treasury value creation: integrating

TRANSCRIPT

Papers

Treasury value creation: Integratingstrategic planning, capital budgeting,enterprise risk management,and liquidityReceived (in revised form): 23rd November, 2010

Roderic Hewlettis the Dean of the College of Business at Bellevue University. He has served in increasingly responsible corporate

financial positions for two decades. In addition to his current position, his academic appointments have included

distinguished professor of international finance and economics, chair of a business department, dean of a

graduate and business school, and executive vice president and chief academic officer of a college. Roderic holds

a bachelor’s degree in business from Cameron University, and a master’s and doctorate in financial economics

from Middle Tennessee State University. He also holds professional designations as a Certified Financial Manager

and Certified Treasury Professional.

Roderic Hewlett, College of Business, Bellevue University, 1000 Galvin Road South, Bellevue, Nebraska 68005-

3098, USA

Tel: +1 (402) 557 7125; E-mail: [email protected]

Abstract Treasury professionals have mastered new skills over the past two

decades by adding leadership roles in capital budgeting, enterprise risk

management, and mid- and long-range liquidity management to their near-term

cash-management tasks. The onset of the severe global recession highlights the

need for treasury to expand and integrate their roles again by integrating their

activities into the full suite of strategic planning goals of the organisation, mastering

a full range of capital development assessment and management capabilities, and

becoming effective organisational planning partners. Treasury works at the

crossroads of money markets, capital markets, risk management, and capital

assessment; these are core organisational strategic tasks and strategic

orchestration is critical in aligning the organisation to the market.

KEYWORDS: capital structure, capital budgeting, enterprise risk management,

liquidity, value creation, cash flow, strategic management, capital development,

risk factors

INTRODUCTIONGlobally, treasurers are addressingmarket and organisational needs that arecertainly as challenging as they havebeen in the past 85 years. Specifically,treasury professionals are challenged to

forecast cash, while increasinglymanaging strategic aspects of thebusiness, such as enterprise riskmanagement, liquidity management,and capital budgeting. Enterprise riskmanagement and capital budgeting,

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)106

while not new financial responsibilitieshave new dimensions and take onheightened significance with theuncertainties accompanying the ongoingglobal recession. Consequently, thesevere recession illustrates the criticalbusiness planning need to analyse capitalbudgeting, capital development, riskmanagement and strategy in anintegrated and holistic fashion. Thisessential need demands a new way ofviewing treasury analysis-planning andnew ways of approaching capital-budgeting development.

Challenges and risksComplicating treasury’s planning plightare the comments in news reports byunion leaders and government officialsthat note that, even during the currentsevere recession, businesses seem to beflush with cash and should be doingmore to offset the global consumptionfall-off through investments, taxes, andhiring. Yet, the amount of cash,seemingly unencumbered, on thebalance sheets of leading businesses inEurope, UK, Asia, and North Americacan be deceiving to those not fullyaware of the real risks and challengesfaced by global businesses. Politicalleaders attempting to lighten theirchallenges, and misunderstanding thenature of risk that business faces, arechanging the regulatory (institutional)environment to burden businesses withnew hiring goals, healthcare mandates,and product sourcing dictates. Politicalmanoeuvring is pressuring leadingcentral banks to position competitivelycurrency exchange rates to increaseexports. Economic protectionism is onthe rise. Risks abound and balancesheets do not tell the whole story.Alternately, using strategies shaped by

experiences drawn from past recessionsdecades ago that lead to seemlyattractive merger and acquisition(M&A) activities, stock repurchaseschemes, or merely protecting futureoptions through cash hoarding, can beequally short-sighted. Internal capitaldevelopment may actually yield highersustainable long-term total returns.Treasury professionals find themselves— more than ever — in the midst of thetempest in the teapot where they mustfully understand global economics andrisk, master short- and medium-termliquidity management, and balance all ofthis against long-term strategicobjectives. These important leadershipresponsibilities are indeed a tall, andunaccustomed, order for treasury. Yet,treasury is exactly the right organisationto establish straightforward methods tobalance strategic financial management,effective capital development, riskmanagement, and liquidity planning.

New concepts and outdatedassessment traditionsWhen treasury professionals practicecapital budgeting, they typically onlyconsider two forms of capital: financialand physical capital. Ignoring otherimportant forms of capital, such ashuman, intellectual, and structural formsthat will propel the organisationthrough this protracted recession andposition the organisation for sustainedgrowth, is ‘penny wise and poundfoolish’. In the 19th and 20th centuries,neoclassical economics became thedominant theoretical window todevelop and view organisationalefficiency and effectiveness metrics.Neoclassical concepts still form themicroeconomic foundations for globalfinancial assessment and management

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 107

tools. During periods of predictabilityand relative calm, the neoclassicalfinancial methods are acceptable;however, moving beyond neoclassical-based formulae, especially during timesof financial distress, to capture neweconomic realities makes a great deal ofbusiness sense.Neoclassical economics grew out of

the 1870 ‘Marginalist Revolution’. Thistremendous advance in economic theoryset the groundwork for the amazingdevelopments in explaining value,market behaviour, financial ideas, andvaluation methods, culminating in themid-20th century with Sharpe’s CapitalAsset Pricing Model1 and Markowitz’sPortfolio Theory.2 These modelsunderpin current thinking about riskand return as well as capital budgetingpractices — including portfolio theoryfor risk management. Neoclassical ideasare based on critical assumptions of fullyinformed and rational behaviour withanalysis grounded in points ofobservable market equilibriums. Duringperiod of relative market clarity, andwhere effective and efficient money andcapital markets exist, there is less cloudingof understanding of underlying globaleconomic behaviour. Additionally,markets appear to be less dynamic andseem to achieve equilibrium. Evenduring periods of relative calm, marketirregularities, uncertainties, and frictionprevent theory from perfectly matchingpractice.Unfortunately, markets, behaviours,

and ‘rationality’ are contextual and asrisk and uncertainty grow so dodynamic risk aversion behaviours thatlead to apparent observed irrationalactions as markets become lesspredictable. This lack of predictabilityaffects global consumer markets,

financial markets, and the fiscal andmonetary habits of major governments.In short, financial models become lessclear and less predictive. Add to this lackof predictability change in underlyingmarket value creation mechanisms and itis clear that expanded financial modelsand tools are necessary for the 21stcentury. Cutting edge research frommultiple disciplines reveals that rationalbehaviour is linked to learned patternsand behaviour.3 These learned economicpatterns become predictable and risk isviewed as deviation from the predictable— in fact Bayesian statistical methodscan help to analyse and predict thislearned behaviour–risk relationship.4

Rationality is reasoning tied to rulesof logic and the logic of stable marketsis steeped in learned patterns. Wholeschools of economic thought are tied toobservable patterns during stable as wellas unstable periods. Observed irrationalbehaviour can be thought of asdiscovery when the rules of logic arechanged — or economic patternsdeviate structurally from historicalpatterns. During this period ofdiscovery, to understand the ‘newnormal’, the rules of risk and riskaversion appear prospectively irrationaland only seem rational in hindsight.5

History is replete with examples ofbubbles and structural economic shiftsthat highlight these irrational riskbehavioural patterns such as the SouthSea Scheme, Railway Mania of 1845,and the various market crashes such asthe Great Depression of 1929.6

Nassim Taleb’s tremendous book thathighlights black swans7 — or outliers —poses further complexity in risk anduncertainty. Outliers lie outside of realmof regular expectations — or learnedpatterns. Black swan logic forces thinking

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)108

beyond empirics and specifics, it forcesholistic and generalised reasoning. Whatseems probable to happen and does notor what does not seem probable anddoes happen are black swancomplications that render using overlysingular methods to analyse and forecastas severe limitations. Taleb demonstratesthat the rare and unexpected doeshappen and can have monumentaleffects, and only holistic planningheuristics hold the promise of capturingthese outlier events.Another limitation of current

economic, financial, models in the 21stcentury is the overreliance of the modelson financial and physical capital as thecash generating engines of a business.Neoclassical production functions lookat physical capital as productive sourceof value and ‘labour’ as a substitute forphysical capital. This view that humanefforts are mere substitutes for, orcomplements to, physical capital made agreat deal of sense during the early- tomid-Industrial Revolution periodsculminating in the 1960s and 1970s.Nevertheless, the 21st century is aknowledge-based form of capitalismthat is driven by human, intellectual,and structural forms of capital inaddition to physical and financial capital.It is time to expand beyond thecenturies-old land (rent), labour (wage),capital (interest), and entrepreneurship(profit) model of economic inputs andreturns and model more relevant inputsand returns. Unfortunately, currentcapital budgeting models typically pairfinancial and physical capital together.Throw in a serious global recession andold models cannot provide the necessaryintegrated planning informationrequired for liquidity, risk management,and capital effectiveness planning.

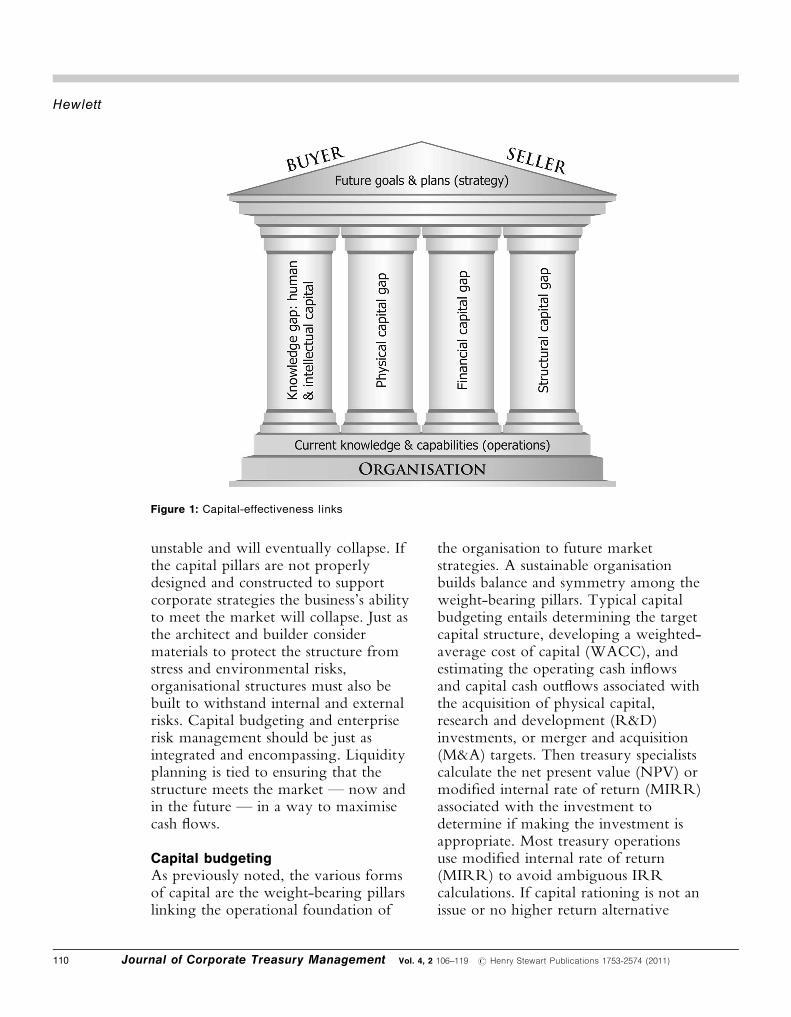

INTEGRATED TREASURYPLANNING MODELA new treasury planning heuristic tocope with 21st century realities as wellas plan for recessions and post-recessiongrowth is a necessity. The modelledheuristic below integrates strategic goals,capital development, enterprise riskmanagement, market behaviours, andliquidity planning for treasury use. Thisnew integrated treasury planning modelsignificantly extends strategic-knowledge models put forward byleading strategic thought leaders such asMichael Zack8 and fully synthesisescapital development models that linkstructural capital,9 human capital andintellectual capital with the traditionalphysical and financial forms of capital.10

The above model should not beviewed as a model for empirical testing,but considered as a heuristic that guidesholistic planning for capitaldevelopment, capital budgeting,strategic planning, enterprise riskmanagement, and merger-acquisitionplanning.The well-informed treasurer will note

that the foregoing model in Figure 1 isliterally the value chain of a businesstoday and in the future. Yes, that isexactly the point — treasury managescash flow, and cash flow is the heart ofthe value proposition of a business. Themodel is capital driven and frames fullanalysis from a risk, capital, and marketperspective. Note that capital is denotedas pillars linking the current operationalfoundation to the aspirations, orstrategic goals, of the organisation tomeet the market. The capitaldevelopment model is analogous toarchitectural designs and buildingconstruction; if there is a gap in thepillars, then the frieze and roof are

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 109

unstable and will eventually collapse. Ifthe capital pillars are not properlydesigned and constructed to supportcorporate strategies the business’s abilityto meet the market will collapse. Just asthe architect and builder considermaterials to protect the structure fromstress and environmental risks,organisational structures must also bebuilt to withstand internal and externalrisks. Capital budgeting and enterpriserisk management should be just asintegrated and encompassing. Liquidityplanning is tied to ensuring that thestructure meets the market — now andin the future — in a way to maximisecash flows.

Capital budgetingAs previously noted, the various formsof capital are the weight-bearing pillarslinking the operational foundation of

the organisation to future marketstrategies. A sustainable organisationbuilds balance and symmetry among theweight-bearing pillars. Typical capitalbudgeting entails determining the targetcapital structure, developing a weighted-average cost of capital (WACC), andestimating the operating cash inflowsand capital cash outflows associated withthe acquisition of physical capital,research and development (R&D)investments, or merger and acquisition(M&A) targets. Then treasury specialistscalculate the net present value (NPV) ormodified internal rate of return (MIRR)associated with the investment todetermine if making the investment isappropriate. Most treasury operationsuse modified internal rate of return(MIRR) to avoid ambiguous IRRcalculations. If capital rationing is not anissue or no higher return alternative

Figure 1: Capital-effectiveness links

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)110

exists, an organisation will make thecapital investment. The new modelhighlights the flaw — capitalinvestments must also consider human,intellectual, structural capital and risk —other than financial risks — as part ofthe capital budgeting process. Thisinclusive capital budgeting processshould be implemented for M&A andR&D projects as well as stand-aloneinvestments in human, intellectual, andstructural capital.It is essential that treasury’s role is

more than just cash management if risk,market sustainability, and liquiditymanagement are the long-term goals ofthe organisation. Treasury professionalsmust be effective communicators,collaborators, mentors, and full partnersin managing the business. Capitalbudgeting is a shared process of analysiswhere line and staff departmentsparticipate in collecting data andtreasury pulls the analysis together andassists in interpreting and assessingresults. The shift from merely assessingfinancial and physical capital to assessingboth tangible and intangible forms ofcapital (human, intellectual, andstructural) that are critical value-creating (cash-enriching) forms ofcapital will be most important in thechallenging 21st century and also themost difficult to articulate. Globally,trillions of pounds, euros, dollars, yuanor yen are invested for training,education, talent acquisition, andleadership training. Capital budgetingprovides the discipline to ensure theinvestment is fully articulated, assessed,and executed properly. Fuzzy logicproduces fuzzy results and anticipatedreturns on capital should never befuzzy. What treasury, in conjunctionwith other functional areas, is

determining is straightforward: are thesehuman capital expenditures aninvestment or mere consumption?Investments yield measurable returns.

Measuring and valuingintangible assetsIn the USA, FASB 142 Goodwill andOther Intangible Assets highlights theincreasing importance of, and theaccounting for, intangible assets andshares and how to account for them, butthe standard lacks guidance on how toassess the value-creating characteristics ofintangible assets. Internationally, IAS 38Intangible Assets also frames theaccounting of these intangible assets butfalls short on assessing the value of theassets to the cash flow to the business.Both standards recognise the growingimportance of intangible assets whichinclude software, patents, customer lists,servicing rights, licences and importquotas, franchises, customer and supplierrelationships, and marketing rights justto name a few. There are many moreintangible assets, or capital, that residewithin an organisation undefined — orallocated — to the financial statements,such as the value of training, experience,and education to enhancing cash flow,processes, procedures, routines, culture,effective communication, leadership, andreputation (beyond goodwill). These aresignificant forms of organisationalcapital and while it may take effort tosort out the valuation and cash-flowparticulars, they have cash value to abusiness.Human capital is the ability,

knowledge, and talent of employees toproduce, innovate, create, and workwell with others. Some forms ofeducation, training, and developmentcan have huge impacts on the cash and

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 111

capabilities of an organisation. WatsonWyatt developed a Human CapitalIndex (HCI) and studied over 750publicly traded companies in the USA,Canada and Europe.11 The findings areconclusive: companies that have stronghuman capital and developmentcapabilities aligning generate higher cashflow and shareholder value. The WatsonWyatt study categorises returns alongtwo key capital dimensions: human andstructural capital. Structural capital is theroutines, processes, procedures, culture,communication, relationships,reputation, and leadership that enhancecapital alignment and market success.9

Why is structural capital important? Ifhuman capital owners — the employees— are unwilling or unable to investtheir formidable human capital in anorganisation effectively, then it isdiminished. Human capital is both aninvestment in human value creationcapability and an investment of one’shuman capital in an organisation — adouble-edge investment strategy.12,13 Ifan organisation’s structural capital ismisaligned or toxic, no amount ofinvestment in other forms of capital willhave their desired impact. Structuralcapital is aligned through goodgovernance, strong projectmanagement, effective leadership anduseful feedback. Remember ISO processcertification demonstrates real-valueconveyance to customers. Quality

standards and six sigma programs areprerequisites to contracts and solid cashflow in many industries. Structuralcapital has cash flow and business valueand investments in structural capitalshould be measured through disciplinedcapital budgeting.Below in Table 1 are some of the key

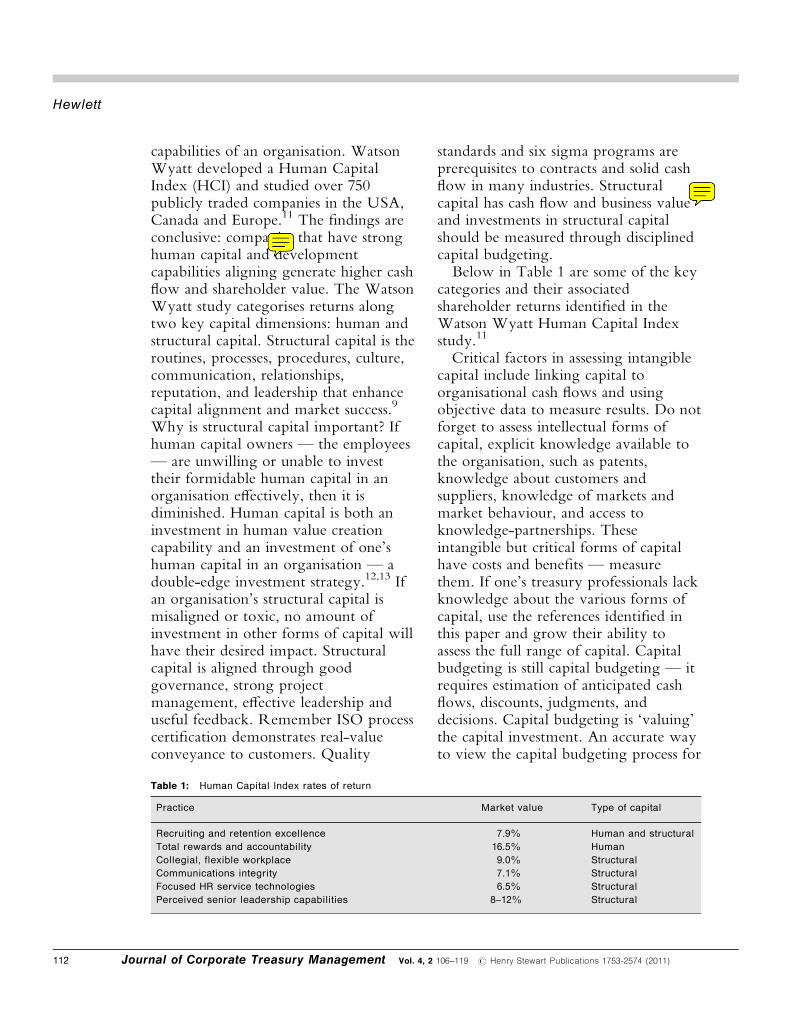

categories and their associatedshareholder returns identified in theWatson Wyatt Human Capital Indexstudy.11

Critical factors in assessing intangiblecapital include linking capital toorganisational cash flows and usingobjective data to measure results. Do notforget to assess intellectual forms ofcapital, explicit knowledge available tothe organisation, such as patents,knowledge about customers andsuppliers, knowledge of markets andmarket behaviour, and access toknowledge-partnerships. Theseintangible but critical forms of capitalhave costs and benefits — measurethem. If one’s treasury professionals lackknowledge about the various forms ofcapital, use the references identified inthis paper and grow their ability toassess the full range of capital. Capitalbudgeting is still capital budgeting — itrequires estimation of anticipated cashflows, discounts, judgments, anddecisions. Capital budgeting is ‘valuing’the capital investment. An accurate wayto view the capital budgeting process for

Table 1: Human Capital Index rates of return

Practice Market value Type of capital

Recruiting and retention excellence 7.9% Human and structural

Total rewards and accountability 16.5% Human

Collegial, flexible workplace 9.0% Structural

Communications integrity 7.1% Structural

Focused HR service technologies 6.5% Structural

Perceived senior leadership capabilities 8–12% Structural

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)112

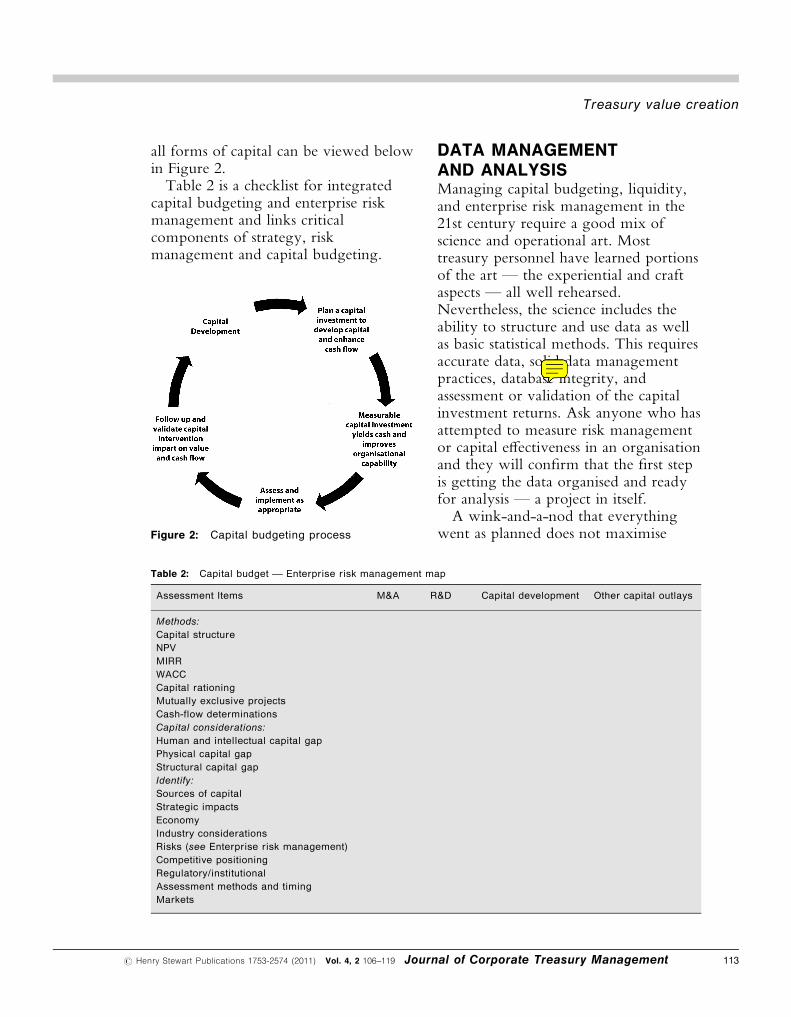

all forms of capital can be viewed belowin Figure 2.Table 2 is a checklist for integrated

capital budgeting and enterprise riskmanagement and links criticalcomponents of strategy, riskmanagement and capital budgeting.

DATA MANAGEMENTAND ANALYSISManaging capital budgeting, liquidity,and enterprise risk management in the21st century require a good mix ofscience and operational art. Mosttreasury personnel have learned portionsof the art — the experiential and craftaspects — all well rehearsed.Nevertheless, the science includes theability to structure and use data as wellas basic statistical methods. This requiresaccurate data, solid data managementpractices, database integrity, andassessment or validation of the capitalinvestment returns. Ask anyone who hasattempted to measure risk managementor capital effectiveness in an organisationand they will confirm that the first stepis getting the data organised and readyfor analysis — a project in itself.A wink-and-a-nod that everything

went as planned does not maximiseFigure 2: Capital budgeting process

Table 2: Capital budget — Enterprise risk management map

Assessment Items M&A R&D Capital development Other capital outlays

Methods:

Capital structure

NPV

MIRR

WACC

Capital rationing

Mutually exclusive projects

Cash-flow determinations

Capital considerations:

Human and intellectual capital gap

Physical capital gap

Structural capital gap

Identify:

Sources of capital

Strategic impacts

Economy

Industry considerations

Risks (see Enterprise risk management)

Competitive positioning

Regulatory/institutional

Assessment methods and timing

Markets

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 113

liquidity, credit ratings, or ensure valuecreation. If an organisation is going totap cash, or financial capital, to enhanceits future, then the results have to bemeasured and lessons learned, gleanedand applied. Treasury professionals mustbecome skilled in multivariate statisticalanalysis, sensitivity analysis, scenario/event modelling, and Monte-Carlosimulation. Returns associated withintangibles — and increasingly tangible— forms of capital are assessed usinggood data and good methods. Therevealed correlations between capitalinvestments and increased cash flows arethe critical indicators of success.Remember, economists and financeprofessionals evaluate what actuallyhappens to critical choice variables whensubjected to the market. Softwareprograms such as EXCEL or EXCELcoupled to SPSS readily handle the datamanagement and number crunchingnecessary to assess returns — no need fornew sophisticated data analysis software.Equally, there is no need for access toproprietary data or extensive databases.The essential ingredient is good data anddatabase management for theorganisation.

ENTERPRISERISK MANAGEMENTMuch like the capital development andbudgeting processes that link currentoperations ultimately to the market,enterprise risk management (ERM) is atreasury systems management device toassess risks to current and future cashflows. After risk identification, treasuryprofessionals need to assess the potentialimpact of the risk — magnitude andpotential. Then, armed with an educatedevaluation, develop a strategy to protectcash flows. Since planned operations

should be manageable within the plan,ERM focuses on the unanticipated orunplanned scenario. So, anythingunexpected that impacts markets such aseconomic events, competitive changes,unforeseen changes in capital that affectstrategy and diminishes operationalreadiness is a risk. The potential todisrupt current and future cash flowsdefines that timing and magnitude ofthe risk. In short, anything that has thepotential unexpectedly to impact cashflow is a risk.Hence ERP is an essential treasury

responsibility. Increasingly, frameworkssuch as the Basel Capital Accord, USSarbanes–Oxley Act, European 8thCompany Law regulations have broughtadditional board scrutiny on risk issuesowing to the new institutionalDirective, Japanese Financial Instrumentsand Exchange Law, and the EuropeanUnion’s Financial Services Action Planthat includes Markets in FinancialServices Directives. The recently passedDodd–Frank Law requires all non-bankfinancial companies and large publicbank holding companies to have a RiskCommittee on their board to overseeERM practices. With increasedregulation of financial businesses, evennon-financial businesses will be impactedby the impact of the regulation. ERM isan ever-increasing part of corporategovernance and compliance for large,medium, and small businesses. Mostcompanies have corporate socialresponsibility (CSR) guidelines thatmandate internal and external risk limitsthat impact ERM practices.A business can use a variety of risk

management techniques to protect itselffrom unanticipated events or changes inthe environment. Some of the moretraditional manners include insurance

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)114

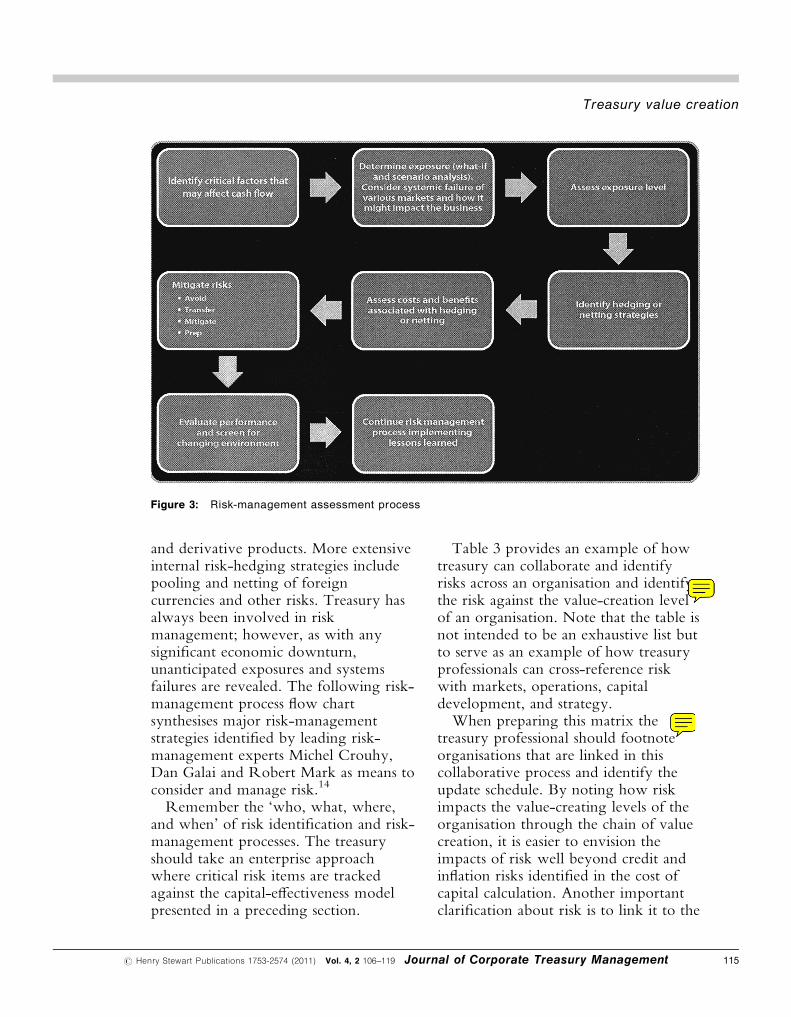

and derivative products. More extensiveinternal risk-hedging strategies includepooling and netting of foreigncurrencies and other risks. Treasury hasalways been involved in riskmanagement; however, as with anysignificant economic downturn,unanticipated exposures and systemsfailures are revealed. The following risk-management process flow chartsynthesises major risk-managementstrategies identified by leading risk-management experts Michel Crouhy,Dan Galai and Robert Mark as means toconsider and manage risk.14

Remember the ‘who, what, where,and when’ of risk identification and risk-management processes. The treasuryshould take an enterprise approachwhere critical risk items are trackedagainst the capital-effectiveness modelpresented in a preceding section.

Table 3 provides an example of howtreasury can collaborate and identifyrisks across an organisation and identifythe risk against the value-creation levelof an organisation. Note that the table isnot intended to be an exhaustive list butto serve as an example of how treasuryprofessionals can cross-reference riskwith markets, operations, capitaldevelopment, and strategy.When preparing this matrix the

treasury professional should footnoteorganisations that are linked in thiscollaborative process and identify theupdate schedule. By noting how riskimpacts the value-creating levels of theorganisation through the chain of valuecreation, it is easier to envision theimpacts of risk well beyond credit andinflation risks identified in the cost ofcapital calculation. Another importantclarification about risk is to link it to the

Figure 3: Risk-management assessment process

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 115

form of capital that is affected by therisk and how is it affected. Do not usefuzzy concepts but concrete examplesand concrete mitigation methods toprotect cash flow and value creation.A few examples highlight the

complex risk-environment–compliance-management link faced by moderntreasury professionals. Current lowinterest rates may look very attractiveright now; however, defined benefitretirement plan funding becomescomplicated due to the undermining ofactuarial assumptions of growth. Thisunderfunding then requires firms tosiphon operating cash flows or tap creditto fully fund the retirement plans.Concomitantly, some may view thisepisode as an opportunity to move todefined contribution plans, but this maynot be attractive to recruit and retain thebest human capital talent necessary toachieve strategic goals. Effectiverecruitment and retention returns to theorganisation rank among highestpotential human capital returnsavailable. The law of unintendedconsequences complicates the scenario— good ERM considers the whole risk

picture including the branchingconsequences. A simple environmentalresponse to recessions — reducedinterest rates fuel a complex risk-capitaldilemma. Treasury personnel do nothave to have the answers for suchcomplex issues. In fact, this complexproblem will most likely be anexecutive leadership solution, buttreasury can identify the nexus of riskand opportunities embedded in ever-changing markets. Treasury can alsoidentify the potential magnitude of theissues and duration as well.Another example highlights that as

global recessions create credit crisis forbanks it places additional burdens on theworking capital of healthy non-financialbusinesses. As banks lend less owing torisk or Basel Accord capitalrequirements, accounts receivables mustincreasingly serve as a backstop forshort-term financing of customers.Critical cash-strapped suppliers may alsoneed quicker payment on accountspayable. Changes in the terms andconditions of sales may well requiregreater creditworthiness of customers.These receivable and payable cash

Table 3: Value creation — risk management matrix

Risk item Operational Capital Strategic Market

Liquidity X X X X

Market X X X

Institutional/regulatory X X X X

Supply chain X X X

Strategic X X X

Operational X X

Competitor actions X X X X

New disruptive technologies X X X

Reputational X X X

Compliance/governance X

Business X X X X

Credit X X

Systemic X X X X

Political X X X X

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)116

impacts can create competing conflictswithin an organisation as investment innon-financial capital becomesconstrained. The clear balancing act andhow it is achieved is an important risk-management task. By understandinghow operations, capital, and strategylink to the market, treasury can betterassess total risk impacts.The bankruptcy of General Motors

and Chrysler highlights how supplychains can be affected by financialdistress that can disrupt healthyautomotive companies. If suppliers gobankrupt, their inability to provideparts, services, and design solutions forother automotive manufacturers — bothforeign and domestic — is curtailed.This demonstrates how intellectual andstructural capital as well as strategy andoperations can be thrown off track. Asmart company will have multiplevariants of production (redundancy) andthe capability to manufacturer criticalcomponents as part of its riskmanagement strategy, but it must alsounderstand the capital trade-offsassociated with this capability.Insightful treasury professionals use

sensitivity analysis, event analysis, andother analysis methods, but they alsomust invest in research to understand thenature and sources of risk as well asdevelop the specific transmissionmechanisms for how risk impacts capital,strategy, and cash flow. Learning fromothers and a lessons’ learned database arehighly valued tools to determine thedegree of risk impacts as well as how it istransmitted. Usually, how to resolve therisk is also a lesson learned.The consequences of not

understanding the linkages of enterpriserisk planning and sustainable strategyhas long-term consequences. For

instance, a recent article, based onGreenwich Associates March 2010survey of 243 financial decision makersat mid-size companies revealed that 47per cent of mid-size firms made staffingreductions, while only 17 per centreduced inventories; however, inventoryreductions saved an annual average ofUS$520,000, while staff reductionsaveraged annual savings ofUS$400,000.15 It may be assumed thatsome of the staff reductions at the mid-size companies may benefit theorganisation, but it is equally true thatreal human capital loss at mid-sizecompanies has significant impacts notalways felt by larger organisations.At times, executives believe hoarding

cash on the balance sheet is a risk-neutralstrategy and the opportunities costs arevery limited, but that is far from the fullpicture of risk. For example, theinability to develop human andstructural capital during a severerecession can impact the sustainability ofthe business post-recession or evenduring the recession. Cash and credit arejust one form of capital that must bemanaged by an organisation. Holdingcash can have risk, capital, and realmarket consequences. Conversely, notunderstanding the need to manageliquidity and investing in low-returntraining or other capital developmentschemes blindly can also have severeimpact on the viability of a business.The point is to consider the fullspectrum of options and consequencesand manage operations–capital–strategy–markets for optimal outcomes.Treasury is in a unique position tointegrate this value analysis. Equallyimportant in risk scans, watch forlearning opportunities from thoseoperations that constantly outperform in

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 117

all economic regimes — statisticaloutliers may just have somethingimportant figured out worthconsidering.12 Risk management is alearning exercise.

THE 21STCENTURY TREASURYWhen it comes to liquiditymanagement, capital budgeting,enterprise risk management, and value-creation, the 21st century treasury officeis the project-management team. Theteam must move beyond technicalwizardry to being a full business partnerin the value creating enterprise.Treasury reporting needs to includebalanced scorecards and dashboards tosimplify abstract ideas of riskmanagement and capital developmentfor decision makers. It is not necessaryfor treasury to be expert on all areas ofthe organisation, but it is critical thattreasury manage for long-term valuecollaboratively.Finance in the 21st century is as much

about communicating, mentoring, andserving as a business partner within theorganisation as it is about technicalcapability. It makes little sense fortreasury and financial professionals tounderstand the impacts of risk and capitaldevelopment on liquidity and strategyand not communicate it with those thatchange organisational direction.Treasury professionals have witnessed

their roles change significantly beyondthe cash conversion cycle in the past twodecades to encompass capital budgeting,enterprise risk management, and otherimportant technology tasks. Yet, thereal challenge for treasury professionalslies ahead and that challenge is made upof fostering the type of applied researchand products for the organisation that

capture holistic risk and liquidityplanning that links the organisation oftoday to the markets of the future. Onlythrough an integrated approach cantreasury fully architect value creation foran organisation.

References1 Sharpe, W. (1964) ‘Capital Asset Prices:

A Theory of Market Equilibrium underConditions of Risk’, Journal of Finance,Vol. 19, No. 3, pp. 425–442.

2 Markowitz, H. (1959) ‘PortfolioSelection’, John Wiley, New York, NY.

3 Hassenzahl, D. (2004) ‘Risk Analysisand Uncertainty: Implications forCounselling’, Guidance and Counselling,Vol. 19, No. 2, pp. 65–71.

4 Oaksford, M. and Chater, N. (2009)‘Precis of Bayesian Rationality: TheProbabilistic Approach to HumanReasoning’, Behavioral and Brain Sciences,Vol. 32, No. 1, pp. 69–84.

5 Grandori, A . (2010) ‘A RationalHeuristic Model of Economic Decision-making’, Rationality and Society, Vol. 22,No. 4, pp. 477–504.

6 Chancellor, E. (1999) ‘Devil Take theHindmost: A History of FinancialSpeculation’, Farrar, Straus, and Giroux,New York, NY.

7 Taleb, N. N. (2007) ‘The Black Swan:The Impact of the Highly Improbable’,Random House, New York, NY.

8 Zack, M. H. (1999) ‘Developing aknowledge strategy’, CaliforniaManagement Review, Vol. 41, No. 3,pp. 125–145.

9 Stewart, T. A. (1997) ‘IntellectualCapital: The New Wealth ofOrganizations’, Doubleday/ Currency,New York, NY.

10 Roos, G., Roos, J., Edvinsson, L. andDragonetti, N. C. (1997) ‘IntellectualCapital: Navigating in the New

Hewlett

Journal of Corporate Treasury Management Vol. 4, 2 106–119 # Henry Stewart Publications 1753-2574 (2011)118

Business Landscape’, New YorkUniversity Press, New York, NY.

11 Pfau, B. N.and Kay, I. T. (2002) ‘TheHuman Capital Edge: 21 PeopleManagement Practices Your CompanyMust Implement (or Avoid) toMaximize Shareholder Value’, McGrawHill, New York, NY.

12 Davenport, T .O. (1999) ‘HumanCapital: What It Is and Why PeopleInvest It’, Jossey-Bass, San Francisco,CA.

13 Hewlett, R. (2005) ‘The Cognitive

Leader: Building WinningOrganizations through KnowledgeLeadership’, Rowman & LittlefieldEducation, Lanham, MD.

14 Crouhy, M., Galai, D. and Mark, R.(2006) ‘The Essentials of RiskManagement’, McGraw Hill, NewYork, NY.

15 Katz, D. M. (2010) ‘Lesson from theDownturn: Cut Inventory, Not People’,28th May, available at: http://www.cfo.com/printable/article.cfm/14501579 (accessed 8th October, 2010).

Treasury value creation

# Henry Stewart Publications 1753-2574 (2011) Vol. 4, 2 106–119 Journal of Corporate Treasury Management 119