top stories - zacks

TRANSCRIPT

1

Global Equity Research

13 June 2014

Top Stories ▼Ipsen (IPN.PA, N – €34.75) (Richard Vosser), Europe Downgrading to Neutral: TASQ (tasquinimod) Overall Survival benefit a bridge too far Since the start of 2013 Ipsen shares have risen 47%, as the value of the base business and significant growth potential from Somatuline have been better appreciated by investors.

UK Banks (Raul Sinha), Europe Prefer domestic UK and pure play EM banks over HSBC & STAN We have been Neutral on StanChart and HSBC in the context of European banks since May and Sept 2013, respectively, driven by the recovery in Europe as well as the prospect of negative EPS revisions in a weak EM revenue environment.

European Technology (Sandeep Deshpande), Europe What to expect at the J.P. Morgan Technology CEO Conference next week - ALERT We have 36 hardware and software companies attending the conference: Several companies (such as SAP, STMicro, ARM, Dassault, Hexagon, and Capgemini) have recently hosted Capital Markets Days, and we look forward to hearing more details on their updated strategies and financial plans.

Tokyo Signals, Noise & Strategy - Vol 20 (Patrick Rial, CFA), Japan Are You Paying Attention? “Like three days passing / cherry blossoms gone, unseen / how I see this world” – Ryota Oshima, 18th century haiku poet.

Asian shipbuilding industries (Sokje Lee), Asia Pacific New shipping economics in eco-ship epoch The ways of ship investment are changing.

Indonesia Automobiles (Aditya Srinath, CFA), Asia Pacific Engine Check: Datsun Go+ completes the LCGC Competitive Landscape Low-cost green cars (LCGCs) now account for 13% of 1ndonesian 4W sales, taking share initially from MPVs.

Food Retail in Emerging Markets (Andrea Teixeira, CFA), Latin America Favor Retailers that Expand Profitably. Picks are: Walmex, CBD, Magnit, Lenta, Savola & BIM In the second annual edition of this proprietary analysis, in collaboration with six of our Global consumer equity research teams, including LatAm, Middle East, Poland, Russia, South Africa, and Turkey teams.

▲Advantest (6857) (N – ¥1,224) (Hisashi Moriyama), Japan Order Trend Strong, Underweight Rating No Longer Justified; Upgrading to Neutral We stated in our June 11 report on SPE sector telephone interviews that orders at Advantest are tracking well ahead of plan.

Q-Strategy Help in EM (Sanaya Tavaria), CEEMEA Stock screens that combine thematic macro and quant EM equities are up 10% in the past three months, outperforming DM by 6%.

Send me your feedback!

GLOBAL Stock Guide

J.P. Morgan Markets

Daily Economic Briefing

Regional First to Market

Inside this Report:

Research by Region

Key Rating, Price Target & EPS Changes

Market at a Glance

Market Monitor

Economics Calendar

J.P. Morgan Forecasts - Economics and Commodities

Analyst Focus List

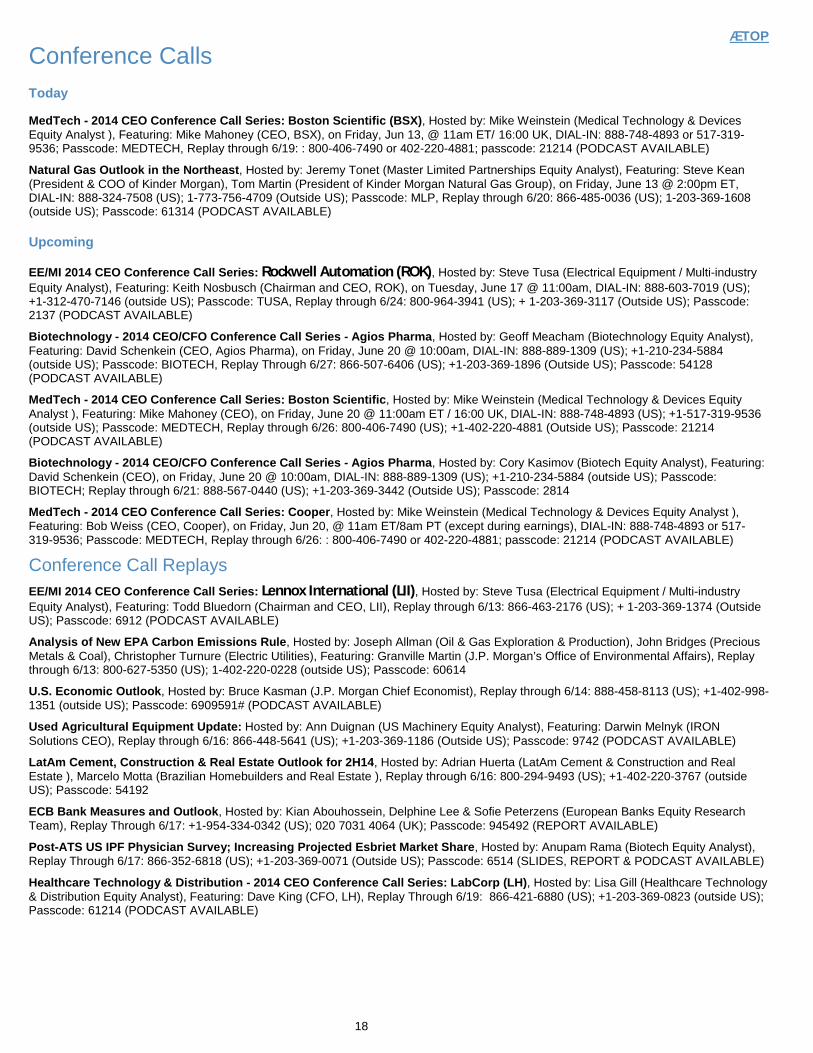

Today’s Events Conference Call: MedTech - 2014 CEO Conference Call Series: Boston Scientific (BSX) at 11am ET/ 16:00 UK, DIAL-IN: 888-748-4893 or 517-319-9536; Passcode: MEDTECH

Conference Call: Natural Gas Outlook in the Northeast at 2:00pm ET, DIAL-IN: 888-324-7508 (US); 1-773-756-4709 (Outside US); Passcode: MLP

Corporate Marketing ANSYS, INC. (LOS ANGELES, PASADENA) DCC (TORONTO) Iroko Pharmaceuticals (Private) (NEW YORK) WILLIAMS-SONOMA, INC. (PRINCETON)

See end pages for analyst certification. For important disclosures, please refer to the disclosure section at the end of the individual linked notes. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

2

Global Published Research áTOP

Europe

Recommendation Changes

▲Dufry (DUFN VX – Neutral) (Jaafar Mestari) Steady-state was the enemy: upgrading to Neutral following The Nuance Group acquisition

▼Ipsen (IPN FP – Neutral) (Richard Vosser) Downgrading to Neutral: TASQ (tasquinimod) Overall Survival benefit a bridge too far

Price Target and Estimate Changes Active Biotech (ACTI SS – Underweight) (James D Gordon) Reiterating our UW recommendation ahead of TASQ Phase III read-out, which looks likely to disappoint

Atkins (WS) (ATK LN – Overweight) (Jolyon S Wellington) FY14 results in line with expectations, showing organic growth and strategic improvement

Dufry (DUFN VX – Neutral) (Jaafar Mestari) Steady-state was the enemy: upgrading to Neutral following The Nuance Group acquisition

HSBC Holdings plc (HSBA LN – Neutral) (Raul Sinha) UK Banks: Prefer domestic UK and pure play EM banks over HSBC & STAN

Ipsen (IPN FP – Neutral) (Richard Vosser) Downgrading to Neutral: TASQ (tasquinimod) Overall Survival benefit a bridge too far

PZ Cussons (PZC LN – Neutral) (Celine Pannuti, CFA) FY14 growth despite tough markets but hard to repeat in FY15. PT cut to 350p

Price Target and Estimate Changes, continued Standard Chartered (STAN LN – Neutral) (Raul Sinha) UK Banks: Prefer domestic UK and pure play EM banks over HSBC & STAN

Storebrand (STB NO – Overweight) (Daniel Do-Thoi) Updating numbers and highlighting paid-up policy conversions as potential upcoming catalyst

Results and Company Views 3i (III LN – Overweight) (Christopher Brown) Action site visit underlines its potential - we believe a doubling of the current value is not unreasonable

Asia Resource Minerals PLC (ARMS LN – Neutral) (Ben Defay) Change of CEO; position relocated to Indonesia - ALERT

Fenner (FENR LN – Neutral) (Andrew J Wilson) AEP Capital Markets Day Feedback - Growth and margin targets the headline takeaways - ALERT

Halma (HLMA LN – Neutral) (Andrew J Wilson) FY14 Results - First Take - ALERT

Sector Research European Technology (Sandeep Deshpande) What to expect at the J.P. Morgan Technology CEO Conference next week - ALERT

UK Non Life (Andreas van Embden) Update on UK Motor insurance regulation from CMA - ALERT

3

Asia

Price Target and Estimate Changes

KPJ Healthcare Berhad (KPJH.KL – Neutral), Malaysia (Simone Yeoh) Earnings downgrades stabilizing but consistency in performance is key from here; prefer IHH (OW)

PT Tower Bersama Infrastructure Tbk (TBIG.JK – Overweight), Indonesia (Princy Singh) Management meeting: Maintaining growth guidance, M&A focus continues

Reliance Power (RPOL.BO – Underweight), India (Sumit Kishore) What's in the price?

Results and Company Views

Bank of China - H (3988.HK – Overweight), China (Katherine Lei) China Summit 2014: Feedback from the Conference

Belle International Holdings Ltd. (1880.HK – Neutral), China (Ebru Sener Kurumlu) Footwear drag continues

Cathay Pacific (0293.HK – Overweight), Hong Kong (Corrine Png) Pax loads improved in May, cargo demand strengthened on US routes; stay OW

China Hongqiao Group (1378.HK – Neutral), China (Daniel Kang) China Summit 2014: Feeback from the Conference

IJM Corporation (IJMS.KL – Overweight), Malaysia (Hoy Kit Mak) Introducing the IJM Corp/IJM Land arbitrage/intrinsic value calculator

IJM Corporation (IJMS.KL – Overweight), Malaysia (Hoy Kit Mak) Scomi investment finally pays off - ALERT

Infosys (INFY.BO – Overweight), India (Viju K George) Revenue growth recovery will likely get delayed due to the management change; this could be a long haul for Infosys

Infosys (INFY.BO – Overweight), India (Viju K George) Vishal Sikka will be the next CEO of Infosys; this could likely be a long haul even if he's the right man for the job

Lenovo Group Limited (0992.HK – Overweight), China (Gokul Hariharan) China Summit 2014: Feedback from the conference – PC profit growth and Moto share gains remain the upside catalysts

Namchow Chemical Industrial Co. (1702.TT, – Not Covered), Taiwan (Andre Chang, CFA) Company Visit Note

Strategy

Emerging Markets Strategy Dashboards, Global (Adrian Mowat) Identifying change and providing perspective on key economic and equity market data of global emerging markets

Q-Strategy Help in EM, Global (Sanaya Tavaria) Stock screens that combine thematic macro and quant

Economics

A par for the course May CPI print, India (Sajjid Z Chinoy)

April IP delivers a housewarming gift to the new government, India (Sajjid Z Chinoy)

Bank of Korea on hold, with comments in line with our expectation, South Korea (Min Joo Kang)

BI holds; focus still on current account balance, Indonesia (Benjamin Shatil)

Import prices declined in May, South Korea (Min Joo Kang)

May new loans higher than expected; signs of rebalancing between bank loans and non-bank financing, China (Grace Ng)

What’s not to like about India’s May trade deficit?, India (Sajjid Z Chinoy)

Sector Research

Asian Refining update, Asia Pacific (Samuel Lee, CFA) Weak middle distillates have led GRMs lower in 2Q

Asian shipbuilding industries, South Korea (Sokje Lee) New shipping economics in eco-ship epoch

Hong Kong Property, Hong Kong (Cusson Leung) Falling land prices to sustain development returns

Hong Kong Property, Hong Kong (Cusson Leung) Intensifying primary launches; stay positive on developers

Indonesia Automobiles, Indonesia (Aditya Srinath, CFA) Engine Check: Datsun Go+ completes the LCGC Competitive Landscape

Know Your Power, India (Sumit Kishore) Election euphoria does not translate into demand growth or PLF improvement in May

4

Promise Inc(3057.TW, – Not Covered), Taiwan (Gokul Hariharan) Riding the strong big data trend - Company Visit Note

SP Setia (SETI.KL – Neutral), Malaysia (Simone Yeoh) 1HFY14 results: Profits below expectations, but pre-sales in line

Weichai Power (2338.HK – Overweight), China (Karen Li, CFA) A step forward to become a world champion with control in KION obtained

Thailand O&G, Thailand (Scott L Darling) Diesel prices cut by 14 satang; slightly negative for PTT Plc

Australia

Publications

Goodman Group (GMG, OW – A$5.19) (Richard Jones, CFA) Japan projects lift FY14 EPS guidance to 7%

Seven Group Holdings (SVW, N – A$7.70) (Anthony Passe-de Silva) Scheme fails to bridge nexus to oil & gas but Group keeps looking

Mineral Resources Limited (MIN, UW – A$9.70) (Anthony Passe-de Silva) Questioning MIN's step into AQA battle

Newcrest Mining (NCM, N – A$9.71) (Mark Busuttil) Higher than expected depreciation expense sees downgrades to FY15 NPAT estimate

Ramsay Health Care (RHC, N – A$46.80) (Steven Wheen) Acquisition now a fait accompli

Publications, continued

Leighton Holdings Limited (LEI, UW – A$19.81) (Anthony Passe-de Silva) Taking steps on path to strategic change but plenty of uncertainty remains

Strategy Weekender (Paul Brunker) Asian investors on Aussie equities: more puzzled than hurt

Australia Economic Update (Ben Jarman) Labour supply ebbs further in Australia

New Zealand Economic Update (Ben Jarman) Wheeler of fortune

Ocado (Borja Olcese) A unique and disruptive business model. Initiating coverage with an Overweight rating and 500p PT

Japan

Recommendation Changes

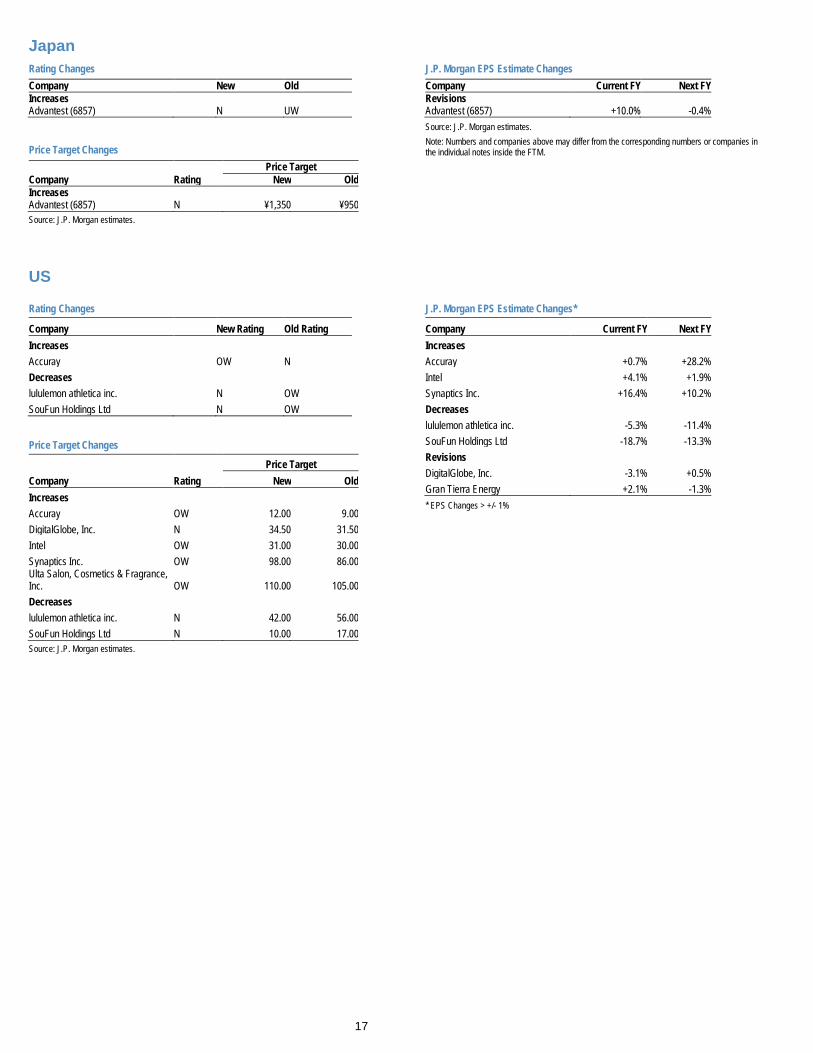

▲Advantest (6857) (Neutral) (Hisashi Moriyama) Order Trend Strong, Underweight Rating No Longer Justified; Upgrading to Neutral

Price Target and Estimate Changes Advantest (6857) (Neutral) (Hisashi Moriyama) Order Trend Strong, Underweight Rating No Longer Justified; Upgrading to Neutral

Results and Company Views Kirin Holdings (2503) (Overweight) (Ritsuko Tsunoda) The World Cup Is Finally Here—Will the Spotlight Fall on Kirin?

Results and Company Views, continued Nintendo (7974) (Underweight) (Haruka Mori) E3 Report (3): Takeaways from Analyst Briefing, Tour of E3 Booth - ALERT

Yamato Holdings (9064) (Neutral) (Dan Lu) Nikkei Reports Eight-company Joint Trucking Initiative - ALERT

Strategy Tokyo Signals, Noise & Strategy - Vol 20 (Patrick Rial, CFA) Are You Paying Attention?

Sector Research Electronic Components Update (Masashi Itaya) May Sales: Rohm

5

LatAm

Recommendation, Price Target and Estimate Changes

Gran Tierra Energy (GTE – Overweight) (Caio M Carvalhal) We Continue Positive on Peruvian Operations and Reinforce OW and Top Pick

LatAm Company and Sector News

Food Retail in Emerging Markets (Andrea Teixeira, CFA) Favor Retailers that Expand Profitably. Picks are: Walmex, CBD, Magnit, Lenta, Savola & BIM

Strategy

Brazil Equity Strategy Presentation (Emy Shayo Cherman) Binary Outcome

Emerging Markets Strategy Dashboards (Adrian Mowat) Identifying change and providing perspective on key economic and equity market data of global emerging markets

JPMQ : Global Pairs Trading Ideas (Robert Smith)

Price Reactions To Earnings Announcements (Robert Smith) Latest True Market Surprises For Global Stocks

Strategy, continued

Q-Strategy Help in EM (Sanaya Tavaria) Stock screens that combine thematic macro and quant

The Earnings Landscape (Robert Smith) EPS revisions ratios for all the major regions and markets

Economics

Brazil (Cassiana Fernandez) The blues remains the same

Credit Research

Gildemeister (AUTGIL - Underweight) (Daniel Sensel) 1Q14 review: "You've got a fast car. Is it fast enough so you can fly away?" - We don't think so

Marfrig (MARFRI - Neutral) (Daniel Sensel) The '20s Look Attractive After the Issuance of the New '19s and the Launch of the Tender for the '21s

CEEMEA

Strategy

Emerging Markets Strategy Dashboards (Adrian Mowat) Identifying change and providing perspective on key economic and equity market data of global emerging markets

Q-Strategy Help in EM (Sanaya Tavaria) Stock screens that combine thematic macro and quant

Economics

Middle East and North Africa Today (Brahim Razgallah)

Economics, continued

Turkey (Yarkin Cebeci) CAD narrows, financing improves in April

Commodities and FX

Natural Gas Weekly & Storage Recap (Scott C. Speaker) Price action suggests gas market recognition of lower end-October storage trajectory potential

6

US

Recommendation Changes

▲Accuray (ARAY – Overweight) (Tycho W. Peterson) Upgrading to Overweight on Continued Order Momentum and Attractive Valuation; PT Goes to $12

▼lululemon athletica inc. (LULU – Neutral) (Brian J. Tunick) Downgrading to Neutral; Decelerating Comps, Rising Investments, and Margin Pressures Pushing Us to the Sidelines

Price Target and Estimate Changes

Accuray (ARAY – Overweight) (Tycho W. Peterson) Upgrading to Overweight on Continued Order Momentum and Attractive Valuation; PT Goes to $12

DigitalGlobe, Inc. (DGI – Neutral) (Paul Coster, CFA) Tweaking Estimates; Establishing YE15 Price Target of $34.50

Intel (INTC – Overweight) (Christopher Danely) Intel Hikes 2Q14 and 2014 Guidance on PC Demand Upside. Raising Estimates and Reiterate Overweight

lululemon athletica inc. (LULU – Neutral) (Brian J. Tunick) Downgrading to Neutral; Decelerating Comps, Rising Investments, and Margin Pressures Pushing Us to the Sidelines

Synaptics Inc. (SYNA – Overweight) (Paul Coster, CFA) Adjusting Model for Renesas; Price Target Goes to $98.00

Ulta Salon, Cosmetics & Fragrance, Inc. (ULTA – Overweight) (Brian J. Tunick) Takeaways from ULTA HQ Visit

Results and Company Views

bluebird bio (BLUE – Overweight) (Cory Kasimov) Previewing Initial Look at LentiGlobin Gene Therapy Data in Beta-Thalassemia at EHA This Weekend

C.R. Bard Inc. (BCR – Neutral) (Michael Weinstein) Panel Support is Unanimous; Modest Efficacy Leaves Door Open for Competition - ALERT

CONSOL Energy (CNX – Overweight) (John Bridges, CFA, ACSM) Everything's Relative; but Compared with the Coal Sector, this Duckling is Now a Swan.

LabCorp (LH – Neutral) (Lisa C. Gill) LH Week Day 5: Conference Call Recap

Results and Company Views, continued

Nektar Therapeutics (NKTR – Overweight) (Cory Kasimov) OIC Panel Provides Some Welcome Relief for Naloxegol... We Anticipate Approval by the 9/16 PDUFA - ALERT

Santander Consumer (SC) (SC – Overweight) (Richard Shane) SC On-Site Visit - ALERT

Strategy

JPMQ: Pairs Trade Model (Dubravko Lakos-Bujas) Pair Trade Close Alert (UAL US / LUV US)

Sector Research

Clinical Laboratories (Lisa C. Gill) Another Positive Month for Office Visits in May - ALERT

Communications Equipment & Data Networking (Rod Hall, CFA) Hall Monitor: June 2014

EE/MI (C. Stephen Tusa, Jr CFA) Takeaways from JPM China Conference: The Year of the Duck

Energy Infrastructure/MLPs (Jeremy Tonet, CFA) Weekly Comp Tables

JPM Trust Tracker (Richard Shane) May 2014 Preview

Med Utilization Tracker (Justin Lake) Doc Office Visits +1.2% in May

Medical Utilization Tracker (Michael Weinstein) Physician Office Visits Up 1.2% in May

Monthly Tire Review: June 2014 (Ryan Brinkman) Industry Fundamentals Strong: Expect Slower But Still Solid Growth As Shipments Cycle Tougher Comps

U.S. Asset Managers (Kenneth B. Worthington, CFA) May 2014 Monthly Performance/Sales: Weaker Sales MoM (ex. MM) Driven by Lower US Equity Sales

U.S. Asset Managers (Kenneth B. Worthington, CFA) Weekly Fund Flows: Jun 05 - Jun 11. Fixed Income and Equity Up, MM Funds Show Outflows

www.jpmorganmarkets.com

Europe Equity Research13 June 2014

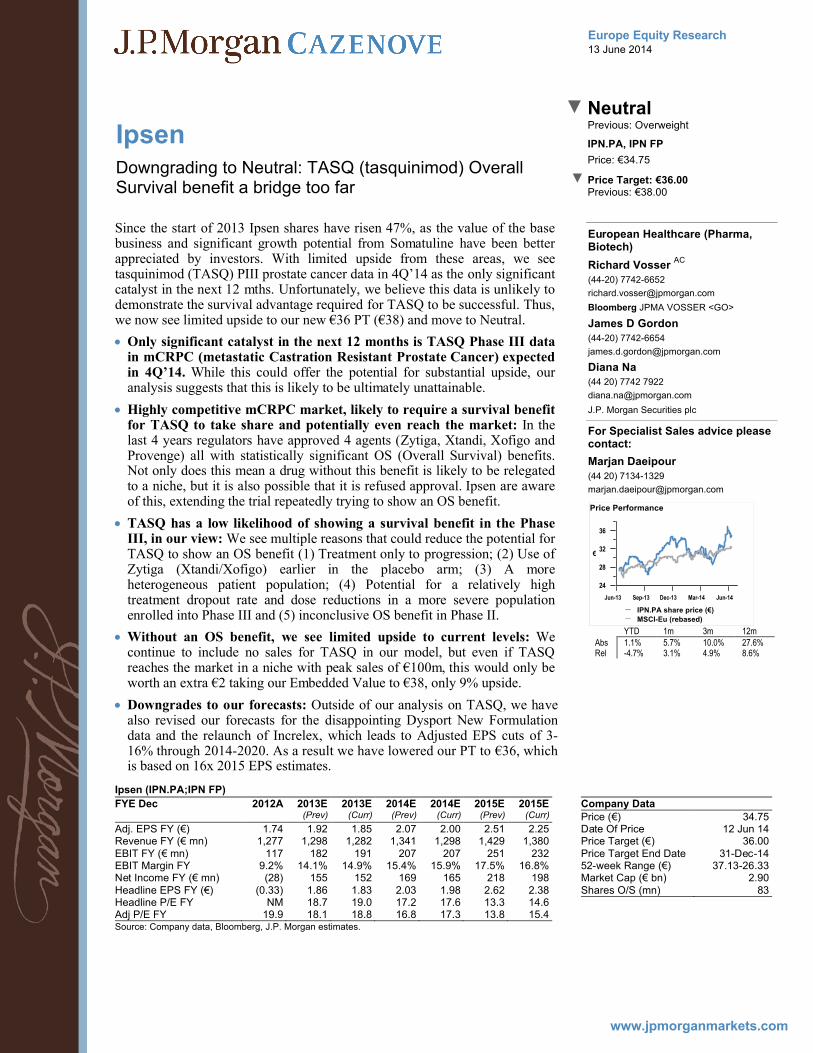

Ipsen▼ Neutral

Previous: Overweight

IPN.PA, IPN FP

Downgrading to Neutral: TASQ (tasquinimod) Overall Survival benefit a bridge too far

▼

Price: €34.75

Price Target: €36.00Previous: €38.00

European Healthcare (Pharma, Biotech)

Richard Vosser AC

(44-20) 7742-6652

Bloomberg JPMA VOSSER <GO>

James D Gordon

(44-20) 7742-6654

Diana Na

(44 20) 7742 7922

J.P. Morgan Securities plc

For Specialist Sales advice please contact:

Marjan Daeipour

(44 20) 7134-1329

YTD 1m 3m 12mAbs 1.1% 5.7% 10.0% 27.6%Rel -4.7% 3.1% 4.9% 8.6%

Ipsen (IPN.PA;IPN FP)

FYE Dec 2012A 2013E(Prev)

2013E(Curr)

2014E(Prev)

2014E(Curr)

2015E(Prev)

2015E(Curr)

Adj. EPS FY (€) 1.74 1.92 1.85 2.07 2.00 2.51 2.25Revenue FY (€ mn) 1,277 1,298 1,282 1,341 1,298 1,429 1,380EBIT FY (€ mn) 117 182 191 207 207 251 232EBIT Margin FY 9.2% 14.1% 14.9% 15.4% 15.9% 17.5% 16.8%Net Income FY (€ mn) (28) 155 152 169 165 218 198Headline EPS FY (€) (0.33) 1.86 1.83 2.03 1.98 2.62 2.38Headline P/E FY NM 18.7 19.0 17.2 17.6 13.3 14.6Adj P/E FY 19.9 18.1 18.8 16.8 17.3 13.8 15.4Source: Company data, Bloomberg, J.P. Morgan estimates.

Company DataPrice (€) 34.75Date Of Price 12 Jun 14Price Target (€) 36.00Price Target End Date 31-Dec-1452-week Range (€) 37.13-26.33Market Cap (€ bn) 2.90Shares O/S (mn) 83

See page 21 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

24

28

32

36

€

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Price Performance

IPN.PA share price (€)

MSCI-Eu (rebased)

Since the start of 2013 Ipsen shares have risen 47%, as the value of the base business and significant growth potential from Somatuline have been betterappreciated by investors. With limited upside from these areas, we see tasquinimod (TASQ) PIII prostate cancer data in 4Q’14 as the only significant catalyst in the next 12 mths. Unfortunately, we believe this data is unlikely to demonstrate the survival advantage required for TASQ to be successful. Thus,we now see limited upside to our new €36 PT (€38) and move to Neutral.

Only significant catalyst in the next 12 months is TASQ Phase III data in mCRPC (metastatic Castration Resistant Prostate Cancer) expected in 4Q’14. While this could offer the potential for substantial upside, our analysis suggests that this is likely to be ultimately unattainable.

Highly competitive mCRPC market, likely to require a survival benefit for TASQ to take share and potentially even reach the market: In the last 4 years regulators have approved 4 agents (Zytiga, Xtandi, Xofigo and Provenge) all with statistically significant OS (Overall Survival) benefits. Not only does this mean a drug without this benefit is likely to be relegated to a niche, but it is also possible that it is refused approval. Ipsen are aware of this, extending the trial repeatedly trying to show an OS benefit.

TASQ has a low likelihood of showing a survival benefit in the Phase III, in our view: We see multiple reasons that could reduce the potential for TASQ to show an OS benefit (1) Treatment only to progression; (2) Use of Zytiga (Xtandi/Xofigo) earlier in the placebo arm; (3) A more heterogeneous patient population; (4) Potential for a relatively high treatment dropout rate and dose reductions in a more severe population enrolled into Phase III and (5) inconclusive OS benefit in Phase II.

Without an OS benefit, we see limited upside to current levels: We continue to include no sales for TASQ in our model, but even if TASQreaches the market in a niche with peak sales of €100m, this would only be worth an extra €2 taking our Embedded Value to €38, only 9% upside.

Downgrades to our forecasts: Outside of our analysis on TASQ, we have also revised our forecasts for the disappointing Dysport New Formulation data and the relaunch of Increlex, which leads to Adjusted EPS cuts of 3-16% through 2014-2020. As a result we have lowered our PT to €36, which is based on 16x 2015 EPS estimates.

www.jpmorganmarkets.com

Europe Equity Research13 June 2014

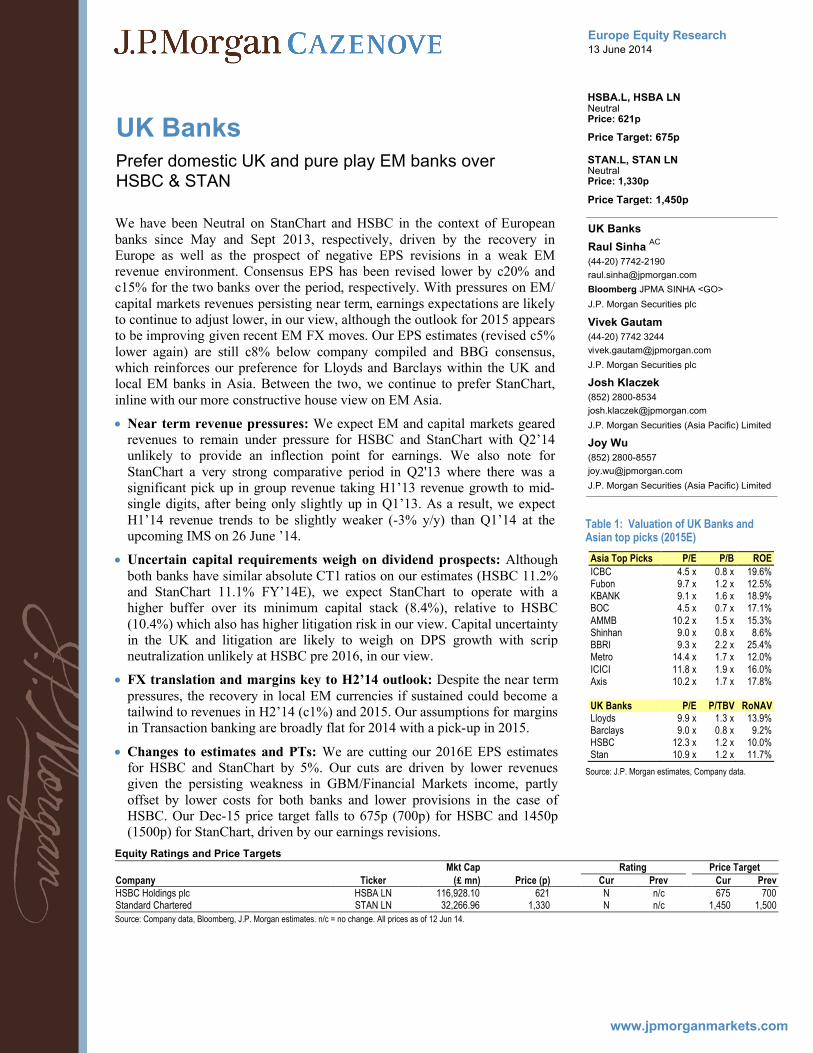

UK Banks

HSBA.L, HSBA LNNeutralPrice: 621p

Price Target: 675p

Prefer domestic UK and pure play EM banks over HSBC & STAN

STAN.L, STAN LNNeutralPrice: 1,330p

Price Target: 1,450p

UK Banks

Raul Sinha AC

(44-20) 7742-2190

Bloomberg JPMA SINHA <GO>

J.P. Morgan Securities plc

Vivek Gautam

(44-20) 7742 3244

J.P. Morgan Securities plc

Josh Klaczek

(852) 2800-8534

J.P. Morgan Securities (Asia Pacific) Limited

Joy Wu

(852) 2800-8557

J.P. Morgan Securities (Asia Pacific) Limited

Equity Ratings and Price Targets

Mkt Cap Rating Price TargetCompany Ticker (£ mn) Price (p) Cur Prev Cur PrevHSBC Holdings plc HSBA LN 116,928.10 621 N n/c 675 700Standard Chartered STAN LN 32,266.96 1,330 N n/c 1,450 1,500

Source: Company data, Bloomberg, J.P. Morgan estimates. n/c = no change. All prices as of 12 Jun 14.

See page 17 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

We have been Neutral on StanChart and HSBC in the context of European banks since May and Sept 2013, respectively, driven by the recovery in Europe as well as the prospect of negative EPS revisions in a weak EM revenue environment. Consensus EPS has been revised lower by c20% and c15% for the two banks over the period, respectively. With pressures on EM/capital markets revenues persisting near term, earnings expectations are likely to continue to adjust lower, in our view, although the outlook for 2015 appears to be improving given recent EM FX moves. Our EPS estimates (revised c5% lower again) are still c8% below company compiled and BBG consensus, which reinforces our preference for Lloyds and Barclays within the UK and local EM banks in Asia. Between the two, we continue to prefer StanChart, inline with our more constructive house view on EM Asia.

Near term revenue pressures: We expect EM and capital markets geared revenues to remain under pressure for HSBC and StanChart with Q2’14 unlikely to provide an inflection point for earnings. We also note for StanChart a very strong comparative period in Q2'13 where there was a significant pick up in group revenue taking H1’13 revenue growth to mid-single digits, after being only slightly up in Q1’13. As a result, we expect H1’14 revenue trends to be slightly weaker (-3% y/y) than Q1’14 at the upcoming IMS on 26 June ’14.

Uncertain capital requirements weigh on dividend prospects: Although both banks have similar absolute CT1 ratios on our estimates (HSBC 11.2% and StanChart 11.1% FY’14E), we expect StanChart to operate with a higher buffer over its minimum capital stack (8.4%), relative to HSBC (10.4%) which also has higher litigation risk in our view. Capital uncertainty in the UK and litigation are likely to weigh on DPS growth with scrip neutralization unlikely at HSBC pre 2016, in our view.

FX translation and margins key to H2’14 outlook: Despite the near term pressures, the recovery in local EM currencies if sustained could become a tailwind to revenues in H2’14 (c1%) and 2015. Our assumptions for margins in Transaction banking are broadly flat for 2014 with a pick-up in 2015.

Changes to estimates and PTs: We are cutting our 2016E EPS estimates for HSBC and StanChart by 5%. Our cuts are driven by lower revenues given the persisting weakness in GBM/Financial Markets income, partlyoffset by lower costs for both banks and lower provisions in the case of HSBC. Our Dec-15 price target falls to 675p (700p) for HSBC and 1450p (1500p) for StanChart, driven by our earnings revisions.

Table 1: Valuation of UK Banks and Asian top picks (2015E)

Asia Top Picks P/E P/B ROE

ICBC 4.5 x 0.8 x 19.6%Fubon 9.7 x 1.2 x 12.5%KBANK 9.1 x 1.6 x 18.9%BOC 4.5 x 0.7 x 17.1%AMMB 10.2 x 1.5 x 15.3%Shinhan 9.0 x 0.8 x 8.6%BBRI 9.3 x 2.2 x 25.4%Metro 14.4 x 1.7 x 12.0%ICICI 11.8 x 1.9 x 16.0%Axis 10.2 x 1.7 x 17.8%

UK Banks P/E P/TBV RoNAVLloyds 9.9 x 1.3 x 13.9%Barclays 9.0 x 0.8 x 9.2%HSBC 12.3 x 1.2 x 10.0%Stan 10.9 x 1.2 x 11.7%

Source: J.P. Morgan estimates, Company data.

www.jpmorganmarkets.com

Europe Equity Research13 June 2014

European TechnologyWhat to expect at the J.P. Morgan Technology CEO Conference next week - ALERT

European Technology

Sandeep Deshpande AC

(44-20) 7134-5276

Bloomberg JPMA DESHPANDE <GO>

J.P. Morgan Securities plc

Stacy Pollard AC

(44-20) 7134-5420

Bloomberg JPMA POLLARD <GO>

J.P. Morgan Securities plc

Chetan Udeshi, CFA

(91-22) 6157-3319

J.P. Morgan India Private Limited

Hannes Leitner

(44-20) 7742-8666

J.P. Morgan Securities plc

See page 2 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

We have 36 hardware and software companies attending the conference: Several companies (such as SAP, STMicro, ARM, Dassault, Hexagon, and Capgemini) have recently hosted Capital Markets Days, and we look forward to hearing more details on their updated strategies and financial plans. Overall,we expect to get a mood of the end market whether consumer or enterprise, development of risk or opportunity in the supply chain as well as gain some color into businesses going into 2H14.

Semiconductor stocks are on a roll so we will be looking to probe whether there are roadblocks coming: The SOX is up 16.4% year to date and most major stocks in our space our on a roll with improving sales and margin. The risk for semi companies is over-build and inventory; thus we will be probing risk of that happening over the next couple of quarters by questioning companies on allocation or lack thereof and lead times. Investors will also be looking at timing of “take off” of new drivers such as Internet of Things as well as whether there is potential for another run in smartphones/tablets.

In Software/Services, SMAC themes are bound to prevail. SMAC = Social, Mobile, Analytics (Big Data) and Cloud. The SMAC trends are a major driver for companies like SAP and Capgemini and, although perhaps slower to be adopted in the CAD/PLM space, companies like Hexagon, Dassault and Aveva will also likely touch on these topics. In addition, JPM analyst Stacy Pollard will host a brief 10-minute session on the morning of the 18th about the Cloud, with materials from the JPM CIO Cloud Survey as well as a recent SaaS Primer report.

In Communications tech focus will be on China build, European potential, margin and potential for disruption by SDN/NFV: China wireless build is a significant ongoing revenue driver in wireless equipment so we will be looking at spending progress on that front as well as whether Europe 4G will at last begin to impact equipment company revenues by 2H. Most comm. tech companies have improving margin YoY as the competitive environment has improved – so can the good times continue or will companies begin to aggressively compete for share at expense of margin. Finally there will also be questions on mid term potential of SDN/NFV to disrupt the router business but also the radio networks.

We are featuring a panel of J.P. Morgan IT experts on the 18th June, where we will hear the firm’s overall IT spending plans in 2014, as well as particular trends in hot areas such as Data & Analytics, Security and Digital infrastructure, among others. Indeed, we’ll hear from both sides (IT buyer and seller) with regards to banks – because we also have several software vendors focused on the financial services sector (Temenos, SimCorp and Misys), and of course this sector remains a large percentage of the revenues for companies like Capgemini (22% for 2013).

The conference runs from 8:30am to 5:00pm both days, the 17th and 18th of June. We also invite you to join us for a Drinks Reception and World Cup Screening from 5:00pm on the 17th.

www.jpmorganmarkets.com

Japan Equity Research12 June 2014

Clients should contact representatives and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

Tokyo Signals, Noise & Strategy - Vol 20Are You Paying Attention?

Strategy

Patrick Rial, CFA AC

(81-3) 6736-8649

JPMorgan Securities Japan Co., Ltd.

Jesper J Koll

(81-3) 6736-8600

JPMorgan Securities Japan Co., Ltd.

Rajiv Batra

(91-22) 6157-3568

J.P. Morgan India Private Limited

See page 18 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor inmaking their investment decision.

“Like three days passing / cherry blossoms gone, unseen / how I see this world” –Ryota Oshima, 18th century haiku poet.

The governance structure of Japan Inc. that persisted throughout the post-War era, which denied shareholders a voice, and certainly their claim as the ultimate owners of capital, is weakening.

Japan’s political leadership has embarked on a fundamental reorientation: return on capital matters and shareholders are moving from the fringe to the center. The concrete steps in the adoption of the stewardship code by domestic asset managers, national pension reform, and the traction that the JPX-Nikkei 400 is generating, all speak to this trend.

Naysayers claim that Japan still lags the rest of the world. While we have quibbles with such generalizations, on the whole, they are correct. However, in the market, fortunes are rarely made by pointing out the way things are, but rather in recognizing changes on the margin that are not yet discounted.

With this in mind, we note that the JPX-Nikkei 400 is emerging as a topic of interest among both investors and corporates. An index rebalance will be announced on Aug. 7. While we think the index has shortcomings as an investment, companies appear eager to take steps to gain admission to this group of “Japan All Stars.” In that sense, the potential impact of the index is greater than if it were an investment product alone.

The speed at which the stewardship code is being adopted by domesticinstitutions has also been a positive surprise. In total, 127 fund operators, both foreign and domestic, have pledged to adopt the code. In the long run, this represents a tidal change in fiduciary oversight, and investors who aren’t paying attention risk missing the cherry blossoms before they fall, in our view.

From the business weeklies: Weekly Toyo Keizai advises on how to navigate the treacherous IPO and new issues markets in Japan. The magazine also surveys top auto journalists on the strength of Toyota’s revival. Diamond Weekly looks at the Sharp’s Kameyama plant 10 years after opening.

New insights from our analysts: Dairo Murata sees top convenience stores continuing to squeeze out 2nd-tier rivals with continuous new store openingsand better cost structures. Hisashi Moriyama raises Toshiba and Fuji Electric to “Overweight” as the consolidation phase in domestic semiconductors has resulted in a limited number of strong players, while the “Internet of things” is set to drive top-line growth going forward.

TIJ: The secrets of Nagano residents' longevity are revealed.

ContentsStrategy Insights 2Noise & Signals from the Local Press 9Tactical View – Neutral 10New Insights from Our Analysts 11J.P. Morgan Japan Top-Down Thesis 12What We’re Watching – Key Drivers of Our Thesis 14This is Japan 15Tokyo Signals, Noise & Strategy Backlog 16

www.jpmorganmarkets.com

Asia Pacific Equity Research12 June 2014

Clients should contact representatives and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

Asian shipbuilding industriesNew shipping economics in eco-ship epoch

Ship Building & Repairs

Sokje Lee AC

(82-2) 758-5729

Bloomberg JPMA SOKJELEE <GO>

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

Minsung Lee

(822) 758-5728

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

Jesper J Koll

(81-3) 6736-8600

JPMorgan Securities Japan Co., Ltd.

See page 12 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

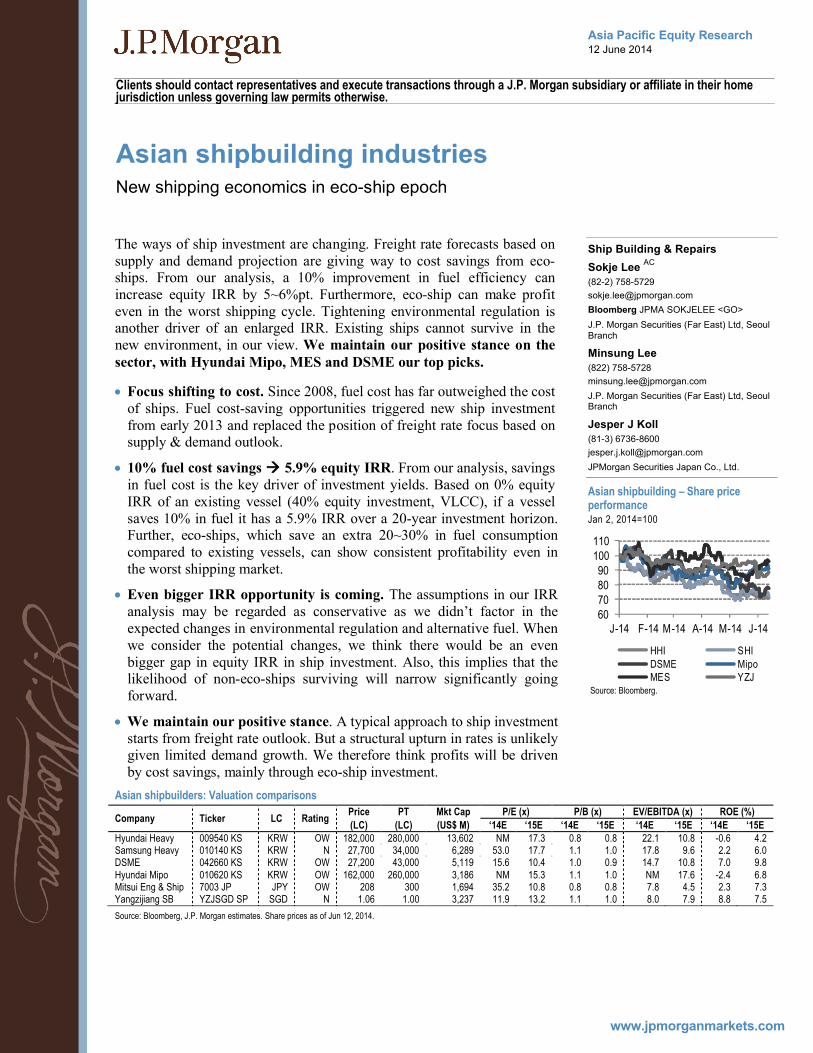

The ways of ship investment are changing. Freight rate forecasts based on supply and demand projection are giving way to cost savings from eco-ships. From our analysis, a 10% improvement in fuel efficiency can increase equity IRR by 5~6%pt. Furthermore, eco-ship can make profit even in the worst shipping cycle. Tightening environmental regulation is another driver of an enlarged IRR. Existing ships cannot survive in the new environment, in our view. We maintain our positive stance on the sector, with Hyundai Mipo, MES and DSME our top picks.

Focus shifting to cost. Since 2008, fuel cost has far outweighed the cost of ships. Fuel cost-saving opportunities triggered new ship investment from early 2013 and replaced the position of freight rate focus based on supply & demand outlook.

10% fuel cost savings 5.9% equity IRR. From our analysis, savings in fuel cost is the key driver of investment yields. Based on 0% equity IRR of an existing vessel (40% equity investment, VLCC), if a vessel saves 10% in fuel it has a 5.9% IRR over a 20-year investment horizon. Further, eco-ships, which save an extra 20~30% in fuel consumption compared to existing vessels, can show consistent profitability even in the worst shipping market.

Even bigger IRR opportunity is coming. The assumptions in our IRR analysis may be regarded as conservative as we didn’t factor in the expected changes in environmental regulation and alternative fuel. When we consider the potential changes, we think there would be an even bigger gap in equity IRR in ship investment. Also, this implies that the likelihood of non-eco-ships surviving will narrow significantly going forward.

We maintain our positive stance. A typical approach to ship investment starts from freight rate outlook. But a structural upturn in rates is unlikely given limited demand growth. We therefore think profits will be driven by cost savings, mainly through eco-ship investment.

Asian shipbuilders: Valuation comparisons

Company Ticker LC RatingPrice PT Mkt Cap P/E (x) P/B (x) EV/EBITDA (x) ROE (%)

(LC) (LC) (US$ M) ‘14E ‘15E ‘14E ‘15E ‘14E ‘15E ‘14E ‘15EHyundai Heavy 009540 KS KRW OW 182,000 280,000 13,602 NM 17.3 0.8 0.8 22.1 10.8 -0.6 4.2Samsung Heavy 010140 KS KRW N 27,700 34,000 6,289 53.0 17.7 1.1 1.0 17.8 9.6 2.2 6.0DSME 042660 KS KRW OW 27,200 43,000 5,119 15.6 10.4 1.0 0.9 14.7 10.8 7.0 9.8Hyundai Mipo 010620 KS KRW OW 162,000 260,000 3,186 NM 15.3 1.1 1.0 NM 17.6 -2.4 6.8Mitsui Eng & Ship 7003 JP JPY OW 208 300 1,694 35.2 10.8 0.8 0.8 7.8 4.5 2.3 7.3Yangzijiang SB YZJSGD SP SGD N 1.06 1.00 3,237 11.9 13.2 1.1 1.0 8.0 7.9 8.8 7.5

Source: Bloomberg, J.P. Morgan estimates. Share prices as of Jun 12, 2014.

Asian shipbuilding – Share price performanceJan 2, 2014=100

Source: Bloomberg.

60708090

100110

J-14 F-14 M-14 A-14 M-14 J-14

HHI SHIDSME MipoMES YZJ

www.jpmorganmarkets.com

Asia Pacific Equity Research12 June 2014

Indonesia AutomobilesEngine Check: Datsun Go+ completes the LCGC Competitive Landscape

Head of ASEAN Strategy & Indonesian Research

Aditya Srinath, CFA AC

(62-21) 5291-8573

Bloomberg JPMA SRINATH <GO>

PT J.P. Morgan Securities Indonesia

Indra Cahya

(62-21) 5291-8575

PT J.P. Morgan Securities Indonesia

Nick Lai

(852) 2800 8543

J.P. Morgan Securities (Asia Pacific) Limited

Akira Kishimoto

(81-3) 6736-8646

JPMorgan Securities Japan Co., Ltd.

See page 5 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

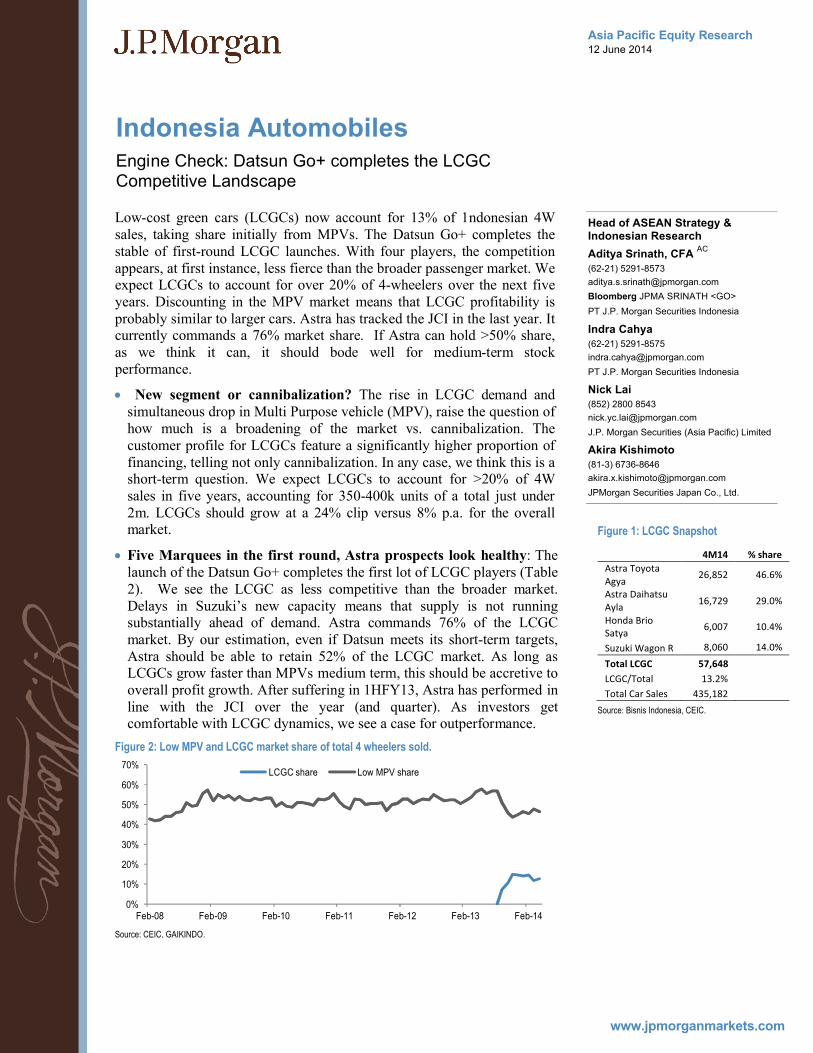

Low-cost green cars (LCGCs) now account for 13% of 1ndonesian 4W sales, taking share initially from MPVs. The Datsun Go+ completes the stable of first-round LCGC launches. With four players, the competition appears, at first instance, less fierce than the broader passenger market. We expect LCGCs to account for over 20% of 4-wheelers over the next fiveyears. Discounting in the MPV market means that LCGC profitability is probably similar to larger cars. Astra has tracked the JCI in the last year. It currently commands a 76% market share. If Astra can hold >50% share, as we think it can, it should bode well for medium-term stock performance.

New segment or cannibalization? The rise in LCGC demand and simultaneous drop in Multi Purpose vehicle (MPV), raise the question of how much is a broadening of the market vs. cannibalization. The customer profile for LCGCs feature a significantly higher proportion offinancing, telling not only cannibalization. In any case, we think this is a short-term question. We expect LCGCs to account for >20% of 4W sales in five years, accounting for 350-400k units of a total just under 2m. LCGCs should grow at a 24% clip versus 8% p.a. for the overall market.

Five Marquees in the first round, Astra prospects look healthy: The launch of the Datsun Go+ completes the first lot of LCGC players (Table 2). We see the LCGC as less competitive than the broader market. Delays in Suzuki’s new capacity means that supply is not running substantially ahead of demand. Astra commands 76% of the LCGC market. By our estimation, even if Datsun meets its short-term targets, Astra should be able to retain 52% of the LCGC market. As long as LCGCs grow faster than MPVs medium term, this should be accretive to overall profit growth. After suffering in 1HFY13, Astra has performed in line with the JCI over the year (and quarter). As investors get comfortable with LCGC dynamics, we see a case for outperformance.

Figure 2: Low MPV and LCGC market share of total 4 wheelers sold.

Source: CEIC, GAIKINDO.

0%

10%

20%

30%

40%

50%

60%

70%

Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13 Feb-14

LCGC share Low MPV share

Figure 1: LCGC Snapshot

4M14 % share

Astra Toyota Agya

26,852 46.6%

Astra Daihatsu Ayla

16,729 29.0%

Honda Brio Satya

6,007 10.4%

Suzuki Wagon R 8,060 14.0%

Total LCGC 57,648

LCGC/Total 13.2%

Total Car Sales 435,182

Source: Bisnis Indonesia, CEIC.

www.jpmorganmarkets.com

Latin America Equity Research13 June 2014

Food Retail in Emerging MarketsFavor Retailers that Expand Profitably. Picks are: Walmex, CBD, Magnit, Lenta, Savola & BIM

LatAm Food & Beverage, Retail and Healthcare

Andrea Teixeira, CFA AC

(1-212) 622-6735

J.P. Morgan Securities LLC

Pedro Leduc

(52-55) 5339-4846

J.P. Morgan Casa de Bolsa, S.A. de C.V., J.P. Morgan Grupo Financiero

Joseph Giordano

(55-11) 4950-3020

Banco J.P. Morgan S.A.

South African Retail

Stephen Carrott

(27-11) 507-0373

J.P. Morgan Equities South Africa Proprietary Ltd.

Russian Consumer & Retail

Elena Jouronova, CFA

(7-495) 967-3888

J.P. Morgan Bank International LLC

European Retail

Borja Olcese

(34-91) 516-1511

J.P. Morgan Securities plc

Jaime Vazquez

(34-91) 516-1421

J.P. Morgan Securities plc

Poland Consumer

Michal Kuzawinski

(48-22) 44 19534

J.P. Morgan Securities plc

MENA Consumer

Muneeza Hasan

(971) 4428-1766

JPMorgan Chase Bank, N.A., Dubai Branch

See page 17 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor inmaking their investment decision.

In the second annual edition of this proprietary analysis, in collaboration with six of our Global consumer equity research teams, including LatAm, Middle East, Poland, Russia, South Africa, and Turkey teams. We analyzed and contrasted key performance and valuation metrics for 21 food retailers in our coverage universe in EM. Our main conclusion is that investors should continue to favor retailers that deliver floor space growth that is accretive to returns, as stock performance tends to track ROIC. EV/EBITDAR, and enterprise value over invested capital against ROIC shows a good predictor of performance (all adjusted for leases).

In LatAm, we continue to favor Walmex, CBD (food), Falabella and Inretail. All these companies have been growing floor space with returns higher than cost of capital, and delivering high marginal ROIC. Focus on small formats such as Bodega express (WMX) or Mini Mercado (CBD) has been paying off, and ROIC is one of the key determinants of EPS growth going forward.

We do not find compelling value in the South Africa food retailers given continued consumer macro-headwinds which have hit food retail sales growth particularly hard. Pick n’ Pay’s turnaround is gaining momentum, but on a Feb FY15 JPME PE of 32x, we feel this is more than priced in, hence our Underweight view. We continue to accumulate SHP on any dips in the share price.

In Russia we favor Magnit and Lenta. Both are, in our view, structural winners in the sector due to their low price formats, focus on operating efficiencies, quality management. Lenta is set to demonstrate the fastest growth among listed peers while Magnit’s attraction is also its strong balance sheet (we recommend buying Magnit’s local shares).

Our preference in Turkey remains for BIM, both in the short term and longer term. BIM has better growth prospects and returns and is less exposed to the cycle. Management also has better track record in delivering guidance.

We believe that the environment in Poland remains highly competitive, reflected in ongoing subdued sales and margin pressure at Biedronka. With negative sales momentum, and reduced margin visibility, we remain cautious.

Within MENA, Savola remains our preferred consumer play as we expect Savola’s retail segment (2014-16E JPMe 46% of rev & 32% of EBITDA) to drive the group’s mid to long-term earnings growth, with continued healthy Hyper/Super mkt ops and Savola’s foray into the convenience store format in 2013 where the company plans to take the total store count to 1,000 in 5yrs (JPMe 770 stores) from 23 in 2013. The segment is set to benefit from indigenous customer traffic underpinned by a healthy rate of urbanization, government spending and improving living standards resulting in growing preference for organized retail.

www.jpmorganmarkets.com

Japan Equity Research12 June 2014

Advantest (6857)▲ Neutral

Previous: Underweight

6857.T, 6857 JT

Order Trend Strong, Underweight Rating No Longer Justified; Upgrading to Neutral

▲

Price: ¥1,224

Price Target: ¥1,350Previous: ¥950

Japan

Electronics/Precision & Industrial

Hisashi Moriyama AC

(81-3) 6736-8601

Bloomberg JPMA MORIYAMA <GO>

JPMorgan Securities Japan Co., Ltd.

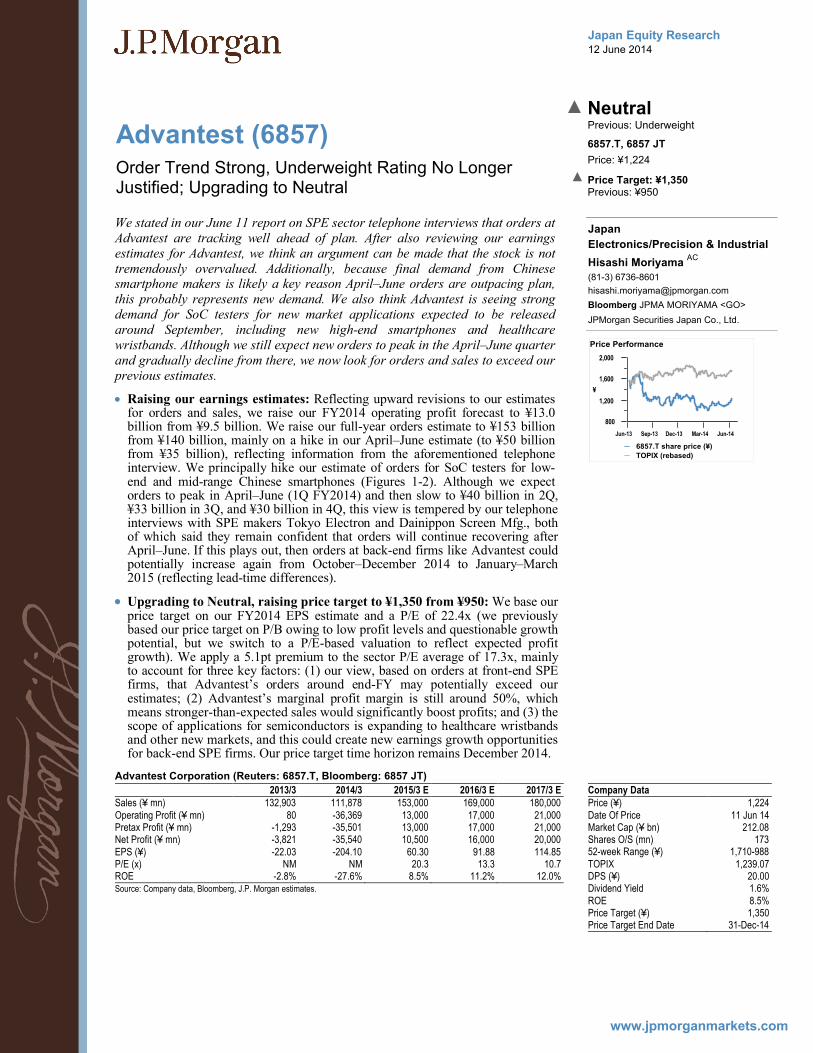

Advantest Corporation (Reuters: 6857.T, Bloomberg: 6857 JT)

2013/3 2014/3 2015/3 E 2016/3 E 2017/3 ESales (¥ mn) 132,903 111,878 153,000 169,000 180,000Operating Profit (¥ mn) 80 -36,369 13,000 17,000 21,000Pretax Profit (¥ mn) -1,293 -35,501 13,000 17,000 21,000Net Profit (¥ mn) -3,821 -35,540 10,500 16,000 20,000EPS (¥) -22.03 -204.10 60.30 91.88 114.85P/E (x) NM NM 20.3 13.3 10.7ROE -2.8% -27.6% 8.5% 11.2% 12.0%Source: Company data, Bloomberg, J.P. Morgan estimates.

Company DataPrice (¥) 1,224Date Of Price 11 Jun 14Market Cap (¥ bn) 212.08Shares O/S (mn) 17352-week Range (¥) 1,710-988TOPIX 1,239.07DPS (¥) 20.00Dividend Yield 1.6%ROE 8.5%Price Target (¥) 1,350Price Target End Date 31-Dec-14

See page 11 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

800

1,200

1,600

2,000

¥

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Price Performance

6857.T share price (¥)

TOPIX (rebased)

We stated in our June 11 report on SPE sector telephone interviews that orders at Advantest are tracking well ahead of plan. After also reviewing our earnings estimates for Advantest, we think an argument can be made that the stock is not tremendously overvalued. Additionally, because final demand from Chinese smartphone makers is likely a key reason April–June orders are outpacing plan, this probably represents new demand. We also think Advantest is seeing strong demand for SoC testers for new market applications expected to be released around September, including new high-end smartphones and healthcare wristbands. Although we still expect new orders to peak in the April–June quarter and gradually decline from there, we now look for orders and sales to exceed our previous estimates.

Raising our earnings estimates: Reflecting upward revisions to our estimates for orders and sales, we raise our FY2014 operating profit forecast to ¥13.0 billion from ¥9.5 billion. We raise our full-year orders estimate to ¥153 billion from ¥140 billion, mainly on a hike in our April–June estimate (to ¥50 billion from ¥35 billion), reflecting information from the aforementioned telephone interview. We principally hike our estimate of orders for SoC testers for low-end and mid-range Chinese smartphones (Figures 1-2). Although we expect orders to peak in April–June (1Q FY2014) and then slow to ¥40 billion in 2Q, ¥33 billion in 3Q, and ¥30 billion in 4Q, this view is tempered by our telephone interviews with SPE makers Tokyo Electron and Dainippon Screen Mfg., both of which said they remain confident that orders will continue recovering after April–June. If this plays out, then orders at back-end firms like Advantest could potentially increase again from October–December 2014 to January–March2015 (reflecting lead-time differences).

Upgrading to Neutral, raising price target to ¥1,350 from ¥950: We base our price target on our FY2014 EPS estimate and a P/E of 22.4x (we previously based our price target on P/B owing to low profit levels and questionable growth potential, but we switch to a P/E-based valuation to reflect expected profit growth). We apply a 5.1pt premium to the sector P/E average of 17.3x, mainly to account for three key factors: (1) our view, based on orders at front-end SPE firms, that Advantest’s orders around end-FY may potentially exceed our estimates; (2) Advantest’s marginal profit margin is still around 50%, which means stronger-than-expected sales would significantly boost profits; and (3) the scope of applications for semiconductors is expanding to healthcare wristbands and other new markets, and this could create new earnings growth opportunities for back-end SPE firms. Our price target time horizon remains December 2014.

www.jpmorganmarkets.com

Global Emerging Markets Equity Research13 June 2014

Q-Strategy Help in EMStock screens that combine thematic macro and quant

Emerging Markets Equity Strategy

Sanaya Tavaria AC

(1-212) 622-5469

J.P. Morgan Securities LLC

Adrian Mowat

(852) 2800-8599

J.P. Morgan Securities (Asia Pacific) Limited

Pedro Martins Junior, CFA

(55-11) 4950-4121

Banco J.P. Morgan S.A.

David Aserkoff, CFA

(44-20) 7134-5887

J.P. Morgan Securities plc

Rajiv Batra

(91-22) 6157-3568

J.P. Morgan India Private Limited

Kevyn H Kadakia

(91-22) 6157-3250

J.P. Morgan India Private Limited

Quantitative Strategy

Robert Smith AC

(852) 2800 8569

Bloomberg JPMA RSMITH <GO>

J.P. Morgan Securities (Asia Pacific) Limited

See page 8 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

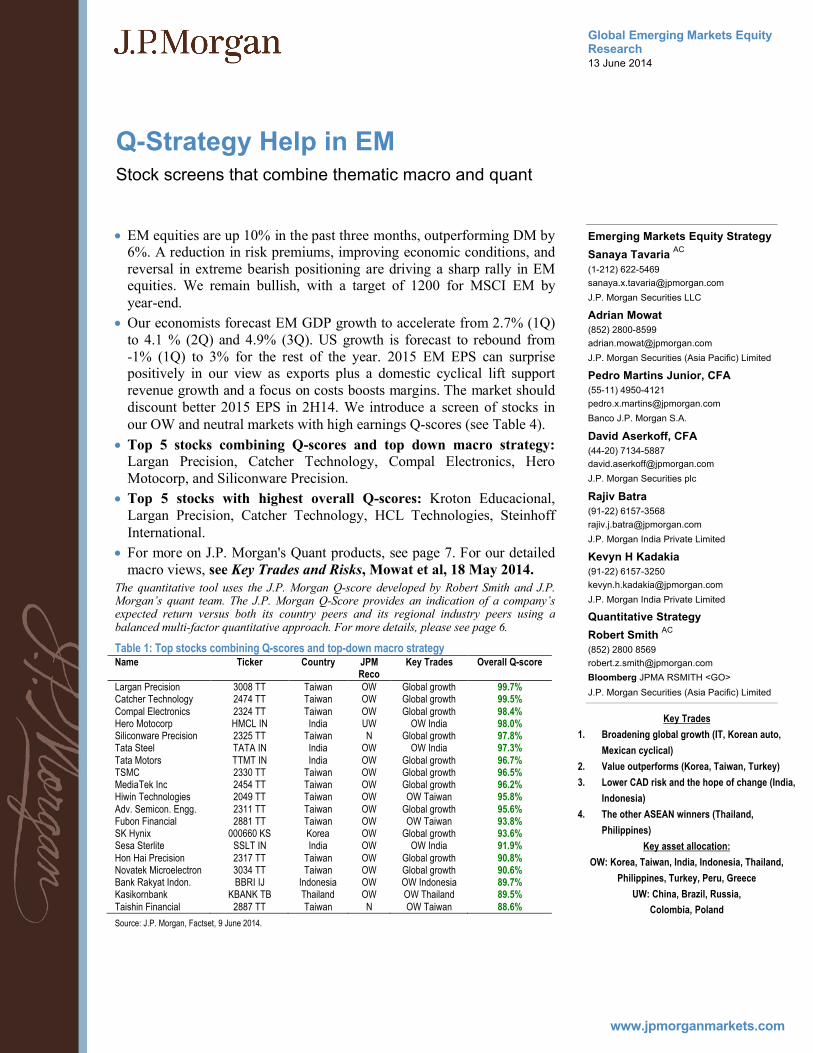

EM equities are up 10% in the past three months, outperforming DM by 6%. A reduction in risk premiums, improving economic conditions, and reversal in extreme bearish positioning are driving a sharp rally in EM equities. We remain bullish, with a target of 1200 for MSCI EM by year-end.

Our economists forecast EM GDP growth to accelerate from 2.7% (1Q)to 4.1 % (2Q) and 4.9% (3Q). US growth is forecast to rebound from -1% (1Q) to 3% for the rest of the year. 2015 EM EPS can surprise positively in our view as exports plus a domestic cyclical lift support revenue growth and a focus on costs boosts margins. The market should discount better 2015 EPS in 2H14. We introduce a screen of stocks in our OW and neutral markets with high earnings Q-scores (see Table 4).

Top 5 stocks combining Q-scores and top down macro strategy:Largan Precision, Catcher Technology, Compal Electronics, Hero Motocorp, and Siliconware Precision.

Top 5 stocks with highest overall Q-scores: Kroton Educacional, Largan Precision, Catcher Technology, HCL Technologies, Steinhoff International.

For more on J.P. Morgan's Quant products, see page 7. For our detailed macro views, see Key Trades and Risks, Mowat et al, 18 May 2014.

The quantitative tool uses the J.P. Morgan Q-score developed by Robert Smith and J.P. Morgan’s quant team. The J.P. Morgan Q-Score provides an indication of a company’s expected return versus both its country peers and its regional industry peers using a balanced multi-factor quantitative approach. For more details, please see page 6.

Table 1: Top stocks combining Q-scores and top-down macro strategyName Ticker Country JPM

RecoKey Trades Overall Q-score

Largan Precision 3008 TT Taiwan OW Global growth 99.7%Catcher Technology 2474 TT Taiwan OW Global growth 99.5%Compal Electronics 2324 TT Taiwan OW Global growth 98.4%Hero Motocorp HMCL IN India UW OW India 98.0%Siliconware Precision 2325 TT Taiwan N Global growth 97.8%Tata Steel TATA IN India OW OW India 97.3%Tata Motors TTMT IN India OW Global growth 96.7%TSMC 2330 TT Taiwan OW Global growth 96.5%MediaTek Inc 2454 TT Taiwan OW Global growth 96.2%Hiwin Technologies 2049 TT Taiwan OW OW Taiwan 95.8%Adv. Semicon. Engg. 2311 TT Taiwan OW Global growth 95.6%Fubon Financial 2881 TT Taiwan OW OW Taiwan 93.8%SK Hynix 000660 KS Korea OW Global growth 93.6%Sesa Sterlite SSLT IN India OW OW India 91.9%Hon Hai Precision 2317 TT Taiwan OW Global growth 90.8%Novatek Microelectron 3034 TT Taiwan OW Global growth 90.6%Bank Rakyat Indon. BBRI IJ Indonesia OW OW Indonesia 89.7%Kasikornbank KBANK TB Thailand OW OW Thailand 89.5%Taishin Financial 2887 TT Taiwan N OW Taiwan 88.6%

Source: J.P. Morgan, Factset, 9 June 2014.

Key Trades

1. Broadening global growth (IT, Korean auto,

Mexican cyclical)

2. Value outperforms (Korea, Taiwan, Turkey)

3. Lower CAD risk and the hope of change (India,

Indonesia)

4. The other ASEAN winners (Thailand,

Philippines)

Key asset allocation:

OW: Korea, Taiwan, India, Indonesia, Thailand,

Philippines, Turkey, Peru, Greece

UW: China, Brazil, Russia,

Colombia, Poland

16

Appendix áTOP

Key Rating, Price Target & EPS Changes Europe

Rating Changes Company New Rating Old Rating Increases

Dufry N UW Decreases

Ipsen N OW Price Target Changes Price Target Company Rating New Old Increases

Dufry N SFr. 166.00 SFr. 141.00 Storebrand OW kr 42.30 kr 41.00 Decreases Active Biotech UW 36.00 kr 59.00 kr Atkins (WS) OW 1,548 p 1,619 p HSBC Holdings plc N 675 p 700 p Ipsen N € 36.00 € 38.00 PZ Cussons N 350 p 370 p Standard Chartered N 1,450 p 1,500 p Source: J.P. Morgan estimates.

J.P. Morgan EPS Estimate Changes Company Current FY Next FY Increases

Storebrand +7.8% +0.1% Decreases Atkins (WS) -0.2% -0.4% HSBC Holdings plc -0.1% -1.1% Ipsen -3.6% -3.4% PZ Cussons -1.1% -4.0% Standard Chartered -3.8% -5.0% Revisions Active Biotech nm nm Dufry -33.7% +4.8% Source: J.P. Morgan estimates

Asia

Price Target Changes Price Target Company Rating New Old Increases

KPJ Healthcare Berhad N R3.60 R3.50 Reliance Power UW INR63.0 INR54.0 PT Tower Bersama Infrastructure Tbk OW Rp8,300.00 Rp6,920.00 Source: J.P. Morgan estimates.

J.P. Morgan EPS Estimate Changes Company Current FY Next FY Increases

PT Tower Bersama Infrastructure Tbk +24.1% +9.4% Revisions KPJ Healthcare Berhad +15.1% -8.1% Reliance Power -6.2% +14.5% J.P. Morgan DPS Estimate Changes Company Current FY Next FY Revisions

KPJ Healthcare Berhad -14.5% +5.4%

Australia

Estimate Changes* Company FY_14 FY_15 Upgrades

RHC 0.0% +5.3% Downgrades MIN -1.8% -5.9% NCM -0.4% -40.0% SVW -1.5% -8.0% * EPS Changes > +/- 1%

Price Target Changes Target Company New Old Upgrades

GMG 5.30 5.21 RHC 48.04 43.43 Downgrades MIN 9.26 10.38 NCM 10.35 11.00 SVW 8.30 8.64 Source: J.P. Morgan estimates.

17

Japan

Rating Changes Company New Old Increases

Advantest (6857) N UW Price Target Changes Price Target Company Rating New Old Increases

Advantest (6857) N ¥1,350 ¥950 Source: J.P. Morgan estimates.

J.P. Morgan EPS Estimate Changes Company Current FY Next FY Revisions

Advantest (6857) +10.0% -0.4% Source: J.P. Morgan estimates. Note: Numbers and companies above may differ from the corresponding numbers or companies in the individual notes inside the FTM.

US

Rating Changes

Company New Rating Old Rating Increases

Accuray OW N Decreases lululemon athletica inc. N OW SouFun Holdings Ltd N OW

Price Target Changes

Price Target Company Rating New Old Increases

Accuray OW 12.00 9.00 DigitalGlobe, Inc. N 34.50 31.50 Intel OW 31.00 30.00 Synaptics Inc. OW 98.00 86.00 Ulta Salon, Cosmetics & Fragrance, Inc. OW 110.00 105.00 Decreases lululemon athletica inc. N 42.00 56.00 SouFun Holdings Ltd N 10.00 17.00 Source: J.P. Morgan estimates.

J.P. Morgan EPS Estimate Changes*

Company Current FY Next FY Increases

Accuray +0.7% +28.2% Intel +4.1% +1.9% Synaptics Inc. +16.4% +10.2% Decreases lululemon athletica inc. -5.3% -11.4% SouFun Holdings Ltd -18.7% -13.3% Revisions DigitalGlobe, Inc. -3.1% +0.5% Gran Tierra Energy +2.1% -1.3% * EPS Changes > +/- 1%

18

Conference Calls áTOP

Today

MedTech - 2014 CEO Conference Call Series: Boston Scientific (BSX), Hosted by: Mike Weinstein (Medical Technology & Devices Equity Analyst ), Featuring: Mike Mahoney (CEO, BSX), on Friday, Jun 13, @ 11am ET/ 16:00 UK, DIAL-IN: 888-748-4893 or 517-319-9536; Passcode: MEDTECH, Replay through 6/19: : 800-406-7490 or 402-220-4881; passcode: 21214 (PODCAST AVAILABLE)

Natural Gas Outlook in the Northeast, Hosted by: Jeremy Tonet (Master Limited Partnerships Equity Analyst), Featuring: Steve Kean (President & COO of Kinder Morgan), Tom Martin (President of Kinder Morgan Natural Gas Group), on Friday, June 13 @ 2:00pm ET, DIAL-IN: 888-324-7508 (US); 1-773-756-4709 (Outside US); Passcode: MLP, Replay through 6/20: 866-485-0036 (US); 1-203-369-1608 (outside US); Passcode: 61314 (PODCAST AVAILABLE)

Upcoming

EE/MI 2014 CEO Conference Call Series: Rockwell Automation (ROK), Hosted by: Steve Tusa (Electrical Equipment / Multi-industry Equity Analyst), Featuring: Keith Nosbusch (Chairman and CEO, ROK), on Tuesday, June 17 @ 11:00am, DIAL-IN: 888-603-7019 (US); +1-312-470-7146 (outside US); Passcode: TUSA, Replay through 6/24: 800-964-3941 (US); + 1-203-369-3117 (Outside US); Passcode: 2137 (PODCAST AVAILABLE)

Biotechnology - 2014 CEO/CFO Conference Call Series - Agios Pharma, Hosted by: Geoff Meacham (Biotechnology Equity Analyst), Featuring: David Schenkein (CEO, Agios Pharma), on Friday, June 20 @ 10:00am, DIAL-IN: 888-889-1309 (US); +1-210-234-5884 (outside US); Passcode: BIOTECH, Replay Through 6/27: 866-507-6406 (US); +1-203-369-1896 (Outside US); Passcode: 54128 (PODCAST AVAILABLE)

MedTech - 2014 CEO Conference Call Series: Boston Scientific, Hosted by: Mike Weinstein (Medical Technology & Devices Equity Analyst ), Featuring: Mike Mahoney (CEO), on Friday, June 20 @ 11:00am ET / 16:00 UK, DIAL-IN: 888-748-4893 (US); +1-517-319-9536 (outside US); Passcode: MEDTECH, Replay through 6/26: 800-406-7490 (US); +1-402-220-4881 (Outside US); Passcode: 21214 (PODCAST AVAILABLE)

Biotechnology - 2014 CEO/CFO Conference Call Series - Agios Pharma, Hosted by: Cory Kasimov (Biotech Equity Analyst), Featuring: David Schenkein (CEO), on Friday, June 20 @ 10:00am, DIAL-IN: 888-889-1309 (US); +1-210-234-5884 (outside US); Passcode: BIOTECH; Replay through 6/21: 888-567-0440 (US); +1-203-369-3442 (Outside US); Passcode: 2814

MedTech - 2014 CEO Conference Call Series: Cooper, Hosted by: Mike Weinstein (Medical Technology & Devices Equity Analyst ), Featuring: Bob Weiss (CEO, Cooper), on Friday, Jun 20, @ 11am ET/8am PT (except during earnings), DIAL-IN: 888-748-4893 or 517-319-9536; Passcode: MEDTECH, Replay through 6/26: : 800-406-7490 or 402-220-4881; passcode: 21214 (PODCAST AVAILABLE)

Conference Call Replays EE/MI 2014 CEO Conference Call Series: Lennox International (LII), Hosted by: Steve Tusa (Electrical Equipment / Multi-industry Equity Analyst), Featuring: Todd Bluedorn (Chairman and CEO, LII), Replay through 6/13: 866-463-2176 (US); + 1-203-369-1374 (Outside US); Passcode: 6912 (PODCAST AVAILABLE)

Analysis of New EPA Carbon Emissions Rule, Hosted by: Joseph Allman (Oil & Gas Exploration & Production), John Bridges (Precious Metals & Coal), Christopher Turnure (Electric Utilities), Featuring: Granville Martin (J.P. Morgan’s Office of Environmental Affairs), Replay through 6/13: 800-627-5350 (US); 1-402-220-0228 (outside US); Passcode: 60614

U.S. Economic Outlook, Hosted by: Bruce Kasman (J.P. Morgan Chief Economist), Replay through 6/14: 888-458-8113 (US); +1-402-998-1351 (outside US); Passcode: 6909591# (PODCAST AVAILABLE)

Used Agricultural Equipment Update: Hosted by: Ann Duignan (US Machinery Equity Analyst), Featuring: Darwin Melnyk (IRON Solutions CEO), Replay through 6/16: 866-448-5641 (US); +1-203-369-1186 (Outside US); Passcode: 9742 (PODCAST AVAILABLE)

LatAm Cement, Construction & Real Estate Outlook for 2H14, Hosted by: Adrian Huerta (LatAm Cement & Construction and Real Estate ), Marcelo Motta (Brazilian Homebuilders and Real Estate ), Replay through 6/16: 800-294-9493 (US); +1-402-220-3767 (outside US); Passcode: 54192

ECB Bank Measures and Outlook, Hosted by: Kian Abouhossein, Delphine Lee & Sofie Peterzens (European Banks Equity Research Team), Replay Through 6/17: +1-954-334-0342 (US); 020 7031 4064 (UK); Passcode: 945492 (REPORT AVAILABLE)

Post-ATS US IPF Physician Survey; Increasing Projected Esbriet Market Share, Hosted by: Anupam Rama (Biotech Equity Analyst), Replay Through 6/17: 866-352-6818 (US); +1-203-369-0071 (Outside US); Passcode: 6514 (SLIDES, REPORT & PODCAST AVAILABLE)

Healthcare Technology & Distribution - 2014 CEO Conference Call Series: LabCorp (LH), Hosted by: Lisa Gill (Healthcare Technology & Distribution Equity Analyst), Featuring: Dave King (CFO, LH), Replay Through 6/19: 866-421-6880 (US); +1-203-369-0823 (outside US); Passcode: 61214 (PODCAST AVAILABLE)

19

Upcoming Conferences

Homepage

Jun 17 – 18, 2014 – Technology CEO Conference London, UK, J.P. Morgan offices, 25 Bank Street

June 18,2014 - European Sectors and Strategy Outlook Hotel Orfila, Madrid

Jun 19, 2014 – 5th Annual Oil & Gas 1x1 Corporate Access Day Hilton Boston Downtown, Boston

Jun 24 – 25, 2014 – Media CEO Conference London, UK, J.P. Morgan offices, 25 Bank Street

June 25, 2014 – Emerging Markets Equity Strategy: 2014 Second Half Outlook London, United Kingdom, J.P. Morgan offices, 25 Bank Street, E14 5JP

June 25 – 26, 2014 – 3rd Southern Cone and Andean Conference Lima, Peru

June 26, 2014 – European Healthcare Conference London, UK, J.P. Morgan offices, 25 Bank Street

June 30,2014 - 2014 Emerging Markets Macro: Second Half Outlook J.P. Morgan, 270 Park Ave, New York July 29 – 30, 2014 – 9th Annual Mexico CEO/CFO Conference Mexico City

Aug 13 – 14, 2014 – Auto Conference New York, NY, J.P. Morgan, 270 Park Avenue

Sept 23 – 24, 2014 – Asia and CEEMEA Emerging Markets Corporate Conference London, UK, J.P. Morgan offices, 25 Bank Street

Nov 12, 2014 – Ultimate Services Investor Conference New York, NY, Westin Grand Central Hotel, 212, East 42nd Street

December 1 – 5, 2014 – 7th Brazil Opportunities Conference São Paulo

For additional conference information contact your J.P. Morgan representative or email [email protected].

Please remember that all J.P. Morgan conferences are by invitation only. Invitations are non-transferable.

20

Corporate Marketing Calendar áTOP

Fri Jun-13-14 Mon Jun-16-14 Tue Jun-17-14 Wed Jun-18-14 Thu Jun-19-14

ANSYS, INC. (LOS ANGELES, PASADENA) DCC (TORONTO) Iroko Pharmaceuticals (Private) (NEW YORK) WILLIAMS-SONOMA, INC. (PRINCETON)

BLUEBIRD BIO (BOSTON) CBL & Associates (BOSTON) COGNIZANT (DALLAS) MegaFon (NEW YORK) NATIONAL BANK OF GREECE (NEW YORK) VERITIV (NEW YORK)

ALLIANCE TRUST PLC (NEW YORK) BLUEBIRD BIO (NEW YORK) COGNIZANT (AUSTIN, HOUSTON) EQT MIDSTREAM PARTNERS (BOSTON) FIRST PACIFIC (WASHINGTON) INOGEN INC (NEW YORK) QUINTAIN ESTATES AND DEVELOPMENT PLC (NEW YORK) RSA INSURANCE GROUP PLC (AUSTIN, DENVER) VERITIV (BOSTON)

ALLIANCE TRUST PLC (RICHMOND) BLOOMIN BRANDS, INC. (NEW YORK) COCA-COLA EAST JAPAN CO., LTD (NEW YORK) FIRST PACIFIC (CHICAGO) INOGEN INC (BOSTON) LENNOX INTERNATIONAL INC (BALTIMORE) QUINTAIN ESTATES AND DEVELOPMENT PLC (BOSTON) VERITIV (PHILADELPHIA, SHORT HILLS)

COCA-COLA EAST JAPAN CO., LTD (NEW YORK) FIRST PACIFIC (LOS ANGELES) GAP INC (NEW YORK) LENNOX INTERNATIONAL INC (NEW YORK) MOHAWK INDUSTRIES INC (BOSTON) QIHOO 360 (NEW YORK) QUINTAIN ESTATES AND DEVELOPMENT PLC (CHICAGO) VERITIV (CHICAGO)

21

Markets at a glance áTOP

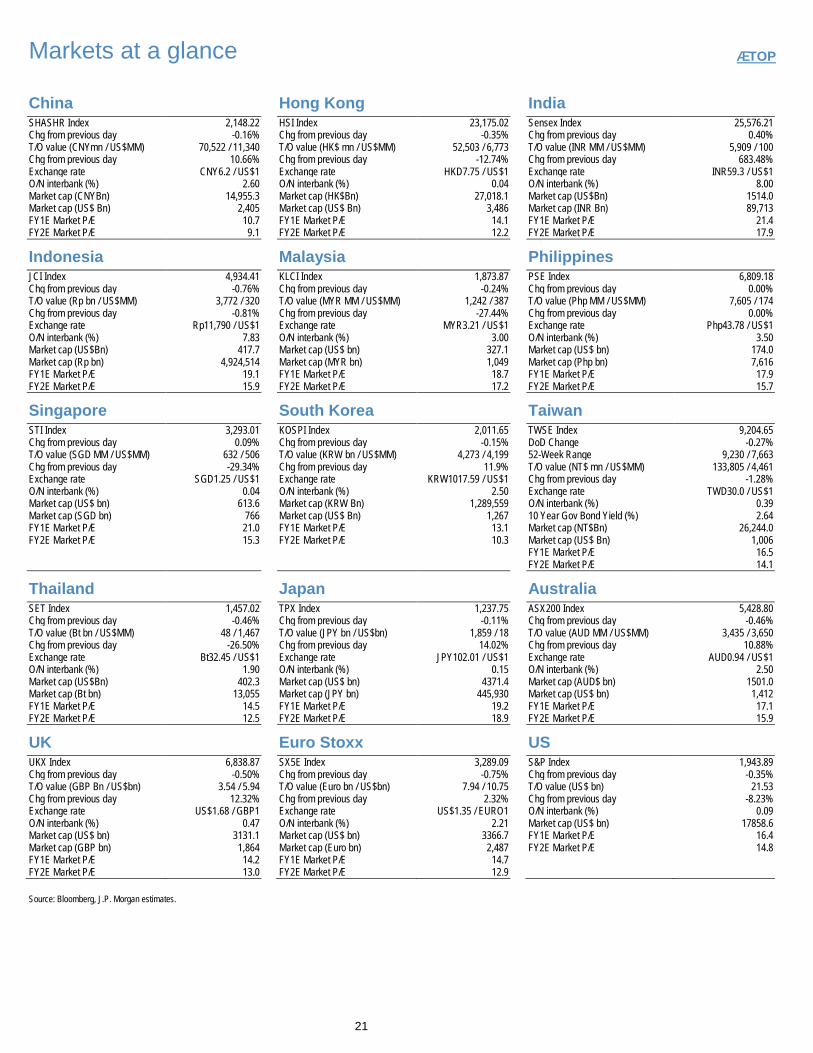

China

Hong Kong

India SHASHR Index 2,148.22

HSI Index 23,175.02

Sensex Index 25,576.21

Chg from previous day -0.16%

Chg from previous day -0.35%

Chg from previous day 0.40% T/O value (CNYmn / US$MM) 70,522 / 11,340

T/O value (HK$ mn / US$MM) 52,503 / 6,773

T/O value (INR MM / US$MM) 5,909 / 100

Chg from previous day 10.66%

Chg from previous day -12.74%

Chg from previous day 683.48% Exchange rate CNY6.2 / US$1

Exchange rate HKD7.75 / US$1

Exchange rate INR59.3 / US$1

O/N interbank (%) 2.60

O/N interbank (%) 0.04

O/N interbank (%) 8.00 Market cap (CNYBn) 14,955.3

Market cap (HK$Bn) 27,018.1

Market cap (US$Bn) 1514.0

Market cap (US$ Bn) 2,405

Market cap (US$ Bn) 3,486

Market cap (INR Bn) 89,713 FY1E Market P/E 10.7

FY1E Market P/E 14.1

FY1E Market P/E 21.4

FY2E Market P/E 9.1

FY2E Market P/E 12.2

FY2E Market P/E 17.9 Indonesia

Malaysia

Philippines

JCI Index 4,934.41

KLCI Index 1,873.87

PSE Index 6,809.18 Chg from previous day -0.76%

Chg from previous day -0.24%

Chg from previous day 0.00%

T/O value (Rp bn / US$MM) 3,772 / 320

T/O value (MYR MM / US$MM) 1,242 / 387

T/O value (Php MM / US$MM) 7,605 / 174 Chg from previous day -0.81%

Chg from previous day -27.44%

Chg from previous day 0.00%

Exchange rate Rp11,790 / US$1

Exchange rate MYR3.21 / US$1

Exchange rate Php43.78 / US$1 O/N interbank (%) 7.83

O/N interbank (%) 3.00

O/N interbank (%) 3.50

Market cap (US$Bn) 417.7

Market cap (US$ bn) 327.1

Market cap (US$ bn) 174.0 Market cap (Rp bn) 4,924,514

Market cap (MYR bn) 1,049

Market cap (Php bn) 7,616

FY1E Market P/E 19.1

FY1E Market P/E 18.7

FY1E Market P/E 17.9 FY2E Market P/E 15.9

FY2E Market P/E 17.2

FY2E Market P/E 15.7

Singapore

South Korea

Taiwan

STI Index 3,293.01

KOSPI Index 2,011.65

TWSE Index 9,204.65 Chg from previous day 0.09%

Chg from previous day -0.15%

DoD Change -0.27%

T/O value (SGD MM / US$MM) 632 / 506

T/O value (KRW bn / US$MM) 4,273 / 4,199

52-Week Range 9,230 / 7,663 Chg from previous day -29.34%

Chg from previous day 11.9%

T/O value (NT$ mn / US$MM) 133,805 / 4,461

Exchange rate SGD1.25 / US$1

Exchange rate KRW1017.59 / US$1

Chg from previous day -1.28% O/N interbank (%) 0.04

O/N interbank (%) 2.50

Exchange rate TWD30.0 / US$1

Market cap (US$ bn) 613.6

Market cap (KRW Bn) 1,289,559

O/N interbank (%) 0.39 Market cap (SGD bn) 766

Market cap (US$ Bn) 1,267

10 Year Gov Bond Yield (%) 2.64

FY1E Market P/E 21.0

FY1E Market P/E 13.1

Market cap (NT$Bn) 26,244.0 FY2E Market P/E 15.3

FY2E Market P/E 10.3

Market cap (US$ Bn) 1,006

FY1E Market P/E 16.5

FY2E Market P/E 14.1

Thailand

Japan

Australia

SET Index 1,457.02

TPX Index 1,237.75

ASX200 Index 5,428.80

Chg from previous day -0.46%

Chg from previous day -0.11%

Chg from previous day -0.46% T/O value (Bt bn / US$MM) 48 / 1,467

T/O value (JPY bn / US$bn) 1,859 / 18

T/O value (AUD MM / US$MM) 3,435 / 3,650

Chg from previous day -26.50%

Chg from previous day 14.02%

Chg from previous day 10.88% Exchange rate Bt32.45 / US$1

Exchange rate JPY102.01 / US$1

Exchange rate AUD0.94 / US$1

O/N interbank (%) 1.90

O/N interbank (%) 0.15

O/N interbank (%) 2.50 Market cap (US$Bn) 402.3

Market cap (US$ bn) 4371.4

Market cap (AUD$ bn) 1501.0

Market cap (Bt bn) 13,055

Market cap (JPY bn) 445,930

Market cap (US$ bn) 1,412 FY1E Market P/E 14.5

FY1E Market P/E 19.2

FY1E Market P/E 17.1

FY2E Market P/E 12.5

FY2E Market P/E 18.9

FY2E Market P/E 15.9 UK

Euro Stoxx

US

UKX Index 6,838.87

SX5E Index 3,289.09

S&P Index 1,943.89

Chg from previous day -0.50%

Chg from previous day -0.75%

Chg from previous day -0.35% T/O value (GBP Bn / US$bn) 3.54 / 5.94

T/O value (Euro bn / US$bn) 7.94 / 10.75

T/O value (US$ bn) 21.53

Chg from previous day 12.32%

Chg from previous day 2.32%

Chg from previous day -8.23% Exchange rate US$1.68 / GBP1

Exchange rate US$1.35 / EURO1

O/N interbank (%) 0.09

O/N interbank (%) 0.47

O/N interbank (%) 2.21

Market cap (US$ bn) 17858.6 Market cap (US$ bn) 3131.1

Market cap (US$ bn) 3366.7

FY1E Market P/E 16.4

Market cap (GBP bn) 1,864

Market cap (Euro bn) 2,487

FY2E Market P/E 14.8 FY1E Market P/E 14.2

FY1E Market P/E 14.7

FY2E Market P/E 13.0

FY2E Market P/E 12.9

Source: Bloomberg, J.P. Morgan estimates.

22

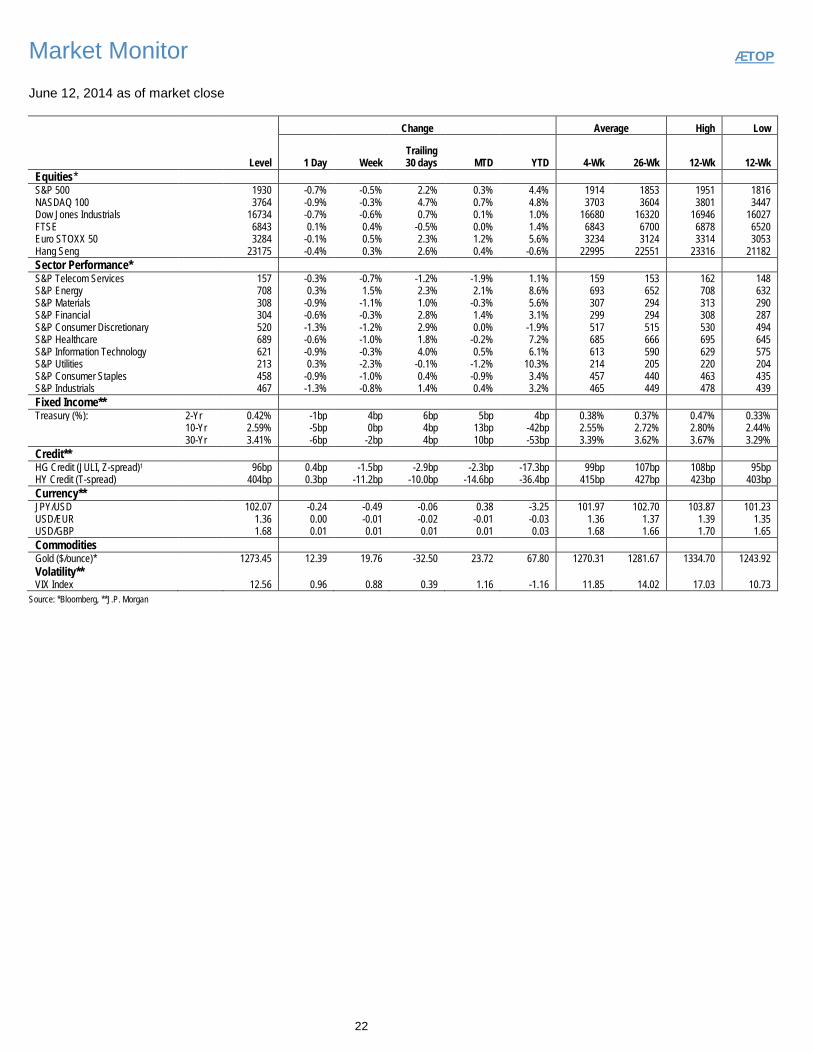

Market Monitor áTOP

June 12, 2014 as of market close

Change Average High Low

Level 1 Day Week Trailing 30 days MTD YTD 4-Wk 26-Wk 12-Wk 12-Wk

Equities* S&P 500

1930 -0.7% -0.5% 2.2% 0.3% 4.4% 1914 1853 1951 1816

NASDAQ 100

3764 -0.9% -0.3% 4.7% 0.7% 4.8% 3703 3604 3801 3447 Dow Jones Industrials

16734 -0.7% -0.6% 0.7% 0.1% 1.0% 16680 16320 16946 16027

FTSE

6843 0.1% 0.4% -0.5% 0.0% 1.4% 6843 6700 6878 6520 Euro STOXX 50

3284 -0.1% 0.5% 2.3% 1.2% 5.6% 3234 3124 3314 3053

Hang Seng

23175 -0.4% 0.3% 2.6% 0.4% -0.6% 22995 22551 23316 21182 Sector Performance* S&P Telecom Services

157 -0.3% -0.7% -1.2% -1.9% 1.1% 159 153 162 148

S&P Energy

708 0.3% 1.5% 2.3% 2.1% 8.6% 693 652 708 632 S&P Materials

308 -0.9% -1.1% 1.0% -0.3% 5.6% 307 294 313 290

S&P Financial

304 -0.6% -0.3% 2.8% 1.4% 3.1% 299 294 308 287 S&P Consumer Discretionary

520 -1.3% -1.2% 2.9% 0.0% -1.9% 517 515 530 494

S&P Healthcare

689 -0.6% -1.0% 1.8% -0.2% 7.2% 685 666 695 645 S&P Information Technology

621 -0.9% -0.3% 4.0% 0.5% 6.1% 613 590 629 575

S&P Utilities

213 0.3% -2.3% -0.1% -1.2% 10.3% 214 205 220 204 S&P Consumer Staples

458 -0.9% -1.0% 0.4% -0.9% 3.4% 457 440 463 435

S&P Industrials

467 -1.3% -0.8% 1.4% 0.4% 3.2% 465 449 478 439 Fixed Income** Treasury (%): 2-Yr 0.42% -1bp 4bp 6bp 5bp 4bp 0.38% 0.37% 0.47% 0.33%

10-Yr 2.59% -5bp 0bp 4bp 13bp -42bp 2.55% 2.72% 2.80% 2.44%

30-Yr 3.41% -6bp -2bp 4bp 10bp -53bp 3.39% 3.62% 3.67% 3.29%

Credit** HG Credit (JULI, Z-spread)1

96bp 0.4bp -1.5bp -2.9bp -2.3bp -17.3bp 99bp 107bp 108bp 95bp

HY Credit (T-spread)

404bp 0.3bp -11.2bp -10.0bp -14.6bp -36.4bp 415bp 427bp 423bp 403bp Currency** JPY/USD

102.07 -0.24 -0.49 -0.06 0.38 -3.25 101.97 102.70 103.87 101.23

USD/EUR

1.36 0.00 -0.01 -0.02 -0.01 -0.03 1.36 1.37 1.39 1.35 USD/GBP

1.68 0.01 0.01 0.01 0.01 0.03 1.68 1.66 1.70 1.65

Commodities Gold ($/ounce)*

1273.45 12.39 19.76 -32.50 23.72 67.80 1270.31 1281.67 1334.70 1243.92

Volatility** VIX Index 12.56 0.96 0.88 0.39 1.16 -1.16 11.85 14.02 17.03 10.73

Source: *Bloomberg, **J.P. Morgan

23

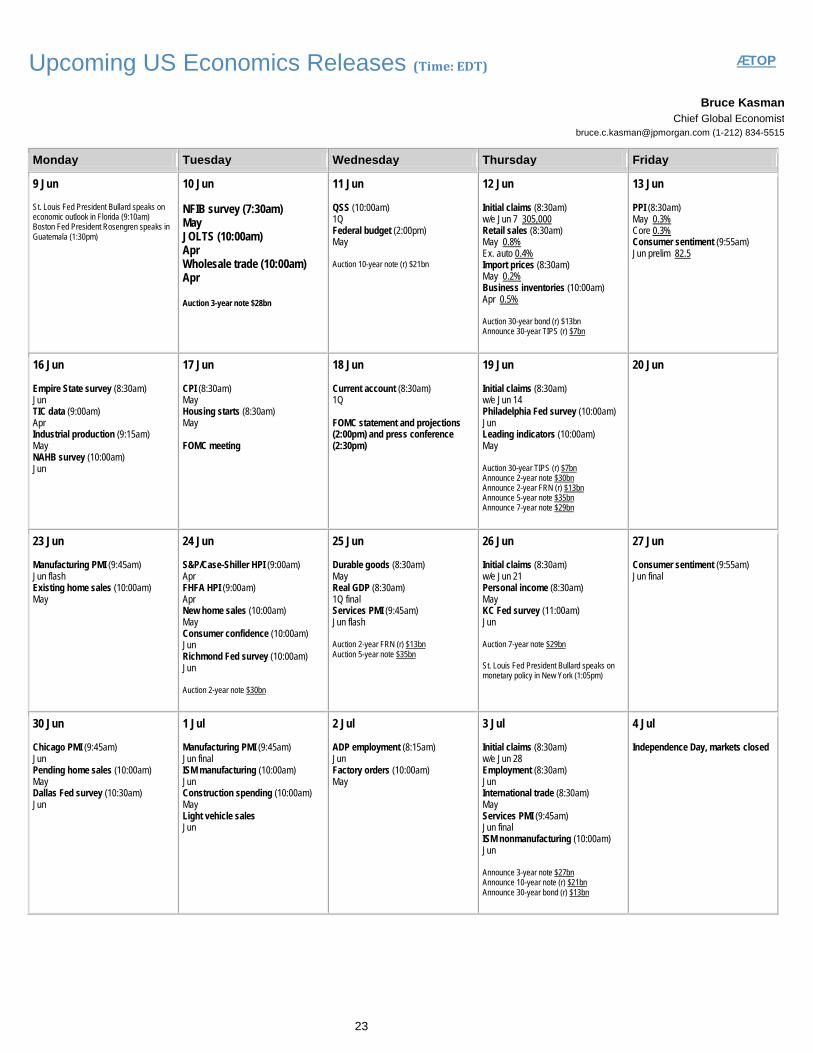

Upcoming US Economics Releases (Time: EDT) áTOP

Bruce Kasman

Chief Global Economist [email protected] (1-212) 834-5515

Monday Tuesday Wednesday Thursday Friday

9 Jun St. Louis Fed President Bullard speaks on economic outlook in Florida (9:10am) Boston Fed President Rosengren speaks in Guatemala (1:30pm)

10 Jun NFIB survey (7:30am) May JOLTS (10:00am) Apr Wholesale trade (10:00am) Apr Auction 3-year note $28bn

11 Jun QSS (10:00am) 1Q Federal budget (2:00pm) May Auction 10-year note (r) $21bn

12 Jun Initial claims (8:30am) w/e Jun 7 305,000 Retail sales (8:30am) May 0.8% Ex. auto 0.4% Import prices (8:30am) May 0.2% Business inventories (10:00am) Apr 0.5% Auction 30-year bond (r) $13bn Announce 30-year TIPS (r) $7bn

13 Jun PPI (8:30am) May 0.3% Core 0.3% Consumer sentiment (9:55am) Jun prelim 82.5

16 Jun Empire State survey (8:30am) Jun TIC data (9:00am) Apr Industrial production (9:15am) May NAHB survey (10:00am) Jun

17 Jun CPI (8:30am) May Housing starts (8:30am) May FOMC meeting

18 Jun Current account (8:30am) 1Q FOMC statement and projections (2:00pm) and press conference (2:30pm)

19 Jun Initial claims (8:30am) w/e Jun 14 Philadelphia Fed survey (10:00am) Jun Leading indicators (10:00am) May Auction 30-year TIPS (r) $7bn Announce 2-year note $30bn Announce 2-year FRN (r) $13bn Announce 5-year note $35bn Announce 7-year note $29bn

20 Jun

23 Jun Manufacturing PMI (9:45am) Jun flash Existing home sales (10:00am) May

24 Jun S&P/Case-Shiller HPI (9:00am) Apr FHFA HPI (9:00am) Apr New home sales (10:00am) May Consumer confidence (10:00am) Jun Richmond Fed survey (10:00am) Jun Auction 2-year note $30bn

25 Jun Durable goods (8:30am) May Real GDP (8:30am) 1Q final Services PMI (9:45am) Jun flash Auction 2-year FRN (r) $13bn Auction 5-year note $35bn

26 Jun Initial claims (8:30am) w/e Jun 21 Personal income (8:30am) May KC Fed survey (11:00am) Jun Auction 7-year note $29bn St. Louis Fed President Bullard speaks on monetary policy in New York (1:05pm)

27 Jun Consumer sentiment (9:55am) Jun final

30 Jun Chicago PMI (9:45am) Jun Pending home sales (10:00am) May Dallas Fed survey (10:30am) Jun

1 Jul Manufacturing PMI (9:45am) Jun final ISM manufacturing (10:00am) Jun Construction spending (10:00am) May Light vehicle sales Jun

2 Jul ADP employment (8:15am) Jun Factory orders (10:00am) May

3 Jul Initial claims (8:30am) w/e Jun 28 Employment (8:30am) Jun International trade (8:30am) May Services PMI (9:45am) Jun final ISM nonmanufacturing (10:00am) Jun Announce 3-year note $27bn Announce 10-year note (r) $21bn Announce 30-year bond (r) $13bn

4 Jul Independence Day, markets closed

24

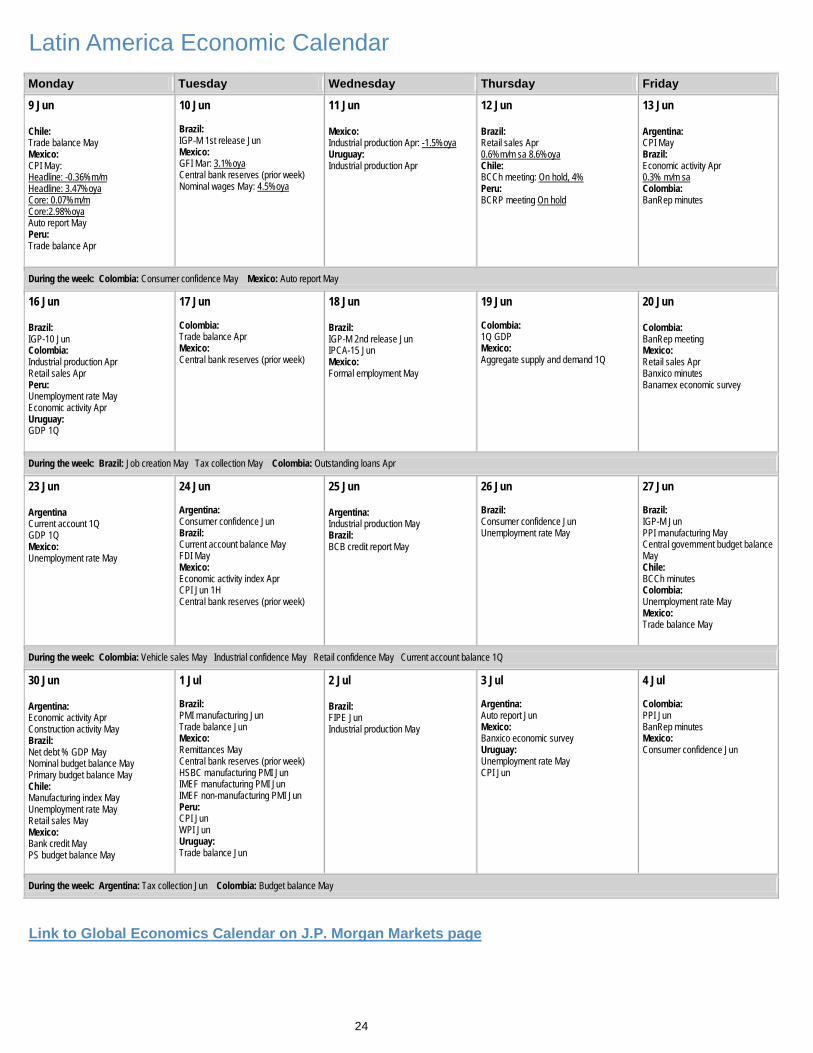

Latin America Economic Calendar Monday Tuesday Wednesday Thursday Friday

9 Jun Chile: Trade balance May Mexico: CPI May: Headline: -0.36%m/m Headline: 3.47%oya Core: 0.07%m/m Core:2.98%oya Auto report May Peru: Trade balance Apr

10 Jun Brazil: IGP-M 1st release Jun Mexico: GFI Mar: 3.1%oya Central bank reserves (prior week) Nominal wages May: 4.5%oya

11 Jun Mexico: Industrial production Apr: -1.5%oya Uruguay: Industrial production Apr

12 Jun Brazil: Retail sales Apr 0.6%m/m sa 8.6%oya Chile: BCCh meeting: On hold, 4% Peru: BCRP meeting On hold

13 Jun Argentina: CPI May Brazil: Economic activity Apr 0.3% m/m sa Colombia: BanRep minutes

During the week: Colombia: Consumer confidence May Mexico: Auto report May 16 Jun Brazil: IGP-10 Jun Colombia: Industrial production Apr Retail sales Apr Peru: Unemployment rate May Economic activity Apr Uruguay: GDP 1Q

17 Jun Colombia: Trade balance Apr Mexico: Central bank reserves (prior week)

18 Jun Brazil: IGP-M 2nd release Jun IPCA-15 Jun Mexico: Formal employment May

19 Jun Colombia: 1Q GDP Mexico: Aggregate supply and demand 1Q

20 Jun Colombia: BanRep meeting Mexico: Retail sales Apr Banxico minutes Banamex economic survey

During the week: Brazil: Job creation May Tax collection May Colombia: Outstanding loans Apr 23 Jun Argentina Current account 1Q GDP 1Q Mexico: Unemployment rate May

24 Jun Argentina: Consumer confidence Jun Brazil: Current account balance May FDI May Mexico: Economic activity index Apr CPI Jun 1H Central bank reserves (prior week)

25 Jun Argentina: Industrial production May Brazil: BCB credit report May

26 Jun Brazil: Consumer confidence Jun Unemployment rate May

27 Jun Brazil: IGP-M Jun PPI manufacturing May Central government budget balance May Chile: BCCh minutes Colombia: Unemployment rate May Mexico: Trade balance May

During the week: Colombia: Vehicle sales May Industrial confidence May Retail confidence May Current account balance 1Q 30 Jun Argentina: Economic activity Apr Construction activity May Brazil: Net debt % GDP May Nominal budget balance May Primary budget balance May Chile: Manufacturing index May Unemployment rate May Retail sales May Mexico: Bank credit May PS budget balance May

1 Jul Brazil: PMI manufacturing Jun Trade balance Jun Mexico: Remittances May Central bank reserves (prior week) HSBC manufacturing PMI Jun IMEF manufacturing PMI Jun IMEF non-manufacturing PMI Jun Peru: CPI Jun WPI Jun Uruguay: Trade balance Jun

2 Jul Brazil: FIPE Jun Industrial production May

3 Jul Argentina: Auto report Jun Mexico: Banxico economic survey Uruguay: Unemployment rate May CPI Jun

4 Jul Colombia: PPI Jun BanRep minutes Mexico: Consumer confidence Jun

During the week: Argentina: Tax collection Jun Colombia: Budget balance May Link to Global Economics Calendar on J.P. Morgan Markets page

25

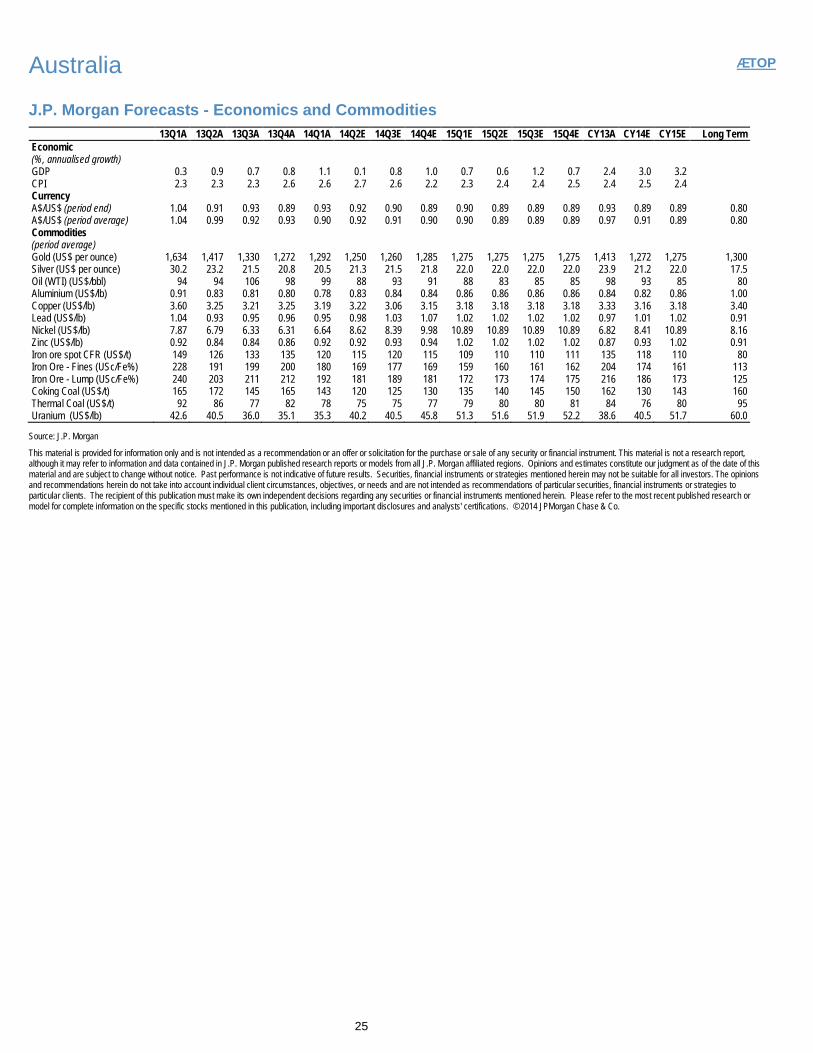

Australia áTOP