low. According to

Kennedy (2008) the bivariate correlations need to be higher than 0.70 for variables to be

dependent. Thus, it seems board and CEO characteristics are chosen independently of

each other. We include the variables in regressions, since significant relationships may

appear when other variables are controlled for.

The tables reveal that a number of variables have few observations. These are time

invariant variables, that is, their value is constant for the four years of rating data. This

applies to the governance variables. Most of these variables will be constant over the

relatively short four year span. However, board variables may be easily changed. In fact,

this gives a further reason for converting the board size into a dummy variable, since the

change from a small board size into a large is less likely than a change, say, from five to

six members.

We explore hypotheses concerning internal governance mechanisms on board and CEO

characteristics, external governance mechanisms, and the effects of following the dual

objectives of financial performance and outreach to the poor. Demsetz and Lehn (1985)

hold that governance mechanisms are substitutes. The firm will choose its internal gov-

ernance mechanism so that the marginal utility of each are equalised. This implies some

dependence among the mechanisms. Thus, if the firm uses more of one mechanism, it

may be advantageous to increase or decrease the use of other. In the first case the mech-

anisms are substitutes, in the second they are complements. A small board, separate

chairman and CEO, international directors, and a female CEO may be good governance

mechanisms in an MFI. But the Demsetz and Lehn (1985) theory does not indicate how

their relationship may be. We turn to other explanations now.

External governance mechanisms concern the MFI ownership type, bank regulation,

international connections, and competition. The Mayers and Smith (2005) argue that

the mutual company has no owners and therefore lack some important governance mech-

anisms, such as the takeover opportunity. Hence, the mutual company strengthens other

governance mechanisms, notably the presence of independent directors. In our case, we

should expect that being an SHF leads the MFI to try avoiding agency problems as

in other shareholder owned firms with a dispersed ownership. Thus, we should expect

4

the SHF MFIs to have smaller boards, no duality, international directors, and a female

CEO.

Likewise, regulation supposedly has the same effects upon internal governance mecha-

nisms. Good governance is part of the Basel II requirements. Thus, the regulated MFIs

must show more transparency, but also assure regulators that their board and CEO act

responsibly.

International donors, shareholders, and lenders are important in microfinance. They

may require a transparent governance structure to be assured that money is safe and well

spent. For instance, many international financial institutions require transparency and

a recognizable governance structure in the MFIs they are dealing with. This has hardly

been elucidated before. But, from Tirole (2006), lenders’ impact can be important,

especially in mitigating the moral hazard problem. The Easterbrook (1984) argument is

really that by increasing the debt equity ratio the bank gets more involved in the running

of the firm. Thus, we should expect international debt to have the same advantageous

effect in MFIs.

Competition motivates the MFI to find beneficial governance structures. Thus, if the MFI

faces strong competition or takeover threats, its oversight efforts may become more lax

(Schmidt, 1997). The idea is that the firm needs to be well run to withstand competition,

and therefore, internal monitoring has little to contribute to further improvement in

company operations. Perhaps paradoxically, this leads to the prediction that the internal

governance mechanisms are weaker the stronger is competition. Weak internal board

monitoring in USA is explained by this. However, one could reason the other way around.

When competition is strong, the firm needs to be well run in all aspects, including its

internal monitoring. Thus, the prediction from this variable is uncertain.

Financial performance may determine the choice of governance mechanisms (Hermalin

and Weisbach, 1998). Their theory says that a CEO may be in a position to negotiate

for laxer oversight after delivering good firm performance. The position may be used to

people the board with persons who are friendly to the CEO. Thus, with continued good

performances the board becomes “endogenously determined” and the CEO entrenched.

The prediction from this theory in our context is that internal governance mechanisms

are weaker in MFIs with good financial performance.

Outreach performance is the extent to which the MFI is able to serve poor customers

and small enterprises. The MFI usually has two main goals, financial sustainability and

outreach to poor people. The outreach measures that the MFI follows may also have

consequences for the MFI’s choice of board and CEO characteristics. Armendariz de

5

Aghion and Morduch (2005, p. 267) mention that the outreach goals may be hard to

measure. On the other hand, the choice of outreach is at the same time the MFI’s choice

of business model, or its choice of market conditions it is facing. For instance, the MFI

may choose to focus upon female borrowers. This means we may use insights from this

field in the discussion of outreach impact.

Raheja (2005) presents a model of board size and its fraction of independent, that is,

outside directors when market conditions are important. More outside directors mean

more monitoring. However, this monitoring is ineffective if insiders do not share their

information with outsiders. Thus, the fraction of outsiders is higher the more important

the outside information. This will vary with the firm’s business condition. In our context,

an MFI operating in different financial products may need a larger board to accommodate

the various information needs. In general, the internal governance mechanisms may vary

with the market conditions facing its business. Harris and Raviv (2008) present a more

general theory yielding the same predictions1.

In this paper, we use the size of the average loan, lending methodology (group or indi-

vidual), the MFI’s conscious gender bias, the number of loan products, and the markets

served (mainly urban or rural) as indicators of outreach or business model. It may be

that the MFI’s ability to tap into local information networks, for instance by giving group

loans, necessitates better internal governance. If the bank lends mainly to women, we

should expect the MFI to prefer a female CEO, who may be better informed of this cus-

tomer segment’s banking needs than a male CEO. Monitoring of the loan contract may

call for better risk management expertise in an urban than a rural setting. The urban

borrower has more borrowing alternatives, and monitoring performed by neighbours and

relatives are not as effective as in the rural villages.

Absent from this analysis are stakeholder variables. For instance, a plausible hypothesis

is that the presence of employee directors may cause owners to strengthen their position

in the board, as Strøm (2009) finds for Norwegian boards. However, few MFIs state

employee directors on the board, making the records unreliable. Among those who do

state the number, very few have employee directors. The same goes for other stakeholders.

This is perhaps surprising, since one of the assumed benefits of the MFI is its ability to

tap into local information networks. Having stakeholders on the board could improve the

MFIs access to local information even further.

1In a literature review Hermalin and Weisbach (2003) note that the theory of the board is littledeveloped, and the field remains largely empirical. Yet, theories of the determination of the board arenumerous, we should also add Adams and Ferreira (2007), but the empirical literature on the determi-nation of boards is short.

6

We also leave out debt. Easterbrook (1984); Jensen (1986) suggest the debt to equity or

to assets as governance mechanisms. This interpretation may be difficult to uphold in

banking organisations, as they may as well be a measure of the bank’s riskiness.

3 Data

We use observations of 290 rated MFIs from 61 countries. Third-party organisations

perform the standardised ratings and outside organisations subsidize parts of the costs

involved (www.ratingfund.org). A main motive behind submitting to a rating is the

improved access to external funding. The third-party and standardised collected MFI

data from the rating agencies must be judged better than self-reported data, as found for

instance in the Mixmarket database. The data cover both financial and outreach data,

that is the income and balance reports and data on key outreach aspects. At each rating

four years of data are obtained, at best. Thus, the maximum number of observations is

1160. The ratings are performed in the period 2001 to 2007, which means that we have

data from 1998 to 2007. Most data are from the period 2001 to 2005.

The dataset contains information from risk assessment reports from five microlender

rating agencies, MicroRate, Microfinanza, Planet Rating, Crisil, and M-Cril, and their

reports can be found at www.ratingfund.org. All five are approved as official rating

agencies by the Ratingfund of the C-GAP. Their rating methodology reveals no major

difference in MFI assessment relevant to variables used in this study. When necessary,

all entries in the dataset have been annualised and dollarised using official exchange

rates.

The use of rating data may introduce sample selection bias. Few larger regulated microfi-

nance banks are included in the dataset, since they have funders who demand traditional

credit ratings offered by agencies such as Standard & Poor’s. Moreover, neither the vir-

tually endless number of small savings and credit cooperatives nor development programs

offering microcredit solely as a social service are included. The 290 MFIs in the dataset

represent commercial and professionally oriented institutions that have decided to be

rated to improve access to funding, benchmark themselves against others, and increase

transparency (see www.ratingfund.org). Despite these limitations, we consider our third

party collected data to be more reliable than self-reported data sources like Mixmarket

(www.mixmarket.org) or questionnaires. Compared to the MFIs included in Mixmarket

Annual MFI Benchmarks (2006), the MFIs in our sample are younger (7 vs. 9 median

years), smaller (median total assets USD 2.9 million vs. USD 6.2 million), have fewer

7

credit clients (4,900 vs. 10,000), and have smaller loan portfolios (USD2.1 million vs.

USD4.4 million), yet the median average loan is approximately the same (USD433 for

our dataset vs. USD456 for the Mixmarket data). Comparing averages between the two is

not meaningful, since the Mixmarket data contain more of the very large MFIs. Overall,

our data seem sufficiently representative. Specifically, we avoid a large firm bias.

3.1 Variable definitions and stylized facts

We need to define the variables used in the analysis before proceeding. This also gives

us the opportunity to supply some stylized facts about MFIs in our data sample. Since

little is known on a global scale, it seems worthwhile to give an overview.

The dependent internal governance mechanism variables are converted to binary variables,

if they are not already. Thus, the board size and the international director variables are

both taken to be binary. We note from table 1 that the average board size is 7.5. The

median is seven. We take the cutoff to be the median, thus, a small board is defined

to include all sizes from the lowest and including seven, the large board size from eight

and up to the maximum of 33. Many MFIs do not have international directors. Their

presence is marked with a dummy being 1 if the MFI has one or more international

directors.

Table 3 gives an overview of the independent variables in the analysis with definitions

at the bottom. The median is supplied as well since many variables are not normally

distributed.

Table 3

The table may be read as a short introduction to microfinance. The industry is notable

in terms of ownership type, regulation, its international dimension, loan size, and main

customer groups. In table 3 the SHF is a dummy variable indicating ownership type.

In fact, the MFIs comprise a number of ownership types, that is, a bank, a non-bank

financial institution, a non-governmental organization (NGO), a cooperative or credit

union, a state bank, and an “other” category. The SHF is defined to be the bank and

the non-bank financial institution. At 57.9 per cent the NGO is by far the largest group,

followed by the bank and non-bank financial institution at 28.3, and the cooperative and

credit union at 11.1 per cent. The remaining categories are only 2.7 per cent of the

sample. Thus, the partition into SHFs and others is a natural choice, since the other

organizational types do not have the same clear ownership structure.

Most MFIs are not regulated, in fact, only 30.2 per cent are under official regulation.

8

This is largely the case since most MFIs in our sample do not accept deposits, but it is

not a perfect overlap between deposit banks and regulated banks. All firms in our sample

is somewhat regulated, in that their accounts are transparent.

Many MFI are founded by international organizations, in fact, 37.6 per cent. We use

this variable as a proxy for international lenders’ influence. The reason for doing so is

the data situation. We have some data on international commercial and subsidized debt,

and on total debt. However, these data do not cover all firms, and further, they are not

as reliable as one would wish. For instance, the rating agencies give different definitions

of a subsidized loan.

The competition variable gives the MFI’s perceived competitive pressure in its market

on a one to seven point scale. The scale is self-constructed from the various scaling

conventions followed by the rating agencies. The measure is subjective in the sense that

it shows the MFI manager’s perceived competitive pressure in its market. The higher

is the score the higher the perceived competition. The table shows that most managers

perceive the competition to be above the 3.5 middle point.

The average loan variable shows the “micro” in microfinance. The average loan is USD

689, and the median is even lower. Besides being small, the loans are given with a short

duration, as practically all contracts are of less than a year’s duration. This fact removes

problems of periodization of the loan effect. Average loan is a prime outreach measure,

and the expectation is that the lower the loan the higher is “depth” outreach (Schreiner,

2002). Furthermore, despite microfinance is known for reviving group loan (Ghatak and

Guinnane, 1999), most of the loans are made to individuals. In our sample about 51 per

cent of the loans are to individuals.

Many MFIs favour women in their lending programme. For instance, the Grameen Bank

focusses to a major extent on women. In our sample, MFIs that report the percentage of

female clients tell that women constitute about 70 per cent of their borrowers, however,

very few report their percentage of female customers. Accordingly, we use the MFI’s

gender bias as a proxy for the actual lending to women. Table 3 shows that nearly half of

the firms have gender bias, that is, a bias for favouring female customers. This outreach

measure belongs to the depth outreach dimension as well, since women are generally

poorer than men, and their use of the loan includes family and community to a larger

extent than men’s (Armendariz de Aghion and Morduch, 2005).

The last outreach measure is rural or urban lending. The categories are mainly rural or

mainly urban, and a third category including both. Table 3 shows that most MFIs do

not lend mainly to urban borrowers.

9

The remaining variables are control variables. The first is an uncertainty measure, port-

folio at risk showing the percentage of loans 30 days or more in arrears. The low number

reflects the finding that the “poor always pay back” as early employees Dowla and Barua

(2006) of the Grameen Bank indicate. The MFI age variable shows the MFI is a fairly

young organization. The firm size variable shows a large dispersion of the MFIs’ size.

The Human Development Index (HDI) is a comparative measure of life expectancy, lit-

eracy, education and standards of living for countries worldwide. It is a standard means

of measuring well-being, especially child welfare. It is used to distinguish whether the

country is a developed, a developing or an under-developed country, and also to measure

the impact of economic policies on quality of life2.

When using a number of explanatory factors, there is always the danger of multicollinear-

ity among the explanatory variables. A first check on this problem is to run a correlation

analysis of the variables.

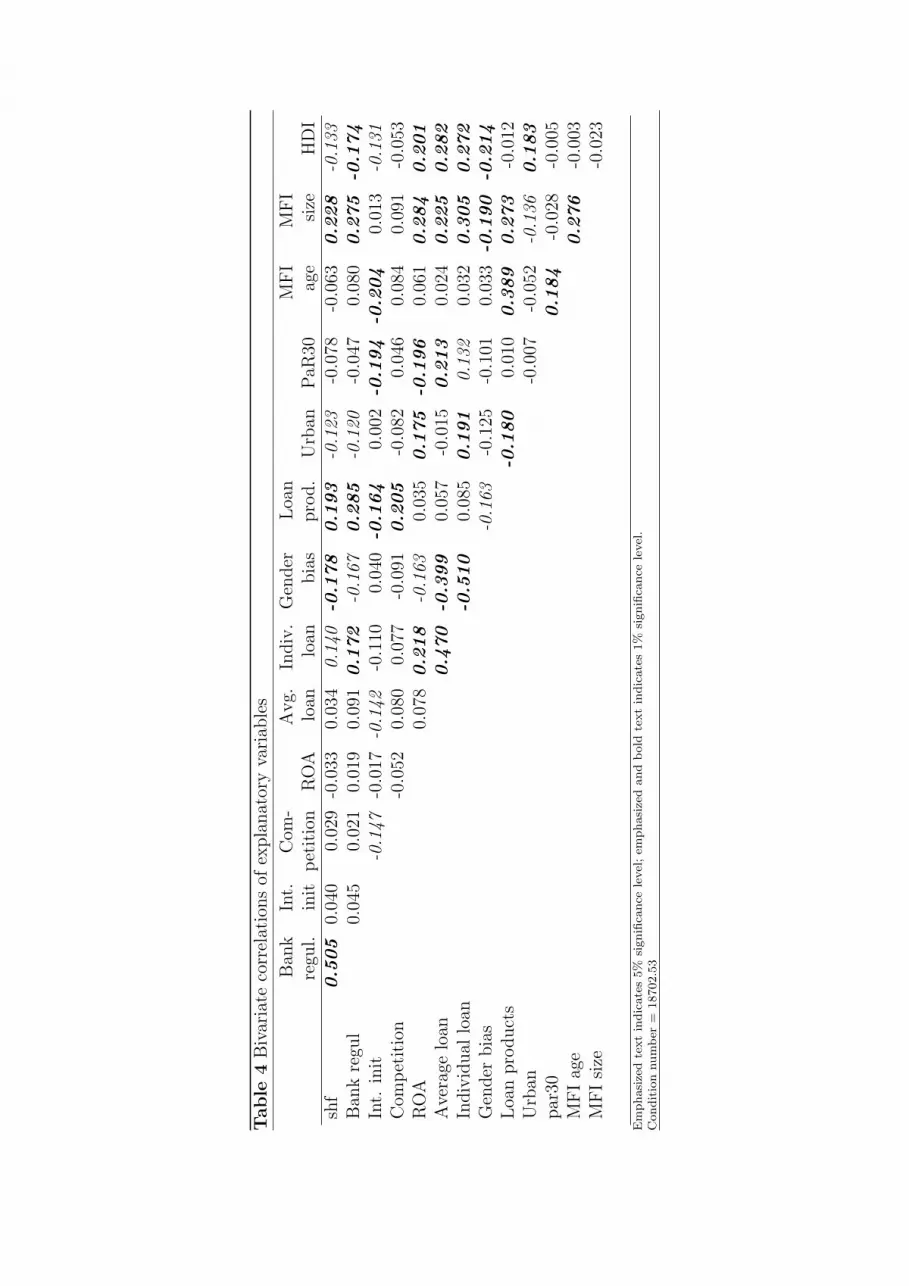

Table 4

None of the correlations reach the 0.70 cutoff that Kennedy (2008) sets, but two are

above 0.50. These are the correlations between the SHF dummy and bank regulation,

and between individual loan and gender bias. However, these are too few and too low

to invalidate the regressions using these as explanatory variables. Specifically, we note

the low correlations between financial and outreach performance variables. ROA is sig-

nificantly correlated to individual loans and to the urban dummy only, and these are

at low levels. Thus, it is valid to use both performance variable sets together in the

analysis.

4 Methods

The many interrelationships among governance variables could mean that we use a simul-

taneous equations setup as in Agrawal and Knoeber (1996) and Strøm (2009). However,

we will follow a simpler procedure by running separate logistic regressions for the internal

governance mechanisms. Since the governance model is unknown, a simultaneous spec-

ification may be faulty, however complex. If an equation in the system is erroneously

specified, the error will contaminate the other equations too (Hayashi, 2000). With sep-

arate regressions, the error stays with the single equation.

2We use a list of countries by Human Development Index as included in a United Nations DevelopmentProgram’s Human Development Statistical Update released on December 18, 2008, compiled on the basisof data from 2006. The new list contains purchasing power parity (PPP) adjustments. The index wasdeveloped in 1990 by Pakistani economist Mahbub ul Haq and Indian economist Amartya Sen.

10

To estimate the probability that the loan methodology is individual loan the probit

method, applied to panel data, is used. The binary choice logit model may be writ-

ten

P (Y = 1|X) =eXβ

1 + eXβ(1)

where P is probability, Y is an internal governance mechanism, X is the set of explanatory

variables, and β is the vector of parameter estimates.

The logistic distribution has somewhat fatter tails than the standard normal distribu-

tion. Two common assumptions are added to the estimating function. The first is that

the internal governance mechanism variables are independently distributed across time

t conditional on the explanatory variables and unobserved firm heterogeneity. The sec-

ond assumption is that unobserved firm heterogeneity is normally distributed with zero

mean and a fixed standard deviation. With these assumptions in hand, we estimate the

relationship with maximum likelihood methods.

Our data cover up to four years of records for each MFI, that is, we have a panel data

structure. However, we may not use well-known methods for panel data, such as fixed

effects or random effects estimation. The logit models meet with the incidental parameters

problem (Woolridge, 2002, p. 484) when assuming a fixed effects model and performing

within transformations, leading to inconsistent estimates. Furthermore, panel estimation

with the random effects model requires very strong assumptions about the heterogeneity.

For these reasons, the panel data methods are dropped. To control for firm heterogeneity

as much as possible we introduce the HDI, which is unique to each country and thus

controls for country effects.

Woolridge (2002) recommends a full range of fixed effects and time dummies in logistic

regression on panel data. We tried, but find little difference to regressions without. Thus,

adding dummies for countries do not improve estimations, and are accordingly dropped.

Neither do we control for time effects in the main regressions. Unreported robustness re-

gressions with nine year dummies show that results are little perturbed. Since unobserved

firm heterogeneity cannot be removed, the coefficient values will be biased. However, the

coefficients will show the correct direction of impact of each explanatory variable.

We test for mis-specification for each independent variable by the Lagrange multiplier

(LM) test, in effect testing whether excluding the variable improves estimation. The

goodness of fit of the specified relation is tested with the likelihood ratio (LR) statistic

2 (Lur − Lr). Here, the Lur is the unrestricted model, that is, the regression with the

assumed independent variables, and Lr is the restricted regression, which we take to be

11

the constant in the regression. We also report the ”pseudo” R2Nag = R2/R2

max where

R2max = 1− [L(0)]2/N , and

R2 = 1− L(0)

L(β̂)

2/N

Here, L(0) is the likelihood of the model with only the intercept, L(β̂)

is the likelihood

of the estimated model and N is the sample size. The pseudo R2 is distributed between

zero and one. Lastly, we also report the percentage correctly classified.

5 Statistical evidence

This section gives an overview of the test results for the assumed relationships. We start

with a simple ANOVA test and then present results from the logit regressions.

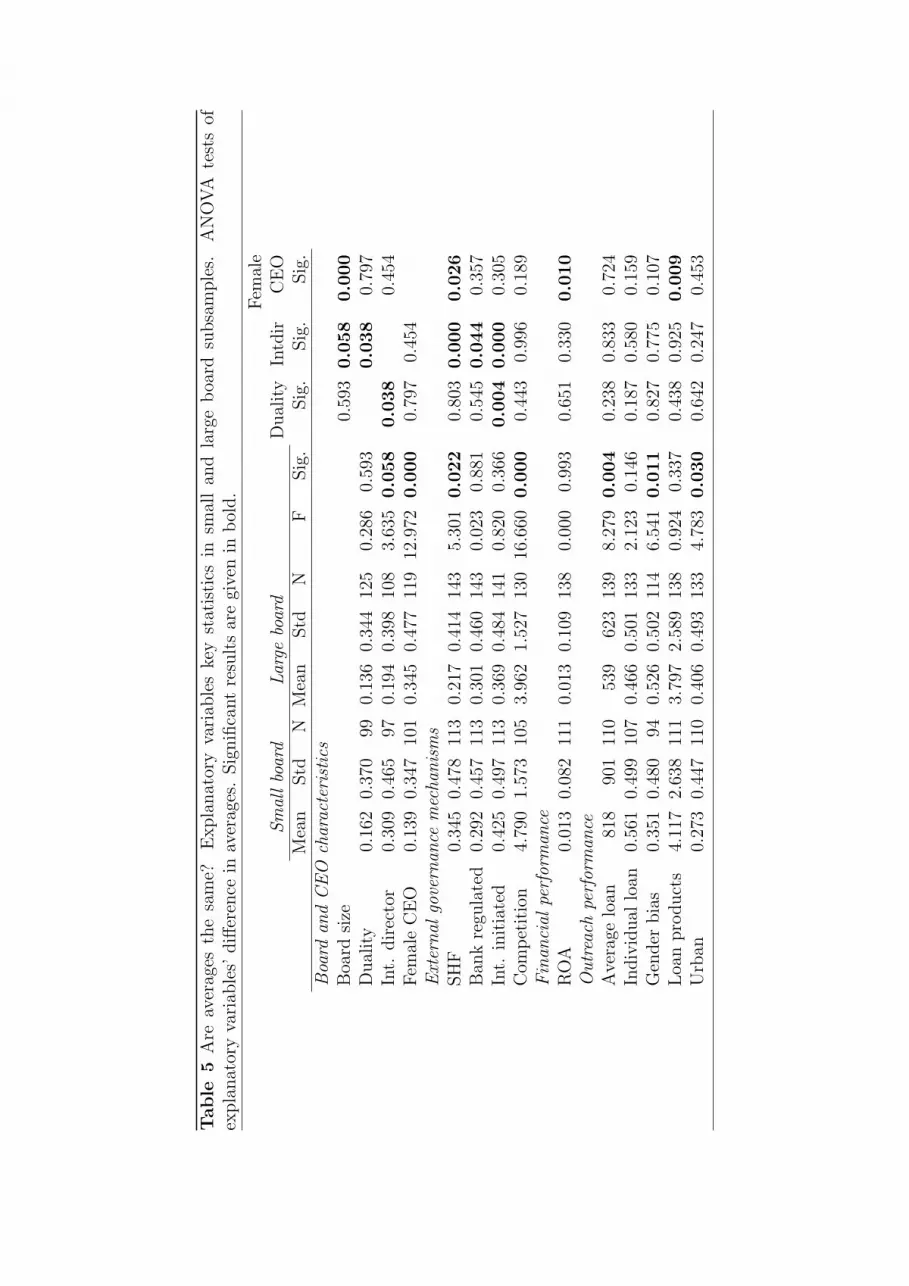

5.1 Partial ANOVA tests

The ANOVA analysis is a simple variable by variable test of average differences. The

tests may give an indication of importance that the single variable may have for the

chosen board or CEO characteristic. To show such tests for all board and CEO char-

acteristics is beyond the scope of this paper. Table 5 gives the test for the board size.

Then the remaining three columns show the significance of the other three dependent

variables.

Table 5

The ANOVA tests show several significant results. First of all, we notice important

relationships between the board and CEO characteristics, indicating that substitution

or complementarities exist among the variables. Furthermore, significant results appear

often for the external governance mechanisms. Thus, the choice of board and CEO

characteristics is at least partially driven by the slowly changing outside governance.

Then the financial and outreach performance measures show some significant results, but

perhaps surprisingly few. For instance, one would expect ROA to show more significant

results if the Hermalin and Weisbach (1998) theory of endogenous determination of board

composition and size is to hold.

All in all, the results from table 5 are encouraging for the further analysis.

12

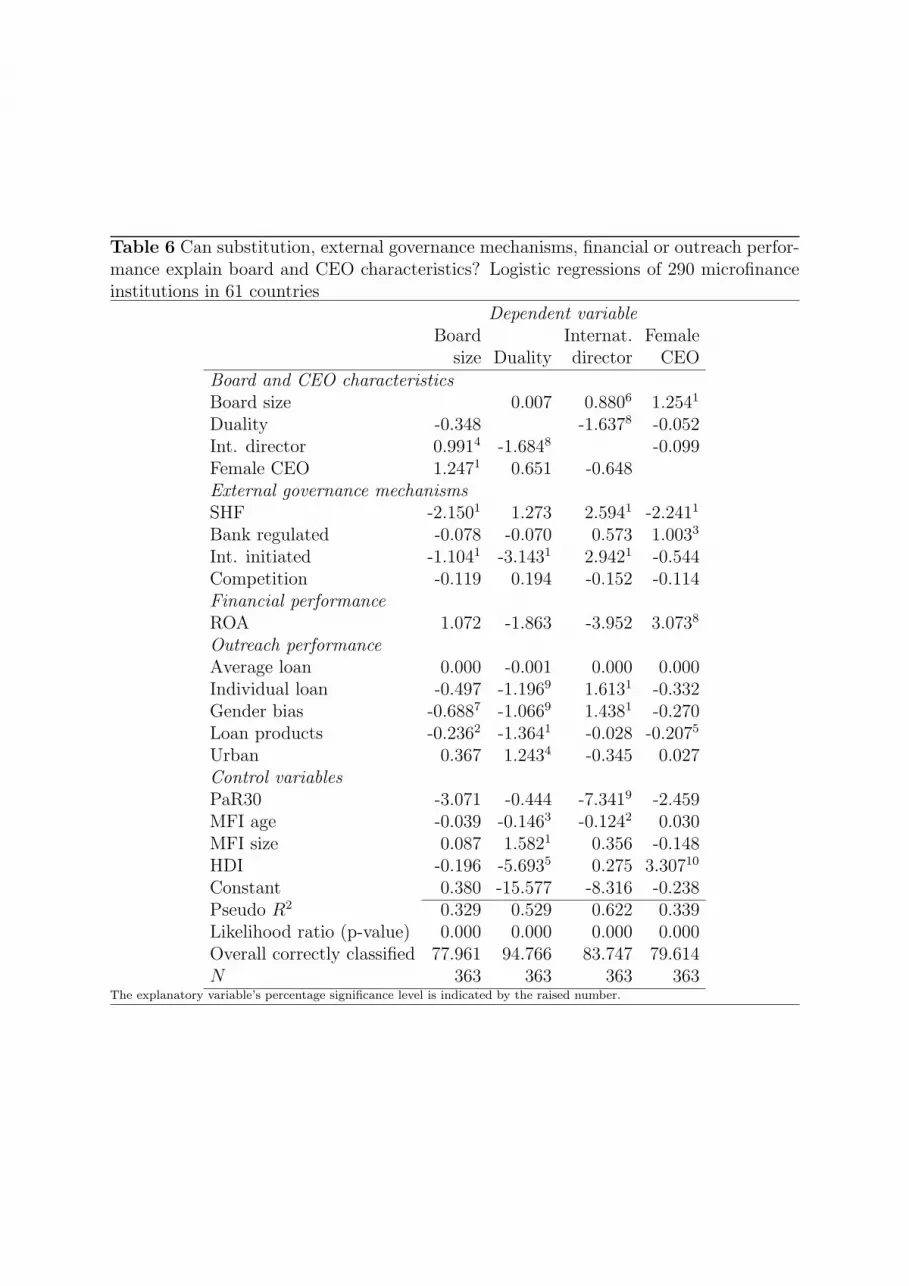

5.2 Logit regressions

What can logit regressions tell us about substitution among board and CEO variables,

the impact of external governance mechanisms, and the role of financial and outreach

performance? Table 6 gives an overview of regressions when the board and CEO variables

alternate as dependent variable.

Table 6

First of all, the table shows satisfactory goodness-of-fit statistics. Thus, the relations

seem to explain the overall variations in the board and CEO characteristics fairly well.

We also note that most of the significant results belong to our explanatory variables, and

not to the control variables. For instance, firm size is significant in only one relation.

The results for the board size as well as the other board and CEO characteristics largely

overlap the results in table 5 for differences in averages in large and small boards.

Let us look at the board and CEO substitution issue. Board size turns out to be positively

related to international directors and to female CEO. International directors and CEO-

chairman duality are negatively related. How can we interpret these results? From the

general literature on boards, a large board and CEO-chairman duality are seen as inferior

governance arrangements. The results from Mersland and Strøm (2009) indicate that

an international director has a neutral influence upon performance, and that a female

CEO has a positive impact upon financial performance. Thus, it seems that a larger

board needs to be balanced with international directors and a female CEO. Or, otherwise

stated, the weaker oversight implied by a larger board needs to be compensated by

international directors and a female CEO. Likewise, a CEO-chairman duality needs to be

compensated with international directors. Together these results indicate that board and

CEO characteristics are chosen in conjunction, confirming the Demsetz and Lehn (1985)

proposition and results in Strøm (2009). It is interesting to note that these relationships

hold for the young MFI organizations as well.

Do external governance mechanisms impact upon board and CEO characteristics? The

two important variables are SHF, that is, the MFI’s incorporation, and international

initiated. Thus, when the MFI is shareholder owned, it tends to have a smaller board,

international directors, but no female CEO. We obtain no significant result for CEO-

chairman duality. Notice that again these results are consistent to some degree. When

the shareholder owned firm improves monitoring by holding a smaller board, the need

for a female CEO decreases at the same time. The same does not apply to international

directors. The reason may be that shareholder owned firms are large and international,

and therefore, find it advantageous to have international members on the board. In

13

our sample, 43.3 per cent of the shareholder owned firms have international commercial

debt, and the percentage for other organizational forms is 35.8. But for the international

subsidized debt, the numbers are the opposite; 41.8 per cent for the shareholder owned

MFIs, 48.4 per cent for other organizational forms. Although none of these differences

are significant using a χ2 test, they may be an indication that the shareholder owned firm

needs an international presence on the board.

The other important external governance mechanism is international initiation. When

the MFI is initiated by an international body, it tends to have a smaller board, no

CEO-chairman duality, and, not surprisingly, international directors. Again we note the

consistency of the results for board size and CEO-chairman duality. Thus, both the SHF

and the international initialized MFI results confirm expectations from general agency

theory built on the assumption of a potential conflict between owners and board and the

CEO. It seems that these two organizational aspects are carriers of the good governance

practices developed for Western companies, as set out in for instance OECD (2004).

We also note that bank regulation has importance for the female CEO only, and that

competition is nowhere significant. For bank regulation this is not as expected. One

would believe bank regulation to have an impact at the board level, since governance

issues are stressed in recent bank regulation (Greenbaum and Thakor, 2007, p. 499-515).

Here, it turns out that the impact comes at the CEO level. Perhaps the explanation is

that in those MFIs that are at all regulated (30.2% in our sample), the regulation is soft

and does not extend to governance.

The Hermalin and Weisbach (1998) theory of endogenous board determination is tested

using the ROA. We do not find any significant results for the board variables, but for

the female CEO. Thus, better firm performance is associated with a female CEO in

MFIs. The surprise is that no effect is found at the board level, since the theory makes

strong predictions about this. However, the Hermalin and Weisbach (1998) theory says

that former performance determines the present board size and composition. We test

for this by lagging ROA one period and performing regressions on all four board and

CEO characteristic using this specification. None of the regressions, including the one

for female CEO, gives a significant result for the lagged ROA. When lagging, we loose a

number of observations, in fact, the number is reduced to 265. Despite this lower number,

almost all other significant results are unperturbed relative to table 6, that is, they are

robust to a different variable specification. Thus, we cannot confirm the Hermalin and

Weisbach hypothesis. The upshot is that the CEO is not able to determine the choice of

board size and composition in the MFI, but that this choice is guided by the choice of

other governance mechanisms, and as we shall see, by outreach performance.

14

Now, the outreach performance shows a number of interesting results. The regressions

tell that the board size is reduced when the MFI has a conscious gender bias and offer

more loan products; that CEO-chairman duality is reduced with a conscious gender bias,

more loan products, and individual lending, but is increased with mainly urban lending;

and that MFI more often have international directors when it offers mainly individual

loans and has a conscious gender bias. Again we note the consistency in the results.

For instance, gender bias induces a smaller board, less CEO-chairman duality, and more

international directors. This pattern of impacts is repeated for the other market condition

variables as well. On the other hand, only the number of loan products impacts upon

the choice of female CEO, and lending mainly to urban customers leads to more CEO-

chairman duality. The last is perhaps surprising, as we should expect an MFI’s conscious

gender bias would lead the MFI to look for a female CEO.

Both Raheja (2005) and Harris and Raviv (2008) stress the need for information when

they explain that board size and composition are determined by market conditions. The

results in table 6 bear this out. For instance, one would expect better risk management

in an MFI giving individual loan since the bank must perform most of the monitoring of

the loan contract on its own, while with a group loan a large part of the monitoring is

transferred to the group members’ mutual oversight. Accordingly, the internal governance

in the MFI situated in an individual loan market needs to be better than the MFI in

the group loan market. In the case of gender bias the board needs to be more efficient

because the information from customers may not be as easily obtainable from the female

customers, who are most often the poorest of the customers. In addition to information

needs, the poorest customers also give the MFI the smallest margins. Thus, to stay in

business, the MFI targeting women simply needs to be cost effective. Last, increasing

the number of loan products indicates a greater information complexity in the MFI’s

operations. This increases the need for good internal governance, and thus should induce

the adaptations that we observe.

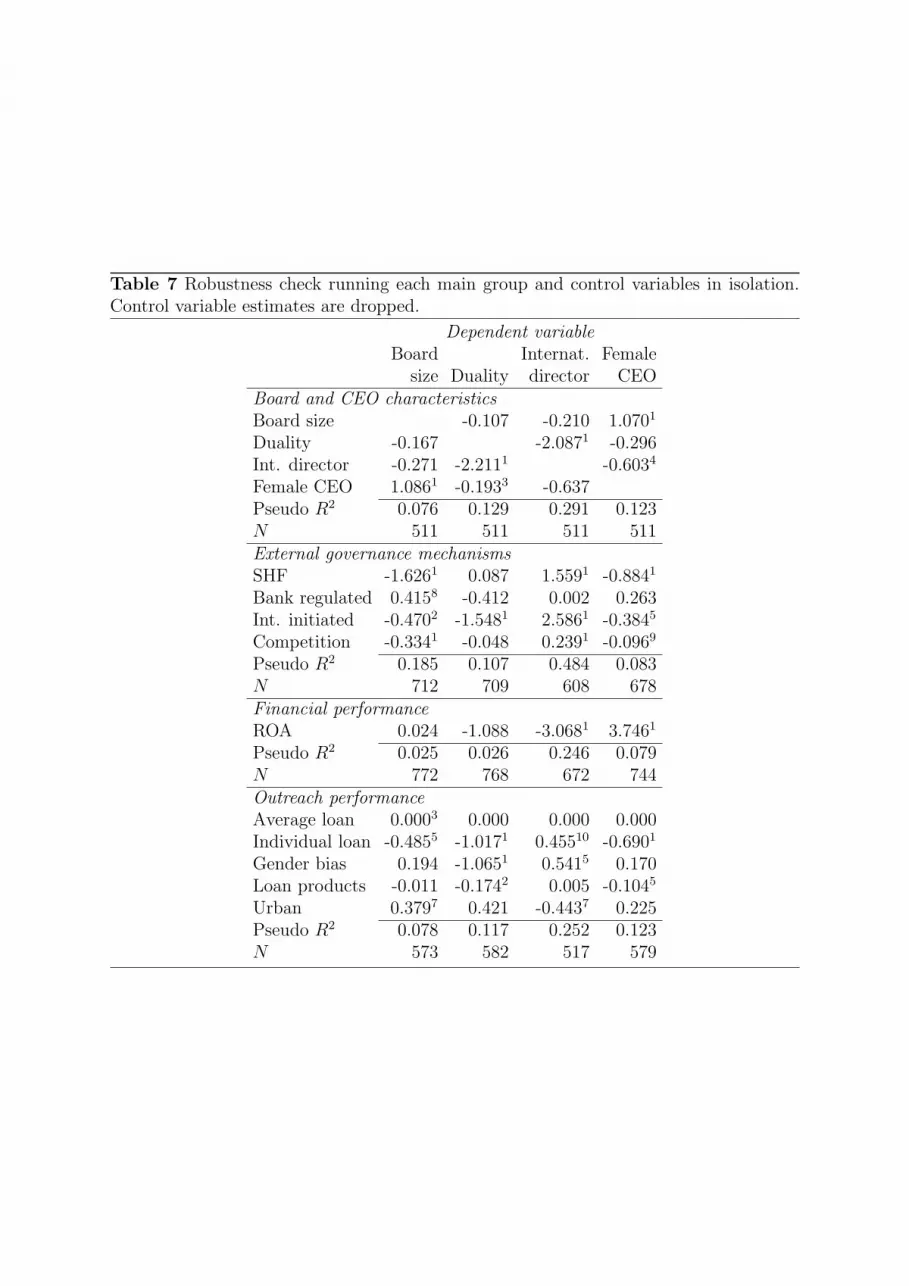

5.3 Robust results?

Multivariate analyses are notoriously difficult to perform. Despite the relatively low cor-

relation coefficients in table 4, interactions may appear when variables are run together.

This is the problem of multicollinearity, that is, the explanatory variables are dependent.

One way to check for multicollinearity is to see if the results are robust to different model

specifications. This is done in table 7 where only each group of explanations is taken at

the time together with the control variables. The results for the control variables are not

15

reported for readability.

Table 7

Compared to table 6 the results in table 7 are clearly different. However, the main

results from table 6 remain in terms of the direction of association and significant results.

The substitution effects are as before. The board size is positively associated with a

female CEO, and the CEO-chairman duality is negatively associated with international

directors. In the external governance group the two important variables SHF and the

international initiated are as in table 6. The conspicuous new finding in this group is

that competition shows significant results. The financial performance, ROA, gains one

significant result when run alone together with the control variables, while the outreach

performance variables show only minor differences in signs and significance. The size

of the coefficients are of minor importance since with panel data only the direction of

association and its significance can be ascertained.

Another possibility is that the panel data property upset the results in both 6 and 7.

The general problem with panel data is that residuals are not independent if the ordinary

least squares method on pooled data is used. However, if we run the models using the

averages of variables, few differences to the main results appear. These regressions are

not reported.

Thus, we cannot rule out multicollinearity in the results. However, this is often the

compromise one has to live with in this kind of research. We often want to keep variables

in the estimating model even when it may cause multicollinearity. The choice is not

between no or some multicollinearity, but what level of multicollinearity one is willing to

accept. Taken together, we are confident that the main results in this paper stand.

6 Conclusions

The main results may be summarized as follows. First, board and CEO characteristics

are substitutes and complements in the formation of board composition and size. This

confirms Demsetz and Lehn (1985) theory that internal governance mechanisms are cho-

sen in conjunction so as to harmonize with each other. Second, the external governance

mechanisms are important in understanding the choice of board and CEO characteris-

tics. The MFI’s ownership type and international initiation favour smaller board and

international directors. Third, the financial performance does not endogenously deter-

mine board characteristics (Hermalin and Weisbach, 1998), instead, there is a link to the

MFI’s choice of female CEO. Fourth, outreach performance is more important for the

16

associations to board and CEO characteristics than financial performance. We put this

down to different information needs when the MFI aims to reach out to specific customer

groups, such as women. Models in Raheja (2005) and Harris and Raviv (2008) predict

these outcomes. Fifth, we find consistency in the relationships between variables and

board size and composition. Thus, when the variable is negatively associated with board

size, it is positively related to international directors and female CEO.

The results from this study are in line with those that Mayers and Smith (2005) find

for mutual and shareholder owned insurance companies, and the evidence in Barth et al.

(2007) on an international sample of banks.

The implications following from these results are first of all, researchers should take

account of the relationships existing between different governance mechanisms when in-

vestingating the impact upon performance. For instance, Mersland and Strøm (2009)

find that ownership type plays no role in explaining financial performance in the MFI.

But perhaps the effect is indirect, say through its influence in reducing board size. An-

other implication is that the MFI should balance its board in several dimensions; first, it

should find a balance between different board and CEO characteristics, second, this in-

ternal balance should address the needs existing among external governance mechanisms

and the chosen customer segment.

17

References

Adams, R. B. and D. Ferreira (2007, Feb). A theory of friendly boards. Journal of Finance 62 (1),217–250.

Agrawal, A. and C. R. Knoeber (1996, Sep). Firm performance and mechanisms to controlagency problems between managers and shareholders. Journal of Financial and QuantitativeAnalysis 31 (3), 377–397.

Allen, F. and D. Gale (2000). Corporate Governance and competition, Chapter 2, pp. 23–84.Cambridge: Cambridge University Press.

Armendariz de Aghion, B. and J. Morduch (2005). The Economics of Microfinance. Cambridge:MIT Press.

Barth, J. R., M. J. Bertus, V. Hartarska, H. J. Jiang, and T. Phumiwasana (2007). A cross-country analysis of bank performance: the role of external governance. In B. E. Gup (Ed.),Corporate Governance in Banking, Chapter 8, pp. 151–183. Cheltenham, UK: Edward ElgarPublishing.

Brickley, J. A., J. L. Coles, and G. Jarrell (1997). Leadership structure: Separating the CEOand chairman of the board. Journal of Corporate Finance 3 (3), 189–220.

Demsetz, H. and K. Lehn (1985, Dec). The structure of corporate ownership: Causes andconsequences. Journal of Political Economy 93 (6), 1155–1177.

Dowla, A. and D. Barua (2006). The Poor Always Pay Back. The Grameen II Story. Bloomfield,USA: Kumarian Press, Inc.

Easterbrook, F. H. (1984, Sep). Two agency-cost explanations of dividends. American EconomicReview 74 (4), 650–59.

Eisenberg, T., S. Sundgren, and M. T. Wells (1998). Larger board size and decreasing firmvalue in small firms. Journal of Financial Economics 48, 35–54.

Ghatak, M. and T. W. Guinnane (1999). The economics of lending with joint liability: Theoryand practice. Journal of Development Economics 60, 195–228.

Greenbaum, S. I. and A. V. Thakor (2007). Contemporary Financial Intermediation. Amster-dam: Elsevier.

Harris, M. and A. Raviv (2008). A theory of board control and size. Review of FinancialStudies 21 (4), 1797–1832.

Hayashi, F. (2000). Econometrics. Princeton and Oxford: Princeton University Press.

Hermalin, B. E. and M. S. Weisbach (1998, Mar). Endogenously chosen boards of directors andtheir monitoring of the CEO. American Economic Review 88 (1), 96–118.

Hermalin, B. E. and M. S. Weisbach (2003, Apr). Boards of directors as an endogenouslydetermined institution: A survey of the economic literature. Economic Policy Review 9 (1),7–26.

18

Jensen, M. C. (1986). Agency cost of free cash flow, corporate finance and takeovers. AmericanEconomic Review 76, 323–339.

Kennedy, P. (2008). A Guide to Econometrics (6th ed. ed.). Oxford, UK: Blackwell Publishing.

Manne, H. (1965). Mergers and the market for corporate control. Journal of Political Econ-omy 73, 110–120.

Mayers, D., A. Shivdasani, and C. W. Smith (1997). Board composition and corporate control:Evidence from the insurance industry. Journal of Business 70 (1), 33–62.

Mayers, D. and C. W. Smith (2005). Agency problems and the corporate charter. Journal ofLaw, Economics, and Organization 21 (2), 417–440.

Mersland, R. and R. Ø. Strøm (2009). Performance and governance in microfinance institutions.Journal of Banking & Finance.

OECD (2004). OECD Employment Outlook. Paris: OECD.

Oxelheim, L. and T. Randøy (2003). The impact of foreign board membership on firm value.Journal of Banking & Finance 27 (12), 2369–2392.

Raheja, C. G. (2005). Determinants of board size and composition: A theory of corporateboards. Journal of Financial and Quantitative Analysis 40 (2), 283–306.

Rock, R., M. Otero, and S. Saltzman (1998). Principles and practices of microfinance gover-nance. Microenterprise Best Practices.

Schmidt, K. M. (1997). Managerial incentives and product market competition. Review ofEconomic Studies 64, 191–213.

Schreiner, M. (2002). Aspects of outreach: A framework for discussion of the social benefits ofmicrofinance. Journal of International Development 14, 591–603.

Strøm, R. Ø. (2009). Better firm performance with employees on the board? In P. O. Bjuggrenand D. Mueller (Eds.), The Modern Firm, Corporate Governance and Investment. London:Edward Elgar Publishing.

Tirole, J. (2006). The Theory of Corporate Finance. Princeton: Princeton University Press.

Woolridge, J. M. (2002). Econometric Analysis of Cross Section and Panel Data. Cambridge,Mass.: The MIT Press.

Yermack, D. (1996). Higher market valuation of companies with a small board of directors.Journal of Financial Economics 40, 185–212.

19

Table 1 Definitions of dependent variables and their main statistical properties

Mean Std Min Max ObsBoard size The number of directors 7.492 3.807 2 33 256Duality A dummy indicating CEO and chair-

man are the same person when 10.142 0.350 0 1 246

Int.dir A dummy indicating international di-rectors when 1

0.228 0.421 0 1 232

Female CEO A dummy indicating a female when 1 0.246 0.432 0 1 244

Table 2 Bivariate correlations of board and CEO characteristicsFemale

Duality Int.dir. CEOBoard size -0.036 -0.133 0.237Significance 0.593 0.058 0.000N 224 205 220Duality -0.151 0.018Significance 0.038 0.797N 191 216Int. director -0.056Significance 0.454N 184

Table 3 Descriptive statistics of main explanatory variables

Mean Median Std Min Max NSHF 0.284 0 0.452 0 1 289Bank regulated 0.302 0 0.460 0 1 288Int. initiated 0.376 0 0.485 0 1 290Competition 4.358 5 1.623 1 7 268ROA 0.013 0.026 0.127 -0.898 0.790 931Average loan 689 430 779 1 6946 943Individual loan 0.516 1 0.501 0 1 281Gender bias 0.440 0 0.497 0 1 234Loan products 4.046 3 2.978 1 30 281Urban 0.353 0 0.479 0 1 275PaR30 0.068 0.037 0.102 0.000 0.980 910MFI age 9.207 7 7.317 0 79 1005MFI size 14.879 14.880 1.365 9.856 19.337 977HDI 0.702 0.745 0.123 0.366 0.874 1152

SHF is a dummy being 1 if the MFI is shareholder owned; Bank regulated is a dummy being 1 if the MFI is undergovernmental regulation; Int. initiated is a dummy being 1 if the MFI is started by an international organization;Competition is a 1 to 7 scale of perceived competition in the MFI’s market; ROA is return on assets; Average loan is theoutstanding loan portfolio divided by the number of borrowers; Individual loan is a dummy being 1 if the MFI is mainlygranting individual loans; Gender bias is a dummy being 1 if the MFI is consciously giving priority to female borrowers;Loan products is the number of financial products the MFI offers; Urban is a dummy being 1 if the MFI is mainly lendingin urban areas; PaR30 is the portfolio at risk, that is, the fraction of loans 30 days overdue; MFI age is the number ofyears since the MFI started; MFI size is the logarithm of assets; HDI is the human development index for each country.

Table

4B

ivar

iate

corr

elat

ions

ofex

pla

nat

ory

vari

able

s

Ban

kIn

t.C

om-

Avg.

Indiv

.G

ender

Loa

nM

FI

MFI

regu

l.in

itpet

itio

nR

OA

loan

loan

bia

spro

d.

Urb

anPaR

30ag

esi

zeH

DI

shf

0.5

05

0.04

00.

029

-0.0

330.

034

0.14

0-0

.178

0.1

93

-0.1

23-0

.078

-0.0

630.2

28

-0.1

33B

ank

regu

l0.

045

0.02

10.

019

0.09

10.1

72

-0.1

670.2

85

-0.1

20-0

.047

0.08

00.2

75

-0.1

74

Int.

init

-0.1

47-0

.017

-0.1

42-0

.110

0.04

0-0

.164

0.00

2-0

.194

-0.2

04

0.01

3-0

.131

Com

pet

itio

n-0

.052

0.08

00.

077

-0.0

910.2

05

-0.0

820.

046

0.08

40.

091

-0.0

53R

OA

0.07

80.2

18

-0.1

630.

035

0.1

75

-0.1

96

0.06

10.2

84

0.2

01

Ave

rage

loan

0.4

70

-0.3

99

0.05

7-0

.015

0.2

13

0.02

40.2

25

0.2

82

Indiv

idual

loan

-0.5

10

0.08

50.1

91

0.13

20.

032

0.3

05

0.2

72

Gen

der

bia

s-0

.163

-0.1

25-0

.101

0.03

3-0

.190

-0.2

14

Loa

npro

duct

s-0

.180

0.01

00.3

89

0.2

73

-0.0

12U

rban

-0.0

07-0

.052

-0.1

360.1

83

par

300.1

84

-0.0

28-0

.005

MFI

age

0.2

76

-0.0

03M

FI

size

-0.0

23

Em

phasi

zed

text

indic

ate

s5%

signifi

cance

level

;em

phasi

zed

and

bold

text

indic

ate

s1%

signifi

cance

level

.C

ondit

ion

num

ber

=18702.5

3

Table

5A

reav

erag

esth

esa

me?

Expla

nat

ory

vari

able

ske

yst

atis

tics

insm

all

and

larg

eboa

rdsu

bsa

mple

s.A

NO

VA

test

sof

expla

nat

ory

vari

able

s’diff

eren

cein

aver

ages

.Sig

nifi

cant

resu

lts

are

give

nin

bol

d.

Fem

ale

Sm

allbo

ard

Lar

gebo

ard

Dual

ity

Intd

irC

EO

Mea

nStd

NM

ean

Std

NF

Sig

.Sig

.Sig

.Sig

.Boa

rdan

dC

EO

char

acte

rist

ics

Boa

rdsi

ze0.

593

0.0

58

0.0

00

Dual

ity

0.16

20.

370

990.

136

0.34

412

50.

286

0.59

30.0

38

0.79

7In

t.dir

ecto

r0.

309

0.46

597

0.19

40.

398

108

3.63

50.0

58

0.0

38

0.45

4Fem

ale

CE

O0.

139

0.34

710

10.

345

0.47

711

912

.972

0.0

00

0.79

70.

454

Ext

ernal

gove

rnan

cem

echa

nis

ms

SH

F0.

345

0.47

811

30.

217

0.41

414

35.

301

0.0

22

0.80

30.0

00

0.0

26

Ban

kre

gula

ted

0.29

20.

457

113

0.30

10.

460

143

0.02

30.

881

0.54

50.0

44

0.35

7In

t.in

itia

ted

0.42

50.

497

113

0.36

90.

484

141

0.82

00.

366

0.0

04

0.0

00

0.30

5C

ompet

itio

n4.

790

1.57

310

53.

962

1.52

713

016

.660

0.0

00

0.44

30.

996

0.18

9Fin

anci

alpe

rfor

man

ceR

OA

0.01

30.

082

111

0.01

30.

109

138

0.00

00.

993

0.65

10.

330

0.0

10

Outrea

chpe

rfor

man

ceA

vera

gelo

an81

890

111

053

962

313

98.

279

0.0

04

0.23

80.

833

0.72

4In

div

idual

loan

0.56

10.

499

107

0.46

60.

501

133

2.12

30.

146

0.18

70.

580

0.15

9G

ender

bia

s0.

351

0.48

094

0.52

60.

502

114

6.54

10.0

11

0.82

70.

775

0.10

7Loa

npro

duct

s4.

117

2.63

811

13.

797

2.58

913

80.

924

0.33

70.

438

0.92

50.0

09

Urb

an0.

273

0.44

711

00.

406

0.49

313

34.

783

0.0

30

0.64

20.

247

0.45

3

Table 6 Can substitution, external governance mechanisms, financial or outreach perfor-mance explain board and CEO characteristics? Logistic regressions of 290 microfinanceinstitutions in 61 countries

Dependent variableBoard Internat. Female

size Duality director CEOBoard and CEO characteristicsBoard size 0.007 0.8806 1.2541

Duality -0.348 -1.6378 -0.052Int. director 0.9914 -1.6848 -0.099Female CEO 1.2471 0.651 -0.648External governance mechanismsSHF -2.1501 1.273 2.5941 -2.2411

Bank regulated -0.078 -0.070 0.573 1.0033

Int. initiated -1.1041 -3.1431 2.9421 -0.544Competition -0.119 0.194 -0.152 -0.114Financial performanceROA 1.072 -1.863 -3.952 3.0738

Outreach performanceAverage loan 0.000 -0.001 0.000 0.000Individual loan -0.497 -1.1969 1.6131 -0.332Gender bias -0.6887 -1.0669 1.4381 -0.270Loan products -0.2362 -1.3641 -0.028 -0.2075

Urban 0.367 1.2434 -0.345 0.027Control variablesPaR30 -3.071 -0.444 -7.3419 -2.459MFI age -0.039 -0.1463 -0.1242 0.030MFI size 0.087 1.5821 0.356 -0.148HDI -0.196 -5.6935 0.275 3.30710

Constant 0.380 -15.577 -8.316 -0.238Pseudo R2 0.329 0.529 0.622 0.339Likelihood ratio (p-value) 0.000 0.000 0.000 0.000Overall correctly classified 77.961 94.766 83.747 79.614N 363 363 363 363

The explanatory variable’s percentage significance level is indicated by the raised number.

Table 7 Robustness check running each main group and control variables in isolation.Control variable estimates are dropped.

Dependent variableBoard Internat. Female

size Duality director CEOBoard and CEO characteristicsBoard size -0.107 -0.210 1.0701

Duality -0.167 -2.0871 -0.296Int. director -0.271 -2.2111 -0.6034

Female CEO 1.0861 -0.1933 -0.637Pseudo R2 0.076 0.129 0.291 0.123N 511 511 511 511External governance mechanismsSHF -1.6261 0.087 1.5591 -0.8841

Bank regulated 0.4158 -0.412 0.002 0.263Int. initiated -0.4702 -1.5481 2.5861 -0.3845

Competition -0.3341 -0.048 0.2391 -0.0969

Pseudo R2 0.185 0.107 0.484 0.083N 712 709 608 678Financial performanceROA 0.024 -1.088 -3.0681 3.7461

Pseudo R2 0.025 0.026 0.246 0.079N 772 768 672 744Outreach performanceAverage loan 0.0003 0.000 0.000 0.000Individual loan -0.4855 -1.0171 0.45510 -0.6901

Gender bias 0.194 -1.0651 0.5415 0.170Loan products -0.011 -0.1742 0.005 -0.1045

Urban 0.3797 0.421 -0.4437 0.225Pseudo R2 0.078 0.117 0.252 0.123N 573 582 517 579