uncharted territory: investigating individual business ethics in cyprus

TRANSCRIPT

Uncharted territory:investigating individualbusiness ethics in Cyprus

Maria Krambia-Kapardisand Anastasios Zopiatisn

The research purpose of the study is to investigate and identify correlates of ethical behaviour and

attitudes of individuals currently working or pursuing a business-related graduate degree in Cyprus.

Analysis of the quantitative questionnaire revealed that the majority of the respondents had a concept of

‘ethical behaviour’, consider ethics important, and hold attitudes that are conducive to ethical behaviour

in business. In addition, findings revealed significant differences in three correlates: age, gender and

position. Finally, reflecting the findings, the authors suggest specific actions that aim to improve ethical

decision making in the Cyprus business environment.

Introduction

Studies on various issues in business have

concentrated on surveying developed economies

and/or powerful countries. There is an apparent

lack of studies, however, on less-developed or

developing economies and on countries with

populations of less than a million people. Cyprus,

an island of approximately 800,000 inhabitants, is

part of this category; an island that has endured

years of occupations and invasions but has

managed to surmount any economic and social

hardships and join the European Union in 2004.

An example of Cyprus’ outstanding economic

situation is not only the fact that it is adopting the

Euro in January 2008 but, also, the recognition it

received by the Index of Economic Freedom 2007

(Wall Street Journal 2007). It has been classified

20th out of 157 countries included in the Index.

Finally, Cyprus, though not one of the 64

countries studied by Hofstede in his seminal work,

falls into the Uncertainty Avoidance quadrant,

with low tolerance on ambiguity. As Hofstede

himself states, any country with more than 50% of

its population practising the Greek Orthodox or

Catholic religion, is found to be in the ‘Uncer-

tainty Avoidance quadrant’ with low tolerance on

ambiguity. Hofstede states this ‘creates a highly

rule-oriented society that institutes laws, rules,

regulations, and controls in order to reduce the

amount of uncertainty within the population’

(www.geert-hofstede.com). In this sense, Cyprus

is a good example of a country plagued by conflict

for most of its history but which has achieved very

significant economic and social development.

Findings from the survey reported below should

be of interest to similar countries.

Literature review

There is a large body of literature on business

ethics and much research has been carried out in

nRespectively, Associate Professor of Accounting and Lecturer in

Hotel and Tourism Management, both at Department of Hotel and

Tourism Management, Cyprus University of Technology, Limassol,

Cyprus.

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd, 9600 Garsington Road,Oxford, OX4 2DQ, UK and 350 Main St, Malden, MA 02148, USA138

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

this area. Business academics have been reporting

empirical studies in this field since the 1980s when

the outgoing chairman of the US Securities

Exchange Commission, John Shad, donated the

bulk of a $30 million gift to Harvard Business

School to fund a business ethics program (Brophy

1987).

Perspectives on ethical behaviour

Some researchers have attempted to explain and

provide insights into why individuals engage in

unethical behaviour. There are five theories,

which appear to highlight the key dimensions of

why a manager would be unethical:

(a) Rational Choice Theory: While the theory was

proposed by economists (Piliavin et al. 1986,

Michaels & Miethe 1989) to explain and

predict behaviour generally and decision

making in particular, it is also applicable in

the case of ethics in business. The individual

assesses the rewards and punishments with

certain behaviours, by carrying out a cost/

benefit analysis. If the expected benefits

exceed the costs then the individual will

proceed with the behaviour.

(b) Deterrence Theory: A particular behaviour is

deterred in direct proportion to the perceived

probability of being caught and the severity of

the punishment for the behaviour when

caught (Buckley et al. 1998: 72). If, for

example, a manager feels that his actions will

be exposed, thus losing his position and being

blacklisted from finding a similar position,

then he is likely not to behave in an unethical

manner.

(c) Social Bond Theory: Developed by Hirschi

(1969), it predicts that unethical behaviour

emerges from a weakening of social bonds to

mainstream society. As Buckley et al. (1998:

72–73) state, ‘if people feel disconnected from

society, they are more prone to behave in ways

which are not socially acceptable’.

(d) Differential Association-Reinforcement Theo-

ry: This is a combination of differential

association theory of deviance (Sutherland &

Cressey 1970) and social learning theory

(Bandura 1972) and was proposed by Akers

(1985). If a manager is a member of a deviant

group that supports unethical behaviour then

he is likely to behave in the same way.

(e) Everybody Else Does it Theory: This is an

attribution theory (Wiese & Buckley 1997)

that simply assumes that if others are un-

ethical and it is common and acceptable

behaviour, then to keep up with them,

managers too engage in unethical behaviour.

In the same way that monolithic theory cannot

account adequately for criminal behaviour (Bartol

2002: 1–7), none of the theoretical perspectives

mentioned above is without its limitations and,

furthermore, they are not mutually exclusive. The

fact of the matter is that they all ignore that

different individuals may choose to act ethically

for different reasons. No study has yet tested the

predictive utility of the five theories. Therefore, a

researcher at best can hope to identify the best

correlates of ethical behaviour as in the study

reported below.

The present authors believe that all five theories

are applicable in Cyprus and because these

theories explain individual ethical behaviour and

not a culture-wide ethical behaviour, it is believed

that such theories basically explain why one

would behave in a certain way. The geographical

position of Cyprus attracts a variety of people

from various part of the world in search of work.

Drawing on Kapardis (2006: 147–148), according

to the Statistics Department of the Ministry of

Labour, in 2005 there was a total of 45,886 people

working in the Republic of Cyprus from non-EU

countries. Workers from EU member countries

numbered 13,168 in the same year. An additional

number of 7,745 people applied for asylum.

Finally, according to the immigration unit of the

Cyprus Police the number of illegal immigrants

in Cyprus was estimated to be approximately

30,000. Thus, about 10% of the population are

foreigners. What is noteworthy, also, is that the

population multiplies, especially between May

and September every year, as about 1 million

tourists visit Cyprus. Consequently, Cypriots’

behaviour and attitudes to different aspects of

life have been influenced by many exogenous

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd. 139

elements, classifying Cyprus as a country where

all theories are applicable.

Studies of correlates of ethics in business

Many researchers have addressed the relationship

between ethics and gender (Collins 2000). ‘Ethical

behaviour’ in this context has been used (Ruegger

& King 1992) to refer to one’s perception of

business ethical conduct, i.e. what stance one

adopts towards certain business practices (Weeks

et al. 1999). Females have been reported as being

more ethically sensitive than males (Peterson et al.

1991, Ruegger & King 1992, Harris & Sutton

1995, Dawson 1997, Weeks et al. 1999, Coate &

Frey 2000, Larkin 2000, Simga-Mugan et al.

2005). Simga-Mugan et al. found that females

were more ethically sensitive than males on all 16

vignettes they used. One possible explanation for

the apparent gender differences reported has been

in terms of gender differences in the early

socialization of females (Peterson et al. 2001:

226). In this vein, Church et al. (2005: 363) have

argued that ‘gender was significant, both directly

and in interaction with moral development’. For

their part, Peterson et al. (2001) claimed that,

whilst the young females demonstrated a higher

level of ethical behaviour than males, the elder

males showed a slightly higher level of ethical

behaviour than females in the groups they

surveyed. Dawson (1997) has argued that whether

there are gender differences or not depends on the

particular situation in terms of the context of the

scenario or ethical situation investigated.

A number of authors (e.g., Singhapakdi & Vitell

1990, Davis & Welton 1991, Radtke 2000),

however, have reported no gender differences in

business ethics. As Smith & Oakley (1997: 39)

state, ‘empirical evidence of gender influences on

ethical viewpoints continues to present confused

and often contradictory results’ and that may well

be due to gender differences in personal moral

orientation which may well be affected by the type

of moral problem being faced (Schminke &

Ambrose 1997). Furthermore, gender differences

may well be context-specific (Dobbins & Platz

1986, Derry 1989, Weber 1990, Trevino 1992).

It can be seen that, while no conclusion is possible

on gender differences on the basis of the available

literature, it does appear that age may well

mediate the relationship, if any, between gender

and ethical judgements.

The influence of managers’ nationality on their

ethical sensitivity has been examined by

Simga-Mugan et al. (2005) in a study of 103

managers in Turkey and 57 in the United States

using 16 vignettes. They found that Turkish males

were more ethically sensitive than their US

counterparts (149). One possible explanation

provided by Simga-Mugan et al. for their country

differences is that ‘ethics of care’ is emphasized in

Turkey whereas in the United States it is ‘ethics of

justice’ that is emphasized (155). The difference

reported between managers in the two countries is

of interest given that, according to the

Transparency International report regarding per-

ceived levels of corruption in 15 countries for

2005, Turkey had a mean score of 3.5 (i.e. ranked

65th) whereas that of the United States was

7.6 (i.e. 17th). This index, therefore, casts doubts

on the significance of Simga-Mugan et al.’s (2005)

findings that Turkish males are more ethically

sensitive than their US counterparts.

Tsalikis & LaTour (1995) investigated differ-

ences in the way bribery and extortion were

perceived by American and Greek business

students and found that: (a) ethical reactions to

bribery and extortion vary by the nationality of

the person offering the bribe and the country

where the bribe is offered; and (b) Greeks

perceived some of the scenarios used as being less

unethical than did Americans.

The importance of culture in MBA students’

ethical ideologies has also been demonstrated by

Axinn et al. (2004), who compared students in the

United States, Malaysia and Ukraine and con-

cluded, like Christies et al. (2003), that culture,

however defined, affects both values and ethics.

Christie et al. have differentiated between

(a) respondents’ general attitudes towards

business ethics and (b) their attitudes towards

questionable business practices and concluded

that the former are related to their personal

integrity while the latter are related ‘to the

external environment and gender, as well as to

their personal integrity’ (263).

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

140r 2008 The Authors

Journal compilation r 2008 Blackwell Publishing Ltd.

Bearing in mind that a manager’s age usually

correlates with work experience, the relationship

between age and ethical beliefs was examined by

Peterson et al. (2001), who found that younger

aged professionals (30 years or less) exhibited a

lower standard of ethical beliefs; in other words,

‘as managers get older they become more . . .

ethical’ (230). Peterson et al.’s conclusion confirms

the finding reported earlier by Trevino (1986) that

the ethical judgements displayed by a practitioner

are related to his/her career stage. Of course, a

manager does not exist in a vacuum but in relation

to significant others in the company. Not surpris-

ingly, therefore, Wiley (1998) has argued that,

regardless of gender, position or company size, a

managers’ ethical behaviour is influenced most by

the behaviour of senior managers and their

immediate supervisors. It can be seen that no

definitive conclusions can be drawn on the basis of

the findings reported in the literature because of

conflicting findings, for example and, also because

no study has examined the importance in man-

agers’ ethical behaviour holding constant other

known correlates. The best that can be surmised

on the basis of the studies discussed above is that

they indicate that a manager’s gender, age, religion

and work experience may well be related to his/her

ethical behaviour.

Research methodology

A quantitative questionnaire was developed and

randomly distributed to 1000 individuals cur-

rently working in Cyprus or pursuing a graduate

business degree (MBA). It was a randomly

selected sample and an attempt was made to

cover all the districts in the non-Turkish part of

Cyprus and all the different industries. The

questionnaire was designed to enable the authors

to:

1. investigate age and gender differences between

professionals with regard to their ethical

perspectives; and

2. investigate probable differences between the

respondents according to their professional

positions.

To ensure a higher response rate, a mixed

distribution method including postal, group and

face-to-face distribution was used to administer

the questionnaire. Finally, utilizing the Statistical

Package for Social Sciences (SPSS), the authors

analyzed the collected data using both descriptive

and inferential statistics. In particular, the authors

utilized independent sample t-test, ANOVA and

Post-hoc multiple comparison tests (Tukey’s

Honestly Significant Difference (HSD) Test) to

identify differences between the respondents as a

function of their gender, age and position cur-

rently held. The authors acknowledge the fact that

when conducting multiple post-hoc comparisons

the family-wise Type I1 error rate is increased.

Unfortunately, this issue has no simple answer.

Rothman (1990) argues that no adjustment is

needed in multiple comparison tests and that each

result should stand on its own and be accepted or

rejected by the work of others. Other scholars (e.g.

Tukey 1991) suggest the utilization of statistical

tests in order to control family-wise error rates.

For our statistical analysis we utilized the Tukey

HSD Test, because it is a very conservative pair-

wise comparison test that minimizes the possibility

of Type I errors. Before administering the survey,

the instrument was tested for reliability by using

the test re-test method.

Findings

From the 1000 questionnaires administered, 565

were completed and returned to the researchers.

Of these, 21 survey questionnaires were incom-

plete, and thus excluded from the study, reducing

the number of usable ones to 544. The overall

usable response rate of 54.4%, the outcome of the

mixed distribution method utilized by the authors,

was viewed as satisfactory considering the low

response rates experienced by other research

activities conducted in Cyprus.

Table 1 displays the demographic and profes-

sional profile of the participants in relation to five

different variables: gender, age, educational back-

ground, professional capacity (position) and the

type of company the respondents are currently

working for.

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd. 141

Ethics: the corporate culture

As already discussed in the literature review

above, the company context is a salient factor in

investigating the ethical judgements of managers.

Research findings show that about two-thirds of

the respondents’ companies involved had a code

of conduct, 86% did not print dishonest state-

ments in advertisements concerning quality or

comparative prices, 72% would not intentionally

pay a bill late and still claim a discount and,

finally, in over half (55%) of the cases the

respondents were considered by their manager as

an associate rather than an employee.

Views on ethics

Research findings indicate that the majority of the

respondents: considered ethics and ethical actions

important (96%), knew the meaning of ‘ethical

behaviour’ (94%), were in favour of whistle-

blowing legislation being introduced in Cyprus

(82%), believed that teaching Business Ethics to

MBA students can prevent unpleasant situations

(78%), believed that moral standards in business

were not fully developed and could be changed,

and for 62% the ethics in the office was the same

as at home. Two-thirds considered ethical pro-

blem-solving skills relevant or believed they could

be applied to business.

Gender differences

In support of other studies discussed above,

female respondents (see Table 2) were found to

be significantly (po0.05%) more ethical than

their male counterparts as far as the following

issues are concerned: (a) would not falsify their

tax records to save taxes, (b) would not hurt

others to achieve advancement, (c) would not put

on the pressure and load it with incentives and

fear, forcing people to forgo their ethics in the

chase for the profit objective, (d) would not be

willing to head-hunt prospective employees from

their competitors in order to obtain trade secrets

of their prior employer, (e) their ethics in the office

is the same as those at home, and (f) peer pressure

and competition do not make their ethics

different.

Position differences

Managers were found to be significantly

(po0.05%) more ethical on the following items

than those who were employees (not including

students who were not in full-time employment):

(a) they would be willing to accept more than their

share of responsibility for errors in their depart-

ment, (b) if they held too much inventory they

would not make returns on the pretence that the

goods are imperfect or not according to samples

sent, (c) their ethics in the office are the same as

those at home, (d) they would not be willing to cut

corners by selling overripe produce or outdated

products, having too much fat in the ground beef

using the wrong tare weight in meatpacking, (e)

would not accept a foreign country’s customs

even though the EU considers some of them

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 1: Demographic and professional profile of the

respondents

Frequency Valid

percentage

Gender

Male 307 56.5

Female 236 43.5

Age

20–25 161 29.8

26–30 144 26.6

31–40 129 23.8

Over 40 107 19.8

Educational background

Secondary school 71 13.3

Bachelor’s/diploma 251 46.9

Masters 197 36.8

Doctorate 16 3.0

Professional capacity

Management 167 30.8

Supervisor 85 315.7

Employee 252 46.4

Not working/student 39 7.2

Type of company

Public company (listed) 65 12.1

Public company (not listed) 16 3.0

Private company 308 57.1

Semi-governmental 60 11.1

Government 51 9.5

Not applicable 39 7.2

(N 5 544).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

142r 2008 The Authors

Journal compilation r 2008 Blackwell Publishing Ltd.

totally dishonest, (f) would not talk to colleagues

about their promotion application in a public

place, (g) do not believe they can get rich through

financial manipulation, (h) they believe that peer

pressure and competition does not make ethics

different, and (i) would not be willing to head-

hunt prospective employees from their competi-

tors in order to obtain trade secrets of their prior

employer. More specifically, as indicated in Table 3,

the higher the position that a manager holds, the

more ethical he/she is.

Drawing on the correlates of ethical judgements

by managers identified in the literature review

above, one plausible explanation for the differ-

ences found between managers and other employ-

ees may well be differences in age and experience.

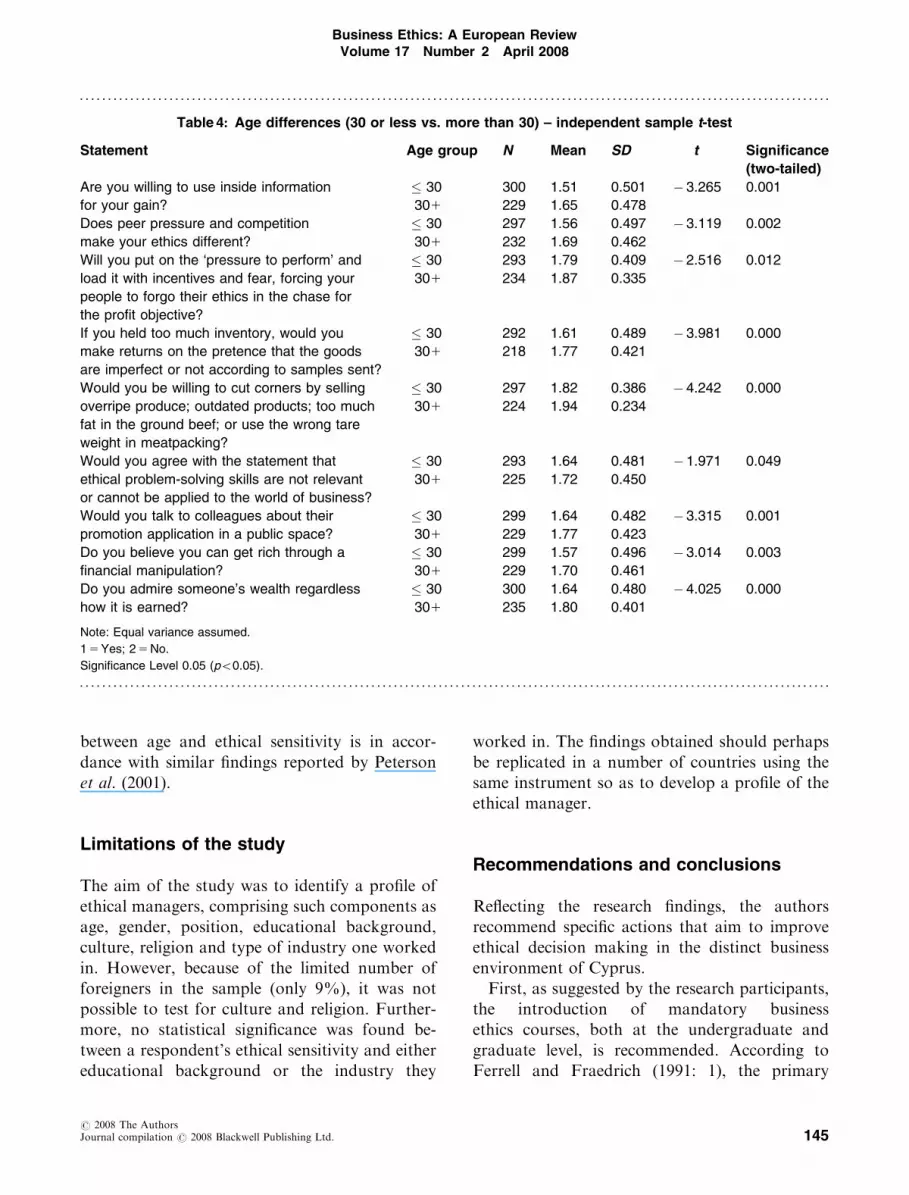

Age differences

The respondents were grouped into those younger

than 30 years and those over 30 years (Peterson

et al. 2001). On the basis of the Cyprus Census

(2001), normally by the time someone in Cyprus is

30, he/she has completed their tertiary education,

has got a job and, most likely, has started a

family. Therefore, the authors consider the age of

30 to be a crucial turning point in one’s life. It was

found (see Table 4) that ‘older managers’ are

significantly (po0.05%) more ethical than the

younger ones on the following issues: (a) would

not be willing to use inside information for their

gain; (b) do not believe that peer pressure would

make their ethics different; (c) would not put on

the pressure to perform and load it with incentives

and fear, forcing their people to forgo their ethics

in the chase for the profit objective; (d) if they held

too much inventory they would not make returns

on the pretence that the goods are imperfect or

not according to samples sent; (e) would not be

willing to cut corners by selling overripe produce

or outdated products, or using too much fat in the

ground beef, or using the wrong tare weight in

meatpacking; (f) would not talk to colleagues

about their promotion application in a public

place; (g) do not believe that they can get rich

through financial manipulation; and, finally, (h)

do not admire someone’s wealth regardless of

how it is earned. The positive relationship

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 2: Gender differences – independent sample t-test

Statement Sex N Mean SD t Significance

(two-tailed)

Would you falsify your records to save

taxes?

Male 304 1.66 0.473 � 3.435 0.001

Female 232 1.80 0.403

Are your ethics in the office the same as

those you use at home?

Male 301 1.45 0.499 3.746 0.000

Female 234 1.29 0.457

Does peer pressure and competition

make your ethics different?

Male 301 1.56 0.497 � 2.995 0.003

Female 230 1.69 0.463

Would your hurt others to achieve

advancement?

Male 302 1.89 0.317 � 2.112 0.035

Female 233 1.94 0.238

Will you put on the ‘pressure to perform’

and load it with incentives and fear,

forcing your people to forgo their ethics in

the chase for the profit objective?

Male 298 1.78 0.416 � 3.455 0.001

Female 231 1.89 0.311

Would you be willing to head-hunt

prospective employees from your

competitors in order to obtain trade

secrets of their prior employer?

Male 298 1.69 0.464 � 2.825 0.005

Female 231 1.80 0.403

Note: Equal variance assumed.

1 5 Yes; 2 5 No.

Significance Level 0.05 (po0.05).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd. 143

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 3: Differences according to position (one-way ANOVA and Post-Hoc Multiple

Comparison Tests; Tukey HSD)

Source DF Sum of

squares

Mean of

squares

F ratio F probability

(significant)

Mean Post-Hoc Analysis

(Tukey HSD)

VAR: Are your ethics in the office the same as those you use at home? M S E NWS

Between groups 3 3.113 1.038 4.476 0.004 M: 1.35 n

Within groups 531 123.100 0.232 S: 1.45

Total 534 126.213 E: 1.34 n

NWS: 1.62 n n

VAR: Does peer pressure and competition make your ethics different?

Between groups 3 2.734 0.911 3.923 0.009 M: 1.68 n

Within groups 527 122.422 0.232 S: 1.48 n n

Total 530 125.156 E: 1.64 n

NWS: 1.53

VAR: Would you be willing to head-hunt prospective employees from your competitors in order to obtain trade secrets of their prior

employer?

Between groups 3 2.579 0.860 4.496 0.004 M: 1.70

Within groups 525 100.370 0.191 S: 1.76 n

Total 528 102.949 E: 1.78 n

NWS: 1.51 n n

VAR: Would you be willing to accept more than your share of responsibility for errors in your department?

Between groups 3 4.736 1.579 6.616 0.000 M: 1.30 n n

Within groups 530 126.470 0.239 S: 1.46

Total 533 131.206 E: 1.49 n

NWS: 1.58 n

VAR: If you held too much inventory, would you make returns on the pretence that the goods are imperfect or not according to samples

sent?

Between groups 3 3.508 1.169 5.479 0.001 M: 1.79 n n n

Within groups 507 108.214 0.213 S: 1.62 n

Total 510 111.722 E: 1.65 n

NWS: 1.51 n

VAR: Would you be willing to cut corners by selling overripe produce; outdated products; too much fat in the ground beef; or use the

wrong tare weight in meatpacking?

Between groups 3 1.170 0.390 3.531 0.015 M: 1.92 n

Within groups 518 57.230 0.110 S: 1.87

Total 521 58.400 E: 1.86

NWS: 1.74 n

VAR: Would you accept foreign countries customs even though the EU considers some of them totally dishonest?

Between groups 3 3.012 1.004 5.042 0.002 M: 1.82 n n n

Within groups 528 105.129 0.199 S: 1.65 n

Total 531 108.141 E: 1.70 n

NWS: 1.56 n

VAR: Would you talk to colleagues about their promotion application in a public space?

Between groups 3 2.797 0.932 4.455 0.004 M: 1.79 n

Within groups 526 110.073 0.209 S: 1.71

Total 529 112.870 E: 1.63 n

NWS: 1.66

VAR: Do you believe you can get rich through a financial manipulation?

Between groups 3 2.356 3785 3.384 0.018 M: 1.70 n

Within groups 530 122.987 0.232 S: 1.52 n

Total 533 125.343 E: 1.62

NWS: 1.53

1 5 Yes; 2 5 No.

Note: M, Management (N 5 167); S, Supervisors (N 5 85); E, Employees (N 5 252); NWS, Not Working/Students (N 5 39).nIndicates a significant difference between the four groups. Post-Hoc Analysis (Tukey test): Significance Level 0.05 (po0.05).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

144r 2008 The Authors

Journal compilation r 2008 Blackwell Publishing Ltd.

between age and ethical sensitivity is in accor-

dance with similar findings reported by Peterson

et al. (2001).

Limitations of the study

The aim of the study was to identify a profile of

ethical managers, comprising such components as

age, gender, position, educational background,

culture, religion and type of industry one worked

in. However, because of the limited number of

foreigners in the sample (only 9%), it was not

possible to test for culture and religion. Further-

more, no statistical significance was found be-

tween a respondent’s ethical sensitivity and either

educational background or the industry they

worked in. The findings obtained should perhaps

be replicated in a number of countries using the

same instrument so as to develop a profile of the

ethical manager.

Recommendations and conclusions

Reflecting the research findings, the authors

recommend specific actions that aim to improve

ethical decision making in the distinct business

environment of Cyprus.

First, as suggested by the research participants,

the introduction of mandatory business

ethics courses, both at the undergraduate and

graduate level, is recommended. According to

Ferrell and Fraedrich (1991: 1), the primary

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 4: Age differences (30 or less vs. more than 30) – independent sample t-test

Statement Age group N Mean SD t Significance

(two-tailed)

Are you willing to use inside information

for your gain?

� 30 300 1.51 0.501 �3.265 0.001

301 229 1.65 0.478

Does peer pressure and competition

make your ethics different?

� 30 297 1.56 0.497 �3.119 0.002

301 232 1.69 0.462

Will you put on the ‘pressure to perform’ and

load it with incentives and fear, forcing your

people to forgo their ethics in the chase for

the profit objective?

� 30 293 1.79 0.409 �2.516 0.012

301 234 1.87 0.335

If you held too much inventory, would you

make returns on the pretence that the goods

are imperfect or not according to samples sent?

� 30 292 1.61 0.489 �3.981 0.000

301 218 1.77 0.421

Would you be willing to cut corners by selling

overripe produce; outdated products; too much

fat in the ground beef; or use the wrong tare

weight in meatpacking?

� 30 297 1.82 0.386 �4.242 0.000

301 224 1.94 0.234

Would you agree with the statement that

ethical problem-solving skills are not relevant

or cannot be applied to the world of business?

� 30 293 1.64 0.481 �1.971 0.049

301 225 1.72 0.450

Would you talk to colleagues about their

promotion application in a public space?

� 30 299 1.64 0.482 �3.315 0.001

301 229 1.77 0.423

Do you believe you can get rich through a

financial manipulation?

� 30 299 1.57 0.496 �3.014 0.003

301 229 1.70 0.461

Do you admire someone’s wealth regardless

how it is earned?

� 30 300 1.64 0.480 �4.025 0.000

301 235 1.80 0.401

Note: Equal variance assumed.

1 5 Yes; 2 5 No.

Significance Level 0.05 (po0.05).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd. 145

objective of such courses is to ‘prepare the next

generation of business leaders to make informed

ethical decisions by providing them the frame-

work to identify, analyze and control ethical

issues in business decision making’. The emphasis

of such a course should be on issues such as

honesty, conflict of interest, dishonest advertising,

unfair pricing, kickbacks, whistle-blowing, code

of ethics, self-governance and discrimination

issues.

Second, the introduction of a Whistle-Blowing

Protection Act, which aims to protect those who

wish to call attention to unethical and wrongful

acts, in order to avoid harm, is considered

imperative. The recent Helios Airlines airplane

crash that claimed the lives of 121 people, was

followed by numerous claims that many knew

information that could have prevented the acci-

dent but failed to disclose it because of fear of

reprisals. This tragic event reiterates the necessity

for comprehensive whistle-blowing legislation in

the country.

Third, local business organizations should

develop and implement a code of conduct and

ethics in order to determine acceptable behaviours

for all their employees within their environment.

An ethics officer should be appointed to oversee

employees’ compliance with the established code

of conduct and ethics. Organizations should be

convinced of the merits of employing ethics

officers, thus allocating all necessary resources

and granting them direct access to the highest

level of leadership.

While in many nations these three suggestions

are implemented, in Cyprus they are quite foreign

or in their infancy. To be more precise, Business

Ethics courses are not mandatory for either

undergraduate or graduate courses, and neither

is the government thinking of implementing a

Whistle-Blowing Protection Act despite the fact

that Cypriot laws are very similar to the United

Kingdom and such law has been implemented in

the United Kingdom. Finally, almost all interna-

tional companies operating in Cyprus do have a

code of conduct or similar and an ethics officer,

but only a handful of local companies have

commenced writing a code of conduct. Despite

the above, it is worth noting that at least

something is being done, which is a positive step

in the right direction.

The three hypotheses tested have been borne

out by the results. The survey found that the

majority of respondents have a concept of ‘ethical

behaviour’, consider ethics important, and hold

attitudes that are conducive for ethical behaviour

in business. At a general level, a number of

inconsistencies emerged between respondents’

espousing a number of ethical views while, at

the same time, approving of certain unethical

practices in the pursuit of profits. The importance

of demographic characteristics of the respondents

was examined in an attempt to account for

differences found in how ethical dilemmas were

resolved. It was revealed that females, those over

the age of 30 and managers were more ethical

than males, those under the age of 30, and non-

managers. The findings obtained reinforce the

importance of gender, age and work experience in

accounting for the degree of ethical sensitivity of

managers. In view of the fact, however, that the

survey reported has its methodological limitations

(e.g., it is a study of perceptions and not

behaviour) and the fact it has been an exploratory

one and the first of its kind in Cyprus, the findings

reported should be regarded as tentative. Conse-

quently, the need for more research in this area

that will also utilize qualitative research methods

cannot be overemphasized.

Acknowledgements

The authors wish to acknowledge the financial

support for the research provided by Pricewater-

houseCoopers.

Note

1. Type I error occurs when a true null hypothesis is

rejected.

References

Akers, R.L. 1985. Deviant Behavior: A Social Learning

Approach, 3rd edition. Belmont, CA: Wadsworth.

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

146r 2008 The Authors

Journal compilation r 2008 Blackwell Publishing Ltd.

Axinn, C.N., Blair, M.E., Heorhiadi, A. and Thach,

S.V. 2004. ‘Comparing ethical ideologies across

cultures’. Journal of Business Ethics, 54:2, 103–

120.

Bandura, A. 1972. Social Learning Theory. Englewood

Cliffs, NJ: Prentice-Hall.

Bartol, C.R. 2002. Criminal Behavior, 6th edition. New

York: Prentice-Hall.

Brophy, B. 1987. ‘Ethics 101: can the good guys win?’.

U.S. News & World Report, 102: 13 April, 54.

Buckley, M.R., Wiese, D.S. and Harvey, M.G. 1998.

‘Identifying factors which may influence unethical

behavior’. Teaching Business Ethics, 2:1, 71–84.

Christies, P.M.J., Kwon, I.G., Stoeberl, P.A. and

Bauhart, R. 2003. ‘A cross-cultural comparison of

ethical attitudes of business managers: India, Korea

and the United States’. Journal of Business Ethics,

46:3, 263–288.

Church, B., Gaa, J.C., Khalid Nainar, S.M. and

Shehata, M.M. 2005. ‘Experimental evidence relat-

ing to the person-situation interactionist model of

ethical decision making’. Business Ethics Quarterly,

15:3, 363–384.

Coate, C.J. and Frey, K.J. 2000. ‘Some evidence on the

ethical disposition of accounting students: context

and gender implications’. Teaching Business Ethics,

4:4, 379–404.

Collins, D. 2000. ‘The quest to improve the human

condition: the first 1500 articles published in Journal

of Business Ethics’. Journal of Business Ethics, 26:1,

1–73.

Cyprus Census. 2001. Retrieved 13 September 2006

from www.mof.gov.cy

Davis, J.R. and Welton, R.E. 1991. ‘Professional

ethics: business students’ perceptions’. Journal of

Business Ethics, 10:6, 451–463.

Dawson, L.M. 1997. ‘Ethical differences between men

and women in the sales profession’. Journal of

Business Ethics, 16:11, 1143–1152.

Derry, R. 1989. ‘An empirical study of moral reason-

ing among managers’. Journal of Business Ethics,

8:11, 855–862.

Dobbins, G.H. and Platz, S.J. 1986. ‘Sex differences in

leadership: how real are they?’. Academy of Manage-

ment Review, 11:1, 118–127.

Ferrell, O.C. and Fraedrich, J. 1991. Business Ethics:

Ethical Decision Making and Cases. Boston, MA:

Houghton Mifflin.

Harris, J.R. and Sutton, C.D. 1995. ‘Unravelling the

ethical decision-making process: clues from an

empirical study comparing Fortune 1000 executives

and MBA students’. Journal of Business Ethics,

14:10, 805–817.

Hirschi, T. 1969. Causes of Delinquency. Berkeley, CA:

University of California Press.

Hofstede, G. www.geert-hofstede.com/hofstede_greece.

shtml Accessed 28 January 2007.

Kapardis, A. 2006. ‘Report on the free movement of

workers in Cyprus in 2005’. In Report for the

European Commission on the Implementation of EU

Free Movement Law in 25 Member States (Volume

1). Nijmegen: Centre for Immigration Law.

Larkin, J.M. 2000. ‘The ability of internal auditors to

identify ethical dilemmas’. Journal of Business

Ethics, 23:4, 401–409.

Michaels, J.W. and Miethe, T.D. 1989. ‘Applying

theories of deviance to academic cheating’. Social

Science Quarterly, 70:4, 870–885.

Peterson, D., Rhoads, A. and Vaught, B.C. 2001.

‘Ethical beliefs of business professionals: a study of

gender, age and external factors’. Journal of Business

Ethics, 31:3, 225–232.

Peterson, R., Beltraminin, R. and Kozmetsky, G.

1991. ‘Concerns of college students regarding busi-

ness ethics: a replication’. Journal of Business Ethics,

10:10, 733–738.

Piliavin, I., Thornton, G., Gartner, R. and Matsueda,

R.L. 1986. ‘Crime, deterrence and rational choice’.

American Sociology Review, 51, 101–119.

Radtke, R.R. 2000. ‘The effects of gender and setting

on accountants’ ethically sensitive decisions’. Jour-

nal of Business Ethics, 24:4, 299–312.

Rothman, K.J. 1990. ‘No adjustments are needed

for multiple comparisons’. Epidemiology, 1:1, 43–46.

Ruegger, D. and King, E.W. 1992. ‘A study of the

effect of age and gender upon student busi ness

ethics’. Journal of Business Ethics, 11:3, 179–186.

Schminke, M. and Ambrose, M.L. 1997. ‘Asymmetric

perception of ethical frameworks of men and women

in business and non-business settings’. Journal of

Business Ethics, 16:7, 719–729.

Simga-Mugan, C., Daly, B.A., Onkal, D. and Kavut,

L. 2005. ‘The influence of nationality and gender on

ethical sensitivity: an application of the issue-

contingent model’. Journal of Business Ethics, 57:2,

139–160.

Singhapakdi, A. and Vitell, S.J. 1990. ‘Marketing

ethics: factors influencing perceptions of ethical

problems and alternatives’. Journal of Macromar-

keting, 10:1, 4–18.

Smith, P.L. and Oakley, E.F. III. 1997. ‘Genders

related differences in ethical and social values of

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

r 2008 The AuthorsJournal compilation r 2008 Blackwell Publishing Ltd. 147

business students: implications for management’.

Journal of Business Ethics, 16:1, 37–45.

Sutherland, E.H. and Cressey, D.R. 1970. Criminol-

ogy, 8th edition. Philadelphia, PA: Lippincott.

Transparency International. 2005. Corruption Index

Percentage. Retrieved 13 September 2006 from

www.ICGG.org.

Trevino, L.K. 1986. ‘Ethical decision making in

organization: a person-situation interactionist mod-

el’. Academy of Management Review, 11:3, 601–617.

Trevino, L.K. 1992. ‘Moral reasoning and business

ethics: implications for research, education, and

management’. Journal of Business Ethics, 11:5–6,

445–459.

Tsalikis, J. and LaTour, M.S. 1995. ‘Bribery and

extortion in international business: ethical percep-

tion of Greeks compared to Americans’. Journal of

Business Ethics, 14:4, 249–265.

Tukey, J.W. 1991. ‘The philosophy of multiple

comparisons’. Statistical Science, 6:1, 100–116.

Wall Street Journal. 2007. ‘Index of Economic

Freedom 2007’. Wall Street Journal, 16 January, 13.

Weber, J. 1990. ‘Managers’ moral reasoning: assessing

their responses to three moral dilemmas’. Human

Relations, 43:7, 687–702.

Weeks, W.A., Moore, C.W., McKinney, J.A. and

Longenecker, J.G. 1999. ‘The effect of gender and

career stage on ethical judgment’. Journal of

Business Ethics, 20:4, 301–313.

Wiese, D.S. and Buckley, M.R. 1997. ‘Are people

really as unethical as we think: a reinterpretation

and some research propositions’. Unpublished

manuscript (cited in Buckley et al. 1998).

Wiley, C. 1998. ‘Re-examining perceived ethics issues

and ethics roles among employment managers’.

Journal of Business Ethics, 17:2, 147–161.

Business Ethics: A European ReviewVolume 17 Number 2 April 2008

148r 2008 The Authors

Journal compilation r 2008 Blackwell Publishing Ltd.